Chapter3

Insurance,Collars,and Other Strategies

Question3.1.

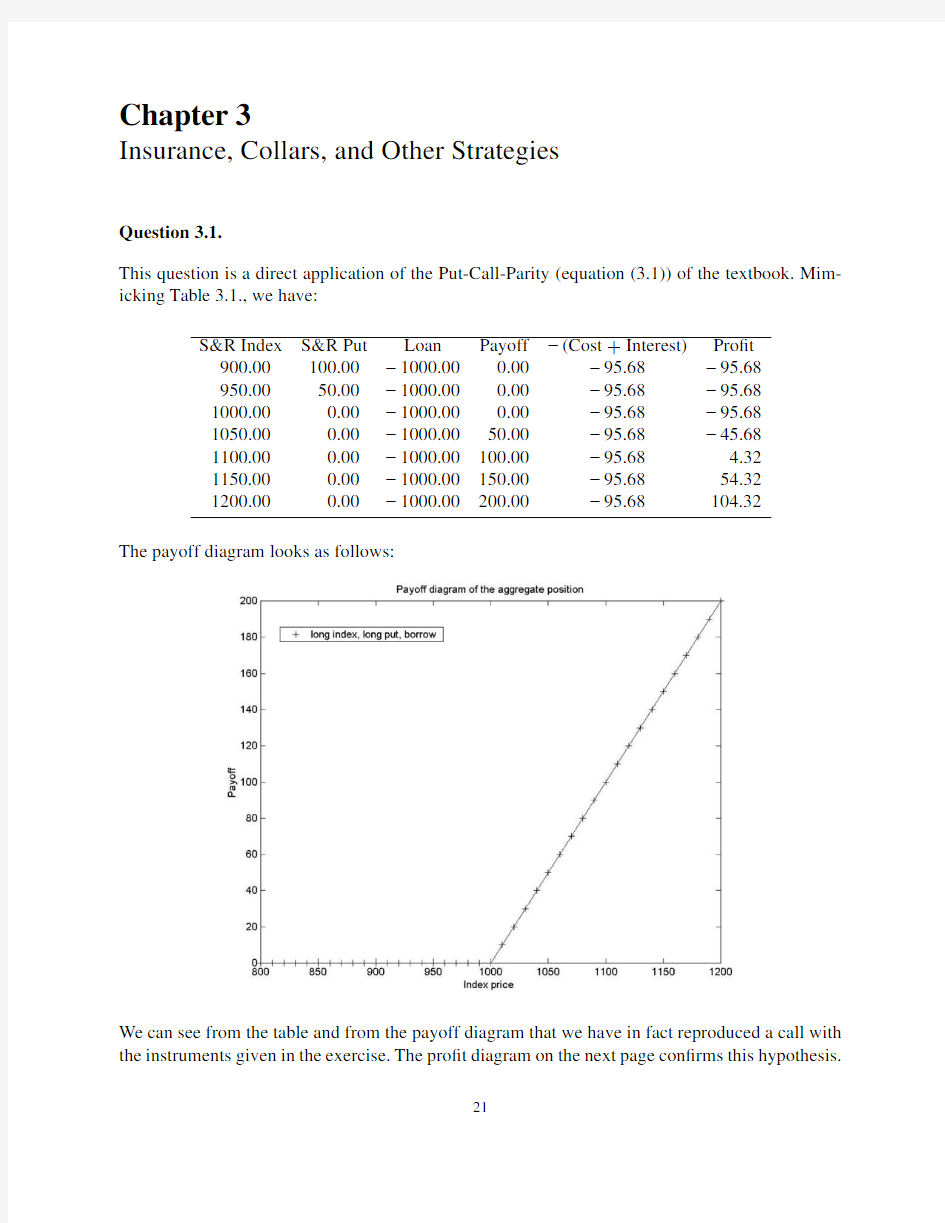

This question is a direct application of the Put-Call-Parity(equation(3.1))of the textbook.Mim-icking Table3.1.,we have:

S&R Index S&R Put Loan Payoff?(Cost+Interest)Pro?t

900.00100.00?1000.000.00?95.68?95.68

950.0050.00?1000.000.00?95.68?95.68

1000.000.00?1000.000.00?95.68?95.68

1050.000.00?1000.0050.00?95.68?45.68

1100.000.00?1000.00100.00?95.68 4.32

1150.000.00?1000.00150.00?95.6854.32

1200.000.00?1000.00200.00?95.68104.32

The payoff diagram looks as follows:

