FRM一级模拟题(1)

- 格式:pdf

- 大小:208.63 KB

- 文档页数:6

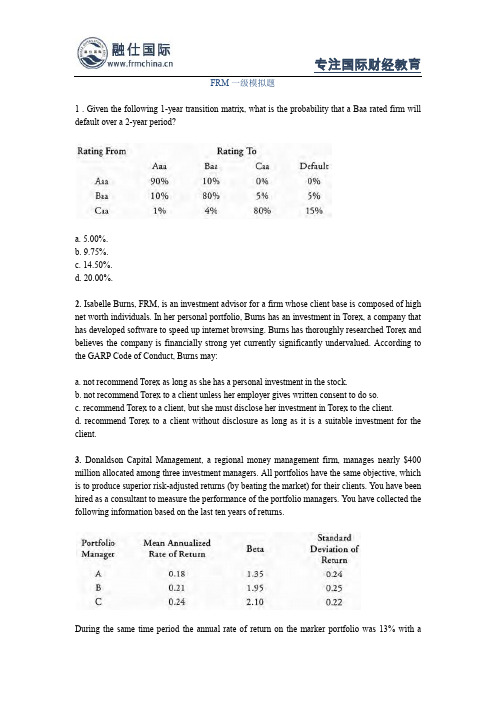

FRM一级模拟题1 . Given the following 1-year transition matrix, what is the probability that a Baa rated firm will default over a 2-year period?a. 5.00%.b. 9.75%.c. 14.50%.d. 20.00%.2. Isabelle Burns, FRM, is an investment advisor for a firm whose client base is composed of high net worth individuals. In her personal portfolio, Burns has an investment in Torex, a company that has developed software to speed up internet browsing. Burns has thoroughly researched Torex and believes the company is financially strong yet currently significantly undervalued. According to the GARP Code of Conduct, Burns may:a. not recommend Torex as long as she has a personal investment in the stock.b. not recommend Torex to a client unless her employer gives written consent to do so.c. recommend Torex to a client, but she must disclose her investment in Torex to the client.d. recommend Torex to a client without disclosure as long as it is a suitable investment for the client.3. Donaldson Capital Management, a regional money management firm, manages nearly $400 million allocated among three investment managers. All portfolios have the same objective, which is to produce superior risk-adjusted returns (by beating the market) for their clients. You have been hired as a consultant to measure the performance of the portfolio managers. You have collected the following information based on the last ten years of returns.During the same time period the annual rate of return on the marker portfolio was 13% with astandard deviation of 19%. In order to assess the portfolio performance of the above managers, you should use:a. the Treynor measure of performance.b. the Sharpe measure of performance.c. the Jensen measure of performance.d. none of the above.4. Which of the following statements about the central limit theorem is least likely correct?a. The variance of the distribution of sample means is s2 / n.b. The central limit theorem has limited usefulness for skewed distributions.c. The mean of the population and the mean of all possible sample means are equal.d. When the sample size n is large, the sampling distribution of the sample means is approximately normal.5. Bank regulators are examining the loan portfolio of a large, diversified lender. The regulators main concern is that the bank remains solvent during turbulent economic times. Which of the following is most likely the area that the regulator will want to focus on?a. Expected loss, since each asset can expect, on average, to decline in value from a positive probability of default.b. Expected loss, given the increase in underwriting standards of new loans.c. Unexpected loss, since the bank will need to set aside additional capital for the unlikely event that recovery rates are larger than expected.d. Unexpected loss, since the bank will need to set aside additional capital for the unlikely event that default losses are larger than expected.。

