Fundamentals of Cost Accounting 4th Solution Manual 习题解答Chap018

- 格式:docx

- 大小:112.27 KB

- 文档页数:21

高级语言程序设计Advanced Language Programme Design工程造价管理Project Pricing Management工业行业技术评估概论Introduction to Industrial Technical Evaluation 公共关系Public Relations公关礼仪Etiquette for Public Relations管理沟通Managerial Communication国际关系与政治International Relationship and Politics国际技术贸易International Technology Trade机械制图Mechanical Drawing计算机科学Computer Science技术创新Technological Innovation技术经济Technological Economics价格学Pricing建筑项目预算Constructive Project Budgeting金融管理软件Financial Management Software经济文献检索Economic Document Searching经济文写作Economic Article Writing经贸科研论文与写作Research Project on Economics & Trade伦理学Ethics逻辑学Logic社会保障Social Security社会调查Social Survey社会学Sociology世界经济概论Introduction to World Economy世界经贸地理World Geography for Economics and Trade世界市场行情World Market Survey世界政治经济与国际关系World Politics, Economy and International Relations 数据结构Database Structure数据库管理Database Management数据库及其应用Database and Applications数据模型与决策Digital Models and Decision-making外国经济地理Economic Geography of Foreign Countries外国经济史History of Foreign Economies外贸函电Business Correspondence for Foreign Trade外贸口语Oral English for Foreign Trade外贸实务Foreign Trade Practices物流运输计划管理Logistics Planning & management系统工程System Engineering现代国际政治与经济Contemporary International Politics and Economics信息分析Information Analysis信息技术与新组织Information Technology and New Organisations形式逻辑Formal Logic英语经贸文章选读Selected English Readings of Economic and Trade Literature营销管理Marketing Management营运管理Operation Management运筹学Operations Research战略管理Strategic Management职业道德伦理Professional Ethics中国对外经贸政策与投资环境Chinese Foreign Trade Policy and Investment Environment中国对外贸易史History of Chinese Foreign Trade中国外贸概论Introduction to Chinese Foreign Trade资刊选读Selected Reading from Foreign Magazines组织行为学Organisational Behaviour大学课程英文名称(做英文成绩单有用)Advanced Computational Fluid Dynamics 高等计算流体力学Advanced Mathematics 高等数学Advanced Numerical Analysis 高等数值分析Algorithmic Language 算法语言Analogical Electronics 模拟电子电路Artificial Intelligence Programming 人工智能程序设计Audit 审计学Automatic Control System 自动控制系统Automatic Control Theory 自动控制理论Auto-Measurement Technique 自动检测技术Basis of Software Technique 软件技术基础Calculus 微积分Catalysis Principles 催化原理Chemical Engineering Document Retrieval 化工文献检索Circuitry 电子线路College English 大学英语College English Test (Band 4) CET-4College English Test (Band 6) CET-6College Physics 大学物理Communication Fundamentals 通信原理Comparative Economics 比较经济学Complex Analysis 复变函数论Computational Method 计算方法Computer Graphics 图形学原理Computer Interface Technology 计算机接口技术Contract Law 合同法Cost Accounting 成本会计Circuit Measurement Technology 电路测试技术Database Principles 数据库原理Design & Analysis System 系统分析与设计Developmental Economics 发展经济学Digital Electronics 数字电子电路Digital Image Processing 数字图像处理Digital Signal Processing 数字信号处理Econometrics 经济计量学Economical Efficiency Analysis for Chemical Technology 化工技术经济分析Economy of Capitalism 资本主义经济Electromagnetic Fields & Magnetic Waves 电磁场与电磁波Electrical Engineering Practice 电工实习Enterprise Accounting 企业会计学Equations of Mathematical Physics 数理方程Experiment of College Physics 物理实验Experiment of Microcomputer 微机实验Experiment in Electronic Circuitry 电子线路实验Fiber Optical Communication System 光纤通讯系统Finance 财政学Financial Accounting 财务会计Fine Arts 美术Functions of a Complex Variable 单复变函数Functions of Complex Variables 复变函数Functions of Complex Variables & Integral Transformations 复变函数与积分变换Fundamentals of Law 法律基础Fuzzy Mathematics 模糊数学General Physics 普通物理Graduation Project(Thesis) 毕业设计(论文)Graph theory 图论Heat Transfer Theory 传热学History of Chinese Revolution 中国革命史Industrial Economics 工业经济学Information Searches 情报检索Integral Transformation 积分变换Intelligent robot(s); Intelligence robot 智能机器人International Business Administration 国际企业管理International Clearance 国际结算International Finance 国际金融International Relation 国际关系International Trade 国际贸易Introduction to Chinese Tradition 中国传统文化Introduction to Modern Science & Technology 当代科技概论Introduction to Reliability Technology 可靠性技术导论Java Language Programming Java 程序设计Lab of General Physics 普通物理实验Linear Algebra 线性代数Management Accounting 管理会计学Management Information System 管理信息系统Mechanic Design 机械设计Mechanical Graphing 机械制图Merchandise Advertisement 商品广告学Metalworking Practice 金工实习Microcomputer Control Technology 微机控制技术Microeconomics & Macroeconomics 西方经济学Microwave Technique 微波技术Military Theory 军事理论Modern Communication System 现代通信系统Modern Enterprise System 现代企业制度Monetary Banking 货币银行学Motor Elements and Power Supply 电机电器与供电Moving Communication 移动通讯Music 音乐Network Technology 网络技术Numeric Calculation 数值计算Oil Application and Addition Agent 油品应用及添加剂Operation & Control of National Economy 国民经济运行与调控Operational Research 运筹学Optimum Control 最优控制Petroleum Chemistry 石油化学Petroleum Engineering Technique 石油化工工艺学Philosophy 哲学Physical Education 体育Political Economics 政治经济学Primary Circuit (反应堆)一回路Principle of Communication 通讯原理Principle of Marxism 马克思主义原理Principle of Mechanics 机械原理Principle of Microcomputer 微机原理Principle of Sensing Device 传感器原理Principle of Single Chip Computer 单片机原理Principles of Management 管理学原理Probability Theory & Stochastic Process 概率论与随机过程Procedure Control 过程控制Programming with Pascal Language Pascal语言编程Programming with C Language C语言编程Property Evaluation 工业资产评估Public Relation 公共关系学Pulse & Numerical Circuitry 脉冲与数字电路Refinery Heat Transfer Equipment 炼厂传热设备Satellite Communications 卫星通信Semiconductor Converting Technology 半导体变流技术Set Theory 集合论Signal & Linear System 信号与线性系统Social Research 社会调查SPC Exchange Fundamentals 程控交换原理Specialty English 专业英语Statistics 统计学Stock Investment 证券投资学Strategic Management for Industrial Enterprises 工业企业战略管理Technological Economics 技术经济学Television Operation 电视原理Theory of Circuitry 电路理论Turbulent Flow Simulation and Application 湍流模拟及其应用Visual C++ Programming Visual C++程序设计Windows NT Operating System Principles Windows NT操作系统原理Word Processing 数据处理姓名NAME性别SEX入学时间1ST TERM ENROLLED IN系别DEPARTMENT专业SPECIALITY毕业时间GRADUATION DA TE19XX-19YY学年度第一/二学期1st/2nd TERM. 19XX-19YY课程名称COURSE TITLE学分CREDIT成绩GRADE高等数学Advanced Mathematics工程数学Engineering Mathematics中国革命史History of Chinese Revolutionary程序设计Programming Design机械制图Mechanical Drawing社会学Sociology体育Physical Education物理实验Physical Experiments电路Circuit物理Physics哲学Philosophy法律基础Basis of Law理论力学Theoretical Mechanics材料力学Material Mechanics电机学Electrical Machinery政治经济学Political Economy自动控制理论Automatic Control Theory模拟电子技术基础Basis of Analogue Electronic Technique 数字电子技术Digital Electrical Technique电磁场Electromagnetic Field微机原理Principle of Microcomputer企业管理Business Management专业英语Specialized English可编程序控制技术Controlling Technique for Programming 金工实习Metal Working Practice毕业实习Graduation Practice。

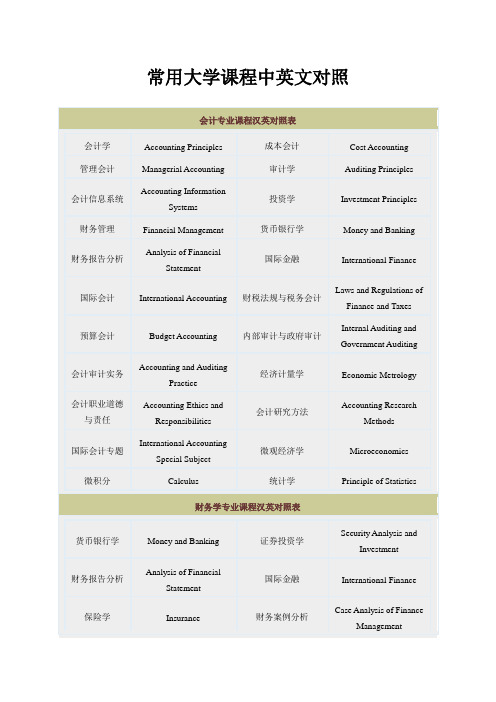

常用大学课程中英文对照大学课程中英文对照大汇集英文字母开头的课程ALGOL语言ALGOL LanguageBASIC & FORTRAN 语言BASIC Language & FORTRAN LanguageBASIC 语言BASIC LanguageBASIC 语言及应用BASIC Language & ApplicationC 语言C LanguageC++程序设计C++ Program DesigningCAD 概论Introduction to CADCAD/CAM CAD/CAMCET-4 College English Test (Band 4)CET-6 College English Test (Band 6)COBOL语言COBOL LanguageCOBOL语言程序设计COBOL Language Program DesigningC与UNIX环境C Language & Unix EnvironmentC语言科学计算方法Scientific Computation Method in CC语言与生物医学信息处理C Language & Biomedical Information Processing dBASE Ⅲ课程设计Course Exercise in dBASE ⅢFORTRAN 77 语言FORTRAN 77 LanguageFORTRAN语言FORTRAN LanguageFoxBase程序设计FoxBase ProgrammingHopf代数Hopf AlgebraHopf代数与代数群量子群Hopf Algebra , Algebraic Group and Qua ntum Group IBM-PC/XT Fundamentals of Microcomputer IBM-PC/XTIBM-PC微机原理Fundamentals of Microcomputer IBM-PCIBM汇编及高级语言的接口IBM Assembly & its Interfaces with Advanced Programming Languages Internet与Intranet技术Internet and Intranet TechnologyLSI设计基础Basic of LSI DesigningOS/2操作系统OS/2 Operation SystemPASCAL大型作业PASCAL Wide Range WorkingPASCAL课程设计Course Exercise in PASCALPASCAL语言PASCAL LanguagePC机原理Principle of PCUnix编程环境Unix Programming EnvironmentUnix操作系统分析Analysis of Unix SystemVLSI的EDA技术EDA Techniques for VLSIVLSI技术与检测方法VLSI Techniques & Its ExaminationVLSI设计基础Basis of VLSI DesignWindows系统Windows Operation SystemX光分析X-ray AnalysisX射线金属学X-Ray & MetallographyX射线与电镜X-ray & Electric MicroscopeZ-80汇编语言程序设计Z-80 Pragramming in Assembly LanguagesB开头的课程板壳非线性力学Nonlinear Mechanics of Plate and Shell板壳理论Plate Theory , Theory of Plate and Shell板壳力学Plate Mechanics办公自动化Office Automatization办公自动化系统毕业设计Office Automatization Thesis办公自动化系统设计Office Automatization Design半波实验Semiwave Experiment半导体变流技术Semiconductor Converting Technology半导体材料Semiconductor Materials半导体测量Measurement of Semiconductors半导体瓷敏元件Semiconductor Porcelain-Sensitive Elements半导体光电子学Semiconductor Optic Electronics半导体化学Semiconductor Chemistry半导体激光器Semiconductor Laser Unit半导体集成电路Semiconductor Integrated Circuitry半导体理论Semi-conductive Theory半导体器件Semiconductor Devices半导体器件工艺原理Technological Fundamentals of Semiconductor Device半导体器件课程设计Course Design of Semiconductor Devices半导体物理Semiconductor Physics半导体专业Semi-conduction Specialty半导体专业实验Specialty Experiment of Semiconductor半群理论Semi-group Theory保健食品监督评价Evaluation and Supervision on Health Food s保险学Insurance保险学Insurance报告文学专题Special Subject On Reportage报刊编辑学Newspaper & Magazine Editing报刊选读Selected Readings of Newspaper & Magazine报纸编辑学Newspaper Editing泵与风机Pumps and Fans泵与水机Pumps & Water Turbines毕业论文Graduation Thesis毕业设计Graduation Thesis毕业实习Graduation Practice编译方法Compilation Method编译方法Methods of Compiling编译技术Technique of Compiling编译原理Fundamentals of Compiling, Principles of Compiler编译原理课程设计Course Design of Compiling变电站的微机检测Computer Testing in Transformer Substation变电站的微机检测与控制Computer Testing & Control in Transformer Substation变分法与张量Calculus of Variations & Tensor变分学Calculus of Variations变流技术Semiconductor Converting Technology变质量系统热力学与新型回转压Variable Quality System Thermal Mechanics & NeoRo 表面活性剂化学及应用Chemistry and Application of Surfactant表面活性物质Surface Reactive Materials并行处理Parallel Processing并行处理与并行程序设计Parallel Processing and Parallel Programming并行算法Parallel Algorithmic波谱学Spectroscopy, Wave Spectrum波谱学实验Spectroscopic Experiment薄膜光学Film Optics薄膜物理Thin Film Physics不育症的病因学Etiology of InfertilityC开头的课程材料的力学性能测试Measurement of Material Mechanical Performance材料化学Material Chemistry材料力学Mechanics of Materials财税法规与税务会计Laws and Regulations of Finance and Taxes财务案例分析Case Analysis of Finance Management财务案例分析Case Analysis of Financial Management财务报告分析Analysis of Financial Statement财务成本管理Financial Cost Management财务管理Financial Management, Financial Cost Management财务管理与分析Financial Management and Analysis财务会计Financial Accountancy财政学Public Finance财政与金融Finance & Banking财政与税收Finance & Revenue财政与税收理论Theories on Public Finance and Tax Revenue财政与信贷Finance & Credit操作系统Disk Operating System (DOS)操作系统课程设计Course Design in Disk Operating System操作系统与编译原理Disk Operating System & Fundamentals of Compiling操作系统原理Fundamentals of Disk Operating System, Principles of Operating System 测量技术基础Foundation of Measurement Technology测量原理与仪器设计Measurement Fundamentals & Meter Design测试技术Testing Technology测试与信号变换处理Testing & Signal Transformation Processing策波测量技术Technique of Whip Wave Measurement策略管理Strategic Management产品学Production产业经济学Industrial Economy产业组织Industrial Organization产业组织学Industrial Organization Technology常微分方程Ordinary Differential Equations场论Field Theory超导磁体及应用Superconductive Magnet & Application超导及应用Superconductive & Application超高真空科学与技术Science and Technology of Ultrahigh Vacuum 60超精密加工和微细加工Super-Precision & Minuteness Processing超精微细加工Super-Precision & Minuteness Processing超声及应用Supersonics Application成本会计Cost Accounting成像原理与技术Principles & Technique of Imaging成组技术Grouping Technique城市规划原理Fundamentals of City Planning城市社会学Urban Sociology程控数字交换Program Controlling of Digital Exchange程序设计Program Designing程序设计方法学Methodology of Programming, Methods of Programming程序设计及算法语言Program Designing & Algorithmic Language程序设计语言Programming Language齿轮啮合原理Principles of Gear Connection冲击测量及误差Punching Measurement & Error冲压工艺Sheet Metal Forming Technology抽象代数Abstract Algebra初等数学Primary Mathematics传坳概论Introduction to Pass Col传动概论Introduction to Transmission传感技术Sensor Technique传感技术及应用Sensor Technique & Application传感器及应用Sensors & Application传感器与检测技术Sensors & Testing Technology传感器原理Fundamentals of Sensors传感器原理及应用Fundamentals of Sensors & Application传热学Heat Transfer船舶操纵Ship Controlling船舶电力系统Ship Electrical Power System船舶电力系统课程设计Course Exercise in Ship Electrical Power System 船舶电气传动自动化Ship Electrified Transmission Automation船舶电站Ship Power Station船舶动力装置Ship Power Equipment船舶概论Introduction to Ships船舶焊接与材料Welding & Materials on Ship船舶机械控制技术Mechanic Control Technology for Ships船舶机械拖动Ship Mechanic Towage船舶建筑美学Artistic Designing of Ships船舶结构Ship Structure船舶结构力学Structural Mechanics for Ships船舶结构与制图Ship Structure & Graphing船舶静力学Ship Statics船舶强度与结构设计Designing Ship Intensity & Structure船舶设计原理Principles of Ship Designing船舶推进Ship Propelling船舶摇摆Ship Swaying船舶摇摆与操纵Ship Swaying & Manipulating船舶振动Ship Vibration船舶阻力Ship Resistance船体建造工艺Ship-Building Technology船体结构Ship Structure船体结构图Ship Structure Graphing船体结构与制图Ship Structure & Graphing船体振动学Ship Vibration船体制图Ship Graphing船用电器设备Marine Electrical Equipment创造心理学Creativity Psychology词汇学Lexicology磁测量技术Magnetic Measurement Technology磁传感器Magnetic Sensor磁存储设备设计原理Fundamental Design of Magnetic Memory Equipment 磁记录Magnetographic磁记录技术Magnetographic Technology磁记录物理Magnetographic Physics磁路设计与场计算Magnetic Path Designing & Magnetic Field Calculati磁盘控制器Magnetic Disk Controler磁性材料Magnetic Materials磁性测量Magnetic Measurement磁性物理Magnetophysics磁原理及应用Principles of Catalyzation & Application催化原理Principles of CatalysisD开头的课程大电流测量Super-Current Measurement大电源测量Super-Power Measurement大机组协调控制Coordination & Control of Generator Networks大跨度房屋结构Large-Span House structure大型锅炉概况Introduction to Large-V olume Boilers大型火电机组控制Control of Large Thermal Power Generator Networks大型数据库原理与高级开发技术Principles of Large-Scale Data-Bas e and Advanced Development Technology 大学德语College German大学俄语College Russian大学法语College French大学日语College Japanese大学生心理学Psychology Introduction大学物理College Physics大学物理实验Experiment of College Physics大学英语College English大学语文College Chinese大众传播学Mass Media代数几何Algebraic Geometry代数几何Algebraic Geometry代数曲面Algebraic Surfaces代数图论Algebraic Graph Theory代数拓扑Algebraic Topology代数学Algebra代用燃料Substitute Fuel代用运放电路Simulated Transmittal Circuit单片机与接口技术Mono-Chip Computers & Interface Technique单片机原理Fundamentals of Mono-Chip Computers单片机原理及应用Fundamentals of Mono-Chip Computers & Applications弹塑性力学Elastic-Plastic Mechanics弹性波Elastic Waves弹性力学Elastic Mechanics, Theory of Elastic Mechanics弹性元件的理论及设计Theory and Design of Elastic Element蛋白质结构基础Principle of Protein Structure蛋白质生物化学技术Biochemical Technology of Protein当代国际关系Contemporary International Relationship当代国外社会思维评价Evaluation of Contemporary Foreign Social Thought当代文学Contemporary Literature当代文学专题Topics on Contemporary Literature当代西方哲学Contemporary Western Philosophy当代戏剧与电影Contemporary Drama & Films当代资本主义经济Contemporary Capitalist Economy党史History of the Party导波光学Wave Guiding Optics德育Moral Education等离子体工程Plasma Engineering低频电子线路Low Frequency Electric Circuit低温测试技术Cryo Testing Technique低温传热学Cryo Conduction低温固体物理Cryo Solid Physics低温技术原理与装置Fundamentals of Cryo Technology & Equipment低温技术中的微机原理Priciples of Microcomputer in Cryo Technology低温绝热Cryo Heat Insulation低温气体制冷机Cryo Gas Refrigerator低温热管Cryo Heat Tube低温设备Cryo Equipment低温生物冻干技术Biological Cryo Freezing Drying Technology低温生物学原理与应用Principle & Application of Cryobiology低温实验技术Cryo Experimentation Technology低温物理导论Cryo Physic Concepts低温物理概论Cryo Physic Concepts低温仪表及测试Cryo Meters & Measurement低温原理Cryo Fundamentals低温原理与设备Cryo Fundamentals & Equipment低温制冷机Cryo Refrigerator低温中的微机应用Application of Microcomputer in Cryo Technology低温装置Cryo Equipment低噪声电子电路Low-Noise Electric Circuit低噪声电子设计Low-Noise Electronic Designing低噪声放大与弱检Low-Noise Increasing & Decreasing低噪声与弱信号检测Detection of Low Noise & Weak Signals地基基础课程设计Course Design of Groundsill Basis地理Geography第二次世界大战史History of World War