Investment-cashflowsensitivitycannotbeagoodmeasureof

- 格式:pdf

- 大小:1.30 MB

- 文档页数:18

CHAPTER 8Making Capital Investment Decisions I. DEFINITIONSINCREMENTAL CASH FLOWSa 1. The changes in a firm’s future cash flows that are a direct consequence of accepting aproject are called _____ cash flows.a. incrementalb. stand-alonec. after-taxd. net present valuee. erosionDifficulty level: EasyEQUIVALENT ANNUAL COSTe 2. The annual annuity stream of payments with the same present value as a project’s costsis called the project’s _____ cost.a. incrementalb. sunkc. opportunityd. erosione. equivalent annualDifficulty level: EasySUNK COSTSc 3. A cost that has already been paid, or the liability to pay has already been incurred, isa(n):a. salvage value expense.b. net working capital expense.c. sunk cost.d. opportunity cost.e. erosion cost.Difficulty level: EasyOPPORTUNITY COSTSd 4. The most valuable investment given up if an alternative investment is chosen is a(n):a. salvage value expense.b. net working capital expense.c. sunk cost.d. opportunity cost.e. erosion cost.Difficulty level: EasyEROSION COSTSe 5. The cash flows of a new project that come at the expense of a firm’s existing projectsare called:a. salvage value expenses.b. net working capital expenses.c. sunk costs.d. opportunity costs.e. erosion costs.Difficulty level: EasyPRO FORMA FINANCIAL STATEMENTSa 6. A pro forma financial statement is one that:a. projects future years’ operations.b. is expressed as a percentage of the total assets of the firm.c. is expressed as a percentage of the total sales of the firm.d. is expressed relative to a chosen base year’s financial statement.e. reflects the past and current operations of the firm.Difficulty level: EasyMACRS DEPRECIATIONb 7. The depreciation method currently allowed under US tax law governing the acceleratedwrite-off of property under various lifetime classifications is called _____ depreciation.a. FIFOb. MACRSc. straight-lined. sum-of-years digitse. curvilinearDifficulty level: EasyDEPRECIATION TAX SHIELDc 8. The cash flow tax savings generated as a result of a firm’s tax-deductible depreciationexpense is called the:a. after-tax depreciation savings.b. depreciable basis.c. depreciation tax shield.d. operating cash flow.e. after-tax salvage value.Difficulty level: EasyCASH FLOWd 9. The cash flow from projects for a company is computed as the:a. net operating cash flow generated by the project, less any sunk costs and erosion costs.b. sum of the incremental operating cash flow and after-tax salvage value of the project.c. net income generated by the project, plus the annual depreciation expense.d. sum of the incremental operating cash flow, capital spending, and net working capitalexpenses incurred by the project.e. sum of the sunk costs, opportunity costs, and erosion costs of the project.Difficulty level: MediumII. CONCEPTSPRO FORMA INCOME STATEMENTb 10. The pro forma income statement for a cost reduction project:a. will reflect a reduction in the sales of the firm.b. will generally reflect no incremental sales.c. has to be prepared reflecting the total sales and expenses of a firm.d. cannot be prepared due to the lack of any project related sales.e. will always reflect a negative project operating cash flow.Difficulty level: EasyINCREMENTAL CASH FLOWb 11. One purpose of identifying all of the incremental cash flows related to a proposedproject is to:a. isolate the total sunk costs so they can be evaluated to determine if the project willadd value to the firm.b. eliminate any cost which has previously been incurred so that it can be omitted fromthe analysis of the project.c. make each project appear as profitable as possible for the firm.d. include both the proposed and the current operations of a firm in the analysis of theproject.e. identify any and all changes in the cash flows of the firm for the past year so they canbe included in the analysis.Difficulty level: MediumINCREMENTAL CASH FLOWe 12. Which of the following are examples of an incremental cash flow?I. an increase in accounts receivableII. a decrease in net working capitalIII. an increase in taxesIV. a decrease in the cost of goods solda. I and III onlyb. III and IV onlyc. I and IV onlyd. I, III, and IV onlye. I, II, III, and IVDifficulty level: MediumINCREMENTAL CASH FLOWc 13. Which one of the following is an example of an incremental cash flow?a. the annual salary of the company president which is a contractual obligationb. the rent on a warehouse which is currently being utilizedc. the rent on some new machinery that is required for an upcoming projectd. the property taxes on the currently owned warehouse which has been sitting idle butis going to be utilized for a new projecte. the insurance on a company-owned building which will be utilized for a new projectDifficulty level: MediumINCREMENTAL COSTSd 14. Project analysis is focused on _____ costs.a. sunkb. totalc. variabled. incrementale. fixedDifficulty level: MediumSUNK COSTc 15. Sunk costs include any cost that:a. will change if a project is undertaken.b. will be incurred if a project is accepted.c. has previously been incurred and cannot be changed.d. is paid to a third party and cannot be refunded for any reason whatsoever.e. will occur if a project is accepted and once incurred, cannot be recouped.Difficulty level: EasySUNK COSTd 16. You spent $500 last week fixing the transmission in your car. Now, the brakes areacting up and you are trying to decide whether to fix them or trade the car in for anewer model. In analyzing the brake situation, the $500 you spent fixing thetransmission is a(n) _____ cost.a. opportunityb. fixedc. incrementald. sunke. relevantDifficulty level: EasyEROSIONb 17. Erosion can be explained as the:a. additional income generated from the sales of a newly added product.b. loss of current sales due to a new project being implemented.c. loss of revenue due to employee theft.d. loss of revenue due to customer theft.e. loss of cash due to the expenses required to fix a parking lot after a heavy rain storm.Difficulty level: EasyEROSIONa 18. Which of the following are examples of erosion?I. the loss of sales due to increased competition in the product marketII. the loss of sales because your chief competitor just opened a store across the street from your storeIII. the loss of sales due to a new product which you recently introducedIV. the loss of sales due to a new product recently introduced by your competitora. III onlyb. III and IV onlyc. I, III and IV onlyd. II and IV onlye. I, II, III, and IVDifficulty level: MediumTYPES OF COSTSd 19. Which of the following should be included in the analysis of a project?I. sunk costsII. opportunity costsIII. erosion costsIV. incremental costsa. I and II onlyb. III and IV onlyc. II and IV onlyd. II, III, and IV onlye. I, II, and IV onlyDifficulty level: MediumNET WORKING CAPITALd 20. All of the following are anticipated effects of a proposed project. Which of theseshould be included in the initial project cash flow related to net working capital?I. an inventory decrease of $5,000II. an increase in accounts receivable of $1,500III. an increase in fixed assets of $7,600IV. a decrease in accounts payable of $2,100a. I and II onlyb. I and III onlyc. II and IV onlyd. I, II, and IV onlye. I, II, III, and IVDifficulty level: MediumNET WORKING CAPITALa 21. Changes in the net working capital:a. can affect the cash flows of a project every year of the project’s life.b. only affect the initial cash flows of a project.c. are included in project analysis only if they represent cash outflows.d. are generally excluded from project analysis due to their irrelevance to the totalproject.e. affect the initial and the final cash flows of a project but not the cash flows of themiddle years.Difficulty level: MediumNET WORKING CAPITALc 22. Which one of the following will decrease net working capital of a firm?a. a decrease in accounts payableb. an increase in inventoryc. a decrease in accounts receivabled. an increase in the firm’s checking account balancee. a decrease in fixed assetsDifficulty level: EasyNET WORKING CAPITALd 23. Net working capital:a. can be ignored in project analysis because any expenditure is normally recouped by theend of the project.b. requirements generally, but not always, create a cash inflow at the beginning of aproject.c. expenditures commonly occur at the end of a project.d. is frequently affected by the additional sales generated by a new project.e. is the only expenditure where at least a partial recovery can be made at the end of aproject.Difficulty level: EasyMACRSd 24. A company which uses the MACRS system of depreciation:a. will have equal depreciation costs each year of an asset’s life.b. will expense the cost of nonresidential real estate over a period of 7 years.c. can depreciate the cost of land, if they so desire.d. will write off the entire cost of an asset over the asset’s class life.e. cannot expense any of the cost of a new asset during the first year of the asset’s life.Difficulty level: EasyMACRSa 25. Bet ‘r Bilt Toys just purchased some MACRS 5-year property at a cost of $230,000.Which of the following will correctly give you the book value of this equipment at theend of year 2?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%I. 52% of the asset costII. 48% of the asset costIII. 68% of 80% of the asset costIV. the asset cost, minus 20% of the asset cost, minus 32% of 80% of the asset costa. II onlyb. III and IV onlyc. I and III onlyd. II and IV onlye. I, II, III, and IVDifficulty level: EasyMACRSe 26. Will Do, Inc. just purchased some equipment at a cost of $650,000. What is theproper methodology for computing the depreciation expense for year 3 if theequipment is classified as 5-year property for MACRS?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $650,000 ⨯ (1-.20) ⨯ (1-.32) ⨯ (1-.192)b. $650,000 ⨯ (1-.20) ⨯ (1-.32)c. $650,000 ⨯ (1+.20) ⨯ (1+.32) ⨯ (1+.192)d. $650,000 ⨯ (1-.192)e. $650,000 ⨯ .192Difficulty level: MediumBOOK VALUEd 27. The book value of an asset is primarily used to compute the:a. annual depreciation tax shield.b. amount of cash received from the sale of an asset.c. amount of tax saved annually due to the depreciation expense.d. amount of tax due on the sale of an asset.e. change in depreciation needed to reflect the market value of the asset.Difficulty level: EasySALVAGE VALUEc 28. The salvage value of an asset creates an after-tax cash inflow to the firm in an amountequal to the:a. sales price of the asset.b. sales price minus the book value.c. sales price minus the tax due based on the sales price minus the book value.d. sales price plus the tax due based on the sales price minus the book value.e. sales price plus the tax due based on the book value minus the sales price.Difficulty level: EasySALVAGE VALUEe 29. The pre-tax salvage value of an asset is equal to the:a. book value if straight-line depreciation is used.b. book value if MACRS depreciation is used.c. market value minus the book value.d. book value minus the market value.e. market value.Difficulty level: EasyPROJECT OCFa 30. A project’s operating cash flow will increase when:a. the depreciation expense increases.b. the sales projections are lowered.c. the interest expense is lowered.d. the net working capital requirement increases.e. the earnings before interest and taxes decreases.Difficulty level: EasyPROJECT CASH FLOWSc 31. The cash flows of a project should:a. be computed on a pre-tax basis.b. include all sunk costs and opportunity costs.c. include all incremental costs, including opportunity costs.d. be applied to the year when the related expense or income is recognized by GAAP.e. include all financing costs related to new debt acquired to finance the project.Difficulty level: EasyPROJECT OCFa 32. Which of the following are correct methods for computing the operating cash flow ofa project assuming that the interest expense is equal to zero?I. EBIT + Depreciation - TaxesII. EBIT + Depreciation + TaxesIII. Net Income + DepreciationIV. (Sales – Costs) ⨯ (Taxes + Depreciation) ⨯ (1-Taxes)a. I and III onlyb. II and IV onlyc. II and III onlyd. I, III, and IV onlye. II, III, and IV onlyDifficulty level: MediumBOTTOM-UP OCFb 33. The bottom-up approach to computing the operating cash flow applies only when:a. both the depreciation expense and the interest expense are equal to zero.b. the interest expense is equal to zero.c. the project is a cost-cutting project.d. no fixed assets are required for the project.e. taxes are ignored and the interest expense is equal to zero.Difficulty level: MediumTOP-DOWN OCFa 34. The top-down approach to computing the operating cash flow:a. ignores all noncash items.b. applies only if a project produces sales.c. can only be used if the entire cash flows of a firm are included.d. is equal to sales - costs - taxes + depreciation.e. includes the interest expense related to a project.Difficulty level: MediumTAX SHIELDd 35. An increase in which one of the following will increase the operating cash flow?a. employee salariesb. office rentc. building maintenanced. equipment depreciatione. equipment rentalDifficulty level: EasyTAX SHIELDc 36. Tax shield refers to a reduction in taxes created by:a. a reduction in sales.b. an increase in interest expense.c. noncash expenses.d. a project’s incremental expenses.e. opportunity costs.Difficulty level: EasyCOST-CUTTINGc 37. A project which is designed to improve the manufacturing efficiency of a firm but willgenerate no additional sales is referred to as a(n) _____ project.a. sunk costb. opportunityc. cost-cuttingd. revenue-cuttinge. revenue-generatingDifficulty level: EasyEQUIVALENT ANNUAL COSTc 38. Toni’s Tools is comparing machines to determine which one to purchase. Themachines sell for differing prices, have differing operating costs, differing machinelives, and will be replaced when worn out. These machines should be compared using:a. net present value only.b. both net present value and the internal rate of return.c. their effective annual costs.d. the depreciation tax shield approach.e. the replacement parts approach.Difficulty level: MediumEQUIVALENT ANNUAL COSTe 39. The equivalent annual cost method is useful in determining:a. the annual operating cost of a machine if the annual maintenance is performed versuswhen the maintenance is not performed as recommended.b. the tax shield benefits of depreciation given the purchase of new assets for a project.c. operating cash flows for cost-cutting projects of equal duration.d. which one of two machines to acquire given equal machine lives but unequal machinecosts.e. which one of two machines to purchase when the machines are mutually exclusive,have different machine lives, and will be replaced once they are worn out.Difficulty level: MediumIII. PROBLEMSRELEVANT CASH FLOWSd 40. Marshall’s & Co. purchased a corner lot in Eglon City five y ears ago at a cost of$640,000. The lot was recently appraised at $810,000. At the time of the purchase, thecompany spent $50,000 to grade the lot and another $4,000 to build a small buildingon the lot to house a parking lot attendant who has overseen the use of the lot for dailycommuter parking. The company now wants to build a new retail store on the site. Thebuilding cost is estimated at $1.2 million. What amount should be used as the initialcash flow for this building project?a. $1,200,000b. $1,840,000c. $1,890,000d. $2,010,000e. $2,060,000Difficulty level: MediumRELEVANT CASH FLOWSe 41. Jamestown Ltd. currently produces boat sails and is considering expanding itsoperations to include awnings for homes and travel trailers. The company owns landbeside its current manufacturing facility that could be used for the expansion. Thecompany bought this land ten years ago at a cost of $250,000. Today, the land isvalued at $425,000. The grading and excavation work necessary to build on the landwill cost $15,000. The company currently has some unused equipment which itcurrently owns valued at $60,000. This equipment could be used for producingawnings if $5,000 is spent for equipment modifications. Other equipment costing$780,000 will also be required. What is the amount of the initial cash flow for thisexpansion project?a. $800,000b. $1,050,000c. $1,110,000d. $1,225,000e. $1,285,000Difficulty level: MediumRELEVANT CASH FLOWSb 42. Wilbert’s, Inc. paid $90,000, in cash, for a piece of equipment three years ago. Lastyear, the company spent $10,000 to update the equipment with the latest technology.The company no longer uses this equipment in their current operations and hasreceived an offer of $50,000 from a firm who would like to purchase it. Wilbert’s isdebating whether to sell the equipment or to expand their operations such that theequipment can be used. When evaluating the expansion option, what value, if any,should Wilbert’s assign to this equipment as an initial cost of the project?a. $40,000b. $50,000c. $60,000d. $80,000e. $90,000Difficulty level: EasyRELEVANT CASH FLOWSa 43. Walks Softly, Inc. sells customized shoes. Currently, they sell 10,000 pairs of shoesannually at an average price of $68 a pair. They are considering adding a lower-pricedline of shoes which sell for $49 a pair. Walks Softly estimates they can sell 5,000 pairsof the lower-priced shoes but will sell 1,000 less pairs of the higher-priced shoes bydoing so. What is the amount of the sales that should be used when evaluating theaddition of the lower-priced shoes?a. $177,000b. $245,000c. $313,000d. $789,000e. $857,000Difficulty level: MediumOPPORTUNITY COSTc 44. Your firm purchased a warehouse for $335,000 six years ago. Four years ago, repairswere made to the building which cost $60,000. The annual taxes on the property are$20,000. The warehouse has a current book value of $268,000 and a market value of$295,000. The warehouse is totally paid for and solely owned by your firm. If thecompany decides to assign this warehouse to a new project, what value, if any, shouldbe included in the initial cash flow of the project for this building?a. $0b. $268,000c. $295,000d. $395,000e. $515,000Difficulty level: EasyOPPORTUNITY COSTd 45. You own a house that you rent for $1,200 a month. The maintenance expenses onthe house average $200 a month. The house cost $89,000 when you purchased itseveral years ago. A recent appraisal on the house valued it at $210,000. The annualproperty taxes are $5,000. If you sell the house you will incur $20,000 in expenses.You are deciding whether to sell the house or convert it for your own use as aprofessional office. What value should you place on this house when analyzing theoption of using it as a professional office?a. $89,000b. $120,000c. $185,000d. $190,000e. $210,000Difficulty level: MediumOPPORTUNITY COSTc 46. Big Joe’s owns a manufacturing facility that is currently sitting idle. The facility islocated on a piece of land that originally cost $129,000. The facility itself cost$650,000 to build. As of now, the book value of the land and the facility are $129,000and $186,500, respectively. Big Joe’s received an offer of $590,000 for the land andfacility last week. They rejected this offer even though they were told that it is areasonable offer in today’s market. If Big Joe’s were to consider using this land andfacility in a new project, what cost, if any, should they include in the project analysis?a. $0b. $315,500c. $590,000d. $650,000e. $779,000Difficulty level: EasyEROSION COSTb 47. Jamie’s Motor Home Sales currently sells 1,000 Class A motor homes, 2,500 Class Cmotor homes, and 4,000 pop-up trailers each year. Jamie is considering adding a mid-range camper and expects that if she does so she can sell 1,500 of them. However, ifthe new camper is added, Jamie expects that her Class A sales will decline to 950 unitswhile the Class C campers decline to 2,200. The sales of pop-ups will not be affected.Class A motor homes sell for an average of $125,000 each. Class C homes are pricedat $39,500 and the pop-ups sell for $5,000 each. The new mid-range camper will sellfor $47,900. What is the erosion cost?a. $6,250,000b. $18,100,000c. $53,750,000d. $93,150,000e. $118,789,500Difficulty level: MediumOCFe 48. Ernie’s E lectrical is evaluating a project which will increase sales by $50,000 andcosts by $30,000. The project will cost $150,000 and be depreciated straight-line to azero book value over the 10 year life of the project. The applicable tax rate is 34%.What is the operating cash flow for this project?a. $3,300b. $5,000c. $8,300d. $13,300e. $18,300Difficulty level: MediumOCFd 49. Kurt’s Kabinets is looking at a project that will require $80,000 in fixed assets andanother $20,000 in net working capital. The project is expected to produce sales of$110,000 with associated costs of $70,000. The project has a 4-year life. The companyuses straight-line depreciation to a zero book value over the life of the project. The taxrate is 35%. What is the operating cash flow for this project?a. $7,000b. $13,000c. $27,000d. $33,000e. $40,000Difficulty level: MediumBOTTOM-UP OCFc 50. Peter’s Boats has sales of $760,000 and a profit margin of 5%. The annualdepreciation expense is $80,000. What is the amount of the operating cash flow if thecompany has no long-term debt?a. $34,000b. $86,400c. $118,000d. $120,400e. $123,900Difficulty level: MediumBOTTOM-UP OCFd 51. Le Place has sales of $439,000, depreciation of $32,000, and net working capital of$56,000. The firm has a tax rate of 34% and a profit margin of 6%. Thefirm has no interest expense. What is the amount of the operating cash flow?a. $49,384b. $52,616c. $54,980d. $58,340e. $114,340Difficulty level: MediumTOP-DOWN OCFb 52. Ben’s Border Café is considering a project which will produce sales of $16,000 andincrease cash expenses by $10,000. If the project is implemented, taxes will increasefrom $23,000 to $24,500 and depreciation will increase from $4,000 to $5,500. Whatis the amount of the operating cash flow using the top-down approach?a. $4,000b. $4,500c. $6,000d. $7,500e. $8,500Difficulty level: MediumTOP-DOWN OCFc 53. Ronnie’s Coffee House i s considering a project which will produce sales of $6,000and increase cash expenses by $2,500. If the project is implemented, taxes willincrease by $1,300. The additional depreciation expense will be $1,000. An initial cashoutlay of $2,000 is required for net working capital. What is the amount of theoperating cash flow using the top-down approach?a. $200b. $1,500c. $2,200d. $3,500e. $4,200Difficulty level: MediumTAX SHIELD OCFc 54. A project will increase sales by $60,000 and cash expenses by $51,000. The projectwill cost $40,000 and be depreciated using straight-line depreciation to a zero bookvalue over the 4-year life of the project. The company has a marginal tax rate of 35%.What is the operating cash flow of the project using the tax shield approach?a. $5,850b. $8,650c. $9,350d. $9,700e. $10,350Difficulty level: MediumDEPRECIATION TAX SHIELDa 55. A project will increase sales by $140,000 and cash expenses by $95,000. The projectwill cost $100,000 and be depreciated using the straight-line method to a zero bookvalue over the 4-year life of the project. The company has a marginal tax rate of 34%.What is the value of the depreciation tax shield?a. $8,500b. $17,000c. $22,500d. $25,000e. $37,750Difficulty level: MediumMACRS DEPRECIATIONd 56. Sun Lee’s Furniture just purchased some fixed assets classified as 5-year property forMACRS. The assets cost $24,000. What is the amount of the depreciation expense forthe third year?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $2,304b. $2,507c. $2,765d. $4,608e. $4,800Difficulty level: EasyMACRS DEPRECIATIONa 57. You just purchased some equipment that is classified as 5-year property for MACRS.The equipment cost $67,600. What will the book value of this equipment be at the endof three years should you decide to resell the equipment at that point in time?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $19,468.80b. $20,280.20c. $27,040.00d. $48,131.20e. $48,672.00Difficulty level: MediumMACRS DEPRECIATIONd 58. LiCheng’s Enterprises just purchased some fixed assets that are classified as 3-yearproperty for MACRS. The assets cost $1,900. What is the amount of thedepreciation expense for year 2?MACRS 3-year propertyYear Rate1 33.33%2 44.44%3 14.82%4 7.41%a. $562.93b. $633.27c. $719.67d. $844.36e. $1,477.63Difficulty level: MediumMACRS DEPRECIATIONb 59. RP&A, Inc. purchased some fixed assets four years ago at a cost of $19,800. They nolonger need these assets so are going to sell them today at a price of $3,500. The assetsare classified as 5-year property for MACRS. What is the current book value of theseassets?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $1,140.48b. $3,421.44c. $3,500.00d. $4,016.67e. $5,702.40Difficulty level: MediumSALVAGE VALUEa 60. You own some equipment which you purchased three years ago at a cost of $135,000.The equipment is 5-year property for MACRS. You are considering selling theequipment today for $82,500. Which one of the following statements is correct if yourtax rate is 34%?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. The tax due on the sale is $14,830.80.b. The book value today is $8,478.c. The book value today is $64,320.d. The taxable amount on the sale is $38,880.e. You will receive a tax refund of $13,219.20 as a result of this sale.。

