Chapter 8 Valuation of Bonds(Finance -东北财经大学, 赵颜之)

- 格式:ppt

- 大小:84.00 KB

- 文档页数:10

CHAPTER 8VALUATION OF KNOWN CASH FLOWS: BONDSObjectivesTo show how to value contracts and securities that promise a stream of cash flows that are known with certainty.To understand the shape of the yield curve .To understand how bond prices and yields change over time.OutlineUsing Present Value Formulas to Value Known Cash FlowsThe Basic Building Blocks: Pure Discount BondsCoupon Bonds, Current Yield, and Yield to MaturityReading Bond ListingsWhy Yields for the Same Maturity DifferThe Behavior of Bond Prices over TimeSummaryA change in market interest rates causes a change in the opposite direction in the market values of all existing contracts promising fixed payments in the future.The market prices of $1 to be received at every possible date in the future are the basic building blocks for valuing all other streams of known cash flows. These prices are inferred from the observed market prices of traded bonds and then applied to other streams of known cash flows to value them.An equivalent valuation can be carried out by applying a discounted cash flow formula with a different discount rate for each future time period.Differences in the prices of fixed-income securities of a given maturity arise from differences in coupon rates, default risk, tax treatment, callability, convertibility, and other features.Over time the prices of bonds converge towards their face value. Before maturity, however, bond prices can fluctuate a great deal as a result of changes in market interest rates.Solutions to Problems at End of ChapterBond Valuation with a Flat Term Structure1. Suppose you want to know the price of a 10-year 7% coupon Treasury bond that pays interestannually.a. You have been told that the yield to maturity is 8%. What is the price?b. What is the price if coupons are paid semiannually, and the yield to maturity is 8% per year?c. Now you have been told that the yield to maturity is 7% per year. What is the price? Could youhave guessed the answer without calculating it? What if coupons are paid semiannually?SOLUTION:a. With coupons paid once a year:b. With coupons paid twice a year:c. Price = 100. When the coupon rate and yield to maturity are the same, the bond sells at par value . theprice equals the face value of the bond).2. Assume six months ago the US Treasury yield curve was flat at a rate of 4% per year (with annual compounding) and you bought a 30-year US Treasury bond. Today it is flat at a rate of 5% per year. What rate of return did you earn on your initial investment:a.If the bond was a 4% coupon bond?b.If the bond was a zero coupon bond?c.How do your answer change if compounding is semiannual?SOLUTION:a and b.Step 1: Find prices of the bonds six months ago:n i PV FV PMT Result304?1004PV =100 Coupon =4%Zero304?1000PV = couponStep 2: Find prices of the bonds today:n i PV FV PMT Result Coupon =5?1004 4%Zero5?1000 couponStep 3: Find rates of return:Rate of return = (coupon + change in price)/initial price4% coupon bond: r = (4 + 100)/100 = or %Zero-coupon bond: r = (0 + / = or %. Note that the zero-coupon bond is more sensitive to yield changes than the 4% coupon bond.c.Step 1: Find prices of the bonds six months ago:n i PV FV PMT Result Coupon=4602?1002PV =100 %Zero602?1000PV = couponStep 2: Find prices of the bonds today:n i PV FV PMT Result59?1002 Coupon=4%Zero59?1000 couponStep 3: Find rates of return:Rate of return = (coupon + change in price) / initial price4% coupon bond: r= (2 + 100)/100 = or %Zero coupon bond: r= (0 + / = or %. Note that the zero-coupon bond is more sensitive to yield changes than the 4% coupon bond.Bond Valuation With a Non-Flat Term Structure3. Suppose you observe the following prices for zero-coupon bonds (pure discount bonds) that have no risk of default:Maturity Price per $1 of Face Value Yield to Maturity1 year%2 yearsa.What should be the price of a 2-year coupon bond that pays a 6% coupon rate, assuming couponpayments are made once a year starting one year from now?b.Find the missing entry in the table.c.What should be the yield to maturity of the 2-year coupon bond in Part a?d.Why are your answers to parts b and c of this question different?SOLUTION:a. Present value of first year's cash flow = 6 x .97 =Present value of second year's cash flow = 106 x .90 =Total present value =b. The yield to maturity on a 2-year zero coupon bond with price of 90 and face value of 100 is %c. The yield to maturity on a 2-year 6% coupon bond with price of isto maturity.Coupon Stripping4. You would like to create a 2-year synthetic zero-coupon bond. Assume you are aware of the following information: 1-year zero- coupon bonds are trading for $ per dollar of face value and 2-year 7% coupon bonds (annual payments) are selling at $ (Face value = $1,000).a. What are the two cash flows from the 2-year coupon bond?b. Assume you can purchase the 2-year coupon bond and unbundle the two cash flows and sell them.i. How much will you receive from the sale of the first payment?ii. How much do you need to receive from the sale of the 2-year Treasury strip to break even?SOLUTION:a. $70 at the end of the first year and $1070 at the end of year 2.b. i. I would receive .93 x $70 = $ from the sale of the first payment.ii. To break even, I would need to receive $ $ = $ from the sale of the 2-year strip.The Law of One price and Bond Pricing5. Assume that all of the bonds listed in the following table are the same except for their pattern of promised cash flows over time. Prices are quoted per $1 of face value. Use the information in the table and the Law of One Price to infer the values of the missing entries. Assume that coupon payments are annual.SOLUTION:Bond 1:From Bond 1 and Bond 4, we can get the missing entries for the 2-year zero-coupon bond. We know from bond 1 that:= +2. This is also equal to (1+z 1) + (1+z 2)2 where z 1 and z 2 are the yields to maturity on one-year zero-coupon and two-year zero-coupon bonds respectively. From bond 4 , we have z 1, we can find z 2.– = (1+z 2)2, hence z 2 = %.To get the price P per $1 face value of the 2-year zero-coupon bond, using the same reasoning: – = , hence P =To find the entries for bond 3: first find the price, then the yield to maturity. To find the price, we can use z 1 and z 2 found earlier:PV of coupon payment in year 1: x =PV of coupon + principal payments in year 2: x = Total present value of bond 3 =Hence the table becomes:Bond Features and Bond Valuation6. What effect would adding the following features have on the market price of a similar bond which does not have this feature?a.10-year bond is callable by the company after 5 years (compare to a 10-year non-callable bond);b.bond is convertible into 10 shares of common stock at any time (compare to a non-convertiblebond);c.10-year bond can be “put back” to the company after 3 years at par (puttable bond) (compare toa 10-year non-puttable bond)d.25-year bond has tax-exempt coupon paymentsSOLUTION:a.The callable bond would have a lower price than the non-callable bond to compensate thebondholders for granting the issuer the right to call the bonds.b.The convertible bond would have a higher price because it gives the bondholders the right to converttheir bonds into shares of stock.c.The puttable bond would have a higher price because it gives the bondholders the right to sell theirbonds back to the issuer at par.d.The