ACCA F8知识点讲解:梳理审计流程

- 格式:doc

- 大小:35.17 KB

- 文档页数:2

【ACCA考前辅导】F8 考点分析(审计风险+风险评估程序)“定义和评估审计风险是审计程序中非常重要的一个部分,在F8历年的考试中,主要以两种形式出现,第一简答题,要求解释一些基本的概念,第二案例题,会给一些具体的案例来给予分析,要求学生写出风险点,以及审计师的应对,本文基于考官的文章,主要讲述了以下几方面的内容:”一:什么是审计风险,如何定义的?二:风险评估程序(Risk assessment procedures)(一)什么是审计风险。

The risk that the auditor expresses an inappropriate audit opinion when the financial statements are materially misstated. Audit risk is a function of material misstatement and detection risk.所谓的审计风险,是指审计师在客户的财务报告存在着重要的错报时,发表了不恰当的审计意见,它主要包括了两块的内容,1.财务报表本身的错报和漏报,2.在检查时出现的风险。

定义的内容在2008年12月的考试里,作为直接的简答题出现了,在之后的考试里,再没有出现过简答题,但作为Syllabus里所要求的一个的重要知识,依旧要求学生熟练的背诵,了解这句话的具体定义,这有助于帮助他们理解审计风险,并且应用到具体的案例题里面。

(二)风险评估程序(Risk assessment procedures)1. ISA 315 requires auditors to perform the following procedures to obtain an understanding of the entity and its environment, including its internal control:。

从CPA的角度带你轻松解读ACCA F8一、审计的一些概念1审计是什么?分为政府审计、企业内部审计、注册会计师审计三类。

其中注册会计是审计是有偿审计,其他都不是。

1)政府审计:主要是检查各级政府机构和国有企业的收支情况。

由国家审计署执行。

审计不都是“查问题”为主的,政府审计可能查出的问题会多些,但也并不是查不出问题就不罢休。

没查出问题/查不出大问题,也算是反过来证明这个政府机构工作比较合规。

2)注册会计师审计:也叫独立审计,是由于企业所有权和经营权的分离,及人类道德上的普遍不健全和大脑功能的普遍不完善而产生的。

A也不是查问题为主的,独立审计更像是在解一道几何证明题。

已知条件:企业的经营情况和财务会计记录,要求证明:管理层所提交的会计报表是真实可靠的。

B独立审计:是一种受托审计,即某一方(一般是企业所有者)受托审计师按照事先约定的步骤和目标对被审计的单位进行审计,而且是有偿的。

所有者通过审计师监督管理者的机制里,有个假设前提:审计师是值得信任的。

正是居于这份信任,所有者会接受审计师的检查结果。

这个结果一般用一份《审计报告》来表达。

只有在审计师检查过管理者的工作,认为会计报表是真实可靠的时,审计师才会出具审计报告(即对管理者所编制的会计报表做一个适当的保证),将别人对自己的信任,背书转让给管理者。

即:审计师得了所有者付出的审计费,就有责任证实/证伪所有者对于管理者的怀疑。

3)企业内部审计:企业内部设置的,检查内部各部门经营管理情况的一项职能。

企业内部审计,则是在做不同项目可能由不同的目的,有时是“查问题”,有时则是在做证明题。

4)独立审计与政府审计的比较异:A取得审计证据难易程度不同。

*独立审计:无国家权威支持,取证时受限较多,审计师(要通过一些间接手段)来取得(相对来说较为间接的)证据。

*政府审计:有国家权威支持,取证容易,只要想到从某个渠道来取得证据,就可以通过合适的方式来获得,尤其是从不同单位和公司取得同一事项的证据进行印证的时候。

Substantive procedures - Additions and disposalsAdditions-Obtain a breakdown of additions, and agree to the non-current asset register to confirm completeness of plant & equipment (P&E) .1.具体的breakdown与固资帐比查完整性-Select a sample of additions and agree cost to supplier invoice to confirm valuation.2.抽样与发票核对查价值-Verify rights and obligations by agreeing the addition of plant and equipment to a supplier invoice in the name of Pear. 3.查发票署名查权利与义务-For a sample of additions recorded in P&E physically verify them on the factory floor to confirm existence.4.查实体.存在性-Review board minutes to ensure that significant capital expenditure purchases have been authorisedby the board. 5.查董事会记录-Review the list of additions and confirm that they relate to capital expenditure items rather than repairs and maintenance. 6查费用化与资本化问题Disposals-Obtain a breakdown of disposals, cast the list and agree all assets removed from the non-current asset register to confirm existence. 1.具体的与总查存在-Select a sample of disposals and agree sale proceeds to supporting documentation such as sundrysales invoices. 2.无耻法查supporting documentation-Recalculate the profit/loss on disposal and agree to the income statement. 3.重计i nventory substantive procedures for balances at the year end.(i) ExistenceAssets, liabilities and equity interests exist.Substantive proceduresDuring the inventory count select a sample of assets recorded in the inventory records and agree to the warehouse to confirm the assets exist.Obtain a sample of pre year-end goods despatch notes and agree that these finished goods are excluded from the inventory records.(ii) Rights and obligationsThe entity holds or controls the rights to assets, and liabilities are the obligations of the entity.(iii) CompletenessAll assets, liabilities and equity interests that should have been recorded have been recorded. Substantive proceduresObtain a copy of the inventory listing and agree the total to the general ledger and the financial statements. During the inventory count select a sample of goods physically present in the warehouse and confirm recorded in the inventory records.(iv) Valuation and allocationAssets, liabilities and equity interests are included in the financial statements at appropriate amounts and any resulting valuation or allocation adjustments are appropriately recorded.Substantive proceduresSelect a sample of goods in inventory at the year end, agree the cost per the records to a recent purchase invoice and ensure that the cost is correctly stated.Select a sample of year-end goods and review post year-end sales invoices to ascertain if net realisable value is above cost or if an adjustment is required.Substantive proceduresDepreciation-Review the reasonableness of the depreciation rates applied to the new leisure facilities and compare to industry averages. depreciation rates 与同行业比较- Perform a proof in total calculation for the depreciation charged on the equipment, discuss with management if significant fluctuations arise. a proof in total AP- Select a sample of leisure equipment and recalculate the depreciation charge to ensure that the non-current asset register is correct. Recalculate the depreciation charge 为accuracy- Review the disclosure of the depreciation charges and policies in the draft financial statements.ACCURACY- Review profits and losses on disposal of assets disposed of in the year, to assess the reasonableness of the depreciation policies. profits and losses on disposal of assets 是否合理Food poisoning1- Review the correspondence from the customers claiming food poisoning to assess whether Pineapple has a present obligation as a result of a past event. 存在1- Send an enquiry letter to the lawyers of Pineapple to obtain their view as to the probability of the claim being successful.1- Review board minutes to understand whether the directors believe that the claim will be successful or not.2- Review the post year-end period to assess whether any payments have been made to any of the claimants. 数字3- Discuss with management as to whether they propose to include a contingent liability disclosure or not, consider the reasonableness of this.4- Obtain a written management representation confirming management's view that the lawsuit is unlikely to be successful and hence no provision is required. 发誓5- Review the adequacy of any disclosures made in the financial statements.trade payablesSubstantive procedures over year-end- Obtain a listing of trade payables from the purchase ledger and agree to the general ledger and the financial statements. 1 账户比数字- Review the list of trade payables against prior years to identify any significant omissions.1与去年比数字- Calculate the trade payable days for Greystone and compare to prior years, investigate any significant differences. 1计算payable ~@丫§比数字- Select a sample of goods received notes before the year-end and follow through to inclusion in the year-end payables balance, to ensure correct cut-off.-Review after date payments, if they relate to the current year 2 cutoff-Obtain supplier statements and reconcile these to the purchase ledger balances, and investigate anyreconciling items. 与供货方比较信息accuracy -Enquire of management their process for identifying goods received but not invoiced or logged in the purchase ledger and ensure that it is reasonable to ensure completeness of payables.询问对收到货但是未收到发票情况的处理方法-Review the purchase ledger for any debit balances, for any significant amounts discuss with management and consider reclassification as current assets. 数据出现异常与管理层讨论原因-Ensure payables included in financial statements as current liabilities. 无耻法正确做账directors' bonus and remuneration-Obtain a schedule of the directors' remuneration including the bonus paid and cast the addition of the schedule.-Agree the individual bonus payments to the payroll records. 12都是账实对照查准确性-Confirm the amount of each bonus paid by agreeing to the cash book and bank statements.-Review the board minutes to confirm whether any additional bonus payments relating to this year have been agreed. 董事会记录-Obtain a written representation from management confirming the completeness of directors' remuneration including the bonus. 书面-Review any disclosures made of the bonus and assess whether these are in compliance with local legislation. 查是否合法合规Audit procedures regarding non-depreciation of buildings-Review audit file to ensure that sufficient appropriate audit evidence has been collected in respect of this matter.-Ensure that GAAP does apply to the specific buildings owned by Galartha Co and that a departure from GAAP is not needed in order for the financial statements to show a true and fair view.-Meet with the directors to confirm their reasons for not depreciating buildings.-Warn the directors that in your opinion buildings should be depreciated and that failure to provide depreciation will result in a modified audit report.-Determine the effect of the disagreement on the audit report in terms of the modified opinion being material or of pervasive materiality to the financial statements.-Draft the appropriate sections of the modified audit report.-Obtain a letter of representation from the directors confirming that depreciation will not be charged on buildings.Procedures to confirm i nventory held at third party locations-Send a letter requesting direct confirmation of inventory balances held at year end from the third party warehouse 函证providers used by Abrahams Co regarding quantities and condition.-Attend the inventory count (if one is to be performed) at the third party warehouses to review the controls in operation to ensure the completeness and existence of inventory. 参与盘点-Inspect any reports produced by the auditors of the warehouses in relation to the adequacy of controls over inventory. 检查报告-Inspect any documentation in respect of third party inventory. 检查第三方仓储文件(ii) Procedures to confirm use of standard costs for inventory valuation-Discuss with management of Abrahams Co the basis of the standard costs applied to the inventoryvaluation, and how often these are reviewed and updated. 与管理层讨论-Review the level of variances between standard and actual costs and discuss with management how these are treated. 与管理层讨论差别-Obtain a breakdown of the standard costs and agree a sample of these costs to actual invoices or wage records to assess their reasonableness. 明细检查差错Going concern procedures -Obtain the company's cash flow forecast and review the cash in and out flows. Assess the assumptions for reasonableness and discuss the findings with management to understand if the company will have sufficient cash flows.-Review the company's post year-end sales and order book to assess if the levels of trade are likely to increase and if the revenue figures in the cash flow forecast are reasonable.-Review the loan agreement and recalculate the covenant which has been breached. Confirm the timing and amount of the loan repayment.-Review any agreements with the bank to determine whether any other covenants have been breached, especially in relation to the overdraft.-Discuss with the directors whether they have contacted any alternative banks for finance to assess whether they have any other means of repaying the loan of $4-8m.-Review any correspondence with shareholders to assess whether any of these are likely to increase their equity investment in the company.财务-Review post year-end correspondence with suppliers to identify if any othershave threatened legal action or refused to supply goods.- Discuss with the finance director whether the sales director has yet been replaced and whether any newcustomers have been obtained to replace the one lost. 运营- Enquire of the lawyers of Strawberry as to the existence of any additional litigation and request their法律assessment of the likely amounts payable to the suppliers.- Perform audit tests in relation to subsequent events to identify any items that might indicate or mitigate the risk of going concern not being appropriate.- Review the post year-end bo ard minutes to identify any other issues that might indicate further financial difficulties for the company.- Consider whether the g oing concern basi s is appropriate for the preparation of the financial statements.- Obtain a written representation c onfirming the director's view that Strawberry is a going concern.其他Procedures the auditor should adopt in respect of auditing accounting estimates include:- Enquire of management how t he accounting estimate is made and the d ata on which it is based.- Determine whether events occurring up to the date of the auditor's report (after the reporting period) provide audit evidence regarding the accounting estimate.- Review the method of measurement used and assess the r easonableness o f assumptions made.-Test the operating effectiveness of the controls over how management made the accounting estimate.-Evaluate overall whether the accounting estimates in the financial statements are either reasonable ormisstated.-Obtain sufficient appropriate audit evidence about whether the disclosures in the financial statements related to accounting estimates and estimation uncertainty are reasonable.-Obtain written representations from management and, where appropriate, those charged with governance whether they believe significant assumptions used in making accounting estimates are reasonable.Procedures during the inventory count-Observe the counting teams of Lily to confirm whether the inventory count instructions are being followed correctly.-observe the procedures for identifying and segregating damaged goods are operating correctly.-Observe the procedures for movements of inventory during the count, to confirm that no raw materials or finished goods have been omitted or counted twice.-Select a sample and perform test counts from inventory sheets to warehouse aisle and from warehouse aisle to inventory sheets.-Select a sample of damaged items as noted on the inventory sheets and inspect these windows to confirm whether the level of damage is correctly noted.-Obtain a photocopy of the completed sequentially numbered inventory sheets for follow up testing on the final audit.-Discuss with the warehouse manager how he has estimated the raw materials quantities. To the extent that it is possible, re-perform the procedures adopted by the warehouse manager.-Identify and record any inventory held fo r third parties (if any) and confirm that it is excluded from the count.Audit procedures using CAATSThe audit team can use audit software to calculate inventory days for the year-to-date to compare against the prior year to identify whether inventory is turning over slower, as this may be an indication that it is overvalued.Audit software can be utilised to produce an aged inventory analysis to identify any slow moving goods, which may require write down or an allowance.Cast the inventory listing to confirm the completeness and accuracy of inventory.Audit software can be used to select a representative sample of items for testing to confirm net realisable value and/or cost.Audit software can be utilised to recalculate cost and net realisable value for a sample of inventory. CAATs can be used to verify cut-off by testing whether the dates of the last GRNs and GDNs recorded relate to pre year end; and that any with a date of 1 January 2013 onwards have been excluded from the inventory records.CAATs can be used to confirm whether any inventory adjustments noted during the count have been correctly updated into final inventory records.Procedures the auditor should adopt in respect of auditing this accrual include:-Agree the year-end income tax payable accrual to the payroll records to confirm accuracy.-Agree the subsequent payment to the post year-end cash book and bank statements to confirm completeness.-Recalculation of the accrual to confirm accuracy.-Review any disclosures made of the income tax accrual and assess whether these are in compliance with accounting standards and legislation.Audit procedures for continuous (perpetual) inventory counts-The audit team should attend at least one of the c ontinuous (perpetual) inventory counts t o review whether the controls over the inventory count are adequate.-C onsider attending the inventory count at the year end to undertake test counts of inventory from records to floor and from floor to records in order to confirm the existence and completeness of inventory. -Review the adjustments made to the inventory records on a monthly basis to gain an understanding of the level of differences arising on a month by month basis.-If significant differences consistently arise, this could indicate that the inventory records are not adequately maintained. D iscuss with manageme nt how they will ensure that year-end inventory will not be under or overstated.Procedures to undertake in relation to the uncorrected misstatement-The extent of the potential misstatement should be considered and therefore a large sample of inventory items should be tested to identify the possible size of the misstatement.-The potential misstatement should be d iscussed with Clarinet Co’s management in order to understand why these inventory differences are occurring.-The misstatement should be compared to materiality to assess if the error is materia l individually.-If not, then it should be added to other errors noted during the audit to assess if in aggregate the uncorrected errors are now material.-If material, the auditors should ask the directors to adjust the inventory balances to correct the misstatements identified in the 2014 year end.-Request a written representation from the directors about the uncorrected misstatements including the inventory errors.-Consider the implication for the audit report if the inventory errors are material and the directors r efuses to make adjustments.Receivables circularisation - procedures 步骤-Obtain a list of receivables balances, cast this and agree it to the receivables control account total at the end of theyear. Ageing of receivables may also be verified at this time.-Determine an appropriate sampling method (cumulative monetary amount, value-weighted selection, random, etc.)-Select the balances to be tested, with specific reference to the categories of receivable noted below.- Extract details of each receivable selected from the ledger and prepare circularisation letters.- Ask the chief accountant at Seeley Co (or other responsible official) to sign the letters.- The auditor posts or faxes the letters to the individual receivables.Substantive procedures to confirm valuation of inventory- Select a representative sample of goods in inventory at the year end, agree the cost per the records to a recent purchase invoice and ensure that the cost is correctly stated.- Select a sample of year end goods and review post year end sales invoices to ascertain if NRV is above cost or if an adjustment is required.- For a sample of manufactured items obtain cost sheets and confirm:- raw material costs to recent purchase invoices- labour costs to time sheets or wage records- overheads allocated are of a production nature.-Review aged inventory reports and identify any slow moving goods, discuss with management why these items have not been written down.- Review the inventory records to identify the level of adjustments made throughout the year for damaged/obsolete items. If significant consider whether the year end records require further adjustments and discuss with management whether any further write downs/provision may be required.- Follow up any damaged/obsolete items noted by the auditor at the inventory counts attended, to ensure that the inventory records have been updated correctly.- Perform a review of the average inventory days for the current year and compare to prior year inventory days. Discuss any significant variations with management.Substantive procedures to confirm completeness of provisions or contingent liability- Discuss with management the nature of the dispute between Smoothbrush and the former finance director (FD), to ensure that a full understanding of the issue is obtained and to assess whether an obligation exists.- Write to the company's lawyers to obtain their views as to the probability of the FD's claim being successful.- Review board minutes and any company correspondence to assess whether there is any evidence to support the former FD's claims of unfair dismissal.-Obtain a written representation from the directors of Smoothbrush confirming their view that the formerFD's chances of a successful claim are remote, and hence no provision or contingent liability is required.Substantive procedures over bank balance:-Obtain the company's bank reconciliatio n and c heck the additions t o e nsure arithmeticalaccuracy.-Obtain a b ank confi rmation lett er from the company's bankers.-Verify the balance per the bank statement to an original year end bank statement and also to the bank confi rmation letter.-Verify the rec onciliation’s balsa per the cash book t o the year end cash book.-Trace all of the outstanding lodgement s to the pre year end cash book, post year end bank statement and also to paying-in-book pre year end.-Trace all u npresented cheques through to a pre year end cash book and post year end statement. For any unusual amounts or signifi cant delays obtain explanations from management.-Review the cash book and bank statements for any u nusual items or large transfers around the year end, as this could be evidence of window dressing.-Examine the bank confi rmation letter for details of any security provided by the company or any legal right of set-off as this may require disclosure.Appropriate procedures to determine that net realisable value of book inventory is above cost would include:(1) Assessment of estimated proceeds from the sale of items of inventory. Sales price in the period following the year-end is one important element of net realisable value. Procedures to determine sales prices include:-Obtain actual sales prices by reference to invoices issued after the year-end and determine that the sales were genuine by vouching sales invoices to orders, despatch notes and subsequent receipt of cash.-If actual sales prices are not available, the auditor should obtain estimated sales prices from management. It would be necessary to assess how reasonable these estimated prices were. The auditor might be aided in this respect by reviewing the reports from sales staff backed up by discussions with management.-Particular attention should be paid to sales prices of books identifi ed as slow-moving. (Tutorial note: Slowmoving books might be identifi ed by obtaining lists of sales made in the preceding (say) six months and reviewing reports from sales staff. The sales statistics would also be useful in this respect.)-For damaged books disposal price may be nil or very low and the auditor should examine records of disposal of such books in the past. (Tutorial note: Damaged books should have been identifi ed during the inventory count.)(2) Determine estimated costs to completion. These costs represent another important element of net realisable value.Relevant procedures include:-Some books may still be in production and will initially be included in inventory at cost to date; for example, they may have been printed but not bound. The auditor should examine production budgets and actual costs (for binding, for example) to determine actual costs to completion. (Tutorial note: It is not uncommon for publishers to print books but leave them unbound until sales in the immediate future are expected.)-Books returned may incur extra costs before they can be made ready for resale and the auditor should examine cost records to obtain a reasonable estimate of such costs.(3) Determine costs to be incurred in marketing, selling and distributing directly related to theitems in question.-In general terms the auditor may determine the percentage relationship between sales and selling and distribution expenses.-However, the distribution costs of heavy books are likely to be higher than for (say) light paperback books and the auditor should assess whether the cost weighting is reasonable.(4) All of the above matters should be discussed with management bearing in mind that, although they represent an internal source of evidence, they are the most informed people regarding the saleability of books on hand and regarding determination of the various elements of net realisable value.(5) Discuss with management the need for an inventory provision for slow moving and/or obsoletebooks.Audit procedures adopted in the examination of the cash fl ow forecast would include:(1) Check that the opening balance of the cash forecast is in agreement with the closing balance of the cash book, to ensure the opening balance of the forecast is accurate.(2) Consider how accurate company forecasts have been in the past by comparing past forecasts with actual outcomes. If forecasts have been reasonably accurate in the past, this would make it more likely that the current forecast is reliable.(3) Determine the assumptions that have been made in the preparation of the cash fl ow forecast. For example, the company is experiencing a poor economic climate, so you would not expect cash fl ows from sales and realisation of receivables to increase, but either to decrease or remain stable. You are also aware that costs are rising so you would expect cost increases to be refl ected in the cash forecasts. (4) Examine the sales department detailed budgets for the two years ahead and, in particular, discuss with them the outlets that they will be targeting. This would help the auditor determine whether the cash derived from sales is soundly based.(5) Examine the production department's assessment of the non-current assets required to increase the production of white bread to the level required by the sales projections. Obtain an assessment of estimated cost of non-current assets, reviewing bids from suppliers, if available. This would provide evidence on material cash outfl ows.(6) Consider the adequacy of the increased working capital that will be required as a result of the expansion. Increased working capital would result in cash outfl ows and it would be important to establish its adequacy.(7) If relevant review the post year end period to compare the actual performance against the forecast fi gures.(8) Recalculate and cast the cash fl ow forecast balances.(9) Review board minutes for any other relevant issues which should be included within the forecast.(10) Review the work of the internal audit department in preparing the cash fl ow forecast.procedures - purchases》procedureReason for procedure ________ Obtam a sample of list of parts documents from the Checks the m 阐oes$d 依对唱 of 毗川心computer, ^race individual parts to the goods rec 除包 note(GRN). Ensures the completeness of recording of 吗箕’ Unmatched items poor to the year end should be deluded the payables accrual, - Confirms that the invoice shoud be included in the payables 【edger, rr^eting Ihe 8mp 佗犯ness assertiE- Confirms the completeness d recording of payables invoices :n the ledger. accurate. ---------------------- - --------------- - ------- --------------- Ottam the unmatched indices fife, irrigate 加Unmatched items at (be year end could indicate unrecorded ite*ns chaining ^eason for GRN not being received /liab l t 做 Ensure included in the pa ),abies accrua । the i 加峻 not being precessed. 的心 had Deen received pe 网 end. For a sample of entries from 加 peyattes ledger, agree Ensues that the :ability does belong to V/estra. meeting the devilsback to the jxjrchase invoice.occurrence assertion. For the sage d entries on the payees ledger, agreeEnsures that the liability has been properly discharged by to the electronic payments l.si confirming that theWestra and that the payments list is therefore compfete, supplier name sr.d amouni is axrect. Ry a sarnie of entries on each ele^ronic payments list, agree detals to tne purchase invoice.Ensures that the payment has been mace for a liability incurredtry Wesira, meeting the occurrence assertion. For the sample of entries in the electronic paymentslist, agree detals to the bank statement.Shows that the payment was actually made to that supplier. Obtain the bank statements, 'race a sampe d paymentstc the ^ectfomc Myments listConfirms tr4tthe payment made does relate :o Westra, confirming the xcurrence assertion. ’ For a sample of GRNs in the week pre- and post- year-end. trace to the supporting invoice and entry in thepayables ledger, ensuring recorded in the conectaccounting year.Confirms the accuracy of cut-in the financial statements.enario provided in the question. An alternative and valid format would points under each heading.For entries in the list of parts where no GRN number has been entered, erquire with goods inwards staff why mere is nc GRN. DocumeM reasors obtained. —— Obtain a sampSe of GRNs. Agree details to the list of parts document on the computer. For a sampie of GRNs from the gcods inwards department, trace to the invoice heid in the acccunts depanment.Checks that goods na^e not been receved but detailsnot redded. Possible cuf-offenor where goods have teenreceived bul GRN not raised.Ensures that the parts received had been ordered byWestra. giving 或比假 for the occussce 郡ertm _____ .Ensures the completeness of recording of liabilitiesGRNs 神 no matching mvace mdic2te a liability 出架incurred. Unmatched GRNs should be included in thepayacies accrual.Note this test will be 仪化山 because there is no crossreference maintained of theGRN 2-;一—Review fie of unmatched GRNs. investigatereasons fa any oid (more than one week) iterrs.Obtain a sample of paid invades. Insure that beGRN is attached._ ------------- ---------------Fo r the sample of invoices, check detail intc thecomputerised payaWes ledger, easunng thecmect account has been updated aid the -nvoice Tutorial note. This answer follows the structure cfthe sc te to use the assertons as main headings andto inake。

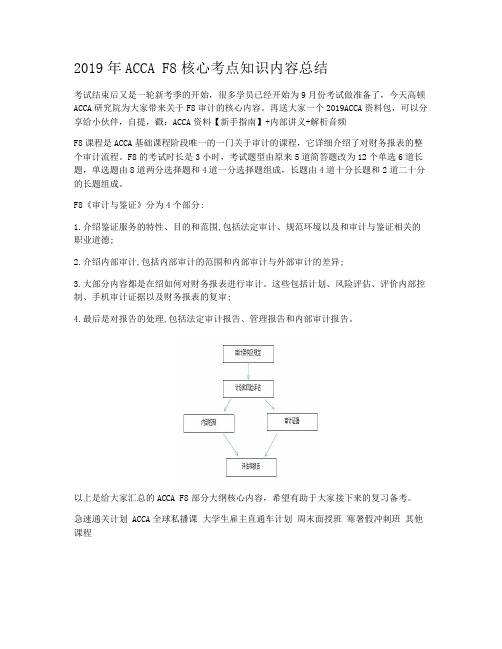

2019年ACCA F8核心考点知识内容总结

考试结束后又是一轮新考季的开始,很多学员已经开始为9月份考试做准备了,今天高顿ACCA研究院为大家带来关于F8审计的核心内容。

再送大家一个2019ACCA资料包,可以分享给小伙伴,自提,戳:ACCA资料【新手指南】+内部讲义+解析音频

F8课程是ACCA基础课程阶段唯一的一门关于审计的课程,它详细介绍了对财务报表的整个审计流程。

F8的考试时长是3小时,考试题型由原来5道简答题改为12个单选6道长题,单选题由8道两分选择题和4道一分选择题组成,长题由4道十分长题和2道二十分的长题组成。

F8《审计与鉴证》分为4个部分:

1.介绍鉴证服务的特性、目的和范围,包括法定审计、规范环境以及和审计与鉴证相关的职业道德;

2.介绍内部审计,包括内部审计的范围和内部审计与外部审计的差异;

3.大部分内容都是在绍如何对财务报表进行审计。

这些包括计划、风险评估、评价内部控制、手机审计证据以及财务报表的复审;

4.最后是对报告的处理,包括法定审计报告、管理报告和内部审计报告。

以上是给大家汇总的ACCA F8部分大纲核心内容,希望有助于大家接下来的复习备考。

急速通关计划 ACCA全球私播课大学生雇主直通车计划周末面授班寒暑假冲刺班其他课程。

ACCA考试《审计与认证业务F8》知识点总结ISA 315 (REVISED),IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENTOne of the major revisions of ISA 315 relates to the inquiries made by external auditors of the internal audit function since internal auditors have better knowledge and understanding of the organisation and its internal control. This article addresses and highlights the components of internal controlThe International Auditing and Assurance Standards Board (IAASB)issues International Standard on Auditing (ISA)for international use. From time to time, ISAs are revised to provide updated standards to auditors. In order to enhance the overall quality of audit, IAASB published a consultation draft on a proposed revision to ISA 315. The objective in revising ISA 315 is to enhance the performance of external auditors by applying the knowledge and findings of an entity’s internal audit function in the risk assessment process, and to strengthen the framework for evaluating the use of internal auditors work to obtain audit evidence.In March 2012, ISA 315 (Revised)was approved and released. One of the major revisions of ISA 315 relates to the inquiries made by external auditors of the internal audit function since internal auditors have better knowledge and understanding of the organisation and its internal control. This article addresses and highlights the components of internal control.OBJECTIVES IN ESTABLISHING INTERNAL CONTROLSGenerally speaking, internal control systems are designed, implemented and maintained by the management and personnel in order to provide reasonable assurance to fulfil the objectives – that is, reliability of financial reporting, efficiency and effectiveness of operations, compliance with laws and regulations and risk assessment of material misstatement. The manner in which the internal control system is designed, implemented and maintained may vary with the entity’s business nature, size and complexity, etc. Auditors focus on both the audit of financial statements and internal controls that relates to the three objectives that may materially affect financial reporting.In order to identify the types of potential misstatements and to determine the nature, timing and extent of audit testing, auditors should obtain an understanding of relevantinternal controls, evaluate the design of the controls, and ascertain whether the controls are implemented and maintained properly.The major components of internal cont rol include control environment, entity’s risk assessment process, information system (including the related business processes, control activities relevant to the audit, relevant to financial reporting, and communication)and monitoring of controls.ACCACONTROL ENVIRONMENTThe control environment consists of the governance and management functions and the attitudes, awareness and actions of the management about the internal control. Auditors may obtain an understanding of the control environments through the following elements.1. Communication and enforcement of integrity and ethical values It is important for the management to create and maintain honest, legal and ethical culture, and to communicate the entity’s ethical and behavioral sta ndards to its employees through policy statements and codes of conduct, etc.2. Commitment to competence It is important that the management recruits competent staff who possess the required knowledge and skills at competent level to accomplish tasks.3. Participation by those charged with governance An entity’s control consciousness is influenced significantly by those charged with governance; therefore, their independence from management, experience and stature, extent of their involvement, as well as the appropriateness of their actions are extremely important.4. Management’s philosophy and operating style Management’s philosophy and operating style consists of a broad range of characteristics, such as management’s attitude to response to business risks, financial reporting, information processing, and accounting functions and personnel, etc. For example, does the targeted earning realistic? Does the management apply aggressive approach where alternative accounting principles or estimates are available? These management’s philosophy and operating style provide a picture to auditors about the management’s attitude about the internal control.5. Organisational structure The organisational structure provides the framework on how the entity’s a ctivities are planned, implemented, controlled and reviewed.6. Assignment of authority and responsibility With the established organisational structure or framework, key areas of authority andreporting lines should then be defined. The assignment of authority and responsibility include the personnel that make appropriate policies and assign resources to staff to carry out the duties. Auditors may perceive the implementation of internal controls through the understanding of the organisational structure and the reporting relationships.7. Human resources policies and practices Human resources policies and practices generally refer to recruitment, orientation, training, evaluation, counselling, promotion, compensation and remedial actions. For example, an entity should establish policies to recruit individuals based on their educational background, previous work experience, and other relevant attributes. Next, classroom and on-the-job training should be provided to the newly recruited staff. Appropriate training is also available to existing staff to keep themselves updated. Performance evaluation should be conducted periodically to review the staff performance and provide comments and feedback to staff on how to improve themselves and further develop their potential and promote to the next level by accepting more responsibilities and, in turn, receiving competitive compensation and benefits.With the ISA 315 (Revised),external auditors are now required to make inquiries of the internal audit function to identify and assess risks of material misstatement. Auditors may refer to the management’s responses of the identified deficiencies of the internal controls and determine whether the management has taken appropriate actions to tackle the problems properly. Besides inquiries of the internal audit function, auditors may collect audit evidence of the control environment through observation on how the employees perform their duties, inspection of the documents, and analytical procedures. After obtaining the audit evidence of the control environment, auditors may then assess the risks of material misstatement.ENTITY’S RISK ASSESSMENT PROCESSAuditors should assess whether the entity has a process to identify the business risks relevant to financial reporting objectives, estimate the significance of them, assess the likelihood of the risks occurrence, and decide actions to address the risks. If auditors have identified such risks, then auditors should evaluate the reasons why the risk assessmentprocess failed to identify the risks, determine whether there is significant deficiency in internal controls in identifying the risks, and discuss with the management.THE INFORMATION SYSTEM, INCLUDING THE RELEVANT BUSINESS PROCESSES, RELEVANT TO FINANCIAL REPORTING AND COMMUNICATIONAuditors should also obtain an understanding of the information system, including the related business processes, relevant to financial reporting, including the following areas:? The classes of transactions in the ent ity’s operations that are significant to the financial statements. The procedures that transactions are initiated, recorded, processed, corrected as necessary, transferred to the general ledger and reported in the financial statements.? How the information system captures events and conditions that are significant to the financial statements.? The financial reporting process used to prepare the entity’s financial statements.? Controls surrounding journal entries.? Understand how the entity communicates financial reporting roles, responsibilities and significant matters to those charged with governance and external – regulatory authorities.CONTROL ACTIVITIES RELEVANT TO THE AUDITAuditors should obtain a sufficient understanding of control activities relevant to the audit in order to assess the risks of material misstatement at the assertion level, and to design further audit procedures to respond to those risks. Control activities, such as proper authorisation of transactions and activities, performance reviews, information processing, physical control over assets and records, and segregation of duties, are policies and procedures that address the risks to achieve the management directives are carried out.MONITORING OF CONTROLSIn addition, auditors should obtain an understanding of major types of activities that the entity uses to monitor internal controls relevant to financial reporting and how the entityinitiates corrective actions to its controls. For instance, auditors should obtain an understanding of the sources and reliability of the information that the entity used in monitoring the activities. Sources of information include internal auditor report, and report from regulators.LIMITATIONS OF INTERNAL CONTROL SYSTEMSEffective internal control systems can only provide reasonable, not absolute, assurance to achieve the entity’s financial reporting objective due to the inherent limitations of internal control – for example, management override of internal controls. Therefore, auditors should identify and assess the risks of material misstatement at the financial statement level and assertion level for classes of transactions, account balances and disclosures.CONCLUSIONAs internal auditors have better understanding of the organisation and expertise in its risk and control, the proposed requirement for the external auditors to make enquiries of internal audit function in ISA 315 (Revised)will enhance the effectiveness and efficiency of audit engagements. External auditors should pay attention to the components of internal control mentioned above in order to make effective andefficient enquiries. An increase in the work of internal audit functions is also expected because of such proposed requirement.Raymond Wong, School of Accountancy, The Chinese University of Hong Kong, and Dr Helen Wong, Hong Kong Community College, Hong Kong Polytechnic UniversityReference ISA 315 (Revised),Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and ItsEnvironment。

ACCA考试《审计与认证业务F8》知识点总结本文由高顿ACCA整理发布,转载请注明出处ISA 315 (REVISED),IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENTOne of the major revisions of ISA 315 relates to the inquiries made by external auditors of the internal audit function since internal auditors have better knowledge and understanding of the organisation and its internal control. This article addresses and highlights the components of internal controlThe International Auditing and Assurance Standards Board (IAASB)issues International Standard on Auditing (ISA)for international use. From time to time, ISAs are revised to provide updated standards to auditors. In order to enhance the overall quality of audit, IAASB published a consultation draft on a proposed revision to ISA 315. The objective in revising ISA 315 is to enhance the performance of external auditors by applying the knowledge and findings of an entity’s internal audit function in the risk assessment process, and to strengthen the framework for evaluating the use of internal auditors work to obtain audit evidence.In March 2012, ISA 315 (Revised)was approved and released. One of the major revisions of ISA 315 relates to the inquiries made by external auditors of the internal audit function since internal auditors have better knowledge and understanding of the organisation and its internal control. This article addresses and highlights the components of internal control.OBJECTIVES IN ESTABLISHING INTERNAL CONTROLSGenerally speaking, internal control systems are designed, implemented and maintained by the management and personnel in order to provide reasonable assurance to fulfil the objectives – that is, reliability of financial reporting, efficiency and effectiveness of operations, compliance with laws and regulations and risk assessment of material misstatement. The manner in which the internal control system is designed, implemented and maintained may vary with the entity’s business nature, size an d complexity, etc. Auditors focus on both the audit of financial statements and internal controls that relates to the three objectives that may materially affect financial reporting.In order to identify the types of potential misstatements and to determine the nature, timing and extent of audit testing, auditors should obtain an understanding of relevant internal controls, evaluate the design of the controls, and ascertain whether the controls are implemented and maintained properly.The major comp onents of internal control include control environment, entity’s risk assessment process, information system (including the related business processes, control activities relevant to the audit, relevant to financial reporting, and communication)and monitoring of controls.ACCACONTROL ENVIRONMENTThe control environment consists of the governance and management functions and the attitudes, awareness and actions of the management about the internal control. Auditors may obtain an understanding of the control environments through the following elements.1. Communication and enforcement of integrity and ethical values It is important for the management to create and maintain honest, legal and ethical culture, and to communicate the entity’s eth ical and behavioral standards to its employees through policy statements and codes of conduct, etc.2. Commitment to competence It is important that the management recruits competent staff who possess the required knowledge and skills at competent level to accomplish tasks.3. Participation by those charged with governance An entity’s control consciousness is influenced significantly by those charged with governance; therefore, their independence from management, experience and stature, extent of their involvement, as well as the appropriateness of their actions are extremely important.4. Management’s philosophy and operating style Management’s philosophy and operating style consists of a broad range of characteristics, such as management’s atti tude to response to business risks, financial reporting, information processing, and accounting functions and personnel, etc. For example, does the targeted earning realistic? Does themanagement apply aggressive approach where alternative accounting principles or estimates are available? These management’s philosophy and operating style provide a picture to auditors about the management’s attitude about the internal control.5. Organisational structure The organisational structure provides the framework on how the entity’s activities are planned, implemented, controlled and reviewed.6. Assignment of authority and responsibility With the established organisational structure or framework, key areas of authority andreporting lines should then be defined. The assignment of authority and responsibility include the personnel that make appropriate policies and assign resources to staff to carry out the duties. Auditors may perceive the implementation of internal controls through the understanding of the organisational structure and the reporting relationships.7. Human resources policies and practices Human resources policies and practices generally refer to recruitment, orientation, training, evaluation, counselling, promotion, compensation and remedial actions. For example, an entity should establish policies to recruit individuals based on their educational background, previous work experience, and other relevant attributes. Next, classroom and on-the-job training should be provided to the newly recruited staff. Appropriate training is also available to existing staff to keep themselves updated. Performance evaluation should be conducted periodically to review the staff performance and provide comments and feedback to staff on how to improve themselves and further develop their potential and promote to the next level by accepting more responsibilities and, in turn, receiving competitive compensation and benefits.With the ISA 315 (Revised),external auditors are now required to make inquiries of the internal audit function to identify and assess risks of material misstatement. Auditors may refer to the management’s responses of the identified deficiencies of the internal controls and determine whether the management has taken appropriate actions to tackle the problems properly. Besides inquiries of the internal audit function, auditors may collect audit evidence of the control environment through observation on how the employees perform their duties, inspection of the documents, and analytical procedures. After obtaining the audit evidence of the control environment, auditors may then assess the risks of material misstatement.ENTITY’S RISK ASSESSMENT PROCESSAuditors should assess whether the entity has a process to identify the business risks relevant to financial reporting objectives, estimate the significance of them, assess the likelihood of the risks occurrence, and decide actions to address the risks. If auditors have identified such risks, then auditors should evaluate the reasons why the risk assessment process failed to identify the risks, determine whether there is significant deficiency in internal controls in identifying the risks, and discuss with the management.THE INFORMATION SYSTEM, INCLUDING THE RELEVANT BUSINESS PROCESSES, RELEVANT TO FINANCIAL REPORTING AND COMMUNICATIONAuditors should also obtain an understanding of the information system, including the related business processes, relevant to financial reporting, including the following areas:? The classes of transactions in the entity’s operations that are significant to the financial statements. The procedures that transactions are initiated, recorded, processed, corrected as necessary, transferred to the general ledger and reported in the financial statements.? How the information system captures events and conditions that are significant to the financial statements.? The financial reporting process used to prepare the entity’s financial statements.? Controls surrounding journal entries.? Understand how the entity communicates financial reporting roles, responsibilities and significant matters to those charged with governance and external – regulatory authorities.CONTROL ACTIVITIES RELEVANT TO THE AUDITAuditors should obtain a sufficient understanding of control activities relevant to the audit in order to assess the risks of material misstatement at the assertion level, and to design further audit procedures to respond to those risks. Control activities, such as proper authorisation of transactions and activities, performance reviews, information processing, physical control over assets and records, and segregation of duties, are policies and procedures that address the risks to achieve the management directives are carried out.MONITORING OF CONTROLSIn addition, auditors should obtain an understanding of major types of activities that the entity uses to monitor internal controls relevant to financial reporting and how the entity initiates corrective actions to its controls. For instance, auditors should obtain an understanding of the sources and reliability of the information that the entity used in monitoring the activities. Sources of information include internal auditor report, and report from regulators.LIMITATIONS OF INTERNAL CONTROL SYSTEMSEffective internal control systems can only provide reasonable, not absolute, assurance to achieve the entity’s financial reporting objective due to the inherent limitations of internal control – for example, management override of internal controls. Therefore, auditors should identify and assess the risks of material misstatement at the financial statement level and assertion level for classes of transactions, account balances and disclosures.CONCLUSIONAs internal auditors have better understanding of the organisation and expertise in its risk and control, the proposed requirement for the external auditors to make enquiries of internal audit function in ISA 315 (Revised)will enhance the effectiveness and efficiency of audit engagements. External auditors should pay attention to the components of internal control mentioned above in order to make effective andefficient enquiries. An increase in the work of internal audit functions is also expected because of such proposed requirement.Raymond Wong, School of Accountancy, The Chinese University of Hong Kong, and Dr Helen Wong, Hong Kong Community College, Hong Kong Polytechnic UniversityReference ISA 315 (Revised),Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and Its Environment更多ACCA资讯请关注高顿ACCA官网:。

ACCAF8备考Tips:审计各阶段及流程详解ACCA F8备考Tips:审计各阶段及流程详解F8(Audit and Assurance)是一门实务性很强的课程,要求大家熟悉审计工作流程,应用会计知识判断被审计单位的财务报告编制过程及结果是否有误。

自2016年9月开始实施的新考试题型包括Section A和Section B两大部分,Section A(Objective Test Cases)共有三道Case,每个Case有五道选择题,每题两分,涉及范围包括大纲的方方面面;Section B共有三道大题,第一题30分,第二题和第三题各自20分,常见的题型包括auditrisk & auditor’s response,internal controldeficiencies/strengths & TOCs,以及substantive procedures等。

大题对大家书面表达的要求比较高,所以理解审计逻辑,勤加练习并学会总结对于大部分没有实务经验的同学们而言非常必要。

我们先来看一下完整的审计工作需要经过哪些阶段,具体又有哪些流程。

上图是完整的审计工作循环,始于engagement letter(业务约定书),终于audit report (审计报告),历经audit planning、auditperformance和completion三个阶段。

1.Beforeaudit process为了签订最开始的engagementletter,审计师在接受业务委托时需要先“自我反省”,看看注册会计师是否符合职业道德准则(Codeof Ethics)的要求,如果有一些情况产生了对独立性(independence)的威胁(具体包括self-interest, self-review, familiarity, advocacy& intimidation threats),则应该考虑适用相对应的保卫措施(常见的safeguards 包括dispose of interests/shares, independent/quality control partner review, remove t he one from the engagementteam等)。

