工程经济答案02

- 格式:doc

- 大小:54.00 KB

- 文档页数:4

第2章现金流量与资金的时间价值一、思考题1.什么是现金流量?财务现金流量和国民经济费用效益流量有什么区别?参考答案:在考察对象一定时期各时点上实际资金流入或资金流出称为现金流量。

对工程项目进行财务评价时,是从项目角度对对工程项目进行财务分析时,按现行财税制度和市场价格确定财务现金流量;对工程项目进行国民经济评价时,是从国民经济角度出发,按资源优化配置原则和和影子价格确定国民经济效益费用流量。

2.什么是现金流量图?参考答案:现金流量图是一种反映经济系统资金运动状态的图式,即把经济系统的现金流量绘入一幅时间坐标图中,表述各现金流入、流出与相应时间的对应关系。

绘制现金流量图的三要素是指:现金大小(资金数额)、现金流量的方向(资金的流入流出)和现金流量的作用点(资金发生的时间)。

3.如何理解资金的时间价值?参考答案:资金的时间价值可以从两方面来理解:①一方面,资金投入生产和其他生产要素相结合,经过一段时间发生增值,使其价值大于原投入的价值。

因此,从投资者的角度看,资金的增值特性使资金具有时间价值;②另一方面,资金一旦用于投资,就不能用于现期消费,牺牲现期消费是为了能在将来得到更多的消费,个人储蓄的目的就是如此。

因此,资金的时间价值体现为对放弃现期消费的损失所应给予的必要补偿4.简述资金时间价值产生的原因?参考答案:(1)资金增值:投入生产要素(劳动力、资金、生产资料、先进技术、管理、经验等)使生产增值,作为生产要素的资金理应享受增值成果。

(2)承担风险:现在得到的钱比许诺十年末支付的钱保险、可靠。

(3)通货膨胀:通货膨胀作为社会发展的总趋势,导致货币贬值,购买力下降。

计算题。

5.什么是等值、现值、终值、折现和年值?参考答案:①等值是指在资金运动过程中,由于时间价值,不同时点的资金绝对值不等,但实际价值相等的现象。

②现值是指发生在(或折算为)某一现金流量序列起点的现金流量价值,简称P 。

折现是指把未来某时点的现金流量折算为起始时点值的过程。

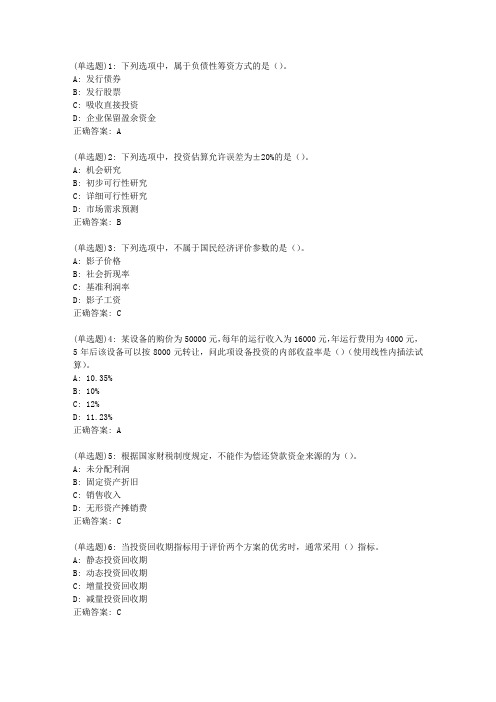

(单选题)1: 下列选项中,属于负债性筹资方式的是()。

A: 发行债券

B: 发行股票

C: 吸收直接投资

D: 企业保留盈余资金

正确答案: A

(单选题)2: 下列选项中,投资估算允许误差为±20%的是()。

A: 机会研究

B: 初步可行性研究

C: 详细可行性研究

D: 市场需求预测

正确答案: B

(单选题)3: 下列选项中,不属于国民经济评价参数的是()。

A: 影子价格

B: 社会折现率

C: 基准利润率

D: 影子工资

正确答案: C

(单选题)4: 某设备的购价为50000元,每年的运行收入为16000元,年运行费用为4000元,5年后该设备可以按8000元转让,问此项设备投资的内部收益率是()(使用线性内插法试算)。

A: 10.35%

B: 10%

C: 12%

D: 11.23%

正确答案: A

(单选题)5: 根据国家财税制度规定,不能作为偿还贷款资金来源的为()。

A: 未分配利润

B: 固定资产折旧

C: 销售收入

D: 无形资产摊销费

正确答案: C

(单选题)6: 当投资回收期指标用于评价两个方案的优劣时,通常采用()指标。

A: 静态投资回收期

B: 动态投资回收期

C: 增量投资回收期

D: 减量投资回收期

正确答案: C。

工程经济模拟测试题二一、单项选择题(每小题1分,共60分)1.现金流量表由现金流入、现金流出和净现金流量构成,其具体内容随工程经济分析的范围和经济评价方法的不同而不同,其中财务现金流量表主要用于A现金收支B财务评价C现金流量D经济评价2.在实际应用中,动态投资回收期由于与其他动态盈利性指标相近,若给出的利率Ic恰好等于财务内部收益率FIRR时,则动态投资回收期P,和项目寿命周期N的关系为A P,=NB P,<NC P,>N D不可比3.某项目建设投产估计总投资2800万,项目建成后各年净收益为320万,则该项目的静态投资回收期为()A8.75年B8.55年C6年D9年4.利息备付率和偿债备付率是评价投资项目偿债能力的重要指标,对于正常经营的企业,利息备付率和偿债备付率应()A均大于1 B分别大于1和2 C均大于2 D分别大于2和15.设备一台,目前实际价值P=8000元,估计残值L=800元,第一年的设备运行成本Q=600元,每年设备的劣化增量是均等的,年劣化值为300元,其经济寿命是()A7年B7.5年C8年D6.5年6.某企业于年初向银行借入1500元,其年有效利率为10%,若按月复利计息,则该年第三季度借款本利和为()元。

