2016年3月ACCA考试F7考前tips

- 格式:doc

- 大小:190.50 KB

- 文档页数:2

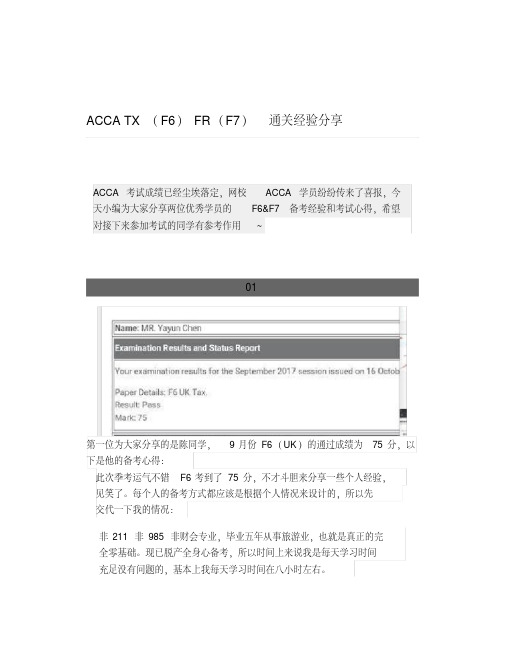

ACCA TX(F6) FR(F7)通关经验分享ACCA考试成绩已经尘埃落定,网校ACCA学员纷纷传来了喜报,今天小编为大家分享两位优秀学员的F6&F7备考经验和考试心得,希望对接下来参加考试的同学有参考作用~01第一位为大家分享的是陈同学,9月份F6(UK)的通过成绩为75分,以下是他的备考心得:此次季考运气不错F6考到了75分,不才斗胆来分享一些个人经验,见笑了。

每个人的备考方式都应该是根据个人情况来设计的,所以先交代一下我的情况:非211非985非财会专业,毕业五年从事旅游业,也就是真正的完全零基础。

现已脱产全身心备考,所以时间上来说我是每天学习时间充足没有问题的,基本上我每天学习时间在八小时左右。

正式备考F6是从8月2日开始,到9月7日考试之间是一个月多一点点的时间。

F6的特点是计算量大却不复杂,知识点多且复杂,所以想学好F6最重要的是要有耐心加细心。

老实说我刚接触F6的那几天是懵逼的,感觉每天学习的知识点特别多,每一类的税要记的细节都特别琐碎,而搭配的练习册和网课的节次是对不上的,所以经常学完了一天的课程量却发现自己没有办法去做习题巩固,这对我这个不会背书只能靠做题记知识点的人来说简直是噩耗。

不过也怪自己没有事先把BPP的教材研究一番,其实网校课程的分节基本还是能在BPP教材的目录里找到对应内容的,然后教材里每小节正文内容末尾会有quick quiz,而且后面还有一些数量不多的对应练习题,是可以用来稍作练习的。

不管是我还是我一位目前已经考完F阶段科目的考友,都认为F6的初期很容易让人产生严重的不适,这个时候不要像我一开始一样慌张,耐心下来,如果发现有网课的知识点没听懂,建议单独去翻一下教材上对应的内容,结合例题多读几遍总能搞懂,尽量不要带着头一天遗留的问题进入第二天的学习。

有条不紊地学完所有基础班的课程,即使最后仍然有很多不解或者认为有很多小知识点记不住,不用担心,开始大量刷题查漏补缺。

ACCA F7及P2考试知识点及答题技巧分享很多小伙伴对于ACCA考试知识点以及相关的答题技巧非常的感兴趣。

那么就让中公财经小编在这里给大家简单介绍一下吧;我们先来看看F7《财务报告》都有哪些必考点。

F7的考试形式为20道多项选择题,每道题2分,以及3道论述题,其中2道15分,1道30分。

20道选择题中,以下这些内容基本为必考考点:Consolidation、PPE & Impairment、Revenue、Loan note & Convertible bonds、Lease、Provision / Contingent & Events after reporting date、Inventory and Biological Assets、EPS、Ratios、Conceptual Framework and others。

