DSGE模型及其在ECB中的运用

- 格式:pdf

- 大小:381.27 KB

- 文档页数:15

作者简介:张杰平(1982-),男,福建泉州,中国人民大学经济学院2009级博士生,研究方向:现代宏观经济学。

《经济问题探索》2012年第4期欧洲中央银行宏观计量模型张杰平(中国人民大学经济学院,北京100872)摘要:中央银行利用宏观计量模型以政策分析和经济预测,从二十世纪四十年代建立的第一代宏观计量模型开始,就已成为世界上许多国家的共识。

目前,各国使用的宏观计量模型已从传统的凯恩斯主义结构宏观计量模型转变为动态随机一般均衡模型(Dynamic Stochastic General Equilibrium ,DSGE )的宏观计量模型。

世界上第一个DSGE 宏观计量模型是由欧洲中央银行首先开发使用的,即在CEE 模型基础上所建立的SW 模型,而且目前为了研究不同的问题,欧洲中央银行又开发了多个其他相关模型。

本文旨在系统介绍欧洲央行开发的DSGE 模型的特点和用途并作深入的评析,这些模型包括SW 、NAWM 、CRM 、EAGLE 和NMCM 等模型。

最后,还将分析我国的相关研究情况并提出相应的政策建议。

关键词:动态随机一般均衡模型;宏观计量模型;中央银行;SW 模型一、前言自从宏观经济学于20世纪30年代出现以来,各国中央银行就先后应用宏观经济模型于各国的宏观政策分析中。

而中央银行所用的宏观经济模型一般称为宏观计量模型(Macro -econometric model ),它主要是经济预测和政策分析的工具。

经济预测指的是,宏观经济中主要经济变量(如GDP 、通货膨胀率和利率等)在将来会怎么发生变化,这就需要应用相应的宏观经济模型在经济过去以及现在发展情况的基础上做出预测;而政策分析,是指政府执行政策时,通过影响短期利率等变量将会怎样影响经济中的其他变量(如GDP 、通货膨胀和就业等)。

过去近百年时间,宏观计量模型经历了从丁伯根1930年代建立的关于荷兰和美国的第一个宏观计量模型,到1940年由考尔斯委员会所主持建立的并盛行于各个国家的凯恩斯主义结构宏观计量模型,再到目前各国中央银行统一使用的DSEG 宏观计量模型,即下面将介绍的第四代宏观计量模型。

DSGE模型下地方政府与金融部门的关系:综述与展望摘要:地方政府与金融部门之间的关系是宏观经济研究中既重要又亟待研究的问题,研究成果广阔且丰富,在未来一段时间内仍会受到金融研究部门和决策部门重视。

本文总结相关研究文献,从现有研究的角度阐述地方政府与金融部门关系的演进历程,重点介绍动态随机一般均衡(DSGE)模型在其中的应用与发展,对现有文献进行整理,进行综合述评与展望,把握DSGE模型在地方政府、金融部门与金融加速器中应用趋势,希冀为今后地方政府与金融部门关系的研究提供一些可行的建议。

关键词:DSGE模型机;地方政府;金融部门;金融加速器1 引言自改革开放以来,中国经济迎来了飞速发展的“黄金时期”,但随后爆发的金融危机也使我国经济陷入泥潭。

为应对经济冲击,各地方政府陆续开启经济刺激计划,导致在未来宏观经济发展过程,我国地方政府债务逐年升高,这一举措给中国经济埋下了隐患。

金融部门是我国经济运转的核心,与其他部门直接或间接相连,金融部门风险可能外溢至其他部门从而导致系统性金融风险发生。

因此,在宏观领域的研究中,地方政府与金融部门之间的关系研究既重要又亟待解决。

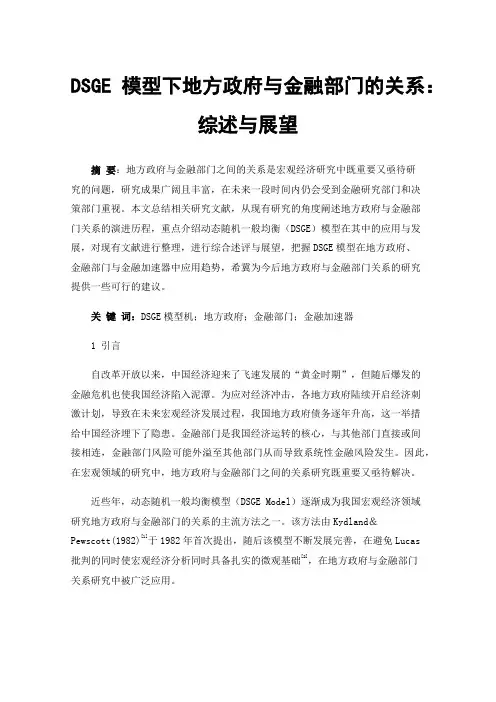

近些年,动态随机一般均衡模型(DSGE Model)逐渐成为我国宏观经济领域研究地方政府与金融部门的关系的主流方法之一。

该方法由Kydland&Pewscott(1982)[1]于1982年首次提出,随后该模型不断发展完善,在避免Lucas批判的同时使宏观经济分析同时具备扎实的微观基础[2],在地方政府与金融部门关系研究中被广泛应用。

图1 DSGE模型结构与应用在面对随机的外部冲击时,很多传统假定都会被打破,模型分析预测结果存在偏差,难以给政策实施提供有效的参考,近年利用DSGE模型的研究则填补了这一缺口,其优势与应用详见图1。

但DSGE模型在模型构建和估计方法上十分复杂,在国内发展于应用仍然受到限制。

本文基于动态随机一般均衡模型(DSGE)研究框架,旨在梳理关于地方政府与金融部门关系研究的文献,对这一领域现有文献进行述评,把握最新趋势。

基于DSGE模型的中国货币政策传导机制研究基于DSGE模型的中国货币政策传导机制研究摘要:货币政策传导机制研究是货币政策制定与实施的重要课题。

本文基于动态随机一般均衡(DSGE)模型,深入研究中国的货币政策传导机制。

首先,介绍了DSGE模型的基本原理和框架,并阐述了该模型在研究货币政策传导机制方面的优势。

随后,对中国货币政策传导机制的核心要素进行分析,包括货币供应、经济体中的部门结构以及金融市场的特点等。

在此基础上,构建了适用于中国的DSGE模型,并通过模型模拟分析,得出了关于中国货币政策传导机制的一些重要结论。

最后,对当前中国货币政策的研究进行总结,并提出一些建议,以进一步深化研究和完善中国的货币政策传导机制。

关键词:货币政策,传导机制,DSGE模型,中国,经济体第一章绪论1.1 研究背景和意义货币政策传导机制是指中央银行通过货币政策工具对经济体实施影响,以达到调控宏观经济的目标的过程。

