A LITERATURE A ALYSIS O BUSI ESS PERFORMA CE FOR SMES –

SUBJECTIVE OR OBJECTIVE MEASURES?

Siti Nur ‘Atikah Zulkiffli a and Nelson Perera b

This paper has been double-blind peer reviewed by an international panel of SIBR

Abstract

The study examines the basic research methodologies and approaches for assessing

business performance. It provides a critical literature analysis on how perception-

based evaluation can be used to evaluate performance, specifically for SMEs. The

analysis of the literature covers articles from major journals related to the topic. The

methodology followed during the conduct of this paper involves starting with the

broad case of articles in general business performance measurement, then focusing

on the indicators used to study SMEs. Next, the review screens the list, focusing on

the differences between subjective and objective measures. The validity issue

related to subjective measures is also discussed.

Key words: business performance, subjective measures, objective measures, small

and medium enterprises.

I.Introduction

Measuring business performance in today’s economic environment is a critical issue for academic scholars and practising managers. In general, business performance is defined as “the operational ability to satisfy the desires of the company’s major shareholders” (Smith & Reece, 1999, p. 153), and it must be assessed to measure an organisation’s accomplishment. Many studies examine the relationship of organisational practice and processes to affect the “bottom line”, and vice versa (Wall et al., 2004). Attempts to examine the relationship between strategy and performance have been made for more than 20 years; many current studies also focus on this aspect. Scholars have examined the importance of performance evaluation and practices for an organisation (Dess & Robinson, 1984; Sapienza et al., 1988; McGrath et al., 1995; Song et al., 2005; Gruber et al., 2010). Much research also focuses on the performance of small firms and, more recently, medium firms as well (Pelham & Wilson, 1996; Jarvis et al., 2000; Alasadi & Abdelrahim, 2008; Thomas et al., 2008).

Regular indicators used in measuring business performance are profit, return on investment (ROI), turnover or number of customers (Wood, 2006), design quality and product improvement (Laura et al., 1996). However, Mann and Kehoe (1994) and Franco-Santos et al. (2007) recommend measuring business performance through the business performance measurement (BPM) system, as it is an important tool within many research a Corresponding author. University of Wollongong, Australia and Universiti Malaysia Terengganu, Malaysia. email: snaz167@https://www.doczj.com/doc/4016506263.html,.au.

b University of Wollongong, Australia. email: nperera@https://www.doczj.com/doc/4016506263.html,.au

Page | 1

areas, particularly in business and social science studies. This system analyses and investigates each quality that affects a firm’s business performance, categorising business performance into two broad areas: operational business performance (OBP) and strategic business performance (SBP).The major function of the system is to focus on investigating all an organisation’s functions at high and low levels of activity (Mann & Kehoe, 1994); it is appropriately applied to measuring the performance of small and medium enterprises (SMEs). This system is also appropriate for both quantitative (for example, questionnaires) and qualitative (for example, structured interview) research methods.

SMEs are often very reluctant to publicly reveal their actual financial performance, and scholars have deliberated on the need for subjective measures (for example, the seven-point Likert scale in empirical research) in evaluating business performance. It is important to consider the aspects of differentiation that may be potentially confounded between subjective (also described as perceived/perception performance) and objective measures. Thus, this paper aims to analyse the related literature on how perception-based evaluation can be used to evaluate SMEs’ performance.

The rest of this paper is organised as follows: Section 2 describes the review methodology, Section 3 discusses subjective and objective performance measures, Section 4 deliberates the validity of subjective performance measures and Section 5 concludes and suggests the future research directions.

