Chap-08

- 格式:ppt

- 大小:924.00 KB

- 文档页数:61

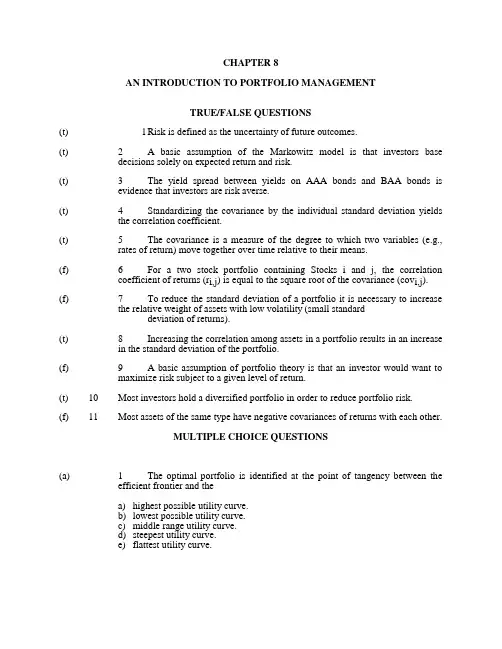

CHAPTER 8 AN INTRODUCTION TO PORTFOLIO MANAGEMENT TRUE/FALSE QUESTIONS (t) 1 Risk is defined as the uncertainty of future outcomes. (t) 2 A basic assumption of the Markowitz model is that investors base decisions solely on expected return and risk. (t) 3 The yield spread between yields on AAA bonds and BAA bonds is evidence that investors are risk averse. (t) 4 Standardizing the covariance by the individual standard deviation yields the correlation coefficient. (t) 5 The covariance is a measure of the degree to which two variables (e.g., rates of return) move together over time relative to their means. (f) 6 For a two stock portfolio containing Stocks i and j, the correlation coefficient of returns (ri,j) is equal to the square root of the covariance (covi,j). (f) 7 To reduce the standard deviation of a portfolio it is necessary to increase the relative weight of assets with low volatility (small standard deviation of returns). (t) 8 Increasing the correlation among assets in a portfolio results in an increase in the standard deviation of the portfolio. (f) 9 A basic assumption of portfolio theory is that an investor would want to maximize risk subject to a given level of return. (t) 10 Most investors hold a diversified portfolio in order to reduce portfolio risk. (f) 11 Most assets of the same type have negative covariances of returns with each other. MULTIPLE CHOICE QUESTIONS (a) 1 The optimal portfolio is identified at the point of tangency between the efficient frontier and the a) highest possible utility curve. b) lowest possible utility curve. c) middle range utility curve. d) steepest utility curve. e) flattest utility curve. 1 (d) 2 An individual investor’s utility curves specify the tradeoffs he or she is willing to make between a) high risk and low risk assets. b) high return and low return assets. c) covariance and correlation. d) return and risk. e) efficient portfolios. (c) 3 As the correlation coefficient between two assets decreases, the shape of the efficient frontier a) approaches a horizontal straight line. b) bends out. c) bends in. d) approaches a vertical straight line. e) none of the above. (d) 4 A portfolio manager is considering adding another security to his portfolio. The correlations of the 5 alternatives available are listed below. Which security would enable the highest level of risk diversification a) 0.0 b) 0.25 c) -0.25 d) -0.75 e) 1.0 (b) 5 A positive covariance between two variables indicates that a) the two variables move in different directions. b) the two variables move in the same direction. c) the two variables are low risk. d) the two variables are high risk. e) the two variables are risk free. (c) 6 A positive relationship between expected return and expected risk is consistent with a) investors being risk seekers. b) investors being risk avoiders. c) investors being risk averse. d) all of the above. e) none of the above. 2 (d) 7 What information must you input to a computer program in order to derive the portfolios that make up the efficient frontier a) Expected returns, covariances and correlations. b) Standard deviations, variances and covariances. c) Expected returns, standard deviations and variances. d) Expected returns, variances and correlations. e) Covariances, correlations and variances. (d) 8 The Markowitz model is based on several assumptions regarding investor behavior. Which of the following is an assumption of the Markowitz model? a) Investors consider investment alternative as being represented by a joint probability distribution of expected returns over some holding period. b) Investors minimize one-period expected utility. c) Investors estimate the risk of the portfolio on the basis of their utility functions. d) Investors base decisions solely on expected return and risk. e) None of the above. (a) 9 As the correlation coefficient between two assets increases, the shape of the efficient frontier a) approaches a horizontal straight line. b) bends out. c) bends in. d) approaches a vertical straight line. e) none of the above. (d) 10 The probability of an adverse outcome is the definition of: a) Statistics. b) Variance. c) Random. d) Risk. e) Semivariance. (c) 11 Which of the following is a measure of risk? a) Range of standard deviations b) Expected return c) Standard deviation d) Covariance e) Correlation 3 (b) 12 Semivariance, when applied to portfolio theory, is concerned with the a) Square root of deviations from the mean. b) Deviations below the mean. c) Deviations above the mean. d) All deviations (above and below the mean). e) Summation of the squared deviations from the mean. (a) 13 With low, zero or negative correlations it is possible to derive portfolios that have a) Lower risk than the individual securities in the portfolio. b) Lower risk than the highest risk individual security in the portfolio. c) Higher risk than the individual securities that make up the portfolio. d) Higher risk than the highest risk individual security in the portfolio. e) None of the above. (d) 14 Which of the following statements are correlation coefficient is false? a) The values range between -1 to +1. b) A value of +1 implies that the returns for the two stocks move together in a completely linear manner. c) A value of -1 implies that the returns move in a completely opposite direction. d) A value of zero means that the returns are zero. e) None of the above (that is, all statements are true) (a) 15 In a two stock portfolio, if the correlation coefficient between two stocks were to decrease over time everything else remaining constant the portfolio's risk would a) Decrease. b) Remain constant. c) Increase. d) Fluctuate positively and negatively. e) Be a negative value. (d) 16 Given the following correlations between pairs of stocks, a portfolio constructed from which pair will have the lowest standard deviation? Correl(A,B) = 0, Correl(C,D) = 1, Correl(E,F) = 0.75, Correl(G,H) = -0.75, Correl(I,J) = -0.50. a) Pair A,B b) Pair C,D c) Pair E,F

