ACCA F3知识点:易混淆的坏账、疑账

- 格式:doc

- 大小:77.51 KB

- 文档页数:3

2014年ACCA新大纲考试科目全介绍Financial Accounting (FFA/F3)科目介绍:F3课程主要向学员介绍了财务会计准则、相关会计科目账户建立以及准确财务信息的提供。

大纲介绍了财务报表编制准备及会计科目建立原则。

接着大纲深入展开了公司各类经营行为的会计记录方法,如何使用试算平衡表使用、如何改正账面错误以及需合并报表或非合并报表财务报告的准备工作。

之后大纲分出两个重点方向展开,一是要求考生能够对财务报表做一些简单的解读;二是要求学员能够做报表合并。

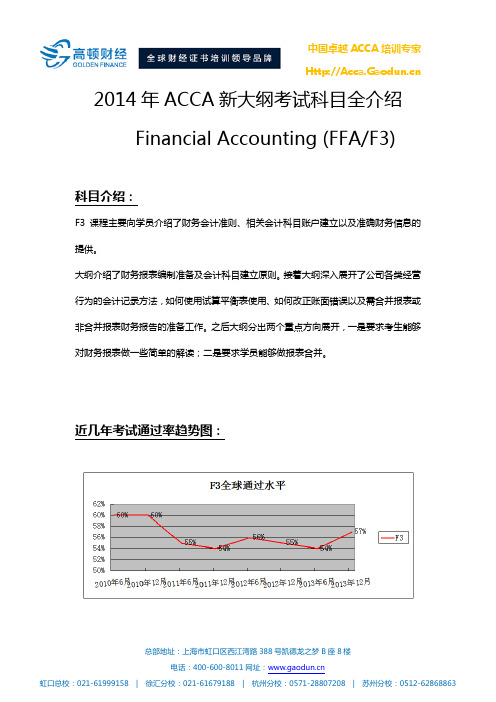

近几年考试通过率趋势图:知识结构:科目关联性:F3课程是ACCA财务会计体系下的基础课程,而财务会计是ACCA主要核心内容,F3也是帮助学员建立财务会计概念财务报表编制、合并、解读的相关知识;因此F3是F7财务报告、P2公司报告的基础。

考试形式:F3的考试时长为2小时。

考生可以采用参加统一笔答考试或在计算机考试中心参与计算机考试两种形式。

考试题型由50个单选变为35个单选2个多任务题,单选题共70分,每个任务题15分。

新旧考纲的主要变化:2014年,主要是考试题型上出现了较大的变化,主要是为了更加接近F7财务报告相关考试要求,缩小了两级考试之间的考试难度。

相比之下,F3考试难度增加了,F7反而降低了,在知识结构上,F3的考纲主要是增加了对编制合并报表的要求。

加强了与F7的联系,为考生步入F7的学习打好铺垫。

并且,编制合并报表从简单的选择题到有一定难度的任务题,要求考生熟练掌握报表格式和编制过程。

具体变化点如下:新考纲--任务题(样题):Question 1The following information relates to Geofrost, a limited liability company, for the year ended 31 October 20X7.Extracts from the statement of profit or loss for the year ended 31 October 20X7Additional information:(1)Depreciation expense for the year was $ 4,658,000(2)Assets with a carrying value of $ 1,974,000 were disposed of at a profit of $ 720,000Complete the cash flow statement of cash flows for the year ended 31 October 20X7 for Geofrost.Statement of cash flows for the year ended 31 October 20X7.Question 2BackgroundOn 1 January 20X3 Gasta Co acquired 75% of the share capital of Erica Co for ﹩1,380,000. The retained earnings of Erica Co at that date were ﹩480,000. Erica Co’s share capital has remained unchanged since the acquisition.The following draft statements of financial position for the two companies have been prepared at 31 December 20X9.The non-controlling interest(NCI) was valued at ﹩450,000 as at 1 January 20X3.Task 1Complete the following to determine the goodwill arising on acquisition.Task 2Are each of the following statements relating to consolidation correct?Yes No The process of consolidation results in a single separate legal entity. ○○NIC will always feature within the consolidated financial statements.○○Goodwill is recalculated using the recent fair values at each reporting period end.○○Task 3Select the formula which correctly calculates NCI as at 31 December 20X9, in accordance with IFRS 10 Consolidated Financial Statements.○ 25% of net assets at 31 December 20X9.○ Fair value of NCI at acquisition + 25% of post acquisition profits.○ Fair valu e of NCI at acquisition +25% retained earnings as at 31 December 20X9Task 4Calculate the following figures which will be reported in Gasta’s consolidated statement of financial position as at 31 December 20X9.。

中公财经培训网:/ ACCA F3目前已全部实施机考,每次机考由题库随机抽取题目,题库定期更新,知识点覆盖所有章节,也就是考官文章中反复强调的“全面考核”。

ACCA F3考试重点归纳F1、F2和F3作为ACCA的基础学科,考官反复强调,对这三科是“全面考核”。

ACCA都会通过各种方法在考试中尽可能的cover the whole syllabus! 因此,请考生千万不要抱任何的侥幸心理。

当然,尽管是全面考核,也一定会有考核重点。

再次强调一次,F3要进行全面考核,因此我以下提到的所谓“重点”仅指该知识点可能在考试中分值所占比例略高。

1. Control account这部分属于会计循环的考核,结合应收应付款,由于该部分只是仅在F3当中考核,因此必定成为考试中的重点。

2. PPE (也常结合编表题目考核,尤其是与投资行为产生的现金流相结合)IAS16这条准则我就不多说什么了,在F3 、F7中都会重点考核,并且会结合其它一些章节进行考核,比如现金流量表和试算平衡表的改错。

此外,在15分的大题中,必定有一个调整事项是关于PPE的,最常见的就是计提折旧和固定资产重估价,总体分值可以达到10分左右。

3. 公司账这是一个F3与F7衔接的章节,因此,也会有比较多分值涉及到此章内容。

(F3的绝大部分内容都在假设是在给一个sole trader做账,但是在F7中只有公司的概念,就不存在sole trader了)这部分你要重点掌握股票发行的账务处理,可赎回优先股的处理,股利的账务处理,税,所有者权益变动表,这几个大的知识点。

(sole trader与company账务处理的区别实际主要在EQUITY部分,所以这部分大部分的知识点都是围绕权益讲解的)4. 报表编制(独体报表包括四张,损益,资产负债表,所有者权益变动,现金流;合并报表包括两张,合并损益及合并资产负债表)。

2015 年12 月ACCA F3考试知识点汇总☆Types of business entity A business can be organized in one of the several ways: ●Sole trader –a business owned and operated by one person.The simple form of business is the sole trader. This is owned and managed by one person, although there might be any number of employees. A sole trader is fully personall y liable for any losses that the business might make.●Partnership –a business owned and operated by two or more people.A partnership is a business owned jointly by a number of partners. The partners are jointly and severely liable for any losses that the business might make. (Traditionally the big accounting firms have been partnerships, although some are con verting their status to limited liability companies.)●Limited Liability Company –a business owned by many people and operated by m any ( though not necessarily the same) people. Companies are owned by shareholders. Sha reholders are also known as members. As a group, they elect the directors who run the b usiness. Companies are always limited companies.In summary, types of business entity should be differentiated in Ownership; Operation right and Liability for the business to undertake.For all three types of entity, the money put up by the individual, the partners or the shareholders, is referred to as the business capital. In the case of a company, this capital is divided into shares. ☆Business Transactions: Main types of business transactions for a business include:●Purchase of inventory for resale●Sales of goods●Purchase of non-current assets●Payment of expenses●Introduction of new capital to the business●Withdrawal of funds from the business by the owner☆Cash and credit transactions:Cash transactions: the buyer pays for the item immediately or possibly in advance. Credit transactions: the buyer does not have to pay for the item on receipt, but is all owed some time ( a credit period) before having to make the payment.☆Definition of accountingRecording : transactions must be recorded as they occur in order to provide up-to-dat e information for management.Summarizing: the transactions for a period are summarized in order to provide inform ation about the company to interested parties.☆Types of accountingFinancial accounting vs management accountingAccounting reports users include:●Management: Need information about the company’s financial situation as it is curre ntly and it is expected to be in the future. This is to enable them to manage the business efficiently and to make effective decisions.●Investors: The providers of risk, capital and their advisers are concerned with theris k inherent in, and return provided by, their investments. They need information to help th em determine whether they should buy, hold or sell.●Trade payables/ Suppliers: Suppliers and other trade payables. Suppliers and other tr ade payables are interested in information that enables them to determine whether amounts owing to them will be paid when due. Trade payables are likely to be interested in an enterprise over a shorter period than lenders unless they are dependent upon the continuanc e of an enterprise as a major customer.●Shareholders: Shareholders are also interested in market value of shares as well as information which enables them to assess the ability of the enterprise to pay dividends.●Lenders: Lenders are interested in information that enables them to determine wheth er their loans, and the interest attaching to them, will be paid when due.●Customers: Customers have an interest in information about the continuance of an e nterprise, especially when they have a long term involvement with or are dependent on, th e enterprise.●Government and their agencies: Governments are their agencies are interested in the allocation of resources and, therefore, the activities of enterprises. They also require infor mation in order to regulate the activities of enterprises, determine taxation policies and as the basis for national income and similar statistics.●Employees: Employees and their representative groups are interested in information a bout the stability and profitability of their employers. They are also interested in informati on which enables them to assess the ability of the enterprise to prove remuneration, retire ment benefits and employment opportunities.●General public: Enterprises affect members of the public in an variety of ways. For example, enterprises may make a substantial contribution to the local economy in many ways including the number of people they employ and their patronage of local suppliers. Financial statements may assist the public by providing information about the trends and recent developments in the prosperity of the enterprise and the range of its activities.☆The business entity conceptThe business entity concept●States that financial accounting information relates only to the activities of the busin ess entity and not to the activities of its owner.●The business entity is treated as separate from its owners.☆Financial Statements include:- a statement of financial position at the end of the period- a statement of comprehensive income for the period- a statement of changes in equity for the period- statement of cash flows for the period- notes, comprising a summary of accounting policies and other explanatory notes The statement of financial position:Statement of Financial Position: showing the financial position of a business at a poin t of time. The Vertical format of the SFP: (Statement of Financial Position as at31 December 2007)●The top half of the balance sheet shows the assets of the business.●The bottom half of the balance sheet shows the capital and liabilities of the busines s.A Statement of financial position at the end of the period (Balance Sheet): W Xang Balance Sheet as at December 31 20X6The horizontal format of the SFP: (Statement of Financial Position as at 31 Decembe r 2007)●The left half of the balance sheet shows the assets of the business.●The right half of the balance sheet shows the capital and liabilities of the business. W XangStatement of Financial Position as at 31 December 20x6☆The accounting equationFinancial accounting is based upon a very simple idea:The amount of resources supplied by the owner is called capital. The actual resources that are then in the business are called assets. Usually, people other than the owner have supplied some, of the assets, for example, a supplier supplies stock of goods on credit. The business is said to owe a liability towards these suppliers. The following accounting equation always holds true:The accounting equation:ASSETS = PROPRITOR’S CAPITAL + LIABILITIES- Any point in time, the assets of the business will be equal to its liabilities plus the capital of the business;- Assets less liabilities equal the capital of the business, which is known as netassets. - Each and every transaction that the business makes or enters into has two aspects to it and have a double effect on the business and the accounting equation. This is known as the duality concept.Duality concept: Each and every transaction that the business makes or enters into ha s two aspects to it and has a double effect on the business and the accounting equations. This is known as duality concept.if A=C+L=0 .......①C=A-L........②Illustration:1). Carl sets up in business by opening a coffee shop –Carl’s Coffee. He puts $5,00 0 into a business bank account.The opening accounting equation is:Assets (Cash in bank)= Capital + Liabilities($5,000) = ($5,000) + ($0)2). Carl buys furniture (chairs and tables) for the shop for $1,500, paying the supplie r out of the business bank account.The accounting equation after this transaction is:Assets Capital + Liabilties( Cash in bank $3,500) = ($5,000) ($0)(Furniture $ 1,500)3). Now Carl spends a further $2,000 to buy coffee-making equipment and $800 on crockery and cutlery, paying cash out of the business bank account.The accounting equation after this transaction is:Assets Capital + Liabilties(Cash in Bank $700) = ($5,000) ($0)(Equipment $2,000)(Fitting & Fixture $800)(Furniture $1,500)4). Carl persuades his bank to lend $1,000 to develop the business. The bank loan is accounted for as a liability of the business.The accounting equation is now as follows:Assets Capital + Liabilties(Cash in Bank $1,700) = ($5,000) ($1,000)(Equipment $2,000)( Fitting & Fixture $800)(Furniture $ 1,500)5). Carl now buys coffee, tea, milk, sugar, biscuits and cakes for $700, and pays in cash from the business bank account.The accounting equation is now as follows:Assets Capital + Liabilties(Inventory $700) = ($5,000) ($1,000)(Equipment $2,000)(Fitting & Fixture $800)(Furniture $1,500)(Cash in Bank $ 1,000)6). In his first day of trading, Carl uses up $650 of his inventory, and makes sales t otaling $1,050. All his sales are in cash.The accounting equation at the end of the day is as follows:Assets Capital + Liabilities(Inventory $50) = (Beginning $5,000) ($1,000)(Equipment $2,000) ( Profit $400)(Fitting & Fixture $800)(Furniture $1,500)( Cash in bank $2,050)☆Classification of Assets and LiabilitiesAssets: An asset is something owned or controlled by the business that will result in future economic benefits to the business. ( an inflow of cash or other assets.) Such as:Current assets:are assets owned by the business with the intention of turning them int o cash within one year (accounting period).This definition allows inventory or receivables to quality as current assets, e ven if the y may not be realized into cash within 12 months.Non-current asset: is an asset held for and used in operation(rather than for selling to customer), with a view to earning income or making profits from its use, for over more than one year ( accounting period).Liability: is something owed by the business to someone else.Current liability: These include the debts of the business that are repayable within the next 12 months.Non-current liabilities: are liabilities that do not need to be settled for at least one ye ar. (excluding the current portion of the debt)Capital: Capital is a type of liability. It represents the owner’s net investment in the business. Capital appears as a credit balance on the balance sheet.Assets –Liabilities = PROPRIETOR’S CAPITALNet Assets =( T otal )Assets –(T otal) LiabilitiesCapital (at SFP date) = Capital introduced + Profit –DrawingsDrawing: Drawings are any amounts taken out of the business by the owner for their own personal use. Drawings will reduce the capital balance reported on the balance sheet.Include:●Money taken out of the business●Goods taken for personal use●Personal expenses paid by the businessIncome statementIncome statement:Mr. W XangIncome statement for the year ended 31 December 20X6●Showing the financial performance of a business over a period of time.●Reports revenue and expenses for the period.●The sales revenue shows the income from goods sold in the year●The cost of buying the goods sold must be deducted from the revenue●The current year’s sales will include goods bought in the previous year, so this ope ning inventory must be added to the current year’s purchases.●Some of this year’s purchases will be unsold at 31/12/20x6 and this closing invento ry must be deducted from purchases to be set off against next year’s sales.●The first part gives gross profit. The second part gives net profit.The I.S. prepared following the accruals concept.Accrual concept:●Income and expenses are recorded in the I.S. as they are earned / incurred regardles s of whether cash has been received/ paid.(Sales revenue: income from goods sold in the year, regardless of whether those good s have been paid for.)☆Relationship between a statement of financial position and a statement of income●The balance sheets are not isolated statements, they are linked over time with the in come statement●As the business records a profit in the income statement, that profit is added to the capital section of the balance sheet, along with any capital introduced. Cash taken out of the business by the proprietor, called drawings, is deducted. Illustration –the accounting equation:The transactions:Day 1 Avon commences business introduction $1,000 cash.Day 2 Buys a motor car for $400 cash.Day 3 Buys inventory for $200 cash.Day 4 Sells all the goods bought on Day 3 for $300 cash.Day 5 Buys inventory for $400 on credit.SFP at the end of each day’s transactions:Solution:Day 1 Assets (Cash $1,000) = Capital ($1,000) + Liabilities ($0)Day 2 Assets (Motor $400) = Capital ($1,000) + Liabilities ($0)(Cash $600)Day 3 Assets ( Inventory $200) = Capital($1,000) + Liabilities ($0)(Motor $400)(Cash $400)Day 4 Assets ( Motor$ 400) = Capital + Liabilities ($0)(Cash $700) (Beginning$1,000)(Profit $100)Day 5 Assets (Inventory $ 400) = Capital + Liabilities( Motor$ 400) (Beginning$1,000)($400)(Cash $700) (Profit $100)Avon Statement of Financial Position as at end of Day 5Example: Continuing from the illustration above, prepare the SFP at the end of each day after accounting for the transactions below:Day 6 Sells half of the goods bought on Day 5 on credit for $250.Day 7 Pays $200 to his supplier.Day 8 Receives $100 from a customer.Day 9 Proprietor draws $75 in cash.Day 10 Pays rent of $40 in cash.Day 11 Receives a loan of $600 repayable in two years.Day 12 Pays cash of $30 for insurance.Your starting point is the SFP at the end of Day 5, from the illustration above. Prepare: SFP at the end of Day 12I.S. for the first 12 days of trading.Solution:Day 6 Assets (Inventory $ 200) = Capital + Liabilities( Motor$ 400) (Beginning$1,000)($400)(Cash $700) (Profit $150)(A/Receivable$250)Day 7 Assets (Inventory $ 200) = Capital + Liabilities( Motor$ 400) (Beginning$1,000)($200)(Cash $500) (Profit $150)(A/Receivable$250)Day 8 Assets (Inventory $ 200) = Capital + Liabilities ( Motor$ 400) (Beginning$1,000)($200)(Cash $600) (Profit $150)(A/Receivable$150)Day 9 Assets (Inventory $ 200) = Capital + Liabilities ( Motor$ 400) (Beginning$1,000)($200)(Cash $525) (Profit $150)(A/Receivable$150) (Drawing $75)Day 10 Assets (Inventory $ 200) = Capital + Liabilities ( Motor$ 400) (Beginning$1,000)($200)(Cash $485) (Profit $110)(A/Receivable$150) (Drawing $75)Day 11 Assets (Inventory $ 200) = Capital + Liabilities ( Motor$ 400) (Beginning$1,000)($200)(Cash $1,085) (Profit $110) ($600)(A/Receivable$150) (Drawing $75)Day 12 Assets (Inventory $ 200) = Capital + Liabilities (Motor$ 400) (Beginning$1,000)($200)(Cash $1,055) (Profit $80 ) ($600)(A/Receivable$150) (Drawing $75)AvonStatement of Financial Position as at end of Day 12AvonIncome statement for the period ended at Day 12Session 3 Double entry bookkeeping☆The duality concept and double entry bookkeepingDuality concept: each and every transaction has a double effect on the business and t he accounting equations.(A= C + L)Rules of double entry bookkeeping:●Each time a transaction is recorded, both effects must be taken into account.●These two effects are equal and opposite such that the accounting equation will al ways prove correct.Assets –Liabilities = Capital●Traditionally, one effect is referred to as the debit side ( Dr.) and the other as the credit side of the entry (Cr.)☆Ledger accounts, debits and creditsLedger account:●transactions are recorded in the relevant ledger accounts. There is a ledger account for each asset, liability, revenue and expenses’item, and for the owner’s capi tal.●Each account has two sides: the debit and credit sides.●The duality concept means that each transaction will affect two ledger accounts ●One account will be debited and the other credited●Whether an entry is to debit or credit side of an account depend on the types of account and the transaction.。

ACCA F3考试重要知识点和考点梳理考察形式1.选择题:2’*35=70’。

包括文字题和计算题。

2.大题:15’*2=30’。

通常是编制两张报表,即SFP,P&L,CFS,CSFP,CP&L,四选二,但是,报表题目也可能以小题的形式出现在选择题,即考查编制报表时的各个working。

知识梳理及重要考点F3,financial accounting, 整本教材的编制顺序,遵照账务处理顺序,如下所示:Chapter1-4:介绍财务会计基础知识。

(1)会计做账主体为企业,即business。

(2)Sole trader, partnership和Limited liabilitycompany各自的特点。

(3)Financial accounting和management accounting的区别。

(4)Accounting equation(5)7种book of prime entry(6)会计5要素及做账原则,即借贷方表示增/减。

(7)Balancing and closing of T accountChapter5-13:常见账户的会计处理,即double entry。

(1) Chapter 5:Returns, discounts and sales tax。

本章主要考查trade discount和early settlement discount的会计处理及这两种折扣情况下如何计算sales tax,即均以折扣后的净值作为计税基础。

而sales revenue的金额,对于trade discount,以折扣后净值确认,对于early settlementdiscount则以折扣前的总数确认;sales tax liability的计算,即output tax减去input tax。

(2)Chapter 6:Inventory。

本章主要考查valuation of inventory,即lower of cost and NRV;adjustment of openingand closing inventory。

超全ACCA FA(F3)8-11章知识点总结(三)(干货精选)ACCA F3是Financial Accounting (FA) 财务会计的简称,主要介绍了财务会计准则、相关会计科目账户建立以及准确财务信息的提供。

