公司理财期末整理(英文版)

- 格式:doc

- 大小:129.64 KB

- 文档页数:8

Chapter 3①The balance sheet②The income statement③The statement of cash flows④tax①The balance sheetEquation: total assets=total liabilities + shareholders’ equityNet working capital(NWC)=current asset – current liabilities是指企业的流动资产总额减Balance sheetCurrent Assets Current Liabilities•Cash & Securities payables•Receivables short-term debt•Inventories ++ long-term liabilitiesFixed Assets +•Tangible Assets shareholders’ equity•Intangible AssetsBook value& market value②the income statementThe income statementSales revenue $135,000Less: cost of sales 108,000Gross profits 27,000Less: Operating expenses 13,500Operating profits 13,500Less: Financing expense 1,350Net profits before taxes 12,150Less: Taxes (15%) 1,823Net profits after taxes $10,327In the income statement below, what was the value of Home Depot’s EBIT in 2009?EBIT = total Revenues -costs -deprecation③the statement of cash flowsExample:Net income for your firm was $10,000 last year. The depreciation expense was $2,500; accounts receivable increased $1,250; accounts payable increased $800; and inventories increased by $2,000.What was the total cash flow from operations for the period?Net income: 10,000Depreciation: 2,500Accounts Receivable: (1,250)Accounts Payable: 800Inventories: (2,000)Cash flow from operations: 10,050Free Cash FlowFree Cash Flow is cash available for distribution to investors after the firm pays for new investments or additions to working capital.Free cash flow = (EBIT – taxes + dep.) - change in net working capital- cap. expenditures④tax: 1.corporate tax2.personal tax一,marginal tax rate二,average tax rateChapter4MuaEvaBook rate of ruturnFinancial ratio (财务比率) and shareholders ’ valueThe Dupont systemprice x shares outstanding)Market value added: Market capitalization minus book value of equty.Market-to-book ratio=equityof value book equity of value market ...................Economic Value Added(EV A)Total capitalization: long-term debt + equityAfter tax operating income = after-tax interest + net incomeEVA :Show the firm’s truly created valueincome earned – income requiredBook Rates of Returnreturn on capital(ROC)资本收益率ROC=after-tax operating income/total capitalizationROC=after-tax operating income/average total capitalizationReturn on asset(ROA)资产收益率ROA=after-tax operating income/total assetsROA=after-tax operating income/average total assetsReturn on equity(ROE)股本回报率,产权回报率ROE=net income/equity因为是operating income 在上章可知operating income 是financial expenses 之前的,故还未减去interest ,故要加after-taxinterset)PPT 中关于ROA ,ROC ,ROE 的练习Financial ratios and shareholders ’ valueEconomic Value Added Operating Income* - [Cost of Capital Total Capitalization]=⨯Shareholder value depends on good investment and financing decisions.Financial Ratios help measure the success and soundness of these decisionsEfficiency RatiosAsset turnover ratio=sales/total assets at start of yearOr=sales/average total assetsReceivables turnover=sales/receivables at start of yearAverage collection period=receivables at start of year/average daily sales=365/receivable turnoverInventory turnover ratio=cost of goods sold/inventory at start of yearAverage days in inventory=inventory at start of year/daily cost of goods sold=365/inventory turnoverProfitability RatiosProfit margin(利润率)=net income/sales(IOPM)Operating profit margin=net income +after-tax interest/sales=after-tax operating income/salesLeverage Ratios杠杆率(debt and equity)Long-term debt ratio=long-term debt/long-term debt+equityLong-term debt equity ratio=long-term debt/equityMeasuring LeverageTotal debt ratio=total liability/total assetsTimes interest earned(利息保障率,利息保障倍数)=EBIT/interest payments用于衡量偿付贷款利息的能力Cash coverage ratio(现金涵盖比率)=EBIT+depreciation/interest paymentsLiquidity Ratios(短期还债能力指标/流动性指标)NWC to total assets ratio(经营运资金比)=net working capital/total assets(Net working capital=current asset – current liabilities) Current ratio(流动比率)=current assets/current liabilities(短期还债能力的一个指标)Quick ratio(速动比率)=cash + marketable securities(有价证券) + receivables/current liabilitiesCash ratio(现金比率)=cash + marketable securities/current liabilitiesThe Dupont systemROA= after-tax operating income/asset=assets sales x sales....income operating tax after -=assets turnover x operating profit margin=leverage ratio x asset turnover x operating profit margin x debt burden股息支付率 再投资率Or call sustainable growth rateChapter 5Future valuePresent valuePv of multiple cash flowsPerpetuitiesAnnutitiesFuture value of annutitiesAnnuities and annuities due EAR & APRAssets Sales Net Income Interest Net Income ROE=x x x Equity Assets Sales Net Income Interest++Dividends Payout Ratio=Earnings Earnings-Dividends Plowback Ratio=Earnings Growth in equity from plowback = Plowback Ratio ROE Earnings - Dividends Earnings Earnings Equity ⨯=⨯Earnings-Dividends = EquityInflationValuing real cash paymentsFuture valueSimple interest: FV simple =initial investment*(1+r*t)Compound interest: FV compound =initial investment*(1+r)tPresent valueDiscount rate: rDiscount factor: DF=t r )1(1+ Present value: PV=FV*t r )1(1+ PV of multiple cash flowsCt=the cash flows in year tExample: Your auto dealer gives you the choice to pay $15,500 cash now or make threepayments: $8,000 now and $4,000 at the end of the following two years. If your cost of money (discount rate) is 8%, which do you prefer?PerpetuitiesPV of perpetuity: PV=C/rExample: In order to create an endowment, which pays $185,000 per year forever, how much money must be set aside today if the rate of interest is 8%?What if the first payment won’t be received until 3 years from today?PV = 2312,500 / (1 + 0.08)3= 1,835,662.5annuities124,0001(1.08)4,0002(1.08)Initial Payment* 8,000.003,703.703,429.36Total PV $15,133.06PV of C PV of C ++=====185,000.08$2,312,500PV ==Present value of an annuity: PV=C*[r 1-t r r )1(1+] The terms within the brackets are collectively called the “annuity factor ”PV of multiple cash flowsFuture value of annuitiesExample: You plan to save $4,000 every year for 20 years and then retire. Given a 10% rate ofAnnuities due(即付年金)(与普通年金(即后付年金)的区别仅在于付款时间的不同,一个n 期的即付年金相当于一个n-1期的普通年金)(期不等于年)PV annuitydue =PV annuity (1+r) FV annuity due =FV annuity(1+r) Example: Suppose you invest $429.59 annually at the beginning of each year at 10% interest. After 50 years, how much would your investment be worth?EAR & APREffective annual interest rate: The period interest rate that is annualized using compound interest.EAR = (1 + monthly rate)12 - 1Annual Percentage Rate: The period interest rate that is annualized using simple interest APR = monthly rate × 12Example : Given a monthly rate of 1%, what is the Effective Annual Rate(EAR)? What is the Annual Percentage Rate (APR)?Inflation000,550$)10.1()000,500($)1(=⨯=+⨯=AD AD Annuity AD FV FV r FV FV %00.12)12()01.0(%68.121)01.1(12=⨯==-=APR EAR 1+nominal interest rate1+inflation rate 1real interest rate=+Valuing real cash payments♦ Example: You make a loan of $5,000 to Jane who will pay it back in 1 year. The interestrate is 8%, and the inflation rate is 5% now. What is the present value of Jane’s IOU? Show that you get the same answer when (a) discounting the nominal payment at the nominal rate and (b) discounting the real payment at the real rate.♦ (a) 5,000 / (1 + 8%) = $4630(b) 5,000 / (1.05) = $4762 (real dollar)4762 / (1.028) = $4630(2.8% is real interest rate)不能用实际利率去贴现名义现金流Chapter 6bond pricing:example: For a $1000 face value bond with a bid price of 103:05 and an asked price of 103:06, how much would an investor pay for the bond?PV=1)1(r coupon ++2)1(r coupon ++…+t r par coupon )1(++ PV bond =PV coupon +PV parvalue=coupon*(annuity factor)+ par value * (discout factor)Example: What is the value of a 3-year annuity that pays $90 each year and an additional$1,000 at the date of the final repayment? Assume a discount rate of 4%.Warning: bond rate inflation -rate interest nominal rate interest Real ≈()()6103% 103.1875% 321.031875$1,000 $1,031.875of face value ⎛⎫+= ⎪⎝⎭⨯=331(1.04)1$90$1,000.04(1.04)$1,138.75Bond PV --+=⨯+⨯+=()()1(1)where 1and (1)Bond Coupons ParValue Bond t tPV PV PV PV coupon Annuity Factor par value Discount Factor r Annuity Factor rDiscount Factor r -=+=⨯+⨯-+==+The coupon rate IS NOT the discount rate used in the Present Value calculations Example: What is the present value of a 4% coupon bond with face value $1,000 that matures in 3 years? Assume a discount rate of 5%. Bond yields Current yield : annual coupon payments divided by bond priceExample:Suppose you spend $1,150 for a $1,000 face value bond that pays a $60 annual coupon payment for 3 years. What is the bond’s current yield?Yield to maturity:PV=1)1(r coupon ++2)1(r coupon ++…+t r par coupon )1(++ Bond rates of returnRate of return 只算一年的couponYTM vs rate of returnYTM ↑ (↓)(unchange) → the price of bond ↓ (↑) (unchange) → the rate of return for that period less (greater)(equal to) than the yield to maturity.Ytm 通过改变price 去改变p1-p0 从而改变rate of return ,由rate of return 公式得,p1-p0和其成正比,ytm 与change in price 成反比,故ytm 与其成反比Chapter 7Stock marketP/E ratio(本益比): price per share divided by earnings per shareAsk price & bid priceAsk price: the price at which current shareholders are willing to sell their sharesBid price: the price at which investors are willing to buy sharesTerminologyinvestment change price +income Coupon =return of Rate investmentincome total =return of Rate1,market cap. 2.P/E ratio 3.dividend yieldExample: You are considering investing in a firm whose shares are currently selling for $50 per share with 1,000,000 shares outstanding. Expected dividends are $2/share and earnings are $6/share.What is the firm’s Market Cap? P/E Ratio? Dividend Yield?Measure of value1. book value2. liquidation value3.market valueBV= Assets - liabilitiesLV = Assets selling price – LiabilitiesMV = Tangible & intangible assets + Inv. OpportunitiesPrice and intrinsic valueVo 内在价值Example: What is the intrinsic value of a share of stock if expected dividends are $2/shareand the expected price in 1 year is $35/share? Assume a discount rate of 10%.Expected return(ER)Valuing common stocksdividend discount modelconsider three simplying cases1. no growth2. constant growth3. noconstant growth Market Capitalization $501,000,000$50,000,000$50P/E Ratio 8.33$6$2Dividend Yield .044%$50=⨯======HH H r P Div r Div r Div P )1(...)1()1(22110+++++++=1.2.Example: What should the price of a share of stock be if the firm will pay a $4 dividend in 1year that is expected to grow at a constant rate of 5%? Assume a discount rate of 10%.3.Example:A firm is expected to pay $2/share in dividends next year. Those dividends are expected to grow by 8% for the next three years and 6% thereafter. If the discount rate is 10%, what is the current price of this security?Required rates of returnExample: What rate of return should an investor expect on a share of stock with a $2 expected dividend and 8% growth rate that sells today for $60?Sustainable growth rateExample: Suppose a firm that pays out 35% of earnings as dividends and expects its return on equity to be 10%. What is the expected growth rate?Valuing growth stocksWhere: EPS= Earnings per share PVGO = Present Value of Growth OpportunitiesSuppose a stock is selling today for $55/share and there are 10,000,000 shares outstanding. If earnings are projected to be $20,000,000, how much value are investors assigning to growth per share? Assume a discount rate of 10%.Return on Equity Plowback Rate = :g ROE bearnings dividends where b earnings=⨯⨯-=.10(1.35).065 6.5%g =⨯-==Chapter 8(NPV ,EAA,IRR) 第8章( 重点复习单元):净现值及其他投资准则,会算NPV ,计算EAA (P191页),认识其他投评估指标(PP 回流期和 IRR 内含报酬率)及其判断准则(取大或取小),重点关注NPV 与IRR ,注意使用IRR 指标的前提是IRR<r (P199页)有关投资组合,要知道其大前提是资金是有约束的;单个项目的特征(可分/不可分),可分的单个项目之间的比较与排序用PI (收益指数)值来衡量,不可分的用各自的NPV 值来比较衡量,比较的前提是它们的寿命期是一样的,如果不一样的话就用最小共同寿命期法或等价年金法来比较 。

CHAPTER 8Making Capital Investment Decisions I. DEFINITIONSINCREMENTAL CASH FLOWSa 1. The changes in a firm’s future cash flows that are a direct consequence of accepting aproject are called _____ cash flows.a. incrementalb. stand-alonec. after-taxd. net present valuee. erosionDifficulty level: EasyEQUIVALENT ANNUAL COSTe 2. The annual annuity stream of payments with the same present value as a project’s costsis called the project’s _____ cost.a. incrementalb. sunkc. opportunityd. erosione. equivalent annualDifficulty level: EasySUNK COSTSc 3. A cost that has already been paid, or the liability to pay has already been incurred, isa(n):a. salvage value expense.b. net working capital expense.c. sunk cost.d. opportunity cost.e. erosion cost.Difficulty level: EasyOPPORTUNITY COSTSd 4. The most valuable investment given up if an alternative investment is chosen is a(n):a. salvage value expense.b. net working capital expense.c. sunk cost.d. opportunity cost.e. erosion cost.Difficulty level: EasyEROSION COSTSe 5. The cash flows of a new project that come at the expense of a firm’s existing projectsare called:a. salvage value expenses.b. net working capital expenses.c. sunk costs.d. opportunity costs.e. erosion costs.Difficulty level: EasyPRO FORMA FINANCIAL STATEMENTSa 6. A pro forma financial statement is one that:a. projects future years’ operations.b. is expressed as a percentage of the total assets of the firm.c. is expressed as a percentage of the total sales of the firm.d. is expressed relative to a chosen base year’s financial statement.e. reflects the past and current operations of the firm.Difficulty level: EasyMACRS DEPRECIATIONb 7. The depreciation method currently allowed under US tax law governing the acceleratedwrite-off of property under various lifetime classifications is called _____ depreciation.a. FIFOb. MACRSc. straight-lined. sum-of-years digitse. curvilinearDifficulty level: EasyDEPRECIATION TAX SHIELDc 8. The cash flow tax savings generated as a result of a firm’s tax-deductible depreciationexpense is called the:a. after-tax depreciation savings.b. depreciable basis.c. depreciation tax shield.d. operating cash flow.e. after-tax salvage value.Difficulty level: EasyCASH FLOWd 9. The cash flow from projects for a company is computed as the:a. net operating cash flow generated by the project, less any sunk costs and erosion costs.b. sum of the incremental operating cash flow and after-tax salvage value of the project.c. net income generated by the project, plus the annual depreciation expense.d. sum of the incremental operating cash flow, capital spending, and net working capitalexpenses incurred by the project.e. sum of the sunk costs, opportunity costs, and erosion costs of the project.Difficulty level: MediumII. CONCEPTSPRO FORMA INCOME STATEMENTb 10. The pro forma income statement for a cost reduction project:a. will reflect a reduction in the sales of the firm.b. will generally reflect no incremental sales.c. has to be prepared reflecting the total sales and expenses of a firm.d. cannot be prepared due to the lack of any project related sales.e. will always reflect a negative project operating cash flow.Difficulty level: EasyINCREMENTAL CASH FLOWb 11. One purpose of identifying all of the incremental cash flows related to a proposedproject is to:a. isolate the total sunk costs so they can be evaluated to determine if the project willadd value to the firm.b. eliminate any cost which has previously been incurred so that it can be omitted fromthe analysis of the project.c. make each project appear as profitable as possible for the firm.d. include both the proposed and the current operations of a firm in the analysis of theproject.e. identify any and all changes in the cash flows of the firm for the past year so they canbe included in the analysis.Difficulty level: MediumINCREMENTAL CASH FLOWe 12. Which of the following are examples of an incremental cash flow?I. an increase in accounts receivableII. a decrease in net working capitalIII. an increase in taxesIV. a decrease in the cost of goods solda. I and III onlyb. III and IV onlyc. I and IV onlyd. I, III, and IV onlye. I, II, III, and IVDifficulty level: MediumINCREMENTAL CASH FLOWc 13. Which one of the following is an example of an incremental cash flow?a. the annual salary of the company president which is a contractual obligationb. the rent on a warehouse which is currently being utilizedc. the rent on some new machinery that is required for an upcoming projectd. the property taxes on the currently owned warehouse which has been sitting idle butis going to be utilized for a new projecte. the insurance on a company-owned building which will be utilized for a new projectDifficulty level: MediumINCREMENTAL COSTSd 14. Project analysis is focused on _____ costs.a. sunkb. totalc. variabled. incrementale. fixedDifficulty level: MediumSUNK COSTc 15. Sunk costs include any cost that:a. will change if a project is undertaken.b. will be incurred if a project is accepted.c. has previously been incurred and cannot be changed.d. is paid to a third party and cannot be refunded for any reason whatsoever.e. will occur if a project is accepted and once incurred, cannot be recouped.Difficulty level: EasySUNK COSTd 16. You spent $500 last week fixing the transmission in your car. Now, the brakes areacting up and you are trying to decide whether to fix them or trade the car in for anewer model. In analyzing the brake situation, the $500 you spent fixing thetransmission is a(n) _____ cost.a. opportunityb. fixedc. incrementald. sunke. relevantDifficulty level: EasyEROSIONb 17. Erosion can be explained as the:a. additional income generated from the sales of a newly added product.b. loss of current sales due to a new project being implemented.c. loss of revenue due to employee theft.d. loss of revenue due to customer theft.e. loss of cash due to the expenses required to fix a parking lot after a heavy rain storm.Difficulty level: EasyEROSIONa 18. Which of the following are examples of erosion?I. the loss of sales due to increased competition in the product marketII. the loss of sales because your chief competitor just opened a store across the street from your storeIII. the loss of sales due to a new product which you recently introducedIV. the loss of sales due to a new product recently introduced by your competitora. III onlyb. III and IV onlyc. I, III and IV onlyd. II and IV onlye. I, II, III, and IVDifficulty level: MediumTYPES OF COSTSd 19. Which of the following should be included in the analysis of a project?I. sunk costsII. opportunity costsIII. erosion costsIV. incremental costsa. I and II onlyb. III and IV onlyc. II and IV onlyd. II, III, and IV onlye. I, II, and IV onlyDifficulty level: MediumNET WORKING CAPITALd 20. All of the following are anticipated effects of a proposed project. Which of theseshould be included in the initial project cash flow related to net working capital?I. an inventory decrease of $5,000II. an increase in accounts receivable of $1,500III. an increase in fixed assets of $7,600IV. a decrease in accounts payable of $2,100a. I and II onlyb. I and III onlyc. II and IV onlyd. I, II, and IV onlye. I, II, III, and IVDifficulty level: MediumNET WORKING CAPITALa 21. Changes in the net working capital:a. can affect the cash flows of a project every year of the project’s life.b. only affect the initial cash flows of a project.c. are included in project analysis only if they represent cash outflows.d. are generally excluded from project analysis due to their irrelevance to the totalproject.e. affect the initial and the final cash flows of a project but not the cash flows of themiddle years.Difficulty level: MediumNET WORKING CAPITALc 22. Which one of the following will decrease net working capital of a firm?a. a decrease in accounts payableb. an increase in inventoryc. a decrease in accounts receivabled. an increase in the firm’s checking account balancee. a decrease in fixed assetsDifficulty level: EasyNET WORKING CAPITALd 23. Net working capital:a. can be ignored in project analysis because any expenditure is normally recouped by theend of the project.b. requirements generally, but not always, create a cash inflow at the beginning of aproject.c. expenditures commonly occur at the end of a project.d. is frequently affected by the additional sales generated by a new project.e. is the only expenditure where at least a partial recovery can be made at the end of aproject.Difficulty level: EasyMACRSd 24. A company which uses the MACRS system of depreciation:a. will have equal depreciation costs each year of an asset’s life.b. will expense the cost of nonresidential real estate over a period of 7 years.c. can depreciate the cost of land, if they so desire.d. will write off the entire cost of an asset over the asset’s class life.e. cannot expense any of the cost of a new asset during the first year of the asset’s life.Difficulty level: EasyMACRSa 25. Bet ‘r Bilt Toys just purchased some MACRS 5-year property at a cost of $230,000.Which of the following will correctly give you the book value of this equipment at theend of year 2?