中国人寿SWOT分析

- 格式:docx

- 大小:12.83 KB

- 文档页数:2

互联网金融背景下保险企业发展策略研究——以中国人寿保险公司为例摘要目前来看,保险市场竞争日益激烈,原因有三:其一,保险行业市场主体在不断增加;其二,保险行业的监管发生了改革;第三,信息科技的发展正大力影响着保险行业传统的经营模式。

随着这些变化的发生,各家保险公司积极开展互联网金融业务,开设官方网站,推出移动应用,并与第三方平台合作。

与此同时,保险行业中也进入了不少以互联网公司为代表的外部资本,发展成为了互联网保险公司,其开展传统业务时也出现了在线代理服务。

保险公司出现的上述变化,在某种程度上代表了现代互联网与保险的深度融合。

2016年互联网保费收入高达2234亿元,与2011年相比,增长幅度出现了质的飞跃,据统计发现,5年期间,互联网保费增长近69倍。

因此,互联网金融的快速发展对于传统保险公司来说,既是一种挑战,也是一种机遇。

本文以中国保险业互联网金融发展为研究对象。

通过以中国人寿保险公司为样本的实证研究,在互联网保险快速发展的背景下,探讨了中国人寿保险公司的优势,劣势,机遇和威胁。

通过SWOT分析,本文认为,中国人寿保险公司应抓住当前互联网金融快速发展的机遇,采取差异化战略,重视产品和业务的差异化。

为了实现互联网保险更好的朝着生态化方向发展,需要开始注重同其他知名互联网平台的合作开展跨境开发和经营。

关键词:保险企业;互联网金融;互联网保险;差异化战略Research on the development strategy of insurancecompanies under the background of Internet Finance ——Taking China's life-insurance company as an exampleABSTRACTWith the increase of insurance market main body and the reform of industry supervision, the insurance market competition is becoming more and more fierce. At the same time, the development of information technology, represented by the Internet and big data, is having a subversive effect on the traditional business model of insurance industry. In recent years, insurance companies have actively entered Internet finance by opening official website stores, introducing mobile applications, and cooperating with third-party platforms. At the same time, many outside capital, which is represented by Internet companies, has entered the insurance industry one after another, setting up Internet insurance companies to carry out business or to carry out online agency business. The changes mark a deepening convergence between the Internet and insurance. Insurance premiums rose nearly 69 times from 2011 to 223.4 billion yuan in 2016, showing a rapid growth trend. For traditional insurance companies, the development of Internet finance is not only a challenge, but also a major development opportunity.This paper takes the development of Internet finance in China's insurance industry as the research object, and discusses the advantages and weaknesses of Chinese life insurance companies under the background of the rapid development of Internet insurance through the empirical study of Chinese life insurance companies as a sample. Through the analysis of SWOT, this paper holds that Chinese life insurance companies should seize the opportunity of the rapid development of Internet finance, adopt differentiation strategy and pay attention to the differentiation of products and operations. And focus on cooperation with other well-known Internet platforms,cross-border operation, in order to better achieve the ecological development of Internet insurance.Key words: insurance companies; Internet finance; differentiation strategy目录摘要 (1)前言 (6)一、互联网保险发展及对保险业的影响 (8)(一)我国互联网保险发展变迁历程及现状分析............ 错误!未定义书签。

