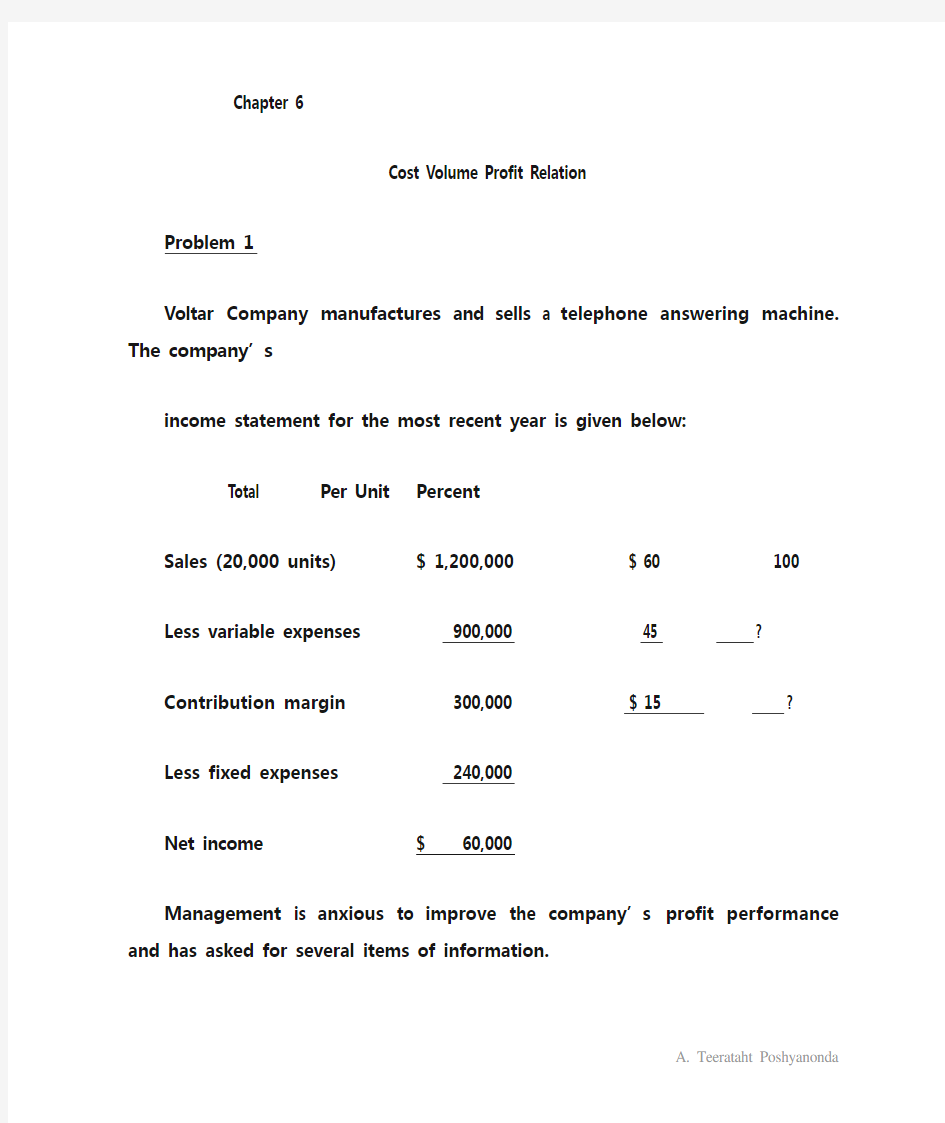

Chapter 6

Cost Volume Profit Relation Problem 1

Voltar Company manufactures and sells a telephone answering machine. The company’s

income statement for the most recent year is given below:

Total Per Unit Percent

Sales (20,000 units) $ 1,200,000 $ 60 100

Less variable expenses 900,000

45 ?

Contribution margin 300,000 $ 15 ?

Less fixed expenses 240,000

Net income $ 60,000

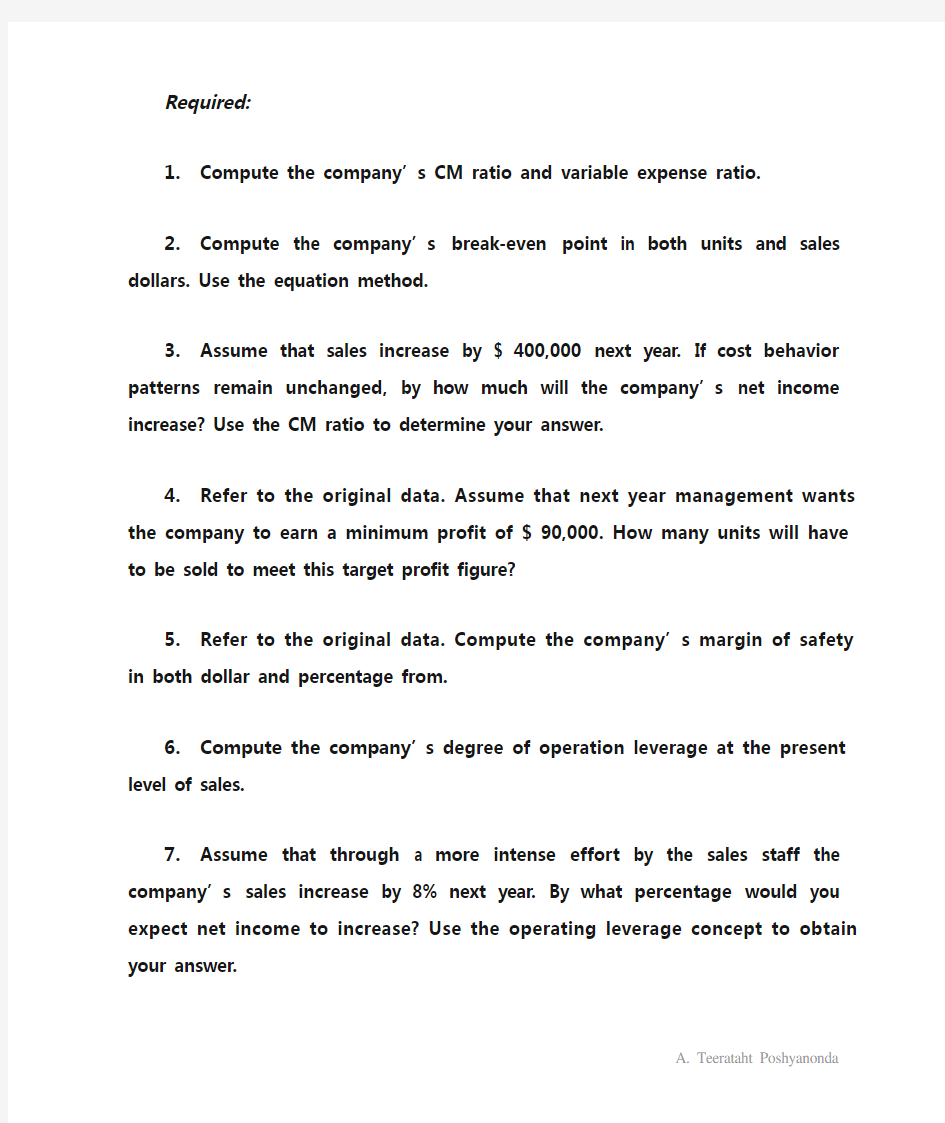

Management is anxious to improve the company’s profit performance and has asked for several items of information. Required:

https://www.doczj.com/doc/5f6498972.html,pute the company’s CM ratio and variable

expense ratio.

https://www.doczj.com/doc/5f6498972.html,pute the company’s break-even point in both

units and sales dollars. Use the equation method.