II典型计算机分析Classical Computer Analysis电测量技术Electric Measurement Technology电厂计算机控制系统Computer Control System in Power Plants电磁测量实验技术Electromagnetic Measurement Experiment & Technology 电磁场计算机Electromagnetic Field Computers电磁场理论Theory of Electromagnetic Fields电磁场数值计算Numerical Calculation of Electromagnetic Fields电磁场与电磁波Electromagnetic Fields & Magnetic Waves电磁场与微波技术Electromagnetic Fields & Micro-Wave Technology电磁场中的数值方法Numerical Methods in Electromagnetic Fields电磁场中的数值计算Numerical Calculation in Electromagnetic Fields电磁学Electromagnetics电动力学Electrodynamics电镀Plating电分析化学Electro-Analytical Chemistry电工材料Electrical Materials电工测量技术基础Measurement Technology of Electrical Engineering电工测试技术基础Testing Technology of Electrical Engineering电工产品学Electrotechnical Products电工电子技术基础Electrical Technology & Electrical Engineering电工电子学Electronics in Electrical Engineering电工基础Fundamental Theory of Electrical Engineering电工基础理论Fundamental Theory of Electrical Engineering电工基础实验Basic Experiment in Electrical Engineering电工技术Electrotechnics电工技术基础Fundamentals of Electrotechnics电工实习Electrical Engineering Practice电工实验Experiment of Electrical Engineering电工实验技术基础Experiment Technology of Electrical Engineering电工学Electrical Engineering电工与电机控制Electrical Engineering & Motor Control电弧电接触Electrical Arc Contact电弧焊及电渣焊Electric Arc Welding & Electroslag Welding电化学测试技术Electrochemical Measurement Technology电化学工程Electrochemical Engineering电化学工艺学Electrochemical Technology电机Motor电机测试技术Motor Measuring Technology电机电磁场的分析与计算Analysis & Calculation of Electrical Motor &电机电磁场的数值计算Calculation of Electrical Motor & Electromagnetic Fields 电机电磁场理论Theory of Electrical Moto & Electromagnetic Fields电机电器与供电Motor Elements and Power Supply电机矩阵分析法Analysis of Electrical Motor Matrix电机课程设计Course Exercise in Electric Engine电机绕组理论Theory of Motor Winding电机绕组理论及应用Theory & Application of Motor Winding电机设计Design of Electrical Motor电机瞬变过程Electrical Motor Change Processes电机统一理论Theory of Electrical Motor Integration电机学Electrical Motor电机学及控制电机Electrical Machinery Control & Technology电机与拖动Electrical Machinery & Towage电机原理Principle of Electric Engine电机原理与拖动Principles of Electrical Machinery & Towage电机专题Lectures on Electric Engine电接触与电弧Electrical Contact & Electrical Arc电介质物理Dielectric Physics电镜Electronic Speculum电力电子电路Power Electronic Circuit电力电子电器Power Electronic Equipment电力电子器件Power Electronic Devices电力电子学Power Electronics电力工程Electrical Power Engineering电力企业管理Management of Electrical Enterprise电力生产技术Technology of Electrical Power Generation电力生产优化管理Optimal Management of Electrical Power Generation电力拖动Electric Traction电力拖动基础Fundamentals for Electrical Towage电力拖动控制系统Electrical Towage Control Systems电力拖动与电气控制Electrical Towage & Electrical Control电力系统Power Systems电力系统电源最优化规划Optimal Planning of Power Source in a Power System 电力系统短路Power System Shortcuts电力系统分析Power System Analysis电力系统规划Power System Planning电力系统过电压Hyper-V oltage of Power Systems电力系统继电保护原理Power System Relay Protection电力系统经济分析Economical Analysis of Power Systems电力系统经济运行Economical Operation of Power Systems电力系统可靠性Power System Reliability电力系统可靠性分析Power System Reliability Analysis电力系统课程设计Course Design of Power Systems电力系统无功补偿及应用Non-Work Compensation in Power Systems & Applicati 电力系统谐波Harmonious Waves in Power Systems电力系统优化设计Optimal Designing of Power Systems电力系统远动Operation of Electric Systems电力系统远动技术Operation Technique of Electric Systems电力系统运行Operation of Electric Systems电力系统自动化Automation of Electric Systems电力系统自动装置Power System Automation Equipment电力系统最优规划Optimal Planning in Power System电力装置课程设计Course Design of Power Equipment电力装置与系统Power Equipment & System电路测量与实验Circuit Measurement & Experiment电路测试技术Circuit Measurement Technology电路测试技术基础Fundamentals of Circuit Measurement Technology电路测试技术及实验Circuit Measurement Technology & Experiments电路分析基础Basis of Circuit Analysis电路分析基础实验Basic Experiment on Circuit Analysis电路分析实验Experiment on Circuit Analysis电路和电子技术Circuit and Electronic Technique电路基本理论Basis Theory of Circuitry电路及电子线路CAD Circuitry CAD电路理论Theory of Circuit电路理论基础Fundamental Theory of Circuit电路理论实验Experiments in Theory of Circuct电路设计与测试技术Circuit Designing & Measurement Technology电气测量技术Electrical Measurement Technology电气传动Electrified Transmission电气控制技术Electrical Control Technology电器设计Electrical Appliances Designing电器学Electrical Appliances电器与控制Electrical Appliances & Control电生理技术基础Basics of Electricphysiological Technology电视传感器图象显示Television Sensor Graphic Display电视接收技术Television Reception Technology电视节目Television Programs电视节目制作Television Program Designing电视新技术New Television Technology电视新闻Television News电视原理Principles of Television电网调度自动化Automation of Electric Network Management电学实验Electrical Experiment电影艺术Art of Film Making电站微机检测控制Computerized Measurement & Control of Power Statio电子材料与元件测试技术Measuring Technology of Electronic Material and Element电子材料元件Electronic Material and Element电子材料元件测量Electronic Material and Element Measurement电子测量与实验技术Technology of Electronic Measurement & Experiment电子测试Electronic Testing电子测试技术Electronic Testing Technology电子测试技术与实验Electronic Testing Technology & Experiment电子测试实验Electronic Testing Experiment电子测试与实验技术Electronic Testing Technology & Experiment电子机械运动控制技术Technology of Electronic Mechanic Movement Control电子技术Technology of Electronics电子技术腐蚀测试中的应用Application of Electronic Technology in Erosion Measurement 电子技术基础Basic Electronic Technology电子技术基础与实验Basic Electronic Technology & Experiment电子技术课程设计Course Exercise in Electronic Technology电子技术实验Experiment in Electronic Technology电子技术综合性设计实验Experiment in Electronic Technology电子理论实验Experiment in Electronic Theory电子商务Electronic Commerce电子系统的ASIC技术ASIC Design Technologies电子显微分析Electronic Micro-Analysis电子显微镜Electronic Microscope电子线路Electronic Circuit电子线路的计算机辅助设计Computer Associate Design of Electronic Circuit电子线路课程设计Course Design of Electronic Circuit电子线路设计与测试技术Electronic Circuit Design & Measurement Technology电子线路设计与测试实验Electronic Circuit Design & Measurement Experiment电子线路实验Experiment in Electronic Circuit电子学Electronics电子学课程设计Course Design of Electronics电子照相技术Electronic Photographing Technology雕塑艺术欣赏Appreciation of Sculptural Art调节原理Principles of Regulation调节装置Regulation Equipment动力机械CAD Dynamical Machine CAD动力学Dynamics动态规划Dynamic Programming动态无损检测Dynamic Non-Destruction Measurement动态信号Dynamic Signal动态信号分析与仪器Dynamic Signal Analysis & Apparatus动物病害学基础Basis of Animal Disease动物免疫学Animal Immunology动物生理与分子生物学Animal Physiology and Molecular Biochemistry动物学Zoology动物遗传工程Animal Genetic Engineering毒理遗传学Toxicological Genetics断裂力学Fracture Mechanics断裂疲劳力学Fatigue Fracture Mechanics锻压测试技术Forging Testing Technique锻压工艺Forging Technology锻压机械液压传动Hydraulic Transmission in Forging Machinery锻压加热设备Forging Heating Equipment锻压设备专题Lectures on Forging Press Equipments锻压系统动力学Dynamics of Forging System锻造工艺Forging Technology锻造加热设备Forging Heat Equipment对外贸易保险International Trade Insurance对外贸易地理International Marketing Geography对外贸易概论Introduction to International Trade对外贸易运输International Trade Transportation多层网络方法Multi-Layer Network Technology多复变函数Analytic Functions of Several Complex Variables多媒体计算机技术Multimedia Computer Technology多媒体技术Multimedia Technology多目标优化方法Multipurpose Optimal Method多项距阵Multi-Nominal Matrix多元统计分析Multivariable StatisticsF开头的课程发电厂Power Plant发电厂电气部分Electric Elements of Power Plants发电厂电气部分与动力部分Electric Elements & Dynamics of Power Plants发电厂电气部分与热力设备Electric Elements & Thermodynamics Equipment of Power Plants 发电厂计算机控制Computer Control in Power Plant发酵工程Zymolysis Engineering发育生物学原理与实验技术Principle and Experimental Technology of Development发展经济学Evolutive Economics法理学Nomology法律基础Fundamentals of Law法学概论An Introduction to Science of Law法学基础Fundamentals of Science of Law翻译Translation翻译理论与技巧Theory & Skills of Translation反不正当经济法Anti-malfeasance Economic Law泛读Extensive Reading泛函分析Functional Analysis泛函分析Functional Analysis房屋建筑学Architectural Design & Construction房屋建筑学课程设计Course Design of House Architecture仿真与辅助设计Simulation & Computer Aided Design放射生物学Radiation Biology放射学Radiology非电量测量Non-Electricity Measurement非金属材料Non-Metal Materials非线性采样系统Non-Linear Sampling System非线性方程组的数值解法Numerical Methods for No-linear System s of Equations非线性光学Nonlinear Optics非线性规划Non-Linear Programming非线性控制理论Non-Linear Control Theory非线性双曲型守恒律解的存在性The Existence of Solutions for Non -linear Hyperbolic Conservation Laws 非线性物理导论Introduction to Nonlinear Physics非线性振荡Non-Linear Oscillation非线性振动Nonlinear Vibration废水处理工程Technology of Wastewater Treatment废水处理与回用Sewage Disposal and Re-use沸腾燃烧Boiling Combustion分布式计算机系统Distributed Computer System / Distributed System分布式系统与分布式处理Distributed Systems and Distributed Processing分离科学Separation Science分析化学Analytical Chemistry分析化学实验Analytical Chemistry Experiment分析力学Analytic Mechanics分析生物化学Analytical Biochemistry分析生物化学Analytical Biochemistry分子病毒学Molecular Virology分子进化工程Engineering of Molecular Evolution分子生物学Molecular Biology分子生物学技术Protocols in Molecular Biology分子遗传学Molecular Genetics风机调节Fan Regulation风机调节.