当然,这些是比较大的考点,在这些考点中还会包含其他内容,比如在Consolidation中会考:Control & Significant Influence、Goodwill、NCI、Intra-group transactions、Fair value appreciation、Account for associate等内容,这里值得注意的是如果30分的计算题没有考合并报表的话,那么在选择题中可能会涉及好几题合并的概念。

另外,在PPE& Impairment中,常常会考Depreciation的计算、Impairment 的判断、CGU计算以及PPE的初始确认等其他概念的判断,大概会涉及2-4题。

下面,我们来说说所占分值*5的Consolidated Financial Statement这道计算题都有哪些得分技巧。

总的来说,你*4先完成每个步骤,再编制报表,答题过程中可以写一行空一行,方便修改补充。

题目一般会要求编制Consolidate SOFP & SPL,*9步一定会涉及Goodwill的计算,这是送分题;NCI 一定是用Fair value Model;至于After acquisition,一定会考Fair value adjustment的后续影响,在编合并报表前,需要计算NCI , Retained Earning的金额,然后考虑是否有Associate,初始如何确认,后续的只要考虑收购后的A的利润以及A→P, P→A的影响,*4编制合并报表。

acca会员关于F6与F7的经验分享acca会员关于F6与F7的经验分享关于F阶段的考试,小编整理了一些以往acca考试经验分享。

希望能够对大家有所帮助,这一次是关于F6跟F7的经验分享。

下面是中公财经网小编整理的一篇F阶段脱坑介绍;由于成建制班免考五门,F6成了我们第一场要面对的全球统考。

第一次正式考过于紧张,外加正值失恋借刷题转移注意力,于是我把bpp整本大砖头一样的练习册反复刷了四五遍,70分pass,可惜后面的考试再也没有超过这个分数了orz。

我觉得F6重推算轻概念,属于刷题可过的一门考试。

working的格式列好了,即使没算对结果,及格还是不难的。

过程分比结果分多得多得多。

个人税比公司税复杂,但是题型结构和套路单一,可以和其他科目一起准备。

此科目不建议考友借用师兄师姐的旧版课程和书籍,因为税率和标准有可能会变化。

F7和F8考试这两门是一起考的,然而在那个考季我作死了。

先是和小伙伴参加了个学院组织的商业比赛,拿了个水冠军,成功混了一个月;再是疯狂投递实习,刷笔试,做简历,跑面试,又混了一个月。

等到我想起还有全球统考这个东西的时候,距离考试只剩下一个月了。

自己作的死只能跪着作完,于是我开始蹲点宿舍楼下的自习室,每天都是凌晨一点回宿舍睡觉,然后清晨六点下楼,除去非ACCA的专业课,平均每天备考“预习”时间大致在9h左右。

最后F7 60分、F8 55分飘过。

F7同样重推算轻概念,working和报表格式建好了,按部就班地做就能过。

但是至今我仍然对现金流量表深怀恐惧。

所幸F7和P2都没碰上,使我成了漏网之鱼。

希望还没考的考友们好好学习现金流量表的内容,不要像我一样抱着侥幸地心理。

考过是其次,重要的是知识的学习。

F7老师教的很好,她是通过分类,先给我们细讲每一条IFRS的处理,再总结四大报表的格式,跟着笔记走就好。

我觉得这不失为一种方法,供考友们参考。

F7老师还总结了一个规律,就是题目的每条Notes实际上都代表着两处调整。

ACCA F7 考前复习Non-current assets非流动资产A non-current asset is an asset acquired for use on a continuing basis, normally over more than one year.非流动资产指购买后连续使用的资产,通常超过一年。

Examples include 例如:❝Land and buildings❝土地和建筑❝Plant and machinery❝机器和设备❝Fixtures and fittings❝固定装置Non-current assets are recorded in the Statement of Financial Position. The items above are tangible non-current assets (with a physical existence).非流动资产记入财务状况表。

