2014年ACCA新大纲解析-P2

- 格式:doc

- 大小:1.59 MB

- 文档页数:9

高顿财经ACCA 2014年ACCA 考试F2管理会计考前最新知识点本文由高顿ACCA 整理发布,转载请注明出处 Responsibility accounting is a system of accounting that segregates revenue and costs into areas of personal responsibility in order to monitor and assess the performance of each part of an organization.The main responsibility centers are:Cost center – the performance of a cost center manager is judged on the extent to which cost targets have been achieved.Revenue center – Within an organization, this is a centre or activity that earns sales revenue. And whose manager is responsible for the revenue earned but not for the costs incurred.Profit center – A part of the business whose manager is responsible and accountable for both costs and revenue. The performance of a profit center manager is measured in terms of the profit made by the centre.Investment center – A profit center with additional responsibilities for investment and possibly also for financing, and whose performance is measured by its return on capital employed (ROCE)..更多ACCA 资讯请关注高顿ACCA 官网:。

ACCA P1P2P3复习以及答题技巧汇总ACCA P1《公司治理,风险和道德》是ACCA专业核心模块的第一门课程,它总共分为四个部分。

1.介绍在代理关系的环境下,企业的整个治理。

这个部分主要是董事的角色和责任以及外部审计师和内部审计师的角色和责任;2.介绍内部监察、内部控制以及实施有效的治理得到的反馈,包括关于决策和决策支持部门的合规问题;3.介绍管理层如何识别、评估和控制风险;4.介绍在会计师责任的背景下个人的以及职业道德和道德框架-职业价值观以及在各种各样的情况下的职业行为。

ACCA P1学习方法首先大家注意公司治理来自于F4中的agency thoery也就是我们经常说的代理理论。

正因为公司的投资人不直接参与公司的管理,从而导致管理者与持有人之间产生一些利益上的冲突,所以上市公司通过完善公司治理来增强监督、减少冲突、降低风险,从而达到股东投资回报最大化。

其次,大家要关注NED(非执行董事)在公司治理中的重要作用,以及他们发挥监督作用具备的条件,这其中要求NED要充分独立。

虽然NED不是公司雇员,和公司之间没有雇佣关系,但是他们对完善和实施公司的发展战略有着重要的作用,另外NED要有足够的时间参与公司的日常经营。

再次,我请同学们关注TURNBULL REPORT和COMBINED CODE中对internal control和risk management的要求。

什么样的internal control system是完善而且有效的,如何进行risk assessment以及如何进行风险处理。

需要强调的五点:第一、考官的历年考题中只有两种格式:Memo 和letter。

烦请大家注意这两种格式第二、大家注意自己写出来的句子要专业,比如有效的内部控制要写sound internal control system, risk embedded等等第三、答题要有逻辑性,适当的通过分段,分层次来讲述自己的观点第四、要注意senario中引号的句子,这些句子一般是考点最后,希望大家多动笔,少用眼睛考虑问题。

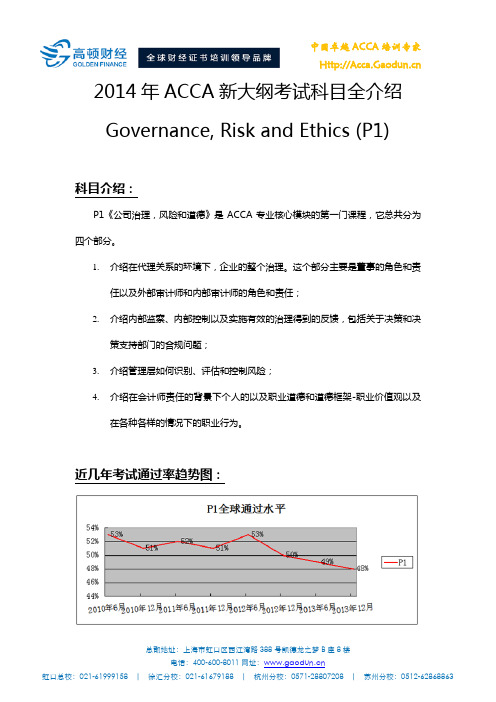

2014年ACCA新大纲考试科目全介绍Governance, Risk and Ethics (P1)科目介绍:P1《公司治理,风险和道德》是ACCA专业核心模块的第一门课程,它总共分为四个部分。