使用.运转Regulation, Application & Operation of Fans风机三元流动理论与设计Tri-Variant Movement Theory & Design of Fans风能利用Wind Power Utilization风险投资分析Analysis of Risk Investment服务业营销Service Industry Marketing辅助机械Aided Machine腐蚀电化学实验Experiment in Erosive Electrochemistry复变函数Complex Variables Functions复变函数与积分变换Functions of Complex Variables & Integral Transformation 复合材料结构力学Structural Mechanics of Composite Material复合材料力学Compound Material Mechanics傅里叶光学Fourier OpticsG开头的课程概率论Probability Theory概率论与数理统计Probability Theory & Mathematical Statistics概率论与随机过程Probability Theory & Stochastic Process概率与统计Probability & Statistics钢笔画Pen Drawing钢的热处理Heat-Treatment of Steel钢结构Steel Structure钢筋混凝土Reinforced Concrete钢筋混凝土及砖石结构Reinforced Concrete & Brick Structure钢砼结构Reinforced Concrete Structure钢砼结构与砌体结构Reinforces Structure and Monsary Structure钢砼课程设计Reinforced Concrete Course Design钢砼设计Experiment of Reinforced Concrete Structure高层建筑基础Tall Building Foundation高层建筑基础设计Designing bases of High Rising Buildings高层建筑结构设计Designing Structures of High Rising Buildings高等材料力学Advanced Material Mechanics高等代数Advanced Algebra高等发光分析Advanced Luminescence Analysis高等分析化学Advanced Analytical Chemistry高等工程力学Advanced Engineering Mechanics高等光学Advanced Optics高等环境微生物Advanced Environmental Microorganism高等教育管理Higher Education Management高等教育史History of Higher Education高等教育学Higher Education高等量子力学Advanced Quantum Mechanics高等生物化学Advanced Biochemistry高等数理方法Advanced Mathematical Method高等数学Advanced Mathematics高等数值分析Advanced Numeric Analysis高等土力学Advanced Soil Mechanics高等无机化学Advanced Inorganic Chemistry高等有机化学Advanced Organic Chemistry高电压测试技术High-Voltage Test Technology高电压技术High-Voltage Technology高电压技术与设备High-V oltage Technology and Device高电压绝缘High-Voltage Insulation高电压实验High-Voltage Experiment高分子材料High Polymer Material高分子材料及加工High Polymer Material & Porcessing高分子化学High Polymer Chemistry高分子化学实验High Polymer Chemistry Experiment高分子化学与物理Polymeric Chemistry and Physics高分子物理High Polymer Physics高分子物理实验High Polymer Physics Experiment高级程序设计语言的设计与实现Advanced Programming Language's Design & Implementation 高级管理信息系统Advanced Management Information Systems高级计算机体系结构Advanced Computer Architecture高级计算机网络Advanced Computer Networks高级计算机网络与集成技术Advanced Computer Networks and Integration Technology高级经济计量Advanced Economic Metrology高级软件工程Advanced Software Engineering高级生化技术Advanced Biochemical Technique高级生物化学Advanced Biochemistry高级食品化学Advanced Food Chemistry高级视听Advanced Videos高级数据库Advanced Database高级数理逻辑Advanced Numerical Logic高级水生生物学Advanced Aquatic Biology高级英语听说Advanced English Listening & Speaking高级植物生理生化Advanced Plant Physiology and Biochemistry高能密束焊High Energy-Dense Beam Welding高频电路High-Frequency Circuit高频电子技术High-Frequency Electronic Technology高频电子线路High-Frequency Electronic Circuit高维代数簇Algebraic Varieties of Higher Dimension高压测量技术High-Voltage Measurement Technology高压测试技术High-Voltage Testing Technology高压电场的数值计算Numerical Calculation in High-V oltage Electronic Field高压电工程High-Voltage Engineering高压电技术High-Voltage Technology高压电器High-Voltage Electrical Appliances高压绝缘High-Voltage Insulation高压实验High-Voltage Experimentation高压实验设备测量High-V oltage Experimentation Equipment Measurement高压试验技术High-Voltage Experimentation Technology工厂电气设备Electric Equipment of Plants工厂供电Factory Electricity Supply工程材料的力学性能测试Mechanic Testing of Engineering Materials工程材料及热处理Engineering Material and Heat Treatment工程材料学Engineering Materials工程测量Engineering Surveying工程测量实习Engineering Measuring Practice工程测试技术Engineering Testing Technique工程测试实验Experiment on Engineering Testing工程测试信息Information of Engineering Testing工程测试与信号处理Engineering Testing & Signal Processing工程地质Engineering Geology工程动力学Engineering Dynamics工程概论Introduction to Engineering工程概预算Project Budget工程经济学Engineering Economics工程静力学Engineering Statics工程力学Engineering Mechanics工程热力学Engineering Thermodynamics工程数学Engineering Mathematics工程项目概预算Engineering Project Estimate & Budget工程项目评估Engineering Project Evaluation工程优化方法Engineering Optimization Method工程运动学Engineering Kinematics工程造价管理Engineering Cost Management工程制图Graphing of Engineering工业产品学Industrial Products工业电子学Industry Electronics工业分析Industrial Analysis工业锅炉Industrial Boiler工业会计学Industrial Accounting工业机器人Industrial Robot工业技术基础Basic Industrial Technology工业技术经济Industrial Technology Economics工业建筑设计原理Principles of Industrial Building Design工业经济理论Industrial Economic Theory工业经济学Industrial Economics工业美术设计Art Designing in Industry工业企业财务管理Industrial Enterprise Financial Management工业企业财务会计Accounting in Industrial Enterprises工业企业管理Industrial Enterprise Management工业企业经营管理Industrial Enterprise Administrative Management 工业社会学Industrial Sociology工业心理学Industrial Psychology工业窑炉Industrial Stoves工艺过程自动化Technics Process Automation工艺设计Technics Design工艺实习Technics Practice工艺原理与研究方法Principles & Research of Technics公差Common Difference公差测试实验Common Difference Testing Experiment公差技术测量Technical Measurement with Common Difference公差与配合Common Difference & Cooperation公共关系Public Relationship公共关系学Public Relations公司法Corporation Law公司组织与管理Organization and Management公司组织与管理Organization and Management of Corporate公文写作Document Writing功能材料原理与技术Principle and Technology of Functional Materials功能高分子Functional Polymer功能性食品Function Foods古代汉语Ancient Chinese古典文学作品选读Selected Readings in Classical Literature骨科医学Osteopathic Medicine固体磁性理论Theory of Magnetism in Solid固体激光Solid State Laser固体激光器件Solid Laser Elements固体激光与电源Solid State Laser & Power Unit固体理论Solid State Theory固体物理Solid-State Physics故障诊断与容错技术Malfunction Diagnoses & Tolerance Technology关税Tariff管理概论Introduction to Management管理沟通Management Communication, Management Negotiation管理会计Managerial Accounting管理经济学Management Economics管理科学专题Management Science Special Subject管理数学Management Mathematics管理系统FOXBASE Management System of FOXBASE管理系统模拟Management System Simulation管理心理学Management Psychology管理信息系统Management Information System管理学Management Theory, Principles of Management管理学Principles of Management光波导理论Light Wave Guide Theory光电技术Photoelectric Technology光电检测与信号处理Optoelectronic Detection and Processing光电课程设计Photoelectric Course Exercise光电摄像技术Photoelectric Photographing Technique光电探测及信号处理Photoelectric Inspect & Signal Processing光电系统课程设计Photoelectric System Course Design光电信号处理Photoelectric Signal Processing光电信号与系统分析Photoelectric Signal & Systematic Analysis光电信息计算机处理Computer Processing in Photoelectric Information光电子技术Photoelectronic Technique光电子学与光电信息技术Optoelectronics and Optoelectronic Information Technology 光辐射探测技术Ray Radiation Detection Technology光接入网技术Technology of Light Access Network光谱Spectrum光谱分析Spectral Analysis光谱学Spectroscopy光纤传感Fibre Optical Sensors光纤传感器Fibre Optical Sensors光纤传感器基础Fundamentals of Fibre Optical Sensors光纤传感器及应用Fibre Optical Sensors & Applications光纤光学Fiber Optics光纤光学课程设计Course Design of Fibre Optical光纤技术实验Experiments in Fibre Optical Technology光纤实验Experiments in Fibre Optical光纤通信基础Basis of Fibre Optical Communication光纤通信技术Fibre Optical Communication Technology光纤通信网络Networks of Fiber Communications光纤通信系统Fibre Optical Communication System, System of Fiber Communications 光纤原理与技术Fibre Optical Operation & Technology光学Optics光学测量Optical Measurement光学分析法Optical Analysis Method光学工艺实习Optical Technology Practice光学计量仪器设计Optical Instrument Gauge Designing光学检测Optical Detection光学设计Optical Design光学信息导论Introduction of Optical Information光学仪器设计Optical Instrument Designing光学仪器与计量仪器设计Optical Instrument & Gauge Instrument Designing光学仪器装配与校正Optical Instrument Installation & Adjustment光学与统计物理Optics and Statistical Physics光学与原子物理Optics & Atomic Physics光子学器件原理与技术Principle and Technology of Photonics Devices光子学专题Special Topics on Photonics广播编辑学Broadcast Editing广播节目制作Broadcast Programming广播新闻Broadcast Journalism广播新闻采写Broadcast Journalism Collection & Composition广告管理Advertising Management广告学Advertisement锅炉课程设计Boiler Combustion Course Designing锅炉燃烧理论Theory of Boiler Combustion锅炉热交换传热强化Boiler Heat Exchange, Conduction & Intensification锅炉原理Principles of Boiler国际财务管理International Finance国际财务管理International Financial Management国际会计International Accounting国际会计专题International Accounting Special Subject国际技术贸易International Technical Trade国际结算International Balance。

