《商业银行经营学》(复习题:附答案)

- 格式:doc

- 大小:82.50 KB

- 文档页数:14

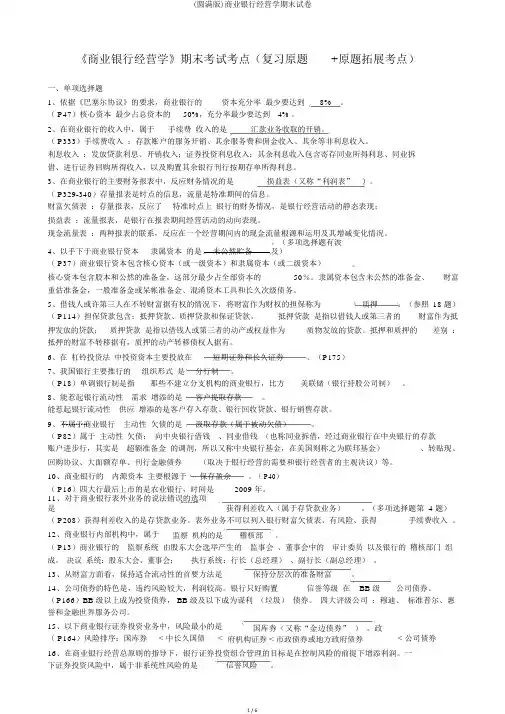

《商业银行经营学》期末考试考点(复习原题+原题拓展考点)一、单项选择题1、依据《巴塞尔协议》的要求,商业银行的资本充分率最少要达到8% 。

( P47)核心资本最少占总资本的50%,充分率最少要达到4% 。

2、在商业银行的收入中,属于手续费收入的是汇款业务收取的开销。

( P333)手续费收入:存款账户的服务开销、其余服务费和佣金收入、其余等非利息收入。

利息收入:发放贷款利息、开销收入;证券投资利息收入;其余利息收入包含寄存同业所得利息、同业拆借、进行证券回购所得收入,以及购置其余银行刊行按期存单所得利息。

3、在商业银行的主要财务报表中,反应财务情况的是损益表(又称“利润表” )。

( P329-340)存量报表是时点的信息,流量是特准期间的信息。

财富欠债表:存量报表,反应了特准时点上银行的财务情况,是银行经营活动的静态表现;损益表:流量报表,是银行在报表期间经营活动的动向表现。

现金流量表:两种报表的联系,反应在一个经营期间内的现金流量根源和运用及其增减变化情况。

4、以手下于商业银行资本隶属资本的是未公然贮备。

(多项选择题有波及)( P37)商业银行资本包含核心资本(或一级资本)和隶属资本(或二级资本)。

核心资本包含股本和公然的准备金,这部分最少占全部资本的50%。

隶属资本包含未公然的准备金、财富重估准备金,一般准备金或呆帐准备金、混淆资本工具和长久次级债务。

5、借钱人或许第三人在不转财富据有权的情况下,将财富作为财权的担保称为质押。

(参照18 题)( P114)担保贷款包含:抵押贷款、质押贷款和保证贷款。

抵押贷款是指以借钱人或第三者的财富作为抵押发放的贷款;质押贷款是指以借钱人或第三者的动产或权益作为质物发放的贷款。

抵押和质押的差别:抵押的财富不转移据有,质押的动产转移债权人据有。

6、在杠铃投资法中投资资本主要投放在短期证券和长久证券。

(P175)7、我国银行主要推行的组织形式是分行制。

( P18)单调银行制是指那些不建立分支机构的商业银行,比方美联储(银行持股公司制)。

简答题1、选择支付工具得原则(61)有利于收购方资本结构得优化目标银行股东得要求遵守国家与地方政府得法律法规税收上得优惠收购方股东得要求证券市场得消化能力2、在银行经营管理得实践中,对存款结构得选择,需要正确处理以下关系:(79)(1)尽量扩大低息存款得吸收,降低利息成本得相对数;(2)正确处理不同存款得利息成本与营业成本得关系,力求不断降低营业成本得支出;(3)活期存款得发展战略必须以不减弱银行得信贷能力为条件;(4)定期存款得发展不以提高自身得比重为目标,而应与银行存款得派生能力相适应。

3、短期借款得管理重点(89)1。

主动把握借款期限与金额,有计划地把借款到期时间与金额分散化,以减少流动性需要过于集中得压力。

2。

尽量把借款到期时间与金额与存款得增长规律相协调,把借款控制在自身承受能力允许得范围内,争取利用存款得增长来解决一部分借款得流动性需要。

3.通过多头拆借得办法将借款对象与金额分散化,力求形成一部分可以长期占用得借款余额.4。

正确统计借款到期得时机与余额,以便做到事先筹措资金,满足短期借款得流动性需要。

4、不良贷款得控制与处理(159)督促企业整改,积极催收到期贷款签订贷款处理协议,借贷双方共同努力,确保贷款安全落实贷款债券债务,防止企业逃废银行债务依靠法律武器,收回贷款本息呆帐冲销5、银行证券投资业务得方式及两种业务方式得区别(176)第一类:商业银行为获利而持有各种组合得证券.第二类:商业银行通过管理证券交易账户来从事广泛得证券业务。

包括:1、作为证券市场专家为客户提供投资咨询与建议。

2、利用证券交易账户,成为国债一级市场得主要承销商。

3、在证券市场上作为“造市者”广泛参与交易.两种业务方式得区别在资产负债表上反映得证券组合与该银行证券交易账户上得证券存货通常按分开得账户进行管理。

1、银行得证券投资组合纳入资产负债表,并有强有力得团队对所投资证券进行科学得测算,运用金融技术进行组合。

过结构性性重组,将其转化为可以在金融市场上出售和流通的证券,据以融通资金的过程。

作用(银行证券投资的功能):①分散风险,获取稳定的收益。

②保持流动性。

③逆经济周期的调节手段。

④合理避税。

为什么资产证券化会降低资本的要求:①由表内业务转为表位业务。

②表外业务对资产的要求比较低。

22、银行证券投资的功能①分散风险,获取稳定的收益。

②保持流动性。

③逆经济周期的调节手段。

④合理避税。

23、杠铃结构方法定义:把证券化分为短期和长期两个组别,银行资金只分布在这两类证券上,而对中期一般不予考虑。

长期证券:偿还期到达中期就卖出,并将收入重投资于长期证券。

(7~8年)短期证券:到期若无流动性补充需要,再投资于短期证券。

(3年以内,根据货币市场状态和证券变现能力自行决定)优点:短期证券保证银行流动性,长期证券收益率较高;利率波动时,投资收益相互抵消。

①预计市场利率↑,长期证券市价↓,出售长期证券资本利得↓;但短期证券本利和未来收入可按不断↑利率重投资。

②预计市场利率↓,短期证券重投资收益率↓;但长期证券市价↑,出售时资本利得↑。

24、表外业务(OBS)定义:指商业银行从事的,按通行的会计准则不列入资产负债表内,不影响其资产负债总额,但能影响银行当期收益,改变银行资产报酬率的经营活动。

作用:①规避了资本限制,增加了盈利来源②为客户提供多样化服务当利率敏感性资产<利率敏感性负债,即银行存在“负缺口”状态时,银行收益随利率上浮而减少,随利率下调而增加。

资金缺口管理:指一定的考察期内到期的或需要重新确定利率的资产和负债。

资金缺口GAP=IRSA-IRSL利率敏感性系数=IRSA/IRSL(一般说,GAP无论正负,绝对值越大风险越大)预期利率上升,则安排正缺口预期利率下降,则安排负缺口*下表为利率变动对利息净收入影响(假设利率变动一致)*下表为有效持续期缺口和利率变动对银行价值影响的表b(GAP)=0c(敏感性系数)=1银行利率风险:当资金缺口绝对值越小,利率风险越小。

《商业银行经营学》复习资料详尽版【本份资料根据学习委员给的提纲详细整理,包括两道计算题完整解答过程,望各位润笔!】题型七个:一、名词解释(3分*4)二、填空题(1分*15)三、单选题(1分*10)四、判断题(1分*10)五、问答题(5分*4)六、计算题(12分*2)9分*1)①威尼斯银行:1587年意大利,是历史上最早的银行,完善了货币经营业,孕育了信贷业务的萌芽。

年英国,标志着资本主义生产方式信用的产生及现代银行的建立。

①信用中介:商业银行通过负债业务,把社会上的各种闲散货币资金集中到银行,再通过资产业务,把它投向需要的资金的各部门,充当有限制资金者和自己短缺者之间的中介人,实现资金的融通。

②支付中介:商业银行利用活期存款账户,为客户办理各种货币结算、货币收付、货币兑换和转移存款等业务活动。

③金融服务:商业银行利用其在国民经济活动中的特殊地位,及其在提供信用中介和支付中介业务过程中所获得的大量信息,运用计算机网络技术等技术手段和工具,为客户提供的其他服务。

④信用创造:商业银行的特殊功能,是指商业银行利用其可以吸收活期存款的有利条件。

通过发放贷款或从事投资业务而衍生出更多存款,从而扩大社会货币供给量.分析:由于市场经济还存在信息不对称、未来不确定等缺陷,政府有必要根据不同时期经些宏观经济政策的实施都和商业银行密切相关.[1]当政府利用财政信用调节经济时,它所发行的财政性债券有很大一部分销售给商业银行。

(如美国联邦政府发行的各种国债中,40%由商业银行认购.)[2]当中央银行代表政府制定和执行货币政策,调节信贷规模,调节社会货币供给量时,主要通过商业银行的业务活动进行。

(如实施紧缩性货币政策,提高法定存款准备金率活在公开市场上卖出有价证券时,商业银行就应当增加准备金或在公开市场上买进有价证券,配合中央银行实现货币政策目标,成为中央银行货币政策实施的微观基础。

)[3]当政府实行产业政策,对经济结构进行调整时,商业银行就要配合政府的产业政策,调整期贷款方向,以支持政府的产业政策。

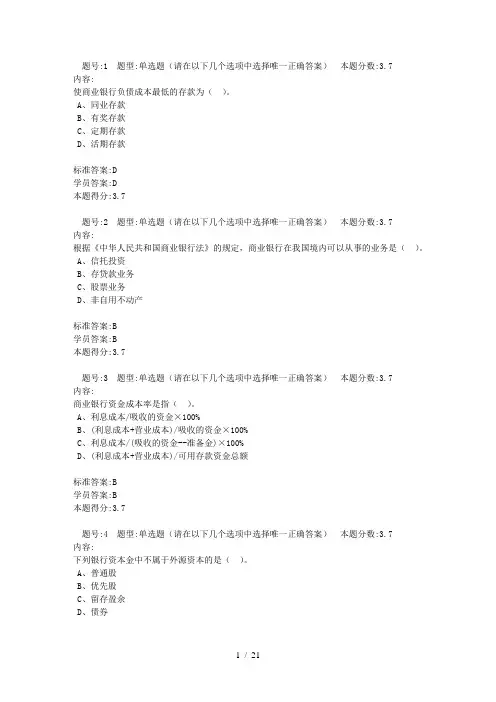

题号:1 题型:单选题(请在以下几个选项中选择唯一正确答案)本题分数:3.7内容:使商业银行负债成本最低的存款为()。

A、同业存款B、有奖存款C、定期存款D、活期存款标准答案:D学员答案:D本题得分:3.7题号:2 题型:单选题(请在以下几个选项中选择唯一正确答案)本题分数:3.7内容:根据《中华人民共和国商业银行法》的规定,商业银行在我国境内可以从事的业务是()。

A、信托投资B、存贷款业务C、股票业务D、非自用不动产标准答案:B学员答案:B本题得分:3.7题号:3 题型:单选题(请在以下几个选项中选择唯一正确答案)本题分数:3.7内容:商业银行资金成本率是指()。

A、利息成本/吸收的资金×100%B、(利息成本+营业成本)/吸收的资金×100%C、利息成本/(吸收的资金--准备金)×100%D、(利息成本+营业成本)/可用存款资金总额标准答案:B学员答案:B本题得分:3.7题号:4 题型:单选题(请在以下几个选项中选择唯一正确答案)本题分数:3.7内容:下列银行资本金中不属于外源资本的是()。

A、普通股B、优先股C、留存盈余D、债券学员答案:C本题得分:3.7题号:5 题型:单选题(请在以下几个选项中选择唯一正确答案)本题分数:3.7内容:关于同业拆借,叙述正确的是()。

A、拆借双方仅限于商业银行B、拆入资金只能用于发放流动资金贷款C、隔夜拆借一般不需要抵押D、拆借利率由中央银行预先规定标准答案:C学员答案:C本题得分:3.7题号:6 题型:单选题(请在以下几个选项中选择唯一正确答案)本题分数:3.7内容:历史上第一家资本主义股份制商业银行建立于()。

A、1407年B、1609年C、1619年D、1694年标准答案:D学员答案:D本题得分:3.7题号:7 题型:单选题(请在以下几个选项中选择唯一正确答案)本题分数:5.56内容:商业银行流动性最高的资产是()。

A、现金资产B、债券C、贷款D、证券标准答案:A学员答案:A本题得分:5.56题号:8 题型:多选题(请在复选框中打勾,在以下几个选项中选择正确答案,答案可以是多个)本题分数:3.7内容:商业银行存款的定价中考虑的因素主要有()。

一、名词解释1、商业银行;2、信用中介;3、支付中介;4、信用创造;5、单一银行制;6、分支银行制;7、集团银行制。

8、流动性;9、资产管理理论;10、负债管理理论;11、一级储备;12、二级储备。

13、内部控制机制;14、分业经营;15、金融创新;16、资产证券化;17、银行监管。

18、银行资本;19、核心资本;20、附属资本;21、资本充足度22、外源资本;23、内源资本;24、债务资本;25、持续增长率。

26、负债业务;27、存款成本;28、存款沉淀率;29、存款工具创新30、同业拆借;31、转贴现;32、转抵押;33、再贴现;34、再贷款;35、回购协议36、负债成本;37、营业成本;38、资金成本;39、可用资金成本40、现金资产;41、库存现金;42、法定存款准备金;43、超额准备金;44、资金头寸;45、基础头寸;46、可用头寸;47、可贷头寸48、贷款承诺费;49、补偿余额;50、信用贷款;51、担保贷款;52、保证贷款;53、抵押贷款;54、质押贷款;55、抵押率;56、票据贴现57、国家债券;58、公司债券;59、商业票据;60、分散投资法;61、梯形投资法;62、杠铃投资法63、中间业务64、银行本票65、代理融通66、保付代理67、贷记卡68、表外业务69、票据发行便利70、远期利率协议71、互换业务72、金融期货交易73、贷款承诺74、进出口融资75、银团贷款76、打包贷款77、出口押汇78、流动性风险79、存储流动性80、同业拆借净值率81、流动性缺口82、利率风险83、资金缺口84、缺口管理85、利率敏感性资金96、久期87、偿还期88、客户风险89、信用分析90、贷款分类91、资产负债表92、损益表93、现金流量表94、银行业绩评价95、ROA96、ROE97、杜邦分析法二、简答题1、简述商业银行的形成和发展。

2、什么是商业银行?它有哪些功能?3、简述商业银行的组织结构。

《商业银行经营学》练习题第一章导论一、名词解释商业银行信用中介支付中介格拉斯-斯蒂格尔法分行制持股公司制流动性银行制度二、填空1、商业银行是以()为目标,以( )为经营对象,( )的企业。

2、( )银行的成立,标志着现代商业银行的产生。

3、现代商业银行形成的途径有( );().4、各国商业银行的发展基本上是循着两种传统:()和()。

5、商业银行在现代经济生活中所发挥的功能主要有( )、()、()、( )和()。

6、股份制商业银行的组织结构包括()、( )、()和()。

7、股份制商业银行的决策系统主要有()、()、( )、和()构成。

8、股份制商业银行的最高权力机构是( )。

9、股份制商业银行的最高行政长官是()。

10、商业银行按资本所有权划分可分为( )、( )、()和( )。

11、商业银行按组织形式可分为()、()和( )。

12、实行单元银行制的典型国家是( )。

13、商业银行经营管理的目标为()、()和()。

14、对我国商业银行实施监管的机构是().三、不定项选择1、商业银行发展至今,已有()的历史。

A100年B200年C300年D500年2、( )银行的成立,标志着现代商业银行的产生。

A英国 B英格兰 C丽如 D东方3、商业银行能够把资金从盈余者手中转移到短缺者手中,使闲置资金得到充分利用。

这种功能被称为( )功能。

A信用中介 B支付中介 C信用创造 D金融服务4、下列银行体制中,只存在于美国的是()A分行制 B私人银行 C国有银行 D单元制5、我国商业银行的组织形式是( )A单元制银行 B分支行制银行 C银行控股公司 D连锁银行6、实行分支行制最典型的国家是( )A美国B日本C法国D英国7、股份制商业银行的最高权利机构是()。

A董事会 B股东大会 C监事会 D总经理8、银行业的兼并对其产生的优势是( ).A扩大了规模 B有利于进行金融创新 C取得优势互补,拓展业务范围 D提高盈利能力9、对银行业加强监管的意义体现在( ).A保护和发挥商业银行在社会经济活动中的作用,促进经济的健康发展。

《商业银行经营学》复习自测题参考答案一、单项选择题1、A2、B3、B4、C5、B6、B7、C8、D9、A 10、A11、A 12、D13、D14、B15、B 16、B 17、A18、D 19、C20、A21、B22、A23、A24、D25、B 26、A27、B28、D 29、C30、A31、D32、C33、D34、B35、A36、B 37、B38、D 39、C40、C二、多项选择题1、ABCD2、ABC3、BCD4、ABCD5、ABCD6、ABC7、ABC8、ABD9、CD 10、ABCD11、AB 12、ABD 13、AD 14、ABCD 15、ABC 16、BCD17、ACD 18、ABCD 19、ABCD 20、ABC21、ABCD22、ABD23、ACD24、ABCD25、ABC 26、AD27、ABC28、ACD29、ABC 30、BC 31、ABC 32、BD 33、BC 34、BCD 35、CD 36、ABCD37、ABCD38、ABCD39、ABC40、BC三、判断题1、B2、A3、A4、B5、B6、A7、A8、B9、A 10、B11、A12、B13、B14、B15、A16、A 17、B18、A19、A20、B21、A 22、A 23、B 24、A 25、B 26、A 27、B 28、B 29、B 30、A31、B 32、A 33、B34、A35、A36、B37、B38、A39、A40、B四、简答题1、商业银行在国民经济中的地位。

答:(1)商业银行已成为国民经济活动的中枢(2)商业银行的业务活动对全社会的货币供给具有重要影响(3)商业银行成为社会经济活动的信息中心(4)商业银行成为国家实施宏观经济政策的重要途径和基础(5)商业银行成为社会资本运动的中心2、影响贷款价格的主要因素。

答:(1)信贷资金的供求状况、(2)资金成本(3)贷款风险程度(4)贷款费用(5)借款人的信用及与银行的关系(6)银行贷款的目标收益率3、商业银行提高资本充足率的策略。

商业银行经营学题目及答案近年来,随着我国金融业的快速发展以及市场竞争的加剧,商业银行作为金融市场中最重要、最活跃的主体之一,其经营管理能力的提升变得尤为重要。

商业银行经营学作为金融学的一个重要分支,专注于商业银行的运营管理,探索和研究银行经营中的问题和解决方案。

在这篇文章中,我们将探讨一些与商业银行经营学相关的常见问题,并提供相应的答案。

一、商业银行资产负债管理1. 什么是商业银行的资产负债管理?商业银行的资产负债管理是指通过合理配置各项资产和负债,使银行的净利润最大化,并同时保持足够的偿债能力。

其目标是平衡风险和回报,提高银行的盈利能力和抵御风险的能力。

2. 商业银行的资产负债管理方法有哪些?商业银行常用的资产负债管理方法包括资产负债收益率管理、平均资产期限匹配、对冲与排队等。

资产负债收益率管理是通过调整资产和负债的比例和结构,使银行的资产收益率与资金成本达到最佳匹配;平均资产期限匹配是通过选择不同期限的资产和负债,使银行的生息资产和借贷资金的平均期限相匹配;对冲与排队则是通过对冲交易和负债清单管理来降低银行的风险。

二、商业银行信贷风险管理1. 商业银行的信贷风险管理是什么?商业银行的信贷风险管理是指通过对贷款申请人的信用状况、项目的可行性等因素进行综合评估,以减少贷款违约风险和损失,并确保银行资产的安全。

2. 商业银行的信贷风险管理方法有哪些?商业银行常用的信贷风险管理方法包括征信调查、贷款审查、担保方式选择等。

征信调查是通过查询申请人的信用记录和支付能力等信息,评估其还款意愿和还款能力;贷款审查是通过审核资金用途和还款来源等文件,评估贷款项目的可行性和风险;担保方式选择是根据借款人的信用状况和贷款规模,选择适当的担保方式来减少风险。

三、商业银行营销策略1. 商业银行的营销策略是什么?商业银行的营销策略是指通过合理的市场调研和产品定位,以及有效的市场推广和销售策略,吸引更多的客户并发展稳定的客户关系,提高银行的营业收入。

简答题1.选择支付工具的原则(61)有利于收购方资本结构的优化目标银行股东的要求遵守国家和地方政府的法律法规税收上的优惠收购方股东的要求证券市场的消化能力2.在银行经营管理的实践中,对存款结构的选择,需要正确处理以下关系:(79)(1)尽量扩大低息存款的吸收,降低利息成本的相对数;(2)正确处理不同存款的利息成本和营业成本的关系,力求不断降低营业成本的支出;(3)活期存款的发展战略必须以不减弱银行的信贷能力为条件;(4)定期存款的发展不以提高自身的比重为目标,而应与银行存款的派生能力相适应。