专注国际财经教育FRM一级模拟题1 . An Asset/Liability Management analyst at a community bank notices that a right to pay fixed swaption was purchased with a notional amount of 200 million with a strike in three months. The bank has only floating rate funding sources. The transaction most likely was done becausethe: .A. bank is anticipating a new $200M fixed rate loan.B. bank is anticipating a new $200M floating rate loan.C. bank is anticipating that a prepayment of $200M will occur on a flxed loan.D. trading area is speculating.Answer: AThe bank purchased the option in order to be able to convert variable rate funding to fixed rate if it needs to. The possibility of making a fixed rate loan would make this a rational strategy.2 . Consider a 2 int0 3-year Bermudan swaption (i.e., an option to obtain a swap that starts in 2 years and matures in 5 years). Consider the following statements:I A lower bound on the Bermudan price is a 2 int0 3 year European swaption.II An upper bound on the Bermudan price is a cap that starts in 2 years and matures in 5 years.III A lower bound on the Bermudan price is a 2 int0 5 year European optionWhich of the following statements is (are) TRUE?A. I onlyB. II onlyC. I and IID. III onlyAnswer: CSince a Bermudan option can be exercised on a discrete set of dates, it is at least as valuable as a European option, so I is correct. A cap would be exercisable continuously during the period, so it would represent the upper bound of the swap (and hence the option on the swap), so II is correct. III confuses the 2 int0 3 year Burmudan swaption and a 2- int0 5-year European option.3 . Which of the following actions would be most profitable when a trader expects a sharp rise in interest rates?A. Sell a payer swaption.B. Buy a payer swaption.C. Sell a receiver swaption.D. Buy a receiver swaption.Answer: BA payer swaption gives the holder the right to pay fixed rate and receive floating rate. Selling a receiver swaption would also be a profitable strategy as it would mean receiving a premium but with a sharp rise in interest rates buying a payer swaption should be a better deal.。

FRM一级模拟题1 . The 2-year spot rate is closest to:a. 2.50%.b. 2.75%.c. 3.00%.d. 3.25%.解析:aThe spot rate is calculated as [(100 / 95.1524)1/4 - 1)] x 2 = 2.50%.2. The 6-month forward rate on an investment that matures in 1.5 years is closest to:a. 2.50%.b. 2.75%.c. 3.00%.d. 3.25%.解析:cThe forward rate can be calculated as [(98.2240 / 96.7713) -1] x 2 = 3%.3. The price of a $1,000 par value Treasury bond (T-bond) with a 3% coupon that matures in 1.5 years is closest to:a. 1,010.02.b. 1,011.85.c. 1,013.68.d. 1,015.51.解析:bThe price is calculated as $15 (0.992556) + $15 (0.982240) + $1,015 (0.967713)= $1,011.85.4. Which of the following statements about interest rate swaps and currency swaps is least likely correct?a. In an interest rate swap, the net interest rate payment is paid on each settlement date by the party owing the greater amount.b. A plain-vanilla interest rate swap involves trading fixed interest rate payments for floating-ratc payments.c. A fixed-for-floating currency swap involves trading floating-rate interest payments on one currency for fixed-rate interest payments on another currency.d. In a currency swap, the net difference between the notional principal amounts is exchanged atsettlement date.解析:dIn a currency swap, the full notional principal is exchanged at the beginning and termination of the swap.5. An option trader is attempting to judge whether an option's premium is cheap or expensive. To do so, he employs a GARCH(1,1) model to forecast volatility. The particular model he estimates has an intercept term equal to 0.000005, a parameter estimate on the latest estimate of variance of 0.85, and a parameter estimate on the latest innovation of 0.13. If the latest volatility estimate from the model were 2.2% per day and the option's underlying asset changed 3%, the trader's estimate of the next period's standard deviation is closest to:a. 0.07%b. 2.31%c. 5.20%.d. 2.62%.解析:bThe GARCH(1,1) estimate of volatility will be:0.000005+(0.13)(0.03)2 +(0.85)(0.022)2 = 0.000533。