货币政策传导机制的研究对于货币政策的制定和执行至关重要,能够提供政策制定者有关货币政策工具选择和调整的重要依据,同时也有助于深化对经济体内各种因素与经济活动之间关联的理解。

随着中国经济的快速发展和金融市场的改革开放,中国的货币政策传导机制研究日益受到高度关注。

然而,由于中国经济的特殊性和金融市场的复杂性,传统的线性经济模型在解释中国货币政策传导机制方面存在一定的局限性。

因此,基于DSGE模型的研究方法正逐渐成为理论界和实证研究中的主流方法,能够更好地揭示中国货币政策传导机制的内在机理和动态调整过程。

1.2 研究内容和方法本文旨在基于DSGE模型深入研究中国货币政策传导机制,并通过模型模拟分析,得出一些关于中国货币政策传导机制的重要结论。

具体而言,本文以中国经济为背景,通过建立适用于中国的DSGE模型,研究中国货币供应的传导机制、不同经济体中的部门结构对货币政策影响的差异以及金融市场的特点对货币政策传导的影响等核心问题。

欧洲中央银行经济预测模型方法欧洲中央银行(ECB)是欧洲货币联盟成员国的中央银行,负责维护欧元区的货币稳定和经济平衡。

为了实现这一目标,ECB使用各种经济预测模型来分析和预测欧元区的经济状况。

下面将介绍一些常用的经济预测模型方法。

1. VAR模型(Vector Autoregression Model)VAR模型是一种广泛应用的宏观经济模型,用于描述经济变量之间的相互关系。

VAR模型通过引入多个经济变量的滞后值,捕捉它们之间的动态关系,从而预测未来的经济走势。

ECB常常使用VAR模型来预测未来的通胀率、利率、失业率等重要的经济指标。

2. DSGE模型(Dynamic Stochastic General Equilibrium Model)DSGE模型是一种基于微观经济理论的宏观经济模型。

DSGE模型通过建立一组动态的一般均衡方程,描述经济主体的决策行为和市场的供需关系。

ECB使用DSGE模型来分析经济政策的效果和预测经济的长期趋势。

3.大数据分析(Big Data Analysis)随着信息技术的快速发展,大数据分析成为一种重要的经济预测方法。

ECB收集和分析大量的经济数据,包括消费者信心指数、零售销售数据、就业数据等,利用数据挖掘和机器学习技术来预测经济的发展趋势。

大数据分析可以帮助ECB更准确地预测经济增长、通胀压力和资产价格波动等重要指标。

4.社会网络分析(Social Network Analysis)社会网络分析是一种基于网络结构的经济预测方法。

ECB通过研究金融机构、企业和个人之间的社会关系网,分析其对经济的影响和传导机制。

社会网络分析可以帮助ECB预测金融风险的传播路径,为制定金融监管政策提供参考。

5.预测市场分析(Prediction Market Analysis)预测市场是一种基于交易市场的经济预测方法。

ECB利用预测市场的交易数据,例如期权、期货和衍生品的价格,来预测未来的经济走势。

基于DSGE模型的货币政策和财政政策效应研究

徐丽兰;黄阳平

【期刊名称】《泉州师范学院学报》

【年(卷),期】2017(035)005

【摘要】通过构建新凯恩斯动态随机一般均衡模型(DSGE),探索我国在封闭经济体制下正确制定财政政策和货币政策的重要意义和政策建议.选取2004-2015年的季度数据,采取贝叶斯估计方法进行数值模拟,并借助脉冲响应分析外生冲击的传导,最后得出以下结论:DSGE模型与我国宏观经济数据的拟合度较高,可以用来分析解决我国经济中出现的问题;财政政策和货币政策应当相机抉择,搭配使用;积极的财政政策对于治理经济危机具有重要意义;货币政策对于治理通货膨胀具有显著作用,因此政府在制定货币政策时需要充分考虑通货膨胀因素的影响.

【总页数】10页(P86-95)

【作者】徐丽兰;黄阳平

【作者单位】集美大学财经学院,福建厦门361021;集美大学区域研究中心,福建厦门361021

【正文语种】中文

【中图分类】F015

【相关文献】

1.财富效应、经济稳定与货币政策选择——基于中国DSGE模型的实证研究 [J], 谢绵陛

2.我国货币政策对房地产市场调控的非对称效应研究r——基于DSGE模型的分析[J], 郭娜;刘镇林;章倩

3.中国货币政策冲击预期效应的实证研究——基于贝叶斯推断的BVAR、BSVAR、BVECM和BDSGE模型 [J], 袁靖;孙爱玲

4.基于DSGE模型的货币政策区域效应研究 [J], 段胜军;李云春

5.高低杠杆下货币政策冲击效应与去杠杆过程中的货币政策平稳性——基于DSGE 模型的金融加速器效应检验 [J], 骆祚炎;陈博杰

因版权原因,仅展示原文概要,查看原文内容请购买。

基于DSGE模型的中国货币政策传导机制研究中国货币传导机制是指货币通过各种渠道对经济体产生影响的过程。

在过去的几十年里,中国的货币传导机制经历了多次调整和改革,以适应经济发展和市场变化。

近年来,随着中国经济的转型和结构调整,对货币传导机制的研究变得尤为重要。

本文基于DSGE模型,旨在深入研究中国货币传导机制,并探讨其对经济波动和稳定的影响。

首先,我们需要了解DSGE模型是什么以及其在宏观经济学中的应用。

DSGE模型是动态随机一般均衡模型(Dynamic Stochastic General Equilibrium Model)的简称。

它是一种用来描述宏观经济体系中各个决策者(家庭、企业、相关部门)行为规律及其相互关系,并通过均衡条件描述市场供求关系和资源配置效率等问题。

在研究中国货币传导机制时,我们需要构建一个包含家庭、企业、银行等主要决策者行为规律以及它们之间相互关系的DSGE模型。

首先,我们需要考虑家庭部门的行为。

家庭在决定消费和储蓄时,会考虑到货币对利率和通货膨胀的影响。

其次,我们需要考虑企业部门的行为。

企业在决定投资和生产时,会考虑到货币对利率、信贷条件和市场需求的影响。

此外,我们还需要考虑银行部门的行为。

银行在决定贷款利率、信贷投放量等方面会受到货币和监管的影响。

通过对上述各个部门行为规律进行建模,并通过均衡条件描述市场供求关系和资源配置效率等问题,我们可以得到一个描述中国经济体系中各个决策者相互关系并受到货币传导机制影响的DSGE模型。

基于该模型,我们可以进行一系列实证研究来深入了解中国货币传导机制及其对经济波动和稳定的影响。

首先,我们可以通过实证分析来估计该模型中各个参数,并检验模型是否能够较好地拟合实际数据。

其次,我们可以使用该模型来研究货币冲击对经济体的影响。

通过对模型中的货币冲击进行模拟,我们可以得到货币对经济增长、通货膨胀、利率等变量的影响路径。

此外,我们还可以通过该模型来研究货币传导机制的非线性特征。

dsge bk条件-概述说明以及解释1.引言1.1 概述在DSGE模型中,我们经常面临的一个重要问题是如何将宏观经济理论和数据相结合。

在实证经济学中,用于估计和验证经济模型的方法有很多种,其中一种广泛应用的方法是Bayesian方法。

Bayesian方法是一种基于贝叶斯定理的统计推断方法,它依赖于先验概率和样本信息,通过计算后验概率来进行参数估计和模型验证。

在DSGE 模型中,我们可以利用Bayesian方法对模型参数进行估计,并将这些参数用于进行政策分析和预测。

然而,由于DSGE模型的复杂性和计算上的困难,仅仅依靠贝叶斯方法进行参数估计是不够的。

为了解决这个问题,经济学家开发了一种称为DSGE模型的后验估计方法,即DSGE-BK条件。

DSGE-BK条件是一种引入先验分布的标准贝叶斯框架,并且在这个框架下,DSGE模型的参数估计问题可以转化为一个优化问题。

具体来说,在DSGE-BK条件下,我们引入先验分布作为参数的权重,并通过最大化后验概率来确定最优的参数估计值。

通过DSGE-BK条件,我们不仅可以得到参数的点估计值,还可以获得参数的置信区间。

这样,我们就可以更准确地评估模型的可靠性,并在进行政策分析和预测时提供更可靠的结果。

总之,DSGE-BK条件提供了一种有效的方法来估计DSGE模型的参数,并在进行经济政策分析和预测时提供更可靠的结果。

在接下来的章节中,我们将详细介绍DSGE-BK条件的具体方法和应用。

1.2 文章结构文章结构部分的内容可以包括以下信息:文章结构是指整篇文章的组织方式和各个部分之间的关系。

一个清晰的文章结构可以帮助读者更好地理解文章的内容和逻辑,同时也有助于作者合理安排材料和思路的呈现。

本文的结构主要分为引言、正文和结论三个部分。

在引言部分,我们将对文章的主题进行概述,向读者介绍DSGE BK 条件的背景和重要性。

同时,我们还会说明文章的结构,以帮助读者了解整篇文章的组织方式和各个部分的内容。

基于DSGE模型的信贷、货币供应量传导研究

李松华

【期刊名称】《工业技术经济》

【年(卷),期】2012(000)011

【摘要】本文通过构建一个包含金融市场的新凯恩斯动态随机一般均衡模型,考察了贷款、货币供应量冲击在我国经济中的传导.采用了贝叶斯方法估计DSGE模型的参数,并运用脉冲响应分析冲击的传导.研究发现,DSGE模型对我国的经济数据拟合较好,且动态地刻画了冲击的传导过程;贷款和货币供应量冲击主要通过投资影响产出,而消费对冲击的传导作用较小.

【总页数】9页(P109-117)