II.Review Methodology

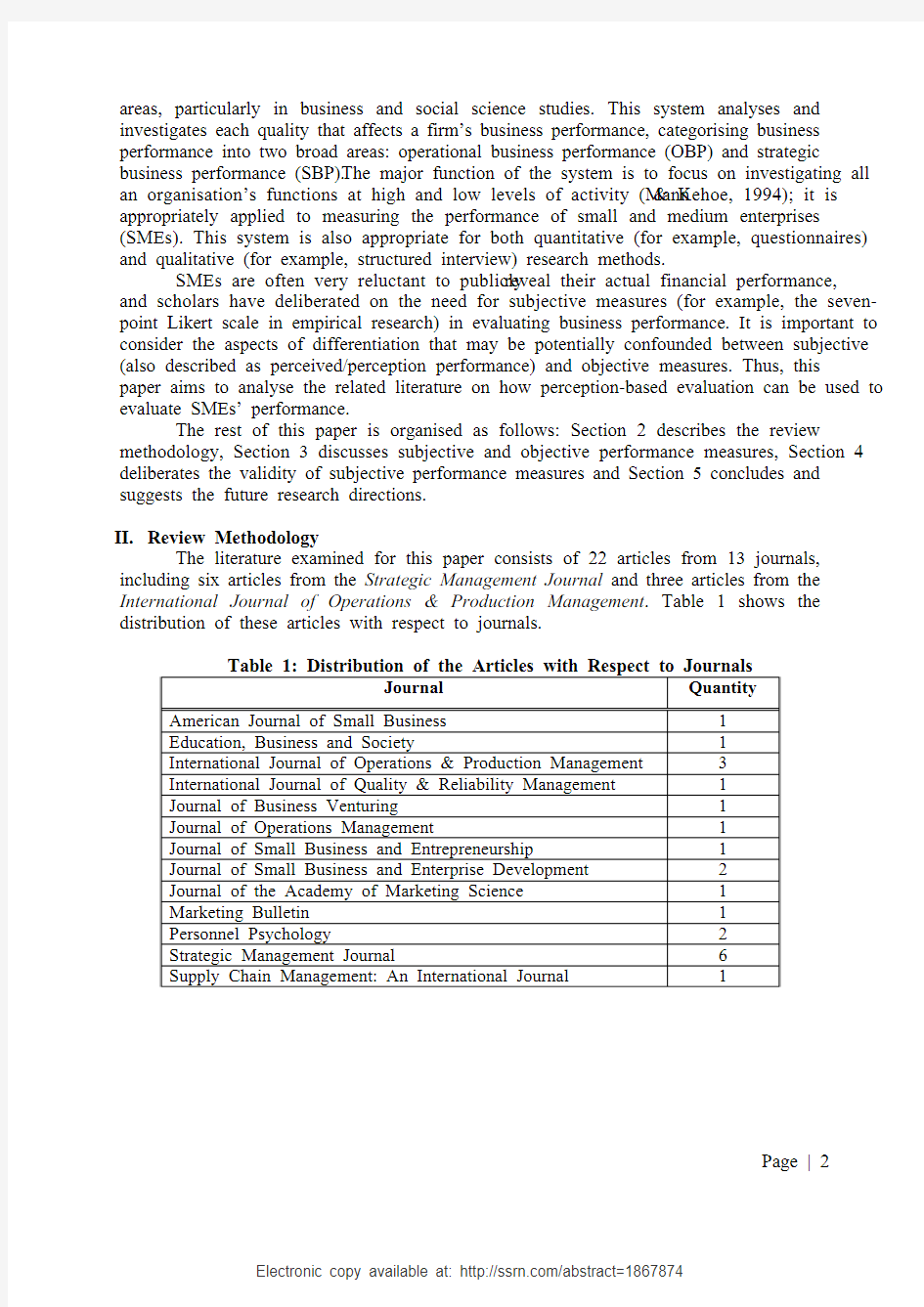

The literature examined for this paper consists of 22 articles from 13 journals, including six articles from the Strategic Management Journal and three articles from the International Journal of Operations & Production Management. Table 1 shows the distribution of these articles with respect to journals.

Table 1: Distribution of the Articles with Respect to Journals

Journal Quantity American Journal of Small Business 1

Education, Business and Society 1

International Journal of Operations & Production Management 3

International Journal of Quality & Reliability Management 1

Journal of Business Venturing 1

Journal of Operations Management 1

Journal of Small Business and Entrepreneurship 1

Journal of Small Business and Enterprise Development 2

Journal of the Academy of Marketing Science 1

Marketing Bulletin 1

Personnel Psychology 2

Strategic Management Journal 6

Supply Chain Management: An International Journal 1

Page | 2

III.Subjective and Objective Performance Measures

Many studies show a preference for subjective measures during the assessment of business performance due to difficulties in obtaining objective financial data. Managers often refuse to provide accurate, objective performance data to researchers. Even if objective data is made available, the data often do not fully represent firms’ actual performance, as managers may manipulate the data to avoid personal or corporate taxes (Dess & Robinson, 1984; Sapienza et al., 1988). Research on SMEs is particularly susceptible to these difficulties, although difficulties can also occur when the research examines business units of multi-industry and privately held firms (Dess & Robinson, 1984).

Consequently, managers are often encouraged to evaluate business performance through general subjective measures that can reflect more-specific objective measures (Wall et al., 2004). Subjective measures can be an effective way to examine business performance, as they allow comparison across firms and contexts, such as industry type, time horizons, cultures or economic conditions (Song et al., 2005). When subjective measures are employed, managers can use the relative performance of their industry as a benchmark when providing a response (Dawes, 1999). Objective performance measures, in contrast, can vary based on industry and can obscure the relationship between independent variables and business performance (as a dependent variable) (Dawes, 1999).

Moreover, the objective data available to the researcher may not be compatible with the intended level of analysis (Wall et al., 2004); in these cases, subjective data can be a good alternative if the measures focus on the firm’s current condition (for example, Kim, 2006a; Kim, 2006b).

It is legal for small firms’ managers to manipulate some data, and to control such manipulation through subjectively adjusting measures (Sapienza et al., 1988). Moreover, many managers of small and private firms consider objective performance measures to be confidential, and guard them from public scrutiny (Sapienza et al., 1988; Gruber et al., 2010). Such managers tend to have a low level of awareness about the desirability of providing accurate and reliable data and feedback to researchers. Therefore, researchers are advised to develop subjective measures, as these provide more complete information (Covin & Slevin, 1989).

Another issue in researching small firms is the difficulty of interpreting some objective performance data. For example, performance may be considered as “poor” if the data shows losses or low profit. Such misinterpretation can occur if, for example, firms have many commitments to research and development (R&D), including product and market development for future growth (Covin & Slevin, 1989). These misinterpretations may be due to variations in profitability data and may lead to the comparison of objective measures among small firms in different industries (Covin & Slevin, 1989; Dawes, 1999). To avoid these sorts of issues, researchers have used subjective measures and focused on firms within the same industry (for example, manufacturing) (Appendix A).

Table 2 outlines some differences between subjective and objective performance measures.

Page | 3

Table 2: Differences between Subjective and Objective Measure in Business

Performance

Differentiation

Aspect

Subjective Measures Objective Measures Indicators ?Focus on overall performance ?Focus on actual financial

indicators

Measurement standard ?Key informants are asked to

rate performance relative to

their competitors (and/or

industry)

?Key informants should provide

absolute financial data (for

example, AUD profit per

employee)

Scale anchors ?Scales range from “very poor”

to “very good”, or “much

lower” to “much higher”, or

“worst in industry” to “best in

industry” etc.