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%I. 52% of the asset costII. 48% of the asset costIII. 68% of 80% of the asset costIV. the asset cost, minus 20% of the asset cost, minus 32% of 80% of the asset costa. II onlyb. III and IV onlyc. I and III onlyd. II and IV onlye. I, II, III, and IVDifficulty level: EasyMACRSe 26. Will Do, Inc. just purchased some equipment at a cost of $650,000. What is theproper methodology for computing the depreciation expense for year 3 if theequipment is classified as 5-year property for MACRS?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $650,000 ⨯ (1-.20) ⨯ (1-.32) ⨯ (1-.192)b. $650,000 ⨯ (1-.20) ⨯ (1-.32)c. $650,000 ⨯ (1+.20) ⨯ (1+.32) ⨯ (1+.192)d. $650,000 ⨯ (1-.192)e. $650,000 ⨯ .192Difficulty level: MediumBOOK VALUEd 27. The book value of an asset is primarily used to compute the:a. annual depreciation tax shield.b. amount of cash received from the sale of an asset.c. amount of tax saved annually due to the depreciation expense.d. amount of tax due on the sale of an asset.e. change in depreciation needed to reflect the market value of the asset.Difficulty level: EasySALVAGE VALUEc 28. The salvage value of an asset creates an after-tax cash inflow to the firm in an amountequal to the:a. sales price of the asset.b. sales price minus the book value.c. sales price minus the tax due based on the sales price minus the book value.d. sales price plus the tax due based on the sales price minus the book value.e. sales price plus the tax due based on the book value minus the sales price.Difficulty level: EasySALVAGE VALUEe 29. The pre-tax salvage value of an asset is equal to the:a. book value if straight-line depreciation is used.b. book value if MACRS depreciation is used.c. market value minus the book value.d. book value minus the market value.e. market value.Difficulty level: EasyPROJECT OCFa 30. A project’s operating cash flow will increase when:a. the depreciation expense increases.b. the sales projections are lowered.c. the interest expense is lowered.d. the net working capital requirement increases.e. the earnings before interest and taxes decreases.Difficulty level: EasyPROJECT CASH FLOWSc 31. The cash flows of a project should:a. be computed on a pre-tax basis.b. include all sunk costs and opportunity costs.c. include all incremental costs, including opportunity costs.d. be applied to the year when the related expense or income is recognized by GAAP.e. include all financing costs related to new debt acquired to finance the project.Difficulty level: EasyPROJECT OCFa 32. Which of the following are correct methods for computing the operating cash flow ofa project assuming that the interest expense is equal to zero?I. EBIT + Depreciation - TaxesII. EBIT + Depreciation + TaxesIII. Net Income + DepreciationIV. (Sales – Costs) ⨯ (Taxes + Depreciation) ⨯ (1-Taxes)a. I and III onlyb. II and IV onlyc. II and III onlyd. I, III, and IV onlye. II, III, and IV onlyDifficulty level: MediumBOTTOM-UP OCFb 33. The bottom-up approach to computing the operating cash flow applies only when:a. both the depreciation expense and the interest expense are equal to zero.b. the interest expense is equal to zero.c. the project is a cost-cutting project.d. no fixed assets are required for the project.e. taxes are ignored and the interest expense is equal to zero.Difficulty level: MediumTOP-DOWN OCFa 34. The top-down approach to computing the operating cash flow:a. ignores all noncash items.b. applies only if a project produces sales.c. can only be used if the entire cash flows of a firm are included.d. is equal to sales - costs - taxes + depreciation.e. includes the interest expense related to a project.Difficulty level: MediumTAX SHIELDd 35. An increase in which one of the following will increase the operating cash flow?a. employee salariesb. office rentc. building maintenanced. equipment depreciatione. equipment rentalDifficulty level: EasyTAX SHIELDc 36. Tax shield refers to a reduction in taxes created by:a. a reduction in sales.b. an increase in interest expense.c. noncash expenses.d. a project’s incremental expenses.e. opportunity costs.Difficulty level: EasyCOST-CUTTINGc 37. A project which is designed to improve the manufacturing efficiency of a firm but willgenerate no additional sales is referred to as a(n) _____ project.a. sunk costb. opportunityc. cost-cuttingd. revenue-cuttinge. revenue-generatingDifficulty level: EasyEQUIVALENT ANNUAL COSTc 38. Toni’s Tools is comparing machines to determine which one to purchase. Themachines sell for differing prices, have differing operating costs, differing machinelives, and will be replaced when worn out. These machines should be compared using:a. net present value only.b. both net present value and the internal rate of return.c. their effective annual costs.d. the depreciation tax shield approach.e. the replacement parts approach.Difficulty level: MediumEQUIVALENT ANNUAL COSTe 39. The equivalent annual cost method is useful in determining:a. the annual operating cost of a machine if the annual maintenance is performed versuswhen the maintenance is not performed as recommended.b. the tax shield benefits of depreciation given the purchase of new assets for a project.c. operating cash flows for cost-cutting projects of equal duration.d. which one of two machines to acquire given equal machine lives but unequal machinecosts.e. which one of two machines to purchase when the machines are mutually exclusive,have different machine lives, and will be replaced once they are worn out.Difficulty level: MediumIII. PROBLEMSRELEVANT CASH FLOWSd 40. Marshall’s & Co. purchased a corner lot in Eglon City five y ears ago at a cost of$640,000. The lot was recently appraised at $810,000. At the time of the purchase, thecompany spent $50,000 to grade the lot and another $4,000 to build a small buildingon the lot to house a parking lot attendant who has overseen the use of the lot for dailycommuter parking. The company now wants to build a new retail store on the site. Thebuilding cost is estimated at $1.2 million. What amount should be used as the initialcash flow for this building project?a. $1,200,000b. $1,840,000c. $1,890,000d. $2,010,000e. $2,060,000Difficulty level: MediumRELEVANT CASH FLOWSe 41. Jamestown Ltd. currently produces boat sails and is considering expanding itsoperations to include awnings for homes and travel trailers. The company owns landbeside its current manufacturing facility that could be used for the expansion. Thecompany bought this land ten years ago at a cost of $250,000. Today, the land isvalued at $425,000. The grading and excavation work necessary to build on the landwill cost $15,000. The company currently has some unused equipment which itcurrently owns valued at $60,000. This equipment could be used for producingawnings if $5,000 is spent for equipment modifications. Other equipment costing$780,000 will also be required. What is the amount of the initial cash flow for thisexpansion project?a. $800,000b. $1,050,000c. $1,110,000d. $1,225,000e. $1,285,000Difficulty level: MediumRELEVANT CASH FLOWSb 42. Wilbert’s, Inc. paid $90,000, in cash, for a piece of equipment three years ago. Lastyear, the company spent $10,000 to update the equipment with the latest technology.The company no longer uses this equipment in their current operations and hasreceived an offer of $50,000 from a firm who would like to purchase it. Wilbert’s isdebating whether to sell the equipment or to expand their operations such that theequipment can be used. When evaluating the expansion option, what value, if any,should Wilbert’s assign to this equipment as an initial cost of the project?a. $40,000b. $50,000c. $60,000d. $80,000e. $90,000Difficulty level: EasyRELEVANT CASH FLOWSa 43. Walks Softly, Inc. sells customized shoes. Currently, they sell 10,000 pairs of shoesannually at an average price of $68 a pair. They are considering adding a lower-pricedline of shoes which sell for $49 a pair. Walks Softly estimates they can sell 5,000 pairsof the lower-priced shoes but will sell 1,000 less pairs of the higher-priced shoes bydoing so. What is the amount of the sales that should be used when evaluating theaddition of the lower-priced shoes?a. $177,000b. $245,000c. $313,000d. $789,000e. $857,000Difficulty level: MediumOPPORTUNITY COSTc 44. Your firm purchased a warehouse for $335,000 six years ago. Four years ago, repairswere made to