Product Data Sheet

Edition 29.01.2008

Revision no: 01

Identification no:

01 08 03 04 001 0 000006

Sika®Chapdur

1 1/4 Construction

Sika®ChapdurSika®Chapdur (Sikafloor®-3 QuartzTop TR)

Coloured mineral dry shake floor hardener

Product

Description Sika®Chapdur is a one part, preblended, coloured mineral dry shake hardener for

concrete comprising of cement, specially selected quartz mineral aggregates,

admixtures and pigments.

Uses n Sika®Chapdur provides a hard wearing, mineral dry shake topping for monolithic

floors. When sprinkled and trowelled into fresh wet concrete floors, it forms a

coloured, wear resistant smooth surface

n Typical uses are in warehouses, factories, shopping malls, public areas,

restaurants and museums

Characteristics /

Advantages n Good wear resistance rating

n Impact resistance

一.LCP协商阶段

GTM900→ISP(LCP REQ)

GTM900向ISP发送LCP REQUEST数据包

W: 7E //flag

FF //address

03 //control C0 21 //协议域,0xC021表示LCP协议

01 //code,01代表configure_request 00 //标识符identifier

00 17 //长度

02 06 00 00 00 00 //表示选项的type为2,06为长度,00 0A 00 00表示ACCM选项的

数据域. ************ //选项type为5,表示magic number,06为长度,后面的是内容 07 02 //选项type为7表示协议域压缩

08 02 //选项type为8表示地址控制域压缩

0D 03 06 //选项type为0D表示回调(Callback)

CA 93 //表示FCS

7E //flag ISP→GTM900(LCP REJ)

ISP向GTM900发送LCP REJECT数据包,表明不支持Magic Number与Callback。

R: 7E

FF 03 C0 21 04 // 表示Configure-Reject

00 //标识符

00 0D //长度

************//magicnumber(被拒绝的选项配置) 0D 03 06 //Callback(被拒绝的选项配置)

D9 EA //FCS

7E

GTM900→ISP(LCP REQ) GTM900向ISP再一次发送LCP REQUEST数据包,此次取消了Magic Number与Callback

W: 7E

FF 03

C0 21

01 //configure_request 01 //标识符+1

00 0E // 长度

02 06 00 00 00 00 //表示选项的type为2,06为长度,00 00 00 00表示ACCM选项的数

MBA全套讲义教材总目录E-commerceEMBA

E-commerce

EMBA

MBA治理技巧

MBA系列教材

MBA遠景教材

MBA资料

财务、金融与保险

财务治理

电子图书

治理概论

治理类

广告与品牌治理

国际贸易

宏观经济学课件

会计

会计类

技术经济

经济法

经济学类

决策分析

期货

清华大学MBA课件

商务技能

生产治理

市场调研

市场营销

统计学

投资学 现代操纵理论

现代操纵理论1

项保华治理随笔

消费者行为学

运筹学

战略治理

证券

职业生涯

专题类

详细名目:

MBA-mulu.doc

MBA-mulu.rar

MBA全套讲义教材名目.doc

文件夹: E-commerce

C_shareBeijing Institute of TechnologyMarketing on the InternetLecture 3.ppt

Class Discussion 2 - HP.doc

Group Project and Presentation.doc

Lecture 4.ppt

Lecture 5.ppt

Lecture 8.ppt

Lecture 9.ppt

Marketing on the Internet Lecture.ppt

文件夹: E-commerce\Sample Paper

egolddragon.doc

footmax.doc

ppmatrix.doc prettygirl_doc.doc

Qubric.doc

文件夹: EMBA

01EMBA-1.ppt

01EMBA-2.ppt