?Scales are not used

IV.The Validity of Subjective Performance Measures

Subjective measurements are strongly correlated with objective measurements in terms of absolute changes in return on assets and sales over the same time period; for example, the correlation (r) of objective and subjective measures to total sales gives a value for r of .80, and to return on assets gives a value of .79 (Dess & Robinson, 1984). These findings support the validity of performance evaluation through subjective measures.

However, less attention has been given to evaluating the validity of subjective performance measurement. Such measurements, which are subject to potential measurement errors and bias, have been examined using several types of validity tests (Chandler & Hanks, 1993; Wall et al., 2004). Three validity tests – convergent, discriminant and construct – have been used to show that subjective measurement is significantly reliable as an alternative to objective measurement in business performance.

Table 3 shows the result of validity tests related to subjective measurement in business performance.

Table 3: Results of Different Validity Tests to Measure Business Performance

Validity Type Results

Convergent ?Subjective performance measures are related to objective

measures.

Discriminant ?Relationships between subjective and objective measures are

systematically stronger than relationships between different

performance constructs measured using the same method (either

subjective or objective).

Construct ?Relationships between subjective and objective performance

measures with a series of independent variables are equivalent.

?Subjective performance measurement has a statistically significant

correlation with objective measurement (p < .01).

?Subjective measurement shows a 95% success rate as compared

with objective measurement.

Source: Adapted from Wall et al. (2004)

Page | 4

The findings of Wall et al. (2004) support the earlier studies that discuss the validation of performance measurement (Hoffman et al., 1991; Chandler & Hanks, 1993). Chandler and Hanks’s 1993 study – supported by Lee et al. (2001) – discussed the validation issues for another three measurement aspects: broadly defined categories, managers’ satisfaction with performance and firm performance relative to competitors. Results showed a high level of correlation between objective and subjective measures, as well as suggesting strong inter-rater reliability (Lee et al., 2001).

Table 4 shows the results of comparison between performance measures that can be used in related studies.

Table 4: Summary Comparison of Performance Measures

Broadly Defined Categories Performance

Relative to

Competitors

Satisfaction

with Performance

Growth Business

Volume

Relevance Very Good Very Good Very Good Unknown

Availability Very Good Very Good Acceptable Very Good

Internal Consistency Good Very Good Very Good Good

Inter-rater Reliability Good Very Good Marginal Acceptable

External Validity Very Good Very Good Very Good Inadequate Source: Chandler and Hanks (1993)

The table shows that broadly defined categories and performance relative to competitors are still useful. However, Chandler and Hanks (1993, p. 400) explain that, “... in reference to the ‘performance relative to competitors’ scale, several respondents who did not disclose performance relative to competitors’ information pencilled in that they had no basis for comparison because they did not know how their competitors were performing”. This suggests that examination of performance relative to competitors should be focused on the entire industry to assess “generalisability”, as some respondents may not know much about their competitors’ performance.

V.Conclusions and Future Research Directions

Examination of the literature on this topic offers guidance in how the various business performance measures in an SME can be organised, interfaced and managed. The literature suggests that subjective evaluations are appropriate alternatives to objective measurement.

It is difficult for researchers to accurately estimate performance, particularly when using mailed questionnaires, as the data will be subject to measurement errors caused by the confidential nature of the data and variance in accounting procedures among participating firms (Dess & Robinson, 1984). Also, managers do prefer to provide such data subjectively to protect confidentiality (Song et al., 2005).

The literature also shows that the evaluation of subjective perceptions is commonly and comprehensively used in social-science research (Pelham & Wilson, 1996; Kim, 2006b; Yong et al., 2007; Alasadi & Abdelrahim, 2008; Gruber et al., 2010); the use of such measures to evaluate performance is acceptable, as it shows high positive correlations with objective measures (Song et al., 2005). However, the equivalence assumptions between subjective and objective performance measures are still being debated.

Future research should endeavour to develop new measurement and performance systems that focus on SMEs and the application of subjective measures. Additionally, future

Page | 5

studies may also need to establish more precise frameworks and empirical testing for performance measures. The contribution of this study has been in examining and expanding the taxonomy of business performance and in shedding light on future research in any discipline that focuses on measuring performance.

Page | 6

Page | 7

Appendix A:

Example of a Research Questionnaire Measuring Business Performance

Market Performance E1 Market-share growth 1 2 3 4 5 6 7 E2 Sales turnover 1 2 3 4 5 6 7 Supplier Performance E3 Supplier product quality 1 2 3 4 5 6 7 E4 Suppler communication 1 2 3 4 5 6 7 E5 Supplier delivery performance 1 2 3 4 5 6 7 Process Performance E6 Work in process (WIP)* inventory 1 2 3 4 5 6 7 E7 Order-fulfilment lead time ** 1 2 3 4 5 6 7 E8 Product-quality development 1 2 3 4 5 6 7 People Performance E9 Performance-appraisal results 1 2 3 4 5 6 7 E10 Skill level of employees 1 2 3 4 5 6 7 E11 Departmental communication 1 2 3 4 5 6 7 Customer-Relationship Performance E12 Resolution of customer complaints 1 2 3 4 5 6 7 E13 Customer loyalty/retention 1 2 3 4 5 6 7 E14 Quality reputation and award achievement 1 2 3 4 5 6 7 E15 Product returns rate 1 2 3 4 5 6 7 E16 The speed of order handling and processing 1 2 3 4 5 6 7

*Work-in-Process (WIP) relates to the products or components that are no longer raw material but have yet to become finished products.

