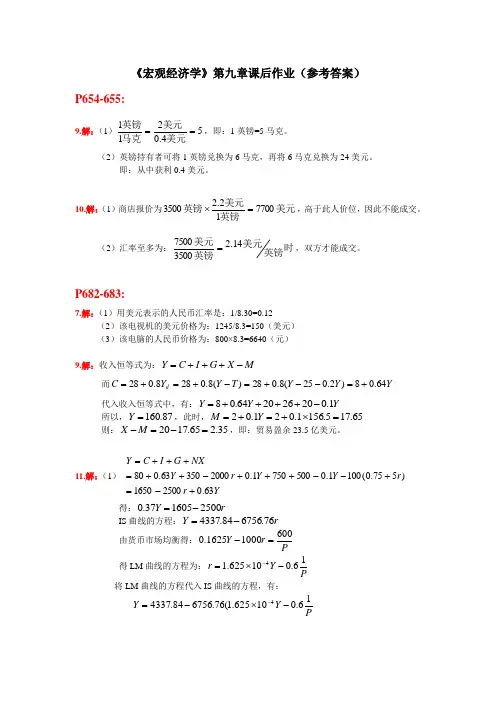

高级宏观经济学_第四版_中文_罗默课后题答案

- 格式:doc

- 大小:7.55 MB

- 文档页数:54

(a)考虑厂商生产 Y 单位产出的成本最小化问题。证明使成本最小化的 k 值唯一确定并独立于 Y,并由此证明所有厂商都选择相同的 k 值。

(b)考虑某单个厂商,若其具有相同生产函数,并且其劳动和资本的投入 是上述 N 个厂商的总和,证明其产出也等于述 N 个厂商成本最小化的总产出。

证明:(a)题目的要厂商选择资本 K 和有效劳动 AL 以最小化成本

页脚

.

.

增长路径上是独立于利率的。对于折现率 而言, 越大,家庭越厌恶风险,越 会选择多消费。

2.5 设想某家庭的效用函数由(2.1)~(2.2)式给定。假设实际利率不 变,令 W 表示家庭的初始财富加上终生劳动收入的现值[(2.6)的右端]。已知 r、 W 和效用函数中的各参数,求 C 的效用最大化路径。

此时的效用收益为 费路径来说,必须满足下列条件:

。总之,对于效用最大化的消

在

时,有下式:

因此,当政府对财富没收一半后,消费会不连续的变化,消费会下降。征收 前,消费者会减少储蓄以避免被没收,之后会降低消费。

(b)从家庭的角度讲,他的消费行为将不会发生不连续的变化。家庭事先 会预测到自己一半的财富会被政府没收,为了最优化他一生的效用,家庭不会使 自己的消费发生不连续的变化,他还是希望平滑自己的消费的。

2.1

答:本题目是在家庭的预算约束下最大化一生的效用,即:

2.2 (1)

(2) W 代表家庭的初始财富加上家庭一生劳动收入的现值,利率 r 是常数。 建立拉格朗日方程如下:

求一阶条件,可得:

抵消

,得:

两边对时间 t 求导,可得: 得到下面的方程: 将方程(3)代入(4),可得:

(3) (4)

页脚

.

(a)已知 和 和 W,则此人效用最大化的 和 是多少?

(b)两期消费之间的替代弹性为

,

或 的替代弹性为 。

。证明,若效用函数为(2.43)式,是则 与 之间

答:(a)这是一个效用最大化的优化问题。

(1)

(2) 求解约束条件:

(3) 将方程(3)代入(1)中,可得:

(4) 这样便将一个受约束的最优化问题转变为一个无约束问题。在方程(4)两

页脚

.

.

答:(a)考虑两个时期的消费,比如在一个极短的时期 ,从

到

。

考虑家庭在

时期减少每单位有效劳动的消费为

。然后他在

投资并消费这一部分财富。如果家庭在最优化他一生的财富,则他的这 一财富变化对一生的效用没有影响。

这一变化有一效用成本

,在

会有一收益

ቤተ መጻሕፍቲ ባይዱ,财富的回报率为 ,不过,此刻有一半的财富会被没收。

.

抵消

然后求消费的增长率 ,可得:

(5)

由于利率 r 是常数,所以消费的增长率为常数。如果

,则市场利率超

过贴现率,则消费会增加;反之,如果

,则市场利率小于贴现率,则消费

会减少。如果

,则 决定了消费增长的幅度。 值越低,也就是替代弹性

越高, 越高,即消费增长的越快。 重写方程(5),得:

对方程(6)积分,积分区间是从时间τ=0 到时间τ=t,可得:

.

.