1.介绍在代理关系的环境下,企业的整个治理。

这个部分主要是董事的角色和责任以及外部审计师和内部审计师的角色和责任;2.介绍内部监察、内部控制以及实施有效的治理得到的反馈,包括关于决策和决策支持部门的合规问题;3.介绍管理层如何识别、评估和控制风险;4.介绍在会计师责任的背景下个人的以及职业道德和道德框架-职业价值观以及在各种各样的情况下的职业行为。

近几年考试通过率趋势图:知识结构:科目关联性:P1课程主要介绍的是公司治理、风险管理和职业道德这三块内容。

P1的课程与基础阶段的F1课程和F8课程相关内容有密切的联系。

特别是F8的第四章道德部分,在P1的内容还会重复的考,需要考生非常熟练的掌握。

考试形式:P1的考试时长为3小时,分为两个部分,A部分一道题50分为必选题,是案例分析的模式;B部分共有三道题每道25分,可以任选两题作答。

2014年12月的考题题型没有任何变化。

新旧考纲的主要变化:2014年12月考纲有了一些改变,新增了部分的内容,PARTA中,the key underpinning concepts 由原本的九个,新增到了十一个,多了innovation和scepticism,又新增了一整块的内容,Public sector governance,考官有一篇专门的文章关于这一部分,建议考生仔细的研读。

另一个比较重大的改变在PARTE部分,在E2D的部分,新加了strategic CSR,而E7的部分,加了很大的篇幅,环境报告,环境会计,与环境审计均做了重点的强调。

其实环境与社会责任审计,在2014年6月的考试里,已经直接出现在第三题中。

在未来的考试里,也很有可能作为一个大题出现。

总体来说,新的考纲增加了过去比较少考的一些部分,总体的难度相较过去为高。

ACCA基础课程P2科目辅导资料本文由高顿ACCA整理发布,转载请注明出处Part A REGULATORY AND ETHICAL FRAMEWORKFinancial reporting framework- Corporate governance: is the system by which companies are directed and controlled (Cadbury Report)。

- Conceptual frameworkTh e IASB’s Framework provides the backbone of the IASB‘s conceptual framework. IASs were based on the IASB Framework.A conceptual framework is a statement of generally accepted theoretical principles which form the frame of reference for financial reporting. These theoretical principles provide the basis for the development of new accounting standards and for the evaluation of those already in existence.. Advantages and disadvantages of a conceptual framework. Generally Accepted Accounting Principles (GAAP)A conceptual framework for financial reporting can be defined as an attempt to codify existing GAAP in order to reappraise current accounting standards and to produce new standards.The IASB’s framework: consists of seven sections- The objective of financial statements- Underlying assumptions- Qualitative characteristics of financial statements- The elements of financial statements- Recognition of the elements of financial statements- Measurement of the elements of financial statements- Concepts of capital and capital maintenance(**)Qualitative characteristics:Fundamental qualitative characteristics are:(a)Relevance: predictive value or confirmatory value(b)Faithful representation: information must be complete, neutral and free from material error (replacing ‘reliability)Enhancing qualitative characteristics are:(a)Comparability: achieved by consistency in use of the same accounting policies(b)Verifiability: credibility, assurance that information faithfully represents the economic phenomena(c)Timeliness: information is provided before it loses the capacity to influence decisions(d)Understandability: for users who have a reasonable knowledge of business and economic activities and who are able to read a financial report; information should not be excluded on the grounds that it may be too complex/difficult for some users to understand. Enhanced when information is classified, characterized and presented clearly and concisely.Revenue recognitionAccruals accounting is based on the matching of costs with the revenue they generate.IAS 18 Revenue is concerned with the recognition of revenues arising from fairly common transactions.- The sale of goods- The rendering of services- The use by others of enterprise assets yielding interest, royalties and dividendsGenerally revenue is recognized when the entity has transferred to the buyer the significant risks and rewards of ownership and when the revenue can be measured reliably.Interest, royalties and dividends are included as income because they arise from the use of an entity’s assets by other parties.Interest is the charge for the use of cash or cash equivalents or amounts due to the entity.Royalties are charges for the use of non-current assets of the entity, e.g. patents, computer software and trademarks.Dividends are distributions of profit to holders of equity investments, in proportion with their holdings, of each relevant class of capital.- Definition:Revenue:is the gross inflow of economic benefits during the period arising in the course of the ordinary activities of an enterprise when those inflows result in increases in equity, other than increases relating to contributions from equity participants.Ie, Revenue does not include sales taxes, value added taxes or goods and service taxes which are only collected for third parties.Fair value: is the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm’s length transaction.Sale of goods:Ie. Where revenue and expenses cannot be estimated reliably, then revenue cannot be recognized, any consideration which has already been received is treated as a liability.Rendering of services:Revenue is recognized only to the extent of the expenses recognized that are recoverable.更多ACCA资讯请关注高顿ACCA官网:。