FRM一级模拟题1 .If the daily returns of two assets are positively correlated, then:A. the covariance of their daily returns must be positiveB. the covariance of their daily returns must be zeroC. the covariance of their daily returns must be negativeD. nothing can be said about the covariance of their daily returnsAnswer: AIf variables are positively correlated, the covariance between the Variables will also be positive.2 .You are given that X and Y are random variables, and each of which follows a standard normal distribution with Covariance (X, Y) = 0.4. What is the variance of (5X+2Y)?A. 11.0B. 29.0C. 29.4D. 37.0Answer: DSince each variable is standardized, its variance is one. Therefore, Var(5X+2Y) = 25 x Var(X)+4xVar(Y)+2 x 5x2x Cov(X,Y) =25+4+8 = 373 . What is the covariance between populations A and B?If the variance ofA is 12, what is the variance of B?A. 10.00B. 2.89C. 8.33D. 14.40Answer:C5 . Which one of the following statements about the correlation coefficient is FALSE?A. It always ranges from -1 to +1B. A correlation coefficient of zero means that two random variables are independentC. It is a measure of linear relationship between two random variablesD. It can be calculated by scaling the covariance between two random variables Answer:BCorrelation describes the linear relationship between two variables. While we would expect to find a correlation of zero for independent .variables, finding a correlation of zero does not mean that two variables are independent.。

frm考试培训训练FRM一级模拟题高顿FRM考试培训训练FRM一级模拟题:If there are restrictions on short selling and borrowing at the risk-free rate,we would expect to see that:A.all investors hold the same market portfolio as predicted by the CAPM.B.highly risk-averse individuals tend to hold heavily diversified portfolios,while those with less risk aversion tend to concentrate their portfolios.C.less risk-averse individuals tend to hold heavily diversified portfolios,while those with more risk aversion tend to concentrate their portfolios.D.both highly risk-averse individuals and those with less risk aversion tend to concentrate their portfolios.Answer:BRestrictions on short selling or borrowing at the risk-free rate make investors construct portfolios with considerably different compositions.Highly risk-averse individuals tend to hold heavily diversified portfolios,while those with less risk aversion tend to concentrate their portfolios.FRM的一级考试四科目复习方法:风险管理基础(Foundations of Risk Management)考试比重:20%和定量分析(Quantitative Analysis)考试比重:20%我的数学底子并不好,理科废柴生。

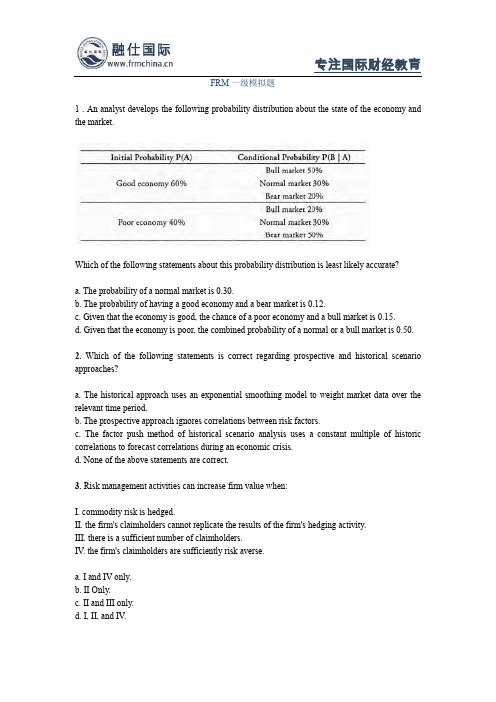

FRM一级模拟题1 . An analyst develops the following probability distribution about the state of the economy and the market.Which of the following statements about this probability distribution is least likely accurate?a. The probability of a normal market is 0.30.b. The probability of having a good economy and a bear market is 0.12.c. Given that the economy is good, the chance of a poor economy and a bull market is 0.15.d. Given that the economy is poor, the combined probability of a normal or a bull market is 0.50.2. Which of the following statements is correct regarding prospective and historical scenario approaches?a. The historical approach uses an exponential smoothing model to weight market data over the relevant time period.b. The prospective approach ignores correlations between risk factors.c. The factor push method of historical scenario analysis uses a constant multiple of historic correlations to forecast correlations during an economic crisis.d. None of the above statements are correct.3. Risk management activities can increase firm value when:I. commodity risk is hedged.II. the firm's claimholders cannot replicate the results of the firm's hedging activity.III. there is a sufficient number of claimholders.IV. the firm's claimholders are sufficiently risk averse.a. I and IV only.b. II Only.c. II and III only.d. I, II, and IV.4. Which of the following characteristics describe top-down approaches to operational risk measurement compared to bottom-up approaches?I. Relatively simple.II. Ability to differentiate high-frequency, low-severity events from low-frequency, high-severity events.III. Dissect processes into individual components.IV. Modest data requirements.a. I and IV.b. I only.c. I, II, and III.d. II, III, and IV.5. A butterfly spread can be created by buying a call option with a:a. low strike price and then selling three call options with strike prices above the purchased option.b. high strike price and then selling three put options with strike prices below the purchased put.c. low strike price, buying another call option with a higher strike price, and selling two call options with a strike price halfway between the low and high strike options.d. low strike price, selling a put option with a high strike price, and selling a call and buying a put with a strike price halfway between the low and high strike options.。