**Lead time is the time between placement and receipt of an order.

Listed below are statements describing the business performance of a firm. These statements are divided into five sections: Market, Suppliers, Process, People and Customer Relationships measures. How would you rate your firm’s actual current conditions of business performance relative to the major industry competitors? Please remember that there are no right or wrong answers and the information you provide will be kept confidential .

Scale

Worst in the Industry Worse in the Industry Bad in the Industry eutral Good in the Industry Better in the Industry

Best in the Industry 1 2 3 4 5 6 7

References

Alasadi, R. & Abdelrahim, A. (2008). Analysis of small business performance in Syria.

Education, Business and Society: Contemporary Middle Eastern Issues, 1(1): 50-62.

Chandler, G. N. & Hanks, S. H. (1993). Measuring the performance of emerging businesses:

A validation study. Journal of Business Venturing, 8(5): 391-408.

Covin, J. G. & Slevin, D. P. (1989). Strategic management of small firms in hostile and benign environments. Strategic Management Journal, 10(1): 75-87.

Dawes, J. (1999). The relationship between subjective and objective company performance measures in market orientation research: Further empirical evidence. Marketing Bulletin, 10: 65-76.

Dess, G. G. & Robinson, J. R. B. (1984). Measuring organizational performance in the absence of objective measures: The case of the privately-held firm and conglomerate business unit. Strategic Management Journal (pre-1986), 5(3): 265-273.

Franco-Santos, M., Kennerley, M., Micheli, P., Martinez, V., Mason, S., Marr, B., Gray, D.

& Neely, A. (2007). Towards a definition of a business performance measurement system. International Journal of Operations & Production Management, 27(8): 784-801.

Gruber, M., Heinemann, F., Brettel, M. & Hungeling, S. (2010). Configurations of resources and capabilities and their performance implications: An exploratory study on technology ventures. Strategic Management Journal, 31(12): 1337-1356.

Hoffman, C. C., Nathan, B. R. & Holden, L. M. (1991). A comparison of validation criteria: Objective versus subjective performance measures and self-versus-supervisor ratings.

Personnel Psychology, 44(3): 601-619.

Jarvis, R., Curran, J., Kitching, J. & Lightfoot, G. (2000). The use of quantitative and qualitative criteria in the measurement of performance in small firms. Journal of Small Business and Enterprise Development, 7(2): 123 - 134.

Kim, S. W. (2006a). The effect of supply chain integration on the alignment between corporate competitive capability and supply chain operational capability.

International Journal of Operations & Production Management, 26(10): 1084-1107.

Kim, S. W. (2006b). Effects of supply chain management practices, integration and competition capability on performance. Supply Chain Management: An International Journal, 11(3): 241-248.

Laura, B. F., Shawnee, K. V. & Cornelia, L. M. D. (1996). The contribution of quality to business performance. International Journal of Operations & Production Management, 16(8): 44-62.

Page | 8

Lee, C., Lee, K. & Pennings, J. M. (2001). Internal capabilities, external networks, and performance: A study on technology-based ventures. Strategic Management Journal, 22(6-7): 615-640.

Mann, R. & Kehoe, D. (1994). An evaluation of the effects of quality improvement activities on business performance. International Journal of Quality & Reliability Management, 11(4): 29-44.

McGrath, R. G., MacMillan, I. C. & Venkataraman, S. (1995). Defining and developing a competence: A strategic process paradigm. Strategic Management Journal,16(4): 251-275.

Pelham, A. M. & Wilson, D. T. (1996). A longitudinal study of the impact of market structure, firm structure, strategy, and market orientation culture on dimensions of small-firm performance. Journal of the Academy of Marketing Science., 24(1): 27-43.

Sapienza, H. J., Smith, K. G. & Gannon, M. J. (1988). Using subjective evaluations of organizational performance in small business research. American Journal of Small Business, 12(3): 45-53.

Smith, T. M. & Reece, J. S. (1999). The relationship of strategy, fit, productivity, and business performance in a services setting. Journal of Operations Management, 17(2): 145-161.

Song, M., Droge, C., Hanvanich, S. & Calantone, R. (2005). Marketing and technology resource complementarity: An analysis of their interaction effect in two environmental contexts. Strategic Management Journal, 26(3): 259-276.

Thomas, W. Y. M., Theresa, L. & Ed, S. (2008). Entrepreneurial Competencies and the Performance of Small and Medium Enterprises: An Investigation through a Framework of Competitiveness. Journal of Small Business and Entrepreneurship, 21(3): 257.

Wall, T. D., Michie, J., Patterson, M., Wood, S. J., Sheehan, M., Clegg, C. W. & West, M.

(2004). On the validity of subjective measures of company performance. Personnel Psychology, 57(1): 95-118.

Wood, E. H. (2006). The internal predictors of business performance in small firms. Journal of Small Business and Enterprise Development, 13(3): 441-452.

Yong, T., Shi-hua, M. & Feng-mei, G. (2007). Empirical study on impact of logistics operations capability on supply chain performance. The 3rd International Conference on Wireless Communications, etworking, and Mobile Computing (WiCOM) 2007.

Shanghai, P.R. China.