【作者】李松华

【作者单位】华北水利水电学院,郑州450011;中国科学院,北京100190

【正文语种】中文

【中图分类】F821.0

【相关文献】

1.基于DSGE模型的利率传导机制研究 [J], 李松华

2.基于DSGE模型的影子银行与信贷传导研究 [J], 王苏生;赵芳;陈刚

3.企业影子银行化与货币政策信贷渠道传导\r——基于DSGE模型的分析 [J], 毛泽盛;周舒舒

4.互联网技术对中国宏观经济的动态效应及传导机制研究——基于DSGE模型的实证分析 [J], 徐晔;黄文

5.论房价波动的区域间传导——基于两地区DSGE模型与动态空间面板模型的研究 [J], 高然;龚六堂

因版权原因,仅展示原文概要,查看原文内容请购买。

dsge贝叶斯估计实体经济体和模拟经济体参数DSGE模型是动态随机一般均衡模型的简称,是一种在宏观经济学领域常用的建模工具。

DSGE模型通过描述个体经济行为,将微观经济理论与宏观经济现象联系起来,是理解经济体系复杂内部结构的有力工具。

贝叶斯估计是一种统计方法,可以用来估计模型的参数,并且能够提供关于参数不确定性的信息。

模拟经济体参数是指根据模型,对经济体参数进行模拟分析,以此来预测未来的宏观经济变化趋势。

在DSGE模型中,经济体的行为可以用一组方程式描述,这些方程式涉及到劳动力供给、企业投资、货币政策等多个领域。

而这些方程中的参数值通常是未知的,需要通过估计来获得。

传统的估计方法有最小二乘法和极大似然估计等,但这些方法对参数的不确定性处理比较困难。

贝叶斯估计则是一种更灵活、能够处理不确定性的估计方法,它可以使用先验分布来描述参数的不确定性,通过观测数据来更新参数的分布,得到后验分布,从而对参数进行估计。

对于DSGE模型的参数,模拟分析是非常重要的。

通过对模型中参数进行模拟,可以得到未来经济体的状态变化,并且可以根据不同参数值的模拟结果来评估政策的效果。

通过对货币政策参数进行模拟,可以评估不同政策对通货膨胀和失业率的影响,为制定货币政策提供重要参考。

DSGE模型的贝叶斯估计和模拟经济体参数是一种将宏观经济理论和微观经济行为联系起来的重要方法。

通过对经济体的行为进行模拟和估计,可以更好地理解和预测宏观经济现象,为经济政策的制定提供有力支持。

在我看来,DSGE模型的贝叶斯估计和模拟经济体参数能够更好地处理参数的不确定性,提高了对经济体的了解和预测的准确性。

这种方法也更有利于制定能够更好地适应未来经济发展的政策。

我认为这种方法在宏观经济学中具有重要的意义。

通过本文的讨论,我对DSGE模型的贝叶斯估计和模拟经济体参数有了更深入的理解。

这种方法不仅可以对经济体的参数进行更准确的估计,还可以通过模拟分析来更好地预测未来的宏观经济变化,为经济政策的制定提供更好的支持。

基于贝叶斯分析框架下的VAR和DSGE模型作者:阳晓明来源:《当代教育理论与实践》 2014年第4期阳晓明(湘潭大学商学院,湖南湘潭411105)摘要:回顾应用宏观经济学的主要分析方法和最新进展,现有校准、向量自回归、一般矩方法和极大似然估计等方法都存在诸多缺点,而贝叶斯分析框架的引入能有效地应对这些问题。

贝叶斯分析方法能很好地将微观文献和宏观研究相结合,将经济理论、数据和政策分析融为一体,而且很适合进行模型比较和政策分析。

基于我国转轨经济和宏观数据的特点,贝叶斯方法将在我国宏观经济建模和预测,中央银行制定和执行货币政策中发挥重要作用。

关键词:应用宏观经济学;贝叶斯分析;中国经济中图分类号:F062.4文献标志码:A文章编号:1674-5884(2014)04-0178-051引言宏观经济学在20世纪30年代“凯恩斯革命”中成为独立的研究领域。

应用宏观经济学一直是宏观经济学中最为活跃的研究领域之一,各种新思路、新方法层出不穷。

“凯恩斯革命”之后的几十年中,由凯恩斯理论导出的结构方程方法成为宏观经济学实证研究的主要方向。

但是20世纪70年代由于受到卢卡斯批判(Lucascri�tique)和宏观经济模型商业应用的冲击,考尔斯委员会(Cowlescommission)结构性联立方程组模型逐渐失去其在应用宏观经济学中的统治地位。

20世纪80年代以后,由于KydlandandPrescott(1982)和LongandPlosser(1983)的开创性工作,第一代动态随机一般均衡(DSGE)模型以(KydlandandPrescott为代表的RBC模型)成为宏观经济学的主流理论方法,许多实证宏观计量方法也围绕如何估计和评价DSGE模型展开[1]。

在实证宏观计量方法方面,经济学家提出了许多正式和非正式的数量方法,如向量自回归(VAR)方法、校准(calibration)方法、一般矩估计方法(GMM)及完全信息极大似然估计(MLE)方法等等。

我国DSGE模型的开发及在货币政策分析中的应用一、本文概述本文旨在探讨我国DSGE(动态随机一般均衡)模型的开发过程及其在货币政策分析中的应用。

DSGE模型作为一种重要的宏观经济分析工具,能够在不确定性的环境下,通过模拟经济系统的动态响应,为政策制定者提供决策依据。

在我国,随着经济的不断发展和开放程度的提高,货币政策在宏观调控中的作用日益重要,因此,研究和开发适合我国国情的DSGE模型,对于提升货币政策的科学性和有效性具有重要意义。

本文将首先介绍DSGE模型的理论基础和构建方法,包括模型的基本结构、参数设定、数据校准等步骤。

然后,结合我国经济的实际情况,详细阐述我国DSGE模型的开发过程,包括模型的设定、参数的估计和校准、模型的验证等。

接着,本文将重点分析我国DSGE模型在货币政策分析中的应用,包括货币政策对经济的影响、货币政策的传导机制、货币政策的优化等问题。

本文还将对DSGE模型在我国的未来发展前景进行展望,并提出相关政策建议。

通过本文的研究,我们期望能够为政策制定者提供一个科学、有效的决策工具,帮助他们更好地理解和把握我国经济的运行规律,制定更加合理、有效的货币政策,以促进我国经济的持续、健康发展。

二、DSGE模型的理论基础DSGE模型,即动态随机一般均衡模型(Dynamic Stochastic General Equilibrium Model),是现代宏观经济学中用于理解和分析经济系统动态行为的重要工具。

DSGE模型以一般均衡理论为基础,将微观经济主体的行为方程和宏观经济总量方程结合在一起,构建一个包含多种经济变量和微观经济主体行为的闭环系统。

一般均衡理论:DSGE模型在本质上是一种一般均衡模型,它假设经济中的所有市场都是出清的,即供给等于需求。

这意味着模型中的所有价格都是内生决定的,而不是外生给定的。

微观经济主体行为方程:DSGE模型详细描述了不同类型经济主体(如家庭、厂商、政府等)的行为方程,包括消费、投资、生产、劳动供给等决策过程。

基于DSGE模型的中国货币政策规则适用性研究

叶娅芬;曹慧;梁姣;周明华;袁教育

【期刊名称】《浙江工业大学学报》

【年(卷),期】2014(042)002

【摘要】采用宏观经济分析的主流工具DSGE模型研究小型开放经济条件下中国货币供应量规则和利率规则的适用性,模型参数估计借助贝叶斯估计方法,货币政策规则影响效果采用MCMC模拟技术.研究结果发现:中国货币供应量规则和利率规则各具优势,并且两者具有很强的内生联动性,货币供应量的增长导致利率的上升.由此可见:当前货币供应量规则不宜由利率规则完全取代,中国应坚持两种规则并用的复合规则体系,从而为央行做出相关决策提供量化支持.