上述项目为有形非流动资产(具有物理实在)。

The cost of an asset can include all the costs incurred in bringing the asset into use, e.g. delivery, installation and set up costs.资产成本包括将资产投入使用产生的所有成本,比如配送、安装和启动成本。

However, the costs of training staff training on how to use an asset are not included in the cost of the asset. The reason is that it is uncertain whether staff will stay in the business and hence the benefit of the training may not last for the full life of the asset.但资产成本不包括培训员工使用资产的培训成本。

ACCA F7-F9答题技巧总结本文由高顿ACCA整理发布,转载请注明出处F71. 时间管理报表做不平或做题时有些小不顺,千万不要纠结,时间差不多了,往下才做是王道。

2. 列示WORKING要写标题,列清楚,(告诉阅卷老师你在算什么,计算过程中的每个数字代表什么,答案是从什么地方来的),这是很重要的一点,因为即使结果错误,只要思路正确依然可以得很多分数。

相反,如果只有一个结果,即使数字正确,但没有过程分补充,能得的分数依然很少。

提醒:合并时P+S 的算式列好以后,要记得进行加总。

算式列好,不做加总,阅卷老师是不会替你加总的!(他每天要批那么多卷子,哪儿有空替你加)但是报表题,SOFP,最后的平衡总数和利润表中的Profit for the financial year是不计分的,考试时,如果时间不够,这里的数字可以不必实际计算。

但是,不计算又如何知道你的表平了呢?所以,还是算一下,来的放心吧。

F81. 时间管理利用好15分钟阅读时间,阅读全卷5题的题干,大致了解考试考点,并对最有把握的一题进行进一步阅读,可以在题目中划出重点内容和大纲以便之后回答。

严格控制时间,过时就空开一些,做下一题。

2. 学会审题分析考题要你做什么,特别注意使用的动词及关键词,如:define是给出定义,explain 除了定义以外还要稍加阐述等。

Only answer what is asked! 不要只回答和题目某一个词相关的自己觉得容易回答的内容。

3.Apply to the case!案例分析的题目一定要结合案例!F91. How to tackle Theory-based questions?Understand theory first before recitingContrast different theoriesA vividpoint= one definition+ one explanation + one example2. How to tackle Calculation-based questions?Follow typical questions tackling procedureUse real exam questions onlyFocus on the main and most familiarquestionsMostly popular questions:Investment appraisal(NPV, IRR, ARR, Payback, Discount payback,Sensitivity analysis, Lease or buy, and etc)Working capital management(AR, Inventory, Cash, AP, and working capital management approach)Cost of capital and source of finance(Capital structure theory, WACC and risk adjusted WACC, Islamic finance)Dividend policy and risk management(Right issue, Bonus issue, Dividend method,Share repurchase, Forward, Future, Option, MMH, EMH)更多ACCA资讯请关注高顿ACCA官网:。