3.Assume that sales increase by $ 400,000 next year.

If cost behavior patterns remain unchanged, by how

much will the company’s net income increase? Use

the CM ratio to determine your answer.

4.Refer to the original data. Assume that next year

management wants the company to earn a

minimum profit of $ 90,000. How many units will

have to be sold to meet this target profit figure?

5.Refer to the original data. Compute the company’s

margin of safety in both dollar and percentage from. 6.Co mpute the company’s degree of operation

leverage at the present level of sales.

7. Assume that through a more intense effort by the sales

staff the company’s sales increase by 8% next year. By what percentage would you expect net income to

increase? Use the operating leverage concept to obtain your answer.

8.Verify your answer to (7) by preparing a new income

statement showing an 8% increase in sales.

9.In an effort to increase sales and profits, management

is considering the use of a higher-quality speaker in the answering machine. The higher-quality speaker would increase variable costs by $ 3 per units, but

management could eliminate one quality inspector who is paid a salary of $ 30,000 per year. The sale manager

estimates that the higher-quality speaker would increase annual sales by at least 20%.

A.Assuming that changes are made as described

above, prepare a projected income statement for

next year. Show data on a total, per unit, and

percentage basis.

https://www.doczj.com/doc/5f6498972.html,pute the company’s new break-even point in

both units and dollars of sales. Use the

contribution margin method.

C.Would you recommend that the changes be made?

Chapter 6 Problem 2

Johnny Reunitis has observed the success of the old-timers’ games in baseball and basketball, and he is considering putting on such a game with retired USFL football players on the day preceding the Super Bowl. He had received permission from the commissioner of the USFL and has lined up quite a few players who need the money and were not famous enough to do light-beer commercials. He is now trying to figure out whether the game can be profitable, and he has complied the following information:

Ticket price $ 20

Average concession revenue per customer $ 10 Advertising $ 75,000 Concession costs 60% of concession revenues

Health insurance $ 50,000

MVP awards $ 25,000

Rental of stadium $100,000

Fee for players $ 200,000 plus 10% of ticket revenues

Required:

1.How many fans would have to attend the game in order

for Reunitis to break-even?

2.If Reunitis wanted to generate a net income of 30% of

ticket revenues, how many fans would have to attend the game?

3.If Reunitis has to pay 20% of his net income to the

player’s pension fund, how many fans will have to

attend in order for the Reunitis to receive $ 60,000? 4.What is dollar level of total revenue must be attained in

order to make net profit (after tax 40%) equal to 10% of total revenue.

5.If Reunitis wanted to generate a profit of $ 1 per

customer, how many customer visit must it have?

Additional Problems (CVP)

Chapter 6 Problem 3

The Leaded Bottoms Company manufactures kewpie dollar for carnivals and sells them for $2 per kewpie. The variable costs of manufacturing and selling are $1.00 and $0.25 per kewpie, respectively. The fixed costs are based upon the following range of activity:

Range of Activity Fixed Costs

0-40,000 kewpies $35,000

40,001-75,000 kewpies 50,000

75,001-125,000 kewpies (maximum capacity)

70,000

During 1998 Leaded Bottoms produced and sold

45,000 kewpies.

Required:

1.Determine the net income for Leaded Bottoms for

1998.

2.How many additional units (above the 45,000) would

Leaded Bottoms need to sell in order to break even

if the additional units will be sold for only $1.90?

3.Answer part 2 again but assume that the company

wishes to generate a profit of $60,000.

4.What is the maximum profit that could be earned by

Leaded Bottoms (disregard parts 2 and 3)?

5.Leaded Bottoms wanted to produce and sell 85,000

units but did not want to incur any additional fixed

costs. The company production supervisor decided

to pay double time for labor in order to produce the

10,000 kewpies above the second range of activity.

If the labor costs are three-fourths of the variable

manufacturing costs, determine the profit that the

company should earn.

Chapter 6 Problem 4

Metal box Company has manufactured a special type of container called “Protector “. The company‘s maximum production capacity per year is 50,000 units and the revenue and cost data ( for one year ) of the product for the last year of the second millennium is given below:

Sales revenue (50,000) $3,000,000

Variable expenses 2,250,000

Fixed expenses 660,000

There is no beginning or ending inventory of the product. The company is anxious to improve the profit performance by improving sales and quality of the product in the forthcoming year, thus it would like the results of the following items:

https://www.doczj.com/doc/5f6498972.html,pute break-even point in both units and sales

dollars

https://www.doczj.com/doc/5f6498972.html,pute the Company’s :

a.contribution margin ratio

b.margin of safety in both dollars and units

c.degree of operating leverage at the present

level of sales.

Chapter 6 Problem 5

Ucom Company manufactures and sells a telephone

answering machine. The company’s income statement for

the most recent year is given below:

Sales (20,000 units) $2,400,000

Less Total expenses:

Direct materials used $900,000

Direct labor 700,000

Manufacturing overhead:

Variable expense $100,000

Fixed expense 110,000 210,000

Sales commission 60,000

Administrative salaries 120,000

Sales salaries 130,000

Depreciation expense 100,000

Royalties (of which $20,000 is fixed) 60,000 2,280,000

Net operating income $ 120,000

Management is anxious to improve the company’s profit performance and has asked for the following information. Required: (show all computations)

https://www.doczj.com/doc/5f6498972.html,pute the company’s:

a.Contribution margin ratio and variable cost ratio

b.Breakeven point in both units and sales dollar

c.Margin of safety in both dollar and percentage form

d.Degree of operating leverage at present level of

sales

2.Refer to original data; assume that next year,

management wants the company to earn a minimum

profit of $90,000. How many units will have to be sold to

meet this target profit?

3.Assume that through a more intense effort by the sales

staff, the company’s sales increases by 10% next year.

By using only t he “degree of operating leverage”,

compute the expected net operating income for next year (Do NOT prepare an income statement).

4.Refer to original data; in an effort to increase sales and

profits, management is considering the use of higher-

quality speaker in the answering machine. The higher-quality speaker would increase direct material costs by $6 per year but fixed cost will reduce by 60,000. The

sales manager estimates that the higher-quality speaker would increase annual sales by 20%. Assuming that

changes are made as described above:

a.What is the yearly breakeven-point in both units and

sales dollar?

b.How many telephone answering machines should

be sold to earn the same net operating income as

the current year?

Chapter 6 Problem 6

Thai Sealant Company manufactures a water sealant at Patumthani plant. The sealant

is used to stop leaks in basement or in concrete to retain walls. In 2006, the company sold 1,600,000 gallon of sealant at a price of $3.00 per gallon with variable production cost per gallon of $1.50. Fixed manufacturing cost for the year was $1,550,000.

In 2007, new automated equipment will be used in production. This will increase fixed manufacturing cost for the year to $1,785,000 while variable production cost has been estimated at 1.3 per gallon.

The sealant division estimates that sales volume can be increase by 12.5% in 2007. The board of director asks you to determine what effect these changes will have on the company’s profit.

Required

1 Prepare a contribution margin income statement for both 2006 and 2007.

2 For 2006, compute the break-even point in gallons and in revenues.

3 For 2007, compute the break-even point in gallons and in revenues.

4 Using the cost and revenue data of 2006, consider each of the following

situations independently. Show all necessary computations.

a) What would be the effect on the break-even point in gallons if

variable cost decreases from $1.50 per gallon to $1.30 per gallon?

b) What would be the effect on the break-even point in gallons if fixed

cost increases by $235,000?

5 Using 1,800,000 gallons as a base, assume that sales in 2007 can be increased

further to 1,890,000 gallons. Determine the percentage increase in sales volume, and what is the operating leverage for 2007?