高级宏观经济学_第四版_中文_罗默课后题答案

第 2 章无限期模型与世代交叠模型

2.1 考 虑 N 个 厂 商 , 每 个 厂 商 均 有 规 模 报 酬 不 变 的 生 产 函 数

, Y F K,AL , 或 者 采 用 紧 凑 形 式

。假设

。假设所有厂商都能以工资 wA 雇用劳动,以成本 r 租赁资 本,并且所有厂商的 A 值都相同。

2.3 (a)假设事先知道在某一时刻 ,政府会没收每个家庭当时所拥有财 富的一半。那么,消费是否会在时刻 发生突然变化?为什么?(如果会的话, 请说明时刻 前后消费之间的关系。)

(b)假设事先知道,在某一时刻 ,政府会没收每个家庭当时所拥有的部 分财富,其数量等于当时所有家庭财富平均水平的一半。那么,消费是否会在 时刻 发生突然变化?为什么?(如果会,请说明时刻 前后消费之间的关系。)

(6)

上式可以简化为: 对方程(7)两边取指数,可得: 下面求解初始消费,将方程(8)代入(2),可得:

(7) ,整理得:

(8)

将

代入上式,可得:

(9)

只要

,从而保证积分收敛,则求解方程(9)可得:

(10)

将方程(10)代入(9)中,求解 :

(11)

为 N 个厂商总的雇佣人数,单一厂商拥有同样的 A 并且选择相同数量的 k,

k 的决定独立于 Y 的选择。因此,如果单一厂商拥有 的劳动人数,则它也会生

产

的产量。这恰好是 N 个厂商成本最小化的总产量。

2.2 相对风险规避系数不变的效用函数的替代弹性。设想某个人只活两 期,其效用函数由方程(2.43)给定。令 和 分别表示消费品在这两期中的 价格,W 表示此人终生收入的价值,因此其预算约束是:

2.4 设方程(2.1)中的瞬时效用函数 为

。考虑家庭在(2.6)

的约束下最大化方程(2.1)的问题。请把每一时刻的 C 表示为初始财富加上劳

动收入现值、 以及效用函数各参数的函数。

答: 2.1 2.6

本题目是在家庭的预算约束下最大化一生的效用。

页脚

.

令 建立拉格朗日方程:

.

(1) (2)

求一阶条件:

抵消 项得: 可以推出: 将其代入预算约束方程,得:

将

代入上式,得:

只要

,则积分项收敛,为

,则:

将方程(7)代入(4): 因此,初始消费为:

(3) (4) (5) (6) (7) (8) (9)

个人的初始财富为 ,方程(9)说明消费是初始财富的一个不变的比例。 为个人的财富边际消费倾向。可以看出,这个财富边际消费倾向在平衡

页脚

.

.

边对 求一阶条件可得:

解得: 将方程(5)代入(3),则有:

(5)

解得: 将方程(6)代入(5)中,则有: (b)由方程(5)可知第一时期和第二时期的消费之比为: 对方程(8)两边取对数可得: 则消费的跨期替代弹性为:

(6) (7) (8) (9)

因此, 越大,表明消费者越愿意进行跨期替代。

,

同时厂商受到生产函数

的约束。这是一个典型的最优化问题。

构造拉格朗日函数: 求一阶导数:

得到:

页脚

.

.

上式潜在地决定了最佳资本 k 的选择。很明显,k 的选择独立于 Y。 上式表明,资本和有效劳动的边际产品之比必须等于两种要素的价格之比, 这便是成本最小化条件。 (b)因为每个厂商拥有同样的 k 和 A,则 N 个成本最小化厂商的总产量为:

(b)考虑某单个厂商,若其具有相同生产函数,并且其劳动和资本的投入 是上述 N 个厂商的总和,证明其产出也等于述 N 个厂商成本最小化的总产出。

证明:(a)题目的要厂商选择资本 K 和有效劳动 AL 以最小化成本

页脚

.

.

增长路径上是独立于利率的。对于折现率 而言, 越大,家庭越厌恶风险,越 会选择多消费。

2.5 设想某家庭的效用函数由(2.1)~(2.2)式给定。假设实际利率不 变,令 W 表示家庭的初始财富加上终生劳动收入的现值[(2.6)的右端]。已知 r、 W 和效用函数中的各参数,求 C 的效用最大化路径。

此时的效用收益为 费路径来说,必须满足下列条件:

。总之,对于效用最大化的消

在

时,有下式:

因此,当政府对财富没收一半后,消费会不连续的变化,消费会下降。征收 前,消费者会减少储蓄以避免被没收,之后会降低消费。

(b)从家庭的角度讲,他的消费行为将不会发生不连续的变化。家庭事先 会预测到自己一半的财富会被政府没收,为了最优化他一生的效用,家庭不会使 自己的消费发生不连续的变化,他还是希望平滑自己的消费的。

2.1

答:本题目是在家庭的预算约束下最大化一生的效用,即:

2.2 (1)

(2) W 代表家庭的初始财富加上家庭一生劳动收入的现值,利率 r 是常数。 建立拉格朗日方程如下:

求一阶条件,可得:

抵消

,得:

两边对时间 t 求导,可得: 得到下面的方程: 将方程(3)代入(4),可得:

(3) (4)

页脚

.

(a)已知 和 和 W,则此人效用最大化的 和 是多少?