bond with the tax-exempt coupon has a higher price because the bondholder is exempted frompaying taxes on the coupons. (Coupons are usually considered and taxed as personal income).Inferring the Value of a Bond Guarantee7. Suppose that the yield curve on dollar bonds that are free of the risk of default is flat at 6% per year. A 2-year 10% coupon bond (with annual coupons and $1,000 face value) issued by Dafolto Corporation is rates B, and it is currently trading at a market price of $918. Aside from its risk of default, the Dafolto bond has no other financially significant features. How much should an investor be willing to pay for a guarantee against Dafolto’s defaulting on this bond?SOLUTION:If the bond was free of the risk of default, its yield would be 6%.the value of a guarantee against default: = $The implied Value of a Call Provision and Convertibility8. Suppose that the yield curve on bonds that are free of the risk of default is flat at 5% per year. A 20-year default-free coupon bond (with annual coupons and $1,000 face value) that becomes callable after 10 years is trading at par and has a coupon rate of %.a.What is the implied value of the call provision?b. A Safeco Corporation bond which is otherwise identical to the callable % coupon bond describedabove, is also convertible into 10 shares of Safeco stock at any time up to the bond’s maturity. If its yield to maturity is currently % per year, what is the implied value of the conversion feature?SOLUTION:a.We have to find the price of the bond if it were only free of the risk of default.is the implied value of the call provision: – 1000 = $Note that the call provision decreases the value of the bond.b.We have to find the price of the Safeco Corporation:This bond has the same features as the % default free callable bond described above, plus an additional feature: it is convertible into stocks. Hence the implied value of the conversion feature is the difference between the values of both bonds: = $. Note that the conversion feature increases the value of the bond.Changes in Interest Rates and Bond Prices9. All else being equal, if interest rates rise along the entire yield curve, you should expect that:i. Bond prices will fallii. Bond prices will riseiii. Prices on long-term bonds will fall more than prices on short-term bonds.iv. Prices on long-term bonds will rise more than prices on short-term bondsa. ii and iv are correctb. We can’t be certain that prices will changec. Only i is correctd. Only ii is correcte. i and iii are correctSOLUTION:The correct answer is e.Bond prices are inversely proportional to yields hence when yields increase, bond prices fall. Long-term bonds are more sensitive to yield changes than short-term bonds.。

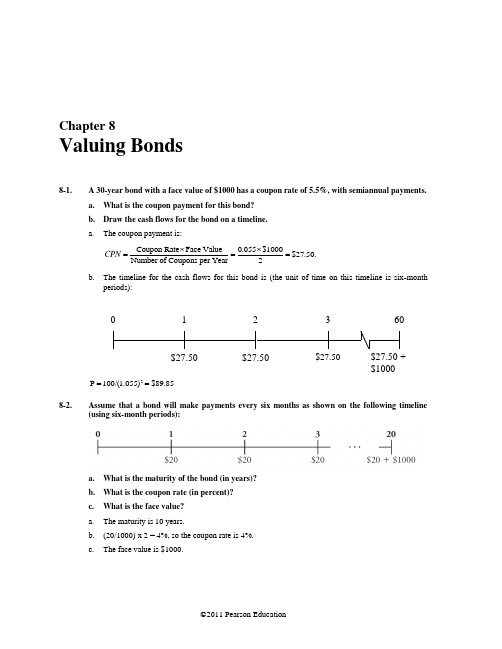

Chapter 8Valuing Bonds8-1.A 30-year bond with a face value of $1000 has a coupon rate of 5.5%, with semiannual payments. a. What is the coupon payment for this bond? b. Draw the cash flows for the bond on a timeline. a. The coupon payment is:Coupon Rate Face Value 0.055$1000$27.50.Number of Coupons per Year 2CPN ⨯⨯===b. The timeline for the cash flows for this bond is (the unit of time on this timeline is six-monthperiods):2P 100/(1.055)$89.85==8-2.Assume that a bond will make payments every six months as shown on the following timeline(using six-month periods):a. What is the maturity of the bond (in years)?b. What is the coupon rate (in percent)?c. What is the face value? a. The maturity is 10 years.b. (20/1000) x 2 = 4%, so the coupon rate is 4%.c. The face value is $1000.1 $27.50 02 $27.503 $27.5060$27.50 +$1000Berk/DeMarzo •Corporate Finance, Second Edition 1078-3.The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value):a. Compute the yield to maturity for each bond.b. Plot the zero-coupon yield curve (for the first five years).c. Is the yield curve upward sloping, downward sloping, or flat?a. Use the following equation.1/nn n FV 1YTM P ⎛⎫+= ⎪⎝⎭1/1111001YTM YTM 4.70%95.51⎛⎫+=⇒= ⎪⎝⎭1/2111001YTM YTM 4.80%91.05⎛⎫+=⇒= ⎪⎝⎭1/3331001YTM YTM 5.00%86.38⎛⎫+=⇒= ⎪⎝⎭1/4441001YTM YTM 5.20%81.65⎛⎫+=⇒= ⎪⎝⎭ 1/5551001YTM YTM 5.50%76.51⎛⎫+=⇒= ⎪⎝⎭b. The yield curve is as shown below.Zero Coupon Yield Curve4.64.855.25.45.60246Maturity (Years)Y i e l d t o M a t u r i t yc. The yield curve is upward sloping.108 Berk/DeMarzo• Corporate Finance, Second Edition8-4. Suppose the current zero-coupon yield curve for risk-free bonds is as follows:a. What is the price per $100 face value of a two-year, zero-coupon, risk-free bond?b. What is the price per $100 face value of a four-year, zero-coupon, risk-free bond?c. What is the risk-free interest rate for a five-year maturity? a.2P 100(1.055)$89.85==b. 4P 100/(1.0595)$79.36==c. 6.05%8-5.In the box in Section 8.1, reported that the three-month Treasury bill sold for a price of $100.002556 per $100 face value. What is the yield to maturity of this bond, expressed as an EAR?410010.01022%100.002556⎛⎫-=- ⎪⎝⎭8-6.Suppose a 10-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading for a price of $1034.74.a. What is the bond’s yield to maturity (expressed as an APR with semiannual compounding)?b. If the bond’s yield to maturity changes to 9% APR, what will the bond’s price be? a.2204040401000$1,034.747.5%(1)(1)(1)222YTM YTM YTM YTM +=+++⇒=+++Using the annuity spreadsheet: NPER Rate PV PMT FVExcel Formula Given: 20 -1,034.74 40 1,000Solve For Rate: 3.75%=RATE(20,40,-1034.74,1000)Therefore, YTM = 3.75% × 2 = 7.50% b.2204040401000$934.96..09.09.09(1)(1)(1)222PV L +=+++=+++ Using the spreadsheetWith a 9% YTM = 4.5% per 6 months, the new price is $934.96NPER Rate PV PMT FV Excel Formula Given: 20 4.50% 40 1,000 Solve For PV: (934.96) =PV(0.045,20,40,1000)Berk/DeMarzo • Corporate Finance, Second Edition 1098-7.Suppose a five-year, $1000 bond with annual coupons has a price of $900 and a yield to maturity of 6%. What is the bond’s coupon rate?25C CC 1000900C $36.26, so the coupon rate is 3.626%.(1.06)(1.06)(1.06)+=+++⇒=+++We can use the annuity spreadsheet to solve for the payment. NPER Rate PV PMT FV Excel Formula Given: 5 6.00% -900.00 1,000Solve For PMT: 36.26 =PMT(0.06,5,-900,1000)Therefore, the coupon rate is 3.626%.8-8.The prices of several bonds with face values of $1000 are summarized in the following table:For each bond, state whether it trades at a discount, at par, or at a premium. Bond A trades at a discount. Bond D trades at par. Bonds B and C trade at a premium.8-9.Explain why the yield of a bond that trades at a discount exceeds the bond’s coupon rate. Bonds trading at a discount generate a return both from receiving the coupons and from receiving a face value that exceeds the price paid for the bond. As a result, the yield to maturity of discount bonds exceeds the coupon rate.8-10.Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield to maturity of 6.75%.a. Is this bond currently trading at a discount, at par, or at a premium? Explain.b. If the yield to maturity of the bond rises to 7% (APR with semiannual compounding), whatprice will the bond trade for? a. Because the yield to maturity is less than the coupon rate, the bond is trading at a premium. b. 2144040401000$1,054.60(1.035)(1.035)(1.035)++++=+++NPER Rate PV PMT FV Excel Formula Given: 14 3.50% 40 1,000Solve For PV:(1,054.60)=PV(0.035,14,40,1000)8-11.Suppose that General Motors Acceptance Corporation issued a bond with 10 years until maturity, a face value of $1000, and a coupon rate of 7% (annual payments). The yield to maturity on this bond when it was issued was 6%. a. What was the price of this bond when it was issued?b. Assuming the yield to maturity remains constant, what is the price of the bond immediatelybefore it makes its first coupon payment? c. Assuming the yield to maturity remains constant, what is the price of the bond immediatelyafter it makes its first coupon payment?110 Berk/DeMarzo • Corporate Finance, Second Editiona. When it was issued, the price of the bond was1070701000P ...