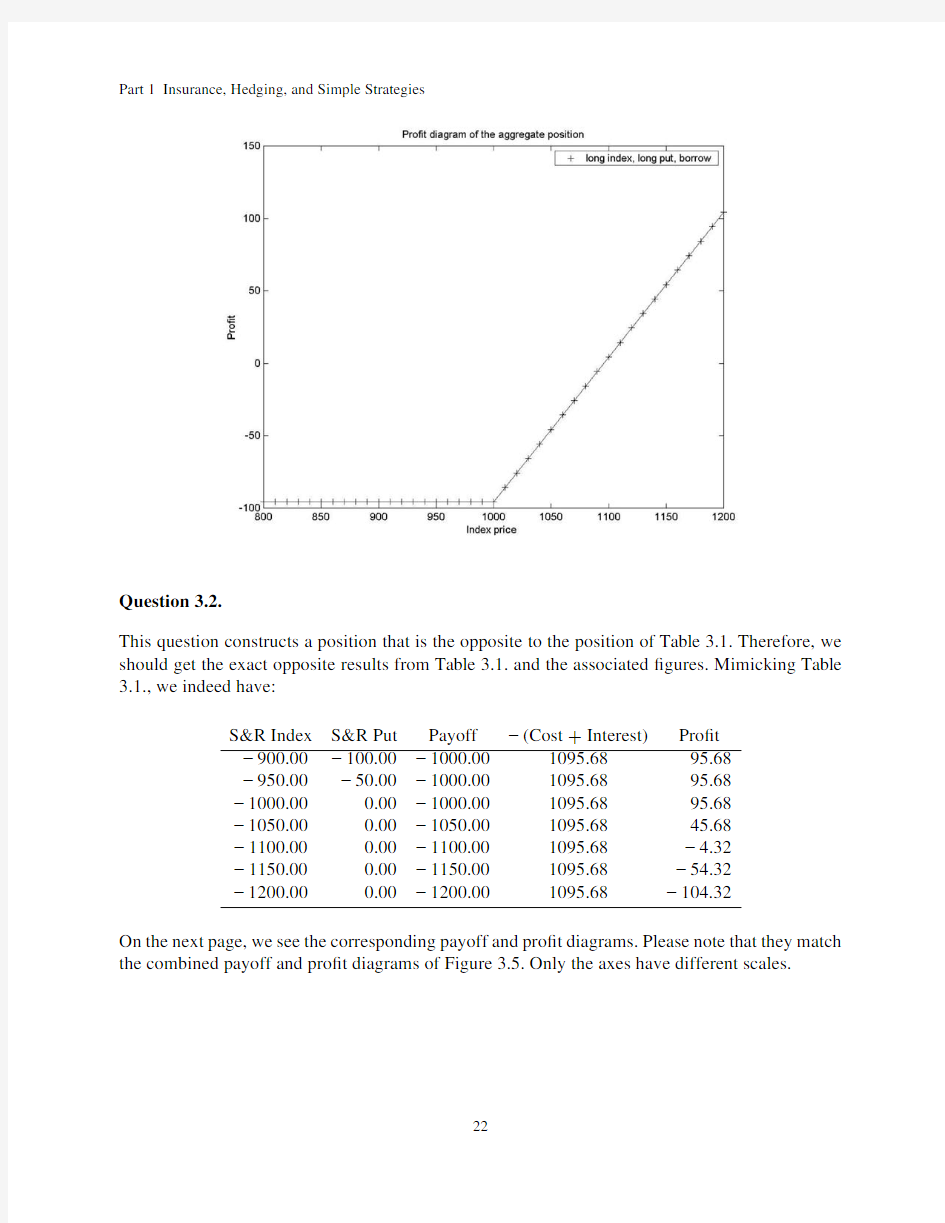

We can see from the table and from the payoff diagram that we have in fact reproduced a call with the instruments given in the exercise.The pro?t diagram on the next page con?rms this hypothesis.

Part1Insurance,Hedging,and Simple Strategies

Question3.2.

This question constructs a position that is the opposite to the position of Table3.1.Therefore,we should get the exact opposite results from Table3.1.and the associated?gures.Mimicking Table 3.1.,we indeed have:

S&R Index S&R Put Payoff?(Cost+Interest)Pro?t

?900.00?100.00?1000.001095.6895.68

?950.00?50.00?1000.001095.6895.68

?1000.000.00?1000.001095.6895.68

?1050.000.00?1050.001095.6845.68

?1100.000.00?1100.001095.68?4.32

?1150.000.00?1150.001095.68?54.32

?1200.000.00?1200.001095.68?104.32

On the next page,we see the corresponding payoff and pro?t diagrams.Please note that they match the combined payoff and pro?t diagrams of Figure3.5.Only the axes have different scales.

Chapter3Insurance,Collars,and Other Strategies Payoff-diagram:

Pro?t diagram:

Part1Insurance,Hedging,and Simple Strategies

Question3.3.

In order to be able to draw pro?t diagrams,we need to?nd the future value of the put premium,the call premium and the investment in zero-coupon bonds.We have for:

the put premium:$51.777×(1+0.02)=$52.81,

the call premium:$120.405×(1+0.02)=$122.81and

the zero-coupon bond:$931.37×(1+0.02)=$950.00

Now,we can construct the payoff and pro?t diagrams of the aggregate position:

Payoff diagram:

From this?gure,we can already see that the combination of a long put and the long index looks exactly like a certain payoff of$950,plus a call with a strike price of950.But this is the alternative given to us in the question.We have thus con?rmed the equivalence of the two combined positions for the payoff diagrams.The pro?t diagrams on the next page con?rm the equivalence of the two positions(which is again an application of the Put-Call-Parity).

Chapter 3Insurance,Collars,and Other Strategies

Pro?t Diagram for a long 950-strike put and a long index combined:

Question 3.4.

This question is another application of Put-Call-Parity.Initially,we have the following cost to enter into the combined position:We receive $1,000from the short sale of the index,and we have to pay the call premium.Therefore,the future value of our cost is: $120.405?$1,000 ×(1+0.02)=?$897.19.Note that a negative cost means that we initially have an in?ow of money.

Now,we can directly proceed to draw the payoff diagram:

Part 1Insurance,Hedging,and Simple Strategies

We can clearly see from the ?gure that the payoff graph of the short index and the long call looks like a ?xed obligation of $950,which is alleviated by a long put position with a strike price of 950.The following pro?t diagram,including the cost for the combined position,con?rms this:

Question 3.5.

This question is another application of Put-Call-Parity.Initially,we have the following cost to enter into the combined position:We receive $1,000from the short sale of the index,and we have to pay the call premium.Therefore,the future value of our cost is: $71.802?$1,000 ×(1+0.02)=?$946.76.Note that a negative cost means that we initially have an in?ow of money.

Chapter3Insurance,Collars,and Other Strategies Now,we can directly proceed to draw the payoff diagram:

In order to be able to compare this position to the other suggested position of the exercise,we need to?nd the future value of the borrowed$1,029.41.We have:$1,029.41×(1+0.02)=$1,050. We can now see from the?gure that the payoff graph of the short index and the long call looks like a?xed obligation of$1,050,which is exactly the future value of the borrowed amount,and a long put position with a strike price of1,050.The following pro?t diagram,including the cost for the combined position we calculated above,con?rms this.The pro?t diagram is the same as the pro?t diagram for a loan and a long1,050-strike put with an initial premium of$101.214.

Part 1Insurance,Hedging,and Simple Strategies

Pro?t Diagram of going short the index and buying a 1,050-strike call:

Question 3.6.

We now move from a graphical representation and veri?cation of the Put-Call-Parity to a mathe-matical representation.Let us ?rst consider the payoff of (a).If we buy the index (let us name it S),we receive at the time of expiration T of the options simply S T .

