3.1 R Case Study 1

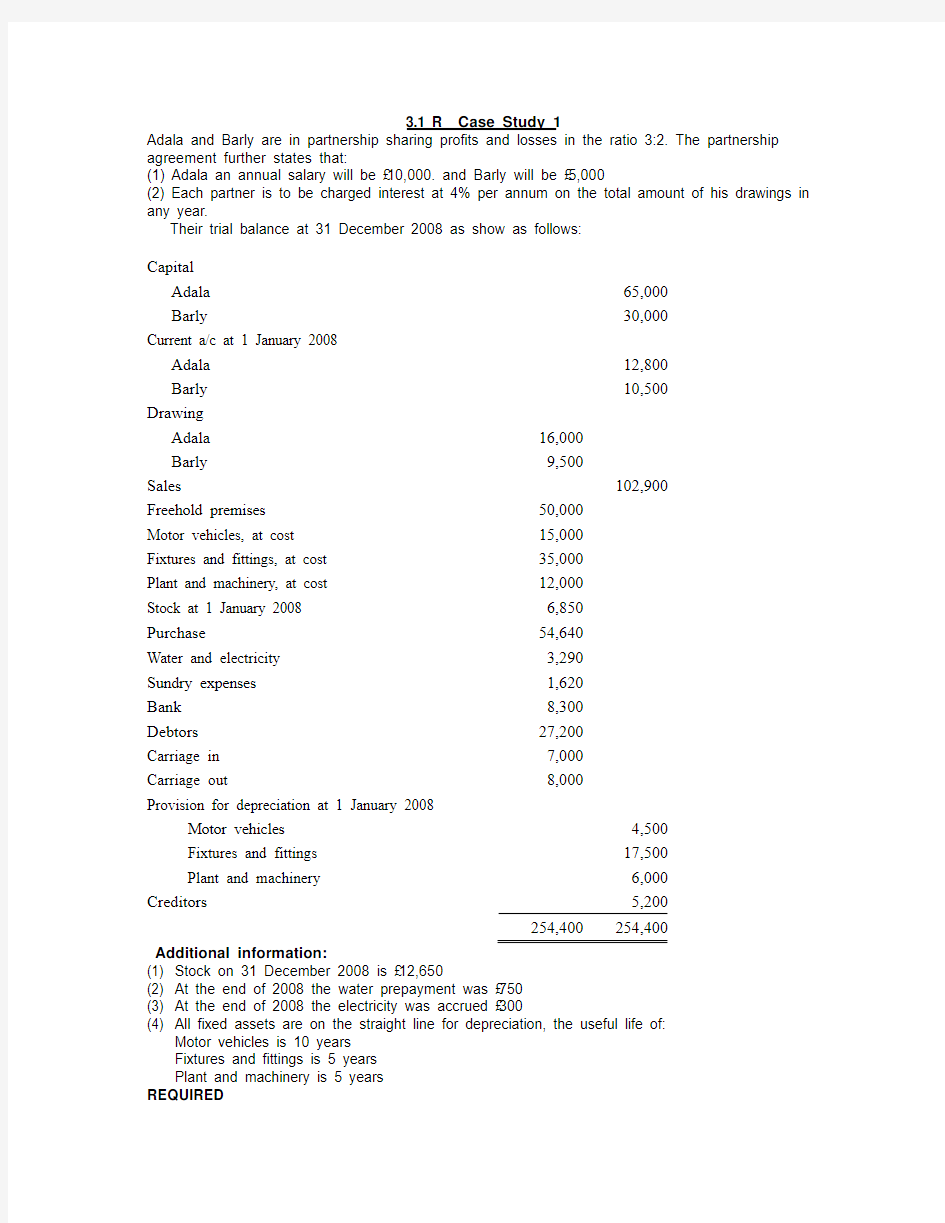

Adala and Barly are in partnership sharing profits and losses in the ratio 3:2. The partnership agreement further states that:

(1) Adala an annual salary will be £10,000. and Barly will be £5,000

(2) Each partner is to be charged interest at 4% per annum on the total amount of his drawings in any year.

Their trial balance at 31 December 2008 as show as follows:

Capital

Adala65,000

Barly30,000

Current a/c at 1 January 2008

Adala12,800

Barly10,500

Drawing

Adala16,000

Barly9,500

Sales102,900

Freehold premises50,000

Motor vehicles, at cost15,000

Fixtures and fittings, at cost35,000

Plant and machinery, at cost12,000

Stock at 1 January 20086,850

Purchase54,640

Water and electricity3,290

Sundry expenses1,620

Bank8,300

Debtors27,200

Carriage in7,000

Carriage out8,000

Provision for depreciation at 1 January 2008

Motor vehicles4,500

Fixtures and fittings17,500

Plant and machinery6,000

Creditors5,200

254,400254,400

Additional information:

(1) Stock on 31 December 2008 is £12,650

(2) At the end of 2008 the water prepayment was £750

(3) At the end of 2008 the electricity was accrued £300

(4) All fixed assets are on the straight line for depreciation, the useful life of:

Motor vehicles is 10 years

Fixtures and fittings is 5 years

Plant and machinery is 5 years

REQUIRED

(a) Prepare for Adala and Barly, in respect of the year ended 31 December 2008:

(i) The Profit & Loss Appropriation Account. (32 Marks)

(ii) Balance sheet on 31 December 2008 (38 Marks)

3.3 Dixion and Speedie

K. Dixon and D. Speedie consulted an accountant in March 20X4 and explained that they had been carrying on a spare-time business as electrical contractors in partnership, since 1 May 20X2. No accounts had ever been prepared and the fear was that the taxman might soon start to get nasty. It was agreed that the accountant should prepare accounts for the year ended 30 April 20X3. The partners produced bank statements for that year and from these the accountant prepared the following summary:

$ $

Receipts from customers 12,600 Cash withdrawn: K Dixon 2,800

D. Speedie 2,000

Payments to suppliers for

electrical goods 6,692

Van purchase(1 Dec 20X2) 740

Advertising 100

Stationery 28

Van insurance (year to 30

Nov. 20X3) 84

Road tax (6months to 31

May 20X3) 48

Tools 90

Balance at 30 April 20X3 18

12,600 12,600

the following further information was given to the accountant:

1 On 1 May 20X

2 Dixon had in his garage a stock of electrical goods valued at $200. He agreed to bring them into the firm and they were gradually used up on the firm’s contracts.

2 At 30 Aril 20X

3 the firm had a stock of electrical goods that had cost $325 and at that date there was an unpaid bill from a supplier for $73.

3 Most of the customers paid by cheque and the cheques went into the firm’s bank account. There had been a number of occasions, however when customers paid in cash, the total amount involved being $410. Speedie had taken this cash himself and not paid it into the firm.

4 Some work was done for a customer on 28 April 20X3 for which he was charged $137. He paid by cheque on 11 May.

5 Dixon used his own car for the firm’s business. It was worth $2,000 in May 20X2 and the partners agreed it should be brought in as the firm’s asset at that valuation. 25% pa was thought to be a fair rate of depreciation to charge against the firm’s profit. Dixon paid all the running costs for the year out of his own pocket. They came to $800, half of which was thought to relate to business usage.

6 Speedie had used his own car up to the time they bought the van. It was agreed not to bring this car into the business. The total running costs for this period were $600, two

thirds of which related to Speedie’s private motoring and they were all paid by Speedie from his own pocket. He also paid $390 in running costs for the van, all of which were for business usage.

7 The van was expected to last for two years after which it would have a scrap value of perhaps $20.

8 All business telephone calls had been made or received on Dixon’s telephone. The bills for the year came to $180 and it was agreed one third of this related to the business.

9 Mrs. Dixon had rendered valuable service during the year in answering the telephone and it was decided that she should be paid $52 out of the firm that she duly received on 31 May 20X3.

10 The partners thought that $50 represented the value of the tools at 30 April 20X3.

11 The accountant’s fee for preparing the accounts was likely to be $100.

You are required:

Prepare the firm’s profit and loss account for the year ended 30 April 20X3 and a balance sheet as at the date.

4.1 Sandy and Monty

Sandy and Monty are in partnership sharing profits and losses in the ratio 2:1. The latest balance sheet is shown below:

Sandy and Monty

Balance Sheet at 31 December Year 9

££

Balance Sheet at 31 December Year 9

££££Fixed Assets Capital Accounts

Premises 85,000 Sandy 100,000

Fixtures & fittings 15,000 Monty 50,000 150,000 Motor vehicles 30,000 130,000 Current Accounts

Sandy 7,000

Current Assets Monty 8,000 15,000 Stock 14,500

Debtors 8,000 Current Liabilities

Bank 18,500 41,000 Creditors 6,000

171,000 171,000 On 1 January Year 10 the partners agreed to allow Paul into the partnership and that the partnership’s assets should be re-valued as under:

£

Premises 120,000

Fixtures & fittings 10,000

Motor vehicles 24,000

Stock 11,500

Sandy, Monty and Paul agreed that the existing goodwill of the business was estimated at £12,000

but that it should not be included in the Revaluation Account.