FRM一级模拟题1 . Which one of the following long positions is more exposed to an increase in interest rates?A. A treasury billB. 10-year fixed coupon bondC. 10-yearfloaterD. 1 0-year reverse floaterAnswer: D ,The l0-year reverse floater has the highest effective duration and hence the most exposure to an increase in interest rates. Both the l0-year floater and the T-bill have short durations (bills have maturities of 52-weeks or less, while floaters, and have average durations equal to the time to reset). The l0-year fixed coupon bond falls in between the bill and the reverse floater2 . What can cause the total duration of a bond index to decrease even as the durations of each subsector (short, mid, and long) increase?A. There is a coupon payment on the largest bond in the indexB. Some bonds in the index rollover from long to mid, and some from mid to shortC. The whole yield curve shifts down by a substantial amountD. This cannot happenAnswer: BAs a bond rolls from one sub-sector to. another, it can increase the duration of each subsector, while lowering the duration for the portfolio as a whole. For example, if the portfolio has asub-sector of bonds with maturities of 2-10 years, and a bond rolls from die longer maturitysub-sector to the mid-maturity one, it is removing a bond from the longer maturity sub-sector that has z lower duration as compared to others in that sub-sector, and adding it to the mid-maturity sub-sector with a duration value that is greater than the other bonds in the mid-maturity sub-sector. The aging of the bond lowers the duration for the portfolio as a whole.3 . Which of the following fixed-income securities most likely has negative effective duration?A. A range accrual noteB. A floating rate noteC. An interest-only tranche of a CMOD. A principal-only tranche of a CMOAnswer: CAn I-O tranche has negative duration because a decline in interest rates causes the I-O price to fall. As rates fall and mortgages begin to prepay, the flows of an I-O tranche vanish. (Whenever some of the principal is paid-off there is less available from which to collect interest.) When rates are very high and prepayments are low, the I-O is like a security with a fixed set of cash flows. Jt has greater notional amount based on which interest will be calculated. The price of an interest-only tranche wⅢmost likely increase as interest rate increases, leading to a negative effective duration.to maturity of 8%. Assume par value of the bond to be $1,000:A. 2.00 yearsB. 1.94 yearsC. 1.87 yearsD. 1.76 years5 . The option-adjusted duration of a callable bond will be close to the duration of a similar non-callable bond when the:A. Bond trades above the call priceB. Bond has a high volatilityC. Bond trades much lower than the call priceD. ' Bond trades above parity。