F3总体来说知识点细碎,考试范围广,要想掌握好F3的知识点,大量的练习是不可少的。

F3的整体难度为2颗星,建议留出一个月时间备考。

小盟君继续为大家分享ACCA F3知识点。

接前两次1-7章知识点,这次分享8-11章。

1. 每期期末算折旧:使用过程中(每期期末算折旧):Dr : depreciation expenseCr :accumulated depreciation2. 固定资产的处置 :卖出固定资产(固定资产的处置):Dr : disposal accountCr : non-current assetDr : accumulated depreciationCr : disposalDr : cash/bankCr : disposal accountDr: disposalCr : disposal gain3.市值涨价(土地、房屋):土地:Dr: land Cr: revaluation surplus房屋:Dr : buildingDr : Accumulated depreciationCr : revaluation surplus4.Capital expenture&Revenue expenture:Capital expenture资本化支出:花出一笔钱的同时要增加一项固定资产;Revenue expenture费用化支出:需要maintain的费用(水费电费……)5.折旧:直线折旧法straight line:dep=(cost-residue value)/years;余额递减法reducing balance line:dep=%(折旧比例)×(cost-RV);Proportionate depreciation 按比例(大部分是按月出现,记得乘以十二分之月份);Full year depreciation;考试一般考的是FIFO 和 weight average6.Fair value现值:NBV (net book value)账面净值Revaluation surplus 重估增值=f.v - NBV7.retained earning :每年都会有一笔尚未实现的收益转到retained earningDr : revaluation surplusCr : retained earning8.研究阶段 :花出去的所有钱都计入到SPL中做为exp的一项9.Research&Development&Useful life:Research:expense;Development:expense(满足资本化实点后是capital);Useful life:amortization(expense)10.Amortization(无形资产的摊销):不进行摊销时:要每年进行重估;有使用年限时:要用直线法进行摊销11.预付:prepayment 付款期>会计期,属于资产12.预提:accural是current liability 付款期晚于账期13.Accured income收款滞后:Dr:accured income;Cr:bank interest income14.Prepaid income提前收款:Dr:rental income;Cr:prepaid income15.Cash/bank:Cash/bank 永远出现在增加的一边,而结转b/f与SPL永远出现在减少的一方。

Suspense accounts and error correctionby Neil Stein 25 Jul 2003 Professional Scheme, Certified Accounting Technician SchemeRelevant to Paper B1, Paper 1.1 and Paper 3Suspense accounts and error correction are popular topics for examiners because they test understanding of bookkeeping principles so well.A suspense account is a temporary resting place for an entry that will end up somewhere else once its final destination is determined. There are two reasons why a suspense account could be opened:1. a bookkeeper is unsure where to post an item and enters it to a suspense account pendinginstructions2. there is a difference in a trial balance and a suspense account is opened with the amount of thedifference so that the trial balance agrees (pending the discovery and correction of the errors causing the difference). This is the only time an entry is made in the records without a corresponding entry elsewhere (apart from the correction of a trial balance error – see error type 8 in Table 1).For examination purposes we are more often concerned with the second of these – differences and error correction.Types of errorBefore we look at the operation of suspense accounts in error correction, we need to think about types of error – not all types affect the balancing of the records and hence the suspense account. Refer to Table 1. Correcting errorsErrors 1 to 5, when discovered, will be corrected by means of a journal entry between the accounts affected. Errors 6 to 9 also require journal entries to correct them, but one side of the journal entry will be to the suspense account opened for the difference in the records. Type 8, trial balance errors, are different. As the suspense account records the difference, an entry to it is needed, because the error affects the difference. However, there is no ledger entry for the other side of the correction – the trial balance is simply amended. An illustrative questionThis is Question 2 from the December 1998 Accounting Framework examination. This was the Foundation stage accounting paper until the new Paper 1.1, Preparing Financial Statements examination came into effect in December 2001.The bookkeeping system of Turner Limited is not computerised, and at 30 September 1998 the bookkeeper was unable to balance the accounts. The trial balance totals were:Debit £1,796,100Credit £1,852,817Nevertheless, he proceeded to prepare draft financial statements, inserting the difference as a balancing figure in the balance sheet. The draft profit and loss account showed a profit of £141,280 for the year ended 30 September 1998.He then opened a suspense account for the difference and began to check through the accounting records to find the difference. He found the following errors and omissions:1. £8,980 – the total of the sales returns book for September 1998, had been credited to the purchasesreturns account.2. £9,600 paid for an item of plant purchased on 1 April 1998 had been debited to plant repairs account.The company depreciates its plant at 20% per annum on a straight line basis, with proportional depreciation in the year of purchase.3. The cash discount totals for the month of September 1998 had not been posted to the nominal ledgeraccounts. The figures were:Discount allowed £836Discount received £9194. £580 insurance prepaid at 30 September 1997 had not been brought down as an opening balance5. The balance of £38,260 on the telephone expense account had been omitted from the trial balance6. A car held as a fixed asset had been sold during the year for £4,800. The proceeds of sale wereentered in the cash book but had been credited to the sales account in the nominal ledger. The original cost of the car £12,000, and the accumulated depreciation to date £8,000, were included in the motor vehicles account and the accumulated depreciation account. The company depreciates motor vehicles at 25% per annum on a straight line basis with proportionate depreciation in the year of purchase but none in the year of sale.Required:a Open a suspense account for the difference between the trial balance totals. Prepare the journal entries necessary to correct the errors and eliminate the balance on the suspense account. Narratives are not required.(10 marks)b Draw up a statement showing the revised profit after correcting the above errors.(6 marks)(16 marks)DiscussionThe approach to the question should be:1 Read the requirement paragraph at the end of the question.2 Attack the question – note that narratives are not required. Begin by opening the suspense account. Which side? More debit is needed to balance the trial balance, so debit the suspense account with £56,717.Then deal with the errors in order:1. Sales returns should have been debited to the sales returns account and they have been credited tothe purchases returns account. There are two errors here – the wrong account has been used and an entry which should have been a debit has been entered as a credit. The suspense account entry must therefore be for 2 x £8,980 or £17,960.2. An error of principle – no suspense account entry. Depreciation must be adjusted.3. Items have not been posted, therefore the suspense account is involved.4. Effectively a posting error – the suspense account is again involved.5. A trial balance error must affect the suspense account – but no ledger entry.6. This one needs thought. Take it one sentence at a time. Is the suspense account involved? No,because we have an error of commission followed by some unrecorded transactions.Attempt Part (a) of the question bef ore studying the answer as detailed in Table 2. Let’s now turn to Part (b). The most convenient format for the answer is two columns for - and +. Set them up and enter the adjustments appropriately. Which of the errors affect the profit? In fact they all do. Attempt Part (b) now before looking at the answer detailed in Table 3.Some hints on preparing suspense accounts∙Does a correction involve the suspense account? The type of error determines this. Practice, and study of Table 1 should ensure that you see immediately which errors affect the balancing of the records and hence the suspense account.∙Which side of the suspense account must an entry go? This is one of the most awkward problems in preparing suspense accounts. The best way of solving it is to ask yourself which side the entry needs to be on in the other account concerned. The suspense account entry is then obviously to the opposite side.∙Look out for errors with two aspects. In the illustrative question earlier, error 1 is a case in point. An entry has been made to the wrong account, but also to the wrong side of the wrong account. Both errors must be corrected. It is very easy to fall into the trap of correcting only one of the errors, especially when working quickly under examination conditions.Neil Stein is Examiner for Paper 1.1。