3.短期借款的管理重点(89)1.主动把握借款期限和金额,有计划地把借款到期时间和金额分散化,以减少流动性需要过于集中的压力。

2.尽量把借款到期时间和金额与存款的增长规律相协调,把借款控制在自身承受能力允许的范围内,争取利用存款的增长来解决一部分借款的流动性需要。

3.通过多头拆借的办法将借款对象和金额分散化,力求形成一部分可以长期占用的借款余额。

4.正确统计借款到期的时机和余额,以便做到事先筹措资金,满足短期借款的流动性需要。

4、不良贷款的控制与处理(159)督促企业整改,积极催收到期贷款签订贷款处理协议,借贷双方共同努力,确保贷款安全落实贷款债券债务,防止企业逃废银行债务依靠法律武器,收回贷款本息呆帐冲销5、银行证券投资业务的方式及两种业务方式的区别(176)第一类:商业银行为获利而持有各种组合的证券。

第二类:商业银行通过管理证券交易账户来从事广泛的证券业务。

包括:1、作为证券市场专家为客户提供投资咨询和建议。

2、利用证券交易账户,成为国债一级市场的主要承销商。

3、在证券市场上作为“造市者”广泛参与交易。

两种业务方式的区别在资产负债表上反映的证券组合与该银行证券交易账户上的证券存货通常按分开的账户进行管理。

1、银行的证券投资组合纳入资产负债表,并有强有力的团队对所投资证券进行科学的测算,运用金融技术进行组合。

商业银行经营学复习题及答案一、名词解释题1.单元制银行:指那些不设立或不能设立分支机构的商业银行,这种银行主要集中在美国。

2.回购协议:指商业银行在出售证券等金融资产是签订协议,约定在一定期限后按约定价格购回所卖政权,以获得及时可用资金的交易方式。

3.打包放款:是出口地银行在出口商备货过程中因出口商头寸不足而向出口商提供的一种短期资金。

银行向出口商提供的这种短期贸易贷款是支持出口商按期履行合同义务、出运货物。

4.欧洲金融债券:指债券发行银行通过其他银行和金融机构,在债券面值货币以外的国家发行并推销债券。

5.质押贷款:是指按规定的质押方式以借款人或第三者的动产或权利作为质物发放的贷款。

6.商业银行(Commercial Bank)是一个以营利为目的,以多种金融负债筹集资金,多种金融资产为经营对象,具有信用创造功能的金融机构。

7.核心资本(Core Captial) 又称一级资本,核心资本至少应占全部资金的50% 。

根据我国商业银行资本充足率管理办法,核心资本包括实收资本或普通股、资本公积、盈余公积、未分配利润和少数股权。

8.大额可转让定期存单(CDs):大额可转让定期存单是银行发行的具有固定期限和一定利率,并且可以转让的金融工具。

这种金融工具的发行和流通所形成的市场称为可转让定期存单市场9.审贷分离制度:审贷分离制度是规范商业银行内部信贷业务运行机制、保障信贷资产质量与安全的一项基本制度。

所谓审贷分离,实际上就是指商业银行在发放贷款时,要将贷款的审查与贷款的具体发放与管理分开。

10.持续期缺口(Duration Gap):持续期是指某项资产或负债的所有预期现金流量的加权平均时间,也就是指某种资产或负债的平均有效期限。

持效期缺口等于总资产持续期-总负债/总资产×总负债持续期。

11.补偿余额(Compensation Balances):补偿余额又称“补偿性存款”指贷款银行要求借款人按借款的一定比例留存银行的那部分存款12.备用信用证(Standby Credit Letter):又称担保信用证,是指不以清偿商品交易的价款为目的,而以贷款融资,或担保债务偿还为目的所开立的信用证。

商业银⾏经营学复习题《商业银⾏经营学》练习题第⼀章导论⼀、名词解释商业银⾏:商业银⾏是以追求利润最⼤化为⽬标,通过多种⾦融负债筹集资⾦,以多种⾦融资产为其经营对象,能利⽤负债进⾏信⽤创造,并向客户提供多功能、综合性服务的⾦融企业。

信⽤中介:是指商业银⾏通过负债业务,把社会上各种闲散资⾦集中到银⾏,再通过资产业务,把它投向需要资⾦的部门,充当资⾦闲置者和资⾦短缺者之间的中介⼈,实现资⾦融通。

⽀付中介:是指商业银⾏利⽤活期存款账户,为客户办理各种货币结算、货币收付、货币兑换和转移存款等业务活动。

格拉斯—斯蒂格尔法:也称作《1933年银⾏法》。

在1930年代⼤危机后的美国⽴法,将投资银⾏业务和商业银⾏业务严格地划分开,保证商业银⾏避免证券业的风险。

该法案禁⽌银⾏包销和经营公司证券,只能购买由美联储批准的债券。

分⾏制银⾏:是指那些在总⾏之下,可在本地或外地设有若⼲分⽀机构,并都可以从事银⾏业务的商业银⾏。

持股公司制银⾏:有⼀个集团公司成⽴股权公司,再由该公司收购或控制若⼲独⽴的银⾏。

流动性:指银⾏资产的变现能⼒。

商业银⾏制度:是指⼀个国家⽤法律形式所确定的该国商业银⾏体系、结构及组成这⼀体系的原则的总和。

五、问答1、什么是商业银⾏?它有哪些功能?商业银⾏是以追求利润最⼤化为⽬标,通过多种⾦融负债筹集资⾦,以多种⾦融资产为其经营对象,能利⽤负债进⾏信⽤创造,并向客户提供多功能、综合性服务的⾦融企业。

商业银⾏在现代经济⽣活中所发挥的功能主要有信⽤中介、⽀付中介、⾦融服务、信⽤创造、调节经济和风险管理。

2、商业银⾏经营原则有哪些?如何贯彻这些原则?安全性⽬标;流动性⽬标;盈利性⽬标;如何贯彻这些原则:从第1章第五节⾃⼰凝练第⼆章商业银⾏资本⼀、名词解释普通股:普通股是指在公司的经营管理和盈利及财产的分配上享有普通权利的股份,代表满⾜所有债权偿付要求及优先股东的收益权与求偿权要求后对企业盈利和剩余财产的索取权,它构成公司资本的基础。

《商业银行经营学》练习题第一章导论一、名词解释商业银行:商业银行是以追求利润最大化为目标,通过多种金融负债筹集资金,以多种金融资产为其经营对象,能利用负债进行信用创造,并向客户提供多功能、综合性服务的金融企业。

信用中介:是指商业银行通过负债业务,把社会上各种闲散资金集中到银行,再通过资产业务,把它投向需要资金的部门,充当资金闲置者和资金短缺者之间的中介人,实现资金融通。

支付中介:是指商业银行利用活期存款账户,为客户办理各种货币结算、货币收付、货币兑换和转移存款等业务活动。

格拉斯—斯蒂格尔法:也称作《1933年银行法》。

在1930年代大危机后的美国立法,将投资银行业务和商业银行业务严格地划分开,保证商业银行避免证券业的风险。

该法案禁止银行包销和经营公司证券,只能购买由美联储批准的债券。

分行制银行:是指那些在总行之下,可在本地或外地设有若干分支机构,并都可以从事银行业务的商业银行。

持股公司制银行:有一个集团公司成立股权公司,再由该公司收购或控制若干独立的银行。

流动性:指银行资产的变现能力。

商业银行制度:是指一个国家用法律形式所确定的该国商业银行体系、结构及组成这一体系的原则的总和。

五、问答1、什么是商业银行?它有哪些功能?商业银行是以追求利润最大化为目标,通过多种金融负债筹集资金,以多种金融资产为其经营对象,能利用负债进行信用创造,并向客户提供多功能、综合性服务的金融企业。