FRM一级模考FRM一级模拟题1 .Which concept gives a measure of historical value added per unit of risk taken and can be useful, among other tools, to risk managers?A. Trackingerror' B. Model alphaC. Information ratioD. HeteroskedasticityAnswer: CWilliam Sharpe developed the concept of information ratio to describe the value added per unit of risk by a manager or activity. It is usually developed by analyzing at least 36 months of returns. Tracking error is an estimate ofhow much risk a manager takes as a measure ofthe deviation from a benchmark.2.A stack-and-roti hedge as described in the Metallgesellschaft case is best described as:A. Buying futures contracts of different expirations and allowing them to expire in sequence.B. Buying futures contracts of different expirations and closing out the position shortly before expiration.C. Using short-term futures to hedge a long-term risk exposure by replacing them with longer-term contracts shortly before they expire.D. Using short-term futures contracts with a larger notional value than the long-term risk they are meant to hedge.Answer: CA stack is a bundle of futures contracts with the same expiration. Over time, a firm may acquire stacks with variousexpiry dates. To hedge a long-term risk exposure, a firm would close out each stack as it approaches expiry and enter into a contract with a more distant delivery, known as a roll.This strategy is called a stack-and-roll hedge and is designed to hedge long-term risk exposures with short-term contracts. Using short-term futures contracts with a larger notional value than the. long-term risk they are meant to hedge could result in over hedging" depending on.the hedge ratio.3 . Past financial disasters have resulted when a firm allows a trader to have dual roles as both the head of trading and the head of the back-office support function. Which of the following case studies did not involve this particular operational risk oversight?IDrysdale SecuritiesII DaiwaIII AlliedIrish BankIV BaringsA. IonlyB. II and IVC. I and IIIAnswer: CThe rogue traders for both Daiwa and Barings had dual rojes as both the head of trading and the head of the back-office support function. This operational risk oversight allowed them to hide millions in losses from senior management. In the Allied Irish Bank case, John Rusnak did not run the back-office operations. The Drysdale Securities case did not deal with a rogue trader.4 .Which of the following reasons does not help explain the problems -of LTCM inAugust and September 1998:A. A spike in correlationsB. An increase in stock index volatilitiesC. A drop in liquidity ' 'D. An increase in interest rates on on-the-run TreasuriesAnswer: DIncreased volatility and higher correlations led to substantial losses in LTCM's highly-leveraged portfolio. A significant drop in market liquidity forced LTCM to liquidate these highly-leveraged positions at substantial discounts. An increase in the spread between U.S. treasury rates and Russian government rates resulted in significant losses.5 .The following is not a problem of having one employee perform trading functionsand back office function s:A. The employee gets paid more because he performs two functions.B. The employee can hide trading mistakes when processing the trades.C. The employee can hide the size of his book.D. The employee firm may not know its true exposure.Answer: ATo minimize operational risk, trading and back office functions should not be performed by the same employee. The risks of doing so include hiding trading mistakes and hiding the size of exposures in the trading book. The extra direct compensation cost of paying the same employee to perform both functions is minimal compared to the potential operational risk costs.。

FRM一级模拟题1 . Consider a 7.75% semi-annual coupon bond with a par value of $100 and four remaining coupons, which is trading at a yield of 8.3750jo. There are 74 days remaining in the current period that has a total of 182 days. The accrued coupon of this bond is CLOSEST to:A. 1.59B. 2.29C. 3.18D. 4.57Answer: BStep l. Calculate w = 74 / 182 = 0.41.Step 2. Accrued coupon = coupon×(l - w) = l00×3.875%×(l - 0.4 1) = $2.2862 . Which of the following theories often used to explain the term structure of interest rates is based on the idea that most investors prefer short-term deposits, all else equal?A. Liquidity preference theory.B. Supply-demand theory.C. Market segmentation theory.D. Unbiased expectations theory.Answer: AThe liquidity preference theory suggests that the shape of the term structure is determined by the fact that most investors prefer short-term liquid assets, holding return constant.3 . Suppose a risk manager has made the mistake of valuing a zero-coupon bond using a swap (par) rate rather than a zero-coupon rate. Assume the par curve is upward sloping. The risk manager is thereforeA. Indifferent to the rate usedB. Over-estimating the value of the bondC. Under-estimating the value of the bondD. Lacking sufficient informationAnswer: BIf the par curve is rising, it must be below the spot curve , using par yield as discount rate , bond value is Pl , using spot rate as discount rate, bond value is PO, lower discount rate ,higher the bond value , so using a par rate rather than a zero-coupon rate overestimate the bond value.4 . What is the relationship between yield on the current inflation-proof bond issued by the U.S. Treasury and a standard Treasury bond with similar terms?A. The yields should be about the same.B. The yield of the inflation bond should be approximately the yield on the treasury minus the 'real interest.C. The yield of the inflation bond should be approximately the yield on the treasury plus the real interest.Answer: DThe yield on the inflation-protected bond is a real yield, or nominal yield minus expected inflation.5 . Which of the following statements about yield curve arbitrage is TRUE?A. No arbitrage conditions require that the zero coupon yield curve is either upward sloping or downward sloping.B. It is a violation of the no-arbitrage condition if the one-year interest rate is 10% or more, higher than the l0-year rate. 'C. As long as all discount factors are less than one but greater than zero, the curve is arbitrage free.D. The no-arbitrage condition requires all forward rates be non-negative.Answer: DFor a no-arbitrage condition to hold, both spot and forward rates must be positive.。