Page | 9

Inventory management Inventory Control On the so-called "inventory control", many people will interpret it as a "storage management", which is actually a big distortion. The traditional narrow view, mainly for warehouse inventory control of materials for inventory, data processing, storage, distribution, etc., through the implementation of anti-corrosion, temperature and humidity control means, to make the custody of the physical inventory to maintain optimum purposes. This is just a form of inventory control, or can be defined as the physical inventory control. How, then, from a broad perspective to understand inventory control? Inventory control should be related to the company's financial and operational objectives, in particular operating cash flow by optimizing the entire demand and supply chain management processes (DSCM), a reasonable set of ERP control strategy, and supported by appropriate information processing tools, tools to achieved in ensuring the timely delivery of the premise, as far as possible to reduce inventory levels, reducing inventory and obsolescence, the risk of devaluation. In this sense, the physical inventory control to achieve financial goals is just a means to control the entire inventory or just a necessary part; from the perspective of organizational functions, physical inventory control, warehouse management is mainly the responsibility of The broad inventory control is the demand and supply chain management, and the whole company's responsibility. Why until now many people's understanding of inventory control, limited physical inventory control? The following two reasons can not be ignored: First, our enterprises do not attach importance to inventory control. Especially those who benefit relatively good business, as long as there is money on the few people to consider the problem of inventory turnover. Inventory control is simply interpreted as warehouse management, unless the time to spend money, it may have been to see the inventory problem, and see the results are often very simple procurement to buy more, or did not do warehouse departments . Second, ERP misleading. Invoicing software is simple audacity to call it ERP, companies on their so-called ERP can reduce the number of inventory, inventory control, seems to rely on their small software can get. Even as SAP, BAAN ERP world, the field of

广东工业大学华立学院 本科毕业设计(论文) 外文参考文献译文及原文 系部会计学系 专业会计学 年级 08级 班级名称 2008级会计(7)班 学号 14010807030 学生姓名吴智聪 2012年 2 月 9 日

目录 1. 外文译文 (1) 2. 外文原文 (5)

中小型企业财务管理中存在的问题及其对策中小型企业在中国经济发展中发挥着重要的作用。统计数据表明,在工商行政管理局登记在册的企业中,中小型企业占了99%,产值和利润分别占总额的60%和40%。此外,中小型企业所提供了75%的城镇就业机会。可见其为中国的稳定和经济繁荣作出了重要贡献。 虽然中小型企业在国民经济中占有重要地位,对中国经济发展与社会稳定具有很重大的意义。但是,中小型企业发展的主要障碍是缺乏有效的财务管理。本文分析了当前中小型企业财务管理中存在的问题,并就改善中小型企业财务管理提出了相应对策。 1.1 中小型企业的财务管理现状 自从21世纪以来,中国的中小型企业的蓬勃发展,在经济增长和社会发展中发挥着非常重要的作用。据财政部统计数据,直到2005年底,中小型企业总数已超过1000万,占中国企业总数的99%。中小型企业提供了75%的城镇就业机会,工业企业的总产值、销售收入、实现的利得税和出口额分别占总数的60%、57%、40%和60%,上缴的税收已经接近了国家税收总额的一半。中小型企业承载着超过75%的技术革新和超过65%的专利发明,他们以其灵活的经营机制和积极创新活动,为经济发展提供了增长的最根本动力。近年来,中国中小企业的消亡率将近70%,大约有30%的中小型企业存在赤字。中小型企业应该如何建立现代企业制度,加强财务管理,并科学地进行资本运作以谋求自身的健康发展,是我们密切关注的一个问题。 1.2 中小型企业财务管理中存在的问题 ⑴财务管理理念滞后,而且方法保守 中小型企业由于管理者自身知识水平的限制,使得企业的管理能力和管理质量较低。他们的管理思想已经不适合现代企业,并且大多数企业领导人缺乏财务管理的理论和方法,忽视了企业资本运作的作用。管理者既不重视财务事,也不参与企业政策的制定和相关管理活动。因此,财务管理无法发挥其应有职能,从而导致企业缺乏现代财务管理的理念,也无从去培训合格的财务人员。 ⑵财务管理工作基础薄弱,缺乏财务监督

文献出处: Waitz M. The small and medium-sized enterprise financing under P2P finance [J]. Journal of Business Research, 2016, 8(6): 81-91. 原文 The small and medium-sized enterprise financing under P2P finance Waitz M Abstract Small and medium-sized enterprise financing difficult is worldwide difficult problem. Article introduces the concept of the Internet financial, mainly summarized the P2P financial in the development of financial innovation and integration of science and technology, a combination of academic research on P2P financial now of the five directions of various views and opinions. Points out the current P2P financial problems in the development of risk control, and analyses the trend of the Internet financial. Keywords: P2P financial; Financial innovation; Risk control 1 Introduction Look from the history of enterprise development, a large enterprise originate from small and medium-sized enterprises. Small and medium-sized enterprises (smes) is the most dynamic part of the national economy, often walk in the forefront of technology development, in the high-tech industry, clean energy, green economy, etc, have good performance, play an important role in the economic transformation. Small and medium-sized enterprise financing difficult is worldwide difficult problem. These small and medium-sized enterprise financing environment and narrow channels, more than 60% are unable to get a bank loan. At present, science and technology enterprises and the characteristics of light assets, financing difficulties, become a huge bottleneck of sustainable development. 2 The concept of the Internet financial In the past two years, the Internet financial show explosive growth, since 2014, the Internet financial sector performance strength. Current economic field exists the phenomenon of two special contradiction, one is the small and medium-sized

本科毕业论文(设计) 外文翻译 原文: Financing of SMEs Abstract The main sources of financing for small and medium sized enterprises (SMEs) are equity, trade credit paid on time, long and short term bank credits, delayed payment on trade credit and other debt. The marginal costs of each financing instrument are driven by asymmetric information and transactions costs associated with nonpayment. According to the Pecking Order Theory, firms will choose the cheapest source in terms of cost. In the case of the static trade-off theory, firms choose finance so that the marginal costs across financing sources are all equal, thus an additional Euro of financing is obtained from all the sources whereas under the Pecking Order Theory the source is determined by how far down the Pecking Order the firm is presently located. In this paper, we argue that both of these theories miss the point that the marginal costs are dependent of the use of the funds, and the asset side of the balance sheet primarily determines the financing source for an additional Euro. An empirical analysis on a unique dataset of Portuguese SME’s confirms that the composition of the asset side of the balance sheet has an impact of the type of financing used and the Pecking Order Theory and the traditional Static Trade-off theory are https://www.doczj.com/doc/4016506263.html, For SME’s the main sources of financing are equity (internally generated cash), trade credit, bank credit and other debt. The choice of financing is driven by the costs of the sources which is primarily determined by costs of solving the asymmetric information problem and the expected costs associated with non-payment of debt. Asymmetric information costs arise from collecting and analysing information to support the decision of extending credit, and the non-payment costs are from