The terms of admission were that profits and losses would be shared in the ratio of Sandy 2, Monty 1 and Paul 1. Paul agreed to pay into the business Bank Account £30,000 for his capital plus an amount in respect of his share of the unrecorded goodwill. The amount received for goodwill is not to be withdrawn by Sandy and Monty.

REQUIRED

(a) Revaluation Account.

(6 marks)

(b) Partners’ Capital Accounts in columnar form.

(8 marks)

(c) Balance sheet of the new partnership at 1 January Year 10 in vertical form.

(11 marks)

(Total 25 marks)

(LCCIBE examination question)

4.2 Half and Crown

Half and Crown are in partnership, trading under the name ‘Twoandsix’ and Shilling and Tanner are in partnership trading under the name of ‘Oneandsix’. The partners have decided to amalgamate into a single four partner firm trading as ‘Oldmoney’. The profit-sharing ratios of the old firms were:

Half and Crown 4 : 3

Shilling and Tanner 3 : 2

The new profit-sharing ratio is

Half 6

Crown 5

Shilling 4

Tanner 3

The summarized balance sheets as at the date of amalgamation were as follows:

two&si

one&six

x

$ $ $ $

capital

account

half 60000

crown 45000 105000

shilling 30000

tanner 20000 50000

current

account

half 1200

crown -1000 200

shilling 15200

tanner 9600 24800

105200 74800

fixed assets

property 29600 40000

Fixtures 7200 5600

Vehicles 12000 48800 7200 52800

Current

assets

stock 33200 26400

investments 3200

debtors 27200 23200

bank 13600 77200 0 49600

Current liabilities

creditors -20800 -24000

overdraft 0 -20800 -3600 -27600

105200 74800

The agreement to amalgamate contains the following provisions:

1 Oldmoney to take over the old partnership net assets at the following values:

Twoandsix Oneandsix

$ $

Stock 33,800 25,560

Vehicles 11,200 5,200

Fixtures 6,400 0

Property 40,000 0

Goodwill 25,200 18,000

Debtors Book value Book value

Less:5% provision Less: 5% provision Creditors Book value Book value

Less :2.5% discount Less: 2.5% discount

These agreed values are to be recorded in the old firm’s accounts before they are closed.

2 The fixtures and property of Oneandsix were sold on the date of amalgamation for $54,000

but the transaction has not yet been recorded in the accounts.

3 Crown is to take over his firm’s investments at a value of $3,040.

4 Total capital of Oldmoney is to $216,000 and is to be contributed by the partners according

to their profit-sharing ratios, any adjustments to be made in cash.

5 Goodwill is not to appear in the accounts of the new firm and is to be written off the

partners’ capital accounts after the adjustments in 4 above.

Prepare

a) For both the old firms: revaluation account

partners’ capital accounts.

b) For the new firm: cash account

partners’ capital accounts.

balance sheet at the date of amalgamation

5.1

Frog. Toad and Whelk have been carrying on a business supplying seafood since 20x1, sharing profits equally. They make up their accounts to 31 March.

On 31 March 20x9 they decided to dissolve the partnership. The balance sheet as at 31 March 20x9 showed:

Fixed assets $ $

Premises 193,750

Fixtures and fittings 62,000

Vehicles 31,000

Current assets

Stock 23,250

Debtors 31,000

54,250

Current liabilities

Creditors 15,500

Bank overdraft 8,675

44,175

Net current assets 10,075

Net assets 296,825

Capital accounts

Frog 77,500

Toad 93,000

Whelk 93,000 263,500

Current accounts

Frog 21,700

Toad 31,775

Whelk (20,150) 33,325

296,825

The assets were sold for the following amounts:

Fixed assets Book Sold

value for

$ $

Premises 193,750 175,000

Fixtures and fittings 62,000 55,000

Vehicles 31,000 26,500

Current assets

Stock 23,250 15,000

Debtors 31,000 38,000

Assume that the assets were acquired by a limited company. Seafoods Ltd., and the purchase consideration was:

Cash :$100,000

Shares: 60,000 $1 ordinary share in Seafoods Ltd. fully paid up.

The partnership continued to pay the creditors.

Write up the following:

a) The journal entries to close the partner capital accounts. Please state any assumptions that you make in relation to the division of the shares between the partners.

b) The journal entries to record the purchase in the books of Seafoods Ltd.

5.2

William Wright and James Proper have developed a business selling military buttons to collectors. Wright and Proper had been in business for ten years as equal partners before deciding to convert their business into a limited company, Brass Buttons Ltd., on 1 July 20x6.

The year end for their business has always been and will continue to be 31 March. The partners continued to use the books of the business without a break, and no entries have been made consequent to the company’s formation.

Brass Buttons Ltd.

Trial balance as at 31 March 20x7

$ $

Sales 924300

Purchases 684000

Rent 21600

Selling expenses 7200

Creditors 111600

Debtors 97200

Stock 300000

Discount allowed 19200

Bad debts 9600

Salaries 64800

Sundry expenses 11400

Fixtures and fittings 28800

Motor vehicles 33600

Cash at bank 67620

Capital account:

Wright 216000

Proper 156000

Drawings:

Wright 32400

Proper 27600

Formation expenses 2880

1407900 1407900

The following information is also available:

1. The trade of the business is seasonal with the average monthly sales in the last quarter of the year being twice the average monthly sales in the first three-quarters of the year.

2. Brass Buttons Ltd. issued 300,000 $1 ordinary shares in settlement of the purchase of the assets and liabilities from Wright and Proper at 1 July 20x6.

3. The remuneration of the directors of the new company, Wright and Proper was agreed at $21,600 per annum each.

4. During the quarter ending 30 June 20x6 the partners’ drawings were:

Wright $7,200

Proper $15,600

5. The reducing balance method of depreciation has been used by the partnership. The rates of depreciation used were 10% per annum for fixtures and fittings and 20% for motor vehicles. The same method of depreciation is to be used by the new company, but the rates are to be changed to 20% for fixtures and fittings and 15% for motor vehicles. During May 20x6 a new van was acquired at a cost of $8,400.

6. Discounts allowed are to be apportioned in accordance with monthly sales, and except where mentioned specifically, expenses occur on a time basis .The rate of gross profit has remained constant during the year.

7. The closing stock at 31 March 20x7 was valued at $336,990.

8. The bad debts arose as follows:

a) $4,200 from a sale made in January 20x6.The debt was written off on 31 December 20x6.

b) $4,800 from a sale made in April 20x6.The debt was written off on 30 June 20x6.

c) $600 from a sale made in August 20x6.The debt was written off on 31 March 20x7.

Prepare the profit and loss account and balance sheet for Brass Buttons Ltd. for the period ended 31 March 20x7.The accounts are to be prepared for internal use only.

(Shefffield Polytechnic)

5.3

X, Y and Z have been in partnership for several years, sharing profit and loss in the ration 3:2:1. Their last balance sheet that was prepared on 31 October 20x1 is as follows:

Balance Sheet of X, Y and Z as at 31 October 20x1

$ $ Capital X 4000 Fixed assets at cost 2000

Y 4000 less depreciation -6000

Z 2000 1400 Current liabilities Current assets

Bank 13000 Stock 5000

Creditors 17000 Debtors 21000

30000 26000 Capital and liabilities 40000 40000 Despite making good profit during recent years they had become increasingly dependent on one credit customer Smithson and in order to retain his custom they had gradually increased his credit limit until he owed the partnership $18,000. It has now been discovered that Smithson is insolvent and that he is unlikely to repay any of the money owed by him to the partnership. Reluctantly X, Y and Z have agreed to dissolve the partnership on the following terms:

1) The stock is to be sold to Nelson Ltd. for $4,000.

2) The fixed assets will be sold for $8,000 except for certain items with a book value of $5,000 that will be taken over by X at an agree valuation of $7,000.

3) The debtors except for Smithson, are expected to pay their accounts in full.

4) The costs of dissolution will be $800 and discounts received from creditors will be $500.

5) Z is unable to meet his liability to the partnership out of his personal funds.

Required:

a)The dissolution account.

b)The capital accounts to the partnership recording the dissolution of the partnership.

6.1 East Coast Toys Ltd and Skegness Hall

East Coast Toys Ltd operates a retail branch at Skegness Hall purchase are made by the company’s main shop in Yarmouth. Goods required by the Skegness branch are delivered to it weekly from Yarmouth and are charged at the company’s normal selling price that is cost price plus 25%. All branch transactions are recorded in the books of the head office.

On 1 April 20X5 stock in trade at the Skegness branch amounted to $10,800 at selling price, and

the branch debtors totaled $1,500. All cash is remitted to head office.

During the year ended 31 March 20X6 the following transactions took place at the branch:

$ Goods received by the branch from head office (at selling price) 65,200

Credit sales to customers 15,400

Goods returned by the branch to head office (at selling price) 800

Cash sales to customers 50,300

Reductions off normal selling prices allowed to 120

cash customers due to goods being sub-standard

Goods returned to branch by credit customers (at selling price) 2,560

Cash received from debtors 11,280

Cash discount for prompt payment allowed to debtors 1,020

Bad debts written off 300

Damaged goods destroyed (at selling price) 120

Stock shortage at March 20X6 (at selling price) 140

Salaries, wages rent and rates, and other expenses relating to the branch for the year ended 31 March 20X6 amounted to $7,200.

You are required:

account, and the branch debtors account for the year ended 31 March 20X6. Also prepare the branch profit and loss account for the year ended 31 March 20X6.

6.2Grange and Derby

Grange Ltd has its head office a Derby and a branch at Gloucester. Goods are supplied by head office at selling price, which is calculated by adding 25% to cost. The branch maintains its own accounting records but some expenses are paid by head office.

At 31March 20X5 the trial balances were as follows:

Debit Credit

H/O Branch H/O Branch

$ $ $ $

Premises 32510 5800

Fixtures and fittings 7890 3400

Ordinary share capital 50000

Reserves 38380

Stock at 1 April 20x4 10700 4890

Purchases 120620

Goods sent to branch 62490

Wags 34988

Insurance 600

Sales 102610 60420

Goods from head office 59990

Branch current account 18200

Provision for unrealised profits 978

Miscellaneous expenses 3852 680

Head office current account 15188

Bank balance 26682 228

Debtor and creditors 9846 620 11430

265888 75608 265888 75608

The following information is available if required:

1. Goods in transit at 31 March 20X5 amounted to $2,500 at transfer price. It was subsequently ascertained that only $2,000 (at transfer price) of these goods arrived.

2. Wages included $13,120 paid in respect of branch wages.

3. Closing stock at head office amounted to $11,580.

4. The insurance premium includes cover for goods in transit to a maximum value of $2,000.

You are required:

a) Prepare in columnar form separate trading and profit and loss accounts for both head office and branch, together with a combined balance sheet.

b) Show the head office current account as it would appear in the books of the branch and state what the balance of this account represents.

(Derbyshire College of Higher Education)

9.3

On 1 January Year 12, Trojan Plc offered for sale 4,000,000 Ordinary Shares of £1 each at £1.50 per share, as follows:

£0.40 per share on application

£0.80 per share (including the premium) on allotment

Balance on first and final call

Applications were received for 14,100,000 on 10 January Year 12. These were dealt with as follows:

Applications Shares Allotted on 25 January Year

12Applications Shares Allotted on 25 January Year

12

300,000number applied for in full12,800,000one share for every 4 applied for

1,000,000one share for every 2 applied for

Excess monies received on application were carried forward and offset against amounts due on allotment; any balances remaining were then refunded on 31 January Year 10, the date when allotment monies were due.

The first and final call was made on 1 July Year 12 and fully received on 10 July Year 12. REQUIRED

(a) Prepare a table as shown below:

Number of Shares Applied

for Number of

Shares

Allotted

Amount

Received on

Application

Total Due on

Application and

Allotment

Balance

Due

Balance

Refunded

££££

300,000

1,000,000

12,800,000

(12 marks)

(b) Prepare Journal entries, without narrations, to record the issue of the above mentioned Ordinary Shares at a premium, including bank entries, for the period 10 January to 10 July Year 12.

(13 marks)

(Total 25 marks)

(LCCIEB Question 1999)

9.4

Peter PLC has following capital structure on January 1, 20X0:

$

Net assets 4,120,000

Share capital

Ordinary share of $1 each 2,400,000

Share premium 520,000

Profit and loss 1,200,000

4,120,000

On January 1, Peter PLC decided to issue new 1,600,000 shares at the quotation price of $1.50, and issue 4,800,000 applications with a price of $0.40 for each application. On January 20, Peter PLC allots three applications for 1 share with further payment of $0.10 for each. The final calls are made on March 31. But on that day, only half of newly issued share have been paid up. So Peter PLC decided to reduce it capital, approved by local court, in following ways:

1)Forfeiture unpaid up share capital.

2)Reduce ordinary share to $0.70 as new pa value

You are required:

1)to prepare journal entry for application and allotment and for above 1) and 2)

2)to prepare extract balance sheet of Peter PLC. on January 20 and March 31 20X0

10.1

The Balance Sheet of Willow plc at January 1 Year 1 has the following capital structure:

$

Ordinary Share Capital ($1 shares) 600,000

6% Debentures 400,000

Undistributed profit 2,340,000

On May 1 Year 2, the company issue new share 600,000 shares at full market price that was $1.5 Profit before interest of debenture was $520,000, and income tax rate was 30%. On September 1, year 3 the company issues new share as bonus issue each 4 share can obtain one of this kind of bonus share from its share premium, and current profit before interest in year 3 is $450,000, assume that Willow plc had no profit from other business activity during year 1 to year 3.

Required

Calculate EPS in year 2 and Year 3.

Right issue

ABC Plc at the beginning of year 5 has following capital structure

Share capital (0.8 for each share) 480,000

5% debenture 100,000

On April 1 in year 5 ABC issue new shares at full market price 400,000 at price of $1.50. Profit before interest in year 5 was $560,000 and income tax rate was 25%. On August 1 in year 6 ABC right issue 5 for 1 share which price $1.20. Profit before interest in year 6 was $620,000 Required:

Calculation of ESP in year 5 and year 6.

Combine Comprehensive Case Study

Alpha Ltd. located in the United States, paid $30 million to hold 80% of the share capital of Barnet Ltd., which is independent entity in China, on March 1, 2012. Also, it issued new shares at full market price with a purpose of exchange with 100% interest in Carrolin Ltd., which is in the United States also, on April 1, 2012, and paid $9 million for a 30% interest in Dubily Ltd. on July 1, 2012.

You are also given following information:

1)On March 1, 2012, retained profit of Barnet Ltd. was ¥57.6. million, at the end of 2013,

Barnet declared dividend of ¥49.6 million and Alpha have not received it but recognized it. 2)The share capital in the balance sheet of Alpha as shown as following is excluding any newly

issued shares for the purpose of exchange with Carrolin Lid.

3)On April 1, 2012, retain reserve of Carrolin was $4 million.

4)On April 1, 2012, share’s price of Alpha quoted $4and share’s price of Carrolin quoted $3

5)On July 1, 2012, accumulated reserve of Dubily was $8 million

6)No interim dividend for all subsidiaries and association of Alpha Ltd.

7)All share capital is $1 for one share at par value except Carrolin that was $2 for one share.

8)The movement of Barnet’s profit and corresponding spot rate are given as foll owing:

Date Barnet’s profit in yuan Exchange rate $:¥

March 1, 2012 57.6 million 1:6.4

December 31, 2012 90 million 1: 6.3

December 31, 2013 100.6 million 1:6.0

9)Their balance sheets prepared at the end of year 2013 is shown as following:

Alpha Barnet Carrolin Dubily

$million ¥million $million $million

Fixed assets 80.00 155.00 25.00 13.00

Investment-to Barnet 30.00

-to Dubily 9.00

Current assets 150.00 173.60 20.00 15.00

Sundry Creditor (50.00)(74.40)(6.00)(5.00)

Proposed Dividend (8.00)(49.60)(3.00)

Net assets 211.00 204.60 36.00 23.00

Share capital 111.00 104.00 16.00 9.00

Retained profits 100.00 100.60 20.00 14.00

Total equities 211.00 204.60 36.00 23.00

You are required to prepare the consolidated balance sheet of above

2017 中级会计实务考试真题及答案解析 (考生回忆版 9.09)

完整版《中级会计实务》真题及答案已经上传至中公考后在线估分系统, 查看请进入 2017 年中级会计考后在线估分系统》 链接为: 选择真题估分→开始练习

矚慫润厲钐瘗睞枥。

一、单项选择题

1.2017 年 5 月 10 日,甲公司将其持有的一项以权益法核算的长期股权投资全部出售,取得价 款 1200 万元,当日办妥相关手续。出售时,该项长期股权投资的账面价值为 1100 万元,其中 投资成本为 700 万元,损益调整为 300 万元,可重分类进损益的其他综合收益为 100 万元, 不考虑增值税等相关税费及其他因素。甲公司处置该项股权投资应确认的投资收益为聞創沟燴鐺險

爱氇。

( A.100 B.500 C.200 D.400

)万元。

【答案】C

【解析】甲公司处置该项股权投资应确认的投资收益 =1200-1100+ 其他综合收益结转 100=200(万元)。残骛楼諍锩瀨濟溆。

1 / 21

2.甲公司系增值税一般纳税人,2016 年 12 月 31 日,甲公司出售一台原价为 452 万元,已 提折旧 364 万元的生产设备,取得的增值税专用发票上注明的价款为 150 万元,增值税税额 为 25.5 万元。出售该生产设备发生不含增值税的清理费用 8 万元,不考虑其他因素,甲公酽

锕极額閉镇桧猪。

司出售该生产设备的利得为( A.54 B.87.5 C.62 D.79.5 【答案】A

)万元。

【解析】甲公司出售该生产设备的利得=(150-8)-(452-364)=54(万元)。

3.下列关于不具有商业实质的企业非货币性资产交换的会计处理表述中,不正确的是(

)。

A.收到补价的,应以换出资产的账面价值减去收到的补价,加上应支付的相关税费,作为换 入资产的成本 B.支付补价的,应以换出资产的账面价值加上支付的补价和应支付的相关税费,作为换入资 产的成本 C.涉及补价的,应当确认损益 D.不涉及补价的,不应确认损益 【答案】C

【解析】 选项 C,不具有商业实质的非货币性资产交换,按照账面价值计量,无论是否涉及 补价,均不确认损益。彈贸摄尔霁毙攬砖。

2 / 21

《初级会计学》复习题 一、填空题: 1 会计的基本职能主要有:会计核算、会计监督。 1、会计核算的基本前提包括:会计主体、持续经营、会计分期和货币计量。 2、会计方法包括会计核算、会计分析、会计考核、会计预测和会计决策。 3、企业资产的价值必须等于负债与所有者权益之和。 4、负债预期会导致经济利益流出企业。 5、会计预测是可行性研究的重要组成部分。 6、会计科目按核算指标的详细程度,可以分为总分类科目和明细分类科目两类。 7、“待摊费用”和“预提费用”都是属于跨期摊配账户。 8、银行存款的清查是采用与开户银行核对账目的方法进行的。 9、原始凭证的审核包括审核原始凭证的真实性、合法性、合理性、完整性、正确性 和及时性。 10、“借贷记账法”的记账规则是:有借必有贷、借贷必相等。 11、选用适当的会计核算组织程序,对科学地组织本单位的会计核算工作具有重要 意义。 12、财务报告主要包括对外报送的会计报表、会计报表附注和财务情况说明书。 13、更正错账的方法一般有划线更正法、红字更正法、补充登记法三种。 14、成本项目一般包括直接材料、直接人工、制造费用等项目。 15、资产负债表的理论依据是资产=负债+所有者权益。 16、会计账簿按用途分类可以分为序时账簿、分类账簿和备查账簿。 17、一项同时涉及现金与银行存款之间的收付经济业务,一般只填制付款凭证。 18、不涉及企业货币资金的经济业务,一般只填制转账凭证。 19、资产负债表中,负债类项目是按其承担经济义务期限长短的顺序排列。 二、单项选择题: 1、( C )是指会计核算和监督的内容。 A、会计职能 B 、会计本质 C 、会计对象 D 、会计方法 2、某企业资产总额为100 万元,用银行存款30 万元购入材料,生产产品领用原材 料 10 万元,此时资产总额为( D )。 A、60 万元 B 、140 万元 C 、70 万元 D 、资产总额不变 3、企业向银行借入50 万元,直接偿还前欠外单位的材料款,这项业务引起企业 ( D )。 A、资产增加 50 万元 B、负债增加50万元 C、资产和负债同时增加50 万元 D、负债总额不变 4、下列属于负债类科目的是( A )。 A、预收账款 B、预付账款 C、待摊费用 D、累计折旧 5、若“应收账款”账户借方余额为500,000 元,“坏账准备”账户贷方余额为2500 元,则“应收账款净额”为(B)。 A、500,000 B、497,500 C、502,500 D、2500 6、下列不属于按用途和结构分类的账户类别是( A、资产账户 B、资本账户 C、财务成果账户 D、调整账户 7、下列属于资产类科目的是( A )。 A、预付账款 B 、预收账款 C 、应付账款A )。 D 、实收资本

行政事业单位会计复习题 第一章总论 一、复习考虑题 1,什么是预算会计?它理由哪几部分组成? 答题要点:预算会计是现代会计中与企业会计相对应的另一分支,是适用于各级政府部门、行政单位和各类非营利组织的会计体系。预算会计是以预算治理为中心,以经济和社会事业进展为目的,以预算收支核算为重点,用于核算社会再生产过程中属于分配领域中的各级政府部门、行政单位、非营利组织预算资金运动过程和结果的会计体系。 由两部分组成,财政部门总预算会计和单位预算会计,

单位预算会计又包括事业单位会计和行政单位会计。 2、与企业会计核算相比,预算会计具有哪些特点? 答题要点:从会计核算内容、会计记账基础、资金来源、会计核算原则了,会计核算难易程度来谈。 3、预算会计的差不多要素包括哪些? 资产、负债、收入、支出、净资产 4、预算会计的差不多会计等式是什么? 资产+支出=负债+净资产+收入 二、单项选择题 1、在下列会计核算的一般原则中,事业单位与企业单位会计核算不同的是( D )。 A、历史成本计价原则 B、及时性 C、真实性 D、专款专用原则

2、下列单位不属于事业单位范畴的是( D ) A、气象局 B、林业研究所 C、出版社 D、福利企业 3、预算会计的差不多等式为( D ) A、资产+支出=负债+所有者权益+收入 B、资产=负债+所有者权益 C、资产=负债+净权益 D、资产+支出=负债+净资产+收入 四、多项选择题 1、依照我国政府机构建制和经费领报关系,行政单位的会计级次具体包括下面( ABC ) A、主管会计单位 B、二级会计单位 C、三级会计单位 D、四级会计单位 2、事业单位区不于企业单位的会计要素包括

中级会计职称考试全套 试题 Company number:【WTUT-WT88Y-W8BBGB-BWYTT-19998】

内部真题资料,考试必过,答案附后 2014年中级会计职称考试真题、模拟题尽收其中,千名业界权威名师精心解析,精细化试题分析、完美解析一网打尽!在线做题就选针题库 一、单项选择题? 1、甲企业采用账龄分析法核算坏账。该企业2005年12月31日应收账款余额为200万元,“坏账准备”科目贷方余额为8万元;2006年发生坏账9万元,发生坏账收回2万元。2006年12月31日应收账款余额为180万元(其中未到期应收账款为60万元,估计损失1%;过期1个月应收账款为40万元,估计损失2%;过期2个月的应收账款为50万元,估计损失4%;过期3个月应收账款为20万元,估计损失6%;过期3个月以上应收账款为10万元,估计损失10%。)企业2006年应提取的坏账准备为()万元。? A、? B、? C、? D、-? 2、2005年9月3日,新纪公司与胜利公司签订了一份不可撤销的销售合同,双方约定,2006年3月6日,新纪公司应按每台56万元的价格向胜利公司提供甲产品6台。2005年12月31日,新纪公司甲产品的账面价值(成本)为448万元,数量为8台,单位成本为56万元,2005年12月31日,甲产品的市场销售价格为60万元/台。假定甲产品每台的销售费用和税金为1万元。2005年12月31日甲产品的账面价值为()万元。? A、448? B、450? C、442? D、440? 3、甲公司于2006年1月1日从证券市场上购入乙公司20%的股份,并对乙公司能够实施重大影响,甲公司于2006年7月1日又从证券市场上购入乙公司30%的股份,乙公司2006年全年实现净利润100万元(假定利润均衡发生)。则甲公司采用权益法核算2006年应确认的投资收益为()? A、35万元? B、25万元? C、45万元? D、50万元? 4、源通公司于2006年1月1日借入一笔长期借款,金额100万元,利率为6%,期限为3年,又于10月1日借入另一笔借款60万元,利率为9%,期限为5年。工程于当年的4月1日正式开工,4~6月的每月初发生资产支出10万元,7月1日至10月31日因工程事故发生停工,11~12月每月初发生资产支出20万元,则当年的利息资本化额为()元。? A、10000? B、9585? C、6897? D、7998? 5、股份有限公司采取收购股票的方式减资时,依次冲减的所有者权益科目是()? A、股本、资本公积、留存收益? B、留存收益、资本公积、股本? C、股本、留存收益、资本公积? D、留存收益、股本、资本公积?