ACCAF中英文单词对照4.贸易折扣(商业折扣)trade discount5.现金折扣cash discount 第一章6. 不含税exclusive7. 含税 inclusiveasset 1.资产8. 交易事项Transaction liability2.负债9. 取走withdrawasset 3.所有者权益equity=capital=net 第五章income=revenue=sales 4.收入1.现金 petty cash=cash on hand expense .费用52.支票 chequeplant .厂房63.自动转账 standing order/direct debt machine .机器74.银行给你存款利息 bank interest on intangible asset 8.无形资产deposit87 .非流动资产9 Non current asset(6 5.银行收取利息手续费bank charges )9属于6.银行收取利息 bank interest on petty cash 10.库存现金overdraftcash11.银行存款7.空头支票 dishonored chequetrade receivable=A/R 12.应收账款8.未结清的款项,别人给我的 uncleared inventory.存货13lodgement10 11 12 14(.流动资产current asset 9.未承兑的汇票unpresent cheque )属于141310.别人给我支票undrawn cheque loan15.贷款11.公司业务错误 business error trade payables=A/P 16.应付账款12.银行业务错误 bank erroradvance from customers .预收账款1713.银行存款余额调节表bank 15 16 18.流动负债( current liabilityreconciliation )属于171814.银行透支 overdraftshare capital 19.实收资本15.银行对账单 bank statementshare premium20.资本公积16.现金账簿/银行存款日记账cash Retained earnings=R/ES 21.留存收益bookstatement of financial .资产负债表2217.总账control accounts =general position=SOFPledgerof 变益动表statement 权有.23所者18.明细账individual ledger =personal changes in equity=SOCIEledger=subsidiary ledger=memo account statement of cash flow 24.现金流量表19.应收账款总账 receivable control statement of comprehensive 25.利润表account =receivable general ledger income=SOCI20.应收账款明细账receivable 第二章ledger=sales ledgerdouble-entry bookkeeping .复式记账121.坏账bad debt=irrecoverable debt Debit 借2. 22.毛利润 gross profit Credit贷3. 23.一般性坏账准备 general allowance prepayment 4. 预付账款24.特殊性坏账准备 specific allowance profit5. 利润debt第四章doubtful25.可疑的坏账value added tax=salestax .增值税125.资产减值损失expense-bad debts input tax 2.进项税额written offoutput tax.销项税额3 allowance for A/R坏账准备26.第六章 life20 确定使用寿命inventoryfinite useful life 1 存货21先进先出 first in first out累计摊销 accumulated amortization 222 每年的折旧 3 特殊计价法specific identificationdepreciation for eachyear加权平均法 period average=weighted 4第八章 average1或有事项continuous contingencies动5 移加权平均法2.average=continuous weighted average 或有负债contingentliabilities3.现时义务method=moving weighted average present obligation cost4.或有资产 contingent assets method5.肯定的 certain 6 成本 historical cost6.可能的 net realizable value probable 7 可变现净值7.8 资或许的准备 possible 的失-计提存货跌价产减值损8.遥远的,渺茫的expense-inventory written-downRemote9.perpetual inventory 预计负债 provision9 永续盘存制第九章 system1.periodic inventory 试算平衡 trial Balance制实10 地盘存2.system交易发生 transaction occur3.购货 purchase 复式记账 Double entry 114.12 数量 quantity 结账 Balance off5.期末调整 Year End Adjustment 单价13 unit cost6.错误 gross profit margin14 毛利润率 Errors7.遗漏第七章 omission8. original purchase price任命错误 commission errors买价19.原则性错误site of preparation errors of principle cost 2 场地准备费10.3 运输费 delivery and handling 加总错误 casting errors11.暂记账户安装费4 installationsuspense account第十章员工培训费 employee training51.6资本化后续支出 capital expenditure 预付账款 prepayment2.revenue expenditure 7 费用化后续支出预提费用 accruals3.其他应收款 other receivable 直线法8 straight line method4.递延收入 Deferred income accumulated depreciation 9 累计折旧5. original cost到期 expire 原值106. 值残净estimated 欠款residual arrear 计11 预7.租客value Tenant8. useful life12 预计使用寿命财务报表 financial statements9.余额递减法13 reducing balance method 资产负债表The Statement of Financial Position账14 net book value=carrying 面价值10.利润表valueThe statement ofcomprehensive income置产资定固15 处fixed disposal of11.asset所有者权益变动表The statement ofchange in equity16 固定资产清理 disposal account第十一章研究性支出17 research cost1.18 现金流量表 The statement of cash development cost 开发性支出flowindefinite useful 不确定使用寿命192.经营活动 operating activities3.投资活动 investing activities4.筹资活动 financing activities5.直接法 The direct method6.间接法 indirect method7.付出利息 Interest paid8.付出所得税 Income tax paid9.付出红利 Dividends paid第十二章1.资产负债表日后事项 Events after thereporting period2.调整事项 adjusting event3.非调整事项 Non-adjustingevent第十三章1.会计政策 Accounting policyAccounting Estimate 会计估计2.。

会计学原理知识点归纳(第一、二章)班级:13国会2班助教:席梦娇第一章知识点梳理1.accounting:熟记定义ers of accounting information:external users:例如…(主要使用financial accounting)internal users:例如…(主要使用managerial accounting)3.fundamentals of accounting(1)GAAP:two organizations to establish GAAP private group:FASBgovernment group:SEC(2)IFRS:issued by IASB< international accounting standard aboard> (3)accounting principles:熟记四条principles的定义(4)accounting assumptions:熟记四条assumptions的定义,了解business entities的分类4.accounting equation:重点掌握5.financial statements:熟记四表一注的构成及编制顺序第二章知识点梳理:1.source documents:熟记定义2.account、general ledger、T-account :熟记书写格式3.double-entry accounting:注意理解(每一笔分录有Dr.必有Cr.,Dr. Cr.必相等)4.recording process:analyzing journals post to ledger trial balance5.preparing trial balance:重点掌握编制步骤Chapter 31.accounting period:常用的几种会计分期2.accrual basis VS cash basis:熟记定义,常考点,可能出名词解释。

常用大学课程中英文对照大学课程中英文对照大汇集英文字母开头的课程ALGOL语言ALGOL LanguageBASIC & FORTRAN 语言BASIC Language & FORTRAN LanguageBASIC 语言BASIC LanguageBASIC 语言及应用BASIC Language & ApplicationC 语言C LanguageC++程序设计C++ Program DesigningCAD 概论Introduction to CADCAD/CAM CAD/CAMCET-4 College English Test (Band 4)CET-6 College English Test (Band 6)COBOL语言COBOL LanguageCOBOL语言程序设计COBOL Language Program DesigningC与UNIX环境 C Language & Unix EnvironmentC语言科学计算方法Scientific Computation Method in CC语言与生物医学信息处理 C Language & Biomedical Information Processing dBASE Ⅲ课程设计Course Exercise in dBASE ⅢFORTRAN 77 语言FORTRAN 77 LanguageFORTRAN语言FORTRAN LanguageFoxBase程序设计FoxBase ProgrammingHopf代数Hopf AlgebraHopf代数与代数群量子群Hopf Algebra , Algebraic Group and Qua ntum GroupIBM-PC/XT Fundamentals of Microcomputer IBM-PC/XTIBM-PC微机原理Fundamentals of Microcomputer IBM-PCIBM汇编及高级语言的接口IBM Assembly & its Interfaces with Advanced Programming Languages Internet与Intranet技术Internet and Intranet TechnologyLSI设计基础Basic of LSI DesigningOS/2操作系统OS/2 Operation SystemPASCAL大型作业PASCAL Wide Range WorkingPASCAL课程设计Course Exercise in PASCALPASCAL语言PASCAL LanguagePC机原理Principle of PCUnix编程环境Unix Programming EnvironmentUnix操作系统分析Analysis of Unix SystemVLSI的EDA技术EDA Techniques for VLSIVLSI技术与检测方法VLSI Techniques & Its ExaminationVLSI设计基础Basis of VLSI DesignWindows系统Windows Operation SystemX光分析X-ray AnalysisX射线金属学X-Ray & MetallographyX射线与电镜X-ray & Electric MicroscopeZ-80汇编语言程序设计Z-80 Pragramming in Assembly LanguagesB开头的课程板壳非线性力学Nonlinear Mechanics of Plate and Shell板壳理论Plate Theory , Theory of Plate and Shell板壳力学Plate Mechanics办公自动化Office Automatization办公自动化系统毕业设计Office Automatization Thesis办公自动化系统设计Office Automatization Design半波实验Semiwave Experiment半导体变流技术Semiconductor Converting Technology半导体材料Semiconductor Materials半导体测量Measurement of Semiconductors半导体瓷敏元件Semiconductor Porcelain-Sensitive Elements半导体光电子学Semiconductor Optic Electronics半导体化学Semiconductor Chemistry半导体激光器Semiconductor Laser Unit半导体集成电路Semiconductor Integrated Circuitry半导体理论Semi-conductive Theory半导体器件Semiconductor Devices半导体器件工艺原理Technological Fundamentals of Semiconductor Device半导体器件课程设计Course Design of Semiconductor Devices半导体物理Semiconductor Physics半导体专业Semi-conduction Specialty半导体专业实验Specialty Experiment of Semiconductor半群理论Semi-group Theory保健食品监督评价Evaluation and Supervision on Health Food s保险学Insurance保险学Insurance报告文学专题Special Subject On Reportage报刊编辑学Newspaper & Magazine Editing报刊选读Selected Readings of Newspaper & Magazine报纸编辑学Newspaper Editing泵与风机Pumps and Fans泵与水机Pumps & Water Turbines毕业论文Graduation Thesis毕业设计Graduation Thesis毕业实习Graduation Practice编译方法Compilation Method编译方法Methods of Compiling编译技术Technique of Compiling编译原理Fundamentals of Compiling, Principles of Compiler编译原理课程设计Course Design of Compiling变电站的微机检测Computer Testing in Transformer Substation变电站的微机检测与控制Computer Testing & Control in Transformer Substation变分法与张量Calculus of V ariations & Tensor变分学Calculus of V ariations变流技术Semiconductor Converting Technology变质量系统热力学与新型回转压V ariable Quality System Thermal Mechanics & NeoRo 表面活性剂化学及应用Chemistry and Application of Surfactant表面活性物质Surface Reactive Materials并行处理Parallel Processing并行处理与并行程序设计Parallel Processing and Parallel Programming并行算法Parallel Algorithmic波谱学Spectroscopy, Wave Spectrum波谱学实验Spectroscopic Experiment薄膜光学Film Optics薄膜物理Thin Film Physics不育症的病因学Etiology of InfertilityC开头的课程材料的力学性能测试Measurement of Material Mechanical Performance材料化学Material Chemistry材料力学Mechanics of Materials财税法规与税务会计Laws and Regulations of Finance and Taxes财务案例分析Case Analysis of Finance Management财务案例分析Case Analysis of Financial Management财务报告分析Analysis of Financial Statement财务成本管理Financial Cost Management财务管理Financial Management, Financial Cost Management财务管理与分析Financial Management and Analysis财务会计Financial Accountancy财政学Public Finance财政与金融Finance & Banking财政与税收Finance & Revenue财政与税收理论Theories on Public Finance and Tax Revenue财政与信贷Finance & Credit操作系统Disk Operating System (DOS)操作系统课程设计Course Design in Disk Operating System操作系统与编译原理Disk Operating System & Fundamentals of Compiling操作系统原理Fundamentals of Disk Operating System, Principles of Operating System 测量技术基础Foundation of Measurement Technology测量原理与仪器设计Measurement Fundamentals & Meter Design测试技术Testing Technology测试与信号变换处理Testing & Signal Transformation Processing策波测量技术Technique of Whip Wave Measurement策略管理Strategic Management产品学Production产业经济学Industrial Economy产业组织Industrial Organization产业组织学Industrial Organization Technology常微分方程Ordinary Differential Equations场论Field Theory超导磁体及应用Superconductive Magnet & Application超导及应用Superconductive & Application超高真空科学与技术Science and Technology of Ultrahigh V acuum 60超精密加工和微细加工Super-Precision & Minuteness Processing超精微细加工Super-Precision & Minuteness Processing超声及应用Supersonics Application成本会计Cost Accounting成像原理与技术Principles & Technique of Imaging成组技术Grouping Technique城市规划原理Fundamentals of City Planning城市社会学Urban Sociology程控数字交换Program Controlling of Digital Exchange程序设计Program Designing程序设计方法学Methodology of Programming, Methods of Programming程序设计及算法语言Program Designing & Algorithmic Language程序设计语言Programming Language齿轮啮合原理Principles of Gear Connection冲击测量及误差Punching Measurement & Error冲压工艺Sheet Metal Forming Technology抽象代数Abstract Algebra初等数学Primary Mathematics传坳概论Introduction to Pass Col传动概论Introduction to Transmission传感技术Sensor Technique传感技术及应用Sensor Technique & Application传感器及应用Sensors & Application传感器与检测技术Sensors & Testing Technology传感器原理Fundamentals of Sensors传感器原理及应用Fundamentals of Sensors & Application传热学Heat Transfer船舶操纵Ship Controlling船舶电力系统Ship Electrical Power System船舶电力系统课程设计Course Exercise in Ship Electrical Power System 船舶电气传动自动化Ship Electrified Transmission Automation船舶电站Ship Power Station船舶动力装置Ship Power Equipment船舶概论Introduction to Ships船舶焊接与材料Welding & Materials on Ship船舶机械控制技术Mechanic Control Technology for Ships船舶机械拖动Ship Mechanic Towage船舶建筑美学Artistic Designing of Ships船舶结构Ship Structure船舶结构力学Structural Mechanics for Ships船舶结构与制图Ship Structure & Graphing船舶静力学Ship Statics船舶强度与结构设计Designing Ship Intensity & Structure船舶设计原理Principles of Ship Designing船舶推进Ship Propelling船舶摇摆Ship Swaying船舶摇摆与操纵Ship Swaying & Manipulating船舶振动Ship V ibration船舶阻力Ship Resistance船体建造工艺Ship-Building Technology船体结构Ship Structure船体结构图Ship Structure Graphing船体结构与制图Ship Structure & Graphing船体振动学Ship V ibration船体制图Ship Graphing船用电器设备Marine Electrical Equipment创造心理学Creativity Psychology词汇学Lexicology磁测量技术Magnetic Measurement Technology磁传感器Magnetic Sensor磁存储设备设计原理Fundamental Design of Magnetic Memory Equipment 磁记录Magnetographic磁记录技术Magnetographic Technology磁记录物理Magnetographic Physics磁路设计与场计算Magnetic Path Designing & Magnetic Field Calculati磁盘控制器Magnetic Disk Controler磁性材料Magnetic Materials磁性测量Magnetic Measurement磁性物理Magnetophysics磁原理及应用Principles of Catalyzation & Application催化原理Principles of CatalysisD开头的课程大电流测量Super-Current Measurement大电源测量Super-Power Measurement大机组协调控制Coordination & Control of Generator Networks大跨度房屋结构Large-Span House structure大型锅炉概况Introduction to Large-V olume Boilers大型火电机组控制Control of Large Thermal Power Generator Networks大型数据库原理与高级开发技术Principles of Large-Scale Data-Bas e and Advanced Development Technology 大学德语College German大学俄语College Russian大学法语College French大学日语College Japanese大学生心理学Psychology Introduction大学物理College Physics大学物理实验Experiment of College Physics大学英语College English大学语文College Chinese大众传播学Mass Media代数几何Algebraic Geometry代数几何Algebraic Geometry代数曲面Algebraic Surfaces代数图论Algebraic Graph Theory代数拓扑Algebraic Topology代数学Algebra代用燃料Substitute Fuel代用运放电路Simulated Transmittal Circuit单片机与接口技术Mono-Chip Computers & Interface Technique单片机原理Fundamentals of Mono-Chip Computers单片机原理及应用Fundamentals of Mono-Chip Computers & Applications弹塑性力学Elastic-Plastic Mechanics弹性波Elastic Waves弹性力学Elastic Mechanics, Theory of Elastic Mechanics弹性元件的理论及设计Theory and Design of Elastic Element蛋白质结构基础Principle of Protein Structure蛋白质生物化学技术Biochemical Technology of Protein当代国际关系Contemporary International Relationship当代国外社会思维评价Evaluation of Contemporary Foreign Social Thought当代文学Contemporary Literature当代文学专题Topics on Contemporary Literature当代西方哲学Contemporary Western Philosophy当代戏剧与电影Contemporary Drama & Films当代资本主义经济Contemporary Capitalist Economy党史History of the Party导波光学Wave Guiding Optics德育Moral Education等离子体工程Plasma Engineering低频电子线路Low Frequency Electric Circuit低温测试技术Cryo Testing Technique低温传热学Cryo Conduction低温固体物理Cryo Solid Physics低温技术原理与装置Fundamentals of Cryo Technology & Equipment低温技术中的微机原理Priciples of Microcomputer in Cryo Technology低温绝热Cryo Heat Insulation低温气体制冷机Cryo Gas Refrigerator低温热管Cryo Heat Tube低温设备Cryo Equipment低温生物冻干技术Biological Cryo Freezing Drying Technology低温生物学原理与应用Principle & Application of Cryobiology低温实验技术Cryo Experimentation Technology低温物理导论Cryo Physic Concepts低温物理概论Cryo Physic Concepts低温仪表及测试Cryo Meters & Measurement低温原理Cryo Fundamentals低温原理与设备Cryo Fundamentals & Equipment低温制冷机Cryo Refrigerator低温中的微机应用Application of Microcomputer in Cryo Technology低温装置Cryo Equipment低噪声电子电路Low-Noise Electric Circuit低噪声电子设计Low-Noise Electronic Designing低噪声放大与弱检Low-Noise Increasing & Decreasing低噪声与弱信号检测Detection of Low Noise & Weak Signals地基基础课程设计Course Design of Groundsill Basis地理Geography第二次世界大战史History of World War II典型计算机分析Classical Computer Analysis电测量技术Electric Measurement Technology电厂计算机控制系统Computer Control System in Power Plants电磁测量实验技术Electromagnetic Measurement Experiment & Technology 电磁场计算机Electromagnetic Field Computers电磁场理论Theory of Electromagnetic Fields电磁场数值计算Numerical Calculation of Electromagnetic Fields电磁场与电磁波Electromagnetic Fields & Magnetic Waves电磁场与微波技术Electromagnetic Fields & Micro-Wave Technology电磁场中的数值方法Numerical Methods in Electromagnetic Fields电磁场中的数值计算Numerical Calculation in Electromagnetic Fields电磁学Electromagnetics电动力学Electrodynamics电镀Plating电分析化学Electro-Analytical Chemistry电工材料Electrical Materials电工测量技术基础Measurement Technology of Electrical Engineering电工测试技术基础Testing Technology of Electrical Engineering电工产品学Electrotechnical Products电工电子技术基础Electrical Technology & Electrical Engineering电工电子学Electronics in Electrical Engineering电工基础Fundamental Theory of Electrical Engineering电工基础理论Fundamental Theory of Electrical Engineering电工基础实验Basic Experiment in Electrical Engineering电工技术Electrotechnics电工技术基础Fundamentals of Electrotechnics电工实习Electrical Engineering Practice电工实验Experiment of Electrical Engineering电工实验技术基础Experiment Technology of Electrical Engineering电工学Electrical Engineering电工与电机控制Electrical Engineering & Motor Control电弧电接触Electrical Arc Contact电弧焊及电渣焊Electric Arc Welding & Electroslag Welding电化学测试技术Electrochemical Measurement Technology电化学工程Electrochemical Engineering电化学工艺学Electrochemical Technology电机Motor电机测试技术Motor Measuring Technology电机电磁场的分析与计算Analysis & Calculation of Electrical Motor &电机电磁场的数值计算Calculation of Electrical Motor & Electromagnetic Fields 电机电磁场理论Theory of Electrical Moto & Electromagnetic Fields电机电器与供电Motor Elements and Power Supply电机矩阵分析法Analysis of Electrical Motor Matrix电机课程设计Course Exercise in Electric Engine电机绕组理论Theory of Motor Winding电机绕组理论及应用Theory & Application of Motor Winding电机设计Design of Electrical Motor电机瞬变过程Electrical Motor Change Processes电机统一理论Theory of Electrical Motor Integration电机学Electrical Motor电机学及控制电机Electrical Machinery Control & Technology电机与拖动Electrical Machinery & Towage电机原理Principle of Electric Engine电机原理与拖动Principles of Electrical Machinery & Towage电机专题Lectures on Electric Engine电接触与电弧Electrical Contact & Electrical Arc电介质物理Dielectric Physics电镜Electronic Speculum电力电子电路Power Electronic Circuit电力电子电器Power Electronic Equipment电力电子器件Power Electronic Devices电力电子学Power Electronics电力工程Electrical Power Engineering电力企业管理Management of Electrical Enterprise电力生产技术Technology of Electrical Power Generation电力生产优化管理Optimal Management of Electrical Power Generation电力拖动Electric Traction电力拖动基础Fundamentals for Electrical Towage电力拖动控制系统Electrical Towage Control Systems电力拖动与电气控制Electrical Towage & Electrical Control电力系统Power Systems电力系统电源最优化规划Optimal Planning of Power Source in a Power System 电力系统短路Power System Shortcuts电力系统分析Power System Analysis电力系统规划Power System Planning电力系统过电压Hyper-V oltage of Power Systems电力系统继电保护原理Power System Relay Protection电力系统经济分析Economical Analysis of Power Systems电力系统经济运行Economical Operation of Power Systems电力系统可靠性Power System Reliability电力系统可靠性分析Power System Reliability Analysis电力系统课程设计Course Design of Power Systems电力系统无功补偿及应用Non-Work Compensation in Power Systems & Applicati 电力系统谐波Harmonious Waves in Power Systems电力系统优化设计Optimal Designing of Power Systems电力系统远动Operation of Electric Systems电力系统远动技术Operation Technique of Electric Systems电力系统运行Operation of Electric Systems电力系统自动化Automation of Electric Systems电力系统自动装置Power System Automation Equipment电力系统最优规划Optimal Planning in Power System电力装置课程设计Course Design of Power Equipment电力装置与系统Power Equipment & System电路测量与实验Circuit Measurement & Experiment电路测试技术Circuit Measurement Technology电路测试技术基础Fundamentals of Circuit Measurement Technology电路测试技术及实验Circuit Measurement Technology & Experiments电路分析基础Basis of Circuit Analysis电路分析基础实验Basic Experiment on Circuit Analysis电路分析实验Experiment on Circuit Analysis电路和电子技术Circuit and Electronic Technique电路基本理论Basis Theory of Circuitry电路及电子线路CAD Circuitry CAD电路理论Theory of Circuit电路理论基础Fundamental Theory of Circuit电路理论实验Experiments in Theory of Circuct电路设计与测试技术Circuit Designing & Measurement Technology电气测量技术Electrical Measurement Technology电气传动Electrified Transmission电气控制技术Electrical Control Technology电器设计Electrical Appliances Designing电器学Electrical Appliances电器与控制Electrical Appliances & Control电生理技术基础Basics of Electricphysiological Technology电视传感器图象显示Television Sensor Graphic Display电视接收技术Television Reception Technology电视节目Television Programs电视节目制作Television Program Designing电视新技术New Television Technology电视新闻Television News电视原理Principles of Television电网调度自动化Automation of Electric Network Management电学实验Electrical Experiment电影艺术Art of Film Making电站微机检测控制Computerized Measurement & Control of Power Statio电子材料与元件测试技术Measuring Technology of Electronic Material and Element电子材料元件Electronic Material and Element电子材料元件测量Electronic Material and Element Measurement电子测量与实验技术Technology of Electronic Measurement & Experiment电子测试Electronic Testing电子测试技术Electronic Testing Technology电子测试技术与实验Electronic Testing Technology & Experiment电子测试实验Electronic Testing Experiment电子测试与实验技术Electronic Testing Technology & Experiment电子机械运动控制技术Technology of Electronic Mechanic Movement Control电子技术Technology of Electronics电子技术腐蚀测试中的应用Application of Electronic Technology in Erosion Measurement 电子技术基础Basic Electronic Technology电子技术基础与实验Basic Electronic Technology & Experiment电子技术课程设计Course Exercise in Electronic Technology电子技术实验Experiment in Electronic Technology电子技术综合性设计实验Experiment in Electronic Technology电子理论实验Experiment in Electronic Theory电子商务Electronic Commerce电子系统的ASIC技术ASIC Design Technologies电子显微分析Electronic Micro-Analysis电子显微镜Electronic Microscope电子线路Electronic Circuit电子线路的计算机辅助设计Computer Associate Design of Electronic Circuit电子线路课程设计Course Design of Electronic Circuit电子线路设计与测试技术Electronic Circuit Design & Measurement Technology电子线路设计与测试实验Electronic Circuit Design & Measurement Experiment电子线路实验Experiment in Electronic Circuit电子学Electronics电子学课程设计Course Design of Electronics电子照相技术Electronic Photographing Technology雕塑艺术欣赏Appreciation of Sculptural Art调节原理Principles of Regulation调节装置Regulation Equipment动力机械CAD Dynamical Machine CAD动力学Dynamics动态规划Dynamic Programming动态无损检测Dynamic Non-Destruction Measurement动态信号Dynamic Signal动态信号分析与仪器Dynamic Signal Analysis & Apparatus动物病害学基础Basis of Animal Disease动物免疫学Animal Immunology动物生理与分子生物学Animal Physiology and Molecular Biochemistry动物学Zoology动物遗传工程Animal Genetic Engineering毒理遗传学Toxicological Genetics断裂力学Fracture Mechanics断裂疲劳力学Fatigue Fracture Mechanics锻压测试技术Forging Testing Technique锻压工艺Forging Technology锻压机械液压传动Hydraulic Transmission in Forging Machinery锻压加热设备Forging Heating Equipment锻压设备专题Lectures on Forging Press Equipments锻压系统动力学Dynamics of Forging System锻造工艺Forging Technology锻造加热设备Forging Heat Equipment对外贸易保险International Trade Insurance对外贸易地理International Marketing Geography对外贸易概论Introduction to International Trade对外贸易运输International Trade Transportation多层网络方法Multi-Layer Network Technology多复变函数Analytic Functions of Several Complex V ariables多媒体计算机技术Multimedia Computer Technology多媒体技术Multimedia Technology多目标优化方法Multipurpose Optimal Method多项距阵Multi-Nominal Matrix多元统计分析Multivariable StatisticsF开头的课程发电厂Power Plant发电厂电气部分Electric Elements of Power Plants发电厂电气部分与动力部分Electric Elements & Dynamics of Power Plants发电厂电气部分与热力设备Electric Elements & Thermodynamics Equipment of Power Plants发电厂计算机控制Computer Control in Power Plant发酵工程Zymolysis Engineering发育生物学原理与实验技术Principle and Experimental Technology of Development发展经济学Evolutive Economics法理学Nomology法律基础Fundamentals of Law法学概论An Introduction to Science of Law法学基础Fundamentals of Science of Law翻译Translation翻译理论与技巧Theory & Skills of Translation反不正当经济法Anti-malfeasance Economic Law泛读Extensive Reading泛函分析Functional Analysis泛函分析Functional Analysis房屋建筑学Architectural Design & Construction房屋建筑学课程设计Course Design of House Architecture仿真与辅助设计Simulation & Computer Aided Design放射生物学Radiation Biology放射学Radiology非电量测量Non-Electricity Measurement非金属材料Non-Metal Materials非线性采样系统Non-Linear Sampling System非线性方程组的数值解法Numerical Methods for No-linear System s of Equations非线性光学Nonlinear Optics非线性规划Non-Linear Programming非线性控制理论Non-Linear Control Theory非线性双曲型守恒律解的存在性The Existence of Solutions for Non -linear Hyperbolic Conservation Laws 非线性物理导论Introduction to Nonlinear Physics非线性振荡Non-Linear Oscillation非线性振动Nonlinear V ibration废水处理工程Technology of Wastewater Treatment废水处理与回用Sewage Disposal and Re-use沸腾燃烧Boiling Combustion分布式计算机系统Distributed Computer System / Distributed System分布式系统与分布式处理Distributed Systems and Distributed Processing分离科学Separation Science分析化学Analytical Chemistry分析化学实验Analytical Chemistry Experiment分析力学Analytic Mechanics分析生物化学Analytical Biochemistry分析生物化学Analytical Biochemistry分子病毒学Molecular Virology分子进化工程Engineering of Molecular Evolution分子生物学Molecular Biology分子生物学技术Protocols in Molecular Biology分子遗传学Molecular Genetics风机调节Fan Regulation风机调节.使用.运转Regulation, Application & Operation of Fans风机三元流动理论与设计Tri-V ariant Movement Theory & Design of Fans风能利用Wind Power Utilization风险投资分析Analysis of Risk Investment服务业营销Service Industry Marketing辅助机械Aided Machine腐蚀电化学实验Experiment in Erosive Electrochemistry复变函数Complex V ariables Functions复变函数与积分变换Functions of Complex V ariables & Integral Transformation 复合材料结构力学Structural Mechanics of Composite Material复合材料力学Compound Material Mechanics傅里叶光学Fourier OpticsG开头的课程概率论Probability Theory概率论与数理统计Probability Theory & Mathematical Statistics概率论与随机过程Probability Theory & Stochastic Process概率与统计Probability & Statistics钢笔画Pen Drawing钢的热处理Heat-Treatment of Steel钢结构Steel Structure钢筋混凝土Reinforced Concrete钢筋混凝土及砖石结构Reinforced Concrete & Brick Structure钢砼结构Reinforced Concrete Structure钢砼结构与砌体结构Reinforces Structure and Monsary Structure钢砼课程设计Reinforced Concrete Course Design钢砼设计Experiment of Reinforced Concrete Structure高层建筑基础Tall Building Foundation高层建筑基础设计Designing bases of High Rising Buildings高层建筑结构设计Designing Structures of High Rising Buildings高等材料力学Advanced Material Mechanics高等代数Advanced Algebra高等发光分析Advanced Luminescence Analysis高等分析化学Advanced Analytical Chemistry高等工程力学Advanced Engineering Mechanics高等光学Advanced Optics高等环境微生物Advanced Environmental Microorganism高等教育管理Higher Education Management高等教育史History of Higher Education高等教育学Higher Education高等量子力学Advanced Quantum Mechanics高等生物化学Advanced Biochemistry高等数理方法Advanced Mathematical Method高等数学Advanced Mathematics高等数值分析Advanced Numeric Analysis高等土力学Advanced Soil Mechanics高等无机化学Advanced Inorganic Chemistry高等有机化学Advanced Organic Chemistry高电压测试技术High-V oltage Test Technology高电压技术High-V oltage Technology高电压技术与设备High-V oltage Technology and Device高电压绝缘High-V oltage Insulation高电压实验High-V oltage Experiment高分子材料High Polymer Material高分子材料及加工High Polymer Material & Porcessing高分子化学High Polymer Chemistry高分子化学实验High Polymer Chemistry Experiment高分子化学与物理Polymeric Chemistry and Physics高分子物理High Polymer Physics高分子物理实验High Polymer Physics Experiment高级程序设计语言的设计与实现Advanced Programming Language's Design & Implementation 高级管理信息系统Advanced Management Information Systems高级计算机体系结构Advanced Computer Architecture高级计算机网络Advanced Computer Networks高级计算机网络与集成技术Advanced Computer Networks and Integration Technology高级经济计量Advanced Economic Metrology高级软件工程Advanced Software Engineering高级生化技术Advanced Biochemical Technique高级生物化学Advanced Biochemistry高级食品化学Advanced Food Chemistry高级视听Advanced V ideos高级数据库Advanced Database高级数理逻辑Advanced Numerical Logic高级水生生物学Advanced Aquatic Biology高级英语听说Advanced English Listening & Speaking高级植物生理生化Advanced Plant Physiology and Biochemistry高能密束焊High Energy-Dense Beam Welding高频电路High-Frequency Circuit高频电子技术High-Frequency Electronic Technology高频电子线路High-Frequency Electronic Circuit高维代数簇Algebraic V arieties of Higher Dimension高压测量技术High-V oltage Measurement Technology高压测试技术High-V oltage Testing Technology高压电场的数值计算Numerical Calculation in High-V oltage Electronic Field高压电工程High-V oltage Engineering高压电技术High-V oltage Technology高压电器High-V oltage Electrical Appliances高压绝缘High-V oltage Insulation高压实验High-V oltage Experimentation高压实验设备测量High-V oltage Experimentation Equipment Measurement高压试验技术High-V oltage Experimentation Technology工厂电气设备Electric Equipment of Plants工厂供电Factory Electricity Supply工程材料的力学性能测试Mechanic Testing of Engineering Materials 工程材料及热处理Engineering Material and Heat Treatment工程材料学Engineering Materials工程测量Engineering Surveying工程测量实习Engineering Measuring Practice工程测试技术Engineering Testing Technique工程测试实验Experiment on Engineering Testing工程测试信息Information of Engineering Testing工程测试与信号处理Engineering Testing & Signal Processing工程地质Engineering Geology工程动力学Engineering Dynamics工程概论Introduction to Engineering工程概预算Project Budget工程经济学Engineering Economics工程静力学Engineering Statics工程力学Engineering Mechanics工程热力学Engineering Thermodynamics工程数学Engineering Mathematics工程项目概预算Engineering Project Estimate & Budget工程项目评估Engineering Project Evaluation工程优化方法Engineering Optimization Method工程运动学Engineering Kinematics工程造价管理Engineering Cost Management工程制图Graphing of Engineering工业产品学Industrial Products工业电子学Industry Electronics工业分析Industrial Analysis工业锅炉Industrial Boiler工业会计学Industrial Accounting工业机器人Industrial Robot工业技术基础Basic Industrial Technology工业技术经济Industrial Technology Economics工业建筑设计原理Principles of Industrial Building Design工业经济理论Industrial Economic Theory工业经济学Industrial Economics工业美术设计Art Designing in Industry工业企业财务管理Industrial Enterprise Financial Management工业企业财务会计Accounting in Industrial Enterprises工业企业管理Industrial Enterprise Management工业企业经营管理Industrial Enterprise Administrative Management 工业社会学Industrial Sociology工业心理学Industrial Psychology工业窑炉Industrial Stoves工艺过程自动化Technics Process Automation工艺设计Technics Design工艺实习Technics Practice工艺原理与研究方法Principles & Research of Technics公差Common Difference公差测试实验Common Difference Testing Experiment公差技术测量Technical Measurement with Common Difference公差与配合Common Difference & Cooperation公共关系Public Relationship公共关系学Public Relations公司法Corporation Law公司组织与管理Organization and Management公司组织与管理Organization and Management of Corporate公文写作Document Writing功能材料原理与技术Principle and Technology of Functional Materials 功能高分子Functional Polymer功能性食品Function Foods古代汉语Ancient Chinese古典文学作品选读Selected Readings in Classical Literature骨科医学Osteopathic Medicine固体磁性理论Theory of Magnetism in Solid固体激光Solid State Laser固体激光器件Solid Laser Elements固体激光与电源Solid State Laser & Power Unit固体理论Solid State Theory固体物理Solid-State Physics故障诊断与容错技术Malfunction Diagnoses & Tolerance Technology 关税Tariff管理概论Introduction to Management管理沟通Management Communication, Management Negotiation管理会计Managerial Accounting管理经济学Management Economics管理科学专题Management Science Special Subject管理数学Management Mathematics管理系统FOXBASE Management System of FOXBASE管理系统模拟Management System Simulation管理心理学Management Psychology管理信息系统Management Information System管理学Management Theory, Principles of Management管理学Principles of Management光波导理论Light Wave Guide Theory光电技术Photoelectric Technology光电检测与信号处理Optoelectronic Detection and Processing光电课程设计Photoelectric Course Exercise光电摄像技术Photoelectric Photographing Technique光电探测及信号处理Photoelectric Inspect & Signal Processing光电系统课程设计Photoelectric System Course Design光电信号处理Photoelectric Signal Processing光电信号与系统分析Photoelectric Signal & Systematic Analysis光电信息计算机处理Computer Processing in Photoelectric Information光电子技术Photoelectronic Technique光电子学与光电信息技术Optoelectronics and Optoelectronic Information Technology 光辐射探测技术Ray Radiation Detection Technology光接入网技术Technology of Light Access Network光谱Spectrum光谱分析Spectral Analysis光谱学Spectroscopy光纤传感Fibre Optical Sensors光纤传感器Fibre Optical Sensors光纤传感器基础Fundamentals of Fibre Optical Sensors光纤传感器及应用Fibre Optical Sensors & Applications光纤光学Fiber Optics光纤光学课程设计Course Design of Fibre Optical光纤技术实验Experiments in Fibre Optical Technology光纤实验Experiments in Fibre Optical光纤通信基础Basis of Fibre Optical Communication光纤通信技术Fibre Optical Communication Technology光纤通信网络Networks of Fiber Communications光纤通信系统Fibre Optical Communication System, System of Fiber Communications 光纤原理与技术Fibre Optical Operation & Technology光学Optics光学测量Optical Measurement光学分析法Optical Analysis Method光学工艺实习Optical Technology Practice光学计量仪器设计Optical Instrument Gauge Designing光学检测Optical Detection光学设计Optical Design光学信息导论Introduction of Optical Information光学仪器设计Optical Instrument Designing光学仪器与计量仪器设计Optical Instrument & Gauge Instrument Designing光学仪器装配与校正Optical Instrument Installation & Adjustment光学与统计物理Optics and Statistical Physics光学与原子物理Optics & Atomic Physics光子学器件原理与技术Principle and Technology of Photonics Devices光子学专题Special Topics on Photonics广播编辑学Broadcast Editing广播节目制作Broadcast Programming广播新闻Broadcast Journalism广播新闻采写Broadcast Journalism Collection & Composition广告管理Advertising Management广告学Advertisement锅炉课程设计Boiler Combustion Course Designing锅炉燃烧理论Theory of Boiler Combustion。