the building which cost $60,000. The annual taxes on the property are$20,000. The warehouse has a current book value of $268,000 and a market value of$295,000. The warehouse is totally paid for and solely owned by your firm. If thecompany decides to assign this warehouse to a new project, what value, if any, shouldbe included in the initial cash flow of the project for this building?a. $0b. $268,000c. $295,000d. $395,000e. $515,000Difficulty level: EasyOPPORTUNITY COSTd 45. You own a house that you rent for $1,200 a month. The maintenance expenses onthe house average $200 a month. The house cost $89,000 when you purchased itseveral years ago. A recent appraisal on the house valued it at $210,000. The annualproperty taxes are $5,000. If you sell the house you will incur $20,000 in expenses.You are deciding whether to sell the house or convert it for your own use as aprofessional office. What value should you place on this house when analyzing theoption of using it as a professional office?a. $89,000b. $120,000c. $185,000d. $190,000e. $210,000Difficulty level: MediumOPPORTUNITY COSTc 46. Big Joe’s owns a manufacturing facility that is currently sitting idle. The facility islocated on a piece of land that originally cost $129,000. The facility itself cost$650,000 to build. As of now, the book value of the land and the facility are $129,000and $186,500, respectively. Big Joe’s received an offer of $590,000 for the land andfacility last week. They rejected this offer even though they were told that it is areasonable offer in today’s market. If Big Joe’s were to consider using this land andfacility in a new project, what cost, if any, should they include in the project analysis?a. $0b. $315,500c. $590,000d. $650,000e. $779,000Difficulty level: EasyEROSION COSTb 47. Jamie’s Motor Home Sales currently sells 1,000 Class A motor homes, 2,500 Class Cmotor homes, and 4,000 pop-up trailers each year. Jamie is considering adding a mid-range camper and expects that if she does so she can sell 1,500 of them. However, ifthe new camper is added, Jamie expects that her Class A sales will decline to 950 unitswhile the Class C campers decline to 2,200. The sales of pop-ups will not be affected.Class A motor homes sell for an average of $125,000 each. Class C homes are pricedat $39,500 and the pop-ups sell for $5,000 each. The new mid-range camper will sellfor $47,900. What is the erosion cost?a. $6,250,000b. $18,100,000c. $53,750,000d. $93,150,000e. $118,789,500Difficulty level: MediumOCFe 48. Ernie’s E lectrical is evaluating a project which will increase sales by $50,000 andcosts by $30,000. The project will cost $150,000 and be depreciated straight-line to azero book value over the 10 year life of the project. The applicable tax rate is 34%.What is the operating cash flow for this project?a. $3,300b. $5,000c. $8,300d. $13,300e. $18,300Difficulty level: MediumOCFd 49. Kurt’s Kabinets is looking at a project that will require $80,000 in fixed assets andanother $20,000 in net working capital. The project is expected to produce sales of$110,000 with associated costs of $70,000. The project has a 4-year life. The companyuses straight-line depreciation to a zero book value over the life of the project. The taxrate is 35%. What is the operating cash flow for this project?a. $7,000b. $13,000c. $27,000d. $33,000e. $40,000Difficulty level: MediumBOTTOM-UP OCFc 50. Peter’s Boats has sales of $760,000 and a profit margin of 5%. The annualdepreciation expense is $80,000. What is the amount of the operating cash flow if thecompany has no long-term debt?a. $34,000b. $86,400c. $118,000d. $120,400e. $123,900Difficulty level: MediumBOTTOM-UP OCFd 51. Le Place has sales of $439,000, depreciation of $32,000, and net working capital of$56,000. The firm has a tax rate of 34% and a profit margin of 6%. Thefirm has no interest expense. What is the amount of the operating cash flow?a. $49,384b. $52,616c. $54,980d. $58,340e. $114,340Difficulty level: MediumTOP-DOWN OCFb 52. Ben’s Border Café is considering a project which will produce sales of $16,000 andincrease cash expenses by $10,000. If the project is implemented, taxes will increasefrom $23,000 to $24,500 and depreciation will increase from $4,000 to $5,500. Whatis the amount of the operating cash flow using the top-down approach?a. $4,000b. $4,500c. $6,000d. $7,500e. $8,500Difficulty level: MediumTOP-DOWN OCFc 53. Ronnie’s Coffee House i s considering a project which will produce sales of $6,000and increase cash expenses by $2,500. If the project is implemented, taxes willincrease by $1,300. The additional depreciation expense will be $1,000. An initial cashoutlay of $2,000 is required for net working capital. What is the amount of theoperating cash flow using the top-down approach?a. $200b. $1,500c. $2,200d. $3,500e. $4,200Difficulty level: MediumTAX SHIELD OCFc 54. A project will increase sales by $60,000 and cash expenses by $51,000. The projectwill cost $40,000 and be depreciated using straight-line depreciation to a zero bookvalue over the 4-year life of the project. The company has a marginal tax rate of 35%.What is the operating cash flow of the project using the tax shield approach?a. $5,850b. $8,650c. $9,350d. $9,700e. $10,350Difficulty level: MediumDEPRECIATION TAX SHIELDa 55. A project will increase sales by $140,000 and cash expenses by $95,000. The projectwill cost $100,000 and be depreciated using the straight-line method to a zero bookvalue over the 4-year life of the project. The company has a marginal tax rate of 34%.What is the value of the depreciation tax shield?a. $8,500b. $17,000c. $22,500d. $25,000e. $37,750Difficulty level: MediumMACRS DEPRECIATIONd 56. Sun Lee’s Furniture just purchased some fixed assets classified as 5-year property forMACRS. The assets cost $24,000. What is the amount of the depreciation expense forthe third year?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $2,304b. $2,507c. $2,765d. $4,608e. $4,800Difficulty level: EasyMACRS DEPRECIATIONa 57. You just purchased some equipment that is classified as 5-year property for MACRS.The equipment cost $67,600. What will the book value of this equipment be at the endof three years should you decide to resell the equipment at that point in time?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $19,468.80b. $20,280.20c. $27,040.00d. $48,131.20e. $48,672.00Difficulty level: MediumMACRS DEPRECIATIONd 58. LiCheng’s Enterprises just purchased some fixed assets that are classified as 3-yearproperty for MACRS. The assets cost $1,900. What is the amount of thedepreciation expense for year 2?MACRS 3-year propertyYear Rate1 33.33%2 44.44%3 14.82%4 7.41%a. $562.93b. $633.27c. $719.67d. $844.36e. $1,477.63Difficulty level: MediumMACRS DEPRECIATIONb 59. RP&A, Inc. purchased some fixed assets four years ago at a cost of $19,800. They nolonger need these assets so are going to sell them today at a price of $3,500. The assetsare classified as 5-year property for MACRS. What is the current book value of theseassets?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $1,140.48b. $3,421.44c. $3,500.00d. $4,016.67e. $5,702.40Difficulty level: MediumSALVAGE VALUEa 60. You own some equipment which you purchased three years ago at a cost of $135,000.The equipment is 5-year property for MACRS. You are considering selling theequipment today for $82,500. Which one of the following statements is correct if yourtax rate is 34%?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. The tax due on the sale is $14,830.80.b. The book value today is $8,478.c. The book value today is $64,320.d. The taxable amount on the sale is $38,880.e. You will receive a tax refund of $13,219.20 as a result of this sale.。

公司理财习题答案第四章Chapter 4: Net Present Value4.1 a. $1,000 ⨯ 1.0510 = $1,628.89b. $1,000 ⨯ 1.0710 = $1,967.15c. $1,000 ⨯ 1.0520 = $2,653.30d. Interest compounds on the I nterest already earned. Therefore, the interest earnedin part c, $1,653.30, is more than double the amount earned in part a, $628.89.4.2 a. $1,000 / 1.17 = $513.16b. $2,000 / 1.1 = $1,818.18c. $500 / 1.18 = $233.254.3 You can make your decision by computing either the present value of the $2,000 that youcan receive in ten years, or the future value of the $1,000 that you can receive now.Present value: $2,000 / 1.0810 = $926.39Future value: $1,000 ⨯ 1.0810 = $2,158.93Either calculation indicates you should take the $1,000 now.4.4 Since this bond has no interim coupon payments, its present value is simply the presentvalue of the $1,000 that will be received in 25 years. Note: As will be discussed in the next chapter, the present value of the payments associated with a bond is the price of that bond.PV = $1,000 /1.125 = $92.304.5 PV = $1,500,000 / 1.0827 = $187,780.234.6 a. At a discount rate of zero, the future value and present value are always the same.Remember, FV = PV (1 + r) t. If r = 0, then the formula reduces to FV = PV.Therefore, the values of the options are $10,000 and $20,000, respectively. Youshould choose the second option.b. Option one: $10,000 / 1.1 = $9,090.91Option two: $20,000 / 1.15 = $12,418.43Choose the second option.c. Option one: $10,000 / 1.2 = $8,333.33Option two: $20,000 / 1.25 = $8,037.55Choose the first option.d. You are indifferent at the rate that equates the PVs of the two alternatives. Youknow that rate must fall between 10% and 20% because the option you wouldchoose differs at these rates. Let r be the discount rate that makes you indifferentbetween the options.