$1073.60.(1.06)(1.06)+=++=++b. Before the first coupon payment, the price of the bond is970701000P 70...$1138.02.(1.06)(1.06)+=++=++c. After the first coupon payment, the price of the bond will be970701000P ...$1068.02.(1.06)(1.06)+=+=++8-12.Suppose you purchase a 10-year bond with 6% annual coupons. You hold the bond for fouryears, and sell it immediately after receiving the fourth coupon. If the bond’s yield to maturity was 5% when you purchased and sold the bond,a. What cash flows will you pay and receive from your investment in the bond per $100 facevalue? b. What is the internal rate of return of your investment?a. First, we compute the initial price of the bond by discounting its 10 annual coupons of $6 and finalface value of $100 at the 5% yield to maturity.NPER Rate PV PMT FV Excel Formula Given:10 5.00%6 100Solve For PV:(107.72)= PV(0.05,10,6,100)Thus, the initial price of the bond = $107.72. (Note that the bond trades above par, as its coupon rate exceeds its yield.)Next we compute the price at which the bond is sold, which is the present value of the bonds cash flows when only 6 years remain until maturity.NPER Rate PV PMT FV Excel Formula Given: 6 5.00%6 100Solve For PV:(105.08)= PV(0.05,6,6,100)Therefore, the bond was sold for a price of $105.08. The cash flows from the investment are therefore as shown in the following timeline.Berk/DeMarzo • Corporate Finance, Second Edition 111b. We can compute the IRR of the investment using the annuity spreadsheet. The PV is the purchaseprice, the PMT is the coupon amount, and the FV is the sale price. The length of the investment N = 4 years. We then calculate the IRR of investment = 5%. Because the YTM was the same at the time of purchase and sale, the IRR of the investment matches the YTM. NPER Rate PV PMT FV Excel Formula Given: 4 –107.72 6 105.08Solve For Rate: 5.00% = RATE(4,6,-107.72,105.08)8-13.Consider the following bonds:a. What is the percentage change in the price of each bond if its yield to maturity falls from 6% to 5%?b. Which of the bonds A –D is most sensitive to a 1% drop in interest rates from 6% to 5% andwhy? Which bond is least sensitive? Provide an intuitive explanation for your answer. a. We can compute the price of each bond at each YTM using Eq. 8.5. For example, with a 6% YTM,the price of bond A per $100 face value is15100P(bond A, 6% YTM)$41.73.1.06== The price of bond D is101011100P(bond D, 6% YTM)81$114.72..06 1.06 1.06⎛⎫=⨯-+= ⎪⎝⎭ One can also use the Excel formula to compute the price: –PV(YTM, NPER, PMT, FV). Once we compute the price of each bond for each YTM, we can compute the % price change as Percent change =()()()Price at 5% YTM Price at 6% YTM .Price at 6% YTM -The results are shown in the table below.Coupon Rate Maturity Price at Price at Percentage Change(annual payments)(years)6% YTM 5% YTM A 0%15$41.73$48.1015.3%B 0%10$55.84$61.399.9%C 4%15$80.58$89.6211.2%D8%10$114.72$123.177.4%Bondb. Bond A is most sensitive, because it has the longest maturity and no coupons. Bond D is the leastsensitive. Intuitively, higher coupon rates and a shorter maturity typically lower a bond’s interest rate sensitivity.112 Berk/DeMarzo • Corporate Finance, Second Edition8-14.Suppose you purchase a 30-year, zero-coupon bond with a yield to maturity of 6%. You hold the bond for five years before selling it.a. If the bond’s yield to maturity is 6% when you sell it, what is the internal rate of return ofyour investment? b. If the bond’s yield to maturity is 7% when you sell it, what is the internal rate of return ofyour investment? c. If the bond’s yield to maturity is 5% when you se ll it, what is the internal rate of return ofyour investment? d. Even if a bond has no chance of default, is your investment risk free if you plan to sell itbefore it matures? Explain. a. Purchase price = 100 / 1.0630 = 17.41. Sale price = 100 / 1.0625 = 23.30. Return = (23.30 / 17.41)1/5– 1 = 6.00%. I.e., since YTM is the same at purchase and sale, IRR = YTM. b. Purchase price = 100 / 1.0630 = 17.41. Sale price = 100 / 1.0725 = 18.42. Return = (18.42 / 17.41)1/5– 1 = 1.13%. I.e., since YTM rises, IRR < initial YTM. c. Purchase price = 100 / 1.0630 = 17.41. Sale price = 100 / 1.0525 = 29.53. Return = (29.53 / 17.41)1/5– 1 = 11.15%. I.e., since YTM falls, IRR > initial YTM. d. Even without default, if you sell prior to maturity, you are exposed to the risk that the YTM maychange.8-15.Suppose you purchase a 30-year Treasury bond with a 5% annual coupon, initially trading at par. In 10 years’ time, the bond’s yield to maturity has risen to 7% (EAR).a. If you sell the bond now, what internal rate of return will you have earned on yourinvestment in the bond? b. If instead you hold the bond to maturity, what internal rate of return will you earn on yourinvestment in the bond? c. Is comparing the IRRs in (a) versus (b) a useful way to evaluate the decision to sell the bond?Explain. a. 3.17% b. 5%c. We can’t simply compare IRRs. By not selling the bond for its current price of $78.81, we willearn the current market return of 7% on that amount going forward.8-16.Suppose the current yield on a one-year, zero coupon bond is 3%, while the yield on a five-year, zero coupon bond is 5%. Neither bond has any risk of default. Suppose you plan to invest for one year. You will earn more over the year by investing in the five-year bond as long as its yield does not rise above what level?The return from investing in the 1 year is the yield. The return for investing in the 5 year for initialprice p 0 and selling after one year at price p1 is 101pp -. We have05151,(1.05)1.(1)p p y ==+Berk/DeMarzo • Corporate Finance, Second Edition 113So you break even when41105545/41/41(1)110.031(1.05)(1.05) 1.03(1)(1.05)1 5.51%.(1.03)p y y p y y +-=-===+=-=For Problems 17–22, assume zero-coupon yields on default-free securities are as summarized in the following table:8-17.What is the price today of a two-year, default-free security with a face value of $1000 and an annual coupon rate of 6%? Does this bond trade at a discount, at par, or at a premium?221260601000...$1032.091(1.04)(1)(1)(1.043)N N CPN CPN CPN FV P YTM YTM YTM ++=+++=+=+++++This bond trades at a premium. The coupon of the bond is greater than each of the zero coupon yields, so the coupon will also be greater than the yield to maturity on this bond. Therefore it trades at a premium8-18.What is the price of a five-year, zero-coupon, default-free security with a face value of $1000? The price of the zero-coupon bond is51000$791.03(1)(10.048)NN FV P YTM ===++ 8-19.What is the price of a three-year, default-free security with a face value of $1000 and an annual coupon rate of 4%? What is the yield to maturity for this bond? The price of the bond is223124040401000...