CFA考试一级章节练习题精选0329-43(附详解)

1、Which of these is the best example of an embedded option granted to bondholders?【单选题】

A.A prepayment option

B.A floor on a floating rate security

C.An accelerated sinking fund provision

正确答案:B

答案解析:“Features of Debt Securities,” Frank J. Fabozzi, CFA

2011 Modular Level I, Vol. 5, p. 337

Study Session 15-61-e

Identify the common options embedded in a bond issue, explain the importance of embedded options, and state whether such options benefit the issuer or the bondholder.

B is correct because the floor benefits the bondholder by keeping the coupon from falling below a certain threshold if market rates decline to very low levels.

2、An analyst does research about reinvestment risk.Which of the following securitiesis most likely to be subject to reinvestment risk during the period of time betweenissuance and maturity?【单选题】

A.Treasury bills.

B.Treasury notes.

C.Treasury coupon strips.

正确答案:B

答案解析:Treasury bills是美国国库券,是短期债券,而且是完全折价债券,到期前没有利息,到期时一次还本,所以没有再投资风险;Treasury coupon strips是美国本息剥离的国债,投资银行将美国的中长期国债的每一笔利息和本金拆分成不同期限的完全折价债券,所以也没有再投资风险;而Treasury notes是美国中期国债,每半年发放一次利息,会有再投资风险。

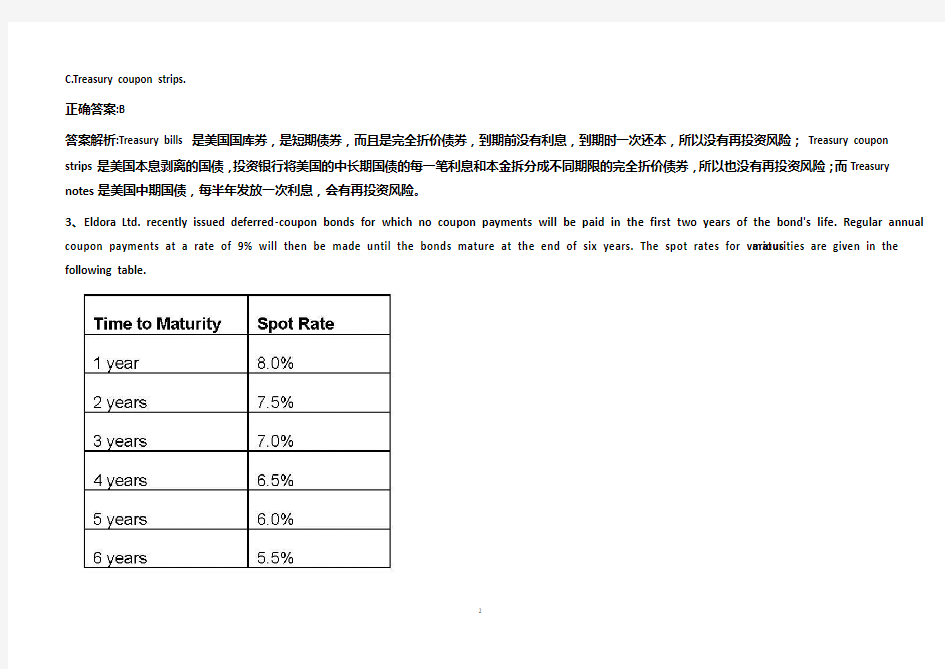

3、Eldora Ltd. recently issued deferred-coupon bonds for which no coupon payments will be paid in the first two years of the bond's life. Regular annual coupon payments at a rate of 9% will then be made until the bonds mature at the end of six years. The spot rates for various maturities are given in the following table.

On the basis of these spot rates, the price of the bond today is closest to:【单选题】

A.100.12.

B.108.20.

C.116.24.

正确答案:A

答案解析:The bond price is computed as:

2014 CFA Level I

"Introduction to Fixed-Income Valuation," by James F. Adams and Donald J. Smith

Section 2.4

4、A long-term bond investor with an investment horizon of 8 years invests in option-free, fixed-ratebonds with a Macaulay duration of 10.5. The investor most likely currently has a:【单选题】

A.positive duration gap and is currently exposed to the risk of lower interest rates.

B.negative duration gap and is currently exposed to the risk of higher interest rates.

C.positive duration gap and is currently exposed to the risk of higher interest rates.

正确答案:C

答案解析:The duration gap is the bond's Macaulay duration minus the investment horizon, which is positive inthis case. A positive duration gap implies that the investor is currently exposed to the risk of higherinterest rates.

CFA Level I

"Understanding Fixed-Income Risk and Return", James F. Adams and Donald J. Smith

Section 4.2

5、Which of the following measures of interest rate risk is most appropriate forbonds with prepayment option?【单选题】

A.Effective duration.

B.Modified duration.

C.Macaulay duration.

正确答案:A

答案解析:对于有内含权或者提前偿付权的债券而言,由于现金流是不确定的,故应该用有效久期测量利率风险,而不能用修正久期或麦考利久期。