【总页数】6页(P225-230)

【作者】叶娅芬;曹慧;梁姣;周明华;袁教育

【作者单位】浙江工业大学之江学院,浙江杭州310024;浙江工业大学理学院,浙江杭州310023;浙江工业大学理学院,浙江杭州310023;浙江工业大学理学院,浙江杭州310023;华龙碧水幼儿园,浙江杭州310052

【正文语种】中文

【中图分类】O212

【相关文献】

1.中国最优货币政策规则选择——基于新凯恩斯主义DSGE模型分析 [J], 楚尔鸣;许先普

2.房地产价格与我国货币政策规则——基于多部门NK-DSGE模型的研究 [J], 徐妍;郑冠群;沈悦

3.中国最优货币政策规则选择研究-基于中国宏观数据估计的DSGE模型比较 [J], 刘震;蒲成毅

4.DSGE模型、货币政策规则与汇率波动分析 [J], 尹双明;张杰平

5.通货膨胀与房地产价格对实体经济的冲击影响-基于不同货币政策规则的DSGE 模型分析 [J], 李巍;张志超

因版权原因,仅展示原文概要,查看原文内容请购买。

dsge模型定义DSGE(Dynamic Stochastic General Equilibrium)模型是宏观经济学中用于解释不同经济变量之间关系的一种数学模型。

它可以被认为是一种宏观经济学的动态优化模型,其中包括家庭、企业和政府在一个通货膨胀逐渐稳定的稳定状态下进行决策的相互作用。

DSGE模型的主要特点是,它通过使用微积分和统计学的工具来建立一个精细的数学模型,以便更好地描述家庭、企业和政府的组织和决策行为。

它假设所有人都是理性的,并在不同的环境中作出最优决策。

这个模型的另一个重要的特点是,它可以用来预测在不同的条件下经济变量的变化。

例如,它可以用来预测某种政策措施会对通货膨胀率、失业率和GDP等经济变量产生怎样的影响。

DSGE模型可以分为以下几个方面:1. 基本假设:DSGE模型的基本假设是整体经济活动是一个由家庭、企业和政府组成的经济系统。

2. 家庭部门:家庭部门被视为最终的消费者,他们通过赚取的收入购买消费品和投资资产。

3. 企业部门:企业是一种生产和销售产品或服务的经济实体,其收入来自于销售产品或服务。

4. 政府部门:政府部门是负责制定宏观经济政策的机构,包括货币政策和财政政策。

5. 市场机制:DSGE模型包含不完美的市场机制,包括短期和长期市场,其中价格和工资并不完全灵活。

DSGE模型的优点在于,它可以建立一个精细的数学模型,以更好地描述整体经济系统的内部运作。

这个模型可以用来预测不同经济变量的变化,从而帮助经济决策者制定政策和调整政策。

然而,DSGE模型的缺点也不可忽视。

首先,它的建模过程需要大量数据和计算能力。

此外,模型的一些假设并不完全符合实际情况,特别是在解释某些现象时可能出现问题。

总之,DSGE模型在宏观经济学中扮演着重要的角色,它可以帮助经济决策者制定政策,并预测不同的经济变量的变化。

虽然它还有一些可被改进之处,但它仍然是一个非常有用的工具。

SERIEs(2010)1:51–65DOI10.1007/s13209-010-0020-9ORIGINAL ARTICLEDSGE models and their use at the ECBFrank Smets·Kai Christoffel·Günter Coenen·Roberto Motto·Massimo RostagnoReceived:16October2009/Accepted:09December2009/Published online:23February2010©The Author(s)2010.This article is published with open access at Abstract Bayesian dynamic stochastic general equilibrium(DSGE)models com-bine microeconomic behavioural foundations with a full-system Bayesian likelihood estimation approach using key macro-economic variables.Because of the usefulness of this class of models for addressing questions regarding the impact and consequences of alternative monetary policies they are nowadays widely used for forecasting and policy analysis at central banks and other institutions.In this paper we provide a brief description of the two main aggregate euro area models at the ECB.Both models share a common core but their detailed specification differs reflecting their specific focus and use.The New Area Wide Model(NAWM)has a more elaborate interna-tional block,which is useful for conditioning the euro area projections on assumptions about foreign economic activity,prices and interest rates and to widen the scope for scenario analysis.The Christiano,Motto and Rostagno(CMR)model instead has a more developedfinancial sector,which allows it to be used for monetary andfinancial scenarios and for cross checking.Based on the comparison of two models wefind a broad agreement on the qualitative predictions they make,although,in quantitative terms,there are some differences.However,the perspectives provided by the two models are often complementary,rather than conflicting.Keywords DSGE models·Central banks·Monetary policyJEL Classification B4·C5·E32·E50Prepared for a special issue of the Spanish Economic Review.The opinions expressed are our own and should not be attributed to the European Central Bank or its Governing Council.F.Smets(B)·K.Christoffel·G.Coenen·R.Motto·M.RostagnoEuropean Central Bank,Frankfurt,Germanye-mail:Frank.Smets@ecb.int1IntroductionCentral banks need a wide range of macro-econometric models and tools for fore-casting and monetary policy analysis.Over the past5years,an increasing number of institutions have introduced Bayesian dynamic stochastic general equilibrium(DSGE) models in their tool kit for policy analysis.1These models combine a consistent,micro-founded DSGE structure,characterised by the derivation of behavioural relationships from the optimising behaviour of agents subject to technological and budget con-straints and the specification of a well-defined general equilibrium,with a full-system Bayesian likelihood estimation using key macro-economic variables.As argued by Smets and Wouters(2003,2004),the DSGE approach is particularly suitable for addressing questions regarding the impact and consequences of alternative monetary policies.The general equilibrium structure lends itself to telling economi-cally coherent stories and structuring forecast-related discussions around it.Off-model information about“deep”structural parameters can be used to calibrate and/or esti-mate the model,which is particularly useful when time series are short.The model structure also helps to identify parameters and the type of shocks hitting the economy and to reduce the risk of over-fitting.Finally,the structural nature of the model and, in particular,its explicit account for the role of expectations makes the analysis less subject to the Lucas critique and more suitable for policy analysis.DSGE models put a premium on the important role of expectations in assessing alternative policy actions. They also give a better feel for which parameters are likely to be policy invariant and which ones are not.The empirical strategy,full-system Bayesian likelihood estimation,also has a num-ber of advantages over the more traditional equation-by-equation estimation of large macro models.First,it formalises the use of prior information and helps identifica-tion,thereby making the estimation algorithm of the highly restricted and non-linear model much more stable.As shown by Canova(this issue),the likelihood function of DSGE models is oftenflat and irregular in a number of the parameters.Prior information helps overcoming such identification issues.Secondly,the Bayesian like-lihood approach delivers a full characterisation of the parameter and shock uncertainty, allowing easily constructing probability distributions for unobserved variables(e.g. the output gap)and derived functions(e.g.forecasts).The state-space formulation underlying the approach,whereby the state equation captures the dynamics of the state variables in the model economy and the observation equations links those state variables to observable macro-economic time series,is a veryflexible tool that can deal explicitly with measurement error,unobservable state variables,large data sets and different sources of information.Finally,the Bayesian estimation methodology provides a natural framework for decision making under uncertainty.As new data and new models appear,decision makers can update their posterior probabilities and appropriately weigh them when making decisions.The attractive combination of rigorous economic reasoning and data coherence that characterises Bayesian DSGE models implies that they can be used successfully for1Examples are the Sveriges Riksbank,the Norges Bank,the Czech National Bank,the Federal Reserve Board,the IMF and the European Commission.scenario analysis and monetary policy design without compromising on their forecast-ing performance,which is comparable to the one of purely statistical and data-driven methods.In this paper,we provide a brief description of the two main aggregate euro area DSGE models that are being used in the context of the ECB’s quarterly projec-tion rounds and the associated cross-checking in the context of the ECB’s monetary analysis.Both models have a core which is similar to that of Christiano et al.(2005) and Smets and Wouters(2003).However,the New Area Wide Model(NAWM)has a more elaborate international block,which is useful for conditioning the euro area pro-jections on assumptions about foreign economic activity,prices and interest rates.The Christiano,Motto and Rostagno(CMR)model instead has a more developedfinancial sector,which allows it to be used in cross checking.In addition to the two estimated euro area DSGE models,a number of other DSGE models have been developed to address specific issues such as the effects offiscal policy,the international interac-tions between the euro area and the rest of the world and country-specific developments within the euro area.2These are not discussed in this paper.The rest of the paper is structured as follows.Section2gives a brief description of the main features of those two models and their use at the ECB.Section3compares some of the empirical and structural features of the two models.First,it discusses and compares the monetary policy transmission mechanism in both models.Secondly,it uses the models to interpret the sources of recent developments in economic activity in the euro area.Finally,it provides an example of the counterfactual policy simula-tions that can be done using the two models.More details and examples of this type of empirical,quantitative policy analysis can be found in the various papers describ-ing the two models and their applications.Finally,the last section(Sect.4)briefly addresses some of the recent criticism of modern DSGE models that has arisen in the light of the currentfinancial crisis and provides some conclusions.2Estimated euro area DSGE models at the ECBMany models are in use at the ECB ranging from purely statistical models to fully fledged structural(DSGE)models.Within the class of DSGE models,two models are routinely used in the policy process.The NAWM has been developed for forecasting purposes and for policy analysis.The CMR model has been developed to support the monetary analysis of the ECB and its two-pillar strategy,and to conduct monetary andfinancial scenarios.The need to serve for different purposes has driven also the modelling choices in developing these models.The NAWM includes a detailed inter-national block,whereas the CMR includes a detailed modelling of the monetary and financial side of the economy.The two models share similar long-run properties and a similar“core block”.This lends itself to interpreting the specificities of the two models in terms of additional transmission channels with respect to their common“core block”.The core model2These models include the version of the NAWM used for globalization studies(Jacquinot and Straub 2008),the NAWM with afinancial block(McAdam and Lombardo(2009)),a DSGE model to analyse macroeconomic interdependencies in the euro area(Gomes et al.2009)and the rational expectation multi country model for the euro area countries used for forecasting and policy analysis(Dieppe et al.2009).Households - consumption/saving decisions - labour supplyProduction - Combine labour and Markets: imperfectcompetition & Monetary Government Fig.1Structure of the Models.Note:The boxes with the solid frame denote the core model that is nested in both models.The boxes with dashed frame at the bottom of the figure show the open economy features of the NAWM whereas the box with dash-dotted frame on the right-hand side of the figure describes the financial dimension modelled in the CMRincludes features introduced in Christiano et al.