$10,000 / (1 + r) = $20,000 / (1 + r)5(1 + r)4 = $20,000 / $10,000 = 21 + r = 1.18921r = 0.18921 = 18.921%4.7 PV of Joneses’ offer = $150,000 / (1.1)3 = $112,697.22Since the PV of Joneses’ offer is less than Smiths’ offer, $115,000, you should chooseSmiths’ offer.4.8 a. P0 = $1,000 / 1.0820 = $214.55b. P10 = P0 (1.08)10 = $463.20c. P15 = P0 (1.08)15 = $680.594.9 The $1,000 that you place in the account at the end of the first year will earn interest for sixyears. The $1,000 that you place in the account at the end of the second year will earninterest for five years, etc. Thus, the account will have a balance of$1,000 (1.12)6 + $1,000 (1.12)5 + $1,000 (1.12)4 + $1,000 (1.12)3= $6,714.614.10 PV = $5,000,000 / 1.1210 = $1,609,866.184.11 a. The cost of investment is $900,000.PV of cash inflows = $120,000 / 1.12 + $250,000 / 1.122 + $800,000 / 1.123= $875,865.52Since the PV of cash inflows is less than the cost of investment, you should notmake the investment.b. NPV = -$900,000 + $875,865.52= -$24,134.48c. NPV = -$900,000 + $120,000 / 1.11 + $250,000 / 1.112 + $800,000 / 1.113= $-4,033.18Since the NPV is still negative, you should not make the investment.4.12 NPV = -($340,000 + $10,000) + ($100,000 - $10,000) / 1.1+ $90,000 / 1.12 + $90,000 / 1.13 + $90,000 / 1.14 + $100,000 / 1.15= -$2,619.98Since the NPV is negative, you should not buy it.If the relevant cost of capital is 9 percent,NPV = -$350,000 + $90,000 / 1.09 + $90,000 / 1.092 + $90,000 / 1.093+ $90,000 / 1.094 + $100,000 / 1.095= $6,567.93Since the NPV is positive, you should buy it.4.13 a. Profit = PV of revenue - Cost = NPVNPV = $90,000 / 1.15 - $60,000 = -$4,117.08No, the firm will not make a profit.b. Find r that makes zero NPV.$90,000 / (1+r)5 - $60,000 = $0(1+r)5 = 1.5r = 0.08447 = 8.447%4.14 The future value of the decision to own your car for one year is the sum of the trade-invalue and the benefit from owning the car. Therefore, the PV of the decision to own thecar for one year is$3,000 / 1.12 + $1,000 / 1.12 = $3,571.43Since the PV of the roommate’s offer, $3,500, is lower than the aunt’s offer, you shouldaccept aunt’s offer.4.15 a. $1.000 (1.08)3 = $1,259.71b. $1,000 [1 + (0.08 / 2)]2 ⨯ 3 = $1,000 (1.04)6 = $1,265.32c. $1,000 [1 + (0.08 / 12)]12 ⨯ 3 = $1,000 (1.00667)36 = $1,270.24d. $1,000 e0.08 ⨯ 3 = $1,271.25公司理财习题答案第四章e. The future value increases because of the compounding. The account is earninginterest on interest. Essentially, the interest is added to the account balance at theend of every compounding period. During the next period, the account earnsinterest on the new balance. When the compounding period shortens, the balancethat earns interest is rising faster.4.16 a. $1,000 e0.12 ⨯ 5 = $1,822.12b. $1,000 e0.1 ⨯ 3 = $1,349.86c. $1,000 e0.05 ⨯ 10 = $1,648.72d. $1,000 e0.07 ⨯ 8 = $1,750.674.17 PV = $5,000 / [1+ (0.1 / 4)]4 ⨯ 12 = $1,528.364.18 Effective annual interest rate of Bank America= [1 + (0.041 / 4)]4 - 1 = 0.0416 = 4.16%Effective annual interest rate of Bank USA= [1 + (0.0405 / 12)]12 - 1 = 0.0413 = 4.13%You should deposit your money in Bank America.4.19 The price of the consol bond is the present value of the coupon payments. Apply theperpetuity formula to find the present value. PV = $120 / 0.15 = $8004.20 Quarterly interest rate = 12% / 4 = 3% = 0.03Therefore, the price of the security = $10 / 0.03 = $333.334.21 The price at the end of 19 quarters (or 4.75 years) from today = $1 / (0.15 ÷ 4) = $26.67The current price = $26.67 / [1+ (.15 / 4)]19 = $13.254.22 a. $1,000 / 0.1 = $10,000b. $500 / 0.1 = $5,000 is the value one year from now of the perpetual stream. Thus,the value of the perpetuity is $5,000 / 1.1 = $4,545.45.c. $2,420 / 0.1 = $24,200 is the value two years from now of the perpetual stream.Thus, the value of the perpetuity is $24,200 / 1.12 = $20,000.4.23 The value at t = 8 is $120 / 0.1 = $1,200.Thus, the value at t = 5 is $1,200 / 1.13 = $901.58.4.24 P = $3 (1.05) / (0.12 - 0.05) = $45.004.25 P = $1 / (0.1 - 0.04) = $16.674.26 The first cash flow will be generated 2 years from today.The value at the end of 1 year from today = $200,000 / (0.1 - 0.05) = $4,000,000.Thus, PV = $4,000,000 / 1.1 = $3,636,363.64.4.27 A zero NPV-$100,000 + $50,000 / r = 0-r = 0.54.28 Apply the NPV technique. Since the inflows are an annuity you can use the present valueof an annuity factor.NPV = -$6,200 + $1,200 8A1.0= -$6,200 + $1,200 (5.3349)= $201.88Yes, you should buy the asset.4.29 Use an annuity factor to compute the value two years from today of the twenty payments.Remember, the annuity formula gives you the value of the stream one year before the first payment. Hence, the annuity factor will give you the value at the end of year two of the stream of payments. Value at the end of year two = $2,000 20A08.0= $2,000 (9.8181)= $19,636.20The present value is simply that amount discounted back two years.PV = $19,636.20 / 1.082 = $16,834.884.30 The value of annuity at the end of year five= $500 15A = $500 (5.84737) = $2,923.6915.0The present value = $2,923.69 / 1.125 = $1,658.984.31 The easiest way to do this problem is to use the annuity factor. The annuity factor must beequal to $12,800 / $2,000 = 6.4; remember PV =C A t r. The annuity factors are in theappendix to the text. To use the factor table to solve this problem, scan across the rowlabeled 10 years until you find 6.4. It is close to the factor for 9%, 6.4177. Thus, the rate you will receive on this note is slightly more than 9%.You can find a more precise answer by interpolating between nine and ten percent.10% ⎤ 6.1446 ⎤a ⎡ r ⎥bc ⎡ 6.4 ⎪ d⎣ 9% ⎦⎣ 6.4177 ⎦By interpolating, you are presuming that the ratio of a to b is equal to the ratio of c to d.(9 - r ) / (9 - 10) = (6.4177 - 6.4 ) / (6.4177 - 6.1446)r = 9.0648%The exact value could be obtained by solving the annuity formula for the interest rate.Sophisticated calculators can compute the rate directly as 9.0626%.公司理财习题答案第四章4.32 a. The annuity amount can be computed by first calculating the PV of the $25,000which you need in five years. That amount is $17,824.65 [= $25,000 / 1.075].Next compute the annuity which has the same present value.$17,824.65 = C 5A.007$17,824.65 = C (4.1002)C = $4,347.26Thus, putting $4,347.26 into the 7% account each year will provide $25,000 fiveyears from today.b. The lump sum payment must be the present value of the $25,000, i.e., $25,000 /1.075 = $17,824.65The formula for future value of any annuity can be used to solve the problem (seefootnote 14 of the text).4.33The amount of loan is $120,000 ⨯ 0.85 = $102,000.20C A= $102,000.010The amount of equal installments isC = $102,000 / 20A = $102,000 / 8.513564 = $11,980.8810.04.34 The present value of salary is $5,000 36A = $150,537.53.001The present value of bonus is $10,000 3A = $23,740.42 (EAR = 12.68% is used since.01268bonuses are paid annually.)The present value of the contract = $150,537.53 + $23,740.42 = $174,277.944.35 The amount of loan is $15,000 ⨯ 0.8 = $12,000.C 48A = $12,0000067.0The amount of monthly installments isC = $12,000 / 48A = $12,000 / 40.96191 = $292.960067.04.36 Option one: This cash flow is an annuity due. To value it, you must use the after-taxamounts. The after-tax payment is $160,000 (1 - 0.28) = $115,200. Value all except the first payment using the standard annuity formula, then add back the first payment of$115,200 to obtain the value of this option.Value = $115,200 + $115,200 30A10.0= $115,200 + $115,200 (9.4269)= $1,201,178.88Option two: This option is valued similarly. You are able to have $446,000 now; this is already on an after-tax basis. You will receive an annuity of $101,055 for each of the next thirty years. Those payments are taxable when you receive them, so your after-taxpayment is $72,759.60 [= $101,055 (1 - 0.28)].Value = $446,000 + $72,759.60 30A.010= $446,000 + $72,759.60 (9.4269)= $1,131,897.47Since option one has a higher PV, you should choose it.4.37 The amount of loan is $9,000. The monthly payment C is given by solving the equation: C 60008.0A = $9,000 C = $9,000 / 47.5042 = $189.46In October 2000, Susan Chao has 35 (= 12 ⨯ 5 - 25) monthly payments left, including the one due in October 2000.Therefore, the balance of the loan on November 1, 2000 = $189.46 + $189.46 34008.0A = $189.46 + $189.46 (29.6651) = $5,809.81Thus, the total amount of payoff = 1.01 ($5,809.81) = $5,867.91 4.38 Let r be the rate of interest you must earn. $10,000(1 + r)12 = $80,000 (1 + r)12 = 8 r = 0.18921 = 18.921%4.39 First compute the present value of all the payments you must make for your children’s education. The value as of one year before matriculation of one child’s education is$21,000 415.0A= $21,000 (2.8550) = $59,955. This is the value of the elder child’s education fourteen years from now. It is the value of the younger child’s education sixteen years from today. The present value of these is PV = $59,955 / 1.1514 + $59,955 / 1.1516 = $14,880.44You want to make fifteen equal payments into an account that yields 15% so that the present value of the equal payments is $14,880.44. Payment = $14,880.44 / 1515.0A = $14,880.44 / 5.8474 = $2,544.804.40 The NPV of the policy isNPV = -$750 306.0A - $800306.0A / 1.063 + $250,000 / [(1.066) (1.0759)] = -$2,004.76 - $1,795.45 + $3,254.33= -$545.88 Therefore, you should not buy the policy.4.41 The NPV of the lease offer isNPV = $120,000 - $15,000 - $15,000 908.0A - $25,000 / 1.0810= $105,000 - $93,703.32 - $11,579.84 = -$283.16 Therefore, you should not accept the offer.4.42 This problem applies the growing annuity formula. The first payment is $50,000(1.04)2(0.02) = $1,081.60. PV = $1,081.60 [1 / (0.08 - 0.04) - {1 / (0.08 - 0.04)}{1.04 / 1.08}40]= $21,064.28 This is the present value of the payments, so the value forty years from today is $21,064.28 (1.0840) = $457,611.46公司理财习题答案第四章4.43 Use the discount factors to discount the individual cash flows. Then compute the NPV ofthe project. Notice that the four $1,000 cash flows form an annuity. You can still use the factor tables to compute their PV. Essentially, they form cash flows that are a six year annuity less a two year