企业成本控制外文翻译文献(文档含英文原文和中文翻译)

译文: 在价值链的成本控制下减少费用和获得更多的利润 摘要: 根据基于价值链的成本管理理念和基于价值的重要因素是必要的。首先,必须有足够的资源,必须创造了有利的价值投资,同时还需要基于客户价值活动链,以确定他们的成本管理优势的价值链。其次,消耗的资源必须尽量减少,使最小的运营成本价值链和确保成本优势是基于最大商业价值或利润,这是一种成本控制系统内部整个视图的创建和供应的具实践,它也是一种成本控制制度基于价值链,包括足够的控制和必要的资源投资价值的观点,创建和保持消费的资源到合理的水平,具有价值的观点主要对象的第一个因素是构造有利的价值链,从创造顾客价值开始;第二个因素是加强有利的价值链,从供应或生产客户价值开始。因此它是一个新型的理念,去探索成本控制从整个视图的创建和供应的商品更盈利企业获得可持续的竞争优势。 关键词:成本控制,价值链,收益,支出,收入,成本会计 1、介绍 根据价值链理论,企业的目的是创造最大的顾客价值;和企业的竞争优势在于尽可能提供尽可能多的价值给他们的客户,作为低成本可能的。这要求企业必须首先考虑他们是否能为顾客创造价值,和然后考虑在很长一段时间内如何创造它。然而,竞争一直以“商品”(或“产品”)作为最直接的载体,因此,传统的成本控制方法主要集中在对“产品”和生产流程的过程。很显然,这不能解决企业的问题,企业是否或如何能为客户创造价值。换句话说,这至少不能从根本上解决它。 因此,企业必须首先投入足够的资源,以便他们能够创建客户值取向,然后提供它以最少的资源费用。所以在整个视图中对价值创造和提供整体的观点来控制成本,它可以为客户提供完美的动力和操作运行机制运行成本的控制,也可以从根本上彻底克服了传统的成本控制方法的缺点,解决了无法控制的创造和供应不足的真正价值。基于此,本文试图从创作的整体观讨论成本控制提供价值并探讨实现良性循环的策略,也就是说,“创造价值投资成本供应价值创造价值”。 2、成本及其控制的基于价值链理念 2.1基于价值链的成本观念 根据价值链理论,如果企业是要被客户接受,它必须创造和提供能满足其客户的价值。因此,成本(价值或资源支付费用)这不离为创造和提供顾客价值的活动,其活动的价值链。因此,我们应该从价值链角度看成本的重要。

毕业设计(论文) 外文文献译文及原文 学生:李树森 学号:201006090217 院(系):电气与信息工程学院 专业:网络工程 指导教师:王立梅 2014年06月10日

JSP的技术发展历史 作者:Kathy Sierra and Bert Bates 来源:Servlet&JSP Java Server Pages(JSP)是一种基于web的脚本编程技术,类似于网景公司的服务器端Java脚本语言—— server-side JavaScript(SSJS)和微软的Active Server Pages(ASP)。与SSJS和ASP相比,JSP具有更好的可扩展性,并且它不专属于任何一家厂商或某一特定的Web服务器。尽管JSP规范是由Sun 公司制定的,但任何厂商都可以在自己的系统上实现JSP。 在Sun正式发布JSP之后,这种新的Web应用开发技术很快引起了人们的关注。JSP为创建高度动态的Web应用提供了一个独特的开发环境。按照Sun的说法,JSP能够适应市场上包括Apache WebServer、IIS4.0在内的85%的服务器产品。 本文将介绍JSP相关的知识,以及JavaBean的相关内容,当然都是比较粗略的介绍其中的基本内容,仅仅起到抛砖引玉的作用,如果读者需要更详细的信息,请参考相应的JSP的书籍。 1.1 概述 JSP(Java Server Pages)是由Sun Microsystems公司倡导、许多公司参与一起建立的一种动态网页技术标准,其在动态网页的建设中有其强大而特别的功能。JSP与Microsoft的ASP技术非常相似。两者都提供在HTML代码中混合某种程序代码、由语言引擎解释执行程序代码的能力。下面我们简单的对它进行介绍。 JSP页面最终会转换成servlet。因而,从根本上,JSP页面能够执行的任何任务都可以用servlet 来完成。然而,这种底层的等同性并不意味着servlet和JSP页面对于所有的情况都等同适用。问题不在于技术的能力,而是二者在便利性、生产率和可维护性上的不同。毕竟,在特定平台上能够用Java 编程语言完成的事情,同样可以用汇编语言来完成,但是选择哪种语言依旧十分重要。 和单独使用servlet相比,JSP提供下述好处: JSP中HTML的编写与维护更为简单。JSP中可以使用常规的HTML:没有额外的反斜杠,没有额外的双引号,也没有暗含的Java语法。 能够使用标准的网站开发工具。即使是那些对JSP一无所知的HTML工具,我们也可以使用,因为它们会忽略JSP标签。 可以对开发团队进行划分。Java程序员可以致力于动态代码。Web开发人员可以将经理集中在表示层上。对于大型的项目,这种划分极为重要。依据开发团队的大小,及项目的复杂程度,可以对静态HTML和动态内容进行弱分离和强分离。 此处的讨论并不是说人们应该放弃使用servlet而仅仅使用JSP。事实上,几乎所有的项目都会同时用到这两种技术。在某些项目中,更适宜选用servlet,而针对项目中的某些请求,我们可能会在MVC构架下组合使用这两项技术。我们总是希望用适当的工具完成相对应的工作,仅仅是servlet并不一定能够胜任所有工作。 1.2 JSP的由来 Sun公司的JSP技术,使Web页面开发人员可以使用HTML或者XML标识来设计和格式化最终