中国人寿保险现状分析关键字:人寿保险老龄化机遇挑战一、中国人寿保险现状人寿保险是人身保险的一种。

和所有保险业务一样,被保险人将风险转嫁给保险人,接受保险人的条款并支付保险费。

与其他保险不同的是,人寿保险转嫁的是被保险人的生存或者死亡的风险。

中国寿险市场在过去十年中已增长成为全世界最大的市场之一,然而,中国人寿保险市场仍处于发展初期。

2021年,中国人寿保险市场的毛保费/GDP渗透率为2.5%,香港为10%,印度为4.4%,马来西亚为3.2%。

未来中国人寿保险业将受益于GDP的增长和人寿保险渗透率的提高。

我们预计到2021年中国人寿保险市场有望增长到4万亿元人民币,届时中国跃居为全球第二大人寿保险市场,仅次于美国。

二、中国人寿保险前景中国人寿保险自1982年恢复以来,保费收入从当初的0.159亿元上身到2021年近1000亿元,平均复合增长56.5%。

截至2021年末,我国人口总数为*****万人,其中,60岁及以上人口占比超过13%,比2021年上升2.93个百分点。

而按照联合国统计标准,60岁以上老年人口达到总人口的10%,为“老龄化社会”;超过14%为“老龄社会”。

据此,前瞻网分析认为,在未来一到两年,我国将正式迈入“老龄社会”。

中国年龄结构特点也使得我国在未来10年进入老龄化阶段后,人口老龄化的速度可能会快于日本韩国,这也对我国未来长期经济增长带来挑战。

据《2013-2021年中国人寿保险行业市场前瞻与投资战略规划分析报告》分析认为,老龄社会的到来,与老年人相关的消费需求也将呈现跳跃式增长。

老龄化在我国是不可逆转的趋势,老年人口抚养比约为11.55,我国未来养老市场需求增大,完全靠社会养老保险并不能满足养老需求,泰康人寿在保险业率先试水保险社区,是一种参与社会养老和医疗保障的创新模式。

分流社保养老压力,建立起全社会的多层次养老保障体系。

特别值得注意的是,人寿保险在保险业中的份额在不断上升。

中国人寿保险股份有限公司的公司基本分析1.1公司基本情况分析(1)公司的基本概况中国人寿保险股份有限公司(“中国人寿”或“本公司”)是中国最大的寿险公司,总部位于北京。

作为《财富》世界500 强和世界品牌500 强企业——中国人寿保险(集团)公司的核心成员,本公司以悠久的历史、雄厚的实力、专业领先的竞争优势及世界知名的品牌赢得了社会最广泛客户的信赖,始终占据中国寿险市场的主导地位。

中国人寿的前身与中华人民共和国同龄,是国内最早经营保险业务的企业之一。

1949 年10 月,中央政府批准组建了国内唯一的保险公司,由此开启了中国人寿的发展元年。

2003 年,中国人寿保险公司成功改制重组为中国人寿保险(集团)公司,并独家发起成立中国人寿保险股份有限公司。

2003 年12 月17 日、18 日, 中国人寿成功在纽约和香港上市,创造了2003 年全球最大IPO。

2007 年1 月9 日中国人寿成功回归A 股,在上海上市,成为首家在三地上市的金融保险企业。

本公司注册资本为人民币28,264,705,000 元。

多元的产品与服务中国人寿是中国领先的个人和团体人寿保险、年金产品、意外险和健康险供应商,公司控股中国人寿养老保险股份有限公司,参股中国人寿财产保险股份有限公司,并逐步涉足于其它保险相关领域。

广泛的分销和服务网络中国人寿拥有由保险营销员、团险直销人员以及专业和兼业代理机构组成的广泛分销和服务网络。

遍布全国的最广泛的分销网络最大的代理人队伍最多的直销人员最广泛的代理网点•1,290,000 余名保险营销员••60,000 余名团险直销人员50,000 个银行保险渠道销售代理网点•174,000 名客户经理及保险规划师无可比拟的客户服务网络• 1.8 万个营业网点•2600 多家客户服务柜面•专职客服人员•全天候服务热线“95519”广泛的客户基础中国人寿拥有最广泛的客户基础,是中国最知名的保险品牌之一。

截至2016 年 6 月30 日,中国人寿拥有约2.31 亿份有效的长期个人和团体人寿保险单、年金合同及长期健康险保单。

Study on Marketing Strategies for China Life Insurance Co. , Ltd. , Anhui Branch Based on 4V

Marketing Mix

作者: 程晓春[1];孙超平[2]

作者机构: [1]中国人寿保险股份有限公司安徽省公司,合肥230041;[2]合肥工业大学管理学院,合肥230009

出版物刊名: 科技和产业

页码: 84-90页

主题词: 4V营销理论;寿险;保障措施

摘要:在概述4V营销理论的基础上,文章运用SWOT分析框架具体分析了国寿安徽分公司实施4V营销策略的必要性和可能性,并运用4V理论提出了公司在实践中寿险营销者应注重综合运用多种策略和手段,影响消费者的购买行为,以达到扩大销售、增加利润的目的; 最后从人员配备、员工培训、信息化建设和政企关系等角度提出了实施4V营销组合策略的保障措施。

中国人寿保险的市场营销策略分析随着市场经济的不断深入和完善,社会对人寿保险的需求不断增大,人寿保险发挥着越来越重要的作用。

为此店铺为大家整理了中国人寿保险的市场营销策略分析,欢迎参阅。

中国人寿保险的市场营销策略分析篇一(一) 研究背景和意义金融是经济的命脉,保险业作为现代金融的三大支柱之一,具有经济补偿、资金融通与社会管理三大功能,对于保障国家经济建设、市场发展和社会安定发挥着极其重要的作用。

2006年,国务院发布了《国务院关于保险业改革发展的若干意见》,简称保险“国十条”,首次从国家层面肯定了改革开放特别是党的十六大以来的保险工作,同时为我国保险业的改革发展提出了要求,指明了方向。

当前,我国保险业发展已经站在一个新的历史起点上,发展潜力和空间巨大。

随着我国经济的高速发展、人民群众生活水平的不断提高和公众风险意识的不断增强,我国保险业在今后相当长的时间内还将会保持高速发展。

但目前保险业发展的黄金机遇期,也出现了一些值得思考的问题:一方面社会大众的保险意识不断提高,一方面人们对保险业的不满也在不断增多;一方面主动需求保险的群体不断扩大,一方面保险公司却出现了“展业难”“增员荒”;一方面保险机构快速增加,一方面公司盈利却在不断减少,部分业务甚至出现了全行业亏损的尴尬情景。

种种迹象显示,我国的保险市场己步入转型期。

在这一时期,保险销售不能再依靠传统“跑马圈地”的粗放发展方式,而应主动研究市场,以正确的营销思想指导销售实践,方可实现可持续发展。

因此,营销策略的选择将会直接影响到公司最终的经营结果和行业声誉,研究寿险公司的营销策略对于增强公司竞争力和行业平稳健康发展具有重要的现实意义。

(二) 研究内容和方法本文运用通过SWOT分析方法对中国人寿保险公司的营销环境进行分析。

首先介绍中国人寿保险公司营销业务发展现状;然后对中国人寿保险的市场营销进行准确定位;与西方发达国家的人寿保险市场营销策略进行对比之后,找出我国人寿保险在市场营销策略中存在的问题、市场转型面临的挑战与机遇等问题,分析中国人寿保险公司营销业务所处的宏观环境和微观环境,梳理其面临的机会和威胁、优势和劣势,得出中国人寿保险公司营销业务发展的相关结论。

对国寿未来发展的想法-概述说明以及解释1.引言1.1 概述国寿作为中国最大的保险公司之一,其未来发展备受关注。

随着社会经济的快速发展和人们保险意识的提高,国寿在未来面临着巨大的发展机遇和挑战。

因此,对国寿未来发展进行深入的思考和研究具有重要意义。

首先,国寿作为保险行业的龙头企业,已经形成了较为完善的经营模式和广泛的客户基础。

公司具备雄厚的资金实力和专业的保险团队,在产品创新、风险控制、服务质量等方面都展现出了强大的竞争力。

然而,随着社会变革的加快和市场竞争的加剧,国寿需要不断提升自身的竞争力,不断创新和优化产品和服务,以满足客户日益增长的多样化需求。

其次,随着我国经济社会的发展和人口老龄化趋势的加快,养老保险市场潜力巨大。

国寿可以借助自身的优势,在养老保险领域加大投入和力度,在产品设计、销售模式、渠道建设等方面进行创新,开发更加灵活、多样化的养老保险产品,以应对人们的养老需求。

另外,国寿还可以加强与金融机构和科技企业的合作,通过技术手段提升运营效率和服务水平,打造智慧养老保险平台,进一步提升市场份额和竞争力。

最后,国寿还可以积极拓展海外市场,利用自身的品牌优势和专业能力,在国际保险市场中寻找新的增长点。

通过与国外保险公司的合作、开展跨境业务等方式,扩大国寿在全球范围内的经营规模和影响力,实现更加全面与多元化的发展。

综上所述,国寿未来发展的前景广阔,机遇与挑战并存。

公司需要进一步提升自身的核心竞争力,在养老保险领域深耕细作,在国际市场中寻求新的突破。

同时,加强内部管理、提升服务水平、加强创新能力也是国寿未来发展的关键。

只有不断适应时代变化、顺应市场需求,才能确保国寿在保险行业的持续发展和领先地位的巩固。

1.2 文章结构文章结构部分的内容可以从以下几个方面展开:首先,为了让读者对文章有一个清晰的认识,本文将采用以下结构进行组织。

文章分为引言、正文和结论三个部分。

在引言部分,将对国寿公司未来发展的概述进行介绍,说明本文的目的和重要性,并给出本文的大纲。

对中国人寿保险股份有限公司的SWOT分析一、公司简介中国人寿保险(集团)公司作为中国最大的商业保险集团,是国内几家资产过万亿的保险集团之一,是中国资本市场最大的机构投资者之一。