A1611.1元B1612.5元C1616.3元D1637.5元7.某企业单位产品售价为7元,该企业成本与销售的关系为Y=40000+4X,则盈亏平衡点的销售量为()A16666.66 B13333.33 C93333.3 D49999.988.利用财务净现值进行项目投资决策评价时,当FNPV<0时,说明该方案A可行B不可行C经济上可行D不能决定9.确定基准收益率的基础是A资金成本与机会成本B投资风险与通货膨胀C现金流量D收入状况10.某建设项目年设计能力为10万台,年固定成本为1200万元,产品单位价格为900元,单台产品可变成本为560元,单台产品销售税金及附加为120元,则盈亏平衡点的产销量为A54545台B54564台C51235台D56231台11.设备租赁的租金计算方法主要有A附加率法与年金法B净现金流量法C还款期法D费用测定法12.某公司拟租出一台设备,设备价值为68万,租期为5年,每年年底收取租金,折现率为10%,附加率为4%,则年租金为A20.92万B23.12万C24.52万D20万13.在投资收益率计算中,IRR是A初始投资收益率B未收回投资的收益率C静态收益率D投资报酬率14.若i1=2i2,n1=n2/2, 则当P相同时A(F/P,i1,n1)<(F/P,i2,n2) B(F/P,i1,n1)=(F/P,i2,n2) C(F/P,i1,n1)>(F/P,i2,n2) D无法比较15.如果本金越大,利率越高,计息周期越多时,复利与单利二者计算的结果就相差A越小B越大C不变D前小后大16.找出实际功能的最低费用作为功能的目标成本,以功能目标成本为基准,通过与功能现实成本的比较,求出二者的比值和二者的差异值,然后选择功能价值低,改善巨大变化期望值大的功能作为价值工程活动的重点对象的活动被称之为A功能价值B功能成本C功能定义D功能评价17.在设备租赁与购买方案的经济比选中,若设备寿命不同,则评价方法应选择A净现值法B年金法C年值法D附加率法18.在单因素敏感性分析中,如果主要分析产品价格波动对方案超额净收益的影响,则可选用()为分析指标A投资回收期B财务内部收益率C财务净现值D都可以19.凡是由过去交易或事项所形成,并为企业所拥有或控制,能够以货币计量并预期能给企业带来未来经济利益的经济资源,都应当作为企业的()A长期投资B投资C资产D所有者权益20在正常的施工技术组织条件下,完成单位合格产品所必须的劳动消耗量标准被称为()A施工定额B人工定额C基础定额D管理定额21.利用未到期应收票据向银行融资的做法,称为A应收票据贴现B银行贴现C抵押贷款D短期借款22.以下不计提折旧的固定资产为A土地B大修理停用的设备C职工宿舍D季节性停用的机械设备23.企业经股东大会或类似机构批准按规定的比例从净利润中提取的盈余公积是A法定盈余公积B任意盈余公积C法定公益金D其他资本公积24.在一个会计年度内完成的施工承包合同,应当在()确认合同收入与合同费用A发生时B会计期未C合同约定的结算时间D完成时25.施工企业非经常性的、兼营的业务所产生的收入是A营业收入B主营业务收入C营业外收入D其他业务收入26.当建设工程竣工验收时,为了鉴定工程质量,对隐瞥工程进行必要的开挖和修复,费用应从()支付A建设单位的基本预备费B建设单位管理费C施工企业管理费D预施工企业措施费27.财务活动是指()A企业再生产过程中的资金运动B筹资活动C投资活动D分配活动28.当企业在多种筹资方式中选择其一时,应选择资金成本最低的方式,这时可使用()资金成本进行比较A综合资金成本B加权平均资金成本C个别资金成本D总资金成本29.以下那种形式被视为典型的商业信用形式A应收账款B票据贴现C应付票据D预收账款30.银行向企业发放借款时,先从本金中扣除利息部分,到期时借款企业再偿还全部本金的一种计息方法是()A收款法B付款法C贴现法D计息法31.一个企业只能选择一家银行的一个营业机构开立一个()账户A一般存款B基本存款C短期借款D现金存款32.企业应当定期和不定期地进行现金盘点,确保现金账面余额与实际库存相符。

工程经济课后答案(Engineering economy after the answer)The first chapter1. what is the engineering economics?Answer: is the principle and method of engineering economy analysis based on knowledge engineering and economics integration and the formation of engineering economy, technology of various projects to complete the project target, economic evaluation, comparison, select the technology advanced and feasible scheme, which provides a practical science of science the basis for correct investment decision.2. how to understand the engineering economy from the broad sense of the object?Answer: the project is in the charge of the generalized specific management subject, including the whole series of activities of managed objects and management means, the.3. what are the characteristics of engineering economics?Answer: engineering economy is the interdisciplinary science engineering technology and economic accounting combination, is a comprehensive science and natural science and social science closelyblends, is a applied science directly linked to a production and construction, economic development. It has the following characteristics:(1) theory and practice. (2) quantitative and qualitative analysis. (3) analysis system analysis and balance. (4)statistical prediction and analysis of uncertainty.What is the significance of the 4. engineering economic analysis?Answer: (1) engineering economic analysis is the effective guarantee to improve the rational use of resources project. (2) engineering economic analysis is an effective way to reduce the project investment risk. (3) engineering economics is a bridge linking technology and economy.The second chapter1. how to understand the investment and assets?Answer: investment, in a certain sense refers to the future in order to gain or to avoid the risk of the funds, funds prior to advance and economic behavior. According to the degree of formation of real assets and direct relationship, can be divided into direct investment and indirect investment. According to the formation of real assets, can be divided into investment in fixed assets, floating assets investment, the investment of intangible assets and deferred assets investment.Assets, is the enterprise owned or controlled by money value economic resources including all property, rights and other rights. Including fixed assets, current assets, intangible assets and deferred assets.2. what is the fixed assets, intangible assets, deferred assetsand current assets?Answer: (1) refers to the use of fixed assets for more than 1 years, the unit value is above the prescribed criteria, and maintain the original physical assets in the process of using.(2) intangible assets refers to no matter, but the long-term benefit of the asset owner. (3) deferred assets refer to cannot be accounted into current profit and loss, the fee shall be amortized in future years amortization. (4) current assets refer to in 1 years or the realization of an operating cycle of more than 1 years or use of assets.3. of the total cost which consists of several?Answer: the total cost of the manufacturing cost of the products (production cost) and cost during the period of composition. The manufacturing cost includes direct materials, direct wages and other direct expenses and manufacturing cost etc.. Period costs include administrative expenses and financial expenses, sales expenses.4. how to distinguish between fixed and variable cost?Answer: (1) the fixed cost refers to a certain scale of production within the limits, and not change with the production cost. The characteristics of these costs is the product yield is increased, the total cost remains unchanged, which reflects increased in the unit product cost.(2) the variable cost refers to the cost of the product with the product yields and in proportion to the increase or decreasethe cost of raw materials, such as direct costs, direct fuel and power costs, packaging fees. The characteristics of these costs is the change of product yield, the total cost is proportional to change, and reflected in the unit product cost in cost is fixed.The relationship between the 5. sales revenue, profits and taxes?Answer: sales revenue is the realization of enterprise capital recovery or advance capital appreciation, it is the monetary expression of production enterprises. The profit is the ultimate achievement of enterprises of all production and business activities in a certain period of time.Tax refers to all kinds of enterprises in tax according to the provisions of the state tax law paid to the state, is an important way for enterprises to provide the accumulation of national.Total profit = - product sales tax and additional sales profit + + net investment income + non business income - operating expensesThe third chapterWhat are the types of expressions 1, economic benefits?Answer: (1) the difference between representation E = V - C(2) E = ratio representation(3) E * 100% = percentage methodWhat is the 2, setting up economic benefit indexes and index system of the effect?Answer: the engineering economic analysis, demonstration, evaluation and selection of the project, all need to measure the scale and standard. This is the standard scale and index, economic benefit index. Because of the complexity of engineering economy, compared with only one or two indicators, sometimes is not enough. At the same time must be using a number of indicators, including indicators of economic indicators and general technology, compared to the analysis from different angles, in order to evaluate the whole picture, to provide the scientific basis for project decision making. Target group set up a number of interrelated and mutual restraint, constitutes an indicator system for evaluating the economic benefits.3, in the engineering economic analysis why we emphasize the comparability principle?Answer: in engineering economic analysis, in addition to the project itself on individual income and expense analysis and evaluation, and more important to determine the economic benefits of the advantages and disadvantages is the comparative analysis between the project plan, so as to determine a project technical and economic benefits of the pros and cons.4, what is the time value of money?Answer: the time value of capital, refers to funds in the process of production and circulation, with the passage of time can produce value-added, the value-added part is called the time value of money.The relationship between the 5, the nominal interest rate and real interest rate?A: so, when the time unit of interest and the interest period is consistent, the real interest rate and nominal interest rate is the same, and equal to the interest rate cycle; when the unit of time and the actual interest rate calculation cycle, the nominal interest rate is equal to the product of an interest rate cycle and a year in the calculation period, and the actual the interest rate equals the nominal interest rate plus interest rates generated by the time value.6, in the project of cash flows have?Answer: (1) investment in fixed assets and loan interest (2) capital investment (3) operating costs (4) sales revenue (5) profit (6) (7) tax subsidies (8) new investment in fixed assets and working capital investment (9) recovery net residual value of fixed assets (10) recovery flow capital7, a project investment of 1 million yuan, third years to start production, need 3 million yuan of liquidity, after put into production, annual sales revenue to offset operating costs 3 million yuan after fifth years, an additional investment of 5 million yuan, and the annual sales income offset when effective operating costs 7 million 500 thousand yuan, the economic lifeof the project is 10 years, residual 1 million yuan, to draw a map of the cash flow of the project?Solution:8, what is the capital equivalent? What are the factors that affect the equivalent of money?Answer: (1) capital equivalent refers to the consideration of time factor, the conversion of cash flow in different time occurred in varying amounts at the same time, in order to meet the balance of payments than at the time of the request. That at any time according to certain interest rate conversion funds for another particular point a different amount of money, but it also points to two different amount of money on the economy is equal, equal economic value, which is the equivalent of money.(2) there are three main factors affecting the equivalent amount of money funds, namely the size of the length of time; capital movement occurs; interest rate.9. investment needs of a project, now to bank loans for 1 million yuan, the annual interest rate is 10%, the loan period of 5 years, a time to pay off. How much is the end of fifth a repayment of bank funds?Solution: (1) draw cash flow chart(2) calculationF = P = P (F/P, i,n) = 100 (f / p, 10%, 5) = 100× 1.6105 = 161.05 (万元)答: 5年末一次偿还银行本利和161.05万元.10. 某工厂拟在第5年年末能从银行取出2万元, 购置一台设备, 若年利率为10%.那么现在应存入银行多少钱?解: (1) 作图(2) 计算p = f = f (p / f, i, n) = 2 (p / f, 10%, 5) = 2× 0.6209 = 1.2418 (万元)答: 现在应存入银行的现值为1.2418万元.11. 某项改扩建工程, 每年向银行借款为100万元, 3年建成投产, 年利率为10%, 问投产时一次还款多少钱?解: (1) 作图(2) 计算f = (a (f / a, i, n) (f / p, i, n) = 1000 (f / a, 10%, 3) (f / p, 10%, 1) = 100×3.310× 1.10 = 364.1 (万元)答: 投产时需一次还清本利和364.1万元.12. 某工厂计划自筹资金于5年后新建一个生产车间, 预计需要投资为5 000万元, 若年利率为5%, 从现在起每年年末应等额存入银行多少钱才行?解: (1) 作图(2) 计算a = f = f (a / f, i, n) = 5000 (a / f, 5%, 5) = 5000× 0.181 = 905 (万元)答: 每年年末应等额存入银行905万元.13. 某项投资, 预计每年受益为2万元, 年利率为10% 时, 10年内可以全部收回投资, 问期初的投资是多少钱?解: (1) 作图(2) 计算p = a = a (p / a, i, n) = 2 (p / a, 10%, 10) = 2× 6.1446 = 12.2892 (万元)答: 期初投资为12.2892万元.14. 某项工程投资借款为50万元, 年利率为10%, 拟分5年年末等额偿还, 求偿还金额是多少?解: (1) 作图(2) 计算a = p = p (a / p, i, n) = 50 (a / p, 10%, 5) = 50× 0.2638 =1.19 (万元)答: 偿还金额是13.19万元.15、某借款金额1万元, 利率8%, 分5年于年末等额偿还, 问每年的偿付值? 若在每年初偿还, 每期偿付值又是多少?解: (1) 作图图1.年末等额偿还图2.年初等额偿还(2) 计算①a = p (a / p, i, n) = 1 (a / p, 8%, 5) = 0.2505万元②p = a + a (p / a, i, n)a = = 0.2319万元答: 若年末等额偿还, 每年偿还0.2505万元, 若在每年初偿还, 每期偿还0.2594万元.16、某项目第1 ~ 4年平均投资50万元, 第4年建成投产, 年净收益40万元, 第5 ~ 10年生产达产后年均净收益70万元.第11 ~ 12年生产约有下降, 年均净收益50万元, 在年利率8% 时, 求终值、现值、第4年期末的等值资金?解: (1) 作图(2) 计算p = - 50 + (- 50) (p / a, 8%, 3) + 40 (p / f, 8%, 4) + 70 (p / a, 8%, 6) (p / f, 8%, 4) + 50 (p / a, 8%, 2) (p / f, 8%, 10) = 129.6142万元f = p (f / p, 8%, 12) = 326.3686万元f = p (f / p, 8%, 4) = 176.2753万元第四章1. 某建设项目方案表明, 该项目在建设的第一年完工, 投资为10 000元, 第二年投产并获净收益为2 000元, 第三年获净收益为3 000元, 第四年至第十年获净收益为5 000元, 试求该项目的静态投资回收期.解: (1) 作图(2) 计算- = 10000 + 2000 + 3000 + 5000 = 0p = 43. 某项目的各年金现金流量如表4 - 17所示, 收益率在15% 时, 试用净现值判断项目的经济性. (表4? - 17见书p95)解: (1) 作图(2) 计算npv = = -40-10 +8 (p / a, 15%, (2) p / f, 1 to 15%, +13 (p / a), 16 (15%), p / d, 3 (15%) +33 p / f, 15%, 20)0.0611 = -40-10×0.8696+8×1.6257×0.8696+13×5.9542×0.6575+33×合理 15.52 > = 04. 甲、乙两项目的有关费用支出如表4 - 18所示, 在收益率为10% 时, 试用费用现值法选择方案. (表4? - 18见书p95)解: (1) 作图(2) 计算pc = 800 +320 (p / a, 1, 9) (1+0.1)800×0.9091+320×5.759× 2402.64 0.9091 = =pc = 900 +300 (p / a, 1, 9) (1+0.1)900×0.9091+300×5.759× 2388.84 0.9091 = =因此乙方案好 > pc pc5. 某方案需要投资为1 995元, 当年见效年收益为1 500元, 年成本支出为500元, 第四年有1 000元追加投资, 服务期为5年, 在收益率为10% 时, 用净现值率法评价方案.解: (1) 作图(2) 计算npv = -1995-1000 (1+0.1) + (1500-500 (p / a), 0.1, 5)-1995-753.3+1000× 1042.5 3.7908 = =1995+1000 (r = = = 2748.3 1995+753.3 1+0.1)npvr = = > 10 合理 is 0.38%.6. 某项目需要投资为2万元, 经济寿命为5年, 残值为0.4万元, 每年收益为1万元, 每年支出成本费用为0.44万元, 若基准收益率为8%, 用效益成本比率法确定方案是否可取?解: (1) 作图(2) 计算1 = (p / a, 8%, 5 +0.4 (p / f), 8%, 5) = = 4.265 3.9927+0.4× 0.68062+0.44× 3.757 3.9927 = =b /c = = 1.1352此方案可取, 除收回投资外, 还可获得相当于投资总成本现值总额0.1352倍的净值.7. 某投资项目, 投资额为1万元, 在5年中每年的平均收入为0.6万元, 每年的费用支出为0.3万元, 期末残值为0.2万元, 若投资收益率为10%, 试用净未来值法评价方案.