ACCA F3考试知识点汇总不知道大家的F3考过了没有,如果正打算考的话,下面的F3的考试知识点就能派上用场了。

考验你英语水平的时候到了。

KaplanEmbed your knowledge on the core models from Johnson and Scholes (the examiner based this paper on their work).When answering questions, write answers like you are writing to your senior management. Make it as professional as possible. Marks are allocated to this in section A.Do not start writing answers straightaway. Take a minute to think about the structure and presentation of the answers.It is important with this level to remember that writing lots of knowledge and theory will not get you through the exam. The key is application to the material and expanding the relevance to the scenario.We suggest watching the news / reading the papers, but with a critical eye. For instance when you see that a business has launched a new product or moved into a new market think about the theories you have learnt that may be relevant. In this case it could be:Porter’s generic strategiesAnsoffBowman’s clockThen apply those theories to the real life situation – understand why they have created this product/why they have gone into this market. With practice you will find it easier to apply the theories to the scenario.And of course you can do this for other areas of the syllabus.There is nothing worse for a marker than getting a script which is just a page of writing. Try to think about making your script easier to read for the marker. Headings andSub-headings along with a bit of space will help. Then use your paragraph to explain the point you are making.If it is easy for the marker to see the points being made this can make the difference between pass and fail for a borderline script, include application, plus relevance within your statement, avoid listing.If you use the word ‘and’ in your answer, are you making two separate points? If yes, maybe you need to split your paragraph into two headings / sub-headings.There are 3 professional marks which will constitute professionalism, presentation and layout.Know the theory and apply it.Create mind maps of the key knowledge, then learn these.Do practice questions under timed conditions and if possible, get them marked.Make sure you’ve read all the current examiner articles, available on the ACCA website.Get good business awareness – read a quality newspaper.Use the reading time to select questions, and get frameworks for answer plans.Do a section B question first.Don’t focus on the numbers – do not spend more than 15 minutes on them per question.Watch the clock – allocate your time efficiently –don’t overrun.Layout your answers in a way that the marker can clearly read and understand.Read the question carefully!BppSection A will be a compulsory case study question with several requirements relating to thesame scenario information. The question will usually assess and link several subject areasfrom across the syllabus, and will require the demonstration of high-level capabilities toevaluate, relate and apply the information in the scenario to the question requirements.There is often some financial or numerical data in the scenario and marks will be availablefor numerical analysis which supports your written argument.Section A continues to consume time in reading and absorbing – three pages of text andnumbers are becoming the norm. Thus, students must not underestimate the importance ofpractising these 50 mark questions not only from a knowledge perspective, but, critically,from a time management and “effort” perspective: reading; assimilating; utilising; all taketime and to be effective in these three activities needs practice like anything else. Your prospects can dramatically improve if you follow this advice.Section B questions are more likely to examine discrete subject areas. They will be based onshort scenarios, and you will be expected to apply information from the scenarios to thequestion requirements. Again the questions can be drawn from all areas of the syllabus, andthe limited extent of the choice (two from three) reinforces the importance of covering allareas of the syllabus. It is also highlighting the point that we have seen calculations examined in the optional Section B questions as well as in the compulsory Section A question. This is a trend we expect to continue. A study strategy which includes making timeto revisit the numerical areas of the syllabus to refresh knowledge would be wise.P3 has the following syllabus areas:A Strategic positionB Strategic choicesC Strategic actionD Business and process changeE Information technologyF Project managementG Financial analysisH PeopleTo stand the best chance of passing P3, you need to have a good understanding of the entiresyllabus. This will enable you to choose the questions you believe are the easiest to pick upmarks (for instance because it is easier to understand the requirements, or easier to structure an answer, or easier to pick up knowledge marks) rather than having to choosequestions because of your own restricted knowledge of the syllabus. A review of the examsin the past couple of years reveals that all the key areas of the syllabus have been examined(indeed, sometimes the same topic is examined in consecutive sittings) which, again, showsthe danger of question spotting or ignoring areas.General advice:The P3 exam is 3 hours and 15 minutes long. There is no longer 15 minutes ‘reading andplanning’ time as this has been incorporated into the actual writing time. This has resulted in1.95 minutes of writing time per mark on offer. Ultimately when it comes to using the timein the exam hall it is important that you play to your strengths and use it in a way that worksbest for you.You may prefer to use the first 15 minutes of the exam to plan your answers, alternativelyyou may choose to start the exam immediately and reallocate the 15 minutes previously。

ACCA F3复习梗概Chapter 16 Correction of Errors1. Types of error in accounting2. The correction of errors by journal entries3. The correction of errors by Suspense accounts4. 重要的账务处理(要清楚正确账务处理方法)Discount allowedDiscount receivedChapter 17 Preparation of financial statements for sole traders Trail balance——to prepare Statements1.Receivables——Credit sales2.Payables——Purchases——Cost of sales3.accruals4.prepayments5.坏账准备账务处理(要清楚来龙去脉)计提坏账准备Dr: Irrecoverable debt expenseCr: Allowance for receivables发生坏账损失Dr: Irrecoverable debt expenseAllowance for receivables(前期计提的坏账准备拿出来用,发挥缓冲的作用)Cr: Trade receivables➢计提坏账准备期末达到的状态:应收账款的期末余额与坏账准备的期末余额成比例。

Chapter 18 Incomplete records1.The accounting and business equationsProfit /(loss) = movement in net assets –capital introduced + drawings2.Receivables——Credit sales3. Payables——Credit Purchases4. The cost of the goods stolen(a)(b)5. Two column cash book根据以下流程图回忆应用两栏式现金帐的概况:6.小贴士●Mark-up is the profit as a percentage of cost.●Gross profit margin is the profit as a percentage of sales.Chapter19 Introduction to company accounting1. Share capital●Authorised (or legal) capital●Issued capital●Called-up capital●Paid-up capital2. Preference shares3. Ordinary shares4. Other equity●Share premium●Revaluation surplus●Reserves——Statutory reserves●Retained earnings5. Bonus (capitalization) issues6. Rights issuesChapter 20 Preparation of financial statements for companies1. 通过课本案例P341、P347来回顾相关要点2. Revaluation SurplusThe revaluation is recognized in the other comprehensive income part of the statement of comprehensive income.and then shown as a movement in the revaluation surplus in the statement of changes in equityChapter 21 Events after the reporting period1. 重点关注在何时需要调整,在何时不需要调整Chapter 22 Statement of cash flows1. Direct method2. Indirect methodChapter 23 Introduction to consolidated financial statements1. 合并报表三部曲●Adding together●Cancellation of like items internal to the group (receivables and payables)●Show NCI——了解以下三种处理方法的区别2. Subsidiaries3.Associates: the equity method4. Trade investmentsChapter 24 The consolidated statement of financial position1.Goodwill2. Retained earnings3. Non-controlling interests4. Intra-group trading5. Acquisition of a subsidiary part way through the yearChapter 25 The consolidated statement of Comprehensive Income1.当年利润要在合并方和被合并方之间分配。

ACCA考试知识点总结:F3易混词汇列举ACCA考试科目中,F3阶段的词汇是非常多的。

并且,有些词汇无论是意思还比较的相近。

为了重点区分这些词,中公财经小编在这里就给大家简单列举了以下;owed to vs owed fromowed to后面跟的是债主,是应该收钱的人;owed from后面跟的是欠钱的人;e.g.He owed money to many people;the number was probably in the thousands.Thousands of people were owed money from him.他欠了很多人的钱,他的债主可能有几千人。

due to vs due fromdue to后面跟的是债主,是应该收钱的人;due from后面跟的是欠钱的人;e.g.Have they been paid the money due to them?Have they been paid the money due from others?他们是否已经得到了别人欠他们的钱?F3中的due to还有“因为、由于”的意思,表示要寻找原因。

Du e to some errors,the total amount of the trial balance’s debit side was not equaled to the credit side.mark up on costvsmark up on sales pricee.g.1)A sold goods to B at a price of$10,000.The profit mark-up was 40%on the sales prices.mark up on sales price意味着sales=100%,profit=40%,cost=100%-40%=60%所以sales=10,000,profit=40%*10,000=4,000,cost=60%*10,000=6,0002)A sold goods to B at a price of$10,000.The profit mark-up was 40%on the cost.mark up on cost意味着cost=100%,profit=40%,sales=cost+profit=140%所以sales=10,000,cost=10,000*100%/140%=7143,profit=10,000*40%/140%=2857Invoice vs receiptsInvoice是发票,是卖方用来提醒买方所须付的金额;receipt是收据,也是卖方给买方的。