上海总部地址:上海市虹口区花园路171号A3幢高顿教育

电话:400-600-8011网址:

考试大纲回顾:

ACCA 考试大纲之P1变化

本文由高顿ACCA 整理发布,转载请注明出处

2014年12月ACCA 考试P1考纲有了一些改变,新增了部分的内容,PARTA 中,the key under pinning concepts 由原本的九个,新增到了十一个,多了 innovation 和 scepticism ,又新增了一整块的内容,Public sector governance ,考官有一篇专门的文章关于这一部分,建议考生仔细的研读。

另一个比较重大的改变在PARTE 部分,在E2D 的部分,新加了strategic CSR ,而E7的部分,加了很大的篇幅,环境报告,环境会计,与环境审计均做了重点的强调。

其实环境与社会责任审计,在2014年6月的考试里,已经直接出现在第三题中。

在未来的考试里,也很有可能作为一个大题出现。

总体来说,新的考纲增加了过去比较少考的一些部分,总体的难度相较过去为高。

2014年ACCA 考试P1考试形式:

P1的考试时长为3小时,分为两个部分,A 部分一道题50分为必选题,是案例分析的模式;B 部分共有三道题每道25分,可以任选两题作答。

2014年12月的考题题型没有任何变化。

本文由高顿ACCA 整理发布,转载请注明出处,更多ACCA 资讯请关注高顿ACCA 官网:。

P2. Financial ReportingIAS 1 Presentation of financial statementsIAS 2 InventoriesIAS 7 Statements of cash flowsIAS 8 Accounting policies, changes in accounting estimates and errors IAS 10 √ Events after the reporting periodIAS 11 √ Construction contractsIAS 12 ★★ Income taxesIAS 16 √ Property, plant and equipmentIAS 17 √ LeasesIAS 18 RevenueIAS 19 ★★★ Employee benefitsIAS 20 Accounting for government grants and disclosure of government assistanceIAS 21 ★★★ The effects of changes in foreign exchange ratesIAS 23 Borrowing costsIAS 24 √ Related party disclosuresIAS 27 Separate financial statementsIAS 28 Investments in associatesIAS 31 Interests in joint venturesIAS 32 Financial instruments: presentationIAS 33 Earnings per shareIAS 34 Interim financial reportingIAS 36 √ Impairment of assetsIAS 37 ★★★ Provisions, contingent liabilities and contingent assetsIAS 38 √ Intangible assetsIAS 39 Financial instruments: recognition and measurementIAS 40 √ Investment propertyIAS 41 √ AgricultureIFRS 2 ★★★ Share‐based paymentIFRS 3 ★ Business combinationsIFRS 5 ★★★ Non‐current assets held for sale and discontinued operations IFRS 7 Financial instruments: disclosuresIFRS 8 ★★★ Operating segmentsIFRS 9 ★★ Financial InstrumentsIFRS 10 ★ Consolidated financial statementsIFRS 11 ★★★ Joint arrangementsIFRS 13 ★★★ Fair value measurementIFRS 15 ★★★ Revenue from contracts with customersIFRS 16 √ Leases不考or非重点:IAS 26 * Accounting and reporting by retirement benefit plans IAS 29 * Financial reporting in hyperinflationary economiesIAS 30 * Disclosure in the financial statements of banks and similar financial institutions (not examinable)IFRS 1* First time adoption of International Financial Reporting StandardsIFRS 4 * Insurance contractsIFRS 6 * Exploration for and evaluation of mineral resourcesIFRS 12* Disclosures of interests in other entitiesIFRS 14* Regulatory deferral accountsPart 1.The IASB’s Conceptual Framework for Financial Reporting1.财报的目的:The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity. Those decisions involve buying, selling or holding equity and debt instruments, and providing or settling loans and other forms of credit.2.财报提供的信息:General purpose financial reports do not and cannot provide all of the information,需要结合其他信息,譬如整个经济环境和预期,政治风向和事件,行业及公司展望等。

P2. Financial ReportingIAS 1 Presentation of financial statementsIAS 2 InventoriesIAS 7 Statements of cash flowsIAS 8 Accounting policies, changes in accounting estimates and errors IAS 10 √ Events after the reporting periodIAS 11 √ Construction contractsIAS 12 ★★ Income taxesIAS 16 √ Property, plant and equipmentIAS 17 √ LeasesIAS 18 RevenueIAS 19 ★★★ Employee benefitsIAS 20 Accounting for government grants and disclosure of government assistanceIAS 21 ★★★ The effects of changes in foreign exchange ratesIAS 23 Borrowing costsIAS 24 √ Related party disclosuresIAS 27 Separate financial statementsIAS 28 Investments in associatesIAS 31 Interests in joint venturesIAS 32 Financial instruments: presentationIAS 33 Earnings per shareIAS 34 Interim financial reportingIAS 36 √ Impairment of assetsIAS 37 ★★★ Provisions, contingent liabilities and contingent assetsIAS 38 √ Intangible assetsIAS 39 Financial instruments: recognition and measurementIAS 40 √ Investment propertyIAS 41 √ AgricultureIFRS 2 ★★★ Share‐based paymentIFRS 3 ★ Business combinationsIFRS 5 ★★★ Non‐current assets held for sale and discontinued operations IFRS 7 Financial instruments: disclosuresIFRS 8 ★★★ Operating segmentsIFRS 9 ★★ Financial InstrumentsIFRS 10 ★ Consolidated financial statementsIFRS 11 ★★★ Joint arrangementsIFRS 13 ★★★ Fair value measurementIFRS 15 ★★★ Revenue from contracts with customersIFRS 16 √ Leases不考or非重点:IAS 26 * Accounting and reporting by retirement benefit plans IAS 29 * Financial reporting in hyperinflationary economiesIAS 30 * Disclosure in the financial statements of banks and similar financial institutions (not examinable)IFRS 1* First time adoption of International Financial Reporting StandardsIFRS 4 * Insurance contractsIFRS 6 * Exploration for and evaluation of mineral resourcesIFRS 12* Disclosures of interests in other entitiesIFRS 14* Regulatory deferral accountsPart 1.The IASB’s Conceptual Framework for Financial Reporting1.财报的目的:The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity. Those decisions involve buying, selling or holding equity and debt instruments, and providing or settling loans and other forms of credit.2.财报提供的信息:General purpose financial reports do not and cannot provide all of the information,需要结合其他信息,譬如整个经济环境和预期,政治风向和事件,行业及公司展望等。

2014年ACCA考试(p2公司报告)考前总结27本文由高顿ACCA整理发布,转载请注明出处DerivativesA derivative is a financial instrument that derives its value from the price or rate of an underlying item.Common examples of derivatives include:(a) Forward contracts: agreements to buy or sell an asset at a fixed price at a fixed future date(b) Futures contracts: similar to forward contracts except that contracts are standardized and traded on an exchange(c) Options: rights (but not obligations) for the option holder to exercise at apre-determined price; the option writer loses out if the option is exercised(d) Swaps: agreements to swap one set of cash flows for another (normally interest rate or currency swaps)IAS 32 Presentation of financial instrumentsThe objective of IAS 32: to enhance financial statement users understanding of the significance of on-balance-sheet and off-balance-sheet financial instruments to an entity’s financial position, performance and cash flows.Financial instruments must be classified as liabilities or equity according to their substance.Compound instruments are split into equity and liability components and presented accordingly in the statement of financial position.IAS32 requires the component parts of the instrument to be classified separately, according to the substance of the contractual arrangement and the definitions of a financial liability and an equity instrument. Ie convertible debt.更多ACCA资讯请关注高顿ACCA官网:。

accap2知识点总结In this article, we will provide a comprehensive summary of the key concepts covered in the ACCA P2 Management Accounting course. We will discuss the importance of management accounting, the different techniques and tools used in management accounting, and how these techniques can be applied in real-life business situations.Importance of Management AccountingManagement accounting plays a critical role in helping organizations make informed business decisions. It involves the use of financial and non-financial information to help managers plan, control, and make decisions to achieve organizational objectives. Management accounting also helps in the monitoring and evaluation of business performance, and in the formulation of strategies for financial planning, control and decision making.The key areas covered in the ACCA P2 Management Accounting course include:1. Cost and Management AccountingCost and management accounting involves the identification, measurement, and analysis of costs to help in control and decision making. This includes classifying costs by behavior, function, and nature, the use of cost allocation methods, and understanding cost-volume-profit relationships.Students will also learn about different costing methods such as job costing, process costing, and activity-based costing. They will also learn how to analyze and interpret cost data to make relevant business decisions.2. BudgetingBudgeting is an essential management accounting tool that involves planning and controlling an organization's financial resources. Students will learn how to prepare different types of budgets such as sales, production, cash, and master budgets. They will also learn about the benefits of budgeting, the budgetary control process, and how to use variance analysis to evaluate the performance of different business activities.3. Capital Investment DecisionsCapital investment decisions involve the evaluation and selection of long-term investment proposals. Students will learn about different capital investment appraisal techniques such as payback period, accounting rate of return, net present value, and internal rate of return. They will also learn how to apply these techniques in different investment scenarios to evaluate the profitability and viability of investment projects.4. Performance ManagementPerformance management involves the use of performance measures and management control systems to assess and improve the performance of individuals, departments, and organizations. Students will learn about different performance measurement frameworks, key performance indicators, and how to design and implement performance management systems to align organizational goals with individual and departmental objectives.Real-Life Application of Management Accounting TechniquesThe concepts and techniques covered in the ACCA P2 Management Accounting course are applicable in various business scenarios. For example, cost and management accounting techniques are used to establish product costs, assess pricing decisions, and improve cost control. Budgeting techniques are used to set targets, allocate resources, and evaluate business performance. Capital investment appraisal techniques are used to evaluate potential investment opportunities and make informed investment decisions. Performance management techniques are used to measure and evaluate employee and organizational performance, as well as to improve accountability and control.ConclusionIn conclusion, the ACCA P2 Management Accounting course covers a wide range of management accounting techniques that are essential for anyone aspiring to pursue a career in management accounting, finance, or business. The course provides students with a solid foundation in understanding the key concepts, tools, and techniques used in management accounting, and how these techniques can be applied in real-life business situations. By mastering these concepts, students will be equipped with the knowledge and skills necessary to add value to the organizations they work for, by helping them make informed and strategic business decisions.。