The payoffs of part (b)are a little bit more complicated.If we deal with options and the maximum function,it is convenient to split the future values of the index into two regions:one where S T We have for the payoffs in (b): Instrument S T $931.37×1.02=$950$931.37×1.02=$950Long Call Option max (S T ?950,0)=0S T ?950Short Put Option ?max $950?S T ,0 0=S T ?$950Total S T S T Chapter 3Insurance,Collars,and Other Strategies We now see that the total aggregate position only gives us S T ,no matter what the ?nal index value is—but this is the same payoff as in part (a).Our proof for the payoff equivalence is complete.Now let us turn to the pro?ts.If we buy the index today,we need to ?nance it.Therefore,we borrow $1,000,and have to repay $1,020after one year.The pro?t for part (a)is thus:S T ?$1,020. The pro?ts of the aggregate position in part (b)are the payoffs,less the future value of the call premium plus the future value of the put premium (because we have sold the put),and less the future value of the loan we gave initially.Note that we already know that a risk-less bond is canceling out of the pro?t calculations.We can again tabulate: Instrument S T ?$950?$950Long Call Option max (S T ?950,0)=0S T ?950Future value call premium ?$120.405×1.02=?$122.81?$120.405×1.02=?$122.81Short Put Option ?max $950?S T ,0 0=S T ?$950Future value put premium $51.777×1.02=$52.81$51.777×1.02=$52.81 Total S T ?1020S T ?1020 Indeed,we see that the pro?ts for part (a)and part (b)are identical as well. Question 3.7. Let us ?rst consider the payoff of (a).If we short the index (let us name it S),we have to pay at the time of expiration T of the options:?S T . The payoffs of part (b)are more complicated.Let us look again at each region separately,and hope to be able to draw a conclusion when we look at the aggregate position. We have for the payoffs in (b): Instrument S T ?$1029.41×1.02=?$1050?$1029.41×1.02=?$1050Short Call Option ?max (S T ?1050,0)=0?max (S T ?1050,0)=1050?S T Long Put Option max $1050?S T ,0 0=$1050?S T Total ?S T ?S T Part 1Insurance,Hedging,and Simple Strategies We see that the total aggregate position gives us ?S T ,no matter what the ?nal index value is—but this is the same payoff as part (a).Our proof for the payoff equivalence is complete. Now let us turn to the pro?ts.If we sell the index today,we receive money that we can lend out.Therefore,we can lend $1,000,and be repaid $1,020after one year.The pro?t for part (a)is thus:$1,020?S T . The pro?ts of the aggregate position in part (b)are the payoffs,less the future value of the put premium plus the future value of the call premium (because we sold the call),and less the future value of the loan we gave initially.Note that we know already that a risk-less bond is canceling out of the pro?t calculations.We can again tabulate: Instrument S T ?$1029.41×1.02=?$1050?$1029.41×1.02=?$1050Future value of borrowed $1050$1050money Short Call Option ?max (S T ?1050,0)=0?max (S T ?1050,0)=1050?S T Future value of premium $71.802×1.02=$73.24$71.802×1.02=$73.24Long Put Option max $1050?S T ,0 =0$1050?S T Future value of premium ?$101.214×1.02=?$103.24?$101.214×1.02=?$103.24Total $1,020?S T $1,020?S T Indeed,we see that the pro?ts for part (a)and part (b)are identical as well. Question 3.8. This question is a direct application of the Put-Call-Parity.We will use equation (3.1)in the follow-ing,and input the given variables: Call (K,t)?P ut (K,t)=P V F 0,t ?K ?Call (K,t)?P ut (K,t)?P V F 0,t =?P V (K) ?Call (K,t)?P ut (K,t)?S 0=?P V (K) ?$109.20?$60.18?$1,000=?K 1.02 ?K =$970.00 Question 3.9. The strategy of buying a call (or put)and selling a call (or put)at a higher strike is called call (put)bull spread.In order to draw the pro?t diagrams,we need to ?nd the future value of the cost of entering in the bull spread positions.We have: Chapter3Insurance,Collars,and Other Strategies Cost of call bull spread: $120.405?$93.809 ×1.02=$27.13 Cost of put bull spread: $51.777?$74.201 ×1.02=?$22.87 The payoff diagram shows that the payoffs to the put bull spread are uniformly less than the payoffs to the call bull spread.There is a difference,because the put bull spread has a negative initial cost, i.e.,we are receiving money if we enter into it.The difference is exactly$50,the value of the difference between the two strike prices.It is equivalent as well to the value of the difference of the future values of the initial premia. Yet,the higher initial cost for the call bull spread is exactly offset by the higher payoff so that the pro?ts of both strategies are the same.It is easy to show this with equation(3.1),the put-call-parity. Payoff-Diagram: Part 1Insurance,Hedging,and Simple Strategies Pro?t diagram: Question 3.10. The strategy of selling a call (or put)and buying a call (or put)at a higher strike is called call (put)bear spread.In order to draw the pro?t diagrams,we need to ?nd the future value of the cost of entering in the bull spread positions.We have:Cost of call bear spread: $71.802?$120.405 ×1.02=?$49.575 Cost of put bear spread: $101.214?