专注国际财经教育FRM一级模拟题1 . Which of the following are characteristics of catastrophe bonds?I Relatively short maturities compared to straight bonds.II Can have useful diversification qualities.III Less risky compared to straight bonds.IV Non-investment grade.A. I, II and IV onlyB. I and III onlyC. I, III, and IV onlyD. II and IV onlyAnswer: ABecause catastrophe bonds are riskier than straight bonds issued by the same firm, they usually have maturities less than three years and are usually non-investment-grade bonds. They also have potentially useful diversification qualities as their returns, being linked. to operational losses, are not highly correlated with market returns.Delta Hedging2 . Which type of derivative contract is least appropriate for a manufacturing company trying to hedge a rise in the cost of its raw materials?A. Long futuresB. Long call optionC. Short put optionD. Floating rate payer on commodity swap .Answer: DThe manufacturer should not be the floating-rate payer if it wants to hedge against an increase in commodity prices. It has a natural short position in the commodity and; thus should hedge to effectively lock in a fixed price. Shorting a put is not the bet strategy, but the premium may offset a flight increase in prices.3 . A trader buys a swaption on a l0-year Libor t0 5% semiannual swap, and, to keep the delta neutral, shorts government bonds. What can be said about the position?A. Volatility risk remains, as well as basis risk and interest rate risk. .B. Interest rate risk is completely eliminatedC. The position is delta-neutral and gamma-positive, hence profit is lockedD. Basis risk should first be hedgedAnswer: AThe value of the swaption is affected by changes in volatility (it has a positive vega). Shorting government bonds dejta-hedges the position, but does not eliminate the inherent volatility risk (vega), convexity risk (gamma), or interest rate risk (rho). Delta-hedging also creates basis risk (LIBOR versus Treasury rates).。