中小企业融资的英文文献 Automatically translated text: The definition of lease financing Finance leases (Financial Leasing) also known as the Equipment Leasing (Equipment Leasing), or modern leasing (Modern Leasing), and is essentially transfer ownership of the assets of all or most of the risks and rewards of the lease. The ultimate ownership of assets to be transferred, or may not transfer. It refers to the specific content of the lessee to the lessor under the lease object and the specific requirements of the supplier selection, vendor financing to purchase rental property, and the use of leased to a lessee, the lessee to the lessor to pay instalments rent, the lease term lease ownership of objects belonging to the lessor of all, the tenant has the right to use the leased items. Term expired, and finished the lessee to pay rent under the lease contract financing to fulfil obligations in full, leasing objects that vesting ownership of all the lessee. Despite the finance lease transactions, the lessors have the identity of the purchase of equipment, but the substantive content of the purchase of equipment suppliers such as the choice of the specific requirements of the equipment, the conditions of the purchase contract negotiations by the lessee enjoy and exercise, lessee leasing object is essentially the purchaser. , Is a finance lease extension of loans and trade and technology updates in the new integrated financial industry. Because of its extension of loans and combination of features, there is a problem in leasing companies can recycling, treatment of leasing, and

XX企业融资开题报告范文 中小企业迅猛发展为世界各国经济发展起到了强有力的推动作用,但在中小企业创建、经营发展过程中,融资困难一直是困扰世界各国中小企业的大问题,为此,探索可行有效的措施解决中小企业融资难题, 己成为世界各国政府中小企业经济政策的重要内容和工作重点。 一、论文选题的背景、意义: (一)背景 改革开放以来,中国经济经历了根本性变化,从完全依靠国有和集体企业发展到民营中小企业发挥重要作用的混合性经济,由于大批国有企业进行资产重组、人员分流和产品结构调整,国有经济拉动经济增长的作用明显减弱,而此时我国中小企业得到了蓬勃发展,成为保持国民经济持续增长的生力军。在我国,中小企业在活跃市场,吸纳就业,促进技术创新与出口创汇等方面发挥着越来越大的作用。并己成为我国国民经济中最具活力的新的经济增长点。 (二)意义 在我国,占企业总数99%的中小企业创造了74%的工业增加值,63% 的gdp,但是其占有的金融资源却不足20%o中小企业的融资难问题己经严重制约了经济社会的发展。杭州的企业体制一般是以中小企业为主,这也导致了杭州的中小企业也存在严重的融资难问题,虽然各个金融机构采取了一系列的措施,但是并没有从根木上解决杭州中小企业的融资难问题。因为中小企业地位的重要性,所以解决中小企业的融资难问题是刻

不容缓的。 二、相关研究的最新成果及动态(参考文献综述的主体与总结部分)(一)国外关于中小企业融资问题的研究 中小企业迅猛发展为世界各国经济发展起到了强有力的推动作用,但在中小企业创建、经营发展过程中,融资困难一直是困扰世界各国中小企业的大问题,为此,探索可行有效的措施解决中小企业融资难题, 己成为世界各国政府中小企业经济政策的重要内容和工作重点。西方国家如美国、日本、意大利、英国等都制定了相关的促进中小企业发展的政策,值得我们借鉴。 国外有关企业融资的理论研究主要是资本结构理论。早期的资木结构理论是美国经济学家大卫杜兰特提出的,包括净收益理论,净经营收益理论和传统理论。现代资本结构理论形成于20世纪五十年代,至七十年代后期,它以mm定理为中心,一部分探讨税收差异对资本结构的影响,被称为税差学派,另一部分研究破产成本与资本结构的关系, 发展成为财务困境成本学派,形成破产成本主义和财务困境主义,最后合并为权衡理论。七十年代后期,由于信息不对称和博弈论的引入, 使资本结构理论研究发生了一次质的飞跃,新资本结构理论以信息不对称为中心,大量引入经济学各方面的最新分析方法,从新的学术视野来分析资木结构问题,提出了不少新的观点 此外,adolphusj.toby(xx)运用xx至xx年间尼日利亚中小型企业的相关数据测试了4个运行现状不佳的企业。认为对中小企业来说,持续的增长,充足的资金流动性和必要的盈利能力是与他们的投资和融资决策密切相