2011年,总保费收入达到3573.75亿元,境内寿险业务市场份额为34.75%,总资产达到2万亿元。

中国人寿保险(集团)公司作为中国最大的商业保险集团,是国内几家资产过万亿的保险集团之一,是中国资本市场最大的机构投资者之一。

2011年,总保费收入达到3573.75亿元,境内寿险业务市场份额为34.75%,总资产达到2万亿元。

中国人寿保险(集团)公司属国有大型金融保险企业,总部设在北京。

公司前身是成立于1949年的原中国人民保险公司,1996年分设为中保人寿保险有限公司,1999年更名为中国人寿保险公司。

集团下设有中国人寿资产管理有限公司、中国人寿财产保险股份有限公司、中国人寿养老保险股份有限公司、中国人寿保险(海外)股份有限公司、国寿投资控股有限公司以及保险职业学院等多家公司和机构,业务范围全面涵盖寿险、财产险、养老保险(企业年金)、资产管理、另类投资、海外业务等多个领域,并通过资本运作参股了多家银行、证券公司等其他金融和非金融机构。

中国人寿保险(集团)公司已连续8年入选《财富》全球500强企业,排名由2002年的290位跃升为2011年的108位;连续3年入选世界品牌500强,位列第278位,是中国保险业唯一一家全球企业、全球品牌“双500强”企业;在“2011中国企业500强”中,营业收入3887.91亿元人民币列第6位。

所属寿险股份公司继2003年12月在纽约、香港两地同步上市之后,又于2007年1月回归境内A股市场,成为内地资本市场“保险第一股”和全球第一家在纽约、香港和上海三地上市的保险公司,目前已成为全球市值最大的上市寿险公司。

二、SWOT分析1、优势(1)中国人寿保险股份有限公司是中国最大的人寿保险公司,拥有深入人心的品牌形象和雄厚的整体实力,其注册资本高达282.65亿元人民币,资本充足率是法定资本充足率的3倍之高,为公司的良性发展提供了强有力的支持。