(b)两期消费之间的替代弹性为

,

或 的替代弹性为 。

。证明,若效用函数为(2.43)式,是则 与 之间

答:(a)这是一个效用最大化的优化问题。

(1)

(2) 求解约束条件:

(3) 将方程(3)代入(1)中,可得:

(4) 这样便将一个受约束的最优化问题转变为一个无约束问题。在方程(4)两

页脚

.

.

答:(a)考虑两个时期的消费,比如在一个极短的时期 ,从

到

。

考虑家庭在

时期减少每单位有效劳动的消费为

。然后他在

投资并消费这一部分财富。如果家庭在最优化他一生的财富,则他的这 一财富变化对一生的效用没有影响。

这一变化有一效用成本

,在

会有一收益

ቤተ መጻሕፍቲ ባይዱ,财富的回报率为 ,不过,此刻有一半的财富会被没收。

.

抵消

然后求消费的增长率 ,可得:

(5)

由于利率 r 是常数,所以消费的增长率为常数。如果

,则市场利率超

过贴现率,则消费会增加;反之,如果

,则市场利率小于贴现率,则消费

会减少。如果

,则 决定了消费增长的幅度。 值越低,也就是替代弹性

越高, 越高,即消费增长的越快。 重写方程(5),得:

对方程(6)积分,积分区间是从时间τ=0 到时间τ=t,可得:

.

.

高级宏观经济学_第四版_中文_罗默课后题答案

第 2 章无限期模型与世代交叠模型

2.1 考 虑 N 个 厂 商 , 每 个 厂 商 均 有 规 模 报 酬 不 变 的 生 产 函 数

, Y F K,AL , 或 者 采 用 紧 凑 形 式

。假设

。假设所有厂商都能以工资 wA 雇用劳动,以成本 r 租赁资 本,并且所有厂商的 A 值都相同。

2.3 (a)假设事先知道在某一时刻 ,政府会没收每个家庭当时所拥有财 富的一半。那么,消费是否会在时刻 发生突然变化?为什么?(如果会的话, 请说明时刻 前后消费之间的关系。)

(b)假设事先知道,在某一时刻 ,政府会没收每个家庭当时所拥有的部 分财富,其数量等于当时所有家庭财富平均水平的一半。那么,消费是否会在 时刻 发生突然变化?为什么?(如果会,请说明时刻 前后消费之间的关系。)

(6)

上式可以简化为: 对方程(7)两边取指数,可得: 下面求解初始消费,将方程(8)代入(2),可得:

(7) ,整理得:

(8)

将

代入上式,可得:

(9)

只要

,从而保证积分收敛,则求解方程(9)可得:

(10)

将方程(10)代入(9)中,求解 :

(11)

为 N 个厂商总的雇佣人数,单一厂商拥有同样的 A 并且选择相同数量的 k,

k 的决定独立于 Y 的选择。因此,如果单一厂商拥有 的劳动人数,则它也会生

产

的产量。这恰好是 N 个厂商成本最小化的总产量。

2.2 相对风险规避系数不变的效用函数的替代弹性。设想某个人只活两 期,其效用函数由方程(2.43)给定。令 和 分别表示消费品在这两期中的 价格,W 表示此人终生收入的价值,因此其预算约束是:

2.4 设方程(2.1)中的瞬时效用函数 为

。考虑家庭在(2.6)

的约束下最大化方程(2.1)的问题。请把每一时刻的 C 表示为初始财富加上劳

动收入现值、 以及效用函数各参数的函数。

答: 2.1 2.6

本题目是在家庭的预算约束下最大化一生的效用。

页脚

.

令 建立拉格朗日方程:

.

(1) (2)

求一阶条件:

抵消 项得: 可以推出: 将其代入预算约束方程,得:

将

代入上式,得:

只要

,则积分项收敛,为

,则:

将方程(7)代入(4): 因此,初始消费为:

(3) (4) (5) (6) (7) (8) (9)

个人的初始财富为 ,方程(9)说明消费是初始财富的一个不变的比例。 为个人的财富边际消费倾向。可以看出,这个财富边际消费倾向在平衡

页脚

.

.

边对 求一阶条件可得:

解得: 将方程(5)代入(3),则有:

(5)

解得: 将方程(6)代入(5)中,则有: (b)由方程(5)可知第一时期和第二时期的消费之比为: 对方程(8)两边取对数可得: 则消费的跨期替代弹性为:

(6) (7) (8) (9)

因此, 越大,表明消费者越愿意进行跨期替代。

,

同时厂商受到生产函数

的约束。这是一个典型的最优化问题。

构造拉格朗日函数: 求一阶导数:

得到:

页脚

.

.

上式潜在地决定了最佳资本 k 的选择。很明显,k 的选择独立于 Y。 上式表明,资本和有效劳动的边际产品之比必须等于两种要素的价格之比, 这便是成本最小化条件。 (b)因为每个厂商拥有同样的 k 和 A,则 N 个成本最小化厂商的总产量为: