Chapter_08Risk and Return(公司理财原理,Brealey & Myers)

- 格式:ppt

- 大小:214.50 KB

- 文档页数:34

Principles of Corporate FinanceSeventh EditionRichard A. Brealey Stewart C. MyersSlides byMatthew WillSlides Edited byMinggao Shen8.Portfolio Theory8-2

McGraw Hill/IrwinCopyright ©2003 by The McGraw-Hill Companies, Inc. All rights reservedTopics CoveredPortfolio TheoryRisk vs. ReturnEfficient Frontier/Efficient PortfoliosPortfolio Theory with Lending Portfolio Theory with BorrowingPortfolio ChoiceThe Market Portfolio8-3

McGraw Hill/IrwinCopyright ©2003 by The McGraw-Hill Companies, Inc. All rights reservedMotivationFirst central intuition in finance:Markets are efficient.Second central intuition in finance:There is a trade-off between risk and return.8-4

McGraw Hill/IrwinCopyright ©2003 by The McGraw-Hill Companies, Inc. All rights reservedMotivationInvestment in one security allows no controlover risk and return featuresOne can only buy, watch performanceand possibly sell!!By investing in many securities a risk -returnprofile can be created to suit most investors risk attitudesUsually, by pooling together a number of risky securities in one portfolio the over all return can be made less volatile (risky)The investor is less likely to be exposed to rapid large losses -the risk has been reduced.Why Building a Portfolio ?

公司理财习题答案

第八章

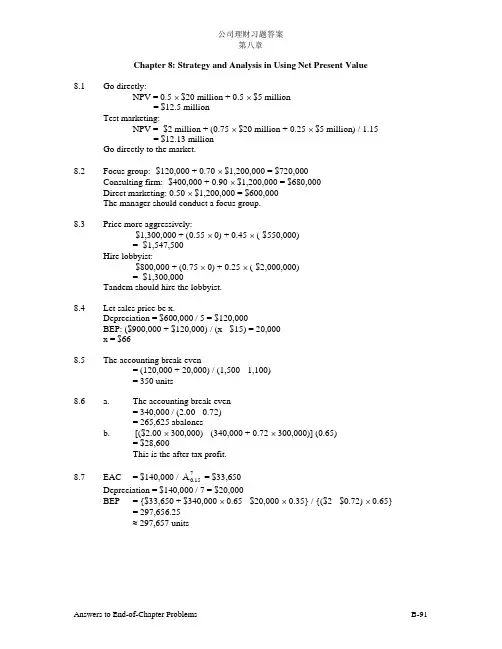

Answers to End-of-Chapter Problems B-91 Chapter 8: Strategy and Analysis in Using Net Present Value

8.1 Go directly:

NPV = 0.5 $20 million + 0.5 $5 million

= $12.5 million

Test marketing:

NPV = -$2 million + (0.75 $20 million + 0.25 $5 million) / 1.15

= $12.13 million

Go directly to the market.

8.2 Focus group: -$120,000 + 0.70 $1,200,000 = $720,000

Consulting firm: -$400,000 + 0.90 $1,200,000 = $680,000

Direct marketing: 0.50 $1,200,000 = $600,000

The manager should conduct a focus group.

8.3 Price more aggressively:

-$1,300,000 + (0.55 0) + 0.45 (-$550,000)

= -$1,547,500

Hire lobbyist:

-$800,000 + (0.75 0) + 0.25 (-$2,000,000)

= -$1,300,000

Tandem should hire the lobbyist.

8.4 Let sales price be x.

Depreciation = $600,000 / 5 = $120,000

BEP: ($900,000 + $120,000) / (x - $15) = 20,000

第十四章

1.优先股和负债的区别有:

1) 在确定公司应纳税收入时,优先股股利不能作为一项利息费用从而免于纳税。从个人投资者角度分析,优先股股利属于应纳税的普通收入。对企业投资者而言,他们投资优先股所获得的股利中有70%是可以免缴所得税的。

2) 在破产清算时,优先股次于负债,但优先于普通股。

3) 对于公司来说,没有法律义务一定要支付优先股股利,相反,公司有义务必须支付债券利息。因此如果没有发放下一年优先股股利,公司一定不是被迫违约的。优先股的应付股利既可以是“可累积”的,也可以是“非累积”的。公司也可以无限期拖延(当然股利无限期拖延支付会对股票市场产生负面影响)

2.有些公司可以从发行优先股中获益,具体原因有:

1) 规范的公共事业机构可以将发行优先股产生的税收劣势转嫁给顾客,因此大部分优先股股票都是由公共事业机构发行的。

2) 向国内税收总署汇报亏损的公司因为没有任何的债务利息可以从中抵扣的应税收入,所以优先股与负债比较而言不存在税收劣势。因此这些公司更愿意发行优先股。

3) 发行优先股的公司可以避免债务融资方式下可能出现的破产威胁。未付优先股股利并非公司债务,所以优先股股东不能以公司不支付股利为由胁迫公司破产清算。

3.不可转换优先股的收益低于公司债券的收益主要有两个原因:

1) 如果企业投资者投资优先股股票,其所获得的股利中有70%是可以免缴所得税的,因此企业投资者更愿意购买其他公司的优先股,从而必须对优先股支付升水,这也降低了优先股的收益率。

2) 发行公司愿意也有能力为债务提供更高的回报,因为债券的利息费用可以减少他们的税务负担。而优先股支付是来自净利润,因此他们不提供税盾。

因为个人投资者不具有税收减免优惠,所以绝大多数的优先股都为企业投资者持有。

4.公司负债与权益的最主要的差别是:

1) 负债不属于公司的所有者权益,因此债权人通常没有表决权,他们用来保护自身利益的工具就是借贷合约,又称“债务契约”。

8-1

1. Consider the following balance sheet for WatchoverU Savings, Inc. (in millions):

Assets Liabilities and Equity

Floating-rate mortgages 1-year time deposits

(currently 10% annually) $50 (currently 6% annually) $70

30-year fixed-rate loans 3-year time deposits

(currently 7% annually) $50 (currently 7% annually) $20

Equity $10

Total Assets $100 Total Liabilities & Equity $100

a. What is WatchoverU’s expected net interest income at year-end?

Current expected interest income: $50m(0.10) + $50m(0.07) = $8.5m.

Expected interest expense: $70m(0.06) - $20m(0.07) = $5.6m.

Expected net interest income: $8.5m - $5.6m = $2.9m.

b. What will net interest income be at year-end if interest rates rise by 2 percent?

After the 200 basis point interest rate increase, net interest income declines to: