1. CPA-00394

On December 30, 1994, Chang Co. sold a machine to Door Co. in exchange for a non-interest-bearing note requiring ten annual payments of $10,000. Door made the first payment on December 30, 1994. The market interest rate for similar notes at date of issuance was 8%. Information on present value factors is as follows:

value

Present

ordinary

of

Present value annuity of

Period of $1 at 8% $1 at 8%

9 0.50 6.25

10 0.46 6.71

In its December 31, 1994, balance sheet, what amount should Chang report as note receivable?

a. $45,000

b. $46,000

c. $62,500

d. $67,100

CPA-00394

Choice "c" is correct. On Dec. 31, 1994, the first payment will have been received with nine more payments to be received. Present value of this ordinary annuity of nine equal payments with a market interest rate of 8% is calculated as $10,000 x 6.25, or $62,500.

Choice "a" is incorrect. The note constitutes an annuity with nine payments since the first payment is made on December 31, 1994.

Choice "b" is incorrect. The note constitutes an annuity with nine payments since the first payment is made on December 31, 1994.

Choice "d" is incorrect. The annuity is for nine periods since the first payment is made on December 31, 1994.

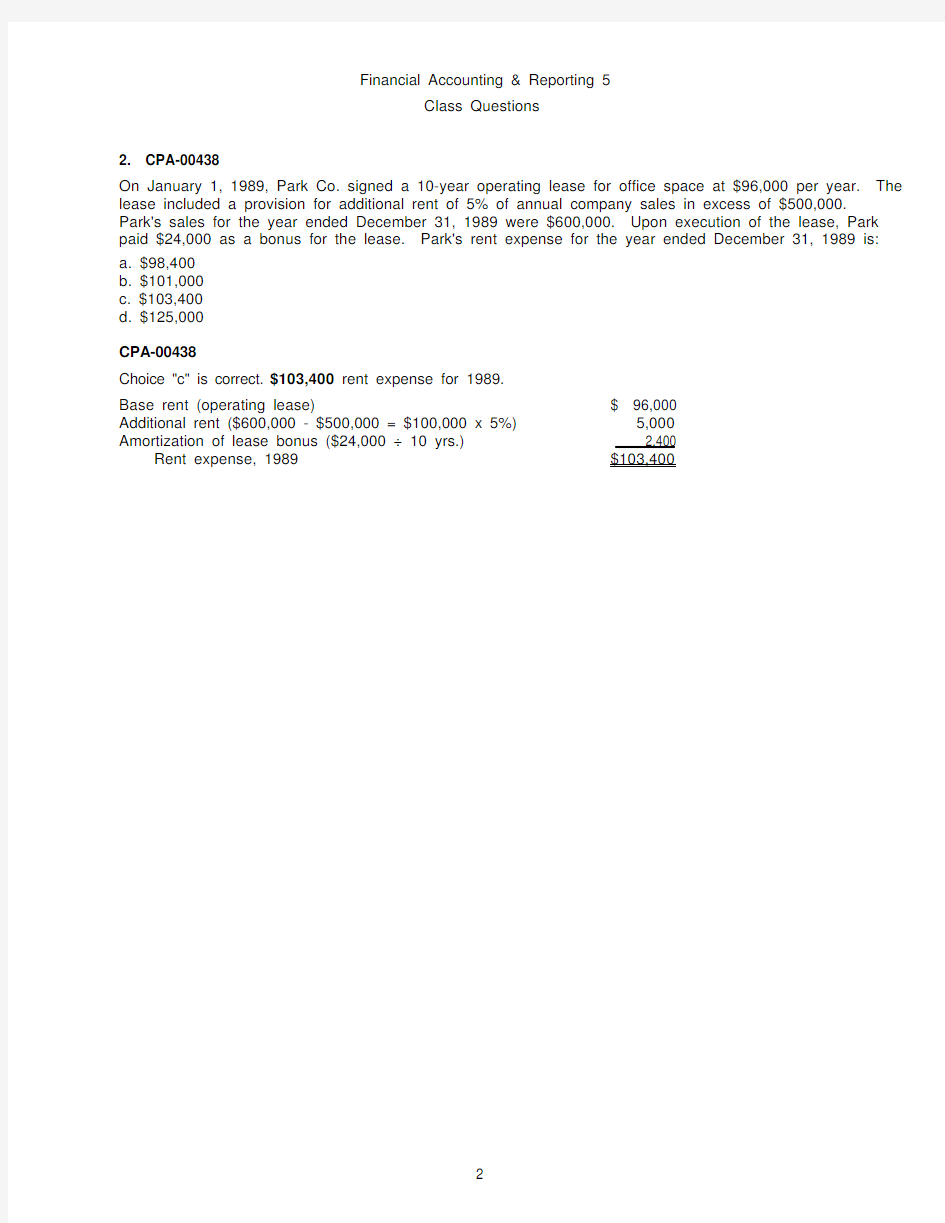

2. CPA-00438

On January 1, 1989, Park Co. signed a 10-year operating lease for office space at $96,000 per year. The lease included a provision for additional rent of 5% of annual company sales in excess of $500,000. Park's sales for the year ended December 31, 1989 were $600,000. Upon execution of the lease, Park paid $24,000 as a bonus for the lease. Park's rent expense for the year ended December 31, 1989 is:

a. $98,400

b. $101,000

c. $103,400

d. $125,000

CPA-00438

Choice "c" is correct. $103,400 rent expense for 1989.

Base rent (operating lease) $ 96,000

Additional rent ($600,000 - $500,000 = $100,000 x 5%) 5,000

Amortization of lease bonus ($24,000 ÷ 10 yrs.) 2,400

Rent expense, 1989 $103,400

3. CPA-00410

Wall Co. leased office premises to Fox, Inc. for a five-year term beginning January 2, 1992. Under the terms of the operating lease, rent for the first year is $8,000 and rent for years 2 through 5 is $12,500 per annum. However, as an inducement to enter the lease, Wall granted Fox the first six months of the lease rent-free. In its December 31, 1992, income statement, what amount should Wall report as rental income?

a. $12,000

b. $11,600

c. $10,800

d. $8,000

CPA-00410

Choice "c" is correct. Rental income is recorded when it is earned (accrual basis), not when the cash is received. Therefore the total rental income should be recognized ratably over the 5 years.

Rent in year 1 (1/2 of $8,000) $ 4,000

Rent in years 2-5 ($12,500 x 4) 50,000

Total rent $ 54,000

1992 Rent (1/5 x $54,000) $ 10,800

Choice "a" is incorrect. Rental income is recorded when it is earned (accrual basis), not when the cash is received. Therefore the total rental income should be recognized ratably over the 5 years.

Choice "b" is incorrect. Only 1/2 of $8,000 is received in 1992.

Choice "d" is incorrect. Rental income is recorded when it is earned (accrual basis), not when the cash is received. Therefore the total rental income should be recognized ratably over the 5 years.

4. CPA-00434

Lease A does not contain a bargain purchase option, but the lease term is equal to 90 percent of the estimated economic life of the leased property. Lease B does not transfer ownership of the property to the lessee by the end of the lease term, but the lease term is equal to 75 percent of the estimated economic life of the leased property. How should the lessee classify these leases?

Lease A Lease B

a. Operating lease Capital lease

b. Operating lease Operating lease

c. Capital lease Capital lease

d. Capital lease Operating lease

CPA-00434

Choice "c" is correct. Both leases have terms equal to or more than 75% of their estimated economic life: therefore, both are capital leases.

Rule: if any one of the following conditions is met, a lease is considered a capital lease and is treated as if owned by the lessee:

1. The lease transfers ownership to the lessee by the end of the lease term.

2. The lease contains a bargain purchase option.

3. The present value at the beginning of the lease term of the "minimum lease payments" equals or

exceeds 90% of the fair market value of the lease Property.

4. The lease term is 75% or more of the estimated economic life of the leased property.

Choice "a" is incorrect. Lease "a" is a capital lease.

Choice "b" is incorrect. Both leases "a" and "b" are capital leases.

Choice "d" is incorrect. Lease "b" is a capital lease.

5. CPA-00424

On December 31, 1990, Day Co. leased a new machine from Parr with the following pertinent information:

Lease term 6 years

Annual rental payable at beginning of each year $50,000

Useful life of machine 8 years

Day's incremental borrowing rate 15%

Implicit interest rate in lease (known by Day) 12%

Present value of an annuity of 1 in advance for 6 periods at 12% 4.61

Present value of an annuity of 1 in advance for 6 periods at 15 % 4.35

The lease is not renewable, and the machine reverts to Parr at the termination of the lease. The cost of the machine on Parr's accounting records is $375,500. At the beginning of the lease term, Day should record a lease liability of:

a. $375,500

b. $230,500

c. $217,500

d. $0

CPA-00424

Choice "b" is correct. $230,500 lease liability at 12-31-90.

Rule: a lease is a capital lease if its term is 75% or more of the life of the leased property. The rate to use to calculate present value is the lessor's "implicit rate" if known by the lessee and if it is lower than the lessee's incremental borrowing rate.

Lease term 6 yr = 75% and is a capital lease

Life of machine 8 yr

Lease payment x PV factor at 12% = PV of lease

$50,000 x 4.61 = $230,500 B

6. CPA-00411

On January 2, 1992, Nori Mining Co. (lessee) entered into a 5-year lease for drilling equipment. Nori accounted for the acquisition as a capital lease for $240,000, which includes a $10,000 bargain purchase option. At the end of the lease, Nori expects to exercise the bargain purchase option. Nori estimates that the equipment's fair value will be $20,000 at the end of its 8-year life. Nori regularly uses straight-line depreciation on similar equipment. For the year ended December 31, 1992, what amount should Nori recognize as depreciation expense on the leased asset?

a. $48,000

b. $46,000

c. $30,000

d. $27,500

CPA-00411

Choice "d" is correct. When a lease is capitalized because of transfer of title or bargain purchase, depreciation is based on the life of the asset, not the lease. The cost includes the bargain purchase price. Depreciation cannot be taken below the salvage value. Depreciation is:

($240,000 - 20,000) / 8 years = $27,500

SFAS 13 para. 10, 13

Choice "a" is incorrect. The life of the asset is used when the asset is capitalized because of bargain purchase. Salvage value must also be considered.

Choice "b" is incorrect. The life of the asset is used when the asset is capitalized because of bargain purchase.

Choice "c" is incorrect. Depreciation is computed on cost less salvage of $20,000.

7. CPA-00397

On January 2, 1995, Marx Co. as lessee signed a five-year noncancelable equipment lease with annual payments of $200,000 beginning December 31, 1995. Marx treated this transaction as a capital lease. The five lease payments have a present value of $758,000 at January 2, 1995, based on interest of 10%. What amount should Marx report as interest expense for the year ended December 31, 1995?

a. $0

b. $48,400

c. $55,800

d. $75,800

CPA-00397

Choice "d" is correct. The lease term began January 2, 1995 on a lease valued at $758,000. The first payment of $200,000 was made on December 31, 1995. Since the interest rate is 10% and one year has expired, Marx Co.'s interest expense is computed as 10% of $758,000 or $75,800. The remainder of the $200,000 payment reduces the obligation under the lease. SFAS 13

Choice "a" is incorrect. If the first payment had been made on January 2, the amount of interest would have been $0 because none of the lease term had elapsed. Interest accrued between January 2 and December 31, which Marx must account for.

Choice "b" is incorrect. Marx will pay 5 x $200,000 or 1,000,000 over the life of the lease or $1,000,000 - $758,000 = $242,000 total interest over the lease term. Simple interest for each of the five years would be $242,000 / 5 or $48,400. However, lease interest expense is computed using the interest method. Choice "c" is incorrect. If the first payment had been made on January 2, the amount of interest would have been $0 because none of the lease term had elapsed, and the lease obligation would have been reduced by the $200,000 of the payment leaving an obligation of $558,000. Under these circumstances the interest expense accrued between January 2 and December 31, which Marx must account for would be 10% of the reduced amount or $55,800.

8. CPA-00439

Peg Co. leased equipment from Howe Corp. on July 1, 1988 for an eight-year period expiring June 30, 1996. Equal payments under the lease are $600,000 and are due on July 1 of each year. The first payment was made on July 1, 1988. The rate of interest contemplated by Peg and Howe is 10%. The cash selling price of the equipment is $3,520,000, and the cost of the equipment on Howe's accounting records is $2,800,000. The lease is appropriately recorded as a sales-type lease. What is the amount of profit on the sale and interest revenue that Howe should record for the year ended December 31, 1988? Profit

on Interest

Sale Revenue

a. $720,000 $176,000

b. $720,000 $146,000

c. $45,000 $176,000

d. $45,000 $146,000

CPA-00439

Choice "b" is correct. $720,000 profit on sale and $146,000 interest revenue.

Rule: in a sales-type lease, any difference between the fair value of the leased asset and its carrying value is recognized as manufacturer's or dealer's profit:

Cash selling price of equipment $ 3,520,000

Less cost of equipment (2,800,000)

Profit recognized on sale $ 720,000

Rule: unearned interest revenue in a sales-type lease is amortized over the period of the lease using the interest method:

PV at inception of the lease at 7/1/88 $3,520,000

Less initial payment 7/1/88 (600,000)

Balance during first year $2,920,000

Interest rate x 10%

Interest revenue 7/1/88 to 6/30/89 (12 mos) $ 292,000

Adjust from full year to half year x ? yr

Interest revenue for YE 12/31/88 $ 146,000

9. CPA-00417

The following information pertains to a sale and leaseback of equipment by Mega Co. on December 31, 1991:

Sales price $400,000

Carrying amount $300,000

Monthly lease payment $ 3,250

Present value of lease payments $ 36,900

Estimated remaining life 25 years

Lease term 1 year

Implicit rate 12%

What amount of deferred gain on the sale should Mega report at December 31, 1991?

a. $0

b. $36,900

c. $63,100

d. $100,000

CPA-00417

Choice "a" is correct.$0 deferred gain in the 12/31/91 BS.

Rule: in a sale/leaseback where the seller-lessee retains more than a minor part, but less than substantially all of the property through the leaseback and realizes a profit in excess of the PV of minimum lease payments, the "excess portion" of the profit should be recognized immediately and the balance should be deferred.

In cases (like this one) where the seller-lessee retains only a minor portion (PV of leaseback is 10% or less of FMV of the asset sold), any gain should be recognized immediately and none deferred.

10. CPA-00458

The market price of a bond issued at a premium is equal to the present value of its principal amount:

a. Only, at the stated interest rate.

b. And the present value of all future interest payments, at the stated interest rate.

c. Only, at the market (effective) interest rate.

d. And the present value of all future interest payments, at the market (effective) interest rat

e.