$51.777 ×1.02=$50.426 The payoff diagram shows that the payoff to the call bear spread is uniformly less than the payoffs to the put bear spread.The difference is exactly $100,equal to the difference in strikes and as well equal to the difference in the future value of the costs of the spreads. There is a difference,because the call bear spread has a negative initial cost,i.e.,we are receiving money if we enter into it. The higher initial cost for the put bear spread is exactly offset by the higher payoff so that the pro?ts of both strategies turn out to be the same.It is easy to show this with equation (3.1),the put-call-parity. Chapter3Insurance,Collars,and Other Strategies Payoff-Diagram: Pro?t Diagram: Part 1Insurance,Hedging,and Simple Strategies Question 3.11. In order to be able to draw the pro?t diagram,we need to ?nd the future value of the costs of establishing the suggested position.We need to ?nance the index purchase,buy the 950-strike put and we receive the premium of the sold call.Therefore,the future value of our cost is: $1,000?$71.802+$51.777 ×1.02=$999.57. Now we can draw the pro?t diagram: The net option premium cost today is:?$71.802+$51.777=?$20.025.We receive about $20if we enter into this collar.If we want to construct a zero-cost collar and keep the 950-strike put,we would need to increase the strike price of the call.By increasing the strike price of the call,the buyer of the call must wait for larger increases in the underlying index before the option pays off.This makes the call option less attractive,and the buyer of the option is only willing to pay a smaller premium.We receive less money,thus pushing the net option premium towards zero.Question 3.12. Our initial cash required to put on the collar,i.e.the net option premium,is as follows:?$51.873+$51.777=?$0.096.Therefore,we receive only 10cents if we enter into this collar.The position is very close to a zero-cost collar. Chapter3Insurance,Collars,and Other Strategies The pro?t diagram looks as follows: If we compare this pro?t diagram with the pro?t diagram of the previous exercise(3.11.),we see that we traded in the additional call premium(that limited our losses after index decreases)against more participation on the upside.Please note that both maximum loss and gain are higher than in question3.11. Question3.13. The following?gure depicts the requested pro?t diagrams.We can see that the aggregation of the bought and sold straddle resembles a bear spread.It is bearish,because we sold the straddle with the smaller strike price. Part1Insurance,Hedging,and Simple Strategies a)b) c) Question3.14. a)This question deals with the option trading strategy known as Box spread.We saw earlier that if we deal with options and the maximum function,it is convenient to split the future values of the index into different regions.Let us name the?nal value of the S&R index S T.We have two strike prices,therefore we will use three regions:One in which S T<950,one in which950≤S T<1,000 and another one in which S T≥1,000.We then look at each region separately,and hope to be able to see that indeed when we aggregate,there is no S&R risk when we look at the aggregate position. Instrument S T<950950≤S T<1,000S T≥1,000 long950call0S T?$950S T?$950 short1000call00$1,000?S T short950put S T?$95000 long1000put$1,000?S T$1,000?S T0 Total$50$50$50 We see that there is no occurrence of the?nal index value in the row labeled total.The option position does not contain S&R price risk. Chapter 3Insurance,Collars,and Other Strategies b)The initial cost is the sum of the long option premia less the premia we receive for the sold options.We have: Cost $120.405?$93.809?$51.77+$74.201=$49.027 c)The payoff of the position after 6months is $50,as we can see from the above table.d)The implicit interest rate of the cash ?ows is:$50.00÷$49.027=1.019~=1.02.The im-plicit interest rate is indeed 2percent. Question 3.15. a)Pro?t diagram of the 1:2950-,1050-strike ratio call spread (the future value of the initial cost of which is calculated as: $120.405?2×$71.802 ×1.02=?$23.66): b)Pro?t diagram of the 2:3950-,1050-strike ratio call spread (the future value of the initial cost of which is calculated as: 2×$120.405?3×$71.802 ×1.02=$25.91. Part1Insurance,Hedging,and Simple Strategies c)We saw that in part a),we were receiving money from our position,and in part b),we had to pay a net option premium to establish the position.This suggests that the true ratio n/m lies between 1:2and2:3. Indeed,we can calculate the ratio n/m as: n×$120.405?m×$71.802=0 ?n×$120.405=m×$71.802 ?n/m=$71.802/$120.405 ?n/m=0.596 which is approximately3:5. Question3.16. A bull spread or a bear spread can never have an initial premium of zero,because we are buying the same number of calls(or puts)that we are selling and the two legs of the bull and bear spreads have different strikes.A zero initial premium would mean that two calls(or puts)with different strikes have the same price—and we know by now that two instruments that have different payoff structures and the same underlying risk cannot have the same price without creating an arbitrage opportunity. A symmetric butter?y spread cannot have a premium of zero because it would violate the convexity condition of options. Chapter3Insurance,Collars,and Other Strategies Question3.17. From the textbook we learn how to calculate the right ratioλ.It is equal to: λ=K3?K2 K3?K1 =1050?1020 1050?950 =0.3 In order to construct the asymmetric butter?y,for every1020-strike call we write,we buyλ950-strike calls and1?