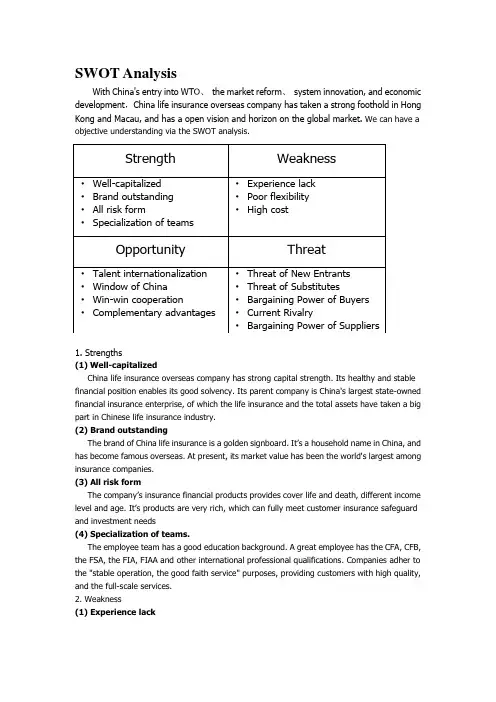

SWOT AnalysisWith China's entry into WTO、the market reform、system innovation, and economic development,China life insurance overseas company has taken a strong foothold in Hong Kong and Macau, and has a open vision and horizon on the global market. We can have a objective understanding via the SWOT analysis.1. Strengths(1)Well-capitalizedChina life insurance overseas company has strong capital strength. Its healthy and stable financial position enables its good solvency. Its parent company is China's largest state-owned financial insurance enterprise, of which the life insurance and the total assets have taken a big part in Chinese life insurance industry.(2) Brand outstandingThe brand of China life insurance is a golden signboard. It’s a household name in China, and has become famous overseas. At present, its market value has been the world's largest among insurance companies.(3) All risk formThe company’s insurance financial products provides cover life and death, different income level and age. It’s products are very rich, which can fully meet customer insurance safeguard and investment needs(4) Specialization of teams.The employee team has a good education background. A great employee has the CFA, CFB, the FSA, the FIA, FIAA and other international professional qualifications. Companies adher to the "stable operation, the good faith service" purposes, providing customers with high quality, and the full-scale services.2. Weakness(1) Experience lackAlthough China Life Overseas Company has been operating in Hong Kong for 26 years, it’s too short for it to lead the international financial and insurance conglomerate. Native culture was well-entrenched. There is a big different between in Domestic and foreign marketing strategy,making it less competitive in competing with the oversea insurance companies. (2) Poor flexibilityThe globalization mode of operation is a remarkable characteristic of the multinational company. For simplified management and economy of consideration, China Life Overseas Company carries out the strategy within the global scope standardization, such as the key strategic, product strategy and brand strategy. It is a unified global headquarters in all countries, a subsidiary is difficult to affect these key strategy planning, It can only be enforced to carry out them. This mode of a specific market, obviously can't reach the best efficiency. (3) High costBecause the China Life Overseas Company applies mechanically the successful mode in China to the process of product promotion, it lacks creative spirit to aim at the overseas reality. Such a high cost makes it less competitive in the fierce competition. Technology advantage is not obvious in the product which has a total cost competitive disadvantage.3. Opportunity(1) Talent internationalizationWe should pay attention to the point of view of the internationalized personnel training for serving us and realize the talents adopted by us with broad mind and spirit of innovation. It’s a good opportunity for us to make up for the deficiency of the individual talent.(2) Window of ChinaIt will be the leading professional insurance company in the Hong Kong-Macau markets, achieved via organic growth and acquisitions, as well as business development and investment management that deliver strong profit growth and value creation. It will be the window of China Life in expanding overseas markets, the base where excellent management talents are nurtured, the platform on which advanced technology and global information exchange, and the link through which our brand image exemplifies.(3) Win-win cooperationAfter China joined WTO, it will speed up the internationalization of enterprises. And it will be helpful for the management of the enterprise management , operation mechanism, talent cultivation and the international community. At the same time, we can promote the China insurance market to learn from foreign company, and actively promote thinking, the technology, the system innovation, improve the product specification, reduce the cost, improve the service quality and improve marketing strategy, enhance our core competitiveness.(4) Complementary advantagesChina Life Insurance Overseas Company Limited is undoubtedly dedicated in becoming the platform for its parent company to develop its global business. Besides being a training ground for its remarkable business management team, it also provides a global platform for the exchange of advanced techniques and information. With this, its worldwide corporate image can be established and promoted.4. Threat(1)Threat of New EntrantsSome factors, such as economies of scale, and brand loyalty, capital scale, decided the new rivals into a degree of difficulty of the industry. The new entrants to the industry brings in new production capacity, and new resources. At the same time, it will divide up the existing enterprise insurance market and win a place, which eventually leads to the reduced profit of the existing enterprise and may endanger the enterprise survival.(2)Threat of SubstitutesPersonal finance becomes increasingly popular. First of all, the product price and potential profit increase will be limited because the substitute. Second, because of the invasion of the producer, China life insurance must improve product quality, reduce cost or make their products with characteristics through reduce price. Otherwise its sales and profit growth target may be frustrated. Third, the competition intensity from substitute by producers will be influenced most by the buyers’ value orientation of the products.(3)Bargaining Power of BuyersIt is the degree to which buyers have the market strength to hold sway over and influence competitors in an industry. The number of customers, customers by the master of information, and the availability of alternatives, decided the influence degree of the buyers in the industry.(4)Bargaining Power of SuppliersThe relative number of buyers to suppliers and threats from substitutes and new entrants affect the buyer-supplier relationship. Supplier's concentration and alternative input availability, decide the relative to the enterprise in the industry supplier of the ability to influence. The strength of supplier depends on what input elements they have to offer to the purchaser. (5)Current RivalryIntensity among rivals increases when industry growth rates slow, demand falls, and product prices descend. As for most of the companies in industries, the mutual interests are closely together. The enterprise competition strategy as a part of the whole enterprise strategy, its goal is to make their enterprises to gain the advantage relative to the competition.。