CPA-00458

Choice "d" is correct. To determine the market price of a bond, the present value of the principal is added to the present value of all interest payments, using the market interest rate.

Choice "a" is incorrect. The stated interest rate is used to calculate the amount of interest payment, but not the market price of the bond.

Choice "b" is incorrect. The stated interest rate is used to calculate the amount of interest payment, but not the market price of the bond.

Choice "c" is incorrect. The market interest rate is used in calculating the price of the bond; however, all the interest payments must also be taken into consideration.

11. CPA-00460

On December 1, 1995, Money Co. gave Home Co. a $200,000, 11% loan. Money paid proceeds of

$194,000 after the deduction of a $6,000 nonrefundable loan origination fee. Principal and interest are

due in 60 monthly installments of $4,310, beginning January 1, 1996. The repayments yield an effective

interest rate of 11% at a present value of $200,000 and 12.4% at a present value of $194,000. What

amount of income from this loan should Money report in its 1995 income statement?

a. $0

b. $1,833

c. $2,005

d. $7,833

CPA-00460

Rule: Loan origination fees shall be deferred and recognized over the life of the loan as an adjustment of

interest income (similar to the treatment of bond discount amortization).

Choice "c" is correct. $2,005 income from this loan in 1995.

Face amount of loan $200,000

Nonrefundable loan origination fee (6,000)

Net amount loaned 194,000

Effective interest rate (yield) 12.4%

24,056 Outstanding one month (12/1/95 - 12/31/95) x 1/12

Interest income for 1995 $ 2,005

12. CPA-00470

On January 2, 1994, West Co. issued 9% bonds in the amount of $500,000, which mature on January 2, 2004. The bonds were issued for $469,500 to yield 10%. Interest is payable annually on December 31. West uses the interest method of amortizing bond discount. In its June 30, 1994, balance sheet, what amount should West report as bonds payable?

a. $469,500

b. $470,475

c. $471,025

d. $500,000

CPA-00470

Choice "b" is correct.

I/S B/S $469,500

$469,500 $500,000

10% x 9%

x

$ 46,950 - $ 45,000 = $1,950 x ? yr = 975

$470,475

Choice "a" is incorrect. Amortization of the bond discount should be recorded.

Choice "c" is incorrect. The interest method should be used.

Choice "d" is incorrect. The reported valuation of the bond payable is the face value less any unamortized bond discount.

13. CPA-00463

On July 1, 1994, Eagle Corp. issued 600 of its 10%, $1,000 bonds at 99 plus accrued interest. The bonds are dated April 1, 1994 and mature on April 1, 2004. Interest is payable semiannually on April 1 and October 1. What amount did Eagle receive from the bond issuance?

a. $579,000

b. $594,000

c. $600,000

d. $609,000

CPA-00463

Choice "d" is correct. The cash collected equals:

Face: 600 x $1,000 $600,000

Issue at: 99%

Bond issue proceeds $594,000

Face $600,000

10%

x

Coupon

Annual interest 60,000

% Year 3/12

Accrued interest $ 15,000

Total cash proceeds $609,000

Choice "a" is incorrect. Accrued interest should be added rather than subtracted.

Choice "b" is incorrect. Accrued interest collected should be included.

Choice "c" is incorrect. The face value does not equal the issuance price. Accrued interest collected should be included.

14. CPA-00477

On January 31, 1992, Beau Corp. issued $300,000 maturity value, 12% bonds for $300,000 cash. The bonds are dated December 31, 1991, and mature on December 31, 2001. Interest will be paid semiannually on June 30 and December 31. What amount of accrued interest payable should Beau report in its September 30, 1992, balance sheet?

a. $27,000

b. $24,000

c. $18,000

d. $9,000

CPA-00477

Choice "d" is correct. Accrued interest payable on September 30, 1992 is the interest owed since the June 30, 1992 payment.

$300,000 x 12% x 3/12 = $9,000

Choice "a" is incorrect. The accrued interest payable on September 30 is only the amount since the June 30 payment. The $27,000 is the interest expense through September 30 (from January 1).

Choice "b" is incorrect. The accrued interest payable on September 30 is only the amount since the June 30 payment. The $24,000 is the interest expense from date of issue (January 31) to September 30. Choice "c" is incorrect. The $18,000 is the interest paid to date in 1992, but the question is interest payable at September 30.

15. CPA-00493

On March 31, 1992, Ashley, Inc.'s bondholders exchanged their convertible bonds for common stock. The carrying amount of these bonds on Ashley's books was less than the market value but greater than the par value of the common stock issued. If Ashley used the book value method of accounting for the conversion, which of the following statements correctly states an effect of this conversion?

a. Stockholders' equity is increased.

b. Additional paid-in capital is decreased.

c. Retained earnings is increase

d.

d. An extraordinary loss is recognized.

CPA-00493

Choice "a" is correct. Under the book value method of exchanging convertible bonds for stock, the book value of the bonds is reallocated to the par value and the additional paid-in capital accounts of the common stock. Thus, stockholders' equity is increased.

Choice "b" is incorrect. Converting bonds to common stock either has no effect on additional paid-in capital (if the bonds' book value equaled the common stocks' par value) or increases additional paid-in capital.

Choice "c" is incorrect. Only the bond accounts and the common stock accounts are affected under the book value method of exchanging convertible bonds for common stock.

Choice "d" is incorrect. No gain or loss is recognized under the book value method.

16. CPA-00473

On December 31, 1993, Moss Co. issued $1,000,000 of 11% bonds at 109. Each $1,000 bond was issued with 50 detachable stock warrants, each of which entitled the bondholder to purchase one share of $5 par common stock for $25. Immediately after issuance, the market value of each warrant was $4. On December 31, 1993, what amount should Moss record as discount or premium on issuance of bonds?

a. $40,000 premium.

b. $90,000 premium.

c. $110,000 discount.

d. $200,000 discount.

CPA-00473

Choice "c" is correct.

1 DR: Cash $1,090,000

4 DR:Discount on bond 110,000

payable $1,000,000

2 CR:Bond

3 CR:APIC--Warrants 200,000

17. CPA-00476

On March 1, 1987, Somar Co. issued 20-year bonds at a discount. By September 1, 1992, the bonds were quoted at 106 when Somar exercised its right to retire the bonds at 105. The amount is material and considered to be unusual in nature and infrequently occurring with respect to Somar Co. How should Somar report the bond retirement on its 1992 income statement?

a. A gain in continuing operations.

b. A loss in continuing operations.

c. An extraordinary gain.

d. An extraordinary loss.

CPA-00476

Choice "d" is correct. The settlement price is greater than the face value of the debt and the face value is greater than the book value. Therefore, the settlement price is greater than the book value and a loss would be recognized on the transaction. This loss would be classified as "extraordinary" because it meets the criteria of APBO No. 30. APB 26 para. 20, SFAS 4 para. 8

18. CPA-00471

On July 31, 1993, Dome Co. issued $1,000,000 of 10%, 15-year bonds at par and (as a typical risk-management strategy to Dome Co.) used a portion of the proceeds to call its 600 outstanding 11%, $1,000 face value bonds, due on July 31, 2003, at 102. On that date, unamortized bond premium relating to the 11% bonds was $65,000. In its 1993 income statement, what amount should Dome report as gain or loss from retirement of bonds?

a. $53,000 gain.

b. $0

c. $(65,000) loss.

d. $(77,000) loss.

