Intermediate Accounting (10)

- 格式:pptx

- 大小:607.04 KB

- 文档页数:49

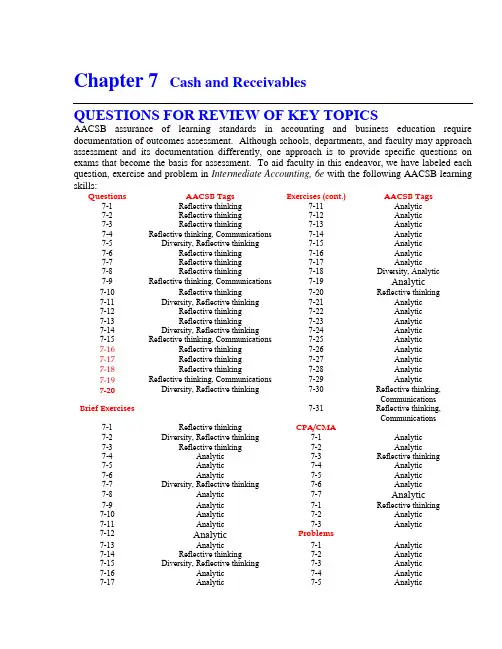

Chapter 7 Cash and Receivables

QUESTIONS FOR REVIEW OF KEY TOPICS

AACSB assurance of learning standards in accounting and business education require

documentation of outcomes assessment. Although schools, departments, and faculty may approach

assessment and its documentation differently, one approach is to provide specific questions on

exams that become the basis for assessment. To aid faculty in this endeavor, we have labeled each

question, exercise and problem in Intermediate Accounting, 6e with the following AACSB learning

skills:

Questions AACSB Tags Exercises (cont.) AACSB Tags

7-1 Reflective thinking 7-11 Analytic

7-2 Reflective thinking 7-12 Analytic

7-3 Reflective thinking 7-13 Analytic

7-4 Reflective thinking, Communications 7-14 Analytic

7-5 Diversity, Reflective thinking 7-15 Analytic

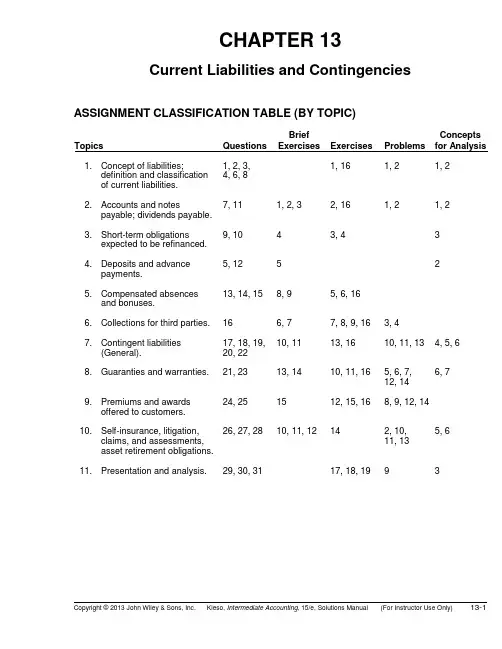

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 13-1 CHAPTER 13

Current Liabilities and Contingencies

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions Brief

Exercises

Exercises

Problems Concepts

for Analysis

1. Concept of liabilities;

definition and classification

of current liabilities. 1, 2, 3,

4, 6, 8 1, 16 1, 2 1, 2

2. Accounts and notes

payable; dividends payable. 7, 11 1, 2, 3 2, 16 1, 2 1, 2

3. Short-term obligations

expected to be refinanced. 9, 10 4 3, 4 3

4. Deposits and advance

payments. 5, 12 5 2

5. Compensated absences

and bonuses. 13, 14, 15 8, 9 5, 6, 16

6. Collections for third parties. 16 6, 7 7, 8, 9, 16 3, 4

7. Contingent liabilities

(General). 17, 18, 19,

20, 22 10, 11 13, 16 10, 11, 13 4, 5, 6

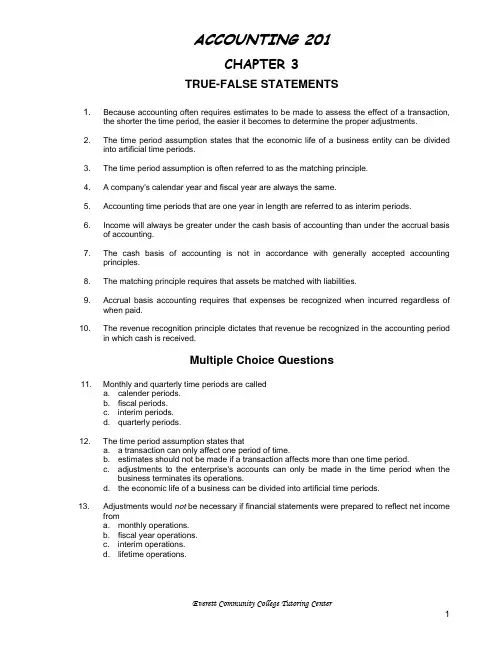

ACCOUNTING 201

CHAPTER 3

TRUE-FALSE STATEMENTS

1. Because accounting often requires estimates to be made to assess the effect of a transaction,

the shorter the time period, the easier it becomes to determine the proper adjustments.

2. The time period assumption states that the economic life of a business entity can be divided

into artificial time periods.

3. The time period assumption is often referred to as the matching principle.

4. A company's calendar year and fiscal year are always the same.

5. Accounting time periods that are one year in length are referred to as interim periods.

6. Income will always be greater under the cash basis of accounting than under the accrual basis

of accounting.

7. The cash basis of accounting is not in accordance with generally accepted accounting

principles.

Chapter 10 - Property, Plant, and Equipment and Intangible Assets: Acquisition and Disposition

10-1 Chapter 10 Property, Plant, and Equipment and

Intangible Assets: Acquisition and Disposition

QUESTIONS FOR REVIEW OF KEY TOPICS

Question 10-1

The difference between tangible and intangible long-lived, revenue-producing assets is that

intangible assets lack physical substance and they primarily refer to the ownership of rights.

Question 10-2

The cost of property, plant, and equipment and intangible assets includes the purchase price

(less any discounts received from the seller), transportation costs paid by the buyer to transport the

asset to the location in which it will be used, expenditures for installation, testing, legal fees to

establish title, and any other costs of bringing the asset to its condition and location for use.