初级会计考试题 一、单项选择题(每题2分,共15题) 第1题产品成本计算的分批法,适用的生产组织是()的企业。 A.大量、成批生产 B.大量、小批生产 C.单件、小批生产 D.单件、成批生产 第2题某企业2010年成本为300万元,销售收入1000万元,则该企业的销售收入成本率为()。 A.15% B.30% C.70% D.85% 第3题某企业生产的产品,属于可比产品,上年实际平均单位成本为60元,上年实际产量为500件,本年实际产量为600件,本年实际平均单位成本为57元,则本年可比产品成本降低额为()元。 A.1800 B.-4200 C.6000 D.1500 第4题某企业生产产品,属于可比产品,上年实际平均单位成本为60元,上年实际产量为500件,本年实际产量为600件,本年实际平均单位成本为57元,则本年产品可比产品成本降低率为()。 A.5% B.3% C.4.17% D.5.67% 第5题甲产品经过两道工序加工完成,采用约当产量比例法将直接人工成本在完工产品和月末在产品之间进行分配。甲产品月初在产品和本月发生的直接人工成本总计23200元。本月完工产品200件,月末第一道工序在产品20件,完成全道工序的40%;第二道工序在产品40件,完成全道工序的60%。月末在产品的直接人工成本为()元。 A.2400 B.3200 C.6000 D.20000 第6题下列各种产品成本计算方法,适用于单件、小批生产的企业的是()。 A.品种法 B.分批法 C.逐步结转分步法 D.平行结转分步法 第7题下列各项中,属于品种法特点的是()。 A.分品种、分批别、分步骤计算产品成本 B.不分品种、分批别、分步骤计算产品成本 C.分品种、分批别、不分步骤计算产品成本 D.分品种、不分批别、不分步骤计算产品成本 第8题适用于多步骤生产的成本计算方法是()。 A.品种法 B.分批法 C.分步法 D.分类法

事业单位会计专业考试试 题及答案解析 Prepared on 24 November 2020

事业单位会计专业考试试题及答案解析[1] 2014-01-23 18:05作者:华图教育来源:华图教育 【导读】事业单位会计专业考试试题及答案解析[1]。 【事业单位会计专业考试试题及答案解析】: 一、单项选择题 1.事业单位盘盈的存货,应()。 A.增加营业外收入 B.增加当期收入 C.冲减营业外支出 D.冲减当期支出 【答案】D 【解析】事业单位存货的清查不通过“待处理财产损溢”科目核算,盘盈的存货冲减“事业支出”或“经营支出”。 2.下列各项中,不属于事业单位应缴预算款的有()。 A.行政性收费收入 B.罚没收入 C.预算外资金 D.无主财物变价收入 【答案】C 【解析】应缴预算款是指行政、事业单位按规定应缴入国家预算的款项,主要包括代收的纳入预算管理的政府性基金、行政性收费、罚没收入、无主财物变价款、赃款和赃物变价款以及其他按预算管理规定应上缴预算的款项。 3.事业单位的下列科目中,年终结账后可能有余额的是()。 A.事业结余 B.经营结余 C.结余分配 D.拨出经费 【答案】B 【解析】事业单位年度终了,将“拨出经费”科目的余额全数转入“事业结余”科目;将“事业结余”和“经营结余”科目的余额转入“结余分配”科目,但如果“经营结余”科目有借方余额,则不结转;结余在分配后,将未分配结余全数转入“事业基金――一般基金”科目中,因此“结余分配”也不会有余额。 4.某事业单位2007年年初事业基金中,一般基金结余为450万元。2007年该事业单位收入为5 300万元,事业支出为4 800万元;拨入专款为800万元,专款支出为700万元,该项目年末尚未最后完成;对外投资为600万元。假定不考虑计算交纳所得税和计提专用基金,则该单位2007年年末事业基金中,一般基金结余为()万元。 【答案】A

事业单位招聘考试会计基础知识重点解析

事业单位招聘考试《会计基础知识》重点解析 【第一章】总论 1.会计的基本职能:会计核算、会计监督。会计核算的环节:确认、计量、记 录、报告。 2.会计核算的工作:记账、算账、报账。 3.会计核算与会计监督的关系:会计核算职能和会计监督职能是相辅相成、辩 证统一的关系。会计核算是会计监督的基础,没有核算所提供的各种信息,监督就失去了依据;而会计监督又是会计核算质量的保障,只有核算、没有监督,就难以保证核算所提供信息的真实性、可靠性。 4.会计核算的基本前提:会计主体、持续经营、会计分期和货币计量。 5.会计核算四项基本前提之间的关系:会计核算的四项基本前提,具有相互依 存、相互补充的关系。具体地说:会计主体确立了会计核算的空间范围,持续经营与会计分期确立了会计核算的时间长度,而货币计量则为会计核算提供了必要手段。没有会计主体就不会有持续经营;没有持续经营就不会有会计分期;没有货币计量就不会有现代会计。 6.会计要素共计有六项,分为两大类。第一类会计要素表现资金运动的静止状 态,反映企业的财务状况,包括资产、负债和所有者权益三项。第二类会计要素表现资金运动的显著变动状态,反映企业的经营成果,包括收入、费用和利润三项。 7.所有者权益包括实收资本(或者股本)、资本公积、盈余公积和未分配利润 等。其中,前两者是由企业所有者直接投入的(例如溢价发行股票),而盈余公积和未分配利润是企业在生产过程当中所实现的利润留存企业所形成的部分,因此,盈余公积和未分配利润又统称为留存收益。因此,也能够表述为:所有者权益包括实收资本(或股本)、资本公积和留存收益等。8.收入与资产、负债和所有者权益的关系:收入表现为企业资产的增加或负债 的减少,或两者兼而有之(部分收入还债),最终导致企业所有者权益的增

中级会计职称考试历年真题 为了帮助考生们进一步了解中级会计职称考试的题型、命题风格、各科目分值分布、考试的重点及难易程度,为大家整理了2010年至2019年近十年的中级会计职称考试真题及答案解析供大家学习,祝大家学习愉快,梦想成真! (蓝色带下划线的内容带有网页链接,按住Ctrl并单击想要查看的内容即可打开网页,如果失败,可右击想要查看的内容-编辑超链接-找到网址。) 2019年 ·2019年《中级会计实务》考试真题及答案解析 ·2019年《经济法》考试真题及答案解析 ·2019年《财务管理》考试真题及答案解析 2018年: ·2018年《中级会计实务》考试真题及答案解析 ·2018年《经济法》考试真题及答案解析 ·2018年《财务管理》考试真题及答案解析 2017年 ·2017年《中级会计实务》考试真题及答案解析 ·2017年《经济法》考试真题及答案解析 ·2017年《财务管理》考试真题及答案解析 2016年 ·2016年《中级会计实务》考试真题及答案解析 ·2016年《经济法》考试真题及答案解析 ·2016年《财务管理》考试真题及答案解析 2015年 ·2015年《中级会计实务》考试真题及参考答案 ·2015年《经济法》考试真题及参考答案 ·2015年《财务管理》考试真题及参考答案

2014年 ·2014年《中级会计实务》考试真题及参考答案 ·2014年《经济法》考试真题及参考答案 ·2014年《财务管理》考试真题及参考答案 2013年 ·2013年《中级会计实务》考试真题及答案解析 ·2013年《经济法》考试真题及答案解析 ·2013年《财务管理》考试真题及答案解析 2012年 ·2012年《中级会计实务》真题及答案解析 ·2012年《经济法》真题及答案解析 ·2012年《财务管理》真题及答案解析 2011年 ·2011年《中级会计实务》考试真题及参考答案 ·2011年《经济法》考试真题及参考答案 ·2011年《财务管理》真题及答案解析 2010年 ·2010年《中级会计实务》真题及答案解析 ·2010年《经济法》真题及答案解析 ·2010年《财务管理》真题及答案解析 注:由于试题压缩包文件过大不便于直接下载,为减少下载过程中的问题请点击以上链接分别下载各科目试题。

第1题单选 某上市公司公开发行普通股1000万股,每股面值1元,每股发行价格5元,支付券商发行费用 120万元。该公司发行普通股计入股本的金额为( )万元。初级会计师考试历年真题答案及解析 A.1000 B.3880 C.4880 D.5000 答案:A 解析:计入股本的金额=1000×1=1000(万元)。 第2题单选 甲、乙公司均为增值税一般纳税人,适用的增值税税率为17%,甲公司接受乙公司投资转入的原材 料一批,账面价值l00000元,投资协议约定价值120000元,假定投资协议约定的价值与公允价值相符,该项投资没有产生资本溢价。甲公司实收资本应增加( )元。 A.100000 B.117000 C.120000 D.140400 答案:D 解析:甲公司实收资本增加=120000 ×(1+17%)=140400(元)。 第3题单选初级会计报名点 某股份有限公司股本为100万元(每股面值l元),资本公积(股本溢价)为150万元,盈余公积为100 万元。经股东大会批准以每股3元价格回购本公司股票100万股并予以注销,不考虑其他因素,下列关于该公司注销库存股的会计处理正确的是( )。 A.借:股本 1000000 资本公积-股本溢价 1500000 盈余公积 500000 贷:库存股 3000000 B.借:股本 1000000 资本公积-股本溢价 1500000 盈余公积 500000 贷:银行存款 3000000 C.借:库存股 3000000 贷:银行存款 3000000 D.借:股本 3000000 贷:银行存款 3000000 答案:A 解析:回购本公司股票: 借:库存股 3000000 贷:银行存款 3000000(1000000 × 3) 注销本公司股票时: 借:股本 1000000 资本公积-股本溢价 1500000 盈余公积 500000 贷:库存股 3000000 第4题单选会计初级考试报名

2018年10月高等教育自学考试全国统一命题考试 政府与事业单位会计 (课程代码“00070) 第一部分选择题 一、单项选择题:本大题共2小题,每小题1分,共20分,在每小题列出的备选项中只有一项是最符合题目要求的,请将其选出。 1、政府与事业单位会计要求“对会计主体的各项经济业务应当及时核算”,其符合会计信息质量要求的原则是() A、真实性 B、相关性 C、及时性 D、实质性 2、下列不属于政府财政会计任务的是() A、合理调度财政资金 B、进行实物资产管理 C、正确处理日常核算事务 D、实施会计监督并参与预算管理 3、下列选项中,符合政府与事业单位会计特点的是() A、专用性 B、盈利性 C、灵活性 D、增值性 4、下列选项中,属于政府财政会计资产类科目的是() A、库存现金 B、有价证券 C、固定资产 D、无形资产 5、省级财政用一般预算结余购入一年期国库券200亿元,应贷记的账户是() A、在途款 B、有价证券 C、与上级往来 D、国库存款 6、下列选项中,属于我国政府与事业单位会计应遵循的基本法律是() A、行政单位会计制度 B、事业单位会计制度 C、中华人民共和国预算法 D、财政总预算会计制度 7、下列选项中,不属于行政单位财政直接支付方式适用范围的是() A、零星支出 B、购买支出 C、工资支出 D、转移支出 8、下列选项中,不包括在货币资金核算范围的是() A、借入款项 B、现金 C、银行存款 D、零余额账户用款额度 9、行政单位“零余额账户用款额度”借方余额反映的是() A、经费支出 B、经费收入

C、已经使用的财政授权支付额度 D、尚未使用的财政授权支付额度 10、下列选项中,属于行政单位收入类科目的是() A、银行存款 B、经费支出 C、其他收入 D、财政应返还额度 11、下列选项中,不属于行政单位使用的银行结算凭证是() A、现金支票 B、转账支票 C、银行信汇凭证 D、商业承兑汇票 12、下列选项中,按规定符合行政单位资产负债表编制时间要求的是() A、按日编制 B、按旬编制 C、按季编制 D、按年编制 13、事业单位依法取得的短期投资,应作为入账价值的是() A、取得时间的实际成本 B、公允价值 C、可变现净值 D、现值 14、下列选项中,不属于事业单位领用材料计价方法的是() A、先进先出法 B、加权平均法 C、个别计价法 D、后进先出法 15、事业单位购入不构成相关硬件但不可缺少的应用软件,应借记的科目是() A、无形资产 B、固定资产 C、存货 D、在建工程 16、事业单位短期投资发生的亏损,应采用的处理方式是() A、冲减其他收入 B、列支其他支出 C、计入事业支出 D、抵减当年结余 17、下列选项中,不属于事业单位“应付职工薪酬”核算内容的是() A、基本工资 B、绩效工资 C、住房公积金 D、扣缴的个人所得税 18、下列选项中,影响事业单位经营结余的因素是() A、财政补助收入 B、上级补助收入 C、经营收入 D、其他收入 19、事业单位盘盈的存货,应按照确定的入账价值采取的会计处理方式是() A、增加事业收入 B、增加其他收入 C、冲减事业支出 D、冲减其他支出 20、某市京剧团将本月实现的净结余上缴市文化局,应借记的科目是() A、财政补助支出 B、上缴上级支出 C、事业支出 D、其他支出 第二部分非选择题 二、辨析题:判断正误,并说明理由。本大题共5小题,每小题4分,共20分。 21、政府财政会计、行政单位会计通过计算单位的收入与费用来核算盈亏。 判断: 理由: 22、在政府财政会计中,“与下级往来”账户具有资产和负债双重性质。

2019年巴塘县事业单位招聘考试《会计操作实务》真题库及答案【含 解析】 说明:本题库收集历年及近期考试真题,全方位的整理归纳备考之用。 注意事项: 1、答题前,考试务必将自己的姓名,准考证号用黑色签字笔或钢笔填写在答题纸规定的位置。 2、监考人员宣布考试结束时,你应立即停止作答。将题本、答题卡和草稿纸都翻过来留在桌上,待监考人员确认数量无误、允许离开后方可离开。 3、特别提醒您注意,所有题目一律在答题卡指定位置答题。未按要求作答的,不得分。 一、选择题(在下列每题四个选项中选择符合题意的,将其选出并把它的标号写在题后的括号内。错选、多选或未选均不得分。) 1、内部审计的责任是对内部控制设计和运行的()进行审查和评价,出具客观公正的审计报告,促 进组织改善内部控制及风险管理。 A、合理性 B、真实性 C、可靠性 D、有效性 【答案】D 2、下列情形中,不属于损害组织经济利益的舞弊的是:()。 A、收受贿赂或回扣 B、贪污、挪用、盗窃组织资产 C、泄露组织的商业秘密 D、出售不存在或不真实的资产 【答案】D 3、订本账一般不适用于()。 A、总分类账 B、固定资产明细账 C、银行存款日记账 D、库存现金日记账 【答案】B 【解析】订本账能避免账页散失和防止抽换账页,但是不能准确为各账户预留账页,预留太多造成浪费,预留太少影响连续登记。订本账同一本账簿在同一时间只能由一个人登记,这样不便于记账人员分工记账。这种账簿一般适用于总分类账、库存现金日记账和银行存款日记账。B项,固定资产明细账一般采用卡片式。 4、一般来说,单位撤销、合并或改变隶属关系时,要进行()。

A、全面清查 B、部清查 C、定期清查 D、技术推算盘点 【答案】A 【解析】单位撤销、合并或改变隶属关系前,企业要进行一次全面清查,以明确经济责任。故选A。 5、“利润分配——未分配利润”账户的借方余额表示()。 A、本期实现的净利润 B、本期发生的净亏损 C、累计实现的净利润 D、累计的未弥补亏损 【答案】D 【解析】“利润分配——未分配利润”账户的贷方余额为历年累积的未分配利润(即可供以后年度分配的利润),借方余额表示累计的未弥补亏损(即留待以后年度弥补的亏损)。故选D。 6、下列哪种情况下,对应付账款不用函证()。 A、控制风险高 B、财务状况不佳 C、应付账款金额较大 D、存在大量小金额的欠款 【答案】D 7、凡需要结出余额的账户,没有余额的账户,应当在“借或贷”栏内写()字。 A、借 B、贷 C、平 D、0~ 【答案】C 【解析】凡需要结出余额的账户,结出余额后,应当在“借或贷”栏内写明“借”或者“贷”等字样。没有余额的账户,应当在“借或贷”栏内写“平”字,并在“余额”栏用“0~”表示。库存现金日记账和银行存款日记账必须逐日结出余额。 8、审计业务涉及的三方关系人是指()。 A、注册会计师、委托人、被审计单位 B、注册会计师、委托人、责任方 C、注册会计师、责任方、预期使用者

一、单项选择题 1.2017 年5 月10 日,甲公司将其持有的一项以权益法核算的长期股权投资全部出售,取得 价款1200 万元,当日办妥相关手续。出售时,该项长期股权投资的账面价值为1100 万元, 其中投资成本为700 万元,损益调整为300 万元,可重分类进损益的其他综合收益为100 万元,不考虑增值税等相关税费及其他因素。甲公司处置该项股权投资应确认的投资收益为 ()万元。 A.100 B.500 C.200 D.400 【答案】C 【解析】甲公司处置该项股权投资应确认的投资收益=1200-1100+其他综合收益结转 100=200(万元)。 2.甲公司系增值税一般纳税人,2016 年12 月31 日,甲公司出售一台原价为452 万元,已 提折旧364 万元的生产设备,取得的增值税专用发票上注明的价款为150 万元,增值税税额