Multiple Choice Questions1. The duration of a bond is a function of the bond'sA) coupon rate.B) yield to maturity.C) time to maturity.D) all of the above.E) none of the above.Answer: D Difficulty: EasyRationale: Duration is calculated by discounting the bond's cash flows at the bond's yield to maturity and, except for zero-coupon bonds, is always less than time to maturity.2. Ceteris paribus, the duration of a bond is positively correlated with thebond'sA) time to maturity.B) coupon rate.C) yield to maturity.D) all of the above.E) none of the above.Answer: A Difficulty: ModerateRationale: Duration is negatively correlated with coupon rate and yield to maturity.3. Holding other factors constant, the interest-rate risk of a coupon bondis higher when the bond's:A) term-to-maturity is lower.B) coupon rate is higher.C) yield to maturity is lower.D) current yield is higher.E) none of the above.Answer: C Difficulty: ModerateRationale: The longer the maturity, the greater the interest-rate risk. The lower the coupon rate, the greater the interest-rate risk. The lower the yield to maturity, the greater the interest-rate risk. These concepts are reflected in the duration rules; duration is a measure of bond price sensitivity to interest rate changes (interest-rate risk).4. The "modified duration" used by practitioners is equal to the MacaulaydurationA) times the change in interest rate.B) times (one plus the bond's yield to maturity).C) divided by (one minus the bond's yield to maturity).D) divided by (one plus the bond's yield to maturity).E) none of the above.Answer: D Difficulty: ModerateRationale: D* = D/(1 + y)5. Given the time to maturity, the duration of a zero-coupon bond is higherwhen the discount rate isA) higher.B) lower.C) equal to the risk free rate.D) The bond's duration is independent of the discount rate.E) none of the above.Answer: D Difficulty: ModerateRationale: The duration of a zero-coupon bond is equal to the maturity of the bond.6. The interest-rate risk of a bond isA) the risk related to the possibility of bankruptcy of the bond's issuer.B) the risk that arises from the uncertainty of the bond's return causedby changes in interest rates.C) the unsystematic risk caused by factors unique in the bond.D) A and B above.E) A, B, and C above.Answer: B Difficulty: ModerateRationale: Changing interest rates change the bond's return, both in terms of the price of the bond and the reinvestment of coupon payments.7. Which of the following two bonds is more price sensitive to changes ininterest rates1) A par value bond, X, with a 5-year-to-maturity and a 10% coupon rate.2) A zero-coupon bond, Y, with a 5-year-to-maturity and a 10%yield-to-maturity.A) Bond X because of the higher yield to maturity.B) Bond X because of the longer time to maturity.C) Bond Y because of the longer duration.D) Both have the same sensitivity because both have the same yield tomaturity.E) None of the aboveAnswer: C Difficulty: ModerateRationale: Duration is the best measure of bond price sensitivity; the longer the duration the higher the price sensitivity.8. Holding other factors constant, which one of the following bonds has thesmallest price volatilityA) 5-year, 0% coupon bondB) 5-year, 12% coupon bondC) 5 year, 14% coupon bondD) 5-year, 10% coupon bondE) Cannot tell from the information given.Answer: C Difficulty: ModerateRationale: Duration (and thus price volatility) is lower when the coupon rates are higher.9. Which of the following is not trueA) Holding other things constant, the duration of a bond increases withtime to maturity.B) Given time to maturity, the duration of a zero-coupon decreases withyield to maturity.C) Given time to maturity and yield to maturity, the duration of a bondis higher when the coupon rate is lower.D) Duration is a better measure of price sensitivity to interest ratechanges than is time to maturity.E) All of the above.Answer: B Difficulty: ModerateRationale: The duration of a zero-coupon bond is equal to time to maturity, and is independent of yield to maturity.10. The duration of a 5-year zero-coupon bond isA) smaller than 5.B) larger than 5.C) equal to 5.D) equal to that of a 5-year 10% coupon bond.E) none of the above.Answer: C Difficulty: EasyRationale: Duration of a zero-coupon bond equals the bond's maturity.11. The basic purpose of immunization is toA) eliminate default risk.B) produce a zero net interest-rate risk.C) offset price and reinvestment risk.D) A and B.E) B and C.Answer: E Difficulty: ModerateRationale: When a portfolio is immunized, price risk and reinvestment risk exactly offset each other resulting in zero net interest-rate risk.12. The duration of a par value bond with a coupon rate of 8% and a remainingtime to maturity of 5 years isA) 5 years.B) years.C) years.D) years.E) none of the above.Answer: D Difficulty: Moderate Rationale:Calculations are shown below.Yr.CF PV of CF@08%Weight * Yr.1$80$80/ = $ * 1 =2$80$80/2 = $ * 2 =3$80$80/3 = $ * 3 =4$80$80/4 = $ * 4 =5$1,080$1,080/5 = $ * 5 =Sum$ yrs. (duration)13. The duration of a perpetuity with a yield of 8% isA) years.B) years.C) years.D) cannot be determined.E) none of the above.Answer: A Difficulty: EasyRationale: D = = years.14. A seven-year par value bond has a coupon rate of 9% and a modified durationofA) 7 years.B) years.C) years.D) years.E) none of the above.Answer: C Difficulty: DifficultRationale:Calculations are shown below.Yr.CF PV of CF@9%Weight * Yr.1$90$ X 1 =2$90$ X 2 =3$90$ X 3 =4$90$ X 4 =5$90$ X 5 =6$90$ X 6 =7$1,090$ X 7 =Sum$ years (duration)modified duration = years/ = years.15. Par value bond XYZ has a modified duration of 6. Which one of the followingstatements regarding the bond is trueA) If the market yield increases by 1% the bond's price will decrease by$60.B) If the market yield increases by 1% the bond's price will increase by$50.C) If the market yield increases by 1% the bond's price will decrease by$50.D) If the market yield increases by 1% the bond's price will increase by$60.E) None of the above.Answer: A Difficulty: ModerateRationale: = -D*-$60 = -6 X $1,00016. Which of the following bonds has the longest durationA) An 8-year maturity, 0% coupon bond.B) An 8-year maturity, 5% coupon bond.C) A 10-year maturity, 5% coupon bond.D) A 10-year maturity, 0% coupon bond.E) Cannot tell from the information given.Answer: D Difficulty: ModerateRationale: The longer the maturity and the lower the coupon, the greater the duration17. Which one of the following par value 12% coupon bonds experiences a pricechange of $23 when the market yield changes by 50 basis pointsA) The bond with a duration of 6 years.B) The bond with a duration of 5 years.C) The bond with a duration of years.D) The bond with a duration of years.E) None of the above.Answer: D Difficulty: DifficultRationale: DP/P = -D X [D(1+y) / (1+y)]; = -D X [.005 / ]; D = .18. Which one of the following statements is true concerning the duration ofa perpetuityA) The duration of 15% yield perpetuity that pays $100 annually is longerthan that of a 15% yield perpetuity that pays $200 annually.B) The duration of a 15% yield perpetuity that pays $100 annually isshorter than that of a 15% yield perpetuity that pays $200 annually.C) The duration of a 15% yield perpetuity that pays $100 annually is equalto that of 15% yield perpetuity that pays $200 annually.D) the duration of a perpetuity cannot be calculated.E) None of the above.Answer: C Difficulty: EasyRationale: Duration of a perpetuity = (1 + y)/y; thus, the duration of a perpetuity is determined by the yield and is independent of the cash flow.19. The two components of interest-rate risk areA) price risk and default risk.B) reinvestment risk and systematic risk.C) call risk and price risk.D) price risk and reinvestment risk.E) none of the above.Answer: D Difficulty: EasyRationale: Default, systematic, and call risks are not part of interest-rate risk. Only price and reinvestment risks are part of interest-rate risk.20. The duration of a coupon bondA) does not change after the bond is issued.B) can accurately predict the price change of the bond for any interestrate change.C) will decrease as the yield to maturity decreases.D) all of the above are true.E) none of the above is true.Answer: E Difficulty: EasyRationale: Duration changes as interest rates and time to maturity change, can only predict price changes accurately for small interest rate changes, and increases as the yield to maturity decreases.21. Indexing of bond portfolios is difficult becauseA) the number of bonds included in the major indexes is so large that itwould be difficult to purchase them in the proper proportions.B) many bonds are thinly traded so it is difficult to purchase them ata fair market price.C) the composition of bond indexes is constantly changing.D) all of the above are true.E) both A and B are true.Answer: D Difficulty: ModerateRationale: All of the above are true statements about bond indexes.22. You have an obligation to pay $1,488 in four years and 2 months. In whichbond would you invest your $1,000 to accumulate this amount, with relative certainty, even if the yield on the bond declines to % immediately after you purchase the bondA) a 6-year; 10% coupon par value bondB) a 5-year; 10% coupon par value bondC) a 5-year; zero-coupon bondD) a 4-year; 10% coupon par value bondE) none of the aboveAnswer: B Difficulty: DifficultRationale: When duration = horizon date, one is immunized, or protected, against one interest rate change. The zero has D = 5. Since the other bonds have the same coupon and yield, solve for the closest value of T that gives D = years. = )/.10 - [ + T(.] / = ; .68 T - .68 + .68 = ; .68 T = ; T = ; T [ln ] = ln ; T = years, so choose the 5-year 10% coupon bond.23. Duration measuresA) weighted average time until a bond's half-life.B) weighted average time until cash flow payment.C) the time required to recoup one's investment, assuming the bond waspurchased for $1,000.D) A and C.E) B and C.Answer: E Difficulty: ModerateRationale: B and C are true, as one receives coupon payments throughout the life of the bond (for coupon bonds); thus, duration is less than time to maturity (except for zeros).24. DurationA) assesses the time element of bonds in terms of both coupon and termto maturity.B) allows structuring a portfolio to avoid interest-rate risk.C) is a direct comparison between bond issues with different levels ofrisk.D) A and B.E) A and C.Answer: D Difficulty: ModerateRationale: Duration is a weighted average of when the cash flows of a bond are received; thus both coupon and time to maturity are considered. If the duration of the portfolio equals the investor's horizon date, the investor is protected against interest rate changes.25. Identify the bond that has the longest duration (no calculationsnecessary).A) 20-year maturity with an 8% coupon.B) 20-year maturity with a 12% coupon.C) 15-year maturity with a 0% coupon.D) 10-year maturity with a 15% coupon.E) 12-year maturity with a 12% coupon.Answer: C Difficulty: ModerateRationale: The lower the coupon, the longer the duration. The zero-coupon bond is the ultimate low coupon bond, and thus would have the longest duration.26. When interest rates decline, the duration of a 10-year bond selling ata premiumA) increases.B) decreases.C) remains the same.D) increases at first, then declines.E) decreases at first, then increases.Answer: A Difficulty: ModerateRationale: The relationship between interest rates and duration is an inverse one.27. An 8%, 30-year corporate bond was recently being priced to yield 10%. TheMacaulay duration for the bond is years. Given this information, the bond's modified duration would be________.A)B)C)D)E) none of the aboveAnswer: C Difficulty: EasyRationale: D* = D/(1 + y); D* = =28. An 8%, 15-year bond has a yield to maturity of 10% and duration of years.If the market yield changes by 25 basis points, how much change will there be in the bond's priceA) %B) %C) %D) %E) none of the aboveAnswer: A Difficulty: ModerateRationale: ΔP/P = X / = %29. One way that banks can reduce the duration of their asset portfolios isthrough the use ofA) fixed rate mortgages.B) adjustable rate mortgages.C) certificates of deposit.D) short-term borrowing.E) none of the above.Answer: B Difficulty: EasyRationale: One of the gap management strategies practiced by banks is the issuance of adjustable rate mortgages, which reduce the interest rate sensitivity of their asset portfolios.30. The duration of a bond normally increases with an increase inA) term to maturity.B) yield to maturity.C) coupon rate.D) all of the above.E) none of the above.Answer: A Difficulty: ModerateRationale: The relationship between duration and term to maturity is a direct one; the relationship between duration and yield to maturity and to coupon rate is negative.31. Which one of the following is an incorrect statement concerning durationA) The higher the yield to maturity, the greater the durationB) The higher the coupon, the shorter the duration.C) The difference in duration is small between two bonds with differentcoupons each maturing in more than 15 years.D) The duration is the same as term to maturity only in the case ofzero-coupon bonds.E) All of the statements are correct.Answer: A Difficulty: ModerateRationale: The relationship between duration and yield to maturity is an inverse one; as is the relationship between duration and coupon rate. The difference in the durations of longer-term bonds of varying coupons (high coupon vs. zero) is considerable. Duration equals term to maturity only with zeros.32. Immunization is not a strictly passive strategy becauseA) it requires choosing an asset portfolio that matches an index.B) there is likely to be a gap between the values of assets and liabilitiesin most portfolios.C) it requires frequent rebalancing as maturities and interest rateschange.D) durations of assets and liabilities fall at the same rate.E) none of the above.Answer: C Difficulty: ModerateRationale: As time passes the durations of assets and liabilities fall at different rates, requiring portfolio rebalancing. Further, every change in interest rates creates changes in the durations of portfolio assets and liabilities.33. Contingent immunizationA) is a mixed-active passive bond portfolio management strategy.B) is a strategy whereby the portfolio may or may not be immunized.C) is a strategy whereby if and when some trigger point value of theportfolio is reached, the portfolio is immunized to insure an minimumrequired return.D) A and B.E) A, B, and C.Answer: E Difficulty: EasyRationale: Contingent immunization insures a minimum average rate of return over time by immunizing the portfolio if and when the value of the portfolio reaches the trigger point required to insure that rate of return.Thus, the strategy is a combination active/passive strategy; but the portfolio will be immunized only if necessary.34. Some of the problems with immunization areA) duration assumes that the yield curve is flat.B) duration assumes that if shifts in the yield curve occur, these shiftsare parallel.C) immunization is valid for one interest rate change only.D) durations and horizon dates change by the same amounts with the passageof time.E) A, B, and C.Answer: E Difficulty: ModerateRationale: Durations and horizon dates change with the passage of time, but not by the same amounts.35. If a bond portfolio manager believesA) in market efficiency, he or she is likely to be a passive portfoliomanager.B) that he or she can accurately predict interest rate changes, he or sheis likely to be an active portfolio manager.C) that he or she can identify bond market anomalies, he or she is likelyto be a passive portfolio manager.D) A and B.E) A, B, and C.Answer: D Difficulty: ModerateRationale: If one believes that one can predict bond market anomalies, one is likely to be an active portfolio manager.36. According to experts, most pension funds are underfunded becauseA) their liabilities are of shorter duration than their assets.B) their assets are of shorter duration than their liabilities.C) they continually adjust the duration of their liabilities.D) they continually adjust the duration of their assets.E) they are too heavily invested in stocks.Answer: B Difficulty: Moderate37. Cash flow matching on a multiperiod basis is referred to as aA) immunization.B) contingent immunization.C) dedication.D) duration matching.E) rebalancing.Answer: C Difficulty: EasyRationale: Cash flow matching on a multiperiod basis is referred to asa dedication strategy.38. Immunization through duration matching of assets and liabilities may beineffective or inappropriate becauseA) conventional duration strategies assume a flat yield curve.B) duration matching can only immunize portfolios from parallel shiftsin the yield curve.C) immunization only protects the nominal value of terminal liabilitiesand does not allow for inflation adjustment.D) both A and C are true.E) all of the above are true.Answer: E Difficulty: EasyRationale: All of the above are correct statements about the limitations of immunization through duration matching.39. The curvature of the price-yield curve for a given bond is referred toas the bond'sA) modified duration.B) immunization.C) sensitivity.D) convexity.E) tangency.Answer: D Difficulty: EasyRationale: Convexity measures the rate of change of the slope of the price-yield curve, expressed as a fraction of the bond's price.40. Consider a bond selling at par with modified duration of years andconvexity of 210. A 2 percent decrease in yield would cause the price to increase by %, according to the duration rule. What would be the percentage price change according to the duration-with-convexity ruleA) %B) %C) %D) %E) none of the above.Answer: B Difficulty: DifficultRationale: P/P = -D*y + (1/2) * Convexity * (y)2; = * + (1/2) * 210 * (.02)2 = .212 + .042 = .254 %)41. A substitution swap is an exchange of bonds undertaken toA) change the credit risk of a portfolio.B) extend the duration of a portfolio.C) reduce the duration of a portfolio.D) profit from apparent mispricing between two bonds.E) adjust for differences in the yield spread.Answer: D Difficulty: ModerateRationale: A substitution swap is an example of bond price arbitrage, undertaken when the portfolio manager attempts to profit from apparent mispricing.42. A rate anticipation swap is an exchange of bonds undertaken toA) shift portfolio duration in response to an anticipated change ininterest rates.B) shift between corporate and government bonds when the yield spread isout of line with historical values.C) profit from apparent mispricing between two bonds.D) change the credit risk of the portfolio.E) increase return by shifting into higher yield bonds.Answer: A Difficulty: ModerateRationale: A rate anticipation swap is pegged to interest rate forecasting, and involves increasing duration when rates are expected to fall and vice-versa.43. An analyst who selects a particular holding period and predicts the yieldcurve at the end of that holding period is engaging inA) a rate anticipation swap.B) immunization.C) horizon analysis.D) an intermarket spread swap.E) none of the above.Answer: C Difficulty: EasyRationale: Horizon analysis involves selecting a particular holding period and predicting the yield curve at the end of that holding period.The holding period return for the bond can then be predicted.44. The process of unbundling and repackaging the cash flows from one or morebonds into new securities is calledA) speculation.B) immunization.C) reverse hedging.D) interest rate arbitrage.E) financial engineering.Answer: E Difficulty: EasyRationale: The process of financial engineering in the bond market creates derivative securities with different durations and interest rate sensitivities.45. An active investment strategyA) implies that market prices are fairly set.B) attempts to achieve returns greater than those commensurate with therisk borne.C) attempts to achieve the proper return that is commensurate with therisk borne.D) requires portfolio managers, while a passive investment strategy doesnot.E) occurs when bond portfolio managers are hyperactive.Answer: B Difficulty: EasyRationale: An active strategy implies that there are mispricings in the markets, which can be exploited to earn superior returns.46. Interest-rate risk is important toA) active bond portfolio managers.B) passive bond portfolio managers.C) both active and passive bond portfolio managers.D) neither active nor passive bond portfolio managers.E) obsessive bond portfolio managers.Answer: C Difficulty: EasyRationale: Active managers try to identify interest rate trends so they can move in the right direction before the changes. Passive managers try to minimize interest-rate risk by offsetting it with price changes in strategies such as immunization.47. Which of the following are true about the interest-rate sensitivity ofbondsI)Bond prices and yields are inversely related.II)Prices of long-term bonds tend to be more sensitive to interest rate changes than prices of short-term bonds.III)Interest-rate risk is directly related to the bond's coupon rate.IV)The sensitivity of a bond's price to a change in its yield to maturity is inversely related to the yield to maturity at which the bond iscurrently selling.A) I and IIB) I and IIIC) I, II, and IVD) II, III, and IVE) I, II, III, and IVAnswer: C Difficulty: ModerateRationale: Number III is incorrect because interest-rate risk is inversely related to the bond's coupon rate.48. Which of the following researchers have contributed significantly to bondportfolio management theoryI)Sidney HomerII)Harry MarkowitzIII)Burton MalkielIV)Martin LiebowitzV)Frederick MacaulayA) I and IIB) III and VC) III, IV, and VD) I, III, IV, and VE) I, II, III, IV, and VAnswer: D Difficulty: ModerateRationale: Harry Markowitz developed the mean-variance criterion but not a theory of bond portfolio management.49. According to the duration conceptA) only coupon payments matter.B) only maturity value matters.C) the coupon payments made prior to maturity make the effective maturityof the bond greater than its actual time to maturity.D) the coupon payments made prior to maturity make the effective maturityof the bond less than its actual time to maturity.E) discount rates don't matter.Answer: D Difficulty: EasyRationale: Duration considers that some of the cash flows are received prior to maturity and this effectively makes the maturity less than the actual time to maturity.50. Duration is important in bond portfolio management becauseI)it can be used in immunization strategies.II)it provides a gauge of the effective average maturity of the portfolio.III)it is related to the interest rate sensitivity of the portfolio.IV)it is a good predictor of interest rate changes.A) I and IIB) I and IIIC) III and IVD) I, II, and IIIE) I, II, III, and IVAnswer: D Difficulty: ModerateRationale: Duration can be used to calculate the approximate effect of interest rate changes on prices, but is not used to forecast interest rates.51. Two bonds are selling at par value and each has 17 years to maturity. Thefirst bond has a coupon rate of 6% and the second bond has a coupon rate of 13%. Which of the following is true about the durations of these bondsA) The duration of the higher-coupon bond will be higher.B) The duration of the lower-coupon bond will be higher.C) The duration of the higher-coupon bond will equal the duration of thelower-coupon bond.D) There is no consistent statement that can be made about the durationsof the bonds.E) The bond's durations cannot be determined without knowing the pricesof the bonds.Answer: B Difficulty: DifficultRationale: In general, duration is negatively related to coupon rate. The greater the cash flows from coupon interest, the lower the duration will be. Since the bonds have the same time to maturity, that isn't a factor.The duration of the 6% coupon bond equals .06)*(1-(1/) = . The duration of the 13% coupon bond equals .13)*(1-(1/) = .52. Which of the following offers a bond indexA) Merrill LynchB) Salomon Smith BarneyC) LehmanD) All of the aboveE) All but Merrill LynchAnswer: D Difficulty: EasyRationale: All of these are mentioned in the text's discussion of bond indexes.53. Which of the following two bonds is more price sensitive to changes ininterest rates1) A par value bond, A, with a 12-year-to-maturity and a 12% coupon rate.2) A zero-coupon bond, B, with a 12-year-to-maturity and a 12%yield-to-maturity.A) Bond A because of the higher yield to maturity.B) Bond A because of the longer time to maturity.C) Bond B because of the longer duration.D) Both have the same sensitivity because both have the same yield tomaturity.E) None of the aboveAnswer: C Difficulty: ModerateRationale: Duration is the best measure of bond price sensitivity; the longer the duration the higher the price sensitivity.54. Which of the following two bonds is more price sensitive to changes ininterest rates1) A par value bond, D, with a 2-year-to-maturity and a 8% coupon rate.2) A zero-coupon bond, E, with a 2-year-to-maturity and a 8%yield-to-maturity.A) Bond D because of the higher yield to maturity.B) Bond E because of the longer durationC) Bond D because of the longer time to maturity.D) Both have the same sensitivity because both have the same yield tomaturity.E) None of the aboveAnswer: B Difficulty: ModerateRationale: Duration is the best measure of bond price sensitivity; the longer the duration the higher the price sensitivity.55. Holding other factors constant, which one of the following bonds has thesmallest price volatilityA) 7-year, 0% coupon bondB) 7-year, 12% coupon bondC) 7 year, 14% coupon bondD) 7-year, 10% coupon bondE) Cannot tell from the information given.Answer: C Difficulty: Moderate。

Unit 18 Mergers and Acquisitions兼并与收购BackgroundA Typical Leveraged Buyout—一个典型的杠杆收购案例背景介绍兼并与收购(M&A)无疑是资本市场上最惊心动魄、最易引发人的成就感的活动之一,每一次较大的兼并与收购活动都会引起市场各方的震动。

特别是近十年来更是兼并与收购业务大行其道的时期。

随着市场竞争的加剧,兼并与收购或被兼并与收购对公司来说都是可能的,有时它的成功并不完全取决于对等双方或各方的真正实力,技术因素往往起着关键的作用。

在当今市场上,投资银行已经成为兼并与收购活动的主要参与者之一。

兼并与收购业务是投资银行收入的主要来源之一,也是投资银行提高自身竞争能力的主要途径,而投资银行参与兼并与收购活动的方式也日益多样化。

本章主要内容包括两部分:第一部分是对兼并与收购业务的具体介绍与论述,包括:兼并与收购的基本业务类型,如:横向收购、纵向收购、混合收购、管理层收购(MBO)和杠杆收购(LBO)等;反收购措施(如“白衣骑士”、“毒丸”防御等)在敌意收购中的应用;并购融资来源以及各种可能情况下的利弊:投资银行在兼并与收购业务中的作用、费用结构和收入来源。

l 第二部分是一个典型的杠杆收购案例。

正如文中所言“研究一个典型的杠杆收购的全过程是有指导意义的。

我们所使用的例子是建立在假设基础上的,它并不说明任何特定的杠杆收购,而是旨在抓住典型的公司合并过程的本质。

把握本质要求把问题做一些简化——_{旦不失其现实意义”。

通过这个假设的但十分详细、具体的杠杆收购过程,读者能以最简单、最典型的方式把握兼并与收购业务中最本质的东西。

The 1980s was one of the most intense periods for M&A activity in Americans history .The prime reasons for this were two fold: The Reagan administration encouraged the trend by not pursuing many potential infringement of the Sherman Anti-Trust Act and also helped it immeasurably by passing indirectly to investors who became involved. The results helped change the face and history, of American finance and engendered some of the most emotional discussion surrounding the investment banking industry since the 1930s.The 1980s was one of the most intense periods for M&A activity in Americans history. 在美国历史上,20世纪80年代是兼并和收购的一个高峰时期。

