金融市场与金融机构Chapter15

- 格式:ppt

- 大小:2.11 MB

- 文档页数:52

金融市场与金融机构金融市场与金融机构理论与实践金融市场与金融机构:理论与实践1. 介绍金融市场与金融机构是现代金融体系的核心组成部分。

金融市场提供资金交换和证券交易的场所,而金融机构则充当资金中介和风险管理的角色。

本文将深入探讨金融市场与金融机构的理论与实践,以加深对这一主题的理解。

2. 金融市场2.1 定义与分类金融市场是指资金供求双方进行交易的场所,主要分为货币市场、资本市场和衍生品市场。

货币市场是短期债权工具的交易场所,资本市场则是长期股权和债权的交易场所,衍生品市场交易的是金融衍生品。

2.2 功能与作用金融市场的功能主要包括资金融通、风险管理、价格发现和流动性提供。

通过金融市场,资金能够从储户流向借款人,从投资者流向资金需求者,实现资源配置的优化。

3. 金融机构3.1 定义与分类金融机构是指在金融市场上从事资金中介和风险管理的机构,主要分为银行、保险公司、证券公司和投资基金公司等。

银行是最常见也是最重要的金融机构,主要承担存款、贷款和支付结算等职能。

3.2 功能与作用金融机构的功能包括资金中介、信息中介和风险管理。

首先,金融机构能够将存款人的资金转化为贷款,实现资金供给的中介;其次,金融机构能够提供关于投资项目的信息,协助投资者做出决策;最后,金融机构通过风险管理的手段,提供安全和稳定的金融服务。

4. 理论与实践4.1 金融市场的理论基础金融市场理论主要包括有效市场假说、资本资产定价模型和行为金融学等。

有效市场假说认为市场已经充分反映了所有可得信息,资本资产定价模型则揭示了资产价格与风险之间的关系,行为金融学则研究了人们在金融决策中的行为模式。

4.2 金融机构的理论基础金融机构理论主要包括债务契约理论、银行关系理论和金融中介理论等。

债务契约理论分析了借贷关系的特征和影响,银行关系理论则研究了银行与客户之间的长期关系,金融中介理论则探讨了金融机构在资源配置中的作用。

4.3 理论与实践的关系金融市场与金融机构的理论与实践密不可分。

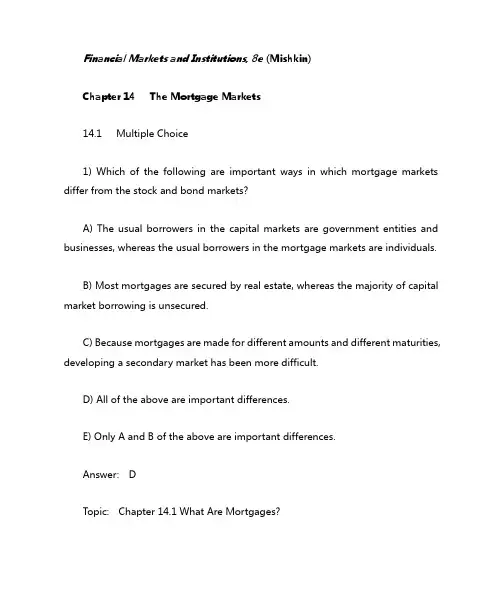

Financial Markets and Institutions, 8e (Mishkin)Chapter 14 The Mortgage Markets14.1 Multiple Choice1) Which of the following are important ways in which mortgage markets differ from the stock and bond markets?A) The usual borrowers in the capital markets are government entities and businesses, whereas the usual borrowers in the mortgage markets are individuals.B) Most mortgages are secured by real estate, whereas the majority of capital market borrowing is unsecured.C) Because mortgages are made for different amounts and different maturities, developing a secondary market has been more difficult.D) All of the above are important differences.E) Only A and B of the above are important differences.Answer: DTopic: Chapter 14.1 What Are Mortgages?Question Status: Previous Edition2) Which of the following are important ways in which mortgage markets differ from stock and bond markets?A) The usual borrowers in capital markets are government entities, whereas the usual borrowers in mortgage markets are small businesses.B) The usual borrowers in capital markets are government entities and large businesses, whereas the usual borrowers in mortgage markets are small businesses.C) The usual borrowers in capital markets are government entities and large businesses, whereas the usual borrowers in mortgage markets are small businesses and individuals.D) The usual borrowers in capital markets are businesses and government entities, whereas the usual borrowers in mortgage markets are individuals.Answer: DTopic: Chapter 14.1 What Are Mortgages?Question Status: Previous Edition3) Which of the following are true of mortgages?A) A mortgage is a long-term loan secured by real estate.B) A borrower pays off a mortgage in a combination of principal and interest payments that result in full payment of the debt by maturity.C) Over 80 percent of mortgage loans finance residential home purchases.D) All of the above are true of mortgages.E) Only A and B of the above are true of mortgages.Answer: DTopic: Chapter 14.1 What Are Mortgages?Question Status: Previous Edition4) Which of the following are true of mortgages?A) A mortgage is a long-term loan secured by real estate.B) Borrowers pay off mortgages over time in some combination of principal and interest payments that result in full payment of the debt by maturity.C) Less than 65 percent of mortgage loans finance residential home purchases.D) All of the above are true of mortgages.E) Only A and B of the above are true of mortgages.Answer: ETopic: Chapter 14.1 What Are Mortgages?Question Status: Previous Edition5) Which of the following are true of mortgage interest rates?A) Interest rates on mortgage loans are determined by three factors: current long-term market rates, the term of the mortgage, and the number of discount points paid.B) Mortgage interest rates tend to track along with Treasury bond rates.C) The interest rate on 15-year mortgages is lower than the rate on 30-year mortgages, all else the same.D) All of the above are true.E) Only A and B of the above are true.Answer: DTopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition6) Which of the following are true of mortgages?A) More than 80 percent of mortgage loans finance residential home purchases.B) The National Banking Act of 1863 rewarded banks that increased mortgage lending.C) Most mortgages during the 1920s and 1930s were balloon loans.D) All of the above are true.E) Only A and C of the above are true.Answer: ETopic: Chapter 14.1 What Are Mortgages?Question Status: Previous Edition7) Which of the following is true of mortgage interest rates?A) Longer-term mortgages have lower interest rates than shorter-term mortgages.B) Mortgage rates are lower than Treasury bond rates because of the tax deductibility of mortgage interest rates.C) In exchange for points, lenders reduce interest rates on mortgage loans.D) All of the above are true.E) Only A and B of the above are true.Answer: CTopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition8) Typically, discount points should not be paid if the borrower will pay off the loan in ________ years or less.A) 5B) 10C) 15D) 20Answer: ATopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition9) Which of the following is true of mortgage interest rates?A) Longer-term mortgages have higher interest rates than shorter-term mortgages.B) In exchange for points, lenders reduce interest rates on mortgage loans.C) Mortgage rates are lower than Treasury bond rates because of the tax deductibility of mortgage interest payments.D) All of the above are true.E) Only A and B of the above are true.Answer: ETopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition10) Which of the following reduces moral hazard for the mortgage borrower?A) CollateralB) Down paymentsC) Private mortgage insuranceD) Borrower qualificationsAnswer: BTopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition11) Which of the following protects the mortgage lender's right to sell property if the underlying loan defaults?A) A lienB) A down paymentC) Private mortgage insuranceD) Borrower qualificationE) AmortizationAnswer: ATopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition12) Which of the following is true of mortgage interest rates?A) Mortgage rates are closely tied to Treasury bond rates, but mortgage rates tend to stay below Treasury rates because mortgages are secured with collateral.B) Longer-term mortgages have higher interest rates than shorter-term mortgages.C) Interest rates are higher on mortgage loans on which lenders charge points.D) All of the above are true.E) Only A and B of the above are true.Answer: BTopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition13) During the early years of an amortizing mortgage loan, the lender appliesA) most of the monthly payment to the outstanding principal balance.B) all of the monthly payment to the outstanding principal balance.C) most of the monthly payment to interest on the loan.D) all of the monthly payment to interest on the loan.E) the monthly payment equally to interest on the loan and the outstanding principal balance.Answer: CTopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition14) During the last years of an amortizing mortgage loan, the lender appliesA) most of the monthly payment to the outstanding principal balance.B) all of the monthly payment to the outstanding principal balance.C) most of the monthly payment to interest on the loan.D) all of the monthly payment to interest on the loan.E) the monthly payment equally to interest on the loan and the outstanding principal balance.Answer: ATopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition15) During the last years of a balloon mortgage loan, the lender appliesA) most of the monthly payment to the outstanding principal balance.B) all of the monthly payment to the outstanding principal balance.C) most of the monthly payment to interest on the loan.D) all of the monthly payment to interest on the loan.E) the monthly payment equally to interest on the loan and the outstanding principal balance.Answer: DTopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition16) During the early years of a balloon mortgage loan, the lender appliesA) most of the monthly payment to the outstanding principal balance.B) all of the monthly payment to the outstanding principal balance.C) most of the monthly payment to interest on the loan.D) all of the monthly payment to interest on the loan.E) the monthly payment equally to interest on the loan and the outstanding principal balance.Answer: DTopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition17) A borrower who qualifies for an FHA or VA loan enjoys the advantage thatA) the mortgage payment is much lower.B) only a very low or zero down payment is required.C) the cost of private mortgage insurance is lower.D) the government holds the lien on the property.Answer: BTopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition18) (I) Conventional mortgages are originated by private lending institutions, and FHA or VA loans are originated by the government. (II) Conventional mortgages are insured by private companies, and FHA or VA loans are insured by the government.A) (I) is true, (II) false.B) (I) is false, (II) true.C) Both are true.D) Both are false.Answer: BTopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition19) Borrowers tend to prefer ________ to ________, whereas lenders prefer ________.A) fixed-rate loans; ARMs; fixed-rate loansB) ARMs; fixed-rate loans; fixed-rate loansC) fixed-rate loans; ARMs; ARMsD) ARMs; fixed-rate loans; ARMsAnswer: CTopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition20) (I) ARMs offer lower initial rates and the rate may fall during the life of the loan. (II) Conventional mortgages do not allow a borrower to take advantage of falling interest rates.A) (I) is true, (II) is false.B) (I) is false, (II) is true.C) Both are true.D) Both are false.Answer: ATopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition21) Growing-equity mortgages (GEMs)A) help the borrower pay off the loan in a shorter time.B) have such low payments in the first few years that the principal balance increases.C) offer borrowers payments that are initially lower than the payments on aconventional mortgage.D) do all of the above.E) do only A and B of the above.Answer: ATopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition22) A borrower with a 30-year loan can create a GEM byA) simply increasing the monthly payments beyond what is required and designating that the excess be applied entirely to the principal.B) converting his ARM into a conventional mortgage.C) converting his conventional mortgage into an ARM.D) converting his conventional mortgage into a GPM.Answer: ATopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition23) Which of the following are useful for home buyers who expect their income to rise in the future?A) GPMsB) RAMsC) GEMsD) Only A and B are useful.E) Only A and C are useful.Answer: ETopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition24) Which of the following are useful for home buyers who expect their income to fall in the future?A) GPMsB) RAMsC) GEMsD) Only A and B are useful.E) Only A and C are useful.Answer: BTopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition25) Retired people can live on the equity they have in their homes by using aA) GEM.B) GPM.C) SAM.D) RAM.Answer: DTopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition26) Second mortgages serve the following purposes:A) they give borrowers a way to use the equity they have in their homes as security for another loan.B) they allow borrowers to get a tax deduction on loans secured by their primary residence or vacation home.C) they allow borrowers to convert their conventional mortgages into GEMs.D) all of the above.E) only A and B of the above.Answer: ETopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition27) Which of the following is a disadvantage of a second mortgage compared to credit card debt?A) The loans are secured by the borrower's home.B) The borrower gives up the tax deduction on the primary mortgage.C) The borrower must pay points to get a second mortgage loan.D) The borrower will find it more difficult to qualify for a second mortgage loan.Answer: ATopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition28) The share of the mortgage market held by savings and loans isA) over 50 percent.B) approximately 40 percent.C) approximately 20 percent.D) less than 5 percent.Answer: DTopic: Chapter 14.4 Mortgage-Lending InstitutionsQuestion Status: Updated from Previous Edition29) The share of the mortgage market held by commercial banks is approximatelyA) 50 percent.B) 30 percent.C) 15 percent.D) 5 percent.Answer: BTopic: Chapter 14.4 Mortgage-Lending Institutions Question Status: Updated from Previous Edition30) A loan-servicing agent willA) package the loan for an investor.B) hold the loan in their investment portfolio.C) collect payments from the borrower.D) do both A and C of the above.E) do both B and C of the above.Answer: CTopic: Chapter 14.5 Loan ServicingQuestion Status: Previous Edition31) Distinct elements of a mortgage loan includeA) origination.B) investment.C) servicing.D) all of the above.E) only B and C of the above.Answer: DTopic: Chapter 14.6 Secondary Mortgage MarketQuestion Status: Previous Edition32) The Federal National Mortgage Association (Fannie Mae)A) was set up to buy mortgages from thrifts so that these institutions could make more loans.B) funds purchases of mortgages by selling bonds to the public.C) provides insurance for certain mortgage contracts.D) does all of the above.E) does only A and B of the above.Answer: ETopic: Chapter 14.6 Secondary Mortgage MarketQuestion Status: Previous Edition33) The Federal Housing Administration (FHA)A) was set up to buy mortgages from thrifts so that these institutions could make more loans.B) funds purchases of mortgages by selling bonds to the public.C) provides insurance for certain mortgage contracts.D) does all of the above.E) does only A and B of the above.Answer: CTopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition34) ________ issues participation certificates, and ________ provides federal insurance for participation certificates.A) Freddie Mac; Freddie MacB) Freddie Mac; Ginnie MaeC) Ginnie Mae; Freddie MacD) Ginnie Mae; Ginnie MaeE) Freddie Mac; no oneAnswer: ETopic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: Previous Edition35) REMICs are most likeA) Freddie Mac pass-through securities.B) Ginnie Mae pass-through securities.C) participation certificates.D) collateralized mortgage obligations.Answer: DTopic: Chapter 14.8 What Is a Mortgage-Backed Security? Question Status: Previous Edition36) Ginnie MaeA) insures qualifying mortgages.B) insures pass-through certificates.C) insures collateralized mortgage obligations.D) does only A and B. of the above.E) does only B and C of the above.Answer: BTopic: Chapter 14.8 What Is a Mortgage-Backed Security? Question Status: Previous Edition37) Mortgage-backed securitiesA) have been growing in popularity in recent years as institutional investors look for attractive investment opportunities.B) are securities collateralized by a pool of mortgages.C) are securities collateralized by both insured and uninsured mortgages.D) are all of the above.E) are only A and B of the above.Answer: DTopic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: Previous Edition38) The most common type of mortgage-backed security isA) the mortgage pass-through, a security that has the borrower's mortgage payments pass through the trustee before being disbursed to the investors.B) collateralized mortgage obligations, a security which reduces prepayment risk.C) the participation certificate, a security which passes the borrower's mortgage payments equally among all the owners of the certificates.D) the securitized mortgage, a security which increases the liquidity of otherwise illiquid mortgages.Answer: ATopic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: Previous Edition39) The interest rate borrowers pay on their mortgages is determined byA) current long-term market rates.B) the term.C) the number of discount points.D) all of the above.Answer: DTopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition40) A loan for borrowers who do not qualify for loans at the usual market rate of interest because of a poor credit rating or because the loan is larger than justified by their income isA) a subprime mortgage.B) a securitized mortgage.C) an insured mortgage.D) a graduated-payment mortgage.Answer: ATopic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: Previous Edition41) The percentage of the total loan paid back immediately when a mortgage loan is obtained, which lowers the annual interest rate on the debt, is calledA) discount points.B) loan terms.C) collateral.D) down payment.Answer: ATopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition42) Which of the following terms are found in mortgage loan contracts to protect the lender from financial loss?A) CollateralB) Down paymentC) Private mortgage insuranceD) All of the aboveAnswer: DTopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition43) What factors are used in determining a person's FICO score?A) Past payment historyB) Outstanding debtC) Length of credit historyD) All of the aboveAnswer: DTopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition44) Between 2000 and 2005, home prices increased an average of ________ per year.A) 2%B) 4%C) 8%D) 12%Answer: CTopic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: New Question45) From 2000 to 2005, housing prices increased, on average, by over 40%. This run up in prices was caused byA) speculators.B) an increase in subprime loans, which increased demand for new and existing houses.C) both A and B.D) None of the above are correct.Answer: CTopic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: Updated from Previous Edition14.2 True/False1) In 2012, mortgage loans to farms represented the largest proportion of mortgage lending in the U.S.Answer: FALSETopic: Chapter 14.1 What Are Mortgages?Question Status: New Question2) Down payments are designed to reduce the likelihood of default on mortgage loans.Answer: TRUETopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition3) Discount points (or simply points) are interest payments made at the beginning of a loan.Answer: TRUETopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition4) A point on a mortgage loan refers to one monthly payment of principal and interest.Answer: FALSETopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition5) Closing for a mortgage loan refers to the moment the loan is paid off.Answer: FALSETopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition6) Private mortgage insurance is a policy that guarantees to make up any discrepancy between the value of the property and the loan amount, should a default occur.Answer: TRUETopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition7) During the early years of a mortgage loan, the lender applies most of the payment to the principal on the loan.Answer: FALSETopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition8) One important advantage to a borrower who qualifies for an FHA or VA loan is the very low interest rate on the mortgage.Answer: FALSETopic: Chapter 14.3 Types of Mortgages9) Adjustable-rate mortgages generally have lower initial interest rates than fixed-rate mortgages.Answer: TRUETopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition10) Mortgage interest rates loosely track interest rates on three-month Treasury bills.Answer: FALSETopic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition11) An advantage of a graduated-payment mortgage is that borrowers will qualify for a larger loan than if they requested a conventional mortgage.Answer: TRUETopic: Chapter 14.3 Types of Mortgages12) Nearly half the funds for mortgage lending comes from mortgage pools and trusts.Answer: FALSETopic: Chapter 14.4 Mortgage-Lending InstitutionsQuestion Status: Updated from Previous Edition13) Many institutions that make mortgage loans do not want to hold large portfolios of long-term securities, because it would subject them to unacceptably high interest-rate risk.Answer: TRUETopic: Chapter 14.4 Mortgage-Lending InstitutionsQuestion Status: Previous Edition14) A problem that initially hindered the marketability of mortgages in a secondary market was that they were not standardized.Answer: TRUETopic: Chapter 14.6 Secondary Mortgage MarketQuestion Status: Previous Edition15) Mortgage-backed securities have declined in popularity in recent years as institutional investors have sought higher returns in other markets.Answer: FALSETopic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: Previous Edition16) Mortgage-backed securities are marketable securities collateralized by a pool of mortgages.Answer: TRUETopic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: Previous Edition17) Fannie Mae and Freddie Mac together either own or insure the risk on nearly one-fourth of America's residential mortgages.Answer: FALSETopic: Chapter 14.4 Mortgage-Lending InstitutionsQuestion Status: Previous Edition18) A FICO score below 660 is considered good while a score above 720 is likely to cause problems in obtaining a loan.Answer: FALSETopic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition19) Subprime loans are those made to borrowers who do not qualify for loans at the usual market rate of interest because of a poor credit rating or because the loan is larger than justified by their income.Answer: TRUETopic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: Previous Edition14.3 Essay1) How has the modern mortgage market changed over recent years?Topic: Chapter 14.1 What Are Mortgages?Question Status: Previous Edition2) Explain the features of mortgage loans that are designed to reduce the likelihood of default.Topic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition3) What are points? What is their purpose?Topic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition4) How does an amortizing mortgage loan differ from a balloon mortgage loan?Topic: Chapter 14.2 Characteristics of the Residential MortgageQuestion Status: Previous Edition5) Evaluate the advantages and disadvantages, from both the lender's and borrower's perspectives, of fixed-rate and adjustable-rate mortgages.Topic: Chapter 14.3 Types of MortgagesQuestion Status: Previous Edition6) Why has the online lending market developed in recent years and what are the advantages and disadvantages of this development?Topic: Chapter 14.4 Mortgage-Lending InstitutionsQuestion Status: Previous Edition7) Why may Fannie Mae and Freddie Mac pose a threat to the health of the financial system?Topic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: Previous Edition8) What are mortgage-backed securities, why were they developed, whattypes of mortgage-backed securities are there, and how do they work?Topic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: Previous Edition9) What are the benefits and side effects of securitized mortgages?Topic: Chapter 14.7 Securitization of MortgagesQuestion Status: Previous Edition10) Discuss the pros and cons of a subprime market for residential mortgages in the U.S.Topic: Chapter 14.8 What Is a Mortgage-Backed Security?Question Status: New Question。

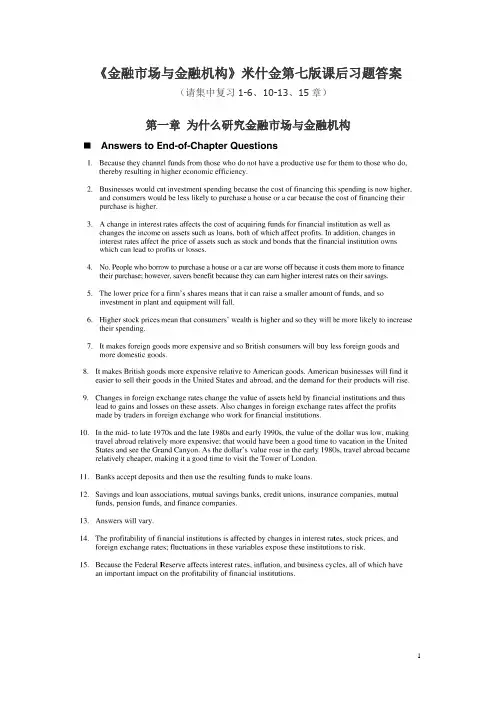

《金融市场与金融机构》米什金第七版课后习题答案

(请集中复习1-6、10-13、15章)

第一章为什么研究金融市场与金融机构

第二章金融体系概览

第三章利率的含义及其在定价中的作用

第四章为什么利率会变化

第五章利率的风险结构和期限结构如何影响利率

第六章金融市场是否有效

第十章货币政策传导:工具、目标战略和战术

第七版中的12题在第五六版中没有,此处的12-19题即为第七版的13-20题

第十一章货币市场

第十二章债券市场

第十三章股票市场

第十四章抵押贷款市场

第十五章外汇市场。

Foundations of Financial Markets and Institutions, 4e (Fabozzi/Modigliani/Jones)Chapter 10 The Level and Structure of Interest RatesMultiple Choice Questions1 The Theory of Interest Rates1) An interest rate is the price paid by a ________ to a ________ for the use of resources during some interval.A) borrower; debtorB) lender; creditorC) borrower; lenderD) lender; borrowerAnswer: CComment: An interest rate is the price paid by a borrower (or debtor) to a lender (or creditor) for the use of resources during some interval.Diff: 2Topic: 10.1 The Theory of Interest RatesObjective: 10.1 Fisher's classical approach to explaining the level of the interest rate2) By the ________, we mean the rate on a loan whose borrower will not default on any obligation.A) risk-free rateB) short termC) real rateD) long termAnswer: AComment: The interest rate that provides the anchor for other rates is the short-term rate:risk-free plus real rate. By short term, we mean the rate on a loan that has one year to maturity. (All other interest rates differ from this rate according to particular aspects of the loan, such as its maturity or risk of default, or because of the presence of inflation.) By the risk-free rate, we mean the rate on a loan whose borrower will not default on any obligation. By the real rate, we mean the rate that would prevail in the economy if the average prices for goods and services were expected to remain constant during the loan’s life.Diff: 1Topic: 10.1 The Theory of Interest RatesObjective: 10.4 the structure of Fisher's Law, which states that the nominal and observable interest rate is composed of two unobservable variables; the real rate of interest and the premium for expected inflation3) By the ________, we mean the rate that would prevail in the economy if the average prices for goods and services were expected to remain constant during the loan's life.A) risk-free rateB) short termC) real rateD) long termAnswer: CComment: The interest rate that provides the anchor for other rates is the short-term rate:risk-free plus real rate. By short term, we mean the rate on a loan that has one year to maturity. (All other interest rates differ from this rate according to particular aspects of the loan, such as its maturity or risk of default, or because of the presence of inflation.) By the risk-free rate, we mean the rate on a loan whose borrower will not default on any obligation. By the real rate, we mean the rate that would prevail in the economy if the average prices for goods and services were expected to remain constant during the loan’s life.Diff: 1Topic: 10.1 The Theory of Interest RatesObjective: 10.4 the structure of Fisher's Law, which states that the nominal and observable interest rate is composed of two unobservable variables; the real rate of interest and the premium for expected inflation4) By the ________, we mean the rate on a loan that has one year to maturity.A) risk-free rateB) short termC) real rateD) long termAnswer: BComment: The interest rate that provides the anchor for other rates is the short-term rate:risk-free plus real rate. By short term, we mean the rate on a loan that has one year to maturity. (All other interest rates differ from this rate according to particular aspects of the loan, such as its maturity or risk of default, or because of the presence of inflation.) By the risk-free rate, we mean the rate on a loan whose borrower will not default on any obligation. By the real rate, we mean the rate that would prevail in the economy if the average prices for goods and services were expected to remain constant during the loan’s life.Diff: 2Topic: 10.1 The Theory of Interest RatesObjective: 10.1 Fisher's classical approach to explaining the level of the interest rate5) Which of the below statements about consumptions and savings is FALSE?A) A chief influence on the saving decision is the individual's marginal rate of time preference, which is the willingness to trade some consumption now for more future consumption.B) Generally, higher current income means the person will save more, although people with the same income may have different time preferences.C) A variable affecting savings is the reward for saving, or the rate of interest on loans that savers make with their unconsumed income.D) The total savings (or the total supply of loans) available at any time is the sum of everybody's savings and a negative function of the interest rate.Answer: DComment: The total savings (or the total supply of loans) available at any time is the sum of everybody’s savings and a positive function of the interest rate.Diff: 2Topic: 10.1 The Theory of Interest RatesObjective: 10.2 the role in Fisher's theory of the saver's time preference and the borrowing firm's productivity of capital6) Which of the below statements about the rate of interest and cost of capital is FALSE?A) The maximum that a firm will invest depends on the rate of interest, which is the cost of loans; the firm will invest only as long as the marginal productivity of capital exceeds or equals the rate of interest.B) Firms will reject only projects whose gain is not less than their cost of financing.C) The firm's demand for borrowing is negatively related to the interest rate; if the rate is high, only limited borrowing and investment make sense.D) At a low rate of interest, more projects offer a profit, and the firm wants to borrow more; his negative relationship exists for each and all firms in the economy.Answer: BComment: The maximum that a firm will invest depends on the rate of interest, which is the cost of loans. The firm will invest only as long as the marginal productivity of capital exceeds or equals the rate of interest. In other words, firms will accept only projects whose gain is not less than their cost of financing. Thus, the firm’s demand for borrowing is negatively related to the interest rate. If the rate is high, only limited borrowing and investment make sense. At a low rate, more projects offer a profit, and the firm wants to borrow more. This negative relationship exists for each and all firms in the economy.Diff: 2Topic: 10.1 The Theory of Interest RatesObjective: 10.2 the role in Fisher's theory of the saver's time preference and the borrowing firm's productivity of capital7) The ________ rate of interest is determined by interaction of the supply and demand functions. As a cost of borrowing and a reward for lending, the rate must reach the point where total supply of savings ________ total demand for borrowing and investment.A) equilibrium; is greaterB) minimum; equalsC) equilibrium; equalsD) minimum; is greaterAnswer: CDiff: 2Topic: 10.1 The Theory of Interest RatesObjective: 10.3 the meaning of equilibrium and how changes in the demand and supply function affect the equilibrium level of the interest rate8) In the absence of inflation, the nominal rate ________ the real rate.A) equalsB) is greater thanC) is less thanD) greater than or equal toAnswer: ADiff: 1Topic: 10.1 The Theory of Interest RatesObjective: 10.3 the meaning of equilibrium and how changes in the demand and supply function affect the equilibrium level of the interest rate9) The relationship between inflation and interest rates is the well-known Fisher's Law, which can be expressed this way: (1 + i) = (1 + r) × (1 + i) where ________.A) r is the nominal rate.B) i is the real rate.C) p is the expected percentage change in the price level of goods and services over the loan's life.D) the nominal rate, p, reflects both the real rate and expected inflation.Answer: CComment: The relationship between inflation and interest rates is the well-known Fisher’s Law, which can be expressed this way: (1 + i) = (1 + r) × (1 + i) where i is the nominal rate, r is the real rate, and p is the expected percentage change in the price level of goods and services over the loan’s life. This equation shows that the nominal rate, i, reflects both the real rate and expected inflation.Diff: 2Topic: 10.1 The Theory of Interest RatesObjective: 10.4 the structure of Fisher's Law, which states that the nominal and observable interest rate is composed of two unobservable variables; the real rate of interest and the premium for expected inflation10) Which of the below IS considered by Fisher's theory.A) Fisher's theory takes into account the power of the government (in concert with depository institutions) to create money.B) Fisher's theory considers the government's often large demand for borrowed funds, which is frequently immune to the level of the interest rateC) Fisher's theory takes into account the possibility that individuals and firms might invest in cash balances.D) Fisher's theory considers an interest rate on loans that embodies no premium for default risk because borrowing firms are assumed to meet all obligations.Answer: DComment: Fisher’s theory is a general one and obviously neglects certain practical matters, such as the power of the government (in concert with depository institutions) to create money and the government’s often la rge demand for borrowed funds, which is frequently immune to the level of the interest rate. Also, Fisher’s theory does not consider the possibility that individuals and firms might invest in cash balances. Expanding Fisher’s theory to encompass these situations produces the loanable funds theory of interest rates.Diff: 2Topic: 10.1 The Theory of Interest RatesObjective: 10.4 the structure of Fisher's Law, which states that the nominal and observable interest rate is composed of two unobservable variables; the real rate of interest and the premium for expected inflation11) The loanable funds theory of interest rates proposes that the general level of interest rates is determined by the complex interaction of two forces. Which of the below is ONE of these forces?A) One force is that the total demand for funds by firms, governments, and households (or individuals) is negatively related to the interest rate including the government's demand.B) One force affecting the level of the interest rate is the total supply of funds by firms, governments, banks, and individuals with rising rates causing banks to be less eager to extend more loans.C) One force is that the total demand for funds by firms, governments, and households (or individuals) is positively related to the interest rate except the government's demand.D) One force affecting the level of the interest rate is the total supply of funds by firms, governments, banks, and individuals with rising rates causing firms and individuals to save and lend more.Answer: DComment: The loanable funds theory of interest rates proposes that the general level of interest rates is determined by the complex interaction of two forces. The first is the total demand for funds by firms, governments, and households (or individuals), which carry out a variety of economic activities with those funds. This demand is negatively related to the interest rate (except for the government’s demand, which may frequently not depend on the level of the interest rate). The second force affecting the level of the interest rate is the total supply of funds by firms, governments, banks, and individuals. Supply is positively related to the level of interest rates, if all other economic factors remain the same. With rising rates, firms and individuals save and lend more, and banks are more eager to extend more loans. (A rising interest rate probably does not significantly affect the government’s supply of savings.)Diff: 3Topic: 10.1 The Theory of Interest RatesObjective: 10.5 the loanable funds theory, which is an expansion of Fisher's theory12) The ________, originally developed by John Maynard Keynes,analyzes the equilibrium level of the interest rate through the interaction of the supply of money and the public's aggregate demand for holding money.A) loanable funds theory of interest ratesB) expectation theory of interest ratesC) liquidity preference theoryD) Fisher theoryAnswer: CDiff: 2Topic: 10.1 The Theory of Interest RatesObjective: 10.6 the meaning of liquidity preference in Keynes's theory of the determination of interest rates13) The public (consisting of individuals and firms) holds money for several reasons. Which of the below is three of these?A) Difficulty of translations, precaution against expected events, and speculation about possible rises in the interest rate.B) Ease of transactions, precaution against unexpected events, and speculation about possible rises in the interest rate.C) Ease of unexpected events, precaution against transactions, and speculation about possible rises in the interest rate.D) Speculation about transactions, fear against unexpected events, and precaution about possible rises in the interest rate.Answer: BDiff: 2Topic: 10.1 The Theory of Interest RatesObjective: 10.6 the meaning of liquidity preference in Keynes's theory of the determination of interest rates14) The ________ represents the initial reaction of the interest rate to a change in the money supply.A) Income effectB) Price expectation effectC) Liquidity effectD) Interest rate effectAnswer: CDiff: 2Topic: 10.1 The Theory of Interest RatesObjective: 10.7 how an increase in the money supply can affect the level of the interest rate through an impact on liquidity, income, and price expectations15) Which of the below statements is FALSE?A) Although an increase in the money supply is an economically expansionary policy, the resultant increase in income depends substantially on the amount of slack in the economy at the time of the Fed's action.B) In Fisher's terms, the interest rate reflects the interaction of the savers' marginal rate of time preference and borrowers' marginal productivity of capital.C) Changes in the money supply can affect the level of interest rates through the liquidity effect, the income effect, and the price expectations effect; their relative magnitudes depend upon the level of economic activity at the time of the change in the money supply.D) Because the price level (and expectations regarding its changes) affects the money demand function, the liquidity effect is an increase in the interest rate.Answer: DComment: Because the price level (and expectations regarding its changes) affects the money demand function, the price expectations effect is an increase in the interest rate.Diff: 2Topic: 10.1 The Theory of Interest RatesObjective: 10.7 how an increase in the money supply can affect the level of the interest rate through an impact on liquidity, income, and price expectations2 The Determinants of the Structure of Interest Rates1) A ________ is an instrument in which the issuer (debtor/borrower) promises to repay to the lender/investor the amount borrowed plus interest over some specified period of time.A) bondB) common stockC) preferred stockD) T-billAnswer: ADiff: 1Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.8 the features of a bond issue2) The ________ should reflect the coupon interest that will be earned plus either (1) any capital gain that will be realized from holding the bond to maturity, or (2) any capital loss that will be realized from holding the bond to maturity.A) yield on a bond investmentB) dividend yield on a bond investmentC) bid-ask spreadD) yield on a stock investmentAnswer: ADiff: 1Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.8 the features of a bond issue3) The ________ the market price, the higher the yield to maturity.A) higherB) less riskyC) more safeD) lowerAnswer: DDiff: 1Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.8 the features of a bond issue4) The ________ of a bond is the amount that the issuer agrees to repay the bondholder at the maturity date.A) principal value (or simply principal)B) face valueC) redemption valueD) All of theseAnswer: DComment: The principal value (or simply principal) of a bond is the amount that the issuer agrees to repay the bondholder at the maturity date. This amount is also referred to as the par value, maturity value, redemption value, or face value.Diff: 2Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.8 the features of a bond issue5) The yield to maturity is determined by a trial-and-error process. The first step in this trial and error process is ________.A) Compute the present value of each cash flow using the best guess interest rate.B) Total the present value of the cash flows using the best guess interest rate.C) Select an interest rate.D) Compare the total present value using the best guess interest rate with the market price of the bond.Answer: CComment: The yield to maturity is determined by a trial-and-error process. Even the algorithm in a calculator or computer program, which computes the yield to maturity (or internal rate of return) in an apparently direct way, uses a trial-and-error process. The steps in that process are as follows:Step 1: Select an interest rate.Step 2: Compute the present value of each cash flow using the interest rate selected in Step 1. Step 3: Total the present value of the cash flows found in Step 2.Step 4: Compare the total present value found in Step 3 with the market price of the bond and, if the total present value of the cash flows found in Step 3 is• equal to the market price, then the interest rate used in Step 1 is the yield to maturity;• greater than the market price, then the interest rate is not the yield to maturity. Therefore, go back to Step 1 and use a higher interest rate;• less than the market price, then the interest rate is not the yield to maturity. Therefore, go back to Step 1 and use a lower interest rate.Diff: 2Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.9 how the yield to maturity of a bond is calculated6) There are several interesting points about the relationship among the coupon rate, market price, and yield to maturity. Which of the below is NOT one of these.A) If the market price is equal to the par value, then the yield to maturity is equal to the coupon rate.B) If the market price is less than the par value, then the yield to maturity is greater than the coupon rate.C) If the market price is greater than the par value, then the yield to maturity is greater than the coupon rate.D) If the market price is greater than the par value, then the yield to maturity is less than the coupon rate.Answer: CComment: There are several interesting points about the relationship among the coupon rate, market price, and yield to maturity as summarized below.1. If the market price is equal to the par value, then the yield to maturity is equal to the coupon rate;2. If the market price is less than the par value, then the yield to maturity is greater than the coupon rate, and;3. If the market price is greater than the par value, then the yield to maturity is less than the coupon rate.Diff: 2Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.9 how the yield to maturity of a bond is calculated7) Consider an 20-year bond with a coupon rate of 8% and a par value of $1,000. The cash flow for this bond is ________ every six months for the first 39 semi-annual periods and then________ for the last (or 40th) six-month period.A) $1,040; $40B) $40; $1,040C) $80; $1,080D) $80; $1,000Answer: BComment: Consider an 20-year bond with a coupon rate of 8% and a par value of $1,000. The cash flow for this bond is $40 every six months for the first 39 semi-annual periods and then $1,040 for the last (or 40th) six-month period.Diff: 2Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.8 the features of a bond issue8) The difference between the yield on any two bond issues is called a ________.A) yield differenceB) difference spreadC) coupon rate spreadD) yield spreadAnswer: DDiff: 2Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.13 what factors affect the yield spread between two bonds9) Treasury securities are used to develop the benchmark interest rates. There are two categories of U.S. Treasury securities: ________.A) discount and coupon securities.B) discount and coupon stocks.C) interest rate and coupon securities.D) discount and compound securities.Answer: ADiff: 2Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.1 Fisher's classical approach to explaining the level of the interest rate10) The most recently auctioned Treasury issues for each maturity are referred to as ________.A) off-the-run issues or current coupon issues.B) minimum interest rate or base interest rateC) on-the- run or current coupon issues.D) benchmark interest rate or minimum interest rate.Answer: CComment: The most recently auctioned Treasury issues for each maturity are referred to as on-the- run or current coupon issues. Issues auctioned prior to the current coupon issues are typically referred to as off-the- run issues; they are not as liquid as on-the-run issues, and, therefore, offer a higher yield than the corresponding on-the-run Treasury issue. The minimum interest rate or base interest rate that investors will demand for investing in a non-Treasury security is the yield offered on a comparable maturity on-the-run Treasury security. The base interest rate is also referred to as the benchmark interest rate.Diff: 2Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.10 why historically the yields on securities issued by the U.S. Department of the Treasury have been used as the benchmark interest rates throughout the world11) Market participants talk of interest rates on non-Treasury securities as ________ to a particular on-the-run Treasury security (or a spread to any particular benchmark interest rate selected). This spread reflects the additional risks the investor faces by acquiring a security thatis not issued by the U.S. government and, therefore, can be called a ________.A) "trading at a premium"; risk premiumB) "trading at a spread"; risk premiumC) "trading at a premium"; risk spreadD) "trading at a discount"; discount premiumAnswer: BComment: Market participants talk of interest rates on non-Treasury securities as “trading at a spread” to a particular on-the-run Treasury security (or a spread to any particular benchmark interest rate selected). For example, if the yield on a 10-year non-Treasury security on May 20, 2008, is 4.78%, then the spread is 100 basis points over the 3.78% Treasury yield. This spread reflects the additional risks the investor faces by acquiring a security that is not issued by the U.S. government and, therefore, can be called a risk premium.Diff: 2Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.13 what factors affect the yield spread between two bonds12) The factors that affect the spread include ________.A) the type of issuer and the expected liquidity of the issueB) the provisions that grant either the issuer or the investor the obligation to do something and the taxability of the interest received by the issuerC) the investor's perceived creditworthiness and the term or maturity of the investor's horizon.D) All of theseAnswer: AComment: The factors that affect the spread are (1) the type of issuer, (2) the issuer’s perceived creditworthiness, (3) the term or maturity of the instrument, (4) provisions that grant either the issuer or the investor the option to do something, (5) the taxability of the interest received by investors, and (6) the expected liquidity of the issue.Diff: 2Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.13 what factors affect the yield spread between two bonds13) Within the corporate market sector, issuers are classified as ________.A) (1) utilities, (2) industrials, (3) finance, and (4) banks.B) (1) high-risk, (2) medium-risk, (3) low-risk, and (4) no-risk.C) (1) foreign, (2) domestic, (3) European, and (4) Asian.D) (1) intramarket, (2) extramarket, (3) ultramarket, and (4) intermarket.Answer: AComment: Within the corporate market sector, issuers are classified as follows: (1) utilities, (2) industrials, (3) finance, and (4) banks.Diff: 2Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.12 the different types of bonds14) The highest-grade bonds are designated by Moody's by the symbol ________.A) BaB) AC) AaD) AaaAnswer: DComment: In all systems, the term high grade means low credit risk, or conversely, high probability of future payments. The highest-grade bonds are designated by Moody’s by the symbol Aaa, and by S&P and Fitch by the symbol AAA. The next highest grade is denoted by the symbol Aa (Moody’s) or AA (S&P and Fitch); for the third grade, all rating systems use A. The next three grades are Baa or BBB, Ba or BB, and B, respectively. There are also C grades. Moody’s uses 1, 2, or 3 to provi de a narrower credit quality breakdown within each class, andS&P and Fitch use plus and minus signs for the same purpose.Diff: 1Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.12 the different types of bonds15) Which of the below statements is FALSE?A) The spread between Treasury securities and non-Treasury securities that are identical in all respects except for credit quality is referred to as a credit spread.B) The spread between any two maturity sectors of the market is called a maturity spread or yield curve spread.C) An option that is included in a bond issue is referred to as a prepayment option.D) The most common type of option in a bond issue is a call provision.Answer: CComment: It is not uncommon for a bond issue to include a provision that gives either the bondholder and/or the issuer an option to take some action against the other party. An option that is included in a bond issue is referred to as an embedded option.Diff: 2Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.12 the different types of bondsTrue/False Questions1 The Theory of Interest Rates1) The liquidity preference theory is Keynes's view that the rate of interest is set in the market for money balances.Answer: TRUEDiff: 1Topic: 10.1 The Theory of Interest RatesObjective: 10.6 the meaning of liquidity preference in Keynes's theory of the determination of interest rates2) Interest is the price paid for the permanent use of resources, and the amount of a loan is its principal.Answer: FALSEComment: Interest is the price paid for the temporary use of resources, and the amount of a loan is its principal.Diff: 1Topic: 10.1 The Theory of Interest RatesObjective: 10.7 how an increase in the money supply can affect the level of the interest rate through an impact on liquidity, income, and price expectations3) In Fisher's terms, the interest rate reflects the interaction of the savers' marginal productivity of capital and borrowers' marginal rate of time preference.Answer: FALSEComment: In Fisher’s terms, the interest rate reflects the interaction of the savers’ marginal rate of time preference and borrowers’ marginal productivity of capital.Diff: 1Topic: 10.1 The Theory of Interest RatesObjective: 10.2 the role in Fisher's theory of the saver's time preference and the borrowing firm's productivity of capital4) The loanable funds theory is an extension of Fisher's theory and proposes that the equilibrium rate of interest reflects the demand and supply of funds, which depend on savers' willingness to save, borrowers' expectations regarding the profitability of investing, and the government's action regarding money supply.Answer: TRUEDiff: 1Topic: 10.1 The Theory of Interest RatesObjective: 10.5 the loanable funds theory, which is an expansion of Fisher's theory2 The Determinants of the Structure of Interest Rates1) Convertible bonds are securities issued by state and local governments and by their creations, such as "authorities" and special districts.Answer: FALSEComment: Municipal bonds are securities issued by state and local governments and by their creations, such as “authorities” and special districts.Diff: 1Topic: 10.2 The Determinants of the Structure of Interest RatesObjective: 10.11 the reason why the yields on U.S. Treasury securities are no longer as popular as benchmark interest rates and what alternative benchmarks are being considered by market participants。