为25.5 万元。出售该生产设备发生不含增值税的清理费用8 万元,不考虑其他因素,甲公 司出售该生产设备的利得为()万元。 A.54 B.87.5 C.62 D.79.5 【答案】A 【解析】甲公司出售该生产设备的利得=(150-8)-(452-364)=54(万元)。 3.下列关于不具有商业实质的企业非货币性资产交换的会计处理表述中,不正确的是()。 A.收到补价的,应以换出资产的账面价值减去收到的补价,加上应支付的相关税费,作为换 入资产的成本 B.支付补价的,应以换出资产的账面价值加上支付的补价和应支付的相关税费,作为换入资 产的成本 C.涉及补价的,应当确认损益 D.不涉及补价的,不应确认损益 【答案】C 【解析】选项C,不具有商业实质的非货币性资产交换,按照账面价值计量,无论是否涉及

一、单项选择题(本类题共20小题,每小题1分,共20分。每小题备选答案中,只有一个符合题意的正确答案。请将选定的答案,按答题卡要求,用2B铅笔填涂答题卡中题号1至20信息点。多选、错选、不选均不得分) 1.下列各项中,会导致留存收益总额发生增减变动的是( )。 A.资本公积转增资本 B.盈余公积补亏 C.盈余公积转增资本 D.以当年净利润弥补往常年度亏损 【答案】 C 【解析】

留存收益包括两部分:盈余公积和未分配利润,只要阻碍盈余公积或者未分配利润,都会导致留存收益的变动。用分录进行分析: 选项A 借:资本公积 贷:股本或实收资本 留存收益不受阻碍。 选项B 借:盈余公积 贷:利润分配—未分配利润 留存收益总额不变。 选项C 借:盈余公积 贷:股本或实收资本

留存收益减少。 选项D 借:本年利润 贷:利润分配—未分配利润 留存收益总额不变。 【点评】本题目考核的是第4章留存收益知识点。本题目中可能有的学员会对D选项产生疑问,事实上看到选项C时能够直接推断出答案来了,因为选项C是特不明确的,那么D就不用再看了,因为单纯从D选项这一时点上分析的话,企业的留存收益总额可不能变动。这道题目相对来讲比较容易,事实上在我们平常的学习中都有反复练习,老师在课程中也都有特不的强调,因此这道题目的分值确信不能丢。 2.某企业2008年1月1日所有者权益构成情况如下:实收资本1500万元,资本公积100万元,盈余公积300万元,未分配利润200万元。2008年度实现利润总额为600万元,企业所得

税税率为25%。假定不存在纳税调整事项及其他因素,该企业2008年12月31日可供分配利润为( )万元。 A.600 B.650 C.800 D.1100 【答案】 B 【解析】本题目考核第4章可供分配利润知识点。企业可供分配利润=当年实现的净利润+年初未分配利润(或-年初未弥补亏损)+其他转入(即盈余公积补亏),,本题目没有涉及盈余公积补亏事项,因此本题目的计算式子: 200+600×(1-25%)=650(万元) 【点评】本题目在做的时候需要看清晰题目给定的是利润总额,而不是净利润,需要扣除所得税费用。本题目事实上考核了两点内容,第一点是由利润总额如何得到净利润,第二点是可供分配利润如何进行计算。

第一章 1. 下列各会计要素,()不是反映财务状况的会计要素。 A.资产 B.负债 C.收入 D.所有者权益 [答案]:C [解析]:反映财务状况的会计要素包括资产、负债、所有权益。 2. 在会计职能中,属于控制职能的是()。 A.进行会计核算 B.实施会计监督 C.参与经济决策 D.评价经营业绩 [答案]:B [解析]:会计监督职能也被称为控制职能,即实施过程控制,包括事前、事中和事后的监督。 3. 下列各会计要素,()不属于所有者权益。 A.资本公积金 B.盈余公积金 C.未分配利润

D.累计折旧 [答案]:D [解析]:所有者权益包括企业投资者对企业的投入资本以及形成的资本公积金、盈余公积金和未分配利润等。 4. 下列方法中,不属于会计核算方法的有()。 A.填制会计凭证 B.登记会计账簿 C.编制财务预算 D.编制会计报表 [答案]:C [解析]:会计核算的七种方法包括:(1)设置会计科目和账户;(2)复式记账;(3)填制和审核会计凭证;(4)登记账簿;(5)成本计算;(6)财产清查;(7)编制会计报表。 5. 会计核算的最终环节是()。 A.确认 B.计量 C.计算 D.报告 [答案]:D [解析]:会计核算的最终环节是报告,是指通过编制会计报表的形式有关方面和人员提供会计信息,它是会计工作的最终环节。

6. 关于会计的说法错误的是()。 A.会计是一项经济管理活动 B.会计的主要工作是核算和监督 C.会计的对象针对的是某一主体平时所发生的经济活动 D.货币是会计唯一计量单位 [答案]:D [解析]:货币是会计核算的主要计量单位,但并不是唯一的计量单位。 7. 下列各项中不属于谨慎性原则要求的是() A.资产计价时从低 B.利润估计时从高 C.不预计任何可能发生的收益 D.负债估计时从高 [答案]:B [解析]:谨慎性原则要求企业在进行会计核算时,不得多计资产或收益、少计负债或费用,也不得计提秘密准备。但如果在资产计价及损益确定时,如果有两种或两种以上的方法或金额可供选择时,应选择使本期净资产和利润较低的方法或金额。即资产计价时从低,负债估计时从高;不预计任何可能的收益,但如果有合理的基础可以估计时,应预计可能发生的损失和费用。 8. 下列不属于会计核算12项一般原则的是() A.划分收益性支出与资本性支出

2015年会计继续教育试题——新《事业单位财务规则》讲解 一、单项选择题(本类题共15小题,每小题2分,共30分。单项选择题 (每小题备选答案中,只有一个符合题意的正确答案,请选择正确选项。) 1.下列各项中,不属于事业单位财务报表的组成是()。 A.财务情况说明书 B.收入支出表 C.资产负债表 D.财政拨款收入支出表 A B C D 答案解析: 事业单位报送的年度财务报告包括资产负债表、收入支出表、财政拨款收入支出表、固定资产投资决算报表等主表,有关附表以及财务情况说明书等。事业单位财务报表包括资产负债表、收入支出表、财政拨款收入支出表、固定资产投资决算报表等主表和有关附表。 2.下列各项中,不属于事业单位预算编制原则的是()。 A.以支定收、收支平衡的原则 B.收支统管、统筹兼顾的原则 C.重点性原则 D.绩效性原则 A B C D 答案解析: 事业单位预算编制原则有:合法性原则、以收定支、收支平衡的原则、收支统管、统筹兼顾的原则、重点性原则、绩效性原则。 3.下列各项中,对项目资金管理的说法不正确的是()。 A.专款专用 B.定期报送资金使用情况 C.不用检查验收 D.单独核算 A B C D 答案解析: 根据新规则第二十三条规定:事业单位从财政部门和主管部门取得的有指定项目和用途的专项资金,应当专款专用、单独核算,并按照规定向财政部门或者主管部门报送专项资金使用情况;项目完成后,应当报送专项资金支出决算和使用效果的书面报告,接受财政部门或者主管部门的检查、验收。

事业单位对项目资金全过程实施控制。项目资金管理有三点要求:专款专用、单独核算;定期报送资金使用情况;检查验收。 4.下列各项中,不属于按照监督实施时间对财务监督分类的是()。 A.事前监督 B.事中监督 C.事后监督 D.日常监督 A B C D 答案解析:财务监督按监督实施时间分为事前监督、事中监督与事后监督。 5.当年预算已执行但未完成,或者因故未执行,下一年度需要按照原用途继续使用的资金的是()。 A.事业基金 B.专用基金 C.结余资金 D.结转资金 A B C D 答案解析:结转资金是指当年预算已执行但未完成,或者因故未执行,下一年度需要按照原用途继续使用的资金。 6.下列各项中,对事业单位收入管理的要求的说法不正确的是()。 A.实行收入统管 B.正确划分各项收入,依法缴纳各种税费 C.保证收入的合法性与合理性 D.实行收入分散管理 A B C D 答案解析:事业单位收入管理的要求主要有: (1)实行收入统管 (2)正确划分各项收入,依法缴纳各种税费 (3)充分利用现有条件积极组织收入 (4)保证收入的合法性与合理性 (5)正确处理社会效益与经济效益的关系 (6)加强事业单位收入票据管理 (7)加强对经营收入的管理 7.下列各项中,关于预算编制的审核说法不正确的是()。 A.事业单位提出预算建议数,需经主管部门审核 B.事业单位预算要报财政部门审核批复 C.事业单位预算要经法定程序审核批复后才能执行 D.事业单位事业收入预算可以由单位自己决定,无需报审