商业决策(双语)知到章节测试答案智慧树2023年最新南昌大学第一章测试1.Strategy part includes three areas,excluding ( )参考答案:Strategic analysis2.In the process of enterprise business management,Corporate strategydesign can be( )参考答案:Strategic action3.本课程是从()视角讲授企业经营战略。

参考答案:决策视角4.Business Strategy includes five parts,excluding()参考答案:Strategy in the same organization5.Strategic decisions are made under conditions of ( ).参考答案:complexity6.The characteristics of strategy exclude( )参考答案:certainty7.一个好的企业的宗旨(使命宣言)主要包括四个方面的内容,其中不包括()参考答案:规模8.企业战略目标的具体表型形式我们常用SMART来表示,其中T代表()参考答案:time bound9.The SMART of objectives,we know the S represents ( )参考答案:specific10.并购包括合并与()参考答案:收购第二章测试1.In environmental issues,study guide includes three parts,excluding( )参考答案:natural environment2.PESTILE represents six key words,and the T represents ( )参考答案:technological environment3.下列属于企业外部利益相关者的是()参考答案:顾客4.Technological environment includes three parts,excluding( )参考答案:environment5.环境保护主要包括六个因素,不包括以下()参考答案:完善环境破坏机制6.The key drivers of environment exclude( )参考答案:government globalization7.The competitive advantage of nations Porter’s Diamond excludes( )参考答案:government conditions8.Poter’s 5 Forces exclude( )参考答案:CONSUMER9.下列属于企业长期目标的是( )参考答案:企业社会责任10.IT on five forces excludes( )参考答案:environment第三章测试1.Dynamics nature of competition excludes( ).参考答案:environment2.The definitions of marketing can be divided into 3 parts,excluding( ).参考答案:dissati sfying the customer’s requirement3.In the following options,Corporate plans exclude( ).参考答案:environment4.In the following options,the marketing mix excludes( ).参考答案:protection5.In the marketing mix ,( )is the first one of Promotion.参考答案:attention6.The key words of consumer goods exclude( )参考答案:price7.In the following options,( )is not the reason of why we segment market orcustomer.参考答案:specific environment8.在管理决策中,许多管理人员认为只要选取满意的方案即可,而无需刻意追求最优的方案。

LNTU …Acc附录A会计信息质量在投资中的决策作用对私人信息和监测的影响安妮比蒂,美国俄亥俄州立大学瓦特史考特廖,多伦多大学约瑟夫韦伯,美国麻省理工学院1简介管理者与外部资本的供应商信息是不对称的在这种情况下企业是如何影响金融资本的投资的呢?越来越多的证据表明,会计质量越好,越可以减少信息的不对称和对融资成本的约束。

与此相一致的可能性是,减少了具有更高敏感性的会计质量的公司的投资对内部产生的现金流量。

威尔第和希拉里发现,对企业投资和与投资相关的会计质量容易不足,是容易引发过度投资的原因。

当投资效率低下时,会计的质量重要性可以减轻外部资本的影响,供应商有可能获得私人信息或可直接监测管理人员。

通过访问个人信息与控制管理行为,外部资本的供应商可以直接影响企业的投资,降低了会计质量的重要性。

符合这个想法的还有比德尔和希拉里的比较会计对不同国家的投资质量效益的影响。

他们发现,会计品质的影响在于美国投资效益,而不是在口本。

他们认为,一个可能的解释是不同的是债务和股权的美国版本的资本结构混合了SUS的日本企业。

我们研究如何通过会计质量灵敏度的重要性来延长不同资金来源对企业的投资现金流量的不同影响。

直接测试如何影响不同的融资来源会计,通过最近获得了债务融资的公司来投资敏感性现金流的质量的效果,债务融资的比较说明了对那些不能够通过他们的能力获得融资的没有影响。