$986.58.1(1.04)(1)(1)(1.043)(1.045)N N CPN CPN CPN FV P YTM YTM YTM ++=+++=++=++++++ The yield to maturity is2...1(1)(1)NCPN CPN CPN FVP YTM YTM YTM +=++++++234040401000$986.58 4.488%(1)(1)(1)YTM YTM YTM YTM +=++⇒=+++8-20.What is the maturity of a default-free security with annual coupon payments and a yield to maturity of 4%? Why?The maturity must be one year. If the maturity were longer than one year, there would be an arbitrage opportunity.114 Berk/DeMarzo • Corporate Finance, Second Edition8-21.Consider a four-year, default-free security with annual coupon payments and a face value of $1000 that is issued at par. What is the coupon rate of this bond? Solve the following equation:2344111110001000(1.04)(1.043)(1.045)(1.047)(1.047)$46.76.CPN CPN ⎛⎫=++++ ⎪+++++⎝⎭=Therefore, the par coupon rate is 4.676%.8-22.Consider a five-year, default-free bond with annual coupons of 5% and a face value of $1000. a. Without doing any calculations, determine whether this bond is trading at a premium or at adiscount. Explain. b. What is the yield to maturity on this bond?c. If the yield to maturity on this bond increased to 5.2%, what would the new price be? a. The bond is trading at a premium because its yield to maturity is a weighted average of the yieldsof the zero coupon bonds. This implied that its yield is below 5%, the coupon rate. b. To compute the yield, first compute the price.2122345...1(1)(1)50505050501000$1010.05(1.04)(1.043)(1.045)(1.047)(1.048)NN CPN CPN CPN FVP YTM YTM YTM +=+++++++=++++=+++++The yield to maturity is:2...1(1)(1)505010001010.05... 4.77%.(1)(1)NN CPN CPN CPN FVP YTM YTM YTM YTM YTM YTM +=+++++++=++⇒=++c. If the yield increased to 5.2%, the new price would be:2...1(1)(1)50501000...$991.39.(1.052)(1.052)NNCPN CPN CPN FV P YTM YTM YTM +=+++++++=++=++8-23.Prices of zero-coupon, default-free securities with face values of $1000 are summarized in thefollowing table:Suppose you observe that a three-year, default-free security with an annual coupon rate of 10% and a face value of $1000 has a price today of $1183.50. Is there an arbitrage opportunity? If so, show specifically how you would take advantage of this opportunity. If not, why not?First, figure out if the price of the coupon bond is consistent with the zero coupon yields implied by the other securities.Berk/DeMarzo • Corporate Finance, Second Edition 115111000970.87 3.0%(1)YTM YTM =→=+ 2221000938.95 3.2%(1)YTM YTM =→=+ 3331000904.56 3.4%(1)YTM YTM =→=+According to these zero coupon yields, the price of the coupon bond should be:231001001001000$1186.00.(1.03)(1.032)(1.034)+++=+++ The price of the coupon bond is too low, so there is an arbitrage opportunity. To take advantage of it:Today1 Year2 Years3 Years Buy 10 Coupon Bonds 11835.00 +1000 +1000 +11,000 Short Sell 1 One-Year Zero +970.87 1000Short Sell 1 Two-Year Zero +938.95 1000Short Sell 11 Three-Year Zeros +9950.16 11,000 Net Cash Flow 24.988-24.Assume there are four default-free bonds with the following prices and future cash flows:Do these bonds present an arbitrage opportunity? If so, how would you take advantage of this opportunity? If not, why not?To determine whether these bonds present an arbitrage opportunity, check whether the pricing is internally consistent. Calculate the spot rates implied by Bonds A, B, and D (the zero coupon bonds), and use this to check Bond C. (You may alternatively compute the spot rates from Bonds A, B, and C, and check Bond D, or some other combination.)111000934.587.0%(1)YTM YTM =⇒=+2221000881.66 6.5%(1)YTM YTM =⇒=+3331000839.62 6.0%(1)YTM YTM =⇒=+Given the spot rates implied by Bonds A, B, and D, the price of Bond C should be $1,105.21. Its price really is $1,118.21, so it is overpriced by $13 per bond. Yes, there is an arbitrage opportunity.To take advantage of this opportunity, you want to (short) Sell Bond C (since it is overpriced). To match future cash flows, one strategy is to sell 10 Bond Cs (it is not the only effective strategy; any multiple of this strategy is also arbitrage). This complete strategy is summarized in the table below.Today 1 Year 2Years 3Years Sell Bond C 11,182.10 –1,000 –1,000–11,000Buy Bond A –934.58 1,0000 0 Buy Bond B –881.66 0 1,0000 Buy 11 Bond D –9,235.82 0 0 11,000Net Cash Flow130.04Notice that your arbitrage profit equals 10 times the mispricing on each bond (subject to rounding error).8-25.Suppose you are given the following information about the default-free, coupon-paying yield curve:a. Use arbitrage to determine the yield to maturity of a two-year, zero-coupon bond.b. What is the zero-coupon yield curve for years 1 through 4?a. We can construct a two-year zero coupon bond using the one and two-year coupon bonds asfollows. Cash Flow in Year: 1 2 3 4 Two-year coupon bond ($1000 Face Value) 100 1,100 Less: One-year bond ($100 Face Value) (100) Two-year zero ($1100 Face Value) - 1,100Now, Price(2-year coupon bond) = 21001100$1115.051.03908 1.03908+=Price(1-year bond) =100$98.04.1.02= By the Law of One Price:Price(2 year zero) = Price(2 year coupon bond) – Price(One-year bond)= 1115.05 – 98.04 = $1017.01Given this price per $1100 face value, the YTM for the 2-year zero is (Eq. 8.3)1/21100(2)1 4.000%.1017.01YTM ⎛⎫=-= ⎪⎝⎭b. We already know YTM(1) = 2%, YTM(2) = 4%. We can construct a 3-year zero as follows:Cash Flow in Year:1 2 3 4Three-year coupon bond ($1000 face value) 60 60 1,060 Less: one-year zero ($60 face value) (60) Less: two-year zero ($60 face value) - (60) Three-year zero ($1060 face value) -- 1,060Now, Price(3-year coupon bond) = 2360601060$1004.29.1.0584 1.0584 1.0584++=By the Law of One Price:Price(3-year zero) = Price(3-year coupon bond) – Price(One-year zero) – Price(Two-year zero) = Price(3-year coupon bond) – PV(coupons in years 1 and 2)= 1004.29 – 60 / 1.02 – 60 / 1.042 = $889.99.Solving for the YTM:1/31060(3)1 6.000%.889.99YTM ⎛⎫=-= ⎪⎝⎭Finally, we can do the same for the 4-year zero:Cash Flow in Year:1 2 3 4Four-year coupon bond ($1000 face value) 120 120 120 1,120 Less: one-year zero ($120 face value) (120) Less: two-year zero ($120 face value) — (120) Less: three-year zero ($120 face value) — — (120) Four-year zero ($1120 face value) —— —1,120Now, Price(4-year coupon bond) = 2341201201201120$1216.50.1.05783 1.05783 1.05783 1.05783+++=By the Law of One Price:Price(4-year zero) = Price(4-year coupon bond) – PV(coupons in years 1–3)= 1216.50 – 120 / 1.02 – 120 / 1.042 – 120 / 1.063 = $887.15. Solving for the YTM:1/41120(4)1 6.000%.887.15YTM ⎛⎫=-= ⎪⎝⎭Thus, we have computed the zero coupon yield curve as shown.8-26.Explain why the expected return of a corporate bond does not equal its yield to maturity. The yield to maturity of a corporate bond is based on the promised payments of the bond. But there is some chance the corporation will default and pay less. Thus, the bond’s expected return is typically less than its YTM.Corporate bonds have credit risk, which is the risk that the borrower will default and not pay all specified payments. As a result, investors pay less for bonds with credit risk than they would for an otherwise identical default-free bond. Because the YTM for a bond is calculated using the promised cash flows, the yields of bonds with credit risk will be higher than that of otherwise identical default-free bonds. However, the YTM of a defaultable bond is always higher than the expected return of investing in the bond because it is calculated using the promised cash flows rather than the expected cash flows.8-27.Grummon Corporation has issued zero-coupon corporate bonds with a five-year maturity. Investors believe there is a 20% chance that Grummon will default