CPA-00471

Choice "a" is correct. A gain of $53,000 is recognized because the $665,000 book value of the debt ($600,000 face value plus $65,000 unamortized premium) is settled for $612,000 ($600,000 at 102). There is no accrued interest because the redemption takes place on an interest date. The proceeds from the new bond issuance are not relevant. Note that the gain is reported as part of continuing operations because the transaction is a typical risk-management strategy of the company.

Choice "b" is incorrect. The retirement price does not equal the book value, so a gain or loss must be recognized.

Choice "c" is incorrect. Gain or loss is not determined solely by the amount of unamortized premium. Choice "d" is incorrect. The combination of the unamortized premium plus the excess of the retirement price over the bond face value is not relevant.

19. CPA-00532

The following information pertains to the transfer of real estate pursuant to a troubled debt restructuring (considered to be an extraordinary event for Knob Co.) by Knob Co. to Mene Corp. in full liquidation of Knob's liability to Mene:

Carrying amount of liability liquidated $150,000

Carrying amount of real estate transferred 100,000

Fair value of real estate transferred 90,000

What amount should Knob report as ordinary gain (loss) on transfer of real estate?

a. ($10,000)

b. $0

c. $50,000

d. $60,000

CPA-00532

Choice "a" is correct. When assets are transferred in a troubled debt restructuring, the asset (real estate) is adjusted to fair value and an ordinary gain or loss is recorded.

Carrying amount $100,000

Fair value of real estate (90,000)

Ordinary loss $ 10,000

SFAS 15 para. 13

Choice "b" is incorrect. When assets are transferred in a troubled debt restructuring, the asset (real estate) is adjusted to fair value and an ordinary gain or loss is recorded.

Choice "c" is incorrect. When assets are transferred in a troubled debt restructuring, the asset (real estate) is adjusted to fair value and an ordinary gain or loss is recorded.

Choice "d" is incorrect. The $60,000 is the gain on the restructuring of the payable, not the gain on the transfer of real estate.

20. CPA-00528

The following information pertains to the transfer of real estate pursuant to a troubled debt restructuring (considered to be an extraordinary event for Knob Co.) by Knob Co. to Mene Corp. in full liquidation of

Knob's liability to Mene:

Carrying amount of liability liquidated $150,000

Carrying amount of real estate transferred 100,000

Fair value of real estate transferred 90,000

What amount should Knob report as a pretax extraordinary gain (loss) on restructuring of payables?

a. ($10,000)

b. $0

c. $50,000

d. $60,000

CPA-00528

Choice "d" is correct. When assets are transferred in a troubled debt restructuring, the asset (real estate)

is adjusted to fair value and an ordinary gain or loss recorded. Then, the gain or loss on restructuring is recorded as the difference between the debt and fair value of asset transferred. This gain or loss is

considered extraordinary if the related event meets the criteria of APBO No. 30 to be treated as an extraordinary item (SFAS No. 145). Otherwise, it is an ordinary gain. In this case, the gain on

restructuring is considered extraordinary and is calculated as follows:

Liability $150,000 Fair value of real estate (90,000)

Gain $ 60,000

SFAS 15 para. 13

Choice "a" is incorrect. The $10,000 is the loss on the adjustment of real estate to fair value, not the restructuring loss.

Choice "b" is incorrect. The restructuring gain or loss is the difference between the liability and the

asset's fair value and is extraordinary in this case.

Choice "c" is incorrect. The restructuring gain or loss is the difference between the liability and the

asset's fair value.

第一部分Concept HDL第二部分Allegro 菜单栏 文件、编辑、察看、器件、连线、文本、模块、组、显示、PSpice、工具、窗口、帮助1.文件菜单 原菜单中文菜单说明 新建 打开 关闭 保存 另存为 保存所有 保存层 转换 恢复 移动 编辑页和符号下一层菜单见下表 编辑层同上 返回 改变组件设置启动的工具 察看搜索栈 物理输出进行封装并输出 物理输入从Allegro导入 IFF输入导入IFF文件 打印设置 打印预览 打印输出可输出原理图 退出 注:若菜单中的说明项为空,则表示不不需要说明或说明项与中文菜单相似。以下相 下一页 前一页 转向 加入新页 下一层 上一层

撤销 重做 移动 复制 复制所有 重复复制 排列 删除 颜色 分割 镜像 翻转 旋转 模块顺序 画弧 画圆 3.察看菜单 放大矩形范围 放大到满屏 放大 缩小 按比例放大 上移 下移 左移 右移 预览 网格设定 状态条 错误信息条 控制窗口 数据栏 工具栏

添加器件 替换器件 改变版本可改变器件符号的显示类 型 修改 部分可设置器件在封装中的位 置 交换针脚 删除 5.连线菜单 连线需要从一点画到另一点 连线点击两点自动连线 添加信号名 添加总线名 连结总线 设定总线参数 画点 连线加粗 连线减细 设置连线的图案 6.文本菜单 特性设置 习惯设置 器件赋值可对电阻电容等进行赋值 理性文本 设置端点的名称 添加注释 打开文本文档 设置字体大小 放大 缩小 交换 重新连结 特性显示下一层菜单如下

显示名称 显示值 两样都显示 不可见 7.模块菜单 添加 重命名 扩展 连线 连线 添加针脚 重命名针 删除针脚 移动针脚 输入针脚 输出针脚 双向针脚 8.组菜单 创建组下一层菜单在下表 设定当前组 显示组的内容 移动 复制 复制全部 设置复制个数 设置文字大小 改变注释 删除 设定颜色 激活 器件 特性显示 矩形框内创建为一组 多边形框内创建为一组 用表达式创建 下一个