S保险公司寿险业务的SWOT分析目录S保险公司寿险业务的SWOT分析 (1)1 优势 (1)2 劣势 (2)3 机遇 (2)4 挑战 (3)5 SWOT矩阵 (3)1 优势品牌优势。

S保险公司保险一直秉承“以优秀的传统文化为基础,以追求卓越为过程,以价值最大化为导向的经营理念。

通过不断的努力,为客户提供了“专业,让生活更简单”的体验。

经过几十年的发展和沉淀,在服务客户的过程中,公司的文化内涵不断彰显,公司的责任感、公司发展的美好愿景也在不断得到客户的认同,公司的品牌影响力越来越强,越来越受关注。

金融服务优势。

S保险公司的业务覆盖面比较广,是一种集保险、证券、银行为一体服务的综合金融平台,截止到2019年底,S保险公司的总资产达到8.22万亿元,营业利润达到1329.55亿元,营业收入达到11688.67亿元,个人客户数量突破2亿人次,使用互联网相关技术支持的客户数量超过5亿人次,这些人多是金融客户。

从S保险公司的业务覆盖范围来看,其掌握了多家金融市场的命脉,内部信息系统的建立比较全面和完善,客户通过S保险公司提供的一个账号可以享受到多个领域的金融服务,服务效率大大增加,服务业务也变得多样化,大大提升了人力资源的使用效率。

这种一站式的、全面的金融服务体系为客户提供了极大便利,成为公司的主要发展优势。

AI技术优势。

S保险公司着力打造客户服务体系,从平安金管家的使用情况来看,目前使用平安金管家的客户已经超过一亿人次,这是一款移动APP产品,客户可以随时随地查看购买的保险产品的状态,了解各个保险类别的特点,随时选择进行相关的服务体验,从而帮助客户节约时间,同时也有利于保险代理人开展相关的保险业务。

同时,S保险公司积极使用和开发AI技术,采用AI技术进行智慧客服的建设。

AI技术支持保险投保申请核算,核算的精确度能达到95%以上,并且用时少,节约时间成本,采用智慧客服还可以进行在线保单服务,通常服务时间在3分钟左右。

保险作为金融行业的三大支柱之一,在我国多个领域发挥着重要作用,对我国经济的发展起着巨大推动作用。

在当前大的经济环境、社会环境和民众观念开放等有利情形下,我国保险业的发展有目共睹,市场规模和产品数量都获得了极大的进步。

但随着市场经济的不断深化、市场开放程度的不断加深,人民对寿险的需求不断增强,众多保险公司都纷纷推出保险产品来抢占市场。

保险行业也进入崭新的发展阶段,同时在发展中也存在着许多问题。

在这样的国内形势以及行业发展的趋势下,中国人寿保险公司酒泉分公司也借此快速发展,但在发展过程中也随之而来出现了各种问题,保险公司应该知道,如果再不埋头苦练“内功”,还用着老观念、老思想的销售模式,必将被这个大的市场环境淘汰,而努力寻找新的营销模式,消除“壁垒”,把握人们的消费心理,把握大的市场环境才是当务之急。

古语云“工欲善其事必先利其器”,用前瞻性的目光看待市场变化,用专业营销知识武装自己,借市场这个大平台培训自己的专业,如此,保险公司才能行走在市场前列。

一、中国人寿保险公司酒泉分公司营销现状(一)酒泉分公司发展现状中国人寿酒泉分公司成立于1951年,自成立以来,一直是酒泉保险行业的排头兵。

在酒泉寿险市场,中国人寿资产规模、客户资源、市场份额、机构数量、从业人员均遥遥领先。

截至2018年底,公司总保费收入93038.92万元,总资产达548420.54万元,目前下辖9个县区级公司,机构网络覆盖全市,销售队伍遍布城乡,共有合同制员工和营销员3000多人。

在售产品涵盖生存养老、疾病医疗、意外保障等全方位保险产品,多层次满足客户在人身保险领域的保险保障需求,已累计为全市33.47多万客户承担了超过517亿元的风险保障。

