金融学第十三章

- 格式:docx

- 大小:10.10 KB

- 文档页数:2

第十三章货币供给案例13-1:2004年前三季度中国货币供给状况及金融宏观调控一、基本原理(一)金融宏观调控具有重要性1.实施宏观经济调控措施是一国政府着眼全局和长远发展做出的重大决策。

宏观调控主要依托于一国货币政策和财政政策的配合和协调。

对货币政策来说,如何实现货币供给的合理、稳健是保证货币供求的真正、持久平衡和实现整个宏观调控有效的关键所在。

2.货币政策宏观调控要走市场化路子,主要运用经济和法律手段,辅之以必要的行政手段。

货币政策的宏观调控走向市场化,才能充分运用市场调控手段,充分发挥资源配置的市场机制功能,通过企业的市场反应实现对宏观经济的有效调控,也才能从根本上解决经济结构、结构体制和经济增长方式问题。

反过来,一国金融宏观调控模式的基本特征,主要取决于该国经济市场化程度,尤其取决于一国金融组织结构、金融市场的发育程度。

(二)金融宏观调控具有复杂性1.对货币政策宏观调控的难度要有充分认识。

特别是我国正处于体制转轨和经济加速发展时期,经济生活中的问题有其特殊的复杂性,解决这些问题也需要有个过程。

所以在具体实施中的手段运用、成本与收益、目标之间以及短期长期等方面必须做出合理且可行的权衡。

2.宏观调控从表面看来是央行和财政当局的事,实际上它牵涉到方方面面、上下左右,是整个国民经济的问题,是一个庞大的系统工程,它涉及到信贷投放和土地供给、资源利用、投资项目审批和清理、经济增长方式的转换、速度和质量的统一、保护环境、企业改革、加强信息化建设等等一系列问题。

所以说,宏观调控不仅是中央的事,不仅是财政银行高层的事,它对地方、部门和企业来说既是挑战和压力,也是机遇和动力。

3.要用积极的办法科学合理地进行调控。

要坚持实事求是,对症下药。

宏观调控中要注重“调整结构”,不要“只压总量”;要“点刹车”,不要“急刹车”;要“切一刀”,不要“一刀切”。

要做到全面分析,准确把握,顺势而为,量力而行,讲求实效,狠抓落实。

国开金融学第十三章在金融市场的运行中,风险与监管是两个永恒的主题。

金融市场的发展和运行,不仅需要有效的风险管理机制,同时也需要合理的监管制度。

国开金融学第十三章将深入探讨金融市场的风险与监管,帮助读者理解这两个重要概念,并分析其在实际金融市场中的应用。

金融市场风险的种类:包括市场风险、信用风险、流动性风险和操作风险等。

这些风险在金融市场的日常运行中都有可能出现,对投资者和金融机构产生影响。

金融市场风险的特点:金融市场风险具有复杂性和不确定性的特点。

这种风险可能源自市场变量的不确定性,也可能源自投资者对风险的认知不足。

金融市场风险的测量:通过运用各种金融工具和风险管理技术,我们可以对金融市场风险进行定量和定性分析。

常用的风险管理工具包括期权、期货、掉期等。

金融市场监管的目标:保护投资者权益、维护市场公平和透明度、促进金融稳定和系统安全。

金融市场监管的原则:依法监管、公开公正、独立性和效率。

这些原则旨在确保监管行为的有效性和公正性。

金融市场监管的手段:包括法律手段、经济手段和行政手段。

其中,法律手段是最基本和最重要的手段,它通过制定和执行相关法律法规来规范市场行为。

在本部分,我们将选取几个具有代表性的金融市场风险与监管案例进行分析。

这些案例将有助于我们更好地理解理论,并将其应用于实际场景。

国开金融学第十三章的学习,使我们深入理解了金融市场的风险与监管。

对于金融机构来说,建立和完善风险管理制度,加强内部风险控制,是确保业务稳健发展的关键。

政府和监管机构也需要根据市场变化及时调整监管策略,以维护市场的公平与透明,保护投资者的权益。

国开金融市场行测题库,是国开证券公司为了测试投资者对金融市场的了解程度和投资技能而设立的。

这个题库包含了各种类型的题目,从基础知识到高级策略,旨在全方位地评估投资者的能力。

国开金融市场行测题库的题目涵盖了金融市场的各个方面,包括但不限于金融市场的基本概念、投资策略、风险管理、金融产品分析等。

《金融学》目录第一章金融概述11 金融的定义与范畴12 金融在现代经济中的作用13 金融体系的构成要素第二章货币与货币制度21 货币的起源与发展22 货币的职能23 货币的形态演变24 货币制度的类型与构成要素25 国际货币体系第三章信用与利息31 信用的含义与形式32 信用工具33 利息与利率的概念34 利率的决定因素与作用35 利率的计算方法第四章金融市场41 金融市场的分类与功能42 货币市场43 资本市场44 金融衍生工具市场45 金融市场的监管第五章金融机构51 金融机构体系的构成52 商业银行53 中央银行54 政策性银行55 非银行金融机构第六章商业银行的业务61 负债业务62 资产业务63 中间业务64 商业银行的风险管理第七章中央银行与货币政策71 中央银行的职能与地位72 货币政策的目标与工具73 货币政策的传导机制74 货币政策的效果评估第八章国际金融81 外汇与汇率82 汇率的决定与影响因素83 国际收支84 国际储备85 国际金融市场与国际资本流动第九章金融风险管理91 金融风险的类型与特征92 金融风险的识别与评估93 金融风险的防范与控制94 金融监管与金融稳定第十章金融创新与金融发展101 金融创新的含义与动力102 金融创新的主要内容与影响103 金融发展的理论与实践104 金融发展与经济增长的关系第十一章金融与科技111 科技对金融的影响112 金融科技的应用领域113 金融科技带来的挑战与机遇第十二章行为金融学121 行为金融学的基本概念122 投资者的心理与行为偏差123 行为金融学在投资决策中的应用第十三章金融伦理与社会责任131 金融伦理的内涵与原则132 金融机构的社会责任133 金融伦理与社会责任的实践案例。

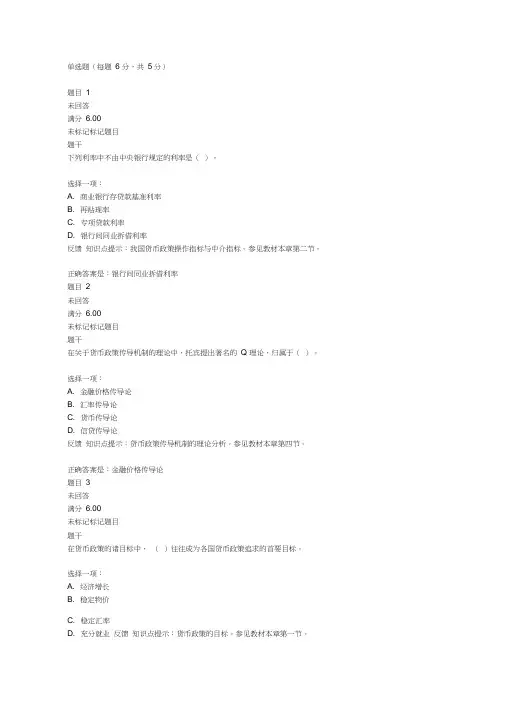

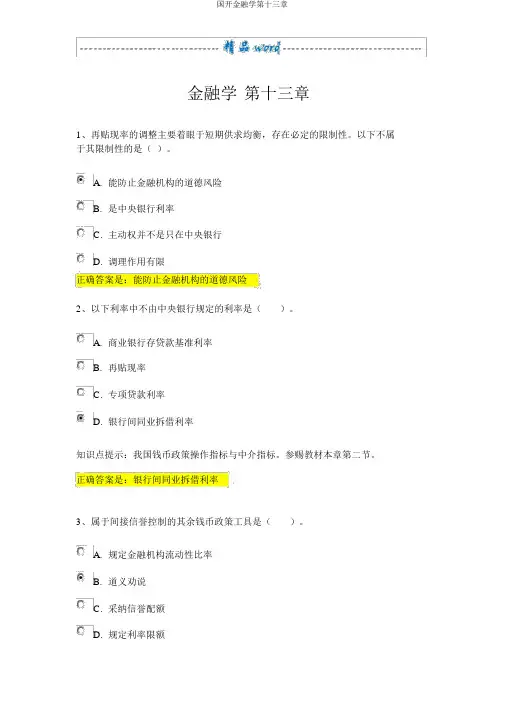

金融学第十三章1、再贴现率的调整主要着眼于短期供求均衡,存在必定的限制性。

以下不属于其限制性的是()。

A.能防止金融机构的道德风险B.是中央银行利率C.主动权并不是只在中央银行D.调理作用有限正确答案是:能防止金融机构的道德风险2、以下利率中不由中央银行规定的利率是()。