人教版新目标八年级英语初二英语上册课文翻译【全册】 一单元 SECTION A 图片周末你通常做什么?我经常去看电影。 1c她在周末做什么?她经常去看电影。 2a你多久看一次电视?每周两次。 2c 你多久看一次电视?我每天看电视。你最喜欢什么节目?《动物世界》。你多久看一次? Grammar Focus 你周末通常做什么?我通常踢足球。他们周末做什么?他们经常去看电影。他周末做什么?他有时看电视。你多久购物一次?我每月购物一次。程多久看一次电视?他每周看两次电视。 3格林中学学生做什么?大多数学生每周锻炼三或四次。一些学生每周锻炼一两次。一些学生非常活跃,每天都锻炼。至于家庭作业,大多数学生每天都做家庭作业。一些学生每周做三或四次家庭作业。没有学生每周做一两次作业。关于“看电视”的结果很有趣。一些学生每周看一两次电视,一些学生每周看三或四次电视。但大多数学生每天都看电视。 4谁是最好的英语学生?你能做什么来提高你的英语水平?你多久读一次英语书?我每周读两次英语书。 SECTION B 1a垃圾食品牛奶水果蔬菜睡觉咖啡 1b刘芳,你多久喝一次牛奶?我每天喝牛奶。你喜欢牛奶吗?不喜欢,但我妈妈想让我喝。她说牛奶对我的健康有益。 2c你多长时间运动一次?我每天都运动。你多长时间……一次? 3a……但是我非常健康。我每天都锻炼,通常是在我放学回家的时候,我的饮食习惯非常好。我尽量多吃蔬菜。我每天都吃水果,每天都喝牛奶。我从不喝咖啡。当然了,我也喜欢垃圾食品,我每周吃二或三次。噢,还有,我每天晚上都睡九个小时。所以你看,我爱惜我身体。我的健康的生活方式帮助我取得了好的成绩。好的食品加上运动帮助我更好地学习。 3b我认为我有点不健康。我几乎不锻炼。我每周吃两次蔬菜,但我从不吃水果。并且我不喜欢喝牛奶。啐!我喜欢垃圾食品,每周吃三到四次。我也喜欢喝咖啡。因此或许我不是很健康,尽管我拥有一个健康的习惯。我每天晚上都睡九个小时。 4 你多久吃一次蔬菜?你做什么运动?玛丽亚每天锻炼。她喜欢玩…… SELF CHECK 1妈妈想让我六点起床跟她一起打乒乓球。爷爷十分健康因为他每天都锻炼。大量的蔬菜帮助你保持健康。你必须得尽量少吃肉。你有健康的生活方式吗? Just for fun你健康吗?噢,我很健康。你最喜欢的运动是什么?我喜欢打篮球。哇! 二单元 SECTION A 图片怎么了?我感冒了。怎么了?我胃痛。我背痛。 1c怎么啦?我喉咙痛。 2a 1.发烧—d.多喝水2.喉咙痛—b.加蜂蜜的热茶 3.胃痛—a.躺下休息 4.牙痛——c.看牙医 2c怎么了?我牙痛。也许你应该去看牙医。好主意。 Grammar Focus 我头痛。你应当上床睡觉。我胃痛。他不应当吃东西。她牙痛。她应当看牙医。 3a怎么啦?我觉得不舒服。我感冒了。什么时候开始的?大约两天前。噢,那太糟糕了。你应当休息一下。是的,我也是这样想的。我希望你快点好起来。 4怎么啦?你喉咙痛吗?不,我不痛。你头痛吗?是的,我头痛。你应当躺下来休息一下。 SECTION B 1a疲乏的;劳累的饥饿的口渴的紧张的;有压力的1b吃个苹果。早点上床睡觉。喝些水。听音乐 2c吉娜怎么啦?她累了。噢,她应当早点上床睡觉。她不应该去参加聚会。 3a健康的生活方式,中国方式 传统中医认为我们需要阴阳食品的平衡以保持健康。例如,你经常没有力气并感到疲倦吗?这或许是因为你吃了太多的阴性食品,你应当吃含阳性较高的食品,像牛肉。吃党参和黄芪草对这方面也是有好处的。但那些太紧张和易怒的人也许吃了太多的阳性食品,中医认为他们应当多吃阴性食品,像豆腐。现在中药在很多西方国家很受欢迎。拥有一个健康的生活方式很容易,均衡饮食很重要。 3b每个人都会不时地感到疲倦。当你疲倦时,你不应当晚上外出。你应当几个晚上早儿上床睡觉,并且你应该锻炼以保持健康,你也应吃水果和其他健康的食品。你不应当在你感到疲倦时学习。

第八章Allegro PCB设计 本章主要讲解如何使用Cadence公司的PCB Editor软件来进行印制电路板(PCB)的设计。由于前面已经讲述了焊盘以及PCB封装的制作,本章主要讲解如何创建PCB外形框图符号、PCB Editor的使用、PCB设计的规则设置以及PCB设计的布局、布线等几个方面。 对于一个项目的设计,如果把原理图的设计看作设计的前端,那么PCB设计就是这个项目的后端,PCB设计是由原理图设计来约束、决定的,一个项目的PCB设计是从原理图输出到PCB设计环境开始的。 一、PCB Editor软件介绍 1、PCB Editor软件的打开 在前面的学习过程当中,我们一直是从项目界面中点击“Layout”按钮来启动PCB Editor软件,另一种方法就是直接启动“开始菜单/程序/Allegro SPB 15.5.1/PCB Editor”。 2、Allegro界面 Allegro是Cadence公司的PCB设计工具,提供了一个完整、易操作的PCB 设计环境,其用户界面包括、标题栏、菜单栏、工具栏、编辑窗口、控制面板、状态栏、命令栏及视窗栏组成,如图8_1所示。 8_1

下面详细介绍一下各栏: 1)标题栏 标题栏是显示当前打开的界面的位置及所选的模块信息。 2)菜单栏 Allegro的菜单栏共由File(文件类)、Edit(编辑类)、View(查看类)、Add (添加类)、Display(显示类)、Setup(设置类)、Shape(敷铜类)、Logic(逻辑类)、Place(布局类)、Route(布线类)、Analyze(分析类)、Manufacture(制造类)、Tools(工具类)以及Help(在线帮助)等14个下拉菜单组成。 (1)File 文件类的下拉菜单中的命令主要包括:新建、打开、查看最近的设计及保存文件,输入、输出一些文件信息,查看一些临时文件,打印设置、打印预览、打印、设定文件属性、更改产品模块,录制scr文件及退出命令。 (2)Edit 编辑栏的下拉菜单中主要包括:移动、复制、镜像、选装、更改、删除、敷铜(Z-copy)、负片层处理、调整线、编辑字符、编辑组、编辑属性、编辑网名的属性、前进及返回上一步命令。 (3)View 查看栏的下拉菜单主要是有关界面的操作,如放大显示、缩小、适中显示、颜色的设置、更新及用户自定义界面等命令。 (4)Add 添加栏的下拉菜单主要包括:添加一条线、添加一个圆弧、添加一个圆、添加矩形、添加字符等命令。 (5)Display 显示栏的下拉菜单中包括:各条目颜色的设置、查看信息、测量、查看各属性、高亮显示、取消高亮显示、显示特定的飞线、不显示飞线等命令。 (6)Setup 设置栏的下拉菜单主要是对Allegro的属性进行设置,如制图参数设置、制图状态设置、字号的设置、设置子层、设置叠层结构及材料、设置过孔、设置规则、定义属性、定义列表、设置特定的区域、设置边框及用户自定义的设置等命令。 (7)Shape 敷铜栏的下拉菜单主要是有关正片敷铜的一些命令,这里的敷铜不仅仅是信号层的敷铜,也包括一些区域和禁止布线区域等。此下拉菜单主要包括:敷铜、选中一个敷铜或避让、手动避让、编辑敷铜的边界、删除孤立的铜、改变敷铜的类型、合并敷铜、检查及动态敷铜的设置等。 (8)Logic 逻辑栏的下拉菜单主要是有关逻辑类的操作,如更改网名、定义网络拓扑、定义差分对、定义直流变量、更改位号、定义分部分、终端分配等命令。 (9)Place 布局栏的下拉菜单基本上都是与布局相关的操作,如手动添加元件、自动添加元件、自动布局、调整引脚映射、更新库、更新设置文件等。 (10)Route