(二)酒泉分公司营销现状1.核心销售指标增幅明显全年实现股份总保费9.8亿元,增幅5.1%。

其中首年期缴保费1.5亿元,增幅39%;十年期及以上首年期缴保费7303万元,增幅32%;标准保费6856万元,增幅16%;短期险保费5539万元,增幅14%。

一、万科(000002 , SZ)优势1、中国房地产龙头企业,主营住宅物业发展,竞争优势明显。

综合竞争力、市场占有率和品牌价值排名第一。

2、万科强大的竞争力不仅体现在其强大的销售规模和跨区域运营能力,还体现在其稳健的商业模式、完善的公司治理结构、强大的融资能力以及快速应变的营销策略等。

3、公司财务状况良好,融资渠道通畅。

即使在2008年行业整体资金较为紧张的背景下,公司仍保持充裕的流动性和健康的负债状况。

4、公司的增长方式由规模速度增长向质量效益增长转变,重点关注项目的质量和赢利能力,这将有助于公司在市场调整期的平稳增长。

5、1992?2008年公司收入和净利润的复合增速分别为28.7%和33.6%。

劣势土地储备约2200万平方米,仅能满足万科2?3年的发展需要,低于行业平均水平,可能会影响其增长并增加土地购置成本。

机会1、中国房地产行业集中度仍较低,万科将通过整合行业资源提高市场占有率。

2、住宅产业化或将成为万科未来核心竞争力的主要来源之一。

威胁绿城、恒大等民营房地产公司的高速扩张,削弱了万科的竞争优势,对其未来增长构成有力威胁。

二、保利地产(600048 ,SH)优势1、公司最大的竞争优势在于其资源优势。

由于公司的控股股东保利集团源于总参装备部,其在全国各主要城市和地区都具有丰富的资源,包括土地、资金和人脉。

这有利于保利地产在全国各地的扩张,而且也非常有利于控制公司的扩张风险。

2、土地储备规模快速增长,保利地产项目储备增至3200万平方米,在一、二线城市形成全国性布局。

其中二、三线城市分布集中在珠三角、环渤海和西南地区,占总储备的71%。

其具有刚性需求占比高、政策紧缩风险小等优势。

3、公司成长性好,增长迅猛。

过去五年保利地产的营业额和净利润的复合增长率分别为72%和77%,远高于同行业其他竞争对手。

4、良好的执行力将保证公司高速发展。

劣势1、公司在2009年购入约1000万平方米的土地储备,土地成本较高,这使其应对市场调整时的销售价格弹性较小。

对中国人寿保险股份有限公司的SWOT分析

一、简介

1、中国人寿保险股份有限公司简介

中国人寿保险股份有限公司是中国大陆历史最悠久、最大的寿险公司,长期居于国内行业第一的位置在全球上市寿险公司中总市值名列第一,在全国范围内有着广泛的知名度和稳固的市场地位

二、SWOT分析

1、SWOT分析的概念

SWOT分析法又称为态势分析法,它是由旧金山大学的管理学教授于20世纪80年代初提出的。

S——优势Strength、W——劣势Weakness、O——机会opportunity、T——威胁Threat。

2、SWOT分析的步骤

(1)分析影响公司竞争力的内外部因素,运用调查研究、数据分析等方法分析出公司所处的外部环境因素O、T和内部能力因素S、W。

(2)构造SWOT矩阵

(3)制定行动计划

三、中国人寿保险股份有限公司的SWOT分析

1、优势

(1)中国人寿保险股份有限公司是中国最大的人寿保险公司,拥有深入人心的品牌形象和雄厚的整体实力,其注册资本高达282.65亿元人民币,资本充足率是法定资本充足率的3倍之高,为公司的良性发展提供了强有力的支持。