为了缓解这一问题,我们限制我们的样本公司有所有最近获得的债务融资和利用访问的差异信息和监测通过公共私人债务获得连续贷款的建议。

我们承认,投资内部现金流敏感性叮能较低获得债务融资的可能性。

然而,这种町能性偏见拒绝了我们的假设。

具体来说,我们确定的数据样本证券公司有1163个采样公司(议会),通过发行资本公共债务或银团债务。

我们限制我们的样本公司最近获得的债务融资持有该公司不断融资与借款。

然而,在样本最近获得的债务融资的公司,也有可能是信号,在资本提供进入私人信息差异和约束他们放在管理中的行为。

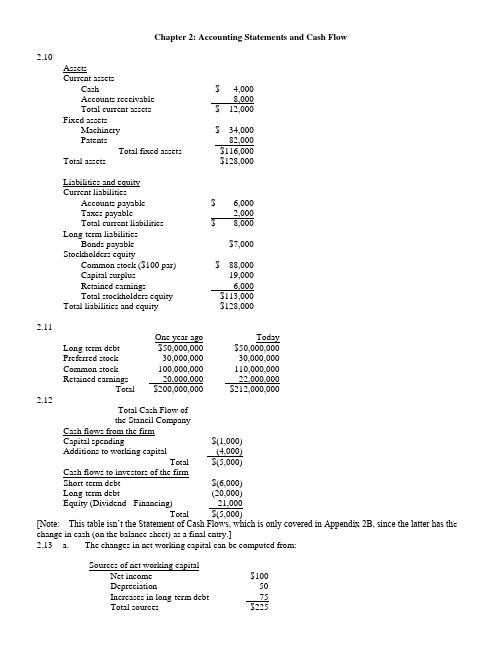

公司财务,第十版,课后答案CHAPTER 2FINANCIAL STATEMENTS AND CASH FLOWAnswers to Concepts Review and Critical Thinking Questions1.True. Every asset can be converted to cash at some price. However, when we are referring to a liquidasset, the added assumption that the asset can be quickly converted to cash at or near market value is important.2.The recognition and matching principles in financial accounting call for revenues, and the costsassociated with producing those revenues, to be “booked” when the revenue pro cess is essentially complete, not necessarily when the cash is collected or bills are paid. Note that this way is not necessarily correct; it’s the way accountants have chosen to do it.3.The bottom line number shows the change in the cash balance on the balance sheet. As such, it is nota useful number for analyzing a company.4. The major difference is the treatment of interest expense. The accounting statement of cash flowstreats interest as an operating cash flow, while the financial cash flows treat interest as a financing cash flow. The logic of the accounting statement of cash flows is that since interest appears on the income statement, which shows the operations for the period, it is an operating cash flow. In reality, interest is a financing e xpense, which results from the company’s choice of debt and equity. We will have more to say about this in a later chapter. When comparing the two cash flow statements, the financial statement of cash flows is a more appropriate measureof the company’s pe rformance because of its treatment of interest.5.Market values can never be negative. Imagine a share of stock selling for –$20. This would meanthat if you placed an order for 100 shares, you would get the stock along with a check for $2,000.How many shares do you want to buy? More generally, because of corporate and individual bankruptcy laws, net worth for a person or a corporation cannot be negative, implying that liabilities cannot exceed assets in market value.6.For a successful company that is rapidly expanding, for example, capital outlays will be large,possibly leading to negative cash flow from assets. In general, what matters is whether the money is spent wisely, not whether cash flow from assets is positive or negative.7.It’s probably not a good sign for an established company to have negative cash flow from operations,but it would be fairly ordinary for a start-up, so it depends.8.For example, if a company were to become more efficient in inventory management, the amount ofinventory needed would decline. The same might be true if the company becomes better at collecting its receivables. In general, anything that leads to a decline in ending NWC relative to beginning would have this effect. Negative net capital spending would mean more long-lived assets were liquidated than purchased.9.If a company raises more money from selling stock than it pays in dividends in a particular period,its cash flow to stockholders will be negative. If a company borrows more than it pays in interest and principal, its cash flowto creditors will be negative.10.The adjustments discussed were purely accounting changes; they had no cash flow or market valueconsequences unless the new accounting information caused stockholders to revalue the derivatives. Solutions to Questions and ProblemsNOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability constraints, when these intermediate steps are included in this solutions manual, rounding may appear to have occurred. However, the final answer for each problem is found without rounding during any step in the problem.Basic1.To find owners’ equity, we must construct a balance sheet as follows:Balance SheetCA $ 5,700 CL $ 4,400NFA 27,000 LTD 12,900OE ??TA $32,700 TL & OE $32,700We know that total liabilities and owners’ equity (TL & OE) must equal total assets of $32,700. We also know that TL & OE is equal to current liabilities plus long-term debt plus owner’s equity, so owner’s equity is:O E = $32,700 –12,900 – 4,400 = $15,400N WC = CA – CL = $5,700 – 4,400 = $1,3002. The income statement for the company is:Income StatementSales $387,000Costs 175,000Depreciation 40,000EBIT $172,000Interest 21,000EBT $151,000Taxes 52,850Net income $ 98,150One equation for net income is:Net income = Dividends + Addition to retained earningsRearranging, we get:Addition to retained earnings = Net income – DividendsAddition to retained earnings = $98,150 – 30,000Addition to retained earnings = $68,1503.To find the book value of current assets, we use: NWC = CA – CL. Rearranging to solve for currentassets, we get:CA = NWC + CL = $800,000 + 2,400,000 = $3,200,000The market value of current assets and net fixed assets is given, so:Book value CA = $3,200,000 Market value CA = $2,600,000 Book value NFA = $5,200,000 Market value NFA = $6,500,000 Book value assets = $8,400,000 Market value assets = $9,100,0004.Taxes = 0.15($50,000) + 0.25($25,000) + 0.34($25,000) + 0.39($273,000 – 100,000)Taxes = $89,720The average tax rate is the total tax paid divided by net income, so:Average tax rate = $89,720 / $273,000Average tax rate = 32.86%The marginal tax rate is the tax rate on the next $1 ofearnings, so the marginal tax rate = 39%.5.To calculate OCF, we first need the income statement:Income StatementSales $18,700Costs 10,300Depreciation 1,900EBIT $6,500Interest 1,250Taxable income $5,250Taxes 2,100Net income $3,150OCF = EBIT + Depreciation – TaxesOCF = $6,500 + 1,900 – 2,100OCF = $6,300/doc/a95a227710a6f524cdbf8525.ht ml capital spending = NFA end– NFA beg + Depreciation Net capital spending = $1,690,000 – 1,420,000 + 145,000Net capital spending = $415,0007.The long-term debt account will increase by $35 million, the amount of the new long-term debt issue.Since the company sold 10 million new shares of stock with a $1 par value, the common stock account will increase by $10 million. The capital surplus account will increase by $48 million, the value of the new stock sold above its par value. Since the company had a net income of $9 million, and paid $2 million in dividends, the addition to retained earnings was $7 million, which will increase the accumulated retained earnings account. So, the new long-term debt and stockholders’ equity portion of the balance sheet will be:Long-term debt $ 100,000,000Total long-term debt $ 100,000,000Shareholders equityPreferred stock $ 4,000,000Common stock ($1 par value) 25,000,000Accumulated retained earnings 142,000,000Capital surplus 93,000,000Total equity $ 264,000,000Total Liabilities & Equity $ 364,000,0008.Cash flow to creditors = Interest paid – Net new borrowingCash flow to creditors = $127,000 – (LTD end– LTD beg)Cash flow to creditors = $127,000 – ($1,520,000 – 1,450,000) Cash flow to creditors = $127,000 – 70,000Cash flow to creditors = $57,0009. Cash flow to stockholders = Dividends paid –Net new equityCash flow to stockholders = $275,000 –[(Common end + APIS end) – (Common beg + APIS beg)]Cash flow to stockholders = $275,000 –[($525,000 + 3,700,000) – ($490,000 + 3,400,000)]Cash flow to stockholders = $275,000 –($4,225,000 –3,890,000)Cash flow to stockholders = –$60,000Note, APIS is the additional paid-in surplus.10. Cash flow from assets = Cash flow to creditors + Cash flow to stockholders= $57,000 – 60,000= –$3,000Cash flow from assets = OCF – Change in NWC – Net capital spending–$3,000 = OCF – (–$87,000) – 945,000OCF = $855,000Operating cash flow = –$3,000 – 87,000 + 945,000Operating cash flow = $855,000Intermediate11. a.The accounting statement of cash flows explains the change in cash during the year. Theaccounting statement of cash flows will be:Statement of cash flowsOperationsNet income $95Depreciation 90Changes in other current assets (5)Accounts payable 10Total cash flow from operations $190Investing activitiesAcquisition of fixed assets $(110)Total cash flow from investing activities $(110)Financing activitiesProceeds of long-term debt $5Dividends (75)Total cash flow from financing activities ($70)Change in cash (on balance sheet) $10b.Change in NWC = NWC end– NWC beg= (CA end– CL end) – (CA beg– CL beg)= [($65 + 170) – 125] – [($55 + 165) – 115)= $110 – 105= $5c.To find the cash flow generated by the firm’s assets, we need the operating cash flow, and thecapital spending. So, calculating each of these, we find:Operating cash flowNet income $95Depreciation 90Operating cash flow $185Note that we can calculate OCF in this manner since there are no taxes.Capital spendingEnding fixed assets $390Beginning fixed assets (370)Depreciation 90Capital spending $110Now we can calculate the cash flow generated by the firm’s assets, which is:Cash flow from assetsOperating cash flow $185Capital spending (110)Change in NWC (5)Cash flow from assets $ 7012.With the information provided, the cash flows from the firm are the capital spending and the changein net working capital, so:Cash flows from the firmCapital spending $(21,000)Additions to NWC (1,900)Cash flows from the firm $(22,900)And the cash flows to the investors of the firm are:Cash flows to investors of the firmSale of long-term debt (17,000)Sale of common stock (4,000)Dividends paid 14,500Cash flows to investors of the firm $(6,500)13. a. The interest expense for the company is the amount of debt times the interest rate on the debt.So, the income statement for the company is:Income StatementSales $1,060,000Cost of goods sold 525,000Selling costs 215,000Depreciation 130,000EBIT $190,000Interest 56,000Taxable income $134,000Taxes 46,900Net income $ 87,100b. And the operating cash flow is:OCF = EBIT + Depreciation – TaxesOCF = $190,000 + 130,000 – 46,900OCF = $273,10014.To find the OCF, we first calculate net income.Income StatementSales $185,000Costs 98,000Depreciation 16,500Other expenses 6,700EBIT $63,800Interest 9,000Taxable income $54,800Taxes 19,180Net income $35,620Dividends $9,500Additions to RE $26,120a.OCF = EBIT + Depreciation – TaxesOCF = $63,800 + 16,500 – 19,180OCF = $61,120b.CFC = Interest – Net new LTDCFC = $9,000 – (–$7,100)CFC = $16,100Note that the net new long-term debt is negative because the company repaid part of its long-term debt.c.CFS = Dividends – Net new equityCFS = $9,500 – 7,550CFS = $1,950d.We know that CFA = CFC + CFS, so:CFA = $16,100 + 1,950 = $18,050CFA is also equal to OCF – Net capital spending – Change in NWC. We already know OCF.Net capital spending is equal to:Net capital spending = Increase in NFA + DepreciationNet capital spending = $26,100 + 16,500Net capital spending = $42,600Now we can use:CFA = OCF – Net capital spending – Change in NWC$18,050 = $61,120 – 42,600 – Change in NWC.Solving for the change in NWC gives $470, meaning the company increased its NWC by $470.15.The solution to this question works the income statement backwards. Starting at the bottom:Net income = Dividends + Addition to ret. earningsNet income = $1,570 + 4,900Net income = $6,470Now, looking at the income statement:EBT –(EBT × Tax rate) = Net incomeRecognize that EBT × tax rate is simply the calculation for taxes. Solving this for EBT yields:EBT = NI / (1– Tax rate)EBT = $6,470 / (1 – .35)EBT = $9,953.85Now we can calculate:EBIT = EBT + InterestEBIT = $9,953.85 + 1,840EBIT = $11,793.85The last step is to use:EBIT = Sales – Costs – Depreciation$11,793.85 = $41,000 – 26,400 – DepreciationDepreciation = $2,806.1516.The market value of shareholders’ equity cannot be negative. A negative market value in this casewould imply that the company would pay you to own the stock. The market value of shareholders’ equity can be stated as: Shareholders’ equity = Max [(TA – TL), 0]. So, if TA is $12,400, equity is equal to $1,500, and if TA is $9,600, equity is equal to $0. We should note here that while the market value of equity cannot be negative, the book value of share holders’ equity can be negative. 