ACCA知识点:F8理解审计战略和审计计划在ACCA考试中,F8当中理解审计战略和审计计划一直是大纲中最为重要,也是难点最多的一部分知识点。

那么今天就为同学们总结一下F8当中理解审计战略和审计计划的习题讲解,这部分内容体系比较复杂重要,所以帮助大家做些题目逐渐了解这章内容。

Audit is a subject where sharp minds can excel. What is really demanded of us is understanding ‘materiality’. As simple as it sounds, it can be the reason why many students might fail paper F8. The first question was about Audit Strategy. And ‘materiality’ was definitely a part of it. Do you know the role of the audit strategy and audit plan in defining materiality?Audit strategy and materialityAn audit strategy outlines the OBJECTIVES of the audit that is to be performed – like crafting the skeleton of a body. The details are yet to be filled in.Once the internal control environment and the risk assessment system of the entity is understood, the independent auditor then needs to define an OVERALL materiality level. This consists of two important components:Performance Materiality, andTolerable Misstatement ErrorThe auditor defines each of the two components. The performance materiality aswell as the tolerable misstatement error differs from organisation to organisation, market to market and economy to economy.Audit plan and materialityThe audit plan is an important document. ISA 300 is the governing standard here. The audit plan provides guidance on:The directionThe supervision, andThe review of audit proceduresWhile going through ISA 320 – Audit Materiality in the study text, I ran a few searches online, discovering that the US regulates its audit procedures under Statements on Auditing Standards (SAS). These are a collection of Generally Accepted Auditing Standards (GAAS).I opened SAS 122, section 320, which was titled Materiality in Planning and Performing an Audit. There, I found what I was looking for – the audit plan:Helps give the auditor insight regarding the effect of the nature of an organisation in defining materiality.Helps outline situation-based factors influencing the materiality.Allows the auditor to take in account several other factors to establisheffective materiality levels.Lets the auditor document any changes/revisions in the materiality level initially defined by the auditor if crucial evidence is found later on at the performance stage.Takes into account any possible changes to the performance materiality level following any change/revision in the overall materiality level.As part of the ACCA student network, we all need to understand the basics of audit firmly to excel in our careers. I believe ACCA studies do not just keep you confined to one book in your bag, but demand you to research on your own.I would love to hear your thoughts on this. Let me know if this article has helped you on your path to success in Paper F8.获取更多ACCA考试知识点可关注永和九年,岁在癸丑,暮春之初,会于会稽山阴之兰亭,修禊事也。

ACCA F8的知识点比较多,考试更注重细节,往往会让很多考生措手不及。

2018年三月考季,ACCA F8的考试通过率更是惨不忍睹,以39%的通过率,“稳坐”F阶段通过率末尾。

ACCA考试以大学生为重要主体,没有实操经验,在ACCA F8这样对实务经验要求比较高的科目来说,这样的通过率和考试成绩也算正常。

在文章开头中公财经网小编就说过F8知识点繁多,单是了解各个知识点是远远不够的,重要的是要把这些知识点联系起来。

今天,中公财经网小编就带大家一起来梳理一下F8的知识点:审计流程。

上图就是一个完整的审计流程,通俗来解释:Tendering就是审计师和客户合作的开始;为了增进合作关系,就有了client acceptance procedure;确定唯一的合作关系,需要用appointment and engagement letter来证明;通过audit planning更加深入的了解彼此,当在相处过程中发现一些似是而非的问题(ROMM),会通过更加细致的调查(substantive procedure)和确认(audit review),最终确认和解决。

充分了解并体会审计师和客户的这种关系和合作,对理解F8的内容是非常有帮助的。

各位同学们不要被F8历年惨淡的考试通过率吓到,只要用对方法,ACCA F8将不再是你的“拦路虎”。

X。

Logical thinking in audit procedureAra Shen沈璐萍各位学员,大家好,新的考季又开始了,考前我们来简单梳理下审计流程中关键步骤的逻辑思路。

ACCA的Fundamental模块里,F8一直是一个比较诡异的“滑铁卢”,绝大部分学员在朝着Professional阶段大门一路高歌而去时,会在F8这门课上突遭不适,而这绝大部分中的99.99%都是在校学生党。

为什么?当然是因为学生党缺乏经验,相信课堂上老师们都有提及,但需要强调的是,学生党不仅是对现实审计了解不足,更重要的是欠缺经验累积形成的审计思考方式,而这种逻辑思考,才是帮助学员脱离死记硬背,从而学而知之的万金油。

审计作为一门高应用型学科,经验积累在所难免,但对于广大学生党学员,现下似乎难以做到。

因此我们在这里更多的是帮助学员们或多或少建立起一种审计逻辑思考方式。

现实审计中我们也经常遇到新的情况,无法用曾经的审计案例生搬硬套,此时我们就需要用逻辑方法来解决新的问题,而同学们可以将考试中的案例都当作现实中可能遇到的新情况,用学习了的审计方法去解决她。

至于有工作经验或形成方法论的学员们,可以关上文章,自行看题了。

废话说了有点多,切入正题。

审计是流程,流程就有步骤,大体如下:接受委托——>审计计划——>内控测试——>实质性程序——>审计报告前两个以及最后一个步骤本文空间有限就不详述了,我们重点来看,在学习到内控测试和实质性程序时,会遇到F8的重点内容:六大循环。

说白了就是通常审计关注的六大块企业活动,我们以大家喜闻乐见的Sales cycle为例子,来看看企业赚钱的过程中,我们作为一个第三方的公证人,如何验证他的真实公允。

民间审计的主旨是在确保Audit risk在审计师可接受的范围内,在Sales环节,我们首先会通过Test of control来验证Sales流程没有重大fraud及error,确保Audit risk 中的RMM在可接受范围内;如果合格,我们就执行正常的实质性程序,如果TOC不合格,则后续的实质性程序就会增加,以降低Detection risk。

ACCA F8的知识点比较多,考试更注重细节,往往会让很多考生措手不及。

2018年三月考季,ACCA F8的考试通过率更是惨不忍睹,以39%的通过率,“稳坐”F阶段通过率末尾。

ACCA考试以大学生为重要主体,没有实操经验,在ACCA F8这样对实务经验要求比较高的科目来说,这样的通过率和考试成绩也算正常。

在文章开头中公财经网小编就说过F8知识点繁多,单是了解各个知识点是远远不够的,重要的是要把这些知识点联系起来。

今天,中公财经网小编就带大家一起来梳理一下F8的知识点:审计流程。

上图就是一个完整的审计流程,通俗来解释:Tendering就是审计师和客户合作的开始;为了增进合作关系,就有了client acceptance procedure;确定唯一的合作关系,需要用appointment and engagement letter来证明;通过audit planning更加深入的了解彼此,当在相处过程中发现一些似是而非的问题(ROMM),会通过更加细致的调查(substantive procedure)和确认(audit review),最终确认和解决。

充分了解并体会审计师和客户的这种关系和合作,对理解F8的内容是非常有帮助的。

各位同学们不要被F8历年惨淡的考试通过率吓到,只要用对方法,ACCA F8将不再是你的“拦路虎”。