中国人寿保险集团更连续9年入选世界500强连续3年入选世界品牌500强是中国唯一一家双500强保险企业。

(2)为适应新的市场和经济形势,中国人寿积极地进行了结构调整。

结构调整后,公司实行展、管分离。

管理上的改革为公司业务的进一步发展提供了可能,而理赔等相关工作的回收也让公司少了很多后顾之忧。

(3)中国人寿保险股份有限公司拥有庞大的营销队伍,广泛的代理网点、银行分支机构和邮政储蓄网点、营业网点覆盖全市。

其中有近一半的网点设在广大农村地区、许多地方仅此一家保险机构。

2、劣势

(1)巨大的运营成本和管理压力使得公司应对市场变化的效率低下。

制度层面上管理不够灵活实际操作中大多依靠地区负责人的管理能力予以弥补,仍然存在忽视制度建设的情况存在发生管理事故的隐患。

(2)公司人才流失现象较严重。

原有的管理体制和僵化的用人体制使得很多专业人才得不到更多的机会和相匹配的重视在同业挖角的吸引下往往选择离开。

(3)财务上对于利润率的要求没有在经营过程中得到充分的重视,仅仅作为次一等的要求而更多的强调市场占有率,由此带来公司经营成本和费用的管制迟迟见不到成效。

3、机会

(1)法律政策环境逐步完善。

保险的资金融通、社会保障和三大功能为构建和谐社会做出了极大贡献,国家和当地政府对寿险采取支持政策,制定了一系列法律法规,完善制度加强监督,促进了寿险业的规范发展。

(2)企业、公民的保险意识不断提高。

通过几十年的宣传和正确引导,人们对保险的认识

正在逐步加深,保险需求也越来越多。

而我国保险密度尚小、保险深度尚浅,国内保险市场发展空间巨大。

(3)随着我国GDP高速增长,国民收入逐年提高,中等收入者开始成为社会的主体。

公民的基本生活得到满足后,有了更多的剩余资产满足更高层次的需求,开始了解更多的理财知识,保险作为更稳健、更安全的理财手段之一得到了越来越多的关注。

(4)作为人口大国,中国正在逐步走向老龄化,社会养老压力的加大极大地促进了寿险、养老保险需求的增加。

4、挑战

(1)保险市场开放后,保险市场的竞争加大。

本土企业和外资企业相继进入市场,争夺市场份额。

(2)经济的发展和社会的进步对公司的资本运用提出了更高的要求。

尤其是在竞争越来越激烈的今天,成本管理已然成为了各公司的重要能力之一。

保险公司面临着人力成本上升,管理成本加大,理赔、保全等服务成本增加,品牌维护成本提高等各方面的挑战。

(3)寿险产品的收益率仍然受国家政策的影响和管制,其吸引力显然难以与银行、证券、股票买卖、基金、期货、外汇等的众多理财想抗衡,尤其是在银行利率连续上升的近几年。

而且随着大家教育水平的提升,对金融相关知识的加深了解,保险产

品将会面临更大的挑战。

四、SWOT矩阵战略

SO依靠内部优势利用外部机会,坚持资本优化,开发多样化的保险产品,以满足市场日增的需求,提高管理水平,进一步提高成本控制水平,加强营销员培训,为客户提供更专业、能都带来更多收益的服务和产品。

ST利用内部优势回避外部威胁,通过更好的服务、更低的成本和更多样化的产品提高市场竞争力,坚持深化公司结构转型,从而可持续发展,提高企业品牌价值,提升竞争力。

WO利用外部机会克服内部弱点,通过加强与银行等机构的合作,加强公司宣传,抢占市场份额,借鉴其他公司管理经验、服务方式等,提高经营水平。

WT减少内部弱点回避外部威胁,重视对人才的关注和培养,提高员工的工作效率和能力

以人为本,提高公司的经营管理能力。

增强公司诚信合规教育和督察,让公司诚信为本、一言九鼎的形象深入人心,从而提高公司的整体竞争力。

五、战略上的建议

当前的市场环境下,市公司所在保险市场发展较为成熟,行业竞争趋于白热化,传统销售渠道总体仍在健康稳步增长,未来的增长将来自于大众客户群的进一步扩大。

县支公司和农村地区,保险行业的渗透率较低,增长速度较高,未来的增长来源将来自于对大众客户的进一步渗透和越来越多买得起保险产品的人群。

而公司在二三线城市和农村地区的市场优势明显随着地区经济发展,这一部分市场将被逐渐开发出来,利益也将渐渐得到体现。

在这些地区公司需要加强制度建设,保护被保险人的利益,避免保费挪用、克扣等恶性事件的发生,维护企业形象,维持公司信誉,视市场情况加强营销力度。

整体上看,公司需要控制运营成本,提高资金运用水平,规避各种风险。

同时,也要特别注重吸引专业人才,为应对更加复杂的市场环境变化做人才准备。