(2005)and Smets and Wouters (2003),which have been shown to help explaining the data well both in the US and the euro area.Such features have become standard in DSGE modelling.They include habit persistence in consumption,adjustment costs in the flow of investment,imperfect competition,sticky prices and sticky wages,and the inclusion of a large number of structural shocks that act as shifters of the structural relationships.Figure 1provides a diagrammatic representation of the main sectors of the economy included in the “core block”(boxes with solid frame in the middle of the figure)and of the additional sectors that are included in the NAWM (boxes with dashed frame at the bottom of the figure)and the CMR model (box shaded with dashed-dotted frame on the right-hand side of the figure).In the NAWM the common core block is embedded into an international environ-ment.3This has wide-ranging consequences for the model dynamics both regarding the influence of foreign developments on the domestic economy as well as by directly influencing the decision process of domestic households and firms.Households are trading both domestic and foreign bonds.The effective return on the risk-less domestic bonds depends on a financial intermediation premium,which drives a wedge between the interest rate controlled by the monetary authority and the return required by the household.Similarly,when taking a position in the international bond market,the household encounters an external financial intermediation premium which depends on the economy-wide (net)holdings of internationally traded foreign bonds expressed in domestic currency relative to domestic nominal output.That is,if the domestic economy is a net debtor,households have to pay an increasing external 3See Christoffel et al.(2008)for a full description of the NAWM model.intermediation premium on their international debt.The uncovered interest parity condition determines the dynamics of the exchange rate.Turning to the production side there are four different kinds offirms.In the pro-duction sector of the tradable,intermediate good there are domesticfirms producing for the domestic market,domesticfirms producing for the foreign market and for-eignfirms producing for the domestic market.The intermediate goodfirms engage in Calvo price setting where both import as well as export goods are priced in the domestic currency.4The representativefirm producing the non-tradablefinal invest-ment and private consumption goods,combines purchases of a bundle of domestically produced intermediate goods,with purchases of a bundle of imported foreign inter-mediate goods.The relative demand for the goods is determined by the relative prices, the price elasticities and the degree of home bias.The resulting tradeflows are affected by domestic and foreign demand,relative prices and by the exchange rate,accounting for limited exchange-rate pass-through in the short to medium run.The design of the NAWM for use in the ECB/Eurosystem staff projections has been guided by two important considerations,namely(i)to provide a comprehensive set of core projection variables and(ii)to allow conditioning on monetary,fiscal and external developments which,in the form of technical assumptions,are an important element of the projections.As a consequence,the scale of the model—compared with a typical DSGE model—is relatively large.Employing Bayesian methods,it is estimated on18 key macroeconomic variables.In addition to standard national account data,data for the nominal effective exchange rate,euro area foreign demand,euro area competitors’export prices as well as oil prices are used,which are deemed important variables in the projections capturing the influence of external developments.Turning to the CMR model,it extends the“core block”by explicitly modelling the monetary andfinancial dimension of the economy.Portfolio andfinancing deci-sions are non-recursive in the model,but they directly affect consumption,investment and prices.The model is a variant of the model withfinancial frictions developed in Christiano et al.(2003,2007),which in turn includes thefinancial accelerator of Bernanke et al.(1999)and the banking system of Chari et al.(1995).The main fea-tures offinancial intermediation in the CMR are the following.First,the presence of many types of assets in the economy that differ in their degree of liquidity and maturity gives rise to portfolio decisions.Second,investment in physical capital is leveraged,giving rise to the need for externalfinancing.There is risk of default; and the presence of asymmetric information in credit markets implies that the incen-tives of borrowers and lenders are not aligned.This leads the lender to charge a premium which is a function of the equity of the borrower.As the value of equity is mainly driven by asset pricefluctuations,there is a direct link between asset prices and real economic activity.Third,in the model part of the working capital has to be financed prior to the time in which revenues from selling current production become available.Fourth,in the model savers and lenders do not interact directly but via financial intermediaries.Intermediaries have their own balance sheet with liabili-ties,mainly different type of deposits,so that it is possible to construct aggregates 4The alternative setting,assuming local currency pricing both for exports and imports,leads to counter-factual production price dynamics in the eurozone and a deterioratedfit of the model in the estimation.O u tp u tInflation Interest rates 0 5101520-0.5-0.4-0.3-0.2-0.10.1Quarters 0 5101520-0.25-0.2-0.15-0.1-0.0500.05Quarters 0 5101520-100102030405060QuartersNAWM CMR NAWM CMR NAWM CMR Fig.2Monetary policy transmission mechanism.Note:The dashed and dash-doted lines show the response of the NAWM and the CMR model to an unanticipated 50basis point increase in interest rates,for output annualized inflation and interest ratessuch as M1and M3,and assets,mainly,different types of loans.The production of deposits requires resources in terms of capital,labour and excess reserves.The pres-ence of excess reserves captures the intermediaries’need for maintaining a liquidity buffer to accommodate unexpected withdrawals.In the model intermediaries cannot default.Finally,in the model financial contracts are denominated in nominal terms.As borrowers and lenders are ultimately interested in the real value of their claims,shifts in the price level unforeseen at the time the financial contract is signed bring about real effects.This is a way to include the “Fisher debt-deflation”channel in the model.The parameter values underlying the quantitative results presented in the remaining of the paper are obtained in two ways.Some structural parameters are calibrated in order to match great-ratios and long-run averages.In the calibration it is ensured that the long-term properties of the two models coincide to the largest possible extent.The remaining structural parameters and the parameters governing the stochastic pro-cesses are estimated by using a Bayesian version of the standard maximum likelihood approach.3A comparison of the NA WM and the CMR models3.1Monetary policy transmission mechanismIn this section we assess the dynamic implications of the models by comparing the transmission mechanism of monetary policy shocks.Figure 2shows the response to an unexpected increase in the nominal interest rate of 50basis points.As the two models share some of the transmission channels,we focus on the role played by the channels which are specific to each of the models.In line with common wisdom regarding the transmission of monetary policy,in the NAWM the increase in the real rate leads to temporarily curtailed demand,with investment falling more strongly than consumption.The responses reflect also the open economy dimension and the endogenous response of the exchange rate adding additional transmission channels affecting both the real and nominal side.On the real side wefind that the positive interest rate differential between foreign and domestic bonds implies an increased demand for domestic bonds.This implies an appreciation of the domestic currency via the uncovered interest parity assump-tion.Since intermediate imports are priced in the local currency the exchange rate movement implies a gradual,but noticeable drop in import prices and an improve-ment of the terms of trade.The improved terms of trade lead to expenditure-switching from domestic towards foreign goods in the composition of thefinal consumption and investment goods.As a consequence,imports fall by less than domestic demand. Exports are priced in producer currency implying a stronger price increase and a more pronounced reduction in exports.Continuing with the price side reaction to a monetary policy shock wefind two additional effects of the open economy dimension.First and as discussed above,the open economy features imply an amplification of the decline in aggregate demand and consequently in factor demand.Firms cut back their demand for labour and,therefore, employment falls.Via its impact onfirms’marginal cost,the resulting decline in wages puts downward pressure on domestic prices.Second,consumption prices will decline more strongly than domestic prices because of the drop in import prices due to the appreciation of the domestic currency.In sum,the peak absolute effect on economic activity and inflation is