ACCA考前复习指南:F7重要知识点.考点总结改革之后的F7考试,考查范围更加全面。

同学们在备考的时候,需要对每个准则基本内容进行准备。

考官一般围绕recognition , measurement和presentation等方面考查。

而选择题部分,考前可以结合三套真题的选择题和练习册的选择题梳理知识点。

试卷分析SectionA SectionB考试题型选择题20题大题:15分x2大题:30分xl考察范围整个考纲Ratio analysisSectionA备考要点■仔细读题■理解准则基础■排除法,举反例■计算题排除干扰自己算SectionB备考要点■计算ratio ,分类别(profitability/liquidity/gearing/i n vest or)■关注题目角色,以谁的角度写report■又寸比ratio :纟吉合题目要求,VS past year/competitors/industry benchmark■特殊关注点:从无到有,变化迅速,人无我有,人有我优■思考:financing sources, overtrading cashflow, risk going concernsConsolidation FS 重要知识点FV of considerationShare exchangeDeferred cashLoan noteContingent considerationFV Adjustment of net asset Depreciatio nFurther value in crease after acquisitionGoodwillImpairment of GoodwillMid?year acquisitiontime apportionIntra-group tradingSale &COSURP considering who is seller (S or P)Intra-group balancereceivables & payablesCIT & GITIntra-group loanInvestment & liabilityFinance cost & Investment incomeNCIFull methods(FV methods) VS proportionate methodsAssociateIntra-trading A&P: URP * P%Impairment of AssociateSingle entity重要知识点IAS16 PPEInitial Cost measurementDepreciationRevaluati on? watch out DT from revaluationDisposalIFRS9 Financial instrumentFinance asset-FVTPL/FVTOCI/Amortizatio n-Watch out Issue cost?Debt instrument & Equity instrumentFinance liability-Loan note■Convertible loan noteIFRS15 Revenue5 steps to recognize revenueConstruction contractService-Deferred revenueAgency sale-sales & repurchase-sales & return-sales & leasebackFactor receivablesIAS 2 Inventory adjustmentopening inventory+ purchase -closing inventory= cost of saleIAS 17 leaseFinance lease-NCL/CL & finance cost-Asset: CV & depreciationoperating lease?annual lease payment(time apportion)TaxCurrent taxDeferred tax-watch out DT from revaluationIAS 37Provision & contingent liabilityIAS 33 EPSEPS 计算:full market issue bonus issue & right issueCashflowInvestment, operating f financing局部计算选择题高频考点梳理Framework选择题文字题为主Qualitative characteristics 理解应用Recognition结合田可准则考察会计处理是否正确Measurement结合任何准则考察会计处理是否正确Historical cost, replacement cost, current cost Conceptual frameworkIAS 16 PPEInitial measurement costCapital expenditure VS revenue expenditure Depreciatio nRevaluationIAS 36 ImpairmentIndicators-carrying value > recoverable amount-external or internal indicatorCalculati on?Lower of carrying value-FV -cost to sell, Value in useCGU?order to impairment-1st specific damaged Asset■2nd Goodwill-3rd other asset (pro rata allocation)IAS 38 Intangible assetRecog nition-Research & development (capitalized criteria) Amortizati on-Finite life■Infinitive life : impairment reviewIFRS 5 NCA - Held for sale & discontinued operations Recognition Criteria 分类为IFRS5 的条件Measureme nt-Lower of:l.FV-cost to sell2.CV■No depreciation being held for saleIAS 23 Borrowing costConditions to be met for capitalizationInterest expenseIAS 20 Government GrantRevenue VS capital grantDeferred income / deducted from value of assetIAS 40 investment propertyFV to p/lIAS 2 InventoryValued at lower of 1: NRV=selling price - cost to sell2:Costopening inventory + purchase -closing inventory二cost of saleIAS 41 AgricultureScopeMeasurement: FVIFRS 15 (IAS 18/IAS11) revenue文字题-Revenue确认时点及金额■结合sales & repurchase z sales &lease back zFactor receivables/agency sales/sales & return 等特殊事项处理。

中公财经培训网:/

关于F7的考试可能各种人有着不同的考试思路。

下面中公财经小编就给大家介绍一下关于F7的考试经验分享。

具体情况如下所示;

F7更加侧重数字计算,我是一个理科生,我本身也更喜欢计算题。

对于计算题,我觉得最主要的诀窍就是多练习。

以前学习数学的时候,我们习惯都是看到一个公式就会去推导它怎么来的,对于F7的有些公式我也会去想它的逻辑,这更加帮助了我的理解。

对于后面编写报表,大的框架大家都要记住,我觉得最主要就是记住每一个小的知识点,然后按步骤多练习,一个题多练习几次,自己也会更加明白其中的套路。

对于怎么把资产负债表做平,我觉得大部分人都不能在第一次做平,一定要按照老师的方法,把每一个数字都用上,做上记号,做了一个小的working后要填上,这样就不会漏填。

考试的时候,不要一味地去追求怼平,最后有时间的时候再来看,清醒一下头脑,这样你会发现自己刚开始没有看到的细节。

我喜欢把资产负债表的差额给算出来,然后慢慢的来凑数,可能你们觉得非常不科学,但是这个方法却给了我很多帮助,我觉得每个人都有适合自己的一套学习方法,大家可以借鉴然后找到自己的方法,希望大家都可以通过考试!

每个人都有自己的一套学习方法,最重要的是适合自己,并且有所成效。

每次ACCA 考试成绩公布后,总会有人欢喜有人忧。

失败不可怕,可怕的是你没有从这次的失败中汲取经验和教训,而让自己在同一个坑里摔了一遍又一遍。

听完他们的学习经验,你是否对自己的学习也有一个重新的认识和规划?希望在即将到来的12月ACCA考试中,你也能够成功脱坑志得意满。

2016accaf7考试攻略:f7考试技巧及复习方法2016accaf7考试攻略:f7考试技巧及复习方法 2016年03月11日点击免费领取:ACCA学习资料大礼包ACCA F7科目是ACCA的技能阶段科目中的一个科目,也是相对比较简单的科目,即使是比较简单的,对于ACCA初学者来说还是有一定困难的,下面就为大家总结一下ACCA F7考试攻略,其中包括F7考试特点,注意事项,学习方法,希望对各位考生学习ACCA提供帮助!ACCA F7考试攻略之ACCA F7课程特点:第一,强调国际会计准则的实际运用。

第二,第二,计算比重大。

ACCA F7考试攻略之ACCAF7课程注意事项:第一,死记硬背国际会计准则的原则是远远不够,更需要的是结合题目的情景去灵活运用。

第二,要做到上述这点,**途径是多做练习题。

只有通过大量的练习,记忆的准则才得以灵活运用。

第三,攻克“计算比重大”这一特点,**途径依然是多做练习题,无他。

ACCA F7考试攻略之ACCA F7学习方法:第一、关于复习时间的安排从开始考ACCA,我的复习基本都是从考试前一个半月左右开始正式的复习,每天保持在2小时左右,到距考试还有一周的时候会把时间增加到3-4小时。

(PS.每学期学校都有相关ACCA的课程,平时上课也就是听听课,做做笔记,但是到真正的备考状态的时候自己真正对书本的了解程度仅有20%)第二、关于备考过程需要准备的资料kaplan或者BPP的教材练习册,最近的10套左右的历年真题加上pilot paper,串讲课以及串讲的讲义。

这些资料如果能够很好的利用考试足够应对。

第三、关于F7的复习F7的复习算是开始的比较晚的,考前不到一个月的时候,F7的基础依旧停留在只知道合并报表的时候有五个必须的步骤,但是具体该怎么写还是不清楚。

重新把书每天过一章,认认真真的做一遍教材里的例题,注意是教材不是练习册,确定教材里的每一个知识点都掌握了。

这里的教材比较推荐bpp的,kaplan讲的有些过于简单了。

F7的考试题型比较固定,前面两个大题一题是合并报表,另一题是独立做一张报表。

针对这两题,上网课的时候老师会带领你一起写分录,写好分录的第一保证就是能让你的报表看起来是平的,因为每一笔都是一借一贷。

所以,有了平的保证能让我们在考场上更有信心的做后面的题目。

同时较好的完成前面两题也为我们通过F7打下基础。

所以我的建议是,在学习F7的时候,尽量多写分录。

对于后面的4-5题是针对具体某个准则的考察,这些准则都有可能出现在第一和第二题的notes中,所以当时老师给的建议是,做熟第一第二题,再在考前准备时,花时间看一下历年考题。

对于第3题一般是现金流量表的考察或者是基于一些ratio的分析,现金流量表作平比较困难,但是其每一步都有分,也有很多easy marks,所以再考试时,如果遇到不平,不用花大把时间在做平上,可以更加注意易得分的科目。