Unit 1 Where did you go on vacation? Section A 1 (1a-2d) 一、教学目标: 1. 语言知识目标: 1) 能掌握以下单词:anyone, anywhere, wonderful, quite a few, most, something, nothing, everyone, of course, myself, yourself 能掌握以下句型: ①—Where did you go on vacation? —I went to the mountains. ②—Where did Tina to on vacation? —She went to the beach. ③—Did you go with anyone? —Yes, I did./No, I didn’t. 2) 能了解以下语法: —复合不定代词someone, anyone, something, anything等的用法。 —yourself, myself等反身代词的用法。 3)一般过去时态的特殊疑问句,一般疑问句及其肯定、否定回答。 2. 情感态度价值观目标: 学会用一般过去时进行信息交流,培养学生的环保意识,热爱大自然。 二、教学重难点 1. 教学重点: 1) 用所学的功能语言交流假期去了什么旅行。 2) 掌握本课时出现的新词汇。 2. 教学难点: 1) 复合不定代词someone, anyone, something, anything等的用法。 2) yourself, myself等反身代词的用法。 三、教学过程 Ⅰ. Lead-in 1. 看动画片来进入本课时的主题谈论上周末做了些什么事情,谈论过去发生的事情。 Ⅱ. Presentation 1. Show some pictures on the big screen. Let Ss read the expressions. 2. Focus attention on the picture. Ask: What can you see? Say: Each picture shows something a person did in the past. Name each activity and ask students to repeat: Stayed at home, Went to mountains, went to New York City 6. Went to the beach, visited my uncle, visited museums, went to summer camp 3. Now, please match each phrase with one of the pictures next to the name of the activity,point to the sample answer. 4. Check the answers. Answers: 1. f 2. b 3. g 4. e 5. c 6. a 7. d III. Listening 1. Point to the picture on the screen. Say: Look at the picture A. Where did Tina go on vacation? She went to mountains. Ask: What did the person do in each picture? 2. Play the recording the first time. 3. Play the recording a second time. Say: There are three conversations. The people talk about what did on vacation. Listen to the recording and write numbers of the names in the right boxes of the picture. 4. Check the answers. IV.Pair work 1. Point out the sample conversation. Ask two Ss to read the conversation to the class.

人教版英语八年级上册 Unit3 I’m more outgoing than my sister 教材全解 【教材内容解析】 Section A 1.Both Sam and Tom can play the drums, but Sam plays them better than Tom. (P. 17) both...and...意为“两者都”,并列两个主语时,谓语动词用复数形式。 Both Tom and Jim are interested in Math. 2.Tara works as hard as Tina. (P. 18) as...as...意为“和……一样”,两个as中间用形容词或者副词原级。 He is as tall as his father. I run as fast as he. 【拓展】not as...as...意为“不如……,比不上……”第一个as是副词,在否定句中可以换成so。She doesn't study as/so hard as her brother. Lucy is not as/so easygoing as Lily. 3.Oh, which one was Lisa(P. 18) which表示“哪一个”,表示在一定数量中进行选择;what用于选择范围较大或者不明确时,表示选择人或物的种类。

There are some books in the box. Which one is yours What is in the box 4.You can tell that Lisa really wanted to win, though.(P. 18) (1) win表示“赢得”后接比赛、奖项等表示物的名词作宾语;beat表示“打败”,后接某人、团队等表示人的名词作宾语。 They finally beat the other side and won the basketball match. Who won the first prize in the singing contest. (2)这里的though作副词,表示“可是、然而”,放在句末,前用都好隔开。 Jim said that he would come. He didn’t, though. 5.But the most important thing is to learn something new and have fun.(P. 18) (1)此处动词不定式作表语,放在be动词后面。 My work is to clean the room every day. His dream is to be a teacher. (2)have fun意为“玩得高兴”,后接动名词。 Did you have fun visiting that country Section B 1....is talented in music. (P. 20) talented作形容词,表示“有才能的、有天赋的”,be talented in表示“在……方面有天赋”。Li Yundi is talented in swimming. 2....truly cares about me. (P. 20)

Cadence allegro菜单解释——file 已有320 次阅读2009-8-16 19:17 | 个人分类: | 关键词 :Cadence allegro file 菜单解释 每一款软件几乎都有File 菜单,接下来详细解释一下allegro 与其他软件不同的菜单。 new 新建 PCB文件,点 new 菜单进入对话框后, drawing type 里面包含有 9 个选项, 一般我们如果设计 PCB就选择默认第一个 board 即可。 如果我们要建封装库选 package symbol即可,其他 7 个选项一般很少用,大家可 以理解字面意思就可以知道什么意思了。 open 打开你所要设计的PCB文件,或者封装库文件。 recent designs 打开你所设计的PCB文件,一般是指近期所设计的或者打开过的PCB文件。 save 保存 save as 另存为,重命名。 import import 菜单包含许多项,下面详细解释一下我们经常用到的命令。 logic 导入网表,详细介绍在 allegro 基础教程连载已经有介绍,在此不再详细介 绍。 artwork 导入从其他 PCB文件导出的 .art 的文件。一般很少用词命令。 命令 IPF和 stream 很少用,略。 DXF导入结构要素图或者其他DXF的文件。 导入方法如下: 点import/DXF 后,在弹出的对话框选择,在DXF file里选择你要导入的DXF的路径, DXF units选择 MM ,然后勾选 use default text table 和 incremental addition ,其他默认即可。再点 edit/view layers 弹出对话框,勾选 select all,DXF layer filter 选择 all,即为导入所有层的信息,然后在下面的 class里选择 board geometry,subclass选择 assembly_notes,因为一般导入结构要素图都是导入这一层,然后 点ok,进入了点 import/DXF 后弹出的对话框,然后点 import 即可将结构要素图导入。 IDF IFF Router PCAD这四个命令也很少用,略。 PADS一般建库的时候导入焊盘。 sub-drawing 命令功能非常强大,也是我们在 PCB设计中经常用的命令,如果能 够非常合理的应用 sub-drawing 命令会提高我们设计 PCB的效率。

人教版英语八年级上册 Unit 10 If you go to the party, you'll have a great time! 教材全解 【教材内容解读】 Section A have a great time、(P、73) 1.If you go to the party, you’ll 相当于enjoy oneself或者have fun。 have a great time意为“过得愉快、玩得开心”, They are having a great time in the park、 =They are enjoying themselves in the park、 2、The students are talking about when to have a class party/ a class meeting/a birthday party、(P、74) have a class meeting意为“开班会”。 We will have a class meeting next week、 3、What will Mark organize? (P、74) organize用作及物动词,表示“组织、安排”, 后接表示组织、活动类的名词做宾语,名词形式为organization 表示“组织”。 Last month, we organized a party、 order food from a restaurant、(P、74) 4.、、、let’s order此处表示“订购、点菜”,order sth、from、、、表示“从……订购某物”。 I ordered some chicken from that shop、 表示“命令”时,常用于order sb、(not) to do sth、结构中【拓展】order还可以作及物动词,意为“命令”,

人教版八年级上册英语知识点 Unit 1 Where did you go on vacation?(谈论假期生活,一般过去时) Unit 2 How often do you exercise?(谈论生活习惯,一般现在时) Unit 3 I'm more outgoing than my sister(谈论事物对比,形容词比较级) Unit 4 What's the best movie theater?(谈论事物比较,形容词最高级) Unit5 Do you want to watch a game show?(谈论内心想法,一般现在时) Unit6 I’m going to study computer science.(谈谈生活的目标,一般将来时) Unit7 Will people have robots?(对将来生活的预言,一般将来时) Unit8 How do you make a banana milk shake?(描述进程,祈使句) Unit9 Can you come to my party?(学习邀请,作出、接受和拒绝邀请,学习表请求的句子) Unit10 If you go to the party, you’ll have a great time.(作出决定,学习if的条件状语从句) ①复习一般过去时 ②复合不定代词的用法 ③反身代词的用法 ④系动词的用法 ⑤动词后的to do和doing 的区别 ⑥ed形容词和ing形容词的区别 ⑦“近义词”的区别 ⑧本单元中的主谓一致现象 ⑨动词过去式的构成及不规则动词表 ⑩用同义短语转换同义句时谓语动词形式一致性的培养。 ⑾感叹句的结构和连词的选择。 Unit1 Where did you go on vacation? 单词 anyone ['eniw?n] pron.任何人 anywhere ['eniwe?(r)] adv.任何地方n.任何(一个)地方 wonderful ['w?nd?fl] adj.精彩的;极好的 few [fju?] adj.很少的;n.少量 most [m??st] adj.最多的;大多数的; something ['s?mθ??] pron.某事物; nothing (=not…anything) ['n?θ??] pron.没有什么n.没有 myself [ma?'self] pron.我自己 everyone ['evriw?n] pron.每人;人人 yourself [j??'self] pron.你自己;你亲自 hen [hen] n.母鸡;雌禽 bored [b??d] adj.无聊的;厌烦的;郁闷的 pig n.猪 diary ['da??ri] n.日记;日记簿(keep a diary) seem [si?m] vi.似乎;好像