reached after about1year,whereas the implied price level effects are gradual and long-lasting.Turning to the CMR model,the asset side of thefinancial sector’s balance sheet introduces three main propagation mechanisms relative to the“core block”.First, there is thefinancial accelerator effect.The deterioration in economic activity brought about by the initial monetary policy tightening leads to a shortfall in earnings and to capital losses,both of which erode the value of borrowers’net worth.The associate rise in the bankruptcy rate leads to a rise in the externalfinance premium charged over and above the risk-free rate controlled by the central bank.This channel tends to magnify the contractionary impact of a policy tightening.The second propagation mechanism,the“Fisher debt-deflation”channel reinforces the standard accelerator effect described above.The debt-deflation effect implies that the decline in the price level brought about by the unexpected increase in the policy rate—thus by construc-tion also the decline in the price level is unforeseen at the time thefinancial contract was signed—increases the real value of the debt outstanding.This redistribution of wealth between borrowers and lenders has real effects on the economy.Note that the Fisher and accelerator mechanisms reinforce each other only in the case of shocks that move the price level and output in the same direction,such as monetary policy shocks,whereas they tend to cancel each other out in the wake of shocks that move the price level and output in opposite directions,such as transitory technology shocks. The third propagation mechanism in the model is given by the need tofinance part of the working capital in advance.The additional propagation mechanisms included in the model should not be taken as necessarily implying stronger downward pressure oninflation.On the one hand,higherfinancing costs lead to lower inflationary pressure via their depressing effect on economic activity.On the other hand,they represent additional costs,putting upward pressure on price developments.The model makes also predictions for the liability side of banks’balance sheet. Given the importance of monetary and credit developments in the ECB monetary pol-icy strategy,understanding the path followed by narrow and broad monetary aggregates in response to a policy tightening is of particular interest.According to the model,a policy tightening triggers an initial positive reaction of the stock of nominal M3.This is driven by the speculative demand for money,captured by the M3components outside M1.This is explained by the fact that the interest rate earned on instruments included in M3–M1is closely linked to market rates.The model suggests that the own rate on M3–M1goes up approximately by the full50basis points rise in the policy rate.The interest rate earned on the liquid component of M3is instead less reactive.According to the model,after the initial rise,M3undergoes a significant and permanent decline. This“perverse”initial decline of M3following a policy tightening found in the model is consistent with evidence obtained on the basis of identified V ARs.Overall,taking into account that the two models share only some of the transmission channels,the quantitative differences between the NAWM and the CMR responses toa policy shock appear to be rather small.3.2Structural interpretation of GDP growthThe models can be used to interpret recent macroeconomic developments in terms of the structural shocks that have hit the economy.The results of this are displayed in Figs.3and4,which provide an additive decomposition of annual GDP growth. The contribution of the different categories of shocks is shown by means of bars of different colour.Looking at the different phases of the business cycle since the start of the European Monetary Union(EMU)in1999,the mainfindings are the following.First,both models suggest that the expansion of1999–early2000is mainly explained in terms of forces that can be probably associated with the convergence process in interest rates in the run-up to EMU(see light blue bars with diagonal lines), and in terms of increased degree of competition,possibly driven by globalisation forces(see green bars,colorfigure online).Demand shocks are found to be lagging (see red bars with diamonds).Second,the interpretation of the slowdown of2000–2001and the following phase of weak growth until2005provided by the two models is less clear cut.The NAWM suggests that the downturn starting in the second half of2000was triggered by adverse influences from abroad.For instance,the emergence of new competitors in euro area export markets eventually led to losses in export market shares.Moreover,the sharp deceleration of economic activity in the United States and its spillovers to the rest of the world caused a pronounced fall in euro area foreign demand from2001onwards. Within the NAWM,these developments are captured by negative export preference and negative foreign demand shocks,respectively.Furthermore we can observe a neg-ative contribution of the technology shock group in the2001slowdown.Looking at the further decomposition we can attribute this mainly to the transitory technology-10.0-8.0-6.0-4.0-2.00.02.04.06.01999200020012002200320042005200620072008Markups Policy International Demand Technology Output Growth Fig.3Structural interpretation of GDP growth in NAWM.Note:GDP growth,year-on-year %change,in deviation from st observation is 2009q2-10.0-8.0-6.0-4.0-2.00.02.04.06.01999200020012002200320042005200620072008Markups Policy Financial Factors in Capital Formation Bank Funding Demand Technology Output GrowthFig.4Structural Interpretation of GDP growth in CMR.Note:GDP growth,year-on-year %change,in deviation from st observation is 2009q2shock which is related to the increased degree of labour hoarding in this episode.The subdued growth of real GDP over the period 2002–2005is then largely explained by negative demand shocks,notably domestic risk premium shocks,that entailed a protracted slump in domestic spending.Since 2003the overall contribution of the foreign shocks has been rather modest.This masks the fact that in 2003the adverse impact of external risk premium shocks (accounting for the marked appreciation ofthe euro)was largely offset by the unwinding of the previous shocks to export pref-erences.In contrast,the favourable developments in euro area foreign demand during the2004–2006period have been largely compensated by the continued apprecia-tion of the euro and a renewed deterioration of foreign preferences for euro area exports.The CMR model suggests a different interpretation of the rapid slowdown of2000–2001.It does not support the occurrence of adverse technological shocks and explains this episode in terms of negativefinancial factors associated with the stock market collapse.Financial shocks mainly capture the sudden re-appraisal of profit prospects, which led to the stock market collapse,which in turn aggravated the already weak balance-sheet position of the corporate sector at the time.The associated rise in the riskiness of lending activity led to a sharp rise in the externalfinance premium.This prompted a cut in investment plans and a painful process aimed at repairing bal-ance sheets.According to the model,financial shocks exerted a progressively stronger downward pull on output until the end of2002and then they started receding.As of2002,the poor economic performance is explained by the CMR also in terms of unfavourable productivity shocks which exerted a downward pull on economic activ-ity and upward pressure on inflation.This countercyclical behaviour of productivity shocks had clear monetary policy implications,as it prevented inflation from quickly receding,notwithstanding the decline in resource utilisation caused by the economic slowdown.Third,both models(although the CMR to a larger extent)find that monetary policy was instrumental in preventing the unfavourable forces that hit the euro area over the period from2001to2006from causing a more severe slowdown.Fourth,both modelsfind that the recovery initiated at the end of2005is different in nature to the earlier recovery in1999,and is mainly a demand driven phenomenon.Turning to the recent recession and to the impact of thefinancial crisis on GDP growth the NAWM explains the downturn in terms of three mayor components.First, thefinancial turmoil led to an increase in perceivedfinancial risks and higher risk premia in terms of the spread between market interest rates and the rates controlled by the monetary authorities.The increased risk premium depressed domestic demand components as captured in the red bars with diamonds.Second,the deterioration of the supply side led to a downward revision of production capabilities as measured in the negative contribution from the technology shock group.Third and most importantly, the global dimension of the crisis implied a substantial reduction in world trade and a corresponding plummeting of exports in the euro area.This effect is particularly important because the reduction in world trade was accompanied by losses in market shares owing to the high proportion of investment goods in euro area exports.The negative contribution of the monetary policy group includes the shock to the sim-ple,empirical monetary policy rule,but not the non-conventional monetary policy measures installed in response to the crisis.According to the CMR,the most important driver of the recent crisis can be traced down to shocks emanating fromfinancial intermediation(see yellow bars with hori-zontal lines),in particular the sudden re-appreciation of credit risk.The second most important contribution to the recent free fall in real economic activity has been the sharp drop in domestic and international demand(see red bars with diamonds).In。