财务管理英文版

- 格式:ppt

- 大小:602.51 KB

- 文档页数:165

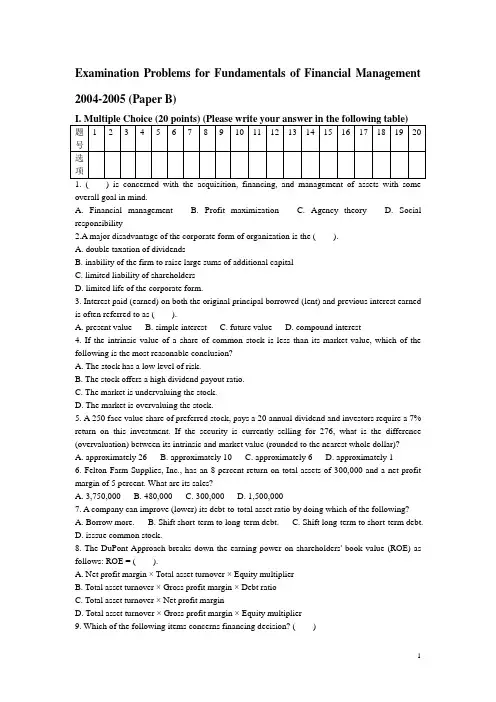

1 Examination Problems for Fundamentals of Financial Management

2004-2005 (Paper B)

I. Multiple Choice (20 points) (Please write your answer in the following table)

题号 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

选项

1. ( ) is concerned with the acquisition, financing, and management of assets with some

overall goal in mind.

A. Financial management B. Profit maximization C. Agency theory D. Social

responsibility

2.A major disadvantage of the corporate form of organization is the ( ).

A. double taxation of dividends

B. inability of the firm to raise large sums of additional capital

C. limited liability of shareholders

D. limited life of the corporate form.

3. Interest paid (earned) on both the original principal borrowed (lent) and previous interest earned

is often referred to as ( ).

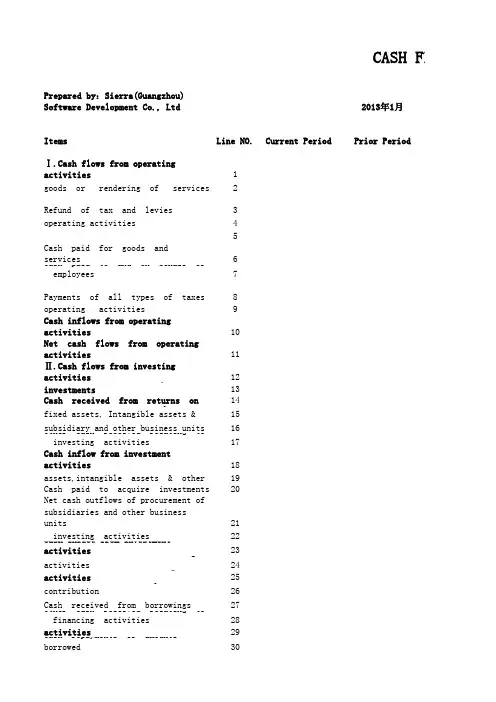

Prepared by:Sierra(Guangzhou) Software Development Co., Ltd2013年1月

ItemsLine NO.Current PeriodPrior Period

Ⅰ.Cash flows from operating activitie1

Cash received from sale of goods or re2

Refund of tax and levies3

Other cash received relating to operat4

Cash inflows from operating activities5

Cash paid for goods and services6

Cash paid to and on behalf of employees7

Payments of all types of taxes8

Other cash paid relating to operating 9

Cash inflows from operating activities10

Net cash flows from operating activiti11

Ⅱ.Cash flows from investing activitie12

Cash received from disposal of investm13Cash received from returns on investme14

Net cash received from disposal of fixe15

Net cash received disposal subsidiary a16

Other cash received relating to investi17

Cash inflow from investment activities18

Cash paid to acquire fixed assets,intan19

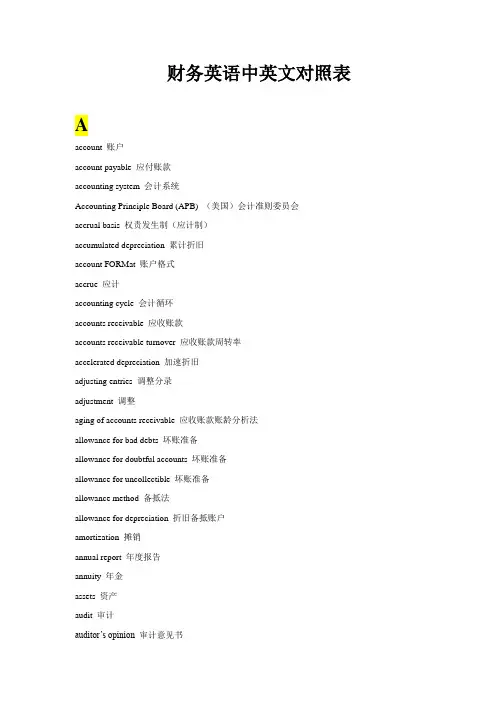

财务英语中英文对照表

A

account 账户

account payable 应付账款

accounting system 会计系统

Accounting Principle Board (APB) (美国)会计准则委员会

accrual basis 权责发生制(应计制)

accumulated depreciation 累计折旧

account FORMat 账户格式

accrue 应计

accounting cycle 会计循环

accounts receivable 应收账款

accounts receivable turnover 应收账款周转率

accelerated depreciation 加速折旧

adjusting entries 调整分录

adjustment 调整

aging of accounts receivable 应收账款账龄分析法

allowance for bad debts 坏账准备

allowance for doubtful accounts 坏账准备

allowance for uncollectible 坏账准备

allowance method 备抵法

allowance for depreciation 折旧备抵账户

amortization 摊销

annual report 年度报告

annuity 年金

assets 资产

audit 审计

auditor’s opinion 审计意见书 auditor 审计师

audit mittee 审计委员会

average collection period 平均收账期

AICPA 美国注册会计师协会

APB Opinions 会计准则委员会意见书

B

balance 余额

bad debt recoveries 坏账收回

bad debts 坏账

Yang。 1

一、判断题(10*2’)

( T )1、A company’s return on equity will always equal or exceed its return on assets.

一个公司的权益收益率总是大于或等于其资产收益率。

( T)2、A company’s assets-to-equity ratio always equals one plus its liabilities-to-equity ratio.

一个公司的资产权益比总是等于1加负债权益比。

( F )3、A company’s collection period should always be less than its payables period.

一个公司的应收账款回收期总是小于其应付账款付款期。

( T )4、A company’s current radio must always be larger than its acid-test-radio.

一个公司的流动比率一定大于速动比率。

( F )5、Economic earnings are more volatile than accounting earnings.

经济利润比会计利润更加变动不定。

( F )6、Ignoring taxes and transactions costs , unrealized paper gains are less valuable than realized cash earnings.

若不考虑税收和交易成本,未实现的纸上盈利不如已实现的现金盈利有价值。

( F)7、A company’s sustainable growth rate is the highest growth rate in sales it can attain without issuing new stock.