新华保险祥瑞一生终身寿险(分红型)学习课件

- 格式:ppt

- 大小:6.00 MB

- 文档页数:3

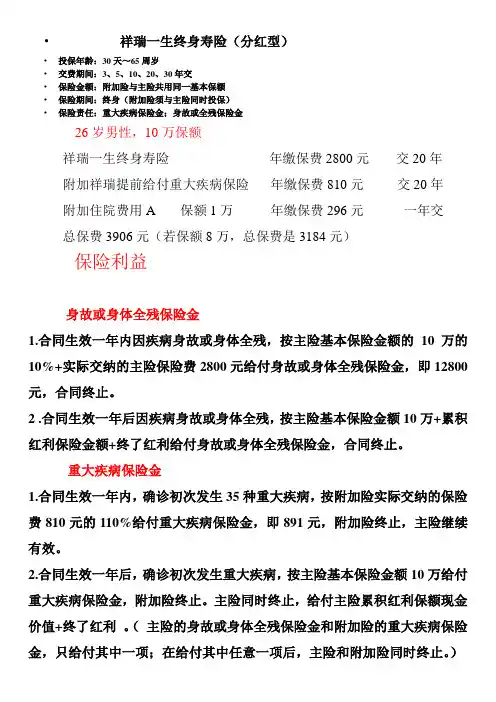

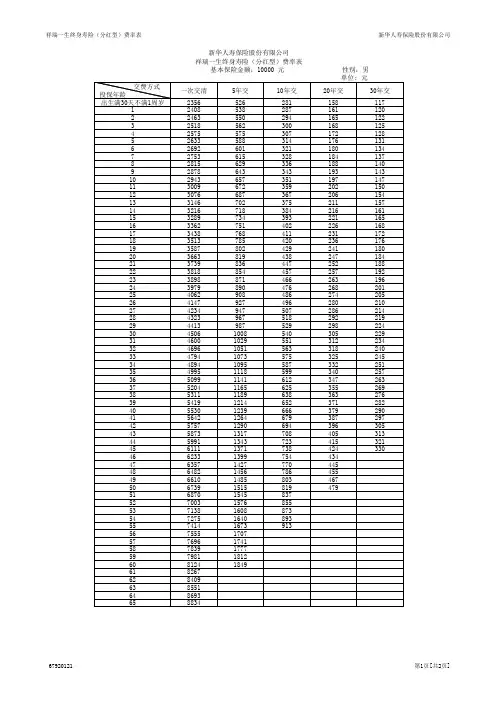

•祥瑞一生终身寿险(分红型)•投保年龄:30天~65周岁•交费期间:3、5、10、20、30年交•保险金额:附加险与主险共用同一基本保额•保险期间:终身(附加险须与主险同时投保)•保险责任:重大疾病保险金;身故或全残保险金26岁男性,10万保额祥瑞一生终身寿险年缴保费2800元交20年附加祥瑞提前给付重大疾病保险年缴保费810元交20年附加住院费用A 保额1万年缴保费296元一年交总保费3906元(若保额8万,总保费是3184元)保险利益身故或身体全残保险金1.合同生效一年内因疾病身故或身体全残,按主险基本保险金额的10万的10%+实际交纳的主险保险费2800元给付身故或身体全残保险金,即12800元,合同终止。

2 .合同生效一年后因疾病身故或身体全残,按主险基本保险金额10万+累积红利保险金额+终了红利给付身故或身体全残保险金,合同终止。

重大疾病保险金1.合同生效一年内,确诊初次发生35种重大疾病,按附加险实际交纳的保险费810元的110%给付重大疾病保险金,即891元,附加险终止,主险继续有效。

2.合同生效一年后,确诊初次发生重大疾病,按主险基本保险金额10万给付重大疾病保险金,附加险终止。

主险同时终止,给付主险累积红利保额现金价值+终了红利。

(主险的身故或身体全残保险金和附加险的重大疾病保险金,只给付其中一项;在给付其中任意一项后,主险和附加险同时终止。

)无忧养老金投保10年后,且被保险人须年满60周岁,他可以选择保单现金价值部分转换为养老金。

保费豁免投保人因意外伤害身故或因意外伤害身体全残,且年龄在18至60岁之间,可以免交主险续期保费,合同继续有效。

住院医疗每次住院,对超过500元的部分按70%--95%的比例报销,其中床位费按每天20元,每次支付180天。

本计划所指重大疾病范畴1.恶性肿瘤——不包括部分早期恶性肿瘤2.急性心肌梗塞3.脑中风后遗症——永久性的功能障碍4.重大器官移植术或造血干细胞移植术——须异体移植手术5.冠状动脉搭桥术(或称冠状动脉旁路移植术)——须开胸手术6.终末期肾病(或称慢性肾功能衰竭尿毒症期)——须透析治疗或肾脏移植手术7.多个肢体缺失——完全性断离8.急性或亚急性重症肝炎9.良性脑肿瘤——须开颅手术或放射治疗10.慢性肝功能衰竭失代偿期——不包括酗酒或药物滥用所致11.脑炎后遗症或脑膜炎后遗症——永久性的功能障碍12.深度昏迷——不包括酗酒或药物滥用所致13.双耳失聪——永久不可逆(除内耳结构损伤等情形外,被保险人申请理赔时年龄必须在三周岁以上,并且提供理赔当时的听力丧失诊断及检查证据。

新华保险培训课件摘要随着我国GDP保持持续增长,社会保险制度的改革,我国保险行业历经三十年的发展,已经形成巨大规模,与社会保障形成一个完整的社会保障体系,已经成为国民经济主要的组成部分,势必发挥越来越重要的作用。