C a d e n c e a l l e g r o菜单解释——f i l e 已有320次阅读2009-8-1619:17|个人分类:|关键词:Cadenceallegrofile菜单解释每一款软件几乎都有File菜单,接下来详细解释一下allegro与其他软件 不同的菜单。 new 新建PCB文件,点new菜单进入对话框后,drawingtype里面包含有9 个选项,一般我们如果设计PCB就选择默认第一个board即可。 如果我们要建封装库选packagesymbol即可,其他7个选项一般很少用,大家可以理解字面意思就可以知道什么意思了。 open 打开你所要设计的PCB文件,或者封装库文件。 recentdesigns 打开你所设计的PCB文件,一般是指近期所设计的或者打开过的PCB文件。 save 保存 saveas 另存为,重命名。 import import菜单包含许多项,下面详细解释一下我们经常用到的命令。 logic导入网表,详细介绍在allegro基础教程连载已经有介绍,在此不 再详细介绍。

artwork导入从其他PCB文件导出的.art的文件。一般很少用词命令。 命令IPF和stream很少用,略。 DXF导入结构要素图或者其他DXF的文件。 导入方法如下: 点import/DXF后,在弹出的对话框选择,在DXFfile里选择你要导入的DXF的路径,DXFunits选择MM,然后勾选usedefaulttexttable和incrementaladdition,其他默认即可。再点edit/viewlayers弹出对话框, 勾选selectall,DXFlayerfilter选择all,即为导入所有层的信息,然后在 下面的class里选择boardgeometry,subclass选择assembly_notes,因 为一般导入结构要素图都是导入这一层,然后点ok,进入了点 import/DXF后弹出的对话框,然后点import即可将结构要素图导入。IDFIFFRouterPCAD这四个命令也很少用,略。 PADS一般建库的时候导入焊盘。 sub-drawing命令功能非常强大,也是我们在PCB设计中经常用的命令,如果能够非常合理的应用sub-drawing命令会提高我们设计PCB的效率。导入sub-drawing命令一般是将我们所导出sub-drawing的组建导入,包 括线孔等等。例如我们在合作的过程中,将其他人画的线导入你所设计 的PCB中,一般导入和导出的文件都是相同的PCB文件,也就是说板框outline和相对坐标零点时一样的,这样我们无论在导入还是导出的的时

1.平移:按住鼠标滚轮拖动。 2.缩放:滚轮向上放大,滚轮向下缩小;按下滚轮,出现双圈,向左上或右上移动鼠标, 出线矩形框,再按下滚轮,放大到矩形区域;按下滚轮,出现双圈,向下移动鼠标,出线矩形框,再按下滚轮,缩小到矩形区域。 3.光标处定为中心点:按下滚轮,出现双圈,再按下滚轮或左键。 4.层叠结构与特征阻抗设置:Setup—>Cross Section(横截面)或Setup—>Subclasses(子 类)—>Etch(蚀刻);或点工具栏上的图标,三种方法都可以打开。 5.颜色管理:点工具栏上的图标。 6.PLANE用正片还是负片:单打独斗,无专人负责管理封装库的,用正片;团队作战, 有专人管理封装库的,用负片。刘佰川做的库只能用正片。 7.常用快捷键: F2 全屏显示 F9 取消命令,也可右键菜单-》Cancel SF8 高亮(先按shift+F8,然后点需高亮的对象;另一种方法是输入文字SF8回车,然后点需高亮的对象) SF7 取消高亮 SF4 测量间距,也可点工具栏上的图标,测量命令下,右键菜单可选择Snap元素类型 8.过滤:右键菜单-》Super filter 9.看线宽:过滤选Off,点某线段,右键-》show element 10.看焊盘或过孔尺寸:过滤选Off,点某焊盘或过孔,右键-》Modify design padstack-》Single instance 11.过孔定义:Constraint Manager-->Physical -->Physical Constraint Set-->All layers,点 击Vias列的单元格可编辑所需使用的过孔种类。 新增过孔:tools-》padstack-》modify library padstack,选择一种编辑,编辑完了另存一个名字。 12.查找器件:菜单Display—>element 或Display—>Highlight,然后窗口右侧,FIND,find by name选symbol(or pin),按回车键。 13.显示设置:setup-》design parameters-》display-》enhanced display modes上面六个全选 上。另外,在颜色管理里面,display-》global transparency拉到100%,shadow mode 设为on,brightness拉到100%,dim active layer方框选上。 14.看布局:窗口右侧,Visibility-》Views下拉列表选Film:A或Film:B。 如果Visibility-》Views下拉列表里什么都没有怎么办? 点菜单manufacture-》artwork,点OK就有了。 15.正片电源层铺铜技巧:先行用ANTI ETCH将区域画好,然后自动铺铜,铺好后再把 ANTI ETCH删除掉。(另一种说法:先在电源层和地层整体铺一块大铜皮,然后用Anti ETCH, 把这些平面分割开来。因为用的是正片,所以分割好之后需把Anti ETCH删除。)16.为什么右键菜单super filter菜单里没有line、shape等元素? 如下图所示,左上角工具栏有3个绿色的按钮,分别为generaledit、etchedit、

2020年初中英语八年级上册全册精编版

新目标人教版初中英语八年级上册精品教案全册 Love me love my dog!! Wish Love to fill around the world! 教学工作计划 【一】.本学期的指导思想: 1、要面向全体学生,关注每个学生的情感,激发他们学习英语的兴趣,帮助他们建立学习的成就感和自信心,培养创新精神; 2、整体设计目标,体现灵活开放,目标设计以学生技能,语言知识,情感态度,学习策略和文化意识的发展为基础; 3、突出学生主体,尊重个体差异; 4、采用活动途径,倡导体验参与,即采用任务型的教学模式,让学生在老师的指导下通过感知、体验、实践、参与和合作等方式,实现任务的目标,感受成功; 5、注重过程评价,促进学生发展,建立能激励学生学习兴趣和自主学习能力发展的评价体系。 总之,让学生在使用英语中学习英语,让学生成为Good User 而不仅仅是Learner。让英语成为学生学习生活中最实用的工具而非累赘,让他们在使用和学习英语的过程中,体味到轻松和成功的快乐,而不是无尽的担忧和恐惧。 仅供学习与交流,如有侵权请联系网站删除谢谢50

【二】.所教班级学生基本情况分析: 本届八年级学生的英语基础方面还很薄弱,经过上学期我们两位英语老师的不懈努力,年段学生的基础知识得到了加强,学习态度也有所好转。但是学生整体的惰性还是很强,自觉性很差。 另外,学生在情感态度,学习策略方面还存在诸多需要进一步解决的问题。例如:很多学生不能明确学习英语的目的,没有真正认识到学习英语的目的在于交流;有些同学在学习中缺乏小组合作意识;大多数同学没有养成良好的学习习惯,不能做好课前预习课后复习,学习没有计划性和策略性;不善于发现和总结语言规律,不注意知识的巩固和积累。 【三】奋斗目标: 钻研新课标,提高教学水平,真正做到教学相长,努力达到学校规定的教学指标。 【四】具体措施: 1. 每天背诵课文中的对话。目的:要求学生背诵并默写,培养语感。 2. 每天记5个生词,2个常用句子或习语。实施:利用“互测及教师抽查”及时检查,保证效果并坚持下去。 仅供学习与交流,如有侵权请联系网站删除谢谢50