on these bonds. If Grummon does default, investors expect to receive only 50 cents per dollar they are owed. If investors require a 6% expected return on their investment in these bonds, what will be the price and yield to maturity on these bonds? Price =5100((1)())67.251.06d d r -+=Yield=1/510018.26%67.25⎛⎫-= ⎪⎝⎭8-28.The following table summarizes the yields to maturity on several one-year, zero-couponsecurities:a. What is the price (expressed as a percentage of the face value) of a one-year, zero-couponcorporate bond with a AAA rating? b. What is the credit spread on AAA-rated corporate bonds? c. What is the credit spread on B-rated corporate bonds? d. How does the credit spread change with the bond rating? Why? a. The price of this bond will be10096.899.1.032P ==+b. The credit spread on AAA-rated corporate bonds is 0.032 – 0.031 = 0.1%.c. The credit spread on B-rated corporate bonds is 0.049 – 0.031 = 1.8%.d. The credit spread increases as the bond rating falls, because lower rated bonds are riskier.8-29.Andrew Industries is contemplating issuing a 30-year bond with a coupon rate of 7% (annual coupon payments) and a face value of $1000. Andrew believes it can get a rating of A from Standard and Poor’s. However, due to recent financial difficulties at the company, Standard and Poor’s is warni ng that it may downgrade Andrew Industries bonds to BBB. Yields on A-rated, long-term bonds are currently 6.5%, and yields on BBB-rated bonds are 6.9%. a. What is the price of the bond if Andrew maintains the A rating for the bond issue? b. What will the price of the bond be if it is downgraded? a. When originally issued, the price of the bonds was3070701000...$1065.29.(10.065)(1.065)P +=++=++b. If the bond is downgraded, its price will fall to3070701000...$1012.53.(10.069)(1.069)P +=++=++8-30.HMK Enterprises would like to raise $10 million to invest in capital expenditures. The companyplans to issue five-year bonds with a face value of $1000 and a coupon rate of 6.5% (annual payments). The following table summarizes the yield to maturity for five-year (annualpay) coupon corporate bonds of various ratings:a. Assuming the bonds will be rated AA, what will the price of the bonds be?b. How much total principal amount of these bonds must HMK issue to raise $10 million today,assuming the bonds are AA rated? (Because HMK cannot issue a fraction of a bond, assume that all fractions are rounded to the nearest whole number.) c. What must the rating of the bonds be for them to sell at par?d. Suppose that when the bonds are issued, the price of each bond is $959.54. What is the likelyrating of the bonds? Are they junk bonds?a. The price will be565651000...$1008.36.(1.063)(1.063)P +=++=++b. Each bond will raise $1008.36, so the firm must issue:$10,000,0009917.139918 bonds.$1008.36=⇒This will correspond to a principle amount of 9918$1000$9,918,000.⨯=c. For the bonds to sell at par, the coupon must equal the yield. Since the coupon is 6.5%, the yieldmust also be 6.5%, or A-rated. d. First, compute the yield on these bonds:565651000959.54...7.5%.(1)(1)YTM YTM YTM +=++⇒=++Given a yield of 7.5%, it is likely these bonds are BB rated. Yes, BB-rated bonds are junk bonds.8-31.A BBB-rated corporate bond has a yield to maturity of 8.2%. A U.S. Treasury security has ayield to maturity of 6.5%. These yields are quoted as APRs with semiannual compounding. Both bonds pay semiannual coupons at a rate of 7% and have five years to maturity.a. What is the price (expressed as a percentage of the face value) of the Treasury bond?b. What is the price (expressed as a percentage of the face value) of the BBB-rated corporatebond? c. What is the credit spread on the BBB bonds? a. 103535 1000...$1,021.06 102.1%(1.0325)(1.0325)P +=++==++b.103535 1000...$951.5895.2%(1.041)(1.041)P +=++==++ c. 0. 178-32.The Isabelle Corporation rents prom dresses in its stores across the southern United States. It has just issued a five-year, zero-coupon corporate bond at a price of $74. You have purchased this bond and intend to hold it until maturity. a. What is the yield to maturity of the bond?b. What is the expected return on your investment (expressed as an EAR) if there is no chanceof default? c. What is the expected return (expressed as an EAR) if there is a 100% probability of defaultand you will recover 90% of the face value? d. What is the expected return (expressed as an EAR) if the probability of default is 50%, thelikelihood of default is higher in bad times than good times, and, in the case of default, you will recover 90% of the face value? e. For parts (b –d), what can you say about the five-year, risk-free interest rate in each case? a.1/51001 6.21%74⎛⎫-= ⎪⎝⎭b. In this case, the expected return equals the yield to maturity.c.1/51000.91 3.99%74⨯⎛⎫-= ⎪⎝⎭d. 1/51000.90.51000.51 5.12%74⨯⨯+⨯⎛⎫-= ⎪⎝⎭e. Risk-free rate is 6.21% in b, 3.99% in c, and less than 5.12% in d.AppendixProblems A.1–A.4 refer to the following table:A.1.What is the forward rate for year 2 (the forward rate quoted today for an investment that beginsin one year and matures in two years)? From Eq 8A.2,22221(1) 1.055117.02%(1) 1.04YTM f YTM +=-=-=+A.2.What is the forward rate for year 3 (the forward rate quoted today for an investment that begins in two years and matures in three years)? What can you conclude about forward rates when the yield curve is flat? From Eq 8A.2,3333222(1) 1.05511 5.50%(1) 1.055YTM f YTM +=-=-=+When the yield curve is flat (spot rates are equal), the forward rate is equal to the spot rate.A.3.What is the forward rate for year 5 (the forward rate quoted today for an investment that begins in four years and matures in five years)? From Eq 8A.2,5555444(1) 1.04511 2.52%(1) 1.050YTM f YTM +=-=-=+When the yield curve is flat (spot rates are equal), the forward rate is equal to the spot rate.A.4.Suppose you wanted to lock in an interest rate for an investment that begins in one year and matures in five years. What rate would you obtain if there are no arbitrage opportunities? Call this rate f 1,5. If we invest for one-year at YTM1, and then for the 4 years from year 1 to 5 at rate f 1,5, after five years we would earn 1YTM 11f 1,54with no risk. No arbitrage means this must equal that amount we would earn investing at the current five year spot rate:(1 + YTM 1)(1 + f 1,5)4 + (1 + YTM 5)5.。