FRM一级模拟题(1)1、The price of INDO stock on any trading day can either increase or decrease. A risk analyst estimates that there is a 20% probability that the price of INDO stock will increase on any trading day. This probability is assumed to be the same for all trading days and the price changes on any given trading day are independent of changes on other days. Based on this information, what is the expected number of days the share price will decrease in the coming five days?A. 3B. 5C. 4D. 12. Which one of the foll owing four statements about hypothesis testing holds true if the level of significance decreases from 5% to 1%?A.It becomes more difficult to reject a null hypothesis when it is actually true.B.The probability of making a type I error increases.C.The probability of making a type II error decreases.D.The failure to reject the null hypothesis when it is actually false decreases to 1%.3. Assume that a rand om variable foll ows a normal distribution with a mean of 100 and a standard d eviation of17.5. What is the probability that this rand om variable value is between 82.5 and 135?A.68%B.81.9%C.82.8%D.95%4. In country X, the probability that a letter sent through the postal system reaches its destination is 2/3. Assume that each postal delivery is independent of every other postal delivery, and assume that if a wife receives a letter from her husband, she will certainly mail a response to her husband. Suppose a man in country X mails a letter to his wife (also in country X) through the postal system. If the man d oes not receive a response letter from his wife, what is the probability that his wife received his letter?A.1/3B.3/5C.2/3D.2/55. Let X and Y are two rand om variables representing the annual returns of two different portfolios. If E[X ] = 3, E[Y ] = 4, and E[XY ] = 11, then what is Cov[X, Y ]?A.-1B.0C.11D.126. Kelly Lewis is analyzing daily return data for a stock market ind ex. From the available data, she calculates that the average daily return is 0.0% and the standard deviation is 1.5%. Concerned that a normal distribution likely underestimates tail risk, she recalls from extreme value theory that a generalized Pareto distribution (GPD) can be used to approximate the probability that the daily return is greater than a loss level y, given the daily return is a loss. That is, if X represents the daily return, then:Using maximum likelihood estimation with the available historical data, she finds that parameter values of? = 0.005 and? = 0.015 provid e the best fit. Given the daily return is a loss, what is the probability that the daily return exceeds –4.5% using a normal distribution and a generalized Pareto distribution?ing a normal distribution: 99.74%; using a generalized Pareto distribution: 94.91%ing a normal distribution: 99.87%; using a generalized Pareto distribution: 94.91%ing a normal distribution: 99.74%; using a generalized Pareto distribution: 97.45%ing a normal distribution: 99.87%; using a generalized Pareto distribution: 94.45%7. Rational Investment Inc. is estimating a daily VaR for its fixed-income portfolio currently valued at $800 million. Using returns for the past 400 days (ord ered in decreasing order, from highest daily return to lowest daily return), the daily returns are the foll owing: 1.99%, 1.89%, 1.88%, 1.87%, . . . , –1.76%, –1.82%, –1.84%, –1.87%, –1.91%.At the 99% confidence l evel, estimate the daily d ollar VaR using the historical simulation method.A.$14.08mmB.$14.56mmC.$14.72mmD.$15.04mm8. Assume that the P/L distribution of a liquid asset is i.i.d. normally distributed. The position has a one-day VaRat the 95% confidence level of $100,000. Estimate the 10-day VaR of the same position at the 99% confid ence level.A.$1,000,000B.$450,000C.$320,000D.$220,0009. On March 13, 2008, William Tell, a fund manager for the Rossini fund, takes a short position in the March Treasury bond (T-bond) futures contract. He plans to deliver the cheapest-to-d eliver Treasury bond with a coupon of 41/2 percent payable semiannually on May 15 and November 15, a conversion factor of 1.3256, and a face value of USD 100,000. The delivery date is Friday, March 15. The settl ement price for the cheapest-to-deliver Treasury bond on March 13 is 682/32. Calculate the invoice price.A.$90,118.87B.$91,727.79C.$92,367.75D.