我国保险市场在从不成熟到成熟的发展过程中,整个行业大体上要经历从单纯追求保费收入规模、到追求实际利润、再到实现个性化服务的三个阶段。

步入21世纪,面对复杂的国内外经济形势,中国保险行业发展驱动因素的效应逐渐减弱,进入了周期性调整阶段,各项矛盾和问题逐渐显现,可以说,中国寿险业已经到了不得不进行改革的阶段。

内蒙古自治区作为中国地域最辽阔、矿产资源丰富的西部少数民族自治区,经济增速保持国内领先水平,却由于自身诸多不利因素的限制,导致保险行业发展方面一直处于较低水平。

内蒙古寿险行业发展历程代表了我国大部分欠发达地区的发展特点,可以说,研究内蒙古寿险行业在转型期的发展,对我国保险行业发展具有典型示范作用。

本文以国内第三大寿险企业——新华人寿保险股份有限公司(以下简称“新华保险”)2004年在内蒙古自治区设立的二级直管分公司为例进行分析和阐述。

通过剖析新华保险内蒙古分公司发展现状,结合相关理论研究,利用SWOT分析方法,提出在当前经济发展形式和企业现状下的寿险发展的思路和举措,解决企业在经营管理实践中遇到的各种问题,本文对新华保险内蒙古分公司的发展环境及发展条件进行分析,提出“以客户为中心”为核心的总体发展战略,及战略实施的路径。

意在通过实现内蒙新华发展战略转型,为中西部城市型机构的未来寿险发展提供借鉴。

关键词:新华保险、内蒙古分公司、发展战略、客户导向、价值成长AbstractWith the reform of China's GDP to maintain sustained growth, the social insurance system, China's insurance industry after three years of development, has become a huge scale, and Social Security to form a complete social security system, has become a major part of the national economy, is bound play an increasingly important role.China's insurance market, from immaturity to maturity in the development process, the industry is generally go through three stages from the simple pursuit of premium income scale, to the pursuit of actual profits, to achieve personalized service.Entering the 21st century, the face of complex domestic and international economic situation, the effects of China's insurance industry drivers gradually weakened into a cyclical adjustment phase, the contradictions and problems gradually, it can be said that China's life insurance industry has to have carry out stage of reform.As China's Inner Mongolia region's most vast, mineral-rich eastern and western ethnic minority autonomous regions, economic growth remained the leading domestic level, but due to their limited number of unfavorable factors, led to the development aspects of the insurance industry has been at a low level.Development of Inner Mongolia, on behalf of the life insurance industry in most underdeveloped areas of development characteristics, we can say, the life insurance industry research and development in Inner Mongolia in the transition period, the development of China's insurance industry has a typical role model. .In this paper, the third largest life insurance companies - China Life Insurance Co., Ltd. (hereinafter referred to as "NCI") in 2004 in Inner Mongolia Autonomous Region, established two straight branches example for analysis and elaboration. By analyzing the development status NCI Inner Mongolia Branch, combining theoretical research, the use of SWOT analysis method, ideas and initiatives in the form of life insurance development economic development and current status of the enterprise, to solve various enterprise management encountered in practice problem,In this paper, the development of the environment and conditions for the development of Inner Mongolia Branch of NCI analyzed that "customer-centric" as the core of the overall development strategy, and strategy implementation path. Inner Mongolia, Xinhua intended to achieve development through strategic transformation,life insurance for the future development of Midwest City-based institutions to provide reference.Keywords: NCI, Inner Mongolia Branch, development strategy, customer-oriented, value growth目录第一章引言 (8)1.1 选题背景及研究意义 (8)1.2 国内外研究现状 (9)1.3 研究思路及方法 (12)1.4 研究内容简介 (14)第二章新华保险内蒙古分公司发展现状评述 (16)2.1 新华保险简介 (16)2.2 新华保险内蒙古分公司发展历程及现状 (19)2.3 新华保险内蒙古分公司发展中存在问题 (22)第三章新华保险内蒙古分公司发展环境分析 (29)3.1 宏观环境分析 (29)3.1.1 政策法律环境分析 (29)3.1.2 经济环境分析 (31)3.1.3 社会文化环境分析 (32)3.2 行业环境分析 (33)3.2.1 行业基本特征分析 (33)3.2.2 行业竞争环境分析 (34)3.2.3 行业发展趋势分析 (36)3.3 发展机遇与威胁分析 (36)第四章新华保险内蒙古分公司发展条件分析 (39)4.1 资源条件分析 (39)4.1.1 产品开发资源分析 (39)4.1.2 人力条件资源分析 (40)4.1.3 企业文化条件分析 (42)4.2 能力条件分析 (44)4.2.1 管理能力条件分析 (44)4.2.2 人力管理体系分析 (47)4.2.3 服务能力条件分析 (48)4.3 优势分析 (48)4.4 劣势分析 (49)第五章新华保险内蒙古分公司发展战略与路径 (52)5.1 SWOT分析 (52)5.2 总体发展战略 (53)5.3 战略发展目标 (53)5.4 目标市场定位 (53)5.5 战略发展路径 (54)第六章新华保险内蒙古分公司战略实施保障举措 (58)6.1 强健营销队伍、推动价值增长 (58)6.2 渠道服务品质改良、防止业务品质下滑 (59)6.3 提升运营支持能力、提高客户满意度 (59)6.4 信息技术支撑、保障客户关系长久提升 (59)6.5 搭建高素质人才队伍、全面提升管理能力 (59)第七章结论及展望 (61)7.1 研究结论 (61)7.2 进一步研究展望 (61)第一章引言1.1 选题背景及研究意义在经过了三十多年发展的中国保险行业后,它已经变成了我国经济的重要支柱,为我国国民经济的增长做出了巨大贡献,承担着巨大的社会责任。