CFA考试一级章节练习题精选0329-31(附详解)

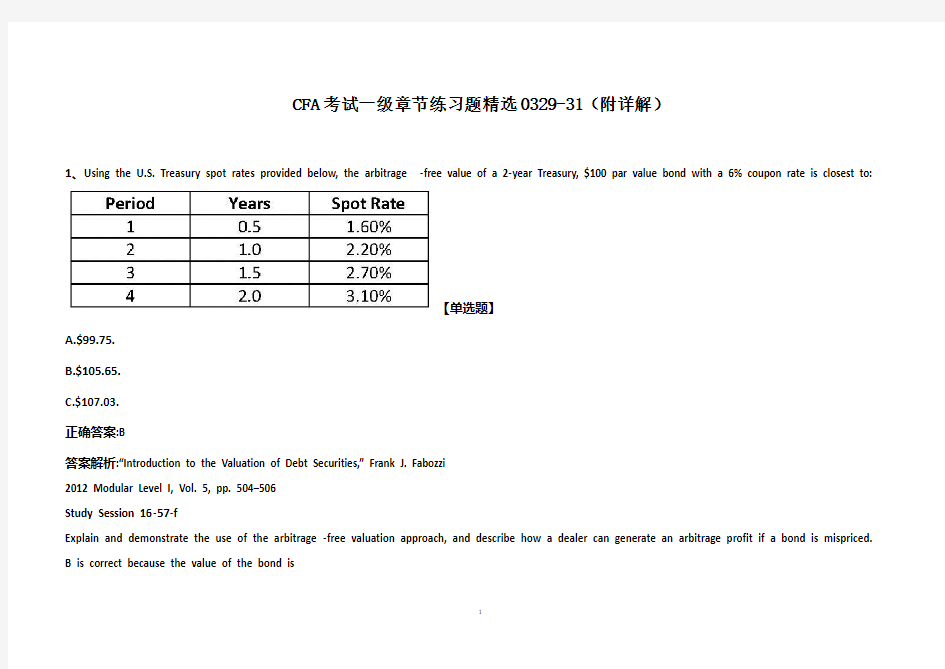

1、Using the U.S. Treasury spot rates provided below, the arbitrage-free value of a 2-year Treasury, $100 par value bond with a 6% coupon rate is closest to:

【单选题】

A.$99.75.

B.$105.65.

C.$107.03.

正确答案:B

答案解析:“Introduction to the Valuation of Debt Securities,” Frank J. Fabozzi

2012 Modular Level I, Vol. 5, pp. 504–506

Study Session 16-57-f

Explain and demonstrate the use of the arbitrage-free valuation approach, and describe how a dealer can generate an arbitrage profit if a bond is mispriced.

B is correct because the value of the bond is

2、The yield of a U.S. bond issue quoted on a bond-equivalent basis is 6.8 percent. The yield-to-maturity on an annual-pay basis is closest to:【单选题】

A.6.69%.

B.6.92%

C.14.06%.

正确答案:B

答案解析:“Yield Measures, Spot Rates, and Forward Rates”, Frank J. Fabozzi, CFA

2010 Modular Level I, Vol. 5, pp. 457

Study Session 16-65-d

Compute and interpret the bond equivalent yield of an annual-pay bond, and the annual-pay yield of a semiannual-pay bond.

B is correct because the yield on an annual-pay basis is calculated as:

The yield on an annual-pay basis is always greater than the yield on a bond-equivalent basis because of compounding.

3、Which of these embedded options most likely benefits the investor?【单选题】

A.The floor in a floating-rate security

B.An accelerated sinking fund provision