Foundation of Financial ManagementModule syllabusTeacher Name: Zhanwei LiuSchool Name: Xuchang University1. Unit descriptionFinancial management is part of the decision-making, planning and control subsystems of an enterprise. It incorporates the treasury function, which includes the management of working capital and the implications arising from exchange rate mechanisms due to international competition, evaluation, selection, management and control of new capital investment opportunities, raising and management of the long-term financing of an entity.The management of risk in the different aspects of the financial activities undertaken is also addressed. Studying this course should provide you with an overview of the problems facing a financial manager in the commercial world. It will introduce you to the concepts and theories of corporate finance that underlie the techniques that are offered as aids for the understanding, evaluation and resolution of financial ma nagers’ problems. This subject guide is written to supplement the Essential and Further reading listed for this course, not to replace them. It makes no assumptions about prior knowledge other than that you have completed Principles of accounting.The aim of the course is to provide an understanding and awareness of both the underlying concepts and practical application of the basics of financial management. The subject guide and the readings should also help to build in your mind the ability to make critical judgments of the strengths and weaknesses of the theories, just as it should be helping to build a critical appreciation of the uses and limitations of the same theories and their possible applications.On successful completion of the module, learners will be able to:●describe how different financial markets function and estimate thevalue of different financial instruments (including stocksand bonds)●make capital budgeting decisions under both certainty and uncertainty●apply the capital assets pricing model in practical scenarios●discuss the capital structure theory and dividend policy of a firm●estimate the value of derivatives and advise management how to usederivatives in risk management and capital budgeting●describe and assess how companies manage working capital andshort- term financing2. Pre-requisite units and assumed knowledgeAccounting, Economics3. Learning aims and outcomesLearning Outcome 1Explain the method of financial analysis and planningASSESSMENT CRITERIA:a. Explain the goals and objectives of financial managementb. Demonstrate a reasonable ability to prepare the three basic financialstatementsc. Discuss the method of financial analysisd. Explain the operating leverage, financial leverage. and combinedleverageLearning Outcome 2Explain the manager how to manage working capitalASSESSMENT CRITERIA:a. Explain the context of risk-return analysisb. Explain the financial manager how to choose between liquid,low-return assets and more profitable, less liquid assets Learning Outcome 3Explain the process of the capital budgetingASSESSMENT CRITERIA:a. Discuss the time value of moneyb. Explain the valuation of bonds and stocksc. Explain the cost of capital and capital structured. Explain the capital budgeting decision and risk-return analysisLearning Outcome 4Explain the long-term financing in the capital marketsASSESSMENT CRITERIA:a. Explain the long-term debt and lease financingb. Explain the common stock and preferred stock financingc. Explain the dividend policy and retained earningsd. Explain the warrants and convertibles covered, as well as the moreconventional methods of financing4. Weighting of final gradeGrades will be assigned on the basis of the following percentages:5. GradingA 100-95 A- 94-90 B+ 89-87B 86-83 B- 82-80 C+ 79-77C 76-73 C- 72-70 D+ 69-67D 66-63 D- 62-60 F 59 or lower6. PoliciesAttendance PolicyAttendance in class is a very important part of your learning experience. As such, failure to attend class will reduce your grade, and may be grounds for failure in the course. If you are late to class, your attendance score may also be affected. In the event of unavoidable absences, such as serious illness, or deaths in the family, students may be requested to provide documentary evidence of the reason for their absence to their academic coordinator. You should not give these to your instructor. Students are solely responsible for the makeup of any missed classes, and for obtaining any class materials or assignments that they may miss. You are expected to come to class prepared to actively participate in class discussions.Participation PolicyStudents should participate in their chosen classes actively and effectively. The Participation Grade is related to the Attendance Grade. Students’ final attendance grade is the maximum of their participation grade.Participation grade will be based on a variety of factors including, but not limited to taking part in class discussions and activities, completingassignments, being able to answer questions correctly, obeying class rules, and being prepared for class, frequent visiting your instructors and chatting in English during their office hours is highly recommended.Policy on Assignments and QuizzesStudents should finish their assignments completely and punctually. Assignment should be submitted on the date appointed by the instructor. If a student cannot hand in the assignment on time, the reasonable excuse will be needed. Late assignments will receive a maximum grade of 80. An assignment that is late for 3 days will be corrected but receive 0.You are recommended print all your assignment in the uniform format with the heading o f Student’s Pledge of no cheating. Written assignment or printed ones without the uniform heading of pledge will receive a maximum grade of 80.It is mandatory to have weekend assignment every week. Any weekend assignment should be submitted on first class of next week. It is mandatory to have holiday assignment on the public holidays. Any holiday assignment should be submitted on the first day on returning to school. Students are required to do a multitude of presentations during the course.Plagiarism and CopyingPlagiarism is using someone else’s work or ideas as your own without giving them proper credit or copying someone else’s work a nd presenting it as your own.There has a very strict plagiarism policy and will not tolerate academic cheating in any form. Penalties can be as severe as expulsion from the university. At the very least, no one will receive any credit for assignments that appear to be copied from another student. To avoid plagiarism, do your own work, or cite the work of others appropriately. You can refer to the course catalogue for more information about plagiarism policy.If you cheat on the homework, I can guarantee you that you will fail the class. Every exam I give has several problems that require you to submit journal entries, create financial statements in proper form, or to create schedulesshowing certain details that you have to calculate. If you do not practice doing these things by doing the homework yourself and correcting your own work in class, you will lose a significant number of points on the exams.Classroom Policies●No eating, cellular phones, electronic dictionaries, smoking, chatting ordrowsing in class.●Please speak in English rather than Chinese in class.●Students are not allowed to attend class without textbooks.●Stand up when answering questions.●Respect classmates’ ideas, opinions, and questions of your classmates.●You are welcome to visit the instructor’s office in his/her office hours.●Take good care of the laboratory facilities. Do not splash water on thedesktop.●When each class is over, hang the earphone on the hanger. Put the trashinto the trash-bin.●All your classroom involvement, performance and after-classcommunications with instructor will affect your participation score.7. Texts and other recoursesThe primary textbook:Stanley B.Block. Foundation of financial management, 14th ed.The supplementary textbook:Richard A. Barealey et al(2011) fundamentals of corporate finance(6th ed.).Renmin university of China pressWEB SITES:Teaching methodsDiscussions and Homework8. Session Plan。