2014年ACCA考试F4公司法与商法第一章总汇2本文由高顿ACCA整理发布,转载请注明出处Session 2 Sources of dataMain contents:1. Types of data2. Secondary data3. Sampling methods2.1 Types of dataData can be classified as follows:(a)Primary and secondary dataPrimary data – are data collected especially for a specific purpose.Secondary data – are data which have been collected elsewhere, for someother purposes, but which can be used or adapted for thesurvey being conducted.(b)Discrete and continuous dataDiscrete data – are data which can only be taken on a finite or countablenumber of values within a given range.Continuous data – are data which can take on any value.(c )Sample and population dataSample data – are data arising as a result of investigating a samplePopulation data – are data arising as a result of investigating the population.2.2 Secondary dataThe main sources of secondary data are: governments; banks; newspaper; trade journals; information bureau; consultancies; libraries and information services.- It is essential to believe that the secondary data used is accurate and reliable.2.3 Sampling methodsData are often collected from a sample rather than from a population. If the whole population is examined, the survey is called a census.There are two types of sampling methods:Probability sampling method – is a sampling method in which there is a known chance of each member of the population appearing in the sample.- Random- Stratified random- Systematic- Multistage- ClusterIf random sampling is used, it is necessary to construct a sampling frame.A sampling frame should have following characteristics- completeness- accuracy- adequacy- up to dateness- convenience- non-duplicationNon probability sampling method – is a sampling method in which the chance of each member of the population appearing in the sample is not know, i.e. quota sampling.Example 1:The following statements relate to which different types of data(i). Secondary data are data collected especially for a specific purpose(ii). Discrete data can take on any value.(iii) Qualitative data are data that cannot be measured(iv). Population data are data arising as a result of investigating a group of people or Objects.Which of the statements are true?A.(i)and(ii)onlyB.(ii)and(iii)onlyC.(ii)and(iv)onlyD.(iii)and(iv)onlySolution is DIt is primary data that is collected for a specific purpose so (i) is false. Continuous data can take on any value so (ii) is false. Both (iii) and (iv) are true.Example 2:Which of the following statements are not true?I If a sample is selected using random sampling, it will be free from bias.II A sampling frame is a numbered list of all items in a sample.III In cluster sampling there is very little potential for bias.IV In quota sampling, investigators are told to interview all the people they meetUp to a certain quota.A I, II, III and IVB I, II and IIIC II and IIID II onlySolution is CA sampling frame is a numbered list of all items in a population (not a sample)Cluster sampling involves selecting one definable subsection of the population which therefore makes the potential for bias considerable.更多ACCA资讯请关注高顿ACCA官网:。

2014年ACCA新大纲考试科目全介绍

Corporate Reporting (P2)

科目介绍:

P2《公司报告》是F7(财务报告)的后续课程,它更加深入地考察会计师对会计准则的掌握以及在商业环境下对财务报告原理和做法的运用与评估。

P2主要分为四大部分。

1.大纲考察的是,根据公认会计原则和相关会计准则,会计师在编制合并财务报表时

所要考虑的财务报告框架;

2.大纲考察的是特殊行业的报表特点,包括非盈利组织和中小企业;

3.大纲更深入地考察会计师的财务分析能力和对公司报告的影响;

4.大纲考察一些会计准则当前的发展变化以及它们对财务报告的影响。

近几年考试通过率趋势图:

知识结构:

科目关联性:

P2课程是ACCA财务会计体系下的最后一门课程,它是前面F3、F7课程的后续课程,在F3和F7的基础上更加深入地考察考生对会计准则的掌握程度和运用相关知识进行财务分析的能力。

和P2某些内容有写关联的是ACCA的最后一门课程P7(高级审计和鉴证)。

考试形式:

P2的考前阅读时间为15分钟,考试时长为3小时,分为两个部分,A部分一道题50分为必选题,考察的是编制合并财务报表,包括合并现金流量表和解决财务报告中的问题;B部分共有三道题每道25分,可以任选两题作答,通常是两道案例分析,一道带计算的论述题,考察的是大纲其他部分内容。

新旧考纲的主要变化:

总体而言,从2014年9月开始的P2考试,没有新的内容加入考纲。

但是在考纲内容上有一些微调。

对于微调内容的对比,我们将以表格的形式展现出来,如下:

从2014年9月之后的考试,这里明确规定有两个制定部分将从考纲中删除,如一下图标所示。

但是在考察文件中会有一些变化,特别有可能会考察大家一些drafts内容。

考试形式:

P2的考试时长为15分钟的阅读时间以及3小时的正式答题时间。

考试形式在并未发生显著变化。

考试分为两个部分:section A 选择题,section B解答题。

Section A 是一道必答题,分值为50分。

Section B 从三题中选择两题做答,分值为25分每题。

题型例举:

Section A 编制合并报表

Section B Essay type question

总结:从题型上看并无过多变化,同学们在复习的时候将历年考题反复练习,常考到的working一定要非常熟练的会算,这样方能通过考试。