对于ration analysis,比较有效的方法是掌握其含义,看几年例题后,再考场上结合题目背景回答。

最后,也再次感谢网校的老师,其独特的理解以及内容与题目结合的教学方法给我们打下了扎实的基础。

标题:泽稷网校ACCA F7考试注意事项解析

1.仔细读题

不要急着做题,题目可以读两遍甚至三遍。

这不是浪费时间,是确保答题所问。

2.写好Working

Working要写详细,并有序号对照。

即使答案错了,只要方法正确也会得分。

3.注意控制答题时间

不要在任何题目上超时,保证每道题都做,题目中如有做不出的难点,可以放弃,以确保拿到题目中简单易得的分数。

4.不要答非所问

在讨论题目中,要确定你答的是题目问的问题。

不要答一些与题目无关的内容,因为不会得分。

5.财务报表要用固定格式

虽然格式本身没有分数,但它可以让你把那些明显的答案写下来,获得简单易得的分数,又可以确保不会落掉任何项目。

6.不要过多计算ratio

财务报表解读的题目,注意不要计算过多的不必要的比率,完全重复题目里的信息是没有分数的。

正确的做法是必须对题目中的信息做出评估,并且分析可能的原因,得出结论。

2016年3月ACCA考试F7考前tips

MCQ’s can come from any syllabus area.

Consolidation of Financial Statements

For the consolidation question (Q1) you will benefit from having the proforma/standard workings of your final answer set up first. For example if the question requires a consolidated SFP then drawing up the SFP with open brackets beside those numbers that do not need a standard working can get all the easy adding across 100% of the Parent and subsidiary figures. The other headings can have the standard working number written beside them instead. A couple of lines would need to be left for each section of the SFP in case other things come up in the additional information.

In addition to this setting up the standard workings can also be done. The subsidiar ies’ share capital figures and the year end retained earnings can be put into these without reading any of the additional information. In addition to this the parents retained earnings figure can also be put into W5 (Retained earnings) without reading any additional narrative.

With all of the proformas and standard workings set up, it means that you are able to tackle the issues in the order that they are presented in the question. It also allows you to deal with both sides of any adjustments as everywhere is set up to make the adjustments. It hopefully prevents non-balancing accounts and means that each issue only has to be addressed once; thus helping with time management. Also if you run out of time, you will get full credit for all that you have already done provided everything is referenced through.

A similar process can be applied to the income statement equivalent of setting up final answer and workings to help tackle the issues that come up.

Single Company Financial Statements

Single company financial statements (question 2). As with the groups question, it may be possible to get the proforma of the final answer set up, particularly if the data in the question is set up with the draft financial statements rather than the trial balance. If possible it then means that open brackets can be used and the draft figures placed in them, ready for adjustments as they arise. Generally speaking there are often

more adjustments required for cost of sales figure in the income statement and the PPE figure in the SFP. As such I would suggest these are likely to need separate workings rather than just a bracket beside the final answer.

If there is a topic/adjustment that you are unsure of, come back to it. You are better to get the adjustments that you are comfortable with done first. It is easy to get bogged down and waste time on a difficult adjustment at the expense of doing an easier one that appears later in the question.

Performance Appraisal

With a performance appraisal question you may be asked to calculate ratios or prepare a statement of cash flow or both. When calculating ratios, if you are unsure of a particular calculation always have a go, as even if the calculation is incorrect you will be awarded merit for your discussion of the incorrect number in the written section of the question. It also really helps the marker if you note your formula down so that your working is clearly identified.

When preparing a statement of cash flow setup you proforma immediately and begin to get the easy marks in the cash flow such as finding the movement in the cash and cash equivalent balance, and finding the movements on basic shares and loans. You will also find the operating activities section familiar and useful for scoring marks. If there are any cash items that you are unfamiliar with come back to these at the end after you have dealt with the items that you can do.

Finally, when appraising the performance of a company ensure that you always refer to the scenario provided to ensure maximum credit is awarded.。