λ1050-strike calls.Since we can only buy whole units of calls,we will in this example buy three950-strike and seven1050-strike calls,and sell ten1020-strike calls.The pro?t diagram looks as follows: Question3.18. The following three?gures show the individual legs of each of the three suggested strategies.The last subplot shows the aggregate position.It is evident from the?gures that you can indeed use all the suggested strategies to construct the same butter?y spread.Another method to show the claim of3.18.mathematically would be to establish the equivalence by using the Put-Call-Parity on b) and c)and showing that you can write it in terms of the instruments of a). Part1Insurance,Hedging,and Simple Strategies pro?t diagram part a) pro?t diagram part b) 中国精算师资格考试体系简介 中国精算师资格考试体系简介中国精算师资格考试体系简介建立中国保险精算制度的基本思路是在其保险精算监管系统中实行首席精算师签字的精算报告制度,制度本身包括两个方面的内容:中国精算师认可制度和保险公司的精算报告制度。 1、中国精算师认可制度 认可制度中国保险业的精算师认可制度是实行考试认可制度。考生通过保险监管部门要求的全部课程考试,可取得中国精算师考试合格证书。 纵观世界各国,大体有两种精算师认可制度。一是考试认可制度,即设定一系列考试课,无论什么教育背景,只要通过全部考试,即可获得精算师资格。这以北美精算师协会和英国精算师协会的考试最为典型,属于这种类型的国家有英、美、加、澳、日本等国家。二是学历认可制度,通常在大学设立精算专业,类似于准精算师和精算师水平,分本科和研究生两个阶段,精算专业研究生毕业,即可获得精算师资格。属于这种类型的有德、法、意、瑞士、西班牙、荷兰、巴西、墨西哥等国家。这两种制度也有其共同点,一是对保险公司的指定精算师或首席精算师,除要求精算师资格外,还要求最低的精算专业从业年限,强调精算工作业绩。 中国精算教育始于1988年南开大学招收第一届中美联合培养 的精算研究生,至今,国内已有近20所院校招收精算专业本科生、研究生,精算教育目前还有迅速发展的趋向。但这些院校师资力量、教学水平差别很大,又没有统一的课程设置标准,如采用学历认可制度,很难控制精算师的质量。有鉴于此,借鉴英、美等国经验,建立中国精算师资格考试制度是符合中国现状的。 中国精算师的职业制度基本思路在考试认可制度下,取得精算师考试合格证书仅是精算师职业制度的开端:①取得中国精算师资格证书者,若以精算师名义在商业保险机构执业,还需向中国保监会申请注册,在取得精算师执业证书后,方可执业:②执业的精算师应加入精算师的专业团体中国精算师协会,每年需参加中国精算师协会规定的职业培训,接受其监督管理;③保险公司聘请一名执业精算师作为公司的首席精算师,并报中国保监会备案(首席精算师需经中国保监会的资格审查认可);④首席精算师离职应当报中国保险监督管理委员会备案。保险公司解除其首席精算师的职务,应当向中国保险监督管理委员会陈述理由,并报中国保险监督管理委员会备案。 2、保险公司精算报告制度 配合中国保险业精算监管系统的建立和完善,中国保监会将逐步建立保险公司的精算报告制度。在每一经营年度完了,保险公司除应向保险监管部门提交精算财务报告外,还必须提供由公司首席精算师签署的有关精算报告,其基本内容是(1)提供各项准备金评估时所采用的精算假设、计算方法、并列明各项准备金结果等;(2)公司偿付能力、财务稳定性分析:(3)模拟、测算不同运营环境下,公司现金 Intro-Maths-Fin-1 Financial Derivatives (A Brief Introduction ) Background This chapter deals with the two basic building blocks of financial derivatives: 1. Options 2. Forwards and futures. We briefly introduce the third class of derivative: swap. We see how a complex swap can be decomposed into a number of forwards and options. Definitions Derivatives securities are financial contracts that ‘derive’ their value from cash market instruments such as stocks, bonds, currencies and commodities. At the time of the maturity of the derivative contract, denoted by T , the price F(T) of the derivative asset is completely determined by the market price of the underlying asset (S T ). For instance, the value at maturity (T ) of a long position in a call option of strike (K) written on an asset (S T ) is: Max [S T ?K ;0] Also, the value of time T of a long position in a forward contract of forward price (F) written on an underlying asset worth (S(T) at time T is given by: S (T )?F Types of derivatives We group derivatives into three general headings: 1. Futures, Forwards, Repos, Reverse Repos and Flexible Repos (Basic building blocks ) 2. Options and 3. Swaps Many of these instruments will be discussed in other parts of the syllabus for the QF Exam. The underlying asset : We let (S t ) represent the price of the relevant cash instrument, which we call the underlying asset . The five main groups of underlying asset : We list five main groups of underlying assets: 我用这个秘诀,快速搞定北美精算师考试FM 科目…… 宏景4月传捷报, 北美精算师考试看宏景。 宏景国际教育在北美精算师SOA考试 2018年3月期的Exam FM通过率再创辉煌! 近日,2018年3月的北美精算师考试Exam FM科目考试成绩公布,宏景学员ZHUOFU LI、XIAOFENG YAN、YIDAN CAO、CHONGPU LIU、LAN LIU、JINPENG GAO、JING LIANG等又一批学员在准精算师ASA阶段考试中,Exam FM 考试内容合格。 接下来,让我们来一睹学员Exam FM 考试合格成绩截图(因涉及信息保护,只展示部分学员成绩截图)★ 有点小激动,这是有史以来第一次,我们SOA学员Exam FM考试通过人数最多的一次;这是有史以来我们学员Exam FM科目通过率最高的一次……对,你没有看错!! 这些喜人成绩的取得与宏景国际教育有口碑的SOA教学质量是分不开的。宏景国际教育北美精算师特训营,提供从考试申请、考位预定、课程培训,到牌照申请等一站式服务,让你有更多的时间和精力去准备考试。全职海归组成的教师团队采用单对单教学模式传授SOA考试金牌秘籍;全球最权威、最经典SOA ASM教 材让你的学习事半功倍……在课堂教学和报考服务、工作推荐等工作上形成一套特色体系,使人才培养质量达到更高的水平。 在此,我们对在此次考试中取得优异成绩的学员表示祝贺。同时,希望他们再接再厉,在新的起点上,奋发图强,坚持不懈,争取更大的辉煌。也希望其他学员能够学习总结师兄师姐成功经验、锲而不舍,在自己的SOA考试中取得优秀的成绩。 来源:宏景AICPA 原创分享,转载请联系授权,未经授权禁止转载。文中图片部分来自于网络,版权归原作所有,如有侵权行为请联系删除。 中国精算师资格考试体系简介 建立中国保险精算制度的基本思路是在其保险精算监管系统中实行首席精算师签字的精算报告制度,制度本身包括两个方面的内容:中国精算师认可制度和保险公司的精算报告制度。 1、中国精算师认可制度 认可制度中国保险业的精算师认可制度是实行考试认可制度。考生通过保险监管部门要求的全部课程考试,可取得中国精算师考试合格证书。 纵观世界各国,大体有两种精算师认可制度。一是考试认可制度,即设定一系列考试课,无论什么教育背景,只要通过全部考试,即可获得精算师资格。这以北美精算师协会和英国精算师协会的考试最为典型,属于这种类型的国家有英、美、加、澳、日本等国家。二是学历认可制度,通常在大学设立精算专业,类似于准精算师和精算师水平,分本科和研究生两个阶段,精算专业研究生毕业,即可获得精算师资格。属于这种类型的有德、法、意、瑞士、西班牙、荷兰、巴西、墨西哥等国家。这两种制度也有其共同点,一是对保险公司的指定精算师或首席精算师,除要求精算师资格外,还要求最低的精算专业从业年限,强调精算工作业绩。 中国精算教育始于1988年南开大学招收第一届中美联合培养的精算研究生,至今,国内已有近20所院校招收精算专业本科生、研究生,精算教育目前还有迅速发展的趋向。但这些院校师资力量、教学水平差别很大,又没有统一的课程设置标准,如采用学历认可制度,很难控制精算师的质量。有鉴于此,借鉴英、美等国经验,建立中国精算师资格考试制度是符合中国现状的。 中国精算师的职业制度基本思路在考试认可制度下,取得精算师考试合格证书仅是精算师职业制度的开端:①取得中国精算师资格证书者,若以精算师名义在商业保险机构执业,还需向中国保监会申请注册,在取得精算师执业证书后,方可执业:②执业的精算师应加入精算师的专业团体中国精算师协会,每年需参加中国精算师协会规定的职业培训,接受其监督管理;③保险公司聘请一名执业精算师作为公司的首席精算师,并报中国保监会备案 (首席精算师需经中国保监会的资格审查认可);④首席精算师离职应当报中国保险监督管理委员 第一篇:利息理论 第一章:利息的基本概念 t t 0 n t 0'()=()()()(0)1)(dr a t a t a t e A n dt A n A δδδ?==-? ???????? ?、有关利息力: ()() 11(1)1(1)(1)2m p m p i d i v d e m p δ ---+=+==-=-=、 =131 t t i it d id δδ? ??+??=?-? 、但贴单利率下的利息力::现下的利息力 4?? ??? 严格单利法(英国法) 投资期的确定常规单利法(欧洲大陆法)银行家规则(欧洲货币法)、 1 1 n k k k n k k s t t s - === ∑∑5、等时间法: 第二章 年金 .... 