A.商业银行存贷款基准利率B.再贴现率C.专项贷款利率D.银行间同业拆借利率知识点提示:我国钱币政策操作指标与中介指标。

参赐教材本章第二节。

正确答案是:银行间同业拆借利率3、属于间接信誉控制的其余钱币政策工具是()。

A.规定金融机构流动性比率B.道义劝说C.采纳信誉配额D.规定利率限额反应知识点提示:其余钱币政策工具。

参赐教材本章第三节。

正确答案是:道义劝说4、保持()稳固是保证市场经济中价钱体制发挥作用的前提。

A.利率B.币值C.汇率D.国际进出正确答案是:币值5、在对于钱币政策传导体制的理论中,托宾提出有名的Q 理论,归属于()。

A.汇率传导论B.信贷传导论C.钱币传导论D.金融价钱传导论知识点提示:钱币政策传导体制的理论剖析。

参赐教材本章第四节。

正确答案是:金融价钱传导论6、公然市场业务政策的优胜性有()。

A.主动性强B.灵巧性强C.调控成效缓和,震动性小D.影响范围广E.通告效应强知识点提示:一般性钱币政策工具。

参赐教材本章第三节。

正确答案是:主动性强 ,灵巧性强,调控成效缓和,震动性小,通告效应强7、其余钱币政策工具中,属于直接信誉控制的是()。

A.采纳信誉配额B.不动产信誉控制C.规定金融机构流动性比率D.规定利率限额E.直接干涉知识点提示:其余钱币政策工具。

参赐教材本章第三节。

正确答案是:采纳信誉配额 , 规定金融机构流动性比率 , 规定利率限额 , 直接干涉8、以下属于选择性钱币政策工具的是()。

A.不动产信誉控制B.花费信誉控制C.优惠利率D.预缴入口保证金E.证券市场信誉控制知识点提示:选择性钱币政策工具。

参赐教材本章第三节。

《⾦融学(第⼆版)》讲义⼤纲及课后习题答案详解⼗三章CHAPTER 13THE CAPITAL ASSET PRICING MODELObjectivesExplain the theory behind the CAPM.Explain how to use the CAPM to establish benchmarks for measuring the performance of investment portfolios. Explain how to infer from the CAPM the correct risk-adjusted discount rate to use in discounted-cash-flow valuation models. Explain the APT and its relationship to the CAPM.Outline13.1 The Capital Asset Pricing Model in Brief13.2 Determinants of the Risk Premium on the Market Portfolio13.3 Beta and Risk Premiums on Individual Securities13.4 Using the CAPM in Portfolio Selection13.5 Valuation and Regulating Rates of Return13.6 Extensions, Modifications, and Alternatives to the CAPMSummaryThe CAPM has three main implications:In equilibrium, ev eryone’s relative holding of risky assets are the same as in the market portfolio.The size of the risk-premium of the market portfolio is determined by the risk-aversion of investors.The risk premium on any asset is equal to its beta times the risk premium on the market portfolio.Whether or not the CAPM is strictly true, it provides a rationale for a very simple passive portfolio strategy: Diversify your holdings of risky assets in the proportions of the market portfolio, andMix this portfolio with the risk-free asset to achieve a desired risk-reward combination.The CAPM is used in portfolio management primarily in two ways:To establish a logical and convenient starting point in asset allocation and security selectionTo establish a benchmark for evaluating portfolio management ability on a risk-adjusted basis.In corporate finance the CAPM is used to determine the appropriate risk-adjusted discount rate in valuation models of the firm and in capital budgeting decisions. The CAPM is also used to establish a “fair” rate of return on invested capital for regulated firms and in cost-plus pricing.Today few financial scholars consider the CAPM in its simplest form to be an accurate model for explaining or predicting risk premiums on risky assets. However, modified versions of the model are still a central feature of the theory and practice of finance.The APT gives a rationale for the expected return-beta relationship that relies on the condition that there be no arbitrage profit opportunities; the CAPM requires that investors be portfolio optimizers. The APT and CAPM are not incompatible; rather, they complement each other.Solutions to Problems at End of ChapterComposition of the Market Portfolio1. Capital markets in Flatland exhibit trade in four securities, the stocks X, Y and Z, and a risklessgovernment security. Evaluated at current prices in US dollars, the total market values of these assets are, respectively, $24 billion, $36 billion, $24 billion and $16 billion.a. Determine the relative proportions of each asset in the market portfolio.b. If one trader with a $100,000 portfolio holds $40,000 in the riskless security, $15,000 in X, $12,000 in Y, and$33,000 in Z, determine the holdings of the three risky assets of a second trader who invests $20, 000 of a $200, 000 portfolio in the riskless security.SOLUTION:The total value of all assets in the economy is 100 billion dollars. a. The proportions of each asset relative to the value of all assets are, respectively, .24 (X), .36 (Y),b. .24 (Z) and .16 (riskless bond.) The proportions of each risky asset to the total value of all risky assets are, respectively, (2/7) (X), (3/7) (Y) and (2/7) (Z).c. . Ignore the question as it appears in the First Edition of the textbook. Instead, the question should be: If aninvestor has $100,000 with $30,000 invested in the riskless asset, how much is invested in securities X, Y, and Z? The answer to this question is $20,000 in X and Z, and $30,000 in Y.Implications of CAPM2. The riskless rate of interest is .06 per year, and the expected rate of return on the market portfolio is .15 per year.a. According to the CAPM , what is the efficient way for an investor to achieve an expected rate of returnof .10 per year?b. If the standard deviation of the rate of return on the market portfolio is .20, what is the standarddeviation on the above portfolio?c. Draw the CML and locate the foregoing portfolio on the same graph.d. Draw the SML and locate the foregoing portfolio on the same graph.e. Estimate the value of a stock with an expected dividend per share of $5 this coming year, an expecteddividend growth rate of 4% per year forever, and a beta of .8. If its market price is less than the value you have estimated, i.e., if it is under-priced, what is true of its mean rate of return?SOLUTION: a.So one would hold a portfolio that is 4/9 invested in the market portfolio and 5/9 in the riskless asset. b.c. The formula for the CML is9415.)1(06.10.)()1()(=+-=?+-?=x xx x r E x r r E M f 08889.)20(.94==?=M x σσσσσ45.06.)()(+=-+=MfM f r r E r r Ed. The formula for the SML ise. Use constant growth rate DDM and find r using the SML relationIf the market price of the stock is less than this, then its expected return is higher than the 13.2% required rate.()ββ09.06.)()(+=-+=f M f r r E r r E 35.54$04.132.504.510=-=-=-=r g r D P 132.8.09.06.09.06.=?+=+=βr3. If the CAPM is valid, which of the following situations is possible? Explain. Consider each situation independently. a.PortfolioExpected ReturnBeta A 0.20 1.4B 0.25 1.2b.PortfolioExpected ReturnStandard DeviationA 0.300.35B 0.400.25c.Portfolio Expected ReturnStandard DeviationRisk-free 0.100Market 0.180.24A 0.160.12d.Portfolio Expected ReturnStandard DeviationRisk-free 0.100Market 0.180.24A0.200.22SOLUTION:a. Impossible. Since the risk premium on the market portfolio is positive, a security with a higher beta must have ahigher expected return.b. Possible. Since portfolios A & B are not necessarily efficient, A can have a higher standard deviation and alower expected return than B.c. Impossible. Portfolio A lies above the CML, implying that the CML is not efficient. If the standard deviation ofA is .12, then according to the CML its expected return cannot be greater than .14.d. Impossible. Portfolio A has a lower standard deviation and a higher mean return than the market portfolio,implying that the market portfolio is not efficient.4. If the Treasury bill rate is currently 4% and the expected return to the market portfolio over the same period is 12%, determine the risk premium on the market. If the standard deviation of the return on the market is .20, what is the equation of the Capital Market Line?SOLUTION: The risk premium on the market portfolio is .08. The slope of the CML is .08/.2 = .4. Thus, the equation of the CML is:Determinants of the Market Risk Premium5. Consider an economy in which the expected return on the market portfolio over a particular period is .25, the standard deviation of the return to the market portfolio over this same period is .25, and the averagedegree of risk aversion among traders is 3. If the government wishes to issue risk-free zero-coupon bonds with a term to maturity of one period and a face value per bond of $100,000, how much can the government expect to receive per bond? []σσσ4.04.)