Enterprise Human Resources Management System Design And Implementation Abstract: Human resource management system is the core content of modern enterprise management. With the rapid development of the computer information technology and unprecedented prevalence of electronic commerce mode,the competition between enterprises is turning from visible economic markets to the network. Developing the human resource management system supported by computer technology,network technology and information technology can not only improve the skill of human resource management and the efficiency of the enterprises but also make human resource management modern and decision sciencefic,Modern human resource management uses B/S mode to avoid C/S modes short coming of difficult in maintdning and reusing.According to the functional requirements of the actual project,this article specificly state the analysis of system,the general desigin of the system,the detail design of system and the practice of the system. The development of the system is the practice of MVC design ideas, maing using the Jsp+Servlet+JavaBean form of development.Jsp is the practice of MVC design ideas’view,in charge of receiving/responding the request of the customer.Servlet mainly responsible for the core business control of the whole system is the practice of the vontroller of MVC design idea to take charge of the statistics and rules of the whole system. In the practice of the system, somr open-source projrcts,such as the Ajax technique,JfreChart statements,fileupload technology,has been used. Using the modern human resource management theropy and analysising the actual situation, comparing the current situation of human resource management system, a huaman resource contents of management system basied on the Internet/Intranet has been designed. The main management,attendance management training more efficient statistics. Keywords:human resource management; B/S mode; Open-source projects; MVC mode. 摘要 人力资源管理系统是现代企业管理的核心内容。随着计算机信息技术的高速发展,电子商务模式的空前盛行,企业之间的竞争也从有形的经济市场转向了网络。开发以计算机技术、网络技术、信息技术支持的现代人力资源管理系统,既能提高企业人力资源管理的技术含量和企业的办事效率,也能使人力资源管理能够进入现代化、决策科学化的进程。现代人力资源管理系统采用了B/S模式,可以避免C/S模式的重用性差、维护难度高的缺点和

毕业论文外文文献 Photography Pen Film director and critic Alexander Astruc's comments in today, wrote a famous: "Following a variety of other arts, especially painting, novel, film is rapidly becoming a tool to express ideas. It swept the market, a mall next to the theater's entertainment products. It is a well preserved image of the times methods. Now is gradually becoming a language, that is, the artist can use it to express themselves through a means of thinking, no matter how abstract this idea, or that it is also used as a kind of artists like prose or fiction a form to express their themes. So, I put this new era for film today called "photo pen" era, that era of writing, the use of the camera …… "Silent film attempts to use symbolic links to all the concept and meaning of the expression. We know, Lenovo exist in the image itself, naturally present in the film development process, there is the role of performance in each posture and expression, present in every word of in; also present in the camera movement, this movement linked to a piece of things, to link people and things …… "Obviously, that is, screenwriter making his own films. Or even say that there is no longer what the movie writer. Because, in such films, the playwright and director, there is nothing between significant

淮阴工学院 毕业设计(论文)外文资料翻译 学院: 专业: 姓名: 学号: 外文出处:Facts for You (用外文写) 附件: 1.外文资料翻译译文;2.外文原文。 注:请将该封面与附件装订成册。

附件1:外文资料翻译译文 中小型企业融资决策 企业的产生、生存及发展均离不开投资与融资活动。随着我国加入WTO 组织,市场经济体制的逐步完善,金融市场的快速发展,投资与融资效率也越来越成为企业发展的关键。对于中小型企业而言,应要根据自身发展需求,认真考虑如何选择自己需要和适合自己发展阶段的融资方式以及各种融资方式的利用时机、条件、成本和风险,确定合适的融资规模以及制定最佳融资期限等问题。要解决这些问题,需要中小型企业制定适当的融资策略,以作出最优化的融资决策。 一、企业融资决策概述 (一)企业融资决策概述 企业融资决策,是企业根据其价值创造目标需要,利用一定时机与渠道,采取经济有效的融资工具,为公司筹集所需资金的一种市场行为。它不仅改变了公司的资产负债结构,而且影响了企业内部管理、经营业绩、可持续发展及价值增长。典型的融资决策包括出售何种债务和股权(融资方式)、如何确定所要出售债务和股权的价值(融资成本)、何时出售些债务和股权(融资时机)等等。而其中最主要的包括融资规模的决策和融资方式的决策。融资规模应为企业完成资金使用目的的最低需要量。而企业的融资方式则多种多样,常见的以下几种: 1.财政融资。财政融资方式从融出的角度来讲,可分为:预算内拨款、财政贷款、通过授权机构的国有资产投资、政策性银行贷款、预算外专项建设基金、财政补贴。 2.银行融资。从资金融出角度即银行的资金运用来说,主要是各种代款,例如:信用贷款、抵押贷款、担保贷款、贴现贷款、融资租凭、证券投资。 3.商业融资。其方式也是多种多样,主要包括商品交易过程中各企业间发生的赊购商品、预收货款等形式。

外文文献翻译译文 一、外文原文 Corporate Performance Management Abstract Two of the most important duties of a chief executive officer are (1) to formulate strategy and (2) to manage his company’s performance. In this article we examine the second of these tasks and discuss how corporate performance should be modeled and managed. We begin by considering the environment in which a company operates, which includes, besides outside stakeholders, the industry it belongs and the market it supplies, and then proceed to explain how the functioning of a company can be understood by an examination of its business, operational and performance management models. Next we describe the structure recommended by the authors for a corporate planning, control and evaluation system, the most important part of a corporate performance management system. The core component of the planning system is the corporate performance evaluation model, the structure of which is mapped into the planning system’s database, simulation models and budgeting tools’ structures, and also used to shape information contained in the system’s products, besides being the nucleus of the language used by the system’s agents to talk about corporate performance. The ontology of planning, the guiding principles of corporate planning and the history of ”MADE”, the corporate performance management system discussed in this article, are reviewed next, before we proceed to discuss in detail the structural components of the corporate planning and control system introduced before. We conclude the article by listing the main steps which should be followed when implementing a performance planning, control and evaluation system for a company. 1.Introduction Two of the most important corporate tasks for which a chief executive officer is p rimarily responsible are (1) to formulate strategy and (2) to manage the company’s performance. In this article we examine the second of these tasks and discuss how