2015年中级会计师《会计实务》考试真题及答案解析( word 版) 一.单选题 1. 甲公司向乙公司发出一批实际成本为30万元的原材料,另支付加工费6万元(不含 增值税),委托乙公司加工成一批适用消费税税率为10%的应税消费品,加工完成后,全部 用于连续生产应税消费品,乙公司代扣代缴的消费税款准予后续抵扣。甲公司和乙公司均系 增值税一般纳税人,适用的增值税均为17%不考虑其他因素,甲公司收回的该批应税消费 品的实际成本为()万元 【参考答案】A 【解析】委托加工物资收回后用于连续加工应税消费品的,加工环节的消费税计入“应 交税费一应交消费税”的借方,不计入委托加工物资的成本,因此本题应税消费品的实际成本 =30+6=36(万元) 2. 甲公司系增值税一般纳税人,2015年8月31日以不含增值税100万元的价格售出 2009年购入的一台生产用机床,增值税销项税额为17万元,该机床原价为200万元(不含 增值税),已计提折旧120万元,已计提减值准备30万元,不考虑其他因素,甲公司处置该机床的利得为()万元。

【参考答案】D 【解析】处置固定资产利得=100-(200-120-30)=50(万元) 3. 下列各项资产准备中,在以后会计期间符合转回条件予以转回时,应直接计入所有 者权益类科目的是() A. 坏账准备 B. 持有至到期投资减值准备 C. 可供出售权益工具减值准备 D. 可供出售债务工具减值准备 【参考答案】C 【解析】可供出售权益工具减值恢复时,通过所有者权益类科目“其他综合收益”转回。 4. 2014年12月31日,甲公司某项无形资产的原价为120万元,已摊销42万元,未 计提减值准备,当日,甲公司对该项无形资产进行减值测试,预计公允价值减去处置费用后的净额为55万元,未来现金流量的现值为60万元,2014年12月31日,甲公司应为该无形资产计提的减值准备为()万元。

单项选择题 “应付利息”科目核算的内容是()。 A. 企业按实际利率计算的利息 B. 企业按合同约定应支付的利息 C. 到期一次还本付息的长期债券应付的利息 D. 到期时一次归还本金和利息的长期借款的利息 【正确答案】B 【答案解析】应付利息”科目核算的是分期付息借款和债券按合同约定应支付的利息。 单项选择题初级会计历年真题及答案解析 2012年9月1日,某企业向银行借入一笔期限2个月、到期一次还本付息的生产经营周转借款200 000元,年利率6%。借款利息不采用预提方式,于实际支付时确认。11月1日,企业以银行存款偿还借款本息的会计处理正确的是()。 A、借:短期借款200 000 应付利息2 000 贷:银行存款202 000 B、借:短期借款200 000 应付利息1 000 财务费用1 000 贷:银行存款202 000初级会计报名 C、借:短期借款200 000 财务费用2 000 贷:银行存款202 000 D、借:短期借款202 000 贷:银行存款202 000 【正确答案】C 【答案解析】本题考核短期借款,题目中说借款利息不采用预提方式,所以可在支付时直接计入当 期损益,计入“财务费用”,还款时直接支付本金和利息。借记“短期借款”、“财务费用”,贷记“银行存款”。 单项选择题初级会计实务教材 某公司向职工发放自产的加湿器作为福利,该产品的成本为每台150元,共有职工500人,计税价 格为200元,增值税税率为17%,计入该公司应付职工薪酬的金额为()元。 A、117000 B、75000 C、100000 D、92000 【正确答案】A 【答案解析】本题的分录是: 借:管理费用117000 贷:应付职工薪酬117000 借:应付职工薪酬117000 贷:主营业务收入100000 应交税费——应交增值税(销项税额)17000 借:主营业务成本75000 贷:库存商品75000 单项选择题初级会计报名条件

行政事业单位 1、行政事业单位会计分类:行政单位会计和事业单位会计 2、行政事业单位会计组织系统:①主管会计单位(同级财政部门领报经费、发生预算管理 关系)②二级会计单位(向上级财政部门领报经费、发生预算管理关系)③基层单位会计 3、行政事业单位会计特点:①会计目标侧重于满足预算管理的需要②以收付实现制为基础 ③会计要素分类:资产、负债、净资产,收入,支出④会计报表简单:资产负债表和收 入支出表⑤某些会计核算不同于企业会计:固定资产不计提折旧 4、资产: 货币资金;应收及预付款项;存货;对外投资(事业基金-投资基金);固定资产; 无形资产 无形资产(按是否实行内部成本核算分为一次性摊销和分期平均摊销,分别计入当期支出) 固定资产一般不计提折旧(除融资租入固定资产外),固定资产的账面余额一般等于固定基金。 5、负债:借入款项;应缴款项;应付和预收款项 应缴款项包括应缴预算款(应缴入财政预算的各种款项)、应缴财政专户款(代收应上缴的财政专户的预算外的资金)、应缴税金。 6、净资产 1、事业基金:一般基金和投资基金(对外投资) 一般基金是事业单位滚存的结余资金,有两个来源,一是从本单位当期未分配结余转入,二是从拨入专款结余按规定留归本单位使用的金额转入,期末都要转入。 2、固定基金:事业单位固定资产所占用的资金。 3、专用基金:按规定提取,设置有专门用途的资金,包括修购基金;职工福利基金; 医疗基金以及住房基金。 4、结余:事业结余(年度终了,事业结余应当全数转入结余分配);经营结余(年度终 了,经营结余应当转入结余分配,但如果是亏损,则不予结转)“经营结余”借方 为亏损。 5、结余分配:事业单位当年实现的结余应按照规定进行分配,主要有两项,一是计算 应缴纳的所得税,二是事业单位计提的专用基金,分配后,结余的当年未分配结余 转入事业基金(一般基金)。 7、收入:事业单位收入包括财政补助收入,上级补助收入、拨入专款、事业收入、经营收 入(可以采用权责发生制)、附属单位缴款、其他收入。 8、支出:开展业务活动或其他活动所发生的各项资金耗费及损失。事业支出、经营支出、 专款支出等。 9、会计报表:资产负债表、收入支出表,分为月报、季报、年报三种。

中级会计实务考试试题Prepared on 21 November 2021

内部真题资料,考试必过,答案附后 一、单项选择题(本类题共15小题,每小题1分,共15分。每小题备选答案中,只有一个符合题意的正确答案。请将选定的答案,按答题卡要求,用2B铅笔填涂答题卡中题号1至15信息点,多选、错选,不选均不得分。) 1.下列各项外币资产发生的汇兑差额,不应计入当期损益的是( )。 A.应收账款 B.交易性金融资产 C.持有至到期投资 D.可供出售权益工具投资 【答案】D 【解析】选项A,计入财务费用,选项B,计入公允价值变动损益,选项C,计入财务费用,选项D,计入资本公积。 【试题点评】本题“考核汇兑差额”知识点。 2.下列关于会计估计及其变更的表述中,正确的是( )。 A.会计估计应以最近可利用的信息或资料为基础 B.对结果不确定的交易或事项进行会计估计会削弱会计信息的可靠性 C.会计估计变更应根据不同情况采用追溯重述或追溯调整法进行处理 D.某项变更难以区分为会计政策变更和会计估计变更的,应作为会计政策变更处理 【答案】A 【解析】选项B,会计估计变更不会削弱会计信息的可靠性;选项C,会计估计变更应采用未来适用法;选项D,应该作为会计估计变更处理。 【试题点评】本题考核“会计估计变更”知识点。 年12月31日,甲公司对一起未决诉讼确认的预计负债为800万元。2011年3月6日,法院对该起诉讼判决,甲公司应赔偿乙公司600万元;甲公司和乙公司均不再上诉。甲公司的所得税税率为25%,按净利润的10%提取法定盈余公积,2010年度财务报告批准报出日为2011年3月31日,预计未来期间能够取得足够的应纳税所得额用以抵扣可抵扣暂时性差异。不考虑其他因素,该事项导致甲公司2010年12月31日资产负债表“未分配利润”项目“期末余额”调整增加的金额为( )万元。