罗斯《公司理财》第9版精要版英文原书课后部分章节答案详细»1 / 17 CH5 11,13,18,19,20 11. To find the PV of a lump sum, we use: PV = FV / (1 + r) t PV = $1,000,000 / (1.10) 80 = $488.19 13. To answer this question, we can use either the FV or the PV formula. Both will give the same answer since they are the inverse of each other. We will use the FV formula, that is: FV = PV(1 + r) t Solving for r, we get: r = (FV / PV) 1 / t –1 r = ($1,260,000 / $150) 1/112 – 1 = .0840 or 8.40% To find the FV of the first prize, we use: FV = PV(1 + r) t FV = $1,260,000(1.0840) 33 = $18,056,409.94 18. To find the FV of a lump sum, we use: FV = PV(1 + r) t FV = $4,000(1.11) 45 = $438,120.97 FV = $4,000(1.11) 35 = $154,299.40 Better start early! 19. We need to find the FV of a lump sum. However, the money will only be invested for six years, so the number of periods is six. FV = PV(1 + r) t FV = $20,000(1.084)6 = $32,449.33 20. To answer this question, we can use either the FV or the PV formula. Both will give the same answer since they are the inverse of each other. We will use the FV formula, that is: FV = PV(1 + r) t Solving for t, we get: t = ln(FV / PV) / ln(1 + r) t = ln($75,000 / $10,000) / ln(1.11) = 19.31 So, the money must be invested for 19.31 years. However, you will not receive the money for another two years. From now, you’ll wait: 2 years + 19.31 years = 21.31 years CH6 16,24,27,42,58 16. For this problem, we simply need to find the FV of a lump sum using the equation: FV = PV(1 + r) t 2 / 17 It is important to note that compounding occurs semiannually. To account for this, we will divide the interest rate by two (the number of compounding periods in a year), and multiply the number of periods by two. Doing so, we get: FV = $2,100[1 + (.084/2)] 34 = $8,505.93 24. This problem requires us to find the FV A. The equation to find the FV A is: FV A = C{[(1 + r) t – 1] / r} FV A = $300[{[1 + (.10/12) ] 360 – 1} / (.10/12)] = $678,146.38 27. The cash flows are annual and the compounding period is quarterly, so we need to calculate the EAR to make the interest rate comparable with the timing of the cash flows. Using the equation for the EAR, we get: EAR = [1 + (APR / m)] m – 1 EAR = [1 + (.11/4)] 4 – 1 = .1146 or 11.46% And now we use the EAR to find the PV of each cash flow as a lump sum and add them together: PV = $725 / 1.1146 + $980 / 1.1146 2 + $1,360 / 1.1146 4 = $2,320.36 42. The amount of principal paid on the loan is the PV of the monthly payments you make. So, the present value of the $1,150 monthly payments is: PV A = $1,150[(1 – {1 / [1 + (.0635/12)]} 360 ) / (.0635/12)] = $184,817.42 The monthly payments of $1,150 will amount to a principal payment of $184,817.42. The amount of principal you will still owe is: $240,000 – 184,817.42 = $55,182.58 This remaining principal amount will increase at the interest rate on the loan until the end of the loan period. So the balloon payment in 30 years, which is the FV of the remaining principal will be: Balloon payment = $55,182.58[1 + (.0635/12)] 360 = $368,936.54 58. To answer this question, we should find the PV of both options, and compare them. Since we are purchasing the car, the lowest PV is the best option. The PV of the leasing is simply the PV of the lease payments, plus the $99. The interest rate we would use for the leasing option is the same as the interest rate of the loan. The PV of leasing is: PV = $99 + $450{1 –[1 / (1 + .07/12) 12(3) ]} / (.07/12) = $14,672.91 The PV of purchasing the car is the current price of the car minus the PV of the resale price. The PV of the resale price is: PV = $23,000 / [1 + (.07/12)] 12(3) = $18,654.82 The PV of the decision to purchase is: $32,000 – 18,654.82 = $13,345.18 3 / 17 In this case, it is cheaper to buy the car than leasing it since the PV of the purchase cash flows is lower. To find the breakeven resale price, we need to find the resale price that makes the PV of the two options the same. In other words, the PV of the decision to buy should be: $32,000 – PV of resale price = $14,672.91 PV of resale price = $17,327.09 The resale price that would make the PV of the lease versus buy decision is the FV ofthis value, so: Breakeven resale price = $17,327.09[1 + (.07/12)] 12(3) = $21,363.01 CH7 3,18,21,22,31 3. The price of any bond is the PV of the interest payment, plus the PV of the par value. Notice this problem assumes an annual coupon. The price of the bond will be: P = $75({1 – [1/(1 + .0875)] 10 } / .0875) + $1,000[1 / (1 + .0875) 10 ] = $918.89 We would like to introduce shorthand notation here. Rather than write (or type, as the case may be) the entire equation for the PV of a lump sum, or the PV A equation, it is common to abbreviate the equations as: PVIF R,t = 1 / (1 + r) t which stands for Present V alue Interest Factor PVIFA R,t = ({1 – [1/(1 + r)] t } / r ) which stands for Present V alue Interest Factor of an Annuity These abbreviations are short hand notation for the equations in which the interest rate and the number of periods are substituted into the equation and solved. We will use this shorthand notation in remainder of the solutions key. 18. The bond price equation for this bond is: P 0 = $1,068 = $46(PVIFA R%,18 ) + $1,000(PVIF R%,18 ) Using a spreadsheet, financial calculator, or trial and error we find: R = 4.06% This is thesemiannual interest rate, so the YTM is: YTM = 2 4.06% = 8.12% The current yield is:Current yield = Annual coupon payment / Price = $92 / $1,068 = .0861 or 8.61% The effective annual yield is the same as the EAR, so using the EAR equation from the previous chapter: Effective annual yield = (1 + 0.0406) 2 – 1 = .0829 or 8.29% 20. Accrued interest is the coupon payment for the period times the fraction of the period that has passed since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six months is one-half of the annual coupon payment. There are four months until the next coupon payment, so two months have passed since the last coupon payment. The accrued interest for the bond is: Accrued interest = $74/2 × 2/6 = $12.33 And we calculate the clean price as: 4 / 17 Clean price = Dirty price –Accrued interest = $968 –12.33 = $955.67 21. Accrued interest is the coupon payment for the period times the fraction of the period that has passed since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six months is one-half of the annual coupon payment. There are two months until the next coupon payment, so four months have passed since the last coupon payment. The accrued interest for the bond is: Accrued interest = $68/2 × 4/6 = $22.67 And we calculate the dirty price as: Dirty price = Clean price + Accrued interest = $1,073 + 22.67 = $1,095.67 22. To find the number of years to maturity for the bond, we need to find the price of the bond. Since we already have the coupon rate, we can use the bond price equation, and solve for the number of years to maturity. We are given the current yield of the bond, so we can calculate the price as: Current yield = .0755 = $80/P 0 P 0 = $80/.0755 = $1,059.60 Now that we have the price of the bond, the bond price equation is: P = $1,059.60 = $80[(1 – (1/1.072) t ) / .072 ] + $1,000/1.072 t We can solve this equation for t as follows: $1,059.60(1.072) t = $1,111.11(1.072) t –1,111.11 + 1,000 111.11 = 51.51(1.072) t2.1570 = 1.072 t t = log 2.1570 / log 1.072 = 11.06 11 years The bond has 11 years to maturity.31. The price of any bond (or financial instrument) is the PV of the future cash flows. Even though Bond M makes different coupons payments, to find the price of the bond, we just find the PV of the cash flows. The PV of the cash flows for Bond M is: P M = $1,100(PVIFA 3.5%,16 )(PVIF 3.5%,12 ) + $1,400(PVIFA3.5%,12 )(PVIF 3.5%,28 ) + $20,000(PVIF 3.5%,40 ) P M = $19,018.78 Notice that for the