、编制报表的准备ASSo P*ed IranSaCtioπs (e gτ. invoices)Summarised tθ.g,l nominal Iedger I Uialbalance)Finandal Statem a fits原始凭证交易汇总一一分类记入序时账一一累计入分类账、编试算平衡表日记账The SeVen main books of Prinne entry are;•SaleS Clay book (records Credit sales, i e., IrnVDiCeS Sent)•PUrGhaSe Clay b∞k (records Credit PUrChaSeS H i e.φ invoicesreceived)•Sales returns day book (records I r BIlJr口吕Of purchases made oo Credit I i.e.. Credit notes received)•CaSh book (transactions i∩volving the bank account)•Petty CaSh book (transactions involving Petty C呂Sh)•JeXJrnaISaIeS day bookThe SaleS day book is USed to keep a IiSt Of all invoices Sent OUt to Credit CUStOmerS each day. Here is an example.Date InVOiCe NUmber CUStOmer TOtal AmOUnt InVOiCedDate SUPPlier TOtal AmOUnt InVoiCed PUrChaSe EleCtriCity03.04.20x9 RST Co. $215 S215 10.04.20x9 J ∪M me. $1,804 $1,80415.04.20x9 DDTCo.$758$758$2,777$2,019$758DateCredit NOte CUStOmer TOtal AmOUnt InVOiCedWhere a business has Very few SaIeS returns, it may record a ^redit note as a negative entry in the SaIeS day book.• The CaSh b∞k may be SPlit into a CaSh receipts book and a CaSh Payments b∞k. • The CaSh PaymentS b∞k may have analysis COIUmnS SUCh asCaSh purchases, payable Iedger (i.e.. amounts Paid to Credit suppliers), rent insurance. WageS etc.CaSh receipts are record® as follows, With the total ColUmn analysed into its ComPOnent parts.03.03.20x9 207 208ABC Ca $4,000XYZCo. $1,200$5,20003.03.20x9 CR008 ABC Co.$2,000Date NarratiVe TOtal DiSCOlJntS ReCeiVabteS CaSh C AIloWed Ledger Sale S SUndry03.03.20x9 CaSh SaIe $150 S150ReCeiVable: ABCCo.$1,000 $50 $1,000DiSCOUnt takenS1t150 $50 StOOO S150•Voucher filled in wħen money is taken OUt to Pay expenses・•At any time t VOUCherS + CaSh = Pre-Set Iimit.•At the end Of the Week/month, the Petty CaSh book is filled in from the vouchers. 4•ThQ amount needed to bring the balance back UP to the preset Iimit = money spent.Certain transact!OnS do not U fir in the main books, for example:•Period end adjustments•COrreCtiOn Of errorsThe journal book lists these sundry transactionsPUrChaSe price. InCIUdIng any ImPOrt duties Paid V but excluding any trade (IlSeOUnt and SaIeS taxOaIdInltIaI estimate CJf the costs Of dismantling and removing tħe Item and restoring the Slte On WhlCh It IS IOCatedDireCtiy attributable CoStS σf bringing the asset to WOrkine ConditiOn for ItS Intended use. eg:$50 $15 $10 S5♦ Key POintS Of Part D NCA-The COSt Of Slte PreParatlOn t eg IeVeIhng the floor Of the factory SO the machine Can be InStaIled■ InmaI delivery and handling COStS-InStaIIatiOn and assembly COStS一PrOfeSSIOnal fees (lawyers, architects, engineers)-COStS Of testing wħether tħe asset IS WOCWng properly, after (JedUetIng the net PfoCeedS from SeIllng SamPIeS PfOdUCed wħen testing equipment-Staff CaStS arising directly from the OXIStrUCtiOn Or acquisition Of the asset♦ Key POintS Of ACCrUaI & Payment♦ Key POintS Of Bank ReCOnCiliatiOn□ Bank Statement VS CaSh book• The bank's records are a I mirrOr image Of the CUStOmer S OWrl records, With debits and CreditS reversed• Difference?1. ErrOr (IJSUaIly in the CaSh book) (USIJally adjust the CaSh book)2. Bank ChargeS Or bank interests (adjust the CaSh book)3. Timing CIifference (adjust the bank Staterne nt)UnPreSented CheqUeS (支票付出去了,钱没有从银行划出) OUtStanding IOdgmentS (支票收到了,钱没进银行的账)∣ ByOoB =$150 ORlGINAL DoCUMbNTSInVOCeS A=$100ChCqUoS rPCRvod A = $120iaies day bookB∞KSOF PRIME ENTRYLEDGER ACCOUNTS INoMlNAL LEDGCR)200 300PeCeVabief I^dQ^r (PenOndI QCCOUnhl A B BaklnCC Balance = $20 Cr =$50 DrA D TotalOVeraIl balance ≡ $30Df - ∙ ∙。

ACCA F3知识点:易混淆的坏账、疑账

财经来说说ACCA F3一个易混淆的知识点,坏账&疑账。

Bad/Irrecoverable debts坏账

坏账是指企业无法收回或收回的可能性极小的应收款项。

由于发生坏账而产生的损失,称为坏账损失。

可能发生坏账的情况有以下几种:

Indicators that a debt may become irrecoverable include:

·Taking longer to pay than is usual.

·Paying in instalments outside normal credit terms.

·Regular disputing of invoices (as a delaying tactic).

·Going into receivership (administration)/liquidation.

当顾客没有能力支付时,就没必要一直保留的这笔账目,相关会计处理如下:

When a business is owed money by a customer who is unable to pay, there is little point keeping the customer's account in the business' books.

·If the debt is not an asset, then it should not be carried in the statement of financial position.·To give a fair presentation in the accounts, irrecoverable debts are written out of the books and expensed to profit or loss, thereby reducing profit (or increasing a loss).

·The double entry to record the write-off is:

Dr Irrecoverable debt expense a/c$x

Cr Trade receivable a/c$x

Doubtful Debts疑账

疑账是指对其内容或清偿能力有怀疑的账户,它有可能变成坏账,但目前还不是坏账。

Eventually, a firm may have to admit defeat and write off the account receivable.

It is unnecessary to match the write-off with the allowance made.

Simply:

Dr Irrecoverable debt expense a/c$x

Cr Trade receivable a/c$x

(i.e. as for any irrecoverable debt)

The debit for irrecoverable debt expense does not result in a double charge to profit or loss. The specific allowance previously made is no longer required and will be set off against the write-off when the movement on the allowance is transferred to the irrecoverable debt expense a/c.

坏账与疑账的区别。