annuity. Thus, the appropriate annuity factor to use with them is 2.6198 (= 4.3553 - 1.7355).Year Cash Flow Factor PV 1 $700 0.9091 $636.37 2 900 0.8264 743.76 3 1,000 ⎤ 4 1,000 ⎥ 2.6198 2,619.80 5 1,000 ⎥ 6 1,000 ⎦ 7 1,250 0.5132 641.50 8 1,375 0.4665 641.44 Total $5,282.87NPV = -$5,000 + $5,282.87 = $282.87 Purchase the machine.4.44 Weekly inflation rate = 0.039 / 52 = 0.00075 Weekly interest rate = 0.104 / 52 = 0.002 PV = $5 [1 / (0.002 - 0.00075)] {1 – [(1 + 0.00075) / (1 + 0.002)]52 ⨯ 30} = $3,429.384.45 Engineer:NPV = -$12,000 405.0A + $20,000 / 1.055 + $25,000 / 1.056 - $15,000 / 1.057- $15,000 / 1.058 + $40,000 2505.0A / 1.058= $352,533.35 Accountant:NPV = -$13,000 405.0A + $31,000 3005.0A / 1.054= $345,958.81 Become an engineer.After your brother announces that the appropriate discount rate is 6%, you can recalculate the NPVs. Calculate them the same way as above except using the 6% discount rate. Engineer NPV = $292,419.47 Accountant NPV = $292,947.04Your brother made a poor decision. At a 6% rate, he should study accounting.4.46 Since Goose receives his first payment on July 1 and all payments in one year intervalsfrom July 1, the easiest approach to this problem is to discount the cash flows to July 1 then use the six month discount rate (0.044) to discount them the additional six months. PV = $875,000 / (1.044) + $650,000 / (1.044)(1.09) + $800,000 / (1.044)(1.092) + $1,000,000 / (1.044)(1.093) + $1,000,000/(1.044)(1.094) + $300,000 / (1.044)(1.095)+ $240,000 1709.0A / (1.044)(1.095) + $125,000 1009.0A / (1.044)(1.0922) = $5,051,150Remember that the use of annuity factors to discount the deferred payments yields the value of the annuity stream one period prior to the first payment. Thus, the annuity factor applied to the first set of deferred payments gives the value of those payments on July 1 of 1989. Discounting by 9% for five years brings the value to July 1, 1984. The use of the six month discount rate (4.4%) brings the value of the payments to January 1, 1984. Similarly, the annuity factor applied to the second set of deferred payments yields the value of those payments in 2006. Discounting for 22 years at 9% and for six months at 4.4% provides the value at January 1, 1984.The equivalent five-year, annual salary is the annuity that solves: $5,051,150 = C 509.0A C = $5,051,150/3.8897C = $1,298,596The student must be aware of possible rounding errors in this problem. The differencebetween 4.4% semiannual and 9.0% and for six months at 4.4% provides the value at January 1, 1984. 4.47 PV = $10,000 + ($35,000 + $3,500) [1 / (0.12 - 0.04)] [1 - (1.04 / 1.12) 25 ]= $415,783.604.48 NPV = -$40,000 + $10,000 [1 / (0.10 - 0.07)] [1 - (1.07 / 1.10)5 ] = $3,041.91 Revise the textbook.4.49The amount of the loan is $400,000 (0.8) = $320,000 The monthly payment is C = $320,000 / 3600067.0.0A = $ 2,348.10 Thirty years of payments $ 2,348.10 (360) = $ 845,316.00 Eight years of payments $2,348.10 (96) = $225,417.60 The difference is the balloon payment of $619,898.404.50 The lease payment is an annuity in advanceC + C 2301.0A = $4,000 C (1 + 20.4558) = $4,000 C = $186.424.51 The effective annual interest rate is[ 1 + (0.08 / 4) ] 4 – 1 = 0.0824The present value of the ten-year annuity is PV = 900 100824.0A = $5,974.24 Four remaining discount periodsPV = $5,974.24 / (1.0824) 4 = $4,352.43公司理财习题答案第四章4.52The present value of Ernie’s retirement incomePV = $300,000 20A / (1.07) 30 = $417,511.5407.0The present value of the cabinPV = $350,000 / (1.07) 10 = $177,922.25The present value of his savingsPV = $40,000 10A = $280,943.26.007In present value terms he must save an additional $313,490.53 In future value termsFV = $313,490.53 (1.07) 10 = $616,683.32He must saveC = $616.683.32 / 20A = $58,210.5407.0。

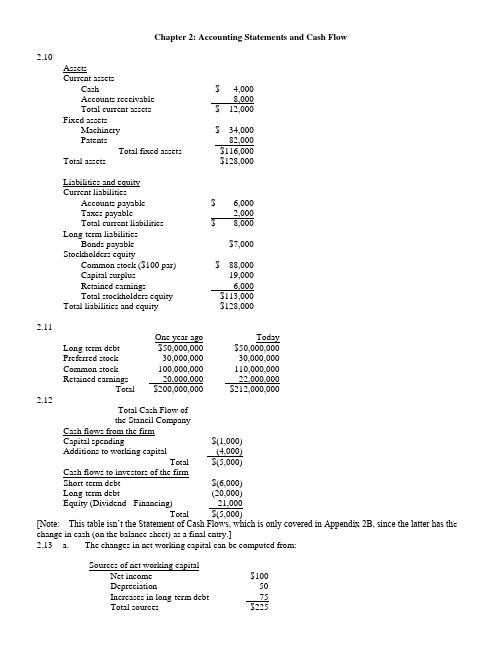

Chapter 2: Accounting Statements and Cash Flow2.10AssetsCurrent assetsCash $ 4,000Accounts receivable 8,000Total current assets $ 12,000Fixed assetsMachinery $ 34,000Patents 82,000Total fixed assets $116,000Total assets $128,000Liabilities and equityCurrent liabilitiesAccounts payable $ 6,000Taxes payable 2,000Total current liabilities $ 8,000Long-term liabilitiesBonds payable $7,000Stockholders equityCommon stock ($100 par) $ 88,000Capital surplus 19,000Retained earnings 6,000Total stockholders equity $113,000Total liabilities and equity $128,0002.11One year ago TodayLong-term debt $50,000,000 $50,000,000Preferred stock 30,000,000 30,000,000Common stock 100,000,000 110,000,000Retained earnings 20,000,000 22,000,000Total $200,000,000 $212,000,0002.12Total Cash Flow ofthe Stancil CompanyCash flows from the firmCapital spending $(1,000)Additions to working capital (4,000)Total $(5,000)Cash flows to investors of the firmShort-term debt $(6,000)Long-term debt (20,000)Equity (Dividend - Financing) 21,000Total $(5,000)[Note: This table isn’t the Statement of Cash Flows, which is only covered in Appendix 2B, since the latter has th e change in cash (on the balance sheet) as a final entry.]2.13 a. The changes in net working capital can be computed from:Sources of net working capitalNet income $100Depreciation 50Increases in long-term debt 75Total sources $225Uses of net working capitalDividends $50Increases in fixed assets* 150Total uses $200Additions to net working capital $25*Includes $50 of depreciation.b.Cash flow from the firmOperating cash flow $150Capital spending (150)Additions to net working capital (25)Total $(25)Cash flow to the investorsDebt $(75)Equity 50Total $(25)Chapter 3: Financial Markets and Net Present Value: First Principles of Finance (Advanced)3.14 $120,000 - ($150,000 - $100,000) (1.1) = $65,0003.15 $40,000 + ($50,000 - $20,000) (1.12) = $73,6003.16 a. ($7 million + $3 million) (1.10) = $11.0 millionb.i. They could spend $10 million by borrowing $5 million today.ii. They will have to spend $5.5 million [= $11 million - ($5 million x 1.1)] at t=1.Chapter 4: Net Present Valuea. $1,000 ⨯ 1.0510 = $1,628.89b. $1,000 ⨯ 1.0710 = $1,967.15c. $1,000 ⨯ 1.0520 = $2,653.30d. Interest compounds on the interest already earned. Therefore, the interest earned inSince this bond has no interim coupon payments, its present value is simply the present value of the $1,000 that will be received in 25 years. Note: As will be discussed in the next chapter, the present value of the payments associated with a bond is the price of that bond.PV = $1,000 /1.125 = $92.30PV = $1,500,000 / 1.0827 = $187,780.23a. At a discount rate of zero, the future value and present value are always the same. Remember, FV =PV (1 + r) t. If r = 0, then the formula reduces to FV = PV. Therefore, the values of the options are $10,000 and $20,000, respectively. You should choose the second option.b. Option one: $10,000 / 1.1 = $9,090.91Option two: $20,000 / 1.15 = $12,418.43Choose the second option.c. Option one: $10,000 / 1.2 = $8,333.33Option two: $20,000 / 1.25 = $8,037.55Choose the first option.d. You are indifferent at the rate that equates the PVs of the two alternatives. You know that rate mustfall between 10% and 20% because the option you would choose differs at these rates. Let r be thediscount rate that makes you indifferent between the options.$10,000 / (1 + r) = $20,000 / (1 + r)5(1 + r)4 = $20,000 / $10,000 = 21 + r = 1.18921r = 0.18921 = 18.921%The $1,000 that you place in the account at the end of the first year will earn interest for six years. The $1,000 that you place in the account at the end of the second year will earn interest for five years, etc. Thus, the account will have a balance of$1,000 (1.12)6 + $1,000 (1.12)5 + $1,000 (1.12)4 + $1,000 (1.12)3= $6,714.61PV = $5,000,000 / 1.1210 = $1,609,866.18a. $1.000 (1.08)3 = $1,259.71b. $1,000 [1 + (0.08 / 2)]2 ⨯ 3 = $1,000 (1.04)6 = $1,265.32c. $1,000 [1 + (0.08 / 12)]12 ⨯ 3 = $1,000 (1.00667)36 = $1,270.24d. $1,000 e0.08 ⨯ 3 = $1,271.25e. The future value increases because of the compounding. The account is earning interest on interest. Essentially, the interest is added to the account balance at the e nd of every compounding period. During the next period, the account earns interest on the new balance. When the compounding period shortens, the balance that earns interest is rising faster.The price of the consol bond is the present value of the coupon payments. Apply the perpetuity formula to find the present value. PV = $120 / 0.15 = $800a. $1,000 / 0.1 = $10,000b. $500 / 0.1 = $5,000 is the value one year from now of the perpetual stream. Thus, the value of theperpetuity is $5,000 / 1.1 = $4,545.45.c. $2,420 / 0.1 = $24,200 is the value two years from now of the perpetual stream. Thus, the value of the perpetuity is $24,200 / 1.12 = $20,000.pply the NPV technique. Since the inflows are an annuity you can use the present value of an annuity factor.ANPV = -$6,200 + $1,200 81.0= -$6,200 + $1,200 (5.3349)= $201.88Yes, you should buy the asset.Use an annuity factor to compute the value two years from today of the twenty payments. Remember, the annuity formula gives you the value of the stream one year before the first payment. Hence, the annuity factor will give you the value at the end of year two of the stream of payments.A= $2,000 (9.8181)Value at the end of year two = $2,000 20.008= $19,636.20The present value is simply that amount discounted back two years.PV = $19,636.20 / 1.082 = $16,834.88The easiest way to do this problem is to use the annuity factor. The annuity factor must be equal to $12,800 / $2,000 = 6.4; remember PV =C A T r. The annuity factors are in the appendix to the text. To use the factor table to solve this problem, scan across the row labeled 10 years until you find 6.4. It is close to the factor for 9%, 6.4177. Thus, the rate you will receive on this note is slightly more than 9%.You can find a more precise answer by interpolating between nine and ten percent.[ 10% ⎤[6.1446 ⎤a ⎡r ⎥bc ⎡6.4 ⎪ d⎣9%⎦⎣6.4177 ⎦By interpolating, you are presuming that the ratio of a to b is equal to the ratio of c to d.(9 - r ) / (9 - 10) = (6.4177 - 6.4 ) / (6.4177 - 6.1446)r = 9.0648%The exact value could be obtained by solving the annuity formula for the interest rate. Sophisticated calculators can compute the rate directly as 9.0626%.[Note: A standard financial calculator’s TVM keys can solve for this rate. With annuity flows, the IRR key on “advanced” financial c alculators is unnecessary.]a. The annuity amount can be computed by first calculating the PV of the $25,000 which youThat amount is $17,824.65 [= $25,000 / 1.075]. Next compute the annuity which has the same present value.A$17,824.65 = C 507.0$17,824.65 = C (4.1002)C = $4,347.26Thus, putting $4,347.26 into the 7% account each year will provide $25,000 five years from today.b. The lump sum payment must be the present value of the $25,000, i.e., $25,000 / 1.075 =$17,824.65The formula for future value of any annuity can be used to solve the problem (see footnote 11 of the text).Option one: This cash flow is an annuity due. To value it, you must use the after-tax amounts. Theafter-tax payment is $160,000 (1 - 0.28) = $115,200. Value all except the first payment using the standard annuity formula, then add back the first payment of $115,200 to obtain the value of this option.AValue = $115,200 + $115,200 30.010= $115,200 + $115,200 (9.4269)= $1,201,178.88Option two: This option is valued similarly. You are able to have $446,000 now; this is already on an after-tax basis. You will receive an annuity of $101,055 for each of the next thirty years. Those payments are taxable when you receive them, so your after-tax payment is $72,759.60 [= $101,055 (1 - 0.28)].AValue = $446,000 + $72,759.60 30.010= $446,000 + $72,759.60 (9.4269)= $1,131,897.47Since option one has a higher PV, you should choose it.et r be the rate of interest you must earn.$10,000(1 + r)12 = $80,000(1 + r)12= 8r = 0.18921 = 18.921%First compute the present value of all the payments you must make for your children’s educati on. The value as of one year before matriculation of one child’s education isA= $21,000 (2.8550) = $59,955.$21,000 415.0This is the value of the elder child’s education fourteen years from now. It is the value of the younger child’s education sixteen years from today. The present value of these isPV = $59,955 / 1.1514 + $59,955 / 1.1516= $14,880.44You want to make fifteen equal payments into an account that yields 15% so that the present value of the equal payments is $14,880.44.A= $14,880.44 / 5.8474 = $2,544.80Payment = $14,880.44 / 15.015This problem applies the growing annuity formula. The first payment is$50,000(1.04)2(0.02) = $1,081.60.PV = $1,081.60 [1 / (0.08 - 0.04) - {1 / (0.08 - 0.04)}{1.04 / 1.08}40]= $21,064.28This is the present value of the payments, so the value forty years from today is$21,064.28 (1.0840) = $457,611.46se the discount factors to discount the individual cash flows. Then compute the NPV of the project. NoticeYou can still use the factor tables to compute their PV. Essentially, they form cash flows that are a six year annuity less a two year annuity. Thus, the appropriate annuity factor to use with them is 2.6198 (= 4.3553 - 1.7355).Year Cash Flow Factor PV0.9091 $636.371$70020.8264 743.769003 1,000 ⎤4 1,000 ⎥ 2.6198 2,619.805 1,000 ⎥6 1,000 ⎦7 1,250 0.5132 641.508 1,375 0.4665 641.44Total $5,282.87NPV = -$5,000 + $5,282.87= $282.87Purchase the machine.Chapter 5: How to Value Bonds and StocksThe amount of the semi-annual interest payment is $40 (=$1,000 ⨯ 0.08 / 2). There are a total of 40 periods;i.e., two half years in each of the twenty years in the term to maturity. The annuity factor tables can be usedto price these bonds. The appropriate discount rate to use is the semi-annual rate. That rate is simply the annual rate divided by two. Thus, for part b the rate to be used is 5% and for part c is it 3%.A+F/(1+r)40PV=C Tra. $40 (19.7928) + $1,000 / 1.0440 = $1,000Notice that whenever the coupon rate and the market rate are the same, the bond is priced at par.b. $40 (17.1591) + $1,000 / 1.0540 = $828.41Notice that whenever the coupon rate is below the market rate, the bond is priced below par.c. $40 (23.1148) + $1,000 / 1.0340 = $1,231.15Notice that whenever the coupon rate is above the market rate, the bond is priced above par.a. The semi-annual interest rate is $60 / $1,000 = 0.06. Thus, the effective annual rate is 1.062 - 1 =0.1236 = 12.36%.A+ $1,000 / 1.0612b. Price = $30 12.006= $748.48A+ $1,000 / 1.0412c. Price = $30 1204.0= $906.15Note: In parts b and c we are implicitly assuming that the yield curve is flat. That is, the yield in year 5applies for year 6 as well.rice = $2 (0.72) / 1.15 + $4 (0.72) / 1.152 + $50 / 1.153= $36.31The number of shares you own = $100,000 / $36.31 = 2,754 sharesPrice = $1.15 (1.18) / 1.12 + $1.15 (1.182) / 1.122 + $1.152 (1.182) / 1.123+ {$1.152 (1.182)(1.06) / (0.12 - 0.06)} / 1.123= $26.95[Insert before last sentence of question: Assume that dividends are a fixed proportion of earnings.] Dividend one year from now = $5 (1 - 0.10) = $4.50Price = $5 + $4.50 / {0.14 - (-0.10)}= $23.75Since the current $5 dividend has not yet been paid, it is still included in the stock price.Chapter 6: Some Alternative Investment Rulesa. Payback period of Project A = 1 + ($7,500 - $4,000) / $3,500 = 2 yearsPayback period of Project B = 2 + ($5,000 - $2,500 -$1,200) / $3,000 = 2.43 yearsProject A should be chosen.b. NPV A = -$7,500 + $4,000 / 1.15 + $3,500 / 1.152 + $1,500 / 1.153 = -$388.96NPV B = -$5,000 + $2,500 / 1.15 + $1,200 / 1.152 + $3,000 / 1.153 = $53.83Project B should be chosen.a. Average Investment:($16,000 + $12,000 + $8,000 + $4,000 + 0) / 5 = $8,000Average accounting return:$4,500 / $8,000 = 0.5625 = 56.25%b. 1. AAR does not consider the timing of the cash flows, hence it does not consider the timevalue of money.2. AAR uses an arbitrary firm standard as the decision rule.3. AAR uses accounting data rather than net cash flows.aAverage Investment = (8000 + 4000 + 1500 + 0)/4 = 3375.00Average Net Income = 2000(1-0.75) = 1500=> AAR = 1500/3375=44.44%a. Solve x by trial and error:-$8,000 + $4,000 / (1 + x) + $3000 / (1 + x)2 + $2,000 / (1 + x)3 = 0x = 6.93%b. No, since the IRR (6.93%) is less than the discount rate of 8%.Alternatively, the NPV @ a discount rate of 0.08 = -$136.62.a. Solve r in the equation:$5,000 - $2,500 / (1 + r) - $2,000 / (1 + r)2 - $1,000 / (1 + r)3- $1,000 / (1 + r)4 = 0By trial and error,IRR = r = 13.99%b. Since this problem is the case of financing, accept the project if the IRR is less than the required rate of return.IRR = 13.99% > 10%Reject the offer.c. IRR = 13.99% < 20%Accept the offer.d. When r = 10%:NPV = $5,000 - $2,500 / 1.1 - $2,000 / 1.12 - $1,000 / 1.13 - $1,000 / 1.14When r = 20%:NPV = $5,000 - $2,500 / 1.2 - $2,000 / 1.22 - $1,000 / 1.23 - $1,000 / 1.24= $466.82Yes, they are consistent with the choices of the IRR rule since the signs of the cash flows change only once.A/ $160,000 = 1.04PI = $40,000 715.0Since the PI exceeds one accept the project.Chapter 7: Net Present Value and Capital BudgetingSince there is uncertainty surrounding the bonus payments, which McRae might receive, you must use the expected value of McRae’s bonuses in the computation of the PV of his contract. McRae’s salary plus the expected value of his bonuses in years one through three is$250,000 + 0.6 ⨯ $75,000 + 0.4 ⨯ $0 = $295,000.Thus the total PV of his three-year contract isPV = $400,000 + $295,000 [(1 - 1 / 1.12363) / 0.1236]+ {$125,000 / 1.12363} [(1 - 1 / 1.123610 / 0.1236]= $1,594,825.68EPS = $800,000 / 200,000 = $4NPVGO = (-$400,000 + $1,000,000) / 200,000 = $3Price = EPS / r + NPVGO= $4 / 0.12 + $3=$36.33Year 0 Year 1 Year 2 Year 3 Year 4 Year 51. Annual Salary$120,000 $120,000 $120,000 $120,000 $120,000 Savings2. Depreciation 100,000 160,000 96,000 57,600 57,6003. Taxable Income 20,000 -40,000 24,000 62,400 62,4004. Taxes 6,800 -13,600 8,160 21,216 21,2165. Operating Cash Flow113,200 133,600 111,840 98,784 98,784 (line 1-4)$100,000 -100,0006. ∆ Net workingcapital7. Investment $500,000 75,792*8. Total Cash Flow -$400,000 $113,200 $133,600 $111,840 $98,784 $74,576*75,792 = $100,000 - 0.34 ($100,000 - $28,800)NPV = -$400,000+ $113,200 / 1.12 + $133,600 / 1.122 + $111,840 / 1.123+ $98,784 / 1.124 + $74,576 / 1.125= -$7,722.52Real interest rate = (1.15 / 1.04) - 1 = 10.58%NPV A = -$40,000+ $20,000 / 1.1058 + $15,000 / 1.10582 + $15,000 / 1.10583= $1,446.76NPV B = -$50,000+ $10,000 / 1.15 + $20,000 / 1.152 + $40,000 / 1.153= $119.17Choose project A.PV = $120,000 / {0.11 - (-0.06)}t = 0 t = 1 t = 2 t = 3 t = 4 t = 5 t = 6 ...$12,000 $6,000 $6,000 $6,000$4,000$12,000 $6,000 $6,000 ...The present value of one cycle is:A+ $4,000 / 1.064PV = $12,000 + $6,000 306.0= $12,000 + $6,000 (2.6730) + $4,000 / 1.064= $31,206.37The cycle is four years long, so use a four year annuity factor to compute the equivalent annual cost (EAC).AEAC = $31,206.37 / 406.0= $31,206.37 / 3.4651= $9,006The present value of such a stream in perpetuity is$9,006 / 0.06 = $150,100o evaluate the word processors, compute their equivalent annual costs (EAC).BangAPV(costs) = (10 ⨯ $8,000) + (10 ⨯ $2,000) 414.0= $80,000 + $20,000 (2.9137)= $138,274EAC = $138,274 / 2.9137= $47,456IOUAPV(costs) = (11 ⨯ $5,000) + (11 ⨯ $2,500) 3.014- (11 ⨯ $500) / 1.143= $55,000 + $27,500 (2.3216) - $5,500 / 1.143= $115,132EAC = $115,132 / 2.3216= $49,592BYO should purchase the Bang word processors.Chapter 8: Strategy and Analysis in Using Net Present ValueThe accounting break-even= (120,000 + 20,000) / (1,500 - 1,100)= 350 units. The accounting break-even= 340,000 / (2.00 - 0.72)= 265,625 abalonesb. [($2.00 ⨯ 300,000) - (340,000 + 0.72 ⨯ 300,000)] (0.65)= $28,600This is the after tax profit.Chapter 9: Capital Market Theory: An Overviewa. Capital gains = $38 - $37 = $1 per shareb. Total dollar returns = Dividends + Capital Gains = $1,000 + ($1*500) = $1,500 On a per share basis, this calculation is $2 + $1 = $3 per sharec. On a per share basis, $3/$37 = 0.0811 = 8.11% On a total dollar basis, $1,500/(500*$37) = 0.0811 = 8.11%d. No, you do not need to sell the shares to include the capital gains in the computation of the returns. The capital gain is included whether or not you realize the gain. Since you could realize the gain if you choose, you should include it.The expected holding period return is:()[]%865.1515865.052$/52$75.54$50.5$==-+There appears to be a lack of clarity about the meaning of holding period returns. The method used in the answer to this question is the one used in Section 9.1. However, the correspondence is not exact, because in this question, unlike Section 9.1, there are cash flows within the holding period. The answer above ignores the dividend paid in the first year. Although the answer above technically conforms to the eqn at the bottom of Fig. 9.2, the presence of intermediate cash flows that aren’t accounted for renders th is measure questionable, at best. There is no similar example in the body of the text, and I have never seen holding period returns calculated in this way before.Although not discussed in this book, there are two generally accepted methods of computing holding period returns in the presence of intermediate cash flows. First, the time weighted return calculates averages (geometric or arithmetic) of returns between cash flows. Unfortunately, that method can’t be used here, because we are not given the va lue of the stock at the end of year one. Second, the dollar weighted measure calculates the internal rate of return over the entire holding period. Theoretically, that method can be applied here, as follows: 0 = -52 + 5.50/(1+r) + 60.25/(1+r)2 => r = 0.1306.This produces a two year holding period return of (1.1306)2 – 1 = 0.2782. Unfortunately, this book does not teach the dollar weighted method.In order to salvage this question in a financially meaningful way, you would need the value of the stock at the end of one year. Then an illustration of the correct use of the time-weighted return would be appropriate. A complicating factor is that, while Section 9.2 illustrates the holding period return using the geometric return for historical data, the arithmetic return is more appropriate for expected future returns.E(R) = T-Bill rate + Average Excess Return = 6.2% + (13.0% -3.8%) = 15.4%. Common Treasury Realized Stocks Bills Risk Premium -7 32.4% 11.2% 21.2%-6 -4.9 14.7 -19.6-5 21.4 10.5 10.9 -4 22.5 8.8 13.7 -3 6.3 9.9 -3.6 -2 32.2 7.7 24.5 Last 18.5 6.2 12.3 b. The average risk premium is 8.49%.49.873.125.246.37.139.106.192.21=++-++- c. Yes, it is possible for the observed risk premium to be negative. This can happen in any single year. The.b.Standard deviation = 03311.0001096.0=.b.Standard deviation = = 0.03137 = 3.137%.b.Chapter 10: Return and Risk: The Capital-Asset-Pricing Model (CAPM)a. = 0.1 (– 4.5%) + 0.2 (4.4%) + 0.5 (12.0%) + 0.2 (20.7%) = 10.57%b.σ2 = 0.1 (–0.045 – 0.1057)2 + 0.2 (0.044 – 0.1057)2 + 0.5 (0.12 – 0.1057)2+ 0.2 (0.207 – 0.1057)2 = 0.0052σ = (0.0052)1/2 = 0.072 = 7.20%Holdings of Atlas stock = 120 ⨯ $50 = $6,000 ⨯ $20 = $3,000Weight of Atlas stock = $6,000 / $9,000 = 2 / 3Weight of Babcock stock = $3,000 / $9,000 = 1 / 3a. = 0.3 (0.12) + 0.7 (0.18) = 0.162 = 16.2%σP 2= 0.32 (0.09)2 + 0.72 (0.25)2 + 2 (0.3) (0.7) (0.09) (0.25) (0.2)= 0.033244σP= (0.033244)1/2 = 0.1823 = 18.23%a.State Return on A Return on B Probability1 15% 35% 0.4 ⨯ 0.5 = 0.22 15% -5% 0.4 ⨯ 0.5 = 0.23 10% 35% 0.6 ⨯ 0.5 = 0.34 10% -5% 0.6 ⨯ 0.5 = 0.3b. = 0.2 [0.5 (0.15) + 0.5 (0.35)] + 0.2[0.5 (0.15) + 0.5 (-0.05)]+ 0.3 [0.5 (0.10) + 0.5 (0.35)] + 0.3 [0.5 (0.10) + 0.5 (-0.05)]= 0.135= 13.5%Note: The solution to this problem requires calculus.Specifically, the solution is found by minimizing a function subject to a constraint. Calculus ability is not necessary to understand the principles behind a minimum variance portfolio.Min { X A2 σA2 + X B2σB2+ 2 X A X B Cov(R A , R B)}subject to X A + X B = 1Let X A = 1 - X B. Then,Min {(1 - X B)2σA2 + X B2σB2+ 2(1 - X B) X B Cov (R A, R B)}Take a derivative with respect to X B.d{∙} / dX B = (2 X B - 2) σA2+ 2 X B σB2 + 2 Cov(R A, R B) - 4 X B Cov(R A, R B)Set the derivative equal to zero, cancel the common 2 and solve for X B.X BσA2- σA2+ X B σB2 + Cov(R A, R B) - 2 X B Cov(R A, R B) = 0X B = {σA2 - Cov(R A, R B)} / {σA2+ σB2 - 2 Cov(R A, R B)}andX A = {σB2 - Cov(R A, R B)} / {σA2+ σB2 - 2 Cov(R A, R B)}Using the data from the problem yields,X A = 0.8125 andX B = 0.1875.a. Using the weights calculated above, the expected return on the minimum variance portfolio isE(R P) = 0.8125 E(R A) + 0.1875 E(R B)= 0.8125 (5%) + 0.1875 (10%)= 5.9375%b. Using the formula derived above, the weights areX A = 2 / 3 andX B = 1 / 3c. The variance of this portfolio is zero.σP 2= X A2 σA2 + X B2σB2+ 2 X A X B Cov(R A , R B)= (4 / 9) (0.01) + (1 / 9) (0.04) + 2 (2 / 3) (1 / 3) (-0.02)= 0This demonstrates that assets can be combined to form a risk-free portfolio.14.2%= 3.7%+β(7.5%) ⇒β = 1.40.25 = R f + 1.4 [R M– R f] (I)0.14 = R f + 0.7 [R M– R f] (II)(I) – (II)=0.11 = 0.7 [R M– R f] (III)[R M– R f ]= 0.1571Put (III) into (I) 0.25 = R f + 1.4[0.1571]R f = 3%[R M– R f ]= 0.1571R M = 0.1571 + 0.03= 18.71%a. = 4.9% + βi (9.4%)βD= Cov(R D, R M) / σM 2 = 0.0635 / 0.04326 = 1.468= 4.9 + 1.468 (9.4) = 18.70%Weights:X A = 5 / 30 = 0.1667X B = 10 / 30 = 0.3333X C = 8 / 30 = 0.2667X D = 1 - X A - X B - X C = 0.2333Beta of portfolio= 0.1667 (0.75) + 0.3333 (1.10) + 0.2667 (1.36) + 0.2333 (1.88)= 1.293= 4 + 1.293 (15 - 4) = 18.22%a. (i) βA= ρA,MσA / σMρA,M= βA σM / σA= (0.9) (0.10) / 0.12= 0.75(ii) σB= βB σM / ρB,M= (1.10) (0.10) / 0.40= 0.275(iii) βC= ρC,MσC / σM= (0.75) (0.24) / 0.10= 1.80(iv) ρM,M= 1(v) βM= 1(vi) σf= 0(vii) ρf,M= 0(viii) βf= 0b. SML:E(R i) = R f + βi {E(R M) - R f}= 0.05 + (0.10) βiSecurity βi E(R i)A 0.13 0.90 0.14B 0.16 1.10 0.16C 0.25 1.80 0.23Security A performed worse than the market, while security C performed better than the market.Security B is fairly priced.c. According to the SML, security A is overpriced while security C is under-priced. Thus, you could invest in security C while sell security A (if you currently hold it).a. The typical risk-averse investor seeks high returns and low risks. To assess thetwo stocks, find theReturns:State of economy ProbabilityReturn on A*Recession 0.1 -0.20 Normal 0.8 0.10 Expansion0.10.20* Since security A pays no dividend, the return on A is simply (P 1 / P 0) - 1. = 0.1 (-0.20) + 0.8 (0.10) + 0.1 (0.20) = 0.08 = 0.09 This was given in the problem.Risk:R A - (R A -)2 P ⨯ (R A -)2 -0.28 0.0784 0.00784 0.02 0.0004 0.00032 0.12 0.0144 0.00144 Variance 0.00960Standard deviation (R A ) = 0.0980βA = {Corr(R A , R M ) σ(R A )} / σ(R M ) = 0.8 (0.0980) / 0.10= 0.784βB = {Corr(R B , R M ) σ(R B )} / σ(R M ) = 0.2 (0.12) / 0.10= 0.24The return on stock B is higher than the return on stock A. The risk of stock B, as measured by itsbeta, is lower than the risk of A. Thus, a typical risk-averse investor will prefer stock B.b. = (0.7) + (0.3) = (0.7) (0.8) + (0.3) (0.09) = 0.083σP 2= 0.72 σA 2 + 0.32 σB 2 + 2 (0.7) (0.3) Corr (R A , R B ) σA σB = (0.49) (0.0096) + (0.09) (0.0144) + (0.42) (0.6) (0.0980) (0.12) = 0.0089635 σP = = 0.0947 c. The beta of a portfolio is the weighted average of the betas of the components of the portfolio. βP = (0.7) βA + (0.3) βB = (0.7) (0.784) + (0.3) (0.240) = 0.621Chapter 11:An Alternative View of Risk and Return: The Arbitrage Pricing Theorya. Stock A:()()R R R R R A A A m m Am A=+-+=+-+βεε105%12142%...Stock B:()()R R R R R B B m m Bm B=+-+=+-+βεε130%098142%...Stock C:()R R R R R C C C m m Cm C=+-+=+-+βεε157%137142%)..(.b.()[]()[]()[]()()()()()()[]()()CB A m cB A m c m B m A m CB A P 25.045.030.0%2.14R 1435.1%925.1225.045.030.0%2.14R 37.125.098.045.02.130.0%7.1525.0%1345.0%5.1030.0%2.14R 37.1%7.1525.0%2.14R 98.0%0.1345.0%2.14R 2.1%5.1030.0R 25.0R 45.0R 30.0R ε+ε+ε+-+=ε+ε+ε+-+++++=ε+-++ε+-++ε+-+=++= c.i.()R R R A B C =+-==+-==+-=105%1215%142%)1113%09815%142%)137%157%13715%142%168%..(..46%.(......ii.R P =+-=12925%1143515%142%)138398%..(..To determine which investment investor would prefer, you must compute the variance of portfolios created bymany stocks from either market. Note, because you know that diversification is good, it is reasonable to assume that once an investor chose the market in which he or she will invest, he or she will buy many stocks in that market.Known:E EF ====001002 and and for all i.i σσεε..Assume: The weight of each stock is 1/N; that is, X N i =1/for all i.If a portfolio is composed of N stocks each forming 1/N proportion of the portfolio, the return on the portfolio is 1/N times the sum of the returns on the N stocks. Recall that the return on each stock is 0.1+βF+ε.()()()()()()[]()()()()()()()[]()[]()[]()()[]()()()()()j i 2j i 22j i i 2222222222P P P P iP ,0.04Corr 0.01,Cov s =isvariance the ,N as limit In the ,Cov 1/N 1s 1/N s )(1/N 1/N F 2F E 1/N F E 0.10.1/N F 0.1E R E R E R Var 0.101/N 00.1E 1/N F E 0.11/N F 0.1E R E 1/N F 0.1F 0.1(1/N)R 1/N R εε+β=εε+β∞⇒εε-+ε+β=ε∑+εβ+β=ε+β=-ε+β+=-==+β+=ε+β+=ε∑+β+=ε+β+=ε+β+==∑∑∑∑∑∑∑∑()()()()()()Thus,F R f E R E R Var R Corr Var R Corr ii ip P p i j PijR 1i =++=++===+=+010*********002250040002500412212111222.........,,εεεεεεa.()()()()Corr Corr Var R Var R i j i j p pεεεε112212000225000225,,..====Since Var ()()R p 1 Var R 2p 〉, a risk averse investor will prefer to invest in the second market.b. Corr ()()εεεε112090i j j ,.,== and Corr 2i()()Var R Var R pp120058500025==..。