商业银行在现代经济生活中所发挥的功能主要有信用中介、支付中介、金融服务、信用创造、调节经济和风险管理。

2、商业银行经营原则有哪些?如何贯彻这些原则?安全性目标;流动性目标;盈利性目标;如何贯彻这些原则:从第1章第五节自己凝练第二章商业银行资本一、名词解释普通股:普通股是指在公司的经营管理和盈利及财产的分配上享有普通权利的股份,代表满足所有债权偿付要求及优先股东的收益权与求偿权要求后对企业盈利和剩余财产的索取权,它构成公司资本的基础。

2023年《商业银行经营学》考试题及答案一、单选题1.《巴塞尔协议Ⅰ》规定核心资本与风险资产比率不得低于(),银行总资本与风险资产比率不得低于()。

A、4%,10%B、8%,4%C、8%,10%D、4%,8%参考答案:D2.商业银行表外风险资产的计算参照()进行。

A、表外风险资产=∑表外资产×风险权数B、表外风险资产=∑表外资产×表内相对性质资产的风险权数C、表外风险资产=∑表外资产×信用转换系数D、表外风险资产=∑表外资产×信用转换系数×表内相对性质资产的风险权数参考答案:D3.属于商业银行外源资本融资策略的是()。

A、发行新股B、增加利润留成C、发行一般性金融债券D、向中央银行借款参考答案:A4.《巴塞尔协议III》规定,正常条件下系统重要性银行资本充足率的最低标准是()。

A、9%B、10%C、10.5%D、11%参考答案:D5.《巴塞尔协议III》中提出的杠杆率标准是()。

A、2%B、3%C、4%D、5%参考答案:B6.《巴塞尔协议III》引入逆周期超额资本的监管标准是()。

A、0-2%B、1-2.5%C、1-2%D、0-2.5%参考答案:D7.《巴塞尔协议III》引入流动性风险监管标准,其中流动性覆盖率的计算公式是()。

A、流动性覆盖率=优质流动性资产储备/未来20天的资金净流出量B、流动性覆盖率=优质流动性资产储备/未来30天的资金净流出量C、流动性覆盖率=优质流动性资产储备/未来50天的资金净流出量D、流动性覆盖率=优质流动性资产储备/未来60天的资金净流出量参考答案:B8.资金成本指为服务客户存款而支付的一切费用,包括利息成本和()之和。

A、可用资金成本B、营业成本C、风险成本D、连锁反应成本参考答案:B9.商业银行的长期借款通常采用()。

A、发行大面额存单B、发行金融债券C、发行企业债券D、再贴现参考答案:B10.按存款人经济性质划分,银行存款可以分为()。

第二章1讨论银行资本的各种不同组成部分及其作用商业银行的资本金除了包括股本、资本盈余、留存收益在内的所有者权益外,还包括一定比例的债务资本,如资本票据、债券等。

商业银行的资本具有双重特点,根据《巴塞尔协议》,常将所有者权益称为一级资本和核心资本,而将长期债务称为二级资本和附属资本。

(1)核心资本包括股本和盈余。

(2)附属资本包括若干种,通常有资本票据和债券两类。

(3)还有一些其他来源如准备金等。

2为何充足的银行资本能降低银行经营风险银行资本充足性是指银行资本数量必须超过金童管理当局所规定的能够保障正常营业自以维持充分信誉的最低限度;同时,银行现有资本或新增资本的构成,应该符合银行总体经营目标或所需新增资本的具体目的。

分为资本数量和资本结构的合理性。

资本量不足,往往是银行盈利性和安全性失衡所致。

为追求利润,过度扩大风险资产,盲目发展表外业务等,这些现象必然导致银行资本量相对不足,加大银行的经营风险。

3为何《巴塞尔协议》有关银行资本规定对国际银行间的公平竞争具有特别重要的意义《巴塞尔协议》对银行资本衡量采用了全新的方法。

其中,表内风险资产和表外风险资产测算是关键。

对资本充足性规定了国际统一的标准,具有很强的约束力。

为了保持资本质量,避免银行集团内部的双重杠杆作用,新协议的适用范围将在全面并表基础上扩大到以银行业务为主的银行集团的持股公司。

新协议还考虑了银行业的进步和业内对1988年协议的批评意见,明确提出五大目标,即把评估资本充足率的工作与银行面对的主要风险更紧密的联系在一起,促进安全稳健性;在充分强调银行自己的内部风险评估体系的基础上,促进公平竞争;激励银行提高风险计量与管理水平;资本反映银行头寸和业务的风险度;重点放在国际活跃银行,基本原则适用于所有银行。

4讨论现行的风险加权资本的要求5银行如何确定其资本金要求?应考虑哪些关键的因素银行最低资本限额应与银行资产结构决定的资产风险相联系,因此银行资本的要求量与银行资本结构及资产结构直接相关。

商业银行经营学试卷(A)一、单项选择题(本大题共6小题,每小题2分,共12分)1。

根据《巴塞尔协议》具体实施要求,国际大银行的资本对风险资产比率应达到(C )以上。

A.1.2 5 % B. 4% C 。

8% D。

50%2。

如某银行在2月7日(星期四)至13日(星期三)期间的非交易性存款平均余额为50 000万元,按照8%的存款准备金率,问该行在2月21日到27日这一周中应保持的准备金平均余额为多少万元。

(A)A.4000 B。

50000 C . 46000 D。

20003.某商业银行总资产1000万元,负债800万元,其财务杠杆比例是(B )。

A.2。

5B。

5 C 。

8 D. 104.《巴塞尔协议》将银行的票据发行便利额度和循环承购便利函业务的信用风险转换系数定为(B )。

A.100%B.50%C . 20% D.0%5.我国商业银行法规定银行的贷款/存款比率不得超过( B )。

A.100%B.75%C.50%D.25%6.甲企业将一张金额为1000万元,还有36天才到期的银行承兑汇票向一家商业银行申请贴现,假设银行当时的贴现率为5%,甲企业得到的贴现额是( B )。

正确答案:B 注:1000(1—5%×36/360)=995 万元A. 1000万元B. 995万元C. 950万元D. 900万元二、判断题(正确打“√",错误打“⨯";每小2题分,共10分)1。

大额可转让定期存单存款的主要特点是稳定且资金成本较低。

(⨯ )2。

一般来说银行财务杠杆比率越高,其投资风险越小。

( ⨯ )3. 当市场利率上升时,银行所持固定收入的金融工具的市场价值亦上升。

(⨯)4. 银行关注类贷款与可疑贷款一样,均属于不良贷款范畴.(⨯ )5. 商业银行可贷头寸即可用头寸减必要的库存现金及央行清算存款.( √ )三、计算题(每小10题分,共20分)1。