解: (1) 作图(2) 计算-1 nfv (f / p = 0.1, 5, +0.3 (f / a), 0.1, 5) +0.2-1.611+0.3×6.105+0.2 0.4205 = = > 0因此该方案可行8. 某项目投资为700万元, 每年的净收益均为200万元, 寿命期为5年, 基准收益率为10%, 试用内部收益率判断方案.解: (1) 作图(2) 计算设npv - 700 + 200 = (p / a, i, 5) npv = 0(p / a, i, 5) = 3.5% 可以作为比较值查表可知12 与15%.i = 12% npv = 200 - 700 + (p / a, i, 5) = > 0 20.96i = 15% npv = 200 - 700 + (p / a, i, 5) = -29.56 < 0i = 0.12 + (13.2%) 0.15-0.12) = > 可行9. 有两个投资方案a和b, 其投资分别为1.8万元和1.6 万元, 年净收益分别为0.34万元和0.3万元, 项目寿命期均为20年, 基准收益率为10%, 用差额投资收益率比较方案.解: (1) 作图(2) 计算the - b, - 0.2. 04. 04. 04.判断方法如上题:i = 15% npv = - 0.2 +. 04 (p / a, 15%, 20) = 0,05 > 0i = - 0.2 to 20% npv = + 0.04 (p / a, 20%, 20 -0.005 < 0) =i '= 0,15 + (0.2-0.15) x = 19.5% > i 则投资大的方案a优10. 某项目总产量为6 000吨, 产品售价为1 335元 / 吨, 其固定成本为1 430 640元, 单位可变成本为930.65元.试求盈亏平衡点产量和盈亏平衡点时的生产能力利用率. (分别用计算法和作图法求解).解: (1) 作图法①画直角坐标图②在纵坐标轴上找点b, c, s, f.已知: b = 1430640元, f = b则c = b + vq = 1430640 + 930.65×6000 = 7014540元s = pq = 1335×6000 = 8010000元③连接fb, fc, os三线.④找出fc与os的交点g, 其对应的产量为3500吨, 即为所求盈亏平衡点产量(2) 计算法bep = = = 3538.123吨bep = ×100% = ×100% = 58.97%11. 生产某种产品有三种工艺方案, 采用方案a, 年固定成本为800万元, 单位变动成本为10元; 采用方案b, 年固定成本为500万元, 单位变动成本为20元; 采用方案c, 年固定成本为300万元, 单位变动成本为30元.用盈亏平衡法分析各种方案适用的生产规模.解:a: c = 800 + 10q(b: c = 500 + 20qc: c = 300 + 30qc = c 800 + 10q = 500 + 20q(c = 800 + 10q = 1100)c = c 500 + 20q = 300 + 30qq = 20(c = 500 + 20q = 900).c = c 800 + 10q = 300 + 30qq = 25(c = 300 + 30q = 1050)q < 20时方案c优20≤q≤30时方案b优q > 30时方案a优12、某项目设计年生产能力为10万吨, 计划投资需要1800万元, 建设期1年, 产品销售价格为63元 / 吨, 年经营成本为250万元, 项目寿命期为10年, 残值60万元, 收益率为10%.试就投资额, 产品价格、经营成本等影响因素对投资方案进行敏感性分析?解:(1) 作图投资回收期法:pt = + 1 = + 1 = 5.74用投资回收期进行敏感性分析20% 10% 0 -10 -20%%投资额 6.68 annex 7.1 5.74 5.26 4.79产品价格 4.56 5.06 5.74 6.68 $8.09经营成本 6:45 6.07 5.74 5.44 5.19净现值法:npv = 1800 + (630 - 250) (p / a, 10%, 9) (p / f, 10%, 1) + 60 (p / f, 10%, 10)= - 1800 + 380×5.759× 0.9091 + 60× 0.3856 = 212.626万元+ 20% + 10% 0 - 10% - 20%投资额 -147.374 32.626 212.6 392.626 572.626产品价格 872.3 542.5 212.6 - 117.2 - 447.1经营成本 - 49.1 81.7 212.6 343.5 474.4第五章1、为什么说工程项目方案的比较是工程经济分析的重要内容?答: 由于工程项目方案受技术、经济和外部环境等其他相关因素的联系和影响, 使方案的决策变得复杂, 要对比较方法和评价指标进行有效选择, 才能选出相对最佳方案, 作出科学的投资决策.2、什么是独立方案, 互斥方案、相关方案?Answer: (1) in a series of alternative projects, if accept a solution does not affect the adoption of the plan, known as the independent scheme, or completely independent scheme.(2) select a program in a number of alternatives, it excludes the adoption of all other schemes, this type of program is called mutual exclusion scheme.(3) in each project, which uses a program will bring a certain impact on the cash flow of other programs, thereby affecting the other scheme adopted or refused, in this relationship in the scheme is called correlation scheme.3, the NPV, IRR, IRR index in the selection scope and evaluation criteria?Answer:indexThe application of NPV IRR IRRAn independent project feasibility judgment and selection criteria can be considered acceptable to all (calculated in accordance with the provisions of the discount rate) independent project NPV 0 can be considered to accept all IRR Benchmarks (or regulations) yields independent projects not applicableTwo, scheme comparison (exclusive plan preferred) no financial constraints, choose the larger NPV generally do not directly use, instead of IRR, when the IRR I benchmark rate of return, with greater investment benchmark is the optimal plan (or set) rate of return, investment selection scheme, otherwise, choose a small investment scheme.Three, the project queuing (optimal combination of independent projects) and exhaustive scheme combination according to the investment (or incremental) order from small to large, and then use the appropriate opportunity cost for the calculation of NPV, the rate of discount compared to 11, according to the principle of sorting is better and exhaustive scheme combination according to the investment (or incremental), ascending sort the calculation of adjacent combination of IRR, according to the IRR benchmark rate of return (or opportunity cost) when the investment was superior to the principle of one by one comparison sort must first sorted according to the investment amount of order, and then turn on the adjacent 22, until the best project.4, in the selection of scheme of NAW, PC and AC, how to select indicators?Answer: the net benefit annual value method for scheme selection, should be carried out to calculate the comparison scheme of AW, to the larger value of AW is the optimal plan. In the comparison of schemes should choose the low cost present value PC or AC low cost scheme.5, a proposed project has three independent investment portfolio, the data are listed in the following table, if the maximum investment limit of 100 million yuan, the investment rate of return of not less than 15%, ask how to make a decision? (VPV) (see page 111)Solution: because the maximum investment limit of 100 million yuan so that only the following four mayScheme ANPV = -2000+1200 (P/A, 15%, 3) = 7 million 398 thousand and 400 yuanScheme BNPV = -6000+3000 (P/A, 15%, 3) = 8 million 496 thousand yuanScheme CNPV = -10000+4000 (P/A, 15%, 3) = -867.2 yuanScheme ABNPV = -8000+4200 (P/A, 15%, 3) = 15 million 894 thousand and 400 yuanSo the selection scheme of ABThe sixth chapter1, what is the tangible and intangible abrasion of equipment?Answer: (1) the role of the force in the process of using the equipment, parts of friction, vibration and fatigue phenomenon resulting in equipment entity wear, the wear is called the first tangible.(2) the so-called invisible wear, is due to the progress of science and technology and the emergence of more perfect performance, high production efficiency of the equipment, so that the original equipment value is reduced; or production equipment has the same structure value does not depend on the initial production cost, but depends on the production cost, and this cost is falling.2 equipment, tangible and intangible abrasion and wear how to measure?Answer: tangible expression (excluding interest) for:Type: tangible equipment wear degree;C - repair all parts for repairs;In determining the wear degree of equipment, the equipment value of reproduction.Wear invisible expressions (without interest) for:Type: - Equipment invisible wear degree;K0 equipment cost;Ks - (consider two kinds of invisible wear value of reproduction equipment).Comprehensive wear (residual value of two kinds of wear occurred at the same time after) for:- after the residual value of tangible equipment- after the residual value of tangible equipment3, why should compensate for the equipment wear?Answer: to reduce the wear caused by the original equipment value.4, equipment wear and wear compensation of what?Answer: the equipment wear forms: to eliminate visible wear - repairCan not eliminate the physical wear replacementInvisible -- wear of the transformation and renewal of secondWhat is the meaning of 5, updating equipment?Answer: to a new device instead of physically unable to continue using the old equipment and the economy should not continue to use the.6, the equipment depreciation rate impact on the enterprise?Answer: if the rate of depreciation provisions is too low, the equipment use expires, still does not have the value of the equipment all transferred to the product, is not sufficient to compensate the consumption of equipment, affecting the normal development of the enterprise, artificially expand profits, false exaggerated accumulation, the results not only make the equipment not timely updated, and false arrange the reproduction of investment. If the depreciation rate is set too high, the actual loss of depreciation for equipment spare, will artificially reduce profits, affect the normal accumulation of funds, impede the expansion of reproduction.7, what is the technology of life and natural life, the economic life of equipment?Answer: (1) the natural life of tangible economic equipment after wear and loss of technical performance and service performance, and fix the value of time.(2) the technology life refers to the equipment due to the performance and benefits of intangible wear and poor, continueto use uneconomical and no transformation of the value in the economic time.(3) the economic life of equipment refers to the use of a certain time, comprehensive visible and invisible friction caused by poor economic benefits, it is uneconomical to continue to use, and no overhaul and transformation of the value of the time.8, a factory purchased a new equipment to 50 thousand yuan, the use of a period of 10 years, the value of 0.15 yuan. The trial straight-line depreciation method, the use of computing devices to second years and eighth years total amount of depreciation method and double declining balance method?Solution:The straight-line method: D = x = 2 * 2 = 9 thousand and 700 yuanD = x = 8 * 8 = 38 thousand and 800 yuanThe total length: D = (P - S) = (5 - 0.15) = 7 thousand and 940 yuanD = (P - S) = (5 - 0.15) = 2 thousand and 650 yuanDouble declining balance method: r = 2 * * 2 = = 0.2D = rP (1 - R) = 0.2 x 5 x (1 - 0.2) = 8 thousand yuanD = rP (1 - R) = 0.2 x 5 x (1 - 0.2) = 2 thousand and 100 yuan10, the equipment purchase cost is 6000 yuan, the first year of the equipment operation cost is 400 yuan, after inferior equipment annual added value of 300 yuan, without consideration of the equipment for the residual value of its economic life?Solution: y = 400+ (T-1 +)= = - 0R T = = 6 yearsThe seventh chapter1, the project feasibility study and why?Answer: (1) the feasibility study is the basis for investment decision.(2) the feasibility study is determined on the basis of the construction project and the preparation of the book design.(3) the feasibility study is the construction project financing and bank loans to the basis.(4) the feasibility study is to sign the contract and agreement with the relevant units on the basis of.(5) the feasibility study is the basis for project construction license.(6) the foreign project feasibility study is the basis of the introduction of foreign technology, equipment and resources as well as foreign negotiation and signing contract.(7) construction project feasibility study is to further supplement and improve the basic information and carry out the experiment and Research on the basis of. As a further collection of design and construction data and carry out the middle test and industrial test etc..What are the 2 and the feasibility of the working procedure?Answer: (1) clear objectives(2) signed on the contract.(3) the investigation of market investigation and resources.(4) preferred sites, technical scheme, determine the production process.(5) determine the product plan, enterprise scale, organization, staffing and equipment selection.(6) prepare the project implementation schedule.(7) economic benefit analysis.(8) the feasibility research report.(9) the decision-making departments for approval.3, what is the financial evaluation?Answer: the financial evaluation, economic evaluation is also known as the enterprise, in the current taxation system and price system condition, analysis and calculate the project's financial profitability and solvency from the financial point of view, in order to determine the financial viability of the project.4, what is the national economic evaluation?Answer: the evaluation of the national economy, is in the premise of rational allocation of national resources, to analyze and calculate the net contribution to the national economy from the angle of the whole country, with economic rationality to judge project.。

技术经济学概论(第二版)习题答案第二章经济性评价基本要素1、答:资金利润率、利率。

2、答:固定资产投资和流动资产都是生产过程中不可缺少的生产要素,二者相互依存,密不可分。

二者的区别在于:(1)固定资产投资的结果形成劳动手段,对企业未来的生产有着决定性影响,而流动资产投资的结果是劳动对象,而且流动资产投资的数量其结构是由固定资产投资的规模及结构所决定的。

(2)固定资产投资从项目动工上马到建成交付使用,常常要经历较长的时间。

在这期间,只投入,不产出,投入的资金好像被冻结。

而流动资产投资,一半时间较短,只要流动资产投资的规模与固定资产投资规模相适应,产品适销对路,流动资产投资可很快收回。

3、答:机会成本、经济成本、沉没成本都是投资决策过程中常用到的一些成本概念。

机会成本:指由于将有限资源使用于某种特定的用途而放弃的其他各种用途的最高收益,并非实际发生的成本,而是由于方案决策时所产生的观念上的成本,对决策非常重要。

例如:某企业有一台多用机床,将其出租则获得7000元的年净收益,自用则获得6000元的年净收益。

若采用出租方案,则机会成本为自用方案的年净收益6000元;若采用自用方案,则机会成本为出租方案的年净收益7000元。

经济成本:是显性成本和隐性成本之和。

显性成本是企业所发生的看得见的实际成本,例如企业购买原材料、设备、劳动力支付借款利息等;隐性成本是企业的自有资源,是实际上已投入,但形式上没有支付报酬的那部分成本,例如:某人利用自己的地产和建筑物开了一个企业,那么此人就放弃了向别的厂商出租土地和房子的租金收入,也放弃了受雇于别的企业而可赚得的工资,这就是隐性成本。

沉没成本:指过去已经支出而现在已经无法得到补偿的成本,对决策没有影响。

例如:某企业一个月前以3300元/吨的购入价格钢材5000吨,而现在钢材价格已降为3000元/吨,则企业在决策是否出售这批钢材时,则不应受3300元/吨购入价格这一沉没成本的影响。

《工程经济学》课后习题答案第一章工程经济学概论1.简述工程与技术之间的关系。

解答:工程是人们在长期的生产和生活实践中,综合应用科学理论和技术手段去改造客观世界的具体实践活动,以及所取得的实际成果。

技术是人类活动的技能和人类在改造世界的过程中采用的方法、手段,是创造和发明。

关系:一项工程能被人们接受必须具备两个前提,即技术的可行和经济的合理。

一项成功的工程项目除了要在技术上可行外,还要产生预期的效益。

2.什么是经济?什么是工程经济学?解答:对经济的理解一般有以下四种含义:(1)经济是生产关系、经济制度与经济基础;(2)经济是指一个国家国民经济的总称;(3)经济是社会的物质生产和再生产过程;(4)经济包含节约、节省的意思。

工程经济学是工程与经济的交叉学科,是研究工程设计和分析的效益和费用,并对此进行系统计量和评价的学科。

也就是说,工程经济学是研究工程技术实践活动经济效果的学科。

它以工程项目为主体,将经济学原理应用到与工程经济相关的问题和投资上,以技术一经济为核心,研究如何有效利用资源提高经济效益。

3.工程经济学的研究对象是什么?解答:工程经济学的研究对象是工程项目的经济性。

工程经济学从技术的可行性和经济的合理性出发,运用经济理论和定量分析方法研究工程技术投资和经济效益的关系。

4.工程经济学的主要特点有哪些?解答:(1)综合性——工程经济学是跨自然科学和社会科学两个领域的交叉学科,本身就具有综合性。

(2)实践性——工程经济学的理论和方法是对实践经验的总结和提高,研究结论也直接应用于实践并接受实践的检验,具有明显的实践性。

(3)系统性——在对一个经济单位进行研究时,要将其放在整个国民经济这个大系统中进行研究。

(4)预测性——建设一个工程项目之前,一般要对该项目进行可行性研究,判断该项目是否可行。

(5)选择性——工程经济分析过程就是方案比较和选优的过程。

(6)定量性——定量分析与定量计算是工程经济学的手段。

中国农业大学网络教育学院土木工程系091工程经济学答案考试类2009-07-03 14:29:39 阅读379 评论0 字号:大中小订阅

1、价值工程的核心是()