备课本冀教版八年级上册 英语 全册教案 班级______ 教师______ 日期______

Unit 1 Me and My class Lesson1Back to School! Teaching objectives: 1. Graspthemastery vocabulary and phrases. 2.Make the students understand the meaning of the text. 3.Learn something about an e-mail written by English. After learning this lesson,the students can write their own e-mails. Teaching Aims 1.Knowledge goals: Master the vocabulary(physics, recent, ) 2. Ability goals: (1) Useful phrases and structures (one…the other…, make friends, introduce sb. to sb., the same as) (2) Understand the meaning of the text 3. Emotion goals: Learn how to express the first day of a new term Important points: Can use phrases freely to make sentences Difficult points: Master important phrases Teaching method:Speaking, Teaching progress: Classopening:Introduce the topic of this unit. Key steps: Step1. Ask the students to disc uss the question in“Chat Show” What did you do in your summer holiday? Step2.Dictation Dictatethesewords: back, be back, grade, student, pupil, class, have, have lessons /classes, more, cousin, brain Step3. Present new sentences be back/be back home e.g. I am back. T: Ask one student “Which Grade are you in this year?” S: I am in Grade 8 this year. T:How many students are there in your school? S: There are about 900 students in my school. T: How many pupils are there in your class? S: My class has 50 pupils. Then the teacher makes the students do pair works, make sure they can

Cade nceallegro 菜单解释一一file 已有320次阅读2009-8-1619:17 |个人分类:|关键词:Cadenceallegrofile 菜单解释每一款软件几乎都有File菜单,接下来详细解释一下allegro与其他软件不同的菜单。 new 新建PCB文件,点n ew菜单进入对话框后,draw in gtype里面包含有9 个选项,一般我们如果设计PCB就选择默认第一个board即可。 如果我们要建封装库选packagesymbol即可,其他7个选项一般很少用,大家可以理解字面意思就可以知道什么意思了。 ope n 打开你所要设计的PCB文件,或者封装库文件。 rece ntdesig ns 打开你所设计的PCB文件,一般是指近期所设计的或者打开过的PCB文件。 save 保存 saveas 另存为,重命名。 import import菜单包含许多项,下面详细解释一下我们经常用到的命令。 logic导入网表,详细介绍在allegro基础教程连载已经有介绍,在此不再详细介绍。

artwork导入从其他PCB文件导出的.art的文件。一般很少用词命令。 命令IPF和stream很少用,略。 DXF导入结构要素图或者其他DXF的文件。 导入方法如下: 点import/DXF后,在弹出的对话框选择,在DXFfile里选择你要导入的 DXF的路径,DXFunits选择MM,然后勾选usedefaulttexttable 和 in creme ntaladditi on,其他默认即可。再点edit/viewlayers弹出对话框,勾选selectall,DXFlayerfilter选择all,即为导入所有层的信息,然后在下面的class 里选择boardgeometry,subclass选择assembly.notes,因为一般导入结构要素图都是导入这一层,然后点ok,进入了点 import/DXF后弹出的对话框,然后点import即可将结构要素图导入。IDFIFFRouterPCA这四个命令也很少用,略。 PADS —般建库的时候导入焊盘。 sub-drawing命令功能非常强大,也是我们在PCB设计中经常用的命令, 如果能够非常合理的应用sub-drawing命令会提高我们设计PCB的效率。导入sub-drawing命令一般是将我们所导出sub-drawing的组建导入,包括线孔等等。例如我们在合作的过程中,将其他人画的线导入你所设计的PCB中,一般导入和导出的文件都是相同的PCB文件,也就是说板框outline和相对坐标零点时一样的,这样我们无论在导入还是导出的的时候总会输

学期教学计划 一. 指导思想 注重素质教育,强调从学生的学习兴趣、生活经验和认知水平出发,倡导体验、实践、参与、合作与交流的学习方式和任务型的教学途径,发展学生的综合语言运用能力,使语言学习的过程成为学生形成积极的情感态度、主动思维和大胆实践、提高跨文化意识和形成自主学习能力的过程。为学生的充分发展创造条件,为继续学习打下基础。 二. 教材分析 《新目标英语八年级(上)》共有十二个单元,每个单元都分为两个部分:A部分和B部分。新课通过听、说、读、写的全面训练,培养学生全面发展的能力。配以适量练习,及时对所学内容进行复习巩固。 教材突出几个方面: 1.语言功能项目(Functions): Talk about how often you do things; Your health, give advice; Future plans; How to get to places; Make,accept and decline invitations; obligations; Personal traits; compare people; Describe a process; follow instructions; Events in the past; Famous people; Future intentions; Make polite requests; ask for permission; Discuss preferences; make comparisons. 2.语法项目: 形容词和副词的比较级和最高级;动词种类:情态动词can、could、must、have to、should;动词用现在进行时来表示按计划或安排将要进行的动作;用“be going to +动词原形”表示将要发生的事或打算;句子成份、句子的类型、简单句的五种基本句型。 3.教学进度安排 三.学生基本情况分析 四.完成教学任务的主要措施 五.教学方式呵学习方式的大体设想 1.遵循英语教学规律,寓思想教育于语言教学中; 2.精讲多练,着重培养交际运用英语的能力; 3.听、说、读、写全面训练,不同阶段有所侧重; 4.尽量使用英语,适当使用母语; 5.发挥教师的主导作用,采取多种教学方法,充分调动学生的主动性和积极性;

學習了一段時間allegro,你是不是也對SKILL函數有了一定的認識,也收集了不少skill 函數吧,但是不是又對函數的應用感到麻煩和被動。現在就說一下怎樣把函數載入到應用功能表,利用滑鼠點擊輕鬆執行。因為好多人不知道怎麼使用,我也是摸索出來的,供大家參考,獨樂樂,與人樂樂,孰樂?! 1、設定環境變數: 首先建立SKILL和SUTENV(這個檔案名可以隨意起,)兩個資料夾,位置可以隨意放置,不過我是放在了candence資料夾下,這樣感覺比較整齊。然後添加環境變數系統變數和使用者HOME 變數,如下圖。 系統變數 HOME變數 2、設定allegro.ilinit文件: 在SUTENV 檔下建一個PCBENV 資料夾,接著在PCBENV 下面建一個名為allegro尾碼為ilinit的文檔,可以用寫字板或者像UE 程式編譯之類的軟體,設置語法如下setSkillPath(buildString(append1(getSkillPath() "D:/Cadence/SPB_15.7/skill"))); load("xxx.il"); load("xxx.il"); … … … “D:/Cadence/SPB_15.7/skill”就是設定好的SKILL 資料夾的位置,注意“/”而不是“”,“xxx.il”代表著所要載入的函數。現在可以把所需的skill函數全部放在SKILL資料夾裡吧。 3、修改allegro中的功能表: 可以選擇把設定的功能表放在HELP之前,名子自己定,內容自己添加。設置的代碼如下: POPUP "&Sutee" BEGIN MENUITEM "&Align Symbol", "align_sym"