$95,619.4710. A newly issued noncallable fixed-rate bond with 30-year maturity carries a coupon rate of 5.5% and trades at par. Its duration is 13.84 years and its convexity is 529.714. Which of the foll owing statements about this bond is true?A.If the bond were to start trading at a premium, its duration woul d decrease.B.If the bond were to start trading at a discount, its duration would not change.C.If the bond were to remain at par, its duration woul d increase as the bond aged.D.If the bond were to remain at par, its duration woul d increase as the bond aged.Answer and Explanation:1、Prob (price up) = 0.20, meaning that Prob (price d own) = 0.80. It is the same for all days. Price change in a given day is independ ent of the price change on other days. So, the number of days where the stock price goes d own within 5 trading days has a binomial distribution with parameter n = 5 and q = 1 –0.20 = 0.80. Its expected value is 5(0.80) = 4.2、Type I error: The rejection of the null hypothesis when it is actually true. Type II error: The failure to reject the null hypothesis when it is actually false.The significance level is the probability of making a type I error.3、(A) is incorrect. Almost 68% of the observations will be within the interval from one standard deviation below the mean to one standard d eviation above the mean, which is within the interval [100 –17.5; 100 +17.5].(B) is correct. 82.5 =100–17.5 and 135 = 100 + 2*17.5. So, the percentage is 34% on the left-hand side of the mean, plus 95%/2 on the right-hand side of the mean.(C) is incorrect. Almost 95% of the items will lie within the interval from two standard deviations bel ow the mean to two standard deviations above the mean, that is, within the interval [100 – 2 * 17.5; 100 + 2 * 17.5]. (D) is incorrect. This answer assumes wrongly that 97.5% of the observations will be within [100 – 2 * 17.5; 100 + 2 * 17.5].4、A = Event that the wife receives the man's letterB = Event that the man d oes not receive a response from his wifeWe need to find P(A|B).First, we know P(A) = 2/3.To get P(B), note that there are three possible scenarios.(1). His letter d oes not get to his wife—probability is 1/3.(2). Her response letter does not get to him—2/9 (= 2/3 * 1/3, probability that she gets his letter times the probability that her letter gets lost).(3). Her response letter d oes get to him—4/9 (= 2/3 * 2/3, probability that she gets his letter times the probability that her letter gets to him).He does not receive a response in scenarios 1 and 2, so P(B) = 5/9.Next, we also know P(B|A) = 1/3 (if she receives the l etter, she responds, so he d oes not get a response only if the letter is l ost, which happens with probability 1/3).Then, by Bayes' rule, P(A|B) = P(B|A) * P(A) / P(B) = (1/3) * (2/3) / (5/9) = 2/5.5、We can rewrite Cov[X, Y ] as E[XY ] – E[X ]E[Y ]. Then, Cov[X, Y ] = 11 – 3 * 4 = –1.(A) is correct because the formula was used correctly, E[XY ] – E[X ]E[Y ].(B) is incorrect because it assumes zero covariance, which is false when the formula is used.(C) is incorrect because the product of the two expectations of X and Y was not subtracted from the joint expectation E[XY ].(D) is incorrect because the covariance is not the product of the two expectations of X and Y.6、The GPD value is derived simply by plugging in y = –0.045 in the equation. The normal distribution value is derived by:Prob(X > –0.045 | X < 0) = 1 – Prob(X < –0.045|X < 0)= 1 – (Prob(X < 0|X < –0.045) * Prob(X < –0.045)) / Prob(X < 0)= 1 – (1.0 * Prob(X < –0.045)) / Prob(X < 0)= 1 – Prob(Z < –3) / Prob(Z < 0)= 1 – 0.0013/0.5= 0.99747、VaR = 1.82% * 800 = 14.56 million Topic:VaR, nonparametric calculation8、The question tests the ability to convert VaRs. The one-day VaR should be multiplied by the square root of time and the ratio of the confidence intervals to get the correct VaR.Alternative (A) simply multiplies the VaR by T.Alternative (C) multiplies the VaR by the square root of T.Alternative (D) multiplies by the square root of T but inverts the ratio (1.64/2.32) instead of (2.32/1.64).9、The invoice is based on a settlement price of 682/32 or 68.0625. The accrued interest is cal culated on the basis of the number of days since the last coupon payment date, November 15, and the delivery date, March 15. That is 121. During the current six-month period between coupon payment dates, November 15 to May 15, there are 182 days. Thus the accrued interest on $100,000 face value of the bond is:121/182 * $100,000 * 0.045/2 = $1,495.88The invoice price is:$100,000 * 0.680625 * 1.3256 + $1,495.88 = $91,719.5310、(A) is correct. At higher interest rates, the bond/price relationship is cl oser to linear than it is when rates are l ow. So, the new duration woul d be lower than 13.84. Alternatively, one can think of duration as a weighted average of the times when cash fl ows are made, where the weights are the percentage of the total value of the bond. When rates rise, the present values associated with the later payments are relatively smaller and the duration falls.(B) is incorrect because it is the exact opposite of (A), the correct answer.(C) is incorrect. It fails to recognize the logic stated in (A).(D) is incorrect because duration is a function of the bond's maturity and, all else constant, duration woul d decrease as the bond's maturity shortened.参与FRM的考生可按照复习计划有效进行,另外高顿网校官网考试辅导高清课程已经开通,还可索取FRM 考试通关宝典,针对性地讲解、训练、答疑、模考,对学习过程进行全程跟踪、分析、指导,可以帮助考生全面提升备考效果。