A.以最低的总费用,实现产品必备功能

B.有组织的活动

C.对作业进行功能分析

D.VE的对象选择

参考答案:A 您的答案:A

2、某住宅开发项目,市场预测售价为2300元/㎡,变动成本为900元/㎡,固定成本为500万元,综合销售税金为150元/㎡。

此项目最少应开发()㎡商品住宅面积才能保本。

A.6500

B.4000

C.5420

D.4635

参考答案:B 您的答案:B

3、银行一年定期储蓄年利率为1.98%,利息税税率为20%,假定通货膨胀率为2.8%,一年定期储蓄的实际利率(年有效利率)为()

A.1.98%

B. 1.584%

C.-1.216%

D.4.384%

参考答案:C 您的答案:C

4、若名义利率一定,年有效利率与一年中计息周期数m的关系为()

A.计息周期增加,年有效利率不变

B.计息周期增加,年有效利率减小

C.计息周期增加,年有效利率增加

D.计息周期减小,年有效利率增加

参考答案:C 您的答案:C

5、从现在起每年年初存款1000元,年利率12%,复利半年计息一次,第5年年末本利和为()元

A.13181

B.6353

C.7189

D.14810

参考答案:C 您的答案:C

6、某人储备养老金,每年年末存款100元,年利率为8%,则20年后他的养老金总额为()

A.4506.2

B.4670

C.4576.2

D.4500

参考答案:C 您的答案:C

7、年有效利率大于名义利率,是因为()

A.计息周期小于一年时

B.计息周期等于一年时

C.计息周期大于一年时

D.计息周期小于等于一年时

参考答案:A 您的答案:A

8、某企业向银行借款,有两种计息方式:一种为年利8%,按月计息;另一种为年利8.5%,半年计息,则企业应选择的有效利率为()

A.8.3%

B.8%

C.8.5%

D.9.2%

参考答案:A 您的答案:B

9、在经济评价中,一个项目内部收益率的决策规则是()。

A.IRR低于基准利率,则投资;

B.IRR大于或等于基准利率,则投资;

C.IRR>0,则投资;

D.IRR<0,则投资

参考答案:B 您的答案:B

10、对于企业采用融资方式租赁设备来说,下列说法中错误的是()。

A.融资租赁适用于长期使用的贵重设备

B.企业可以随时通知对方取消租约

C.企业可以降低技术过时的风险

D.企业不可以处置租赁设备

参考答案:B 您的答案:B

11、某建材厂设计能力为年生产某型号预制构件7200件,每件售价5000元,该厂固定成本680万元,每件产品变动成本为3000元,则该厂的盈亏平衡产量为()。

A.3500

B.3000

C.4420

D.3400

参考答案:D 您的答案:D

12、敏感性分析中评价指标的确定,一般根据项目实际情况而选择。

如果主要分析投资大小对方案资金回收能力的影响,则选用()作为分析指标。

A.投资回收期

B.项目投资收益率

C.财务净现值

D.财务内部收益率

参考答案:A 您的答案:A

13、价值工程中的总成本是指()。

A.生产成本

B.使用成本

C.使用和维护费用

D.产品寿命成本

参考答案:D 您的答案:D

14、对于产出不同的投资方案进行评价,其评价原则是()。

A.比较内部收益率的大小

B.比较净现值的大小

C.比较年度等值的大小

D.投资增额的内部收益率是否大于基准贴现率

参考答案:D 您的答案:D

15、财务净现值( )。

A.反映投资方案的获利能力

B.是动态评价指标

C.是静态评价指标

D.是把计算期间内各年净现金流量折现到投资方案开始实施时的现值之和

E.是投资效率指标

参考答案:A, B, D 您的答案:

16、基准收益率可以是( )。

A.企业确定的最低标准的收益水平

B.行业确定的最低标准的收益水平

C.投资者确定的最低标准的收益水平

D.银行贷款利率

E.判断投资方案在经济上是否可行的依据

参考答案:A, B, C, E 您的答案:

17、下列有关盈亏平衡分析的说法中,正确的是( )。

A.根据生产成本和销售收入与产销量之间是否为线性关系,盈亏平衡分析可分为线性盈亏平衡分析和非线性盈亏平衡分析

B.当企业在小于盈亏平衡点的产量下组织生产,则企业盈利

C.全部成本可以划分成固定成本和变动成本,借款利息应视为变动成本

D.一般来讲,盈亏平衡分析只适用于项目的财务评价

E.盈亏平衡分析不能揭示产生项目风险的根源

参考答案:A, D, E 您的答案:

18、下列指标中与资金时间价值有关的指标有()。

A.投资收益率

B.净现值率

C.投资利润率

D.内部收益率

E.利息倍付率

参考答案:A, B, D 您的答案:

19、建筑安装工程费用项目的组成包括()。

A.直接费用

B.间接费用

C.企业管理费

D.税金

E.利润

参考答案:A, B, C, D, E 您的答案:

20、下列哪些是定量预测法()

A.时间序列预测法

B.回归分析法等。

C.德尔斐法

D.专家个人预测法

参考答案:A, B 您的答案:。