1.... 1+i 11+i 1n n n n n n n n a a a a s s s s -+? ==+???==-? (1) 、(1) ...... 2m n m n m m n m n m v a a a v a a a ++?=-???=-?、 3、零头付款问题:(1)上浮式(2)常规(3)扣减式 4:变利率年金(1)各付款期间段的利率不同 (2)各付款所依据的利率不同 5、付款频率与计息频率不同的年金 (1)付款频率低于计息频率的年金 : 1.......1........n k n k k n k n k k a s s is s a a s ia a ?????? ???????? ? ?? ????? ??????? 现值期末付年金:永续年金现值:终值:现值:期初付年金:永续年金现值:终值: (2)付款频率高于计息频率的年金 ()()()()()()..() ()()..()1:1.......(1)1 11........(1)1n m m n m n m m n m n n m m m n n m v a i i i i v a d d i s i ??-=??????+-?=????? ?-?=?????+-??=???? 现值期末付年金:永续年金现值:终值:s 现值:期初付年金:永续年金现值:终值: (3)连续年金(注意:与永续年金的区别) 00 1(1)1(1)n n t n n n n t n v a v dt i s i dt δδ---?-==???+-?=+=???? 一、国内精算专业的发展现状 精算起源于英国,若从1693年哈雷设计出第一张生命表算起,精算学在西方已经有三百多年的历史。英国的精算师协会是第一个精算师职业组织,距今已有150多年的历史,然而现在规模最大,拥有最多精算师会员的组织却是美国的北美精算师协会。大多数保险业比较发达的国家都有自己的精算职业和职业组织,一些保险业相对落后的国家也都纷纷在努力建立自己的精算职业,这是应经济发展尤其是金融保险业发展的迫切需要而产生的。 作为一名合格称职的精算师不仅要有扎实的数理基础,而且还要精通投资、统计、税务、财会、金融、管理、法律、计算机、外语等方面的专业知识,因此,精算师的成才,往往需要很长的一段时间。根据国外的经验,培养一个合格的精算师通常需要6-8年的时间。在我国,由于保险业的发展尚处于起步阶段,精算师的培养通常需要更长的时间。 1980年我国保险业恢复营业以来,直至1987年11月南开大学与北美精算学会(Society of Actuaries,SoA)签订精算教育合作协议,并在1988年秋招收了国内首届精算研究生(三年制),设立了我国第一个外国(北美)精算学会的考试中心,并于1992年秋季首次举行SoA考试。这标志着中国高校精算专业系统教育的正式起步。 从某种意义上讲,中国系统的精算教育是从高校的学历教育开始的,而且是从较高的硕士学历教育开始,同时,由于也伴随着建立了高校内的职业资格考试中心,所以也可以看作在中国形成精算行业的 一种开端。从这个意义上讲,中国的精算行业是从高等教育开始的。也正是因为这一点,为中国的精算行业打上了一种烙印:一方面,具有较高的技术起点、队伍年轻、与国际接轨和学科先进整齐的特点;另一方面,也在很大程度上与现实的保险行业或公司经营有距离,实务经验不足,与中国保险业的迅速发展并不是非常匹配。 无论怎样,中国的高校精算教育已有了35年以上的历史,高等学校和外界都付出了很多的努力,培养的学生已成为目前中国精算实务队伍中的主力和骨干。 进入上个世纪90年代以后,国际上金融业尤其是保险行业出现了更迅猛的发展,而且还出现了相互渗透和融合的趋势,金融投资领域中数学方法有了深入和广泛的应用,这些都引起了国际上精算考试教育的多次大的变革,而且这种变革还在进行中。目前中国精算师队伍的主要来源还是高等院校,所以,高等教育中精算专业的学历教育对我国精算职业的健康发展,乃至保险行业的整体发展都是相当重要的。 继南开大学之后,后来又陆续有湖南大学、复旦大学、中央财经大学等多所高校引进了精算教育,开设了精算相关方向或课程。与此同时,精算考试与认证也日渐完善,目前全国已成立了11个北美寿险精算师考试中心(分别设立于南开大学、湖大大学、复旦大学、人 北美精算师ASA如何申请 1.哪些人适合申请精算? 这里所说的适合包含两层含义,一层是自己觉得适合,另一层是自己具备一定条件有把握收到ADMISSION或OFFER. 先说第一层,何为自己觉得适合?这里需要考虑几个问题。第一个问题是你选择专业的指导思想是什么?兴趣,热门,高薪……? 如果你选的是第一个答案那你继续往下看。第二个问题是你是否对数学感兴趣,你是否有很强的分析能力和business sense, 你是否愿意一辈子和模型打交道?这个问题的思考不仅有助于你的PS写作,而且对你今后的CAREER有指导意义,因为有些人选了精算专业,工作后才发现虽然年薪很高,可是自己事业上却有点力不从心。 第二层,你申请的胜算有多少? 首先,我们把申请人群作个区分。申请人大致可分为在中国的和在美国的。这个区分相当重要,因为他们的录取机会相差很大。明确了自己属于哪个申请群,你就知道自己的竞争对手和应该怎样使你的申请材料超越对手。 如果你在美国,那恭喜你。只要你有足够的MONEY,录取不是件很难的事。不管你以前是学什么专业的,你都有机会被录取。 计算机,机械,环境,英语,文学,教育……NO PROBLEM! 美国的高等教育很普及,大学只要你有钱都能上。有些人可能想不通,为 什么念英语的也能念精算?但是,这就是事实。在这念精算的中国人很多,背景五花八门,不过大家都念得很好。 如果你在中国,那也恭喜你,因为你受到了挑战。人生有什么比受到挑战更快乐的了?它使你超越别人和自我。拿破仑说过:我感谢困难,因为它像篱笆,把不如我的都挡在了后面。 挑战之一来自你的专业,因为你属于这个申请群,所以你的专业必须和精算有联系。这包括数学,统计,金融(保险,投资,银行),会计等等。 挑战之二来自你的背景。因为国内的申请人数庞大,所以你必须脱颖而出。你的竞争对手很强,你必须比他们更强。 挑战之三来自你的签证。美国签证很难,精算签证尤胜。 看到这有些人垂头丧气,有些人手舞足蹈。前者对生活抱悲观态度,后者则用乐观向上的精神指引人生。你属于哪种?你希望自己是哪种?要不要改变?申请的过程是痛苦的,每个人都会有软弱的时候,你必须有一个强大的精神支柱! 2、材料的准备 所有申请材料中两样东西最重要,成绩单和PS。成绩单是死的,PS是活的。 如果你是大一大二或者大三,那你的成绩单也是活的,趁着在校多修修很精算有关的课程。 以下着重阐述PS写作。 Financial Mathematics Exam—December 2015 The Financial Mathematics exam is three-hour exam that consists of 35 multiple-choice questions and is administered as a computer-based test. For additional details, please refer to Exam Rules The goal of the syllabus for this examination is to provide an understanding of the fundamental concepts of financial mathematics, and how those concepts are applied in calculating present and accumulated values for various streams of cash flows as a basis for future use in: reserving, valuation, pricing, asset/liability management, investment income, capital budgeting, and valuing contingent cash flows. The candidate will also be given an introduction to financial instruments, including derivatives, and the concept of no-arbitrage as it relates to financial mathematics. The Financial Mathematics Exam assumes a basic knowledge of calculus and an introductory knowledge of probability. The following learning objectives are presented with the understanding that candidates are allowed to use specified calculators on the exam. The education and examination of candidates reflects that fact. In particular, such calculators eliminate the need for candidates to learn and be examined on certain mathematical methods of approximation. Please check the Updates section on this exam's home page for any changes to the exam or syllabus. Each multiple-choice problem includes five answer choices identified by the letters A, B, C, D, and E, only one of which is correct. Candidates must indicate responses to each question on the computer. Candidates will be given three hours to complete the exam. As part of the computer-based testing process, a few pilot questions will be randomly placed in the exam (paper and pencil and computer-based forms). These pilot questions are included to judge their effectiveness for future exams, but they will NOT be used in the scoring of this exam. All other questions will be considered in the scoring. All unanswered questions are scored incorrect. Therefore, candidates should answer every question on the exam. There is no set requirement for the distribution of correct answers for the multiple-choice preliminary examinations. It is possible that a particular answer choice could appear many times on an examination or not at all. Candidates are advised to answer each question to the best of their ability, independently from how they have answered other questions on the examination. Since the CBT exam will be offered over a period of a few days, each candidate will receive a test form composed of questions selected from a pool of questions. Statistical scaling methods are used to ensure within reasonable and practical limits that, during the same testing period of a few days, all forms of the test are comparable in content and passing criteria. The methodology that has been adopted is used by many credentialing programs that give multiple forms of an exam. The ranges of weights shown in the Learning Objectives below are intended to apply to the large majority of exams administered. On occasion, the weights of topics on an individual exam may fall outside the published range. Candidates should also recognize that some questions may cover multiple learning objectives. 关于北美精算师,你必须知道的入门级知识——Exam P 成为一名北美准精算师(ASA)必须要经历五门SOA的准精算师考试,而其中最简单也是大部分人最先开始学习准备的就是Exam P,即probability。顾名思义,Exam P考察的就是最基本的数理统计与概率问题。下面我们就来了解一下Exam P的考试形式与内容。 考试目的 考生可以掌握用于定量评估风险的基本的概率方法,并着重于用这些方法应用解决精算学中遇到的问题。参加这门考试的考生应具有一定的微积分基础,并了解基本的概率、保险和风险管理的概念。 考试形式 Exam P采用机考的形式,总共30道单项选择题,考试时间为3个小时。每道选择题共有5个选项,其中只有一个正确选项。 与SAT考试不同的是,Exam P考试答错并不会额外扣分,也就是说考生一定不要空任何一道题。Exam P中会随机分布几道“pilot question”,这些题目是主办方用来分析从而改进将来的考试而出现的,它们的正确与否并不会影响到考生的实际分数。但是由于考生并无法分辨出这些题目,所以对每一道题目,考生都要同样认真地对待。 考试内容 概率(占总分10%-20%) 最基本的事件概率计算问题。包括集合方程与表示(sat functions)、互斥事件(mutually exclusive events)、事件独立性(independence of events)、组合概率(Combinatorial probability)、条件概率(Conditional probability)以及贝叶斯定理(Bayes theorem)等。 拥有单因素概率分布的随机变量(占总分35%-45%) 连续分布或离散分布的单因素随机变量的研究。包括PDF&CDF(Probability density functions and Cumulative distribution functions)、独立随机事件的和的分布、众数(Mode)、中位数(Median)、百分位数(Percentile)、动差(Moment)、方差(Variance)以及变形等问题。 拥有多因素概率分布的随机变量(占总分35%-45%) 包括联合PDF&CDF、中心极限定理(central limit theorem)、条件与边缘概率分布与动差(Conditional and marginal probability distributions and moments)、条件与边缘概率分布的方差、协方差与概率系数(Covariance and correlation coefficients)以及变换与顺序统计(Transformation and order statistics)等。 提醒:众所周知,2018年7月1日起,SOA新课程体系将正式生效,其中Exam P科目不变,考试大纲有变动,具体有那些变化???后台回复“Exam P”免费获取Exam P最新考试大纲。 考试时间 November 2001 Course 2 Interest Theory, Economics and Finance Society of Actuaries/Casualty Actuarial Society 1.Ernie makes deposits of 100 at time 0, and X at time 3 . The fund grows at a force of interest 2 100 t t δ=, t > 0 . The amount of interest earned from time 3 to time 6 is X. Calculate X. (A)385 (B)485 (C)585 (D)685 (E)785 2.The production of a good requires two inputs, labor and capital. At its current level of daily output, a competitive firm employs 100 machine hours of capital and 200 labor hours. The marginal product of machine hours is 10 units. The marginal product of labor hours is 5 units. The rental rate, or “price,” of capital is 20 per machine hour. If the firm minimizes its costs, what is the hourly wage rate? (A) 2.5 (B) 5.0 (C)10.0 (D)20.0 (E)40.0 精算学大学排名及专业介绍 一精算业 精算是依据经济学的基本原理,利用现代数学方法,对各种经济活动未来的财务风险进行分析、估价和管理的一门综合性的应用科学。精算方法和精算技术是现代保险、金融、投资科学管理的有效工具。其一直是被广泛应用于保险及其它金融行业、寿险业务、年金市场、财务运营、资金运作和预测未来等多个领域甚至退休保障等社会福利中。从社会保障标准的计算、财政收支计划的测算以及投资活动的分析,到人寿保险业中对于人生老病死等随机事件的把握,都离不开精算师周密、科学的分析和运算。 二精算师 精算师(Actuary,拉丁语意思"经营")是一种处理金融风险的商业性职业,是运用精算方法和技术解决经济问题的专业人士,是评估经济活动未来财务风险的专家。精算师更被国际社会形象地比喻为协调和平衡社会经济运作的"第一小提琴手"。 精算师采用数学、经济、财政和统计工具,在商业保险业,投资和经济预测领域从事产品开发、责任准备金核算、利源分析及动态偿付能力测试等重要工作,确保保险监管机关的监管决策、保险公司的经营决策建立在科学基础之上和为保险公司作风险评估及制定投资方针,并定期作出检讨及跟进。 精算师也会在咨询公司(主要的客户是规模较细的保险公司及银行)、养老金投资公司、医疗保险公司及投资公司工作。 三成为精算师的条件 要想成为精算师,首先必需掌握一些基础课程,如微积分、线性代数、概率论与数理统计、保险学和风险管理等。不仅如此,由于精算师所从事的是经济领域的职业,因而他们还必需有较高的经济学修养,掌握会计、金融、经济学和计算机等科学。这样,精算师才能对经济环境的变化有较强的反应能力。此外,精算师的职业还要求掌握语言表达、商业写作、哲学等科学知识取得精算师资格必需通过一些科目的严格考试,并获得精算组织的认可。例如,在美国和加拿大,作为一名合格的精算师,必需取得美国灾害保险精算学会 (Casuality Actuarial Society)或北美精算学会(Society of Actuaries) 的正式会员资格。北美精算学会是在人寿保险、健康保险和年金保险领域从事研究、考试和接受会员的国际组织,它负责从吸收非正式会员到正式会员的一系列考试。 四精算师的职业优势 1. 有较高的社会地位. 精算师是一份有着重要作用的职业,有时甚至是公司发展的关键所在.有着较高的社会地位.有人说,按英国标准来讲,中国只有两个精算师,而按美国精算师学会的名单,中国尚不存在一个合格的精算师。 2. 职业空缺 金融行业简介 一、行业简介 定义:简单来说,金融就是资金的融通。金融是货币流通和信用活动以及与之相联系的经济活动的总称,广义的金融泛指一切与信用货币的发行、保管、兑换、结算,融通有关的经济活动,甚至包括金银的买卖,狭义的金融专指信用货币的融通。 核心:金融的核心是跨时间、跨空间的价值交换,所有涉及到价值或者收入在不同时间、不同空间之间进行配置的交易都是金融交易,金融学就是研究跨时间、跨空间的价值交换为什么会出现、如何发生、怎样发展,等等。 金融在国民经济中具有举足轻重的地位和作用,是社会资金运动的中枢神经系统。现代市场经济条件下,以货币流通和社会信用总和为内容的金融在社会资金的筹措和分配中所占的比重越来越大。因此,金融作为一国社会资金流通系统的基本组成部分,对经济的增长和发展起着十分重要的调节控制作用。 金融的构成要素有5点: 1、金融对象:货币(资金)。由货币制度所规范的货币流通具有垫支性、周转性和增值性。 2、金融方式:以借贷为主的信用方式为代表。金融市场上交易的对象,一般是信用关系的书面证明、债权债务的契约文书等,包括直接融资:无中介机构介入;间接融资:通过中介结构的媒介作用来实现的金融 3、金融机构:通常区分为银行和非银行金融机构 4、金融场所:即金融市场,包括资本市场、货币市场、外汇市场,保险市场,衍生性金融工具市场,等等; 5、制度和调控机制:对金融活动进行监督和调控等。 各要素间关系:金融活动一般以信用工具为载体,并通过信用工具的交易,在金融市场中发挥作用来实现货币资金使用权的转移,金融制度和调控机制在其中发挥监督和调控作用。 二、金融机构 金融机构,是指专门从事货币信用活动的中介组织。我国的金融机构,按地位和功能可分为四大类: 第一类,中央银行,即中国人民银行。 第二类,银行。包括政策性银行、商业银行。 北美精算师考试内容及考试制度 北美精算师考试内容及考试制度北美精算师考试内容及考试制度 北美精算师考试制度分为二个阶段:第一阶段是准精算师(asa)。目前对准精算师的考试要求为300学分。除了100系列的11门课程(复利数学、精算数学等)外,还须通过200系列的4门课程(经济保障计划、精算实务等)。每门课在10至30学分不等。 学员在获得300学分后即成为asa,之后可继续考fsa课程。asal00系列的11门课程的考试均采用英文试卷,选择题形式,考试时间分别为1个半小时至4个小时不等;200系列采用英语书写答题形式。考生是否通过某一门课程考试以及所获得的分数,是到该课程全部试卷批完后,按成绩顺序排列后确定的。 第二阶段是精算师(fsa)。考生在取得准精算师资格证书后方可参加fsa课程考试。目前把精算师的考试课程分为财务、团体与健康保险、个人人寿与健康保险、养老金、投资五个方向,每个方向又分若干门课,每门课学分在10至30分不等。要取得fsa资格必须通过以上一个方向的所有课程考试,以及再选择以上方向的其他课程,使学分达到150分,即学分总计要达到450分。当fsa要素的课程考试全部通过后,考生还要参加最后一门课程:正式精算师认可课程(fac),其内容主要是职业道德和案例,时间为二天 半,一般只要自始至终参加,在结束后的晚宴上会获得fsa证书。 北美精算师协会的考点分布在全世界各个国家和地区,考试每年5月和11月举行两次,考试时间由北美精算师协会确定,世界各地统一,考卷由北美精算师协会提供。 报名及考试地点:南开大学、湖南财经学院、复旦大学、中国人民大学、中山大学、中国科技大学、陕西财经学院、平安总公司北美精算学会考试课程 准精算师考试: 100系列课程:100微积分和线性代数、110概率论和数理统计、120应用统计、130运筹学、135数值分析、140复利数学、150精算数学、151风险理论、160生存模型和生命表编制、161人口数学、165匀修数学 200系列课程:200经济保障计划概论、210精算实务概论、220资产管理和公司财务概论、230资产和负债管理原理正精算师的考试课程分为五个方向: 一财务包括科目:财务管理、公司财务等 二团体和健康保险包括科目:团体和个人健康保险的设计和销售等 三个人人寿和年金保险包括科目:个人人寿和年金保险的精算实务调查、人寿保险法和税收等 四养老金包括科目:养老金估价原理i、退休计划设计等 SAMPLE SOLUTIONS FOR DERIVATIVES MARKETS Question #1 Answer is D If the call is at-the-money, the put option with the same cost will have a higher strike price. A purchased collar requires that the put have a lower strike price. (Page 76) Question #2 Answer is C 66.59 – 18.64 = 500 – K exp(–0.06) for K = 480 (Page 69) Question #3 Answer is D The accumulated cost of the hedge is (84.30-74.80)exp(.06) = 10.09. Let x be the market price. If x < 0.12 the put is in the money and the payoff is 10,000(0.12 – x) = 1,200 – 10,000x. The sale of the jalapenos has a payoff of 10,000x – 1,000 for a profit of 1,200 – 10,000x + 10,000x – 1,000 – 10.09 = 190. From 0.12 to 0.14 neither option has a payoff and the profit is 10,000x – 1,000 – 10.09 = 10,000x – 1,010. If x >0.14 the call is in the money and the payoff is –10,000(x – 0.14) = 1,400 – 10,000x. The profit is 1,400 – 10,000x + 10,000x – 1,000 – 10.09 = 390. The range is 190 to 390. (Pages 33-41) Question #4 Answer is B The present value of the forward prices is 10,000(3.89)/1.06 + 15,000(4.11)/1.0652 + 20,000(4.16)/1.073 = 158,968. Any sequence of payments with that present value is acceptable. All but B have that value. (Page 248) Question #5 Answer is E Models for Financial Economics—April 2012 The Models for Financial Economics is called Exam MFE by the SOA and Exam 3F by the CAS. This three-hour exam consist of 30 multiple-choice questions. Also, a normal distribution calculator will be available during the test by clicking a link on the item screen. Details are available on the Prometric Web Site. The examination is jointly sponsored and administered by the SOA, CAS, and the Canadian Institute of Actuaries (CIA). The examination is also jointly sponsored by the American Academy of Actuaries (AAA) and the Conference of Consulting Actuaries (CCA). The purpose of the syllabus is to develop the candidate’s knowledge of the theoretical basis of certain actuarial models and the application of those models to insurance and other financial risks. A thorough knowledge of calculus, probability, interest theory and the earlier chapters of the McDonald textbook (which are in the syllabus of Exam FM/2) is assumed. Formulas are provided for the density and distribution functions for the standard normal and lognormal random variables. For paper and pencil examinations, tables of the standard normal distribution function are provided. Since the tables will be provided to the candidate at the examination, candidates will not be allowed to bring copies of the tables into the examination room. For CBT candidates, a normal distribution calculator is provided. See the link below for more information. Note: It is anticipated that candidates will have done the relevant exercises in the textbooks. Check the Updates section of the web site for any changes to the exam or syllabus. The ranges of weights shown are intended to apply to the large majority of exams administered. On occasion, the weights of topics on an individual exam may fall outside the published range. Candidates should also recognize that some questions may cover multiple learning outcomes. Each multiple-choice problem includes five answer choices identified by the letters A, B, C, D, and E, only one of which is correct. Candidates must indicate responses to each question on the computer. As part of the computer-based testing process, a few pilot questions will be randomly placed in the exam (paper and pencil and computer-based forms). These pilot questions are included to judge their effectiveness for future exams, but they will NOT be used in the scoring of this exam. All other questions will be considered in the scoring. All unanswered questions are scored incorrect. Therefore, candidates should answer every question on the exam. There is no set requirement for the distribution of correct answers for the SOA/CAS/CIA multiple-choice preliminary examinations. It is possible that a particular answer choice could appear many times on an examination or not at all. Candidates are advised to answer each question to the best of their ability, independently from how they have answered other questions on the examination. Since the CBT exam will be offered over a period of a few days, each candidate will receive a test form composed of questions selected from a pool of questions. Statistical scaling methods are used to ensure within reasonable and practical limits that, during the same testing period of a few days, all forms of the test are comparable in content and passing中国精算师资格考试体系简介

PAK Study Manual QF-北美精算师(QFIQF)

【SOA】我用这个秘诀,快速搞定美国精算师FM考试

中国精算师资格考试体系简介

精算师考试金融数学课本知识精粹

中国精算师考试体系及课程讲解

北美精算师ASA如何申请

北美精算师考试官方样题2015-12-exam-fm-syllabus

【SOA】关于北美精算师,你必须知道的入门级知识——Exam P

北美精算师(SOA)考试 FM 2001 November 年真题

精算学大学排名及专业介绍

金融行业简介

北美精算师考试内容及考试制度

09年SOA北美精算师考试第二门FM官方样题第一部分(主要是金融数学)答案

北美精算师(SOA)考试MFE 2012年4月课程大纲

相关主题

文本预览