coupon payments of $1,400, we found the PV A for the coupon payments, and then discounted the lump sum back to today. Bond N is a zero coupon bond with a $20,000 par value, therefore, the price of the bond is the PV of the par, or: P N = $20,000(PVIF3.5%,40 ) = $5,051.45 CH8 4,18,20,22,244. Using the constant growth model, we find the price of the stock today is: P 0 = D 1 / (R – g) = $3.04 / (.11 – .038) = $42.22 5 / 17 18. The price of a share of preferred stock is the dividend payment divided by the required return. We know the dividend payment in Year 20, so we can find the price of the stock in Y ear 19, one year before the first dividend payment. Doing so, we get: P 19 = $20.00 / .064 P 19 = $312.50 The price of the stock today is the PV of the stock price in the future, so the price today will be: P 0 = $312.50 / (1.064) 19 P 0 = $96.15 20. We can use the two-stage dividend growth model for this problem, which is: P 0 = [D 0 (1 + g 1 )/(R – g 1 )]{1 – [(1 + g 1 )/(1 + R)] T }+ [(1 + g 1 )/(1 + R)] T [D 0 (1 + g 2 )/(R –g 2 )] P0 = [$1.25(1.28)/(.13 –.28)][1 –(1.28/1.13) 8 ] + [(1.28)/(1.13)] 8 [$1.25(1.06)/(.13 – .06)] P 0 = $69.55 22. We are asked to find the dividend yield and capital gains yield for each of the stocks. All of the stocks have a 15 percent required return, which is the sum of the dividend yield and the capital gains yield. To find the components of the total return, we need to find the stock price for each stock. Using this stock price and the dividend, we can calculate the dividend yield. The capital gains yield for the stock will be the total return (required return) minus the dividend yield. W: P 0 = D 0 (1 + g) / (R – g) = $4.50(1.10)/(.19 – .10) = $55.00 Dividend yield = D 1 /P 0 = $4.50(1.10)/$55.00 = .09 or 9% Capital gains yield = .19 – .09 = .10 or 10% X: P 0 = D 0 (1 + g) / (R – g) = $4.50/(.19 – 0) = $23.68 Dividend yield = D 1 /P 0 = $4.50/$23.68 = .19 or 19% Capital gains yield = .19 – .19 = 0% Y: P 0 = D 0 (1 + g) / (R – g) = $4.50(1 – .05)/(.19 + .05) = $17.81 Dividend yield = D 1 /P 0 = $4.50(0.95)/$17.81 = .24 or 24% Capital gains yield = .19 – .24 = –.05 or –5% Z: P 2 = D 2 (1 + g) / (R – g) = D 0 (1 + g 1 ) 2 (1 +g 2 )/(R – g 2 ) = $4.50(1.20) 2 (1.12)/(.19 – .12) = $103.68 P 0 = $4.50 (1.20) / (1.19) + $4.50(1.20) 2 / (1.19) 2 + $103.68 / (1.19) 2 = $82.33 Dividend yield = D 1 /P 0 = $4.50(1.20)/$82.33 = .066 or 6.6% Capital gains yield = .19 – .066 = .124 or 12.4% In all cases, the required return is 19%, but the return is distributed differently between current income and capital gains. High growth stocks have an appreciable capital gains component but a relatively small current income yield; conversely, mature, negative-growth stocks provide a high current income but also price depreciation over time. 24. Here we have a stock with supernormal growth, but the dividend growth changes every year for the first four years. We can find the price of the stock in Y ear 3 since the dividend growth rate is constant after the third dividend. The price of the stock in Y ear 3 will be the dividend in Y ear 4, divided by the required return minus the constant dividend growth rate. So, the price in Y ear 3 will be: 6 / 17 P3 = $2.45(1.20)(1.15)(1.10)(1.05) / (.11 – .05) = $65.08 The price of the stock today will be the PV of the first three dividends, plus the PV of the stock price in Y ear 3, so: P 0 = $2.45(1.20)/(1.11) + $2.45(1.20)(1.15)/1.11 2 + $2.45(1.20)(1.15)(1.10)/1.11 3 + $65.08/1.11 3 P 0 = $55.70 CH9 3,4,6,9,15 3. Project A has cash flows of $19,000 in Y ear 1, so the cash flows are short by $21,000 of recapturing the initial investment, so the payback for Project A is: Payback = 1 + ($21,000 / $25,000) = 1.84 years Project B has cash flows of: Cash flows = $14,000 + 17,000 + 24,000 = $55,000 during this first three years. The cash flows are still short by $5,000 of recapturing the initial investment, so the payback for Project B is: B: Payback = 3 + ($5,000 / $270,000) = 3.019 years Using the payback criterion and a cutoff of 3 years, accept project A and reject project B. 4. When we use discounted payback, we need to find the value of all cash flows today. The value today of the project cash flows for the first four years is: V alue today of Y ear 1 cash flow = $4,200/1.14 = $3,684.21 V alue today of Y ear 2 cash flow = $5,300/1.14 2 = $4,078.18 V alue today of Y ear 3 cash flow = $6,100/1.14 3 = $4,117.33 V alue today of Y ear 4 cash flow = $7,400/1.14 4 = $4,381.39 To findthe discounted payback, we use these values to find the payback period. The discounted first year cash flow is $3,684.21, so the discounted payback for a $7,000 initial cost is: Discounted payback = 1 + ($7,000 – 3,684.21)/$4,078.18 = 1.81 years For an initial cost of $10,000, the discounted payback is: Discounted payback = 2 + ($10,000 –3,684.21 –4,078.18)/$4,117.33 = 2.54 years Notice the calculation of discounted payback. We know the payback period is between two and three years, so we subtract the discounted values of the Y ear 1 and Y ear 2 cash flows from the initial cost. This is the numerator, which is the discounted amount we still need to make to recover our initial investment. We divide this amount by the discounted amount we will earn in Y ear 3 to get the fractional portion of the discounted payback. If the initial cost is $13,000, the discounted payback is: Discounted payback = 3 + ($13,000 – 3,684.21 – 4,078.18 – 4,117.33) / $4,381.39 = 3.26 years 7 / 17 6. Our definition of AAR is the average net income divided by the average book value. The average net income for this project is: A verage net income = ($1,938,200 + 2,201,600 + 1,876,000 + 1,329,500) / 4 = $1,836,325 And the average book value is: A verage book value = ($15,000,000 + 0) / 2 = $7,500,000 So, the AAR for this project is: AAR = A verage net income / A verage book value = $1,836,325 / $7,500,000 = .2448 or 24.48% 9. The NPV of a project is the PV of the outflows minus the PV of the inflows. Since the cash inflows are an annuity, the equation for the NPV of this project at an 8 percent required return is: NPV = –$138,000 + $28,500(PVIFA 8%, 9 ) = $40,036.31 At an 8 percent required return, the NPV is positive, so we would accept the project. The equation for the NPV of the project at a 20 percent required return is: NPV = –$138,000 + $28,500(PVIFA 20%, 9 ) = –$23,117.45 At a 20 percent required return, the NPV is negative, so we would reject the project. We would be indifferent to the project if the required return was equal to the IRR of the project, since at that required return the NPV is zero. The IRR of the project is: 0 = –$138,000 + $28,500(PVIFA IRR, 9 ) IRR = 14.59% 15. The profitability index is defined as the PV of the cash inflows divided by the PV of the cash outflows. The equation for the profitability index at a required return of 10 percent is: PI = [$7,300/1.1 + $6,900/1.1 2 + $5,700/1.1 3 ] / $14,000 = 1.187 The equation for the profitability index at a required return of 15 percent is: PI = [$7,300/1.15 + $6,900/1.15 2 + $5,700/1.15 3 ] / $14,000 = 1.094 The equation for the profitability index at a required return of 22 percent is: PI = [$7,300/1.22 + $6,900/1.22 2 + $5,700/1.22 3 ] / $14,000 = 0.983 8 / 17 We would accept the project if the required return were 10 percent or 15 percent since the PI is greater than one. We would reject the project if the required return were 22 percent since the PI。