某一银行总资本为6000万元,计算其资本充足率。

1、Fill in the Blank Questions(1)_______________________ is a newer service provided by banks where thebank lends money to individuals for the purchase of durable and other goods.Answer: Consumer lending(2)The loosening of government regulation and control of financial institutions iscalled ______ . Answer: deregulation(3)A bank which now offers all of the available financial services is known as a__________bank. Answer: universal(4)A(n) buys and sells securities on behalf of their customers and fortheir own accounts. Examples of this type of financial service provider include Merrill Lynch and Charles Schwab.Answer: security broker (or dealer)(5)One tool that the Federal Reserve uses to control the money supply is___________. The Federal Reserve will buy and sell T-bills when they areusing this tool of monetary policy. Answer: open market operations(6)The federal bank regulatory agency which examines the most banks is the______________. Answer: FDIC(7)The short term securities of the bank, including T-Bills and commercial paper,are often called __________________________ because they are the second line of defense to meet demands for cash. Answer: secondary reserves(8)A(n)__________________________ is a deposit account which pays an interestrate competitive with money market mutual funds and which generally haslimited check writing ability. Answer: money market deposit account(9)__________________________ can be held by individuals andnonprofit institutions, bear interest and permit drafts from being written against the account to pay third parties.Answer: Now accounts(10)T he equity multiplier for a bank measures the amount of_____________________ of the bank and is one part of the evaluation of the bank's ROE. Answer: leverage (debt)(11)__________________________ is the risk that the financial institution may notbe able to meet the needs of depositors for cash. Answer: Liquidity risk(12)A traditional measure of earnings efficiency is the __________________ ortotal interest income over total earnings assets less total interest expenses over total interest bearing bank liabilities. It measures the effectiveness of a firm’s intermediation function in the borrowing and lending of money. Answer:earnings spread(13)T he__________________ is the interest rate that equalizes the current marketprice of a bond with the present value of the future cash flows. Answer: yield to maturity (YTM)(14)_________________________ is the difference between interest-sensitive assetsand interest-sensitive liabilities. Answer: Dollar interest-sensitive gap(15)A(n)_________________________ allows the holder the right to either sellsecurities to another investor (put) or buy securities from another investor (call) for a set price before the expiration date. Answer: option(16)A(n)_________________________ is a contract where two parties exchangeinterest payments in order to save money and hedge against interest rate risk.Answer: interest rate swap(17)A(n)_________________________ is where there is both a minimum and amaximum interest rate set on a loan. Answer: interest rate collar(18)A(n) _________________________ is a contingent claim of the bank that issuesit. The issuing bank, in return for a fee, guarantees the repayment of a loanreceived by its customer or the fulfillment of a contract made by its customer to a third party. Answer: standby credit agreement(19)A relatively new type of credit derivative is a CDO which stands for__________________. Answer: collateralized debt obligation(20)24. Lenders can set aside a group of loans on their balance sheet, issue bonds andpledge the loans as collateral against the bonds in ____________ . These usually stay on the bank’s balance sheet as liabilities. Answer: loan backed bonds (21)D ebt instruments issued by cities, states and other political entities and which areexempt from federal taxes are collectively known as _____________________ .Answer: municipal securities(22)__________________ is the risk that the company whose bonds the financialinstitution owns may retire the entire issue of corporate bonds in advance of their maturity leaving the bank with the risk of earnings losses resulting fromreinvesting the cash at lower interest rates. Answer: Call risk(23)T he _________________________ is the total difference between its sources anduses of funds. Answer: liquidity gap(24)T he oldest approach to meeting liquidity needs which relies on the sale of liquidassets to meet liquidity demands is called _________________________. Answer: asset liquidity management(25)_________________________ are the stable base of deposited funds that are nothighly sensitive to movements in market interest rates and tend to remain with a depository institution. Answer: Core deposits(26)W hen financial institutions tempt customers by paying postage both ways inbank-by-mail services or by offering free gifts such as teddy bears, they arepracticing ___________. Answer: nonprice competition(27)W hen a customer is charged based on the number and kinds of services used, withthe customers that use a number of services being charged less or having some fees waived, this is called __________________ pricing. Answer: relationship (28)__________________ is the amount in excess of par value paid by the bank'sshareholders. Answer: Surplus(29)C ore capital such as common stock, surplus, undivided profits, qualifyingnoncumulative preferred stock, etc. is referred to as __________________ capital as defined by the Basel agreement. Answer: Tier 1(30)T he largest component of capital among banks is ____________. Answer: surplus1、True/False Questions(1)According to the textbook, banks are those financial institutions that today offerthe widest range of financial services of any business firm in the economy.Answer: True(2)The role performed by banks in the economy in which they transform savings intocredit is known as the intermediation role.Answer: True(3)The aging of the population means less savings in the economy for banks to workwith, according to the textbook. Answer: False(4)Banks which offer virtually all financial services are known as universal banks.Answer: True(5)In the United States, fixed fees charged for deposit insurance, regardless of howrisky a bank is, led to a problem known as moral hazard.Answer: True(6)When the Federal Reserve buys T-bills through its open market operations, itcauses the growth of bank deposits and loans to decrease. Answer: False(7)Loans and leases are financial outputs on a financial institution's balance sheet orReport of Condition. Answer: True(8)Off balance sheet items for a bank are fee generating transactions which are notrecorded on their balance sheet. Answer: True(9)A bank's ROA equals its ROE times the ratio of total assets divided by total equitycapital. Answer: False(10)I n the textbook the ratio of pre tax net operating income to total operatingrevenues is described as a measure of the effectiveness of a financial insitution's(12)Usually the principal goal of asset-liability management is to maximize or atleast stabilize a bank's margin or spread. Answer: True(13)A liability-sensitive bank will experience an increase in its net interest margin ifinterest rates rise. Answer: False(14) A futures hedge against interest-rate changes generally requires a bank totake an opposite position in the futures market from its current position in the cash market. Answer: True(15)T he long hedge in financial futures contracts is most likely to be used insituations where a bank would suffer losses due to rising interest rates. Answer: False(16)T he buyer of a loan participation must watch both the borrower and the sellerbank closely. Answer: True(17)I n a CMO, the different tiers (or tranches) of security purchasers face the sameprepayment risk. Answer: False(18)M ost loans that banks sell off their balance sheets carry interest rates that usuallyare connected to long-term interest rates (such as the 30-year Treasury bond rate).Answer: False(19)P repayment risk on securitized assets generally increases when interest rates rise.Answer: False(20)W hen a bank irrevocably guarantees a commercial paper issue, the bank's creditrating substitutes for the borrower's credit rating. Answer: True(21)B orrowed liquidity (liability) management is less risky for a financial institutionthan is asset conversion. Answer: False(22)M ost liquidity problems in banking arise from inside a bank, not from itscustomers. Answer: False(23)D eposits owned by commercial banks and held with other banks are calledcorrespondent deposits.Answer: True(24)T he number one factor households consider in selecting a bank to hold theirchecking account is, according to recent studies cited in this chapter, low fees and low minimum balance. Answer: False(25)W hen a bank temporarily offers higher than average interest rates or lower thanaverage customer fees in order to attract new business they are practicing conditional pricing. Answer: False(26)One fundamental purpose for regulating capital is to limit losses to thefederal government arising from deposit insurance claims. Answer: True(27)U nder the international capital (Basel) agreement Tier 2 capital must be raised toa minimum of 4 percent of risk-weighted assets. Answer: False(28)Recent research suggests that interest-rate contracts display considerably lessrisk exposure than do foreign-currency contracts.Answer: True2、Multiple Choice Questions(1) Drew Davis goes to his local bank to get help developing a financial plan and making investment decisions. Which of the more recent services banks offer is Drew taking advantage of ?A) Getting a consumer loanB) Getting financial adviceC) Managing cashD) Getting venture capital servicesE) Buying a retirement planAnswer: B(2) Jonathan Robbins has a bank account in a bank that does not have a physical branch. Jonathan does all of his banking business over the internet. What type of bank does Jonathan have his account at?A) Virtual BankB) Mortgage BankC) Community BankD) Affiliated BankE) None of the aboveAnswer: A(3) Banks are regulated for which of the reasons listed below?A) Banks are leading repositories of the public's savings.B) Banks have the power to create money.C) Banks provide businesses and individuals with loans that support consumption and investment spending.D) Banks assist governments in conducting economic policy, collecting taxes and dispensing government payments.E) All of the above.Answer: E(4) The equivalent of the Federal Reserve System in Europe is known as the:A) European UnionB) Bank of LondonC) Basle GroupD) European Central BankE) Swiss Bank CorporationAnswer: D(5) A financial institution's bad-debt reserve, as reported on its balance sheet, is called:A) Unearned income or discountB) Allowance for possible loan lossesC) Intangible assetsD) Customer liability on acceptancesE) None of the aboveAnswer: B(6)Nonperforming loans are credits on which any scheduled loan repayments and interest payments are past due for more than:A) 30 daysB) 60 daysC) 90 daysD) 180 daysE) None of the above.Answer: C(7) The so-called employee productivity ratio for a bank is equal to:A) Net operating revenue less total interest expenses per employee.B) Total interest and noninterest expense per employeeC) Net operating income per full-time-equivalent employeeD) Total operating earnings less salaries and wages expense per employee.E) None of the above.Answer: C(8) Which of the following would be the best example of a ratio used to examine the bank's interest rate risk?A) Demand deposits/ total assetsB) Interest on time deposits/ total time depositsC) Interest on real estate loans/ total real estate loansD) Interest sensitive assets/ interest sensitive liabilitiesAnswer: D(9) A bank is asset sensitive if its:A) Loans and securities are affected by changes in interest rates.B) Interest-sensitive assets exceed its interest-sensitive liabilities.C) Interest-sensitive liabilities exceed its interest-sensitive assets.D) Deposits and borrowings are affected by changes in interest rates.E) None of the above.Answer: B(10) A bond has a face value of $1000 and five years to maturity. This bond hasa coupon rate of 13 percent and is selling in the market today for $902. Coupon payments are made annually on this bond. What is the yield to maturity (YTM) for this bond?A) 13%B) 12.75%C) 16%D) 11.45%E) Cannot be calculated from the information givenAnswer: C(11) An option buyer can:A) Exercise the option.B) Sell the option to another buyer.C) Allow the option to expire.D) All of the above.E) A and B only.Answer: D(12) A put option would most likely be used to:A) Protect fixed-rate loans and securities.B) Protect variable-rate loans and securities.C) Offset a positive interest-sensitive gap.D) Offset a negative interest-sensitive gap.E) None of the above.Answer: A(13) A financial institution that buys a put option:A) Has the right to accept delivery of the underlying security at the contract price if they wishB) Has the right to make delivery of the underlying security at the contract price if they wishC) Is obligated to accept delivery of the underlying security at the contract priceD) Is obligated to make delivery of the underlying security at the contract price Answer: B(14) Loan-backed securities, which closely resemble traditional bonds, carry various forms of credit enhancements, which may include all of the following, EXCEPT:A) Credit letter guaranteeing repayment of the securities.B) Set aside of a cash reserve.C) Division into different risk classes.D) Early payment clauses.E) None of the above.Answer: D(15) When two banks simply agree to exchange a portion of their customers' loan repayments, they are using:A) A credit optionB) A standby letter of creditC) A credit linked noteD) A credit swapE) None of the aboveAnswer: D(16) Principal roles that a financial institution's investment portfolio play include which of the following?A) Income stabilityB) Geographic diversificationC) Hedging interest rate riskD) Backup liquidityE) All of the aboveAnswer: E(17) Which of the following statements is (are) correct regarding duration?A) In comparing two bonds with the same yield to maturity and the same maturity, a bond with a higher coupon rate will have a longer duration.B) In comparing two loans with the same maturity and the same interest rate, a fully amortized(分期付款) loan will have a shorter duration than a loan with a balloon payment(付款的最后一笔较大).C) The duration will always be shorter than the maturity for all debt instruments.D) All of the aboveE) B and CAnswer: B(18) A bank expects in the week about to begin $30 million in incoming deposits, $20 million in deposit withdrawals, $15 million in revenues from the sale of nondeposit services, $25 million in customer loan repayments, $5 million in sales of bank assets, $45 million in money market borrowings, $60 million in acceptable loan requests, $10 million in repayments of bank borrowings, $5 million in cash outflows to cover other operating expenses, and $10 million in dividend payments to its stockholders. This bank's net liquidity position for the week is:A) $30 millionB) $20 millionC) $10 millionD) $15 millionE) None of the aboveAnswer: D(19)Financial institutions face significant liquidity problems because of:A) Imbalances between the maturities of their assets and their principal liabilities.B) Their high proportion of liabilities subject to immediate withdrawal.C) Their sensitivity to changes in interest rates.D) Both A and BE) All of the above.Answer: E(20)A bank determines from an analysis on its deposits that account processing and other operating expenses cost the bank $3.95 per month. It has also determined that its non operating expenses on its deposits are $1.35 per month. The bank wants to have a profit margin which is 10 percent of monthly costs. What monthly fee should this bank charge on its deposit accounts?A) $5.30 per monthB) $3.95 per monthC) $5.83 per monthD) $5.70 per monthE) None of the aboveAnswer: C(21) A bank quotes an APY of 8%. A small business that has an account with this bank had $2500 in their account for half the year and $5000 in their account for the other half of the year. How much in total interest earnings did this bank make during the year?A) $300B) $200C) $400D) $150E) None of the aboveAnswer: A(22)An account at a bank that carries a fixed maturity date with a fixed interest rate and which often carries a penalty for early withdrawal of money is called:A) Demand depositB) Transaction depositC) Time depositD) Money market mutual depositE) None of the aboveAnswer: C(23)The risk that a customer the bank has entered into a contract with will fail to pay or to perform, forcing the bank to find a replacement contract that may be less satisfactory is what form of risk listed below?A) Counterparty riskB) Interest-rate riskC) Operating riskD) Credit riskE) Liquidity riskAnswer: A(24)A bank has a profit margin of 5 percent, an asset utilization ratio of 11 percent , an equity multiplier of 12 and a retention ratio of 60 percent. What is this bank's ICGR?A) 6.6 percentB) 3.96 percentC) 7.2 percentD) .33 percentE) None of the aboveAnswer: B(25)A bank has $200 million in assets in the 0 percent risk-weight category. It has $400 million in assets in the 20 percent risk-weight category. It has $1000 million in assets in the 50 percent risk-weight category and has $1000 million in assets in the 100 percent risk-weight category. This bank has $96 million in Tier 1 capital and $48 million in Tier 2 capital. What is this bank's ratio of Tier 1 capital to risk assets?A) 6.08 percentB) 3.04 percentC) 9.11 percentD) 5.54 percentE) None of the aboveAnswer: A3、Short Answer(1) The term bank has been applied broadly over the years to include a diverse set of financial-service institutions, which offer different financial service packages. Identify as many of the different kinds of “banks” as you can. How do the“banks” you have identified compare to the largest banking group of all –the commercial banks? Why do you think so many different financial firms have been called banks? How might this terminological confusion affect financial-service customers?The general public tends to classify anything as a bank that offers some sort of financial service, especially deposit and loan services. Other institutions that are often referred to as a bank without being one are savings associations, credit unions, money market funds, mutual funds, hedge funds, security brokers and dealers, investment banks, finance companies, financial holding companies and life and property/casualty insurance companies. All of these institutions offer some of the services that a commercial bank offers, but generally not the entire scope of services. Since providers of financial services are normally called banks by the general public they are able to take away business from traditional banks and it is of utmost importance for commercial banks to clarify their unique position among financial services providers.(2) What is monetary policy?Monetary policy consists of regulation and control over the growth of money and credit in an attempt to pursue broad economic goals such as full employment,avoidance of inflation, and sustainable economic growth. Its principal tools are open market operations, changes in the discount (lending) rate, and changes in reserve requirements behind deposits.(3) What factors influence the stock price of a financial-services corporation?A bank's stock price is affected by all those factors affecting its profitability and risk exposure, particularly its rate of return on equity capital and risk to shareholder earnings. A bank can raise its stock price by creating an expectation in the minds of investors of greater earnings in the future, by lowering the bank's perceived risk exposure, or by a combination of increases in expected earnings and reduced risk. (4) What makes it so difficult to correctly forecast interest rate changes?Interest rates cannot be set by an individual bank or even by a group of banks; they are determined by thousands of investors trading in the credit markets. Moreover, each market rate of interest has multiple components--the risk-free interest rate plus various risk premium. A change in any of these rate components can cause interest rates to change. To consistently forecast market interest rates correctly would require bankers to correctly anticipate changes in the risk-free interest rate and in all rate components. Another important factor is the timing of the changes. To be able to take full advantage of their predictions, they also need to know when the changes will take place.(6) What is a long hedge in financial futures? A short hedge?A long hedger offsets risk by buying financial futures contracts around the time new deposits are expected, when a loan is to be made, or when securities are added to the bank's portfolio. Later, as deposits and loans approach maturity or securities are sold, a like amount of futures contracts is sold. A short hedger offsets risk by selling futures contracts when the bank is expecting a large cash inflow in the near future. Later, as deposits come flowing in, a like amount of futures contracts is purchased.(7) What advantages do sales of loans have for lending institutions trying to raise funds?Loan sales permit a lending institution to get rid of less desirable or lower-yielding loans and allow them to raise additional funds. In addition, replacing loans that are sold with marketable securities can increase the liquidity of the lending institution.(8) What is a credit swap? For what kinds of situations was it developed?A credit swap is where two lenders agree to swap portions of the ir customer’s loan repayments. It was developed so that banks do not have to rely on one narrow market area. They can spread out the risk in the portfolio over a larger market area.(9) What kinds of assets are most amenable to the securitization process?The best types of assets to pool are high quality, fairly uniform loans, such as home mortgages or credit card receivables.(10) What are the principal sources from which the supply of liquidity comes?Supplies of funds stem principally from incoming deposits, sales of bank assets, particularly money market securities, and repayments of outstanding loans. Liquidity also comes from the sale of nondeposit services and borrowings from the money market(11) Which deposits are the least costly for depository institutions? The most costly?Commercial checkable deposits, particularly regular noninterest bearing demand deposits, are usually the least costly. The most costly deposits are passbook savings accounts having substantial deposit and withdrawal activity and higher interest-rate time deposits.(12) What are the most significant differences between Basel I and Basel II? Explain the importance of the concepts of internal risk assessment, V AR, and market disciplineBasel I used a one size fits all a pproach to determine a bank’s capital requirements. Basel II recognizes that different banks have different risk exposures and should be subject to different capital requirements. It also broadens the types of risk considered for determining capital requirements, including credit, market and operational risk. Internal risk assessment refers to an innovation in Basel II which allows banks to measure their own risk exposure. These measurements are subject to review by the regulators to ensure that they are reasonable. The V AR model is one of the models used to determine a bank’s risk exposure. It measures the price or market risk of a portfolio of assets whose value may decline due to adverse movements in the financial markets or interest rates. Market discipline refers to the market determining the bank’s risk exposure. In order to achieve that a bank would be required to issue subordinated debt. Since this debt is not guaranteed the buyers of these notes would be very vigilant about the issuing bank’s financial condition.4、Calculation(1) Suppose a bank has an allowance for loan losses of $1.25 million at the beginning of the year, charges current income for a $250,000 provision for loan losses, charges off worthless loans of $150,000, and recovers $50,000 on loans previously charged off. What will be the balance in the bank's allowance for loan losses at year-end?The balance in the allowance for loan loss (ALL) account at year end will be:Beginning ALL = $1.25 millionPlus: Annual Provisionfor Loan Losses = +0.25Recoveries onLoans Previously = +0.05Charged OffMinus: ChargeOffs of Worthless = -0.15LoansEnding ALL = $1.40 million(2) Suppose a bank has an ROA of 0.80 percent and an equity multiplier of 12x. What is its ROE? Suppose this bank's ROA falls to 0.60 percent. What size equity multiplier must it have to hold its ROE unchanged?The bank's ROE is:ROE = 0.80 percent *12 = 9.60 percent.If ROA falls to 0.60 percent, the bank's ROE and equity multiplier can be determined from:ROE = 9.60% = 0.60 percent * Equity MultiplierEquity Multiplier = 9.60 percent = 16x.0.60 percent(3) Suppose that a thrift institution has an average asset duration of 2.5 years and an average liability duration of 3.0 years. If the bank holds total assets of $560 million and total liabilities of $467 million, does it have a significant duration gap? If interest rates rise, what will happen to the value of the bank's net worth?Duration Gap = D A – D L * Assets s Liabilitie = 2.5 yrs. – 3.0 yrs. ⎪⎭⎫ ⎝⎛million $560million $467 = 2.5 years – 2.5018 years= -0.018 yearsThis bank has a very slight negative duration gap; so small in fact that we could consider it insignificant. If interest rates rise, the bank's liabilities will fall slightly more in value than its assets, resulting in a small increase in net worth.(4) A bank plans to borrow $55 million in the money market at a current interest rate of 4.5 percent. However, the borrowing rate will float with market conditions. To protect itself the bank has purchased an interest-rate cap of 5 percent to cover this borrowing. If money market interest rates on these funds suddenly climb to 5.5 percent as the borrowing begins, how much in total interest will the bank owe andhow much of an interest rebate will it receive assuming the borrowing is only for one month?Total Amount Interest Number of Months Interest Owed = Borrowed * Rate Charged * 12= $55 million x 0..055 x 112= $0.527 million or $252,083.33.How much of an interest rebate will the bank receive for its one-month borrowing?[]12MonthsofNumberxBorrowedAmt.xRateCap-RateInterestMarketRebateInterest == (.055 - .05) x $55 million x 112= $22,916.67.(5) Suppose a corporate bond an investment officer would like to purchase for her bank has a before-tax yield of 8.98 percent and the bank is in the 35 percent federal income tax bracket. What is the bond's after-tax gross yield? What after tax rate of return must a prospective loan generate to be competitive with the corporate bond? Does a loan have some advantages for a lending institution that a corporate bond would not have?After-tax Gross Yield on Corporate Bond = 8.98 %( 1 - 0.35) = 5.84%.A prospective loan must generate a comparable yield to that of the bond to be competitive. However, granting a loan to a corporation may have the added advantage of bringing in additional service business for the bank that merely purchasing a corporate bond would not do. In this case the bank would accept a somewhat lower yield on the loan compared to the bond in anticipation of getting more total revenue from the loan relationship due to the sale of other bank services. (6) Suppose that a thrift institution’s liquidity division estimates that it holds $19 million in hot money deposits and other IOUs against which it will hold an 80 percent liquidity reserve, $54 million in vulnerable funds against which it plans to hold a 25 percent reserve, and $112 million in stable or core funds against which it will hold a 5 percent liquidity reserve. The thrift expects its loans to grow 8 percent annually; its。