17. a. Taxes Growth = 0.15($50,000) + 0.25($25,000) + 0.34($86,000 – 75,000) = $17,490Taxes Income = 0.15($50,000) + 0.25($25,000) + 0.34($25,000) + 0.39($235,000)+ 0.34($8,600,000 – 335,000)= $2,924,000b. Each firm has a marginal tax rate of 34% on the next $10,000 of taxable income, despite theirdifferent average tax rates, so both firms will pay an additional $3,400 in taxes.18.Income StatementSales $630,000COGS 470,000A&S expenses 95,000Depreciation 140,000EBIT ($75,000)Interest 70,000Taxable income ($145,000)Taxes (35%) 0/doc/a95a227710a6f524cdbf8525.ht ml income ($145,000)b.OCF = EBIT + Depreciation – TaxesOCF = ($75,000) + 140,000 – 0OCF = $65,000/doc/a95a227710a6f524cdbf8525.ht ml income was negative because of the tax deductibility of depreciation and interest expense.However, the actual cash flow from operations was positive because depreciation is a non-cash expense and interest is a financing expense, not an operating expense.19. A firm can still pay out dividends if net income is negative; it just has to be sure there is sufficientcash flow to make the dividend payments.Change in NWC = Net capital spending = Net new equity = 0. (Given)Cash flow from assets = OCF – Change in NWC – Net capitalspendingCash flow from assets = $65,000 – 0 – 0 = $65,000Cash flow to stockholders = Dividends – Net new equityCash flow to stockholders = $34,000 – 0 = $34,000Cash flow to creditors = Cash flow from assets – Cash flow to stockholdersCash flow to creditors = $65,000 – 34,000Cash flow to creditors = $31,000Cash flow to creditors is also:Cash flow to creditors = Interest – Net new LTDSo:Net new LTD = Interest – Cash flow to creditorsNet new LTD = $70,000 – 31,000Net new LTD = $39,00020. a.The income statement is:Income StatementSales $19,900Cost of good sold 14,200Depreciation 2,700EBIT $ 3,000Interest 670Taxable income $ 2,330Taxes 932Net income $1,398b.OCF = EBIT + Depreciation – TaxesOCF = $3,000 + 2,700 – 932OCF = $4,768c.Change in NWC = NWC end– NWC beg= (CA end– CL end) – (CA beg– CL beg)= ($5,135 – 2,535) – ($4,420 – 2,470)= $2,600 – 1,950 = $650Net capital spending = NFA end– NFA beg + Depreciation = $16,770 – 15,340 + 2,700= $4,130CFA = OCF – Change in NWC – Net capital spending= $4,768 – 650 – 4,130= –$12The cash flow from assets can be positive or negative, since it represents whether the firm raised funds or distributed funds on a net basis. In this problem, even though net income and OCF are positive, the firm invested heavily in both fixed assets and net working capital; it had to raise a net $12 in funds from its stockholders and creditors to make these investments.d.Cash flow to creditors = Interest – Net new LTD= $670 – 0= $670Cash flow to stockholders = Cash flow from assets – Cash flow to creditors= –$12 – 670= –$682We can also calculate the cash flow to stockholders as:Cash flow to stockholders = Dividends – Net new equitySolving for net new equity, we get:Net new equity = $650 – (–682)= $1,332The firm had positive earnings in an accounting sense (NI > 0) and had positive cash flow from operations. The firm invested $650 in new net working capital and $4,130 in new fixed assets.The firm had to raise $12 from its stakeholders to support this new investment. It accomplished this by raising $1,332 in theform of new equity. After paying out $650 of this in the form of dividends to shareholders and $670 in the form of interest to creditors, $12 was left to meet the firm’s cash flow needs for investment.21. a.Total assets 2011 = $936 + 4,176 = $5,112Total liabilities 2011 = $382 + 2,160 = $2,542Owners’ equity 2011 = $5,112 – 2,542 = $2,570Total assets 2012 = $1,015 + 4,896 = $5,911Total liabilities 2012 = $416 + 2,477 = $2,893Owners’ equity 2012 = $5,911 – 2,893 = $3,018b.NWC 2011 = CA11 – CL11 = $936 – 382 = $554NWC 2012 = CA12 – CL12 = $1,015 – 416 = $599Change in NWC = NWC12 – NWC11 = $599 – 554 = $45c.We can calculate net capital spending as:Net capital spending = Net fixed assets 2012 –Net fixed assets 2011 + DepreciationNet capital spending = $4,896 – 4,176 + 1,150Net capital spending = $1,870So, the company had a net capital spending cash flow of $1,870. We also know that net capital spending is:Net capital spending = Fixed assets bought –Fixed assets sold$1,870 = $2,160 – Fixed assets soldFixed assets sold = $2,160 – 1,870 = $290To calculate the cash flow from assets, we must first calculate the operating cash flow. The operating cash flow is calculated as follows (you can also prepare a traditional income statement): EBIT = Sales – Costs – DepreciationEBIT = $12,380 – 5,776 – 1,150EBIT = $5,454EBT = EBIT – InterestEBT = $5,454 – 314EBT = $5,140Taxes = EBT ? .40Taxes = $5,140 ? .40Taxes = $2,056OCF = EBIT + Depreciation – TaxesOCF = $5,454 + 1,150 – 2,056OCF = $4,548Cash flow from assets = OCF – Change in NWC – Net capital spending.Cash flow from assets = $4,548 – 45 – 1,870Cash flow from assets = $2,633/doc/a95a227710a6f524cdbf8525.ht ml new borrowing = LTD12 – LTD11Net new borrowing = $2,477 – 2,160Net new borrowing = $317Cash flow to creditors = Interest – Net new LTDCash flow to creditors = $314 – 317Cash flow to creditors = –$3Net new borrowing = $317 = Debt issued – Debt retiredDebt retired = $432 – 317 = $11522.Balance sheet as of Dec. 31, 2011Cash $4,109 Accounts payable $4,316 Accounts receivable 5,439 Notes payable 794 Inventory 9,670 Current liabilities $5,110 Current assets $19,218Long-term debt $13,460 Net fixed assets $34,455 Owners' equity 35,103 Total assets $53,673 Total liab. & equity $53,673 Balance sheet as of Dec. 31, 2012Cash $5,203 Accounts payable $4,185Accounts receivable 6,127 Notes payable 746Inventory 9,938 Current liabilities $4,931Current assets $21,268Long-term debt $16,050 Net fixed assets $35,277 Owners' equity 35,564Total assets Total liab. & equity2011 Income Statement 2012 Income Statement Sales $7,835.00Sales $8,409.00 COGS 2,696.00COGS 3,060.00 Other expenses 639.00Other expenses 534.00 Depreciation 1,125.00Depreciation 1,126.00 EBIT $3,375.00EBIT $3,689.00 Interest 525.00Interest 603.00 EBT $2,850.00EBT $3,086.00 Taxes 969.00Taxes 1,049.24 Net income $1,881.00Net income $2,036.76 Dividends $956.00Dividends $1,051.00 Additions to RE 925.00Additions to RE 985.76 23.OCF = EBIT + Depreciation –TaxesOCF = $3,689 + 1,126 – 1,049.24OCF = $3,765.76Change in NWC = NWC end– NWC beg = (CA – CL) end– (CA – CL) begChange in NWC = ($21,268 – 4,931) – ($19,218 – 5,110)Change in NWC = $2,229Net capital spending = NFA end– NFA beg+ DepreciationNet capital spending = $35,277 – 34,455 + 1,126Net capital spending = $1,948Cash flow from assets = OCF – Change in NWC – Net capital spendingCash flow from assets = $3,765.76 – 2,229 – 1,948Cash flow from assets = –$411.24Cash flow to creditors = Interest – Net new LTDNet new LTD = LTD end– LTD begCash flow to creditors = $603 – ($16,050 – 13,460)Cash flow to creditors = –$1,987Net new equity = Common stock end– Common stock beg Common stock + Retained earnings = Total owners’ equity Net new equity = (OE – RE) end– (OE – RE) begNet new equity = OE end– OE beg + RE beg– RE endRE end= RE beg+ Additions to RENet new equity = OE end–OE beg+ RE beg–(RE beg + Additions to RE)= OE end– OE beg– Additions to RENet new equity = $35,564 – 35,103 – 985.76 = –$524.76Cash flow to stockholders = Dividends – Net new equityCash flow to stockholders = $1,051– (–$524.76)Cash flow to stockholders = $1,575.76As a check, cash flow from assets is –$411.24Cash flow from assets = Cash flow from creditors + Cash flow to stockholdersCash flow from assets = –$1,987 + 1,575.76Cash flow from assets = –$411.24Challenge24.We will begin by calculating the operating cash flow. First, we need the EBIT, which can becalculated as:EBIT = Net income + Current taxes + Deferred taxes + InterestEBIT = $173 + 98 + 19 + 48EBIT = $338Now we can calculate the operating cash flow as:Operating cash flowEarnings before interest and taxes $338Depreciation 94Current taxes (98)Operating cash flow $334The cash flow from assets is found in the investing activities portion of the accounting statement of cash flows, so: Cash flow from assetsAcquisition of fixed assets $215Sale of fixed assets (23)Capital spending $192The net working capital cash flows are all found in the operations cash flow section of the accounting statement of cash flows. However, instead of calculating the net working capital cash flows as the change in net working capital, we must calculate each item individually. Doing so, we find:Net working capital cash flowCash $14Accounts receivable 18Inventories (22)Accounts payable (17)Accrued expenses 9Notes payable (6)Other (3)NWC cash flow ($7)Except for the interest expense and notes payable, the cash flow to creditors is found in the financing activities of the accounting statement of cash flows. The interest expense from the income statement is given, so:Cash flow to creditorsInterest $48Retirement of debt 162Debt service $210Proceeds from sale of long-term debt (116)Total $94And we can find the cash flow to stockholders in the financing section of the accounting statement of cash flows. The cash flow to stockholders was:Cash flow to stockholdersDividends $ 86Repurchase of stock 13Cash to stockholders $ 99Proceeds from new stock issue (44)Total $ 55/doc/a95a227710a6f524cdbf8525.ht ml capital spending = NFA end– NFA beg + Depreciation = (NFA end– NFA beg) + (Depreciation + AD beg) – AD beg = (NFA end– NFA beg)+ AD end– AD beg= (NFA end + AD end) – (NFA beg + AD beg) = FA end– FA beg26. a.The tax bubble causes average tax rates to catch up to marginal tax rates, thus eliminating thetax advantage of low marginal rates for high income corporations.b.Assuming a taxable income of $335,000, the taxes will be:Taxes = 0.15($50K) + 0.25($25K) + 0.34($25K) + 0.39($235K) = $113.9KAverage tax rate = $113.9K / $335K = 34%The marginal tax rate on the next dollar of income is 34 percent.For corporate taxable income levels of $335K to $10M,average tax rates are equal to marginal tax rates.Taxes = 0.34($10M) + 0.35($5M) + 0.38($3.333M) = $6,416,667Average tax rate = $6,416,667 / $18,333,334 = 35%The marginal tax rate on the next dollar of income is 35 percent. For corporate taxable income levels over $18,333,334, average tax rates are again equal to marginal tax rates.c.Taxes = 0.34($200K) = $68K = 0.15($50K) + 0.25($25K) +0.34($25K) + X($100K);X($100K) = $68K – 22.25K = $45.75KX = $45.75K / $100KX = 45.75%。