()(+=++=MfMf r rE r r ESOLUTION:According to the CAPM, E(r M) - r f = Aσ2, so that r f = E(r M) - Aσ2.Substituting into this formula we find: r f = .25 – 3 x .252 = .0625Therefore the revenue raised by the government per bond issued is $100,000 = $94,117.651.06256. . Norma Swanson has invested 40% of her wealth in MGM stock and 60% in Industrial Light and Magic stock. Norma believes the returns to these stocks have a correlation of .06 and that their respective means and standard deviations are: MGM ILMExpected Return (%) 10 15Standard Deviation (%) 15 25a.Determine the expected value and standard deviation of the return on Norma’s portfolio.b.Would a risk-averse investor such as Norma prefer a portfolio composed entirely of only MGM stock? Ofonly ILM stock? Why or why not?SOLUTION:a.The expected return is .13, and the standard deviation is .1649.b. A risk averse investor will not want to hold a portfolio composed entirely of MGM or of ILM stock, becauseone can, in general, achieve the same expected return with a lower standard deviation by combining a portfolio of MGM and ILM with the risk-free asset.7. Consider a portfolio exhibiting an expected return of 20% in an economy in which the riskless interest rate is 8%, the expected return to the market portfolio is thirteen percent, and the standard deviation of the return to the market portfolio is .25. Assuming this portfolio is efficient, determine:a.its beta.b.the standard deviation of its return.c.its correlation with the market return.SOLUTION:/doc/ad5801fd700abb68a982fb59.html e the security market line to infer that the beta of this portfolio is 2.4:.20 = .08 + β(.13 - .08)β = (.20 - .08)/(.13 - .08) = .12/.05 = 2.4/doc/ad5801fd700abb68a982fb59.html e the capital market line to infer that the standard deviation of the yield to this portfolio is .6:.20 = .08+ (.13 - .08) σ = .08+ .2 σ.25σ = .12/.2 = .6c.By definition the following relationships hold:β = cov/σ2Mρ = covσiσMwhere ρ denotes the correlation coefficient. We know that β = 2.4, σM = .25, and σi = .6.So from the definition of β, we get that the cov is 2.4 x .252 = .15. Substituting this into the definition of ρ: ρ = cov = .15 __ = 1σiσM .6 x .25Application of CAPM to Corporate Finance8. . The Suzuki Motor Company is contemplating issuing stock to finance investment in producing a new sports-utility vehicle, the Seppuku. Financial analysts within Suzuki forecast that this investment will have precisely the same risk as the market portfolio, where the annual return to the market portfolio is expected to be 15% and the current risk-free interest rate is 5%. The analysts further believe that the expected return to the Seppuku project will be 20% annually. Derive the maximal beta value that would induce Suzuki to issue the stock.SOLUTION:The project would be on the borderline if its required return were 20% per year. Since the risk-free rate is 5% and the risk premium on the market portfolio is 10%, the required return would be 20% if the beta were 1.5.9. . Roobel and Associates, a firm of financial analysts specializing in Russian financial markets, forecasts that the stock of the Yablonsky Toy Company will be worth 1,000 roubles per share one year from today. If the riskless interest rate on Russian government securities is 10% and the expected return to the market portfolio is 18% determine how much you would pay for a share of Yablonsky stock today if:a.the beta of Yablonsky is 3.b.the beta of Yablonsky is 0.5.SOLUTION:Use the security market line in each case to determine a required rate of return, then infer the current price from the forecasted price of 1,000 roubles and the required rate of return you have determined.a.If beta is 3, the required return is .10+ 3x.08 = .34. You would pay 1,000/1.34 = 746.27 roubles;b.If beta is .5, the required return is .10+ .5x.08 = .14. You would pay 1,000/1.14 = 877.19 roubles.Application of CAPM to Portfolio Management10. Suppose that the stock of the new cologne manufacturer, Eau de Rodman, Inc., has been forecast to havea return with standard deviation .30 and a correlation with the market portfolio of .9. If the standard deviation of the yield on the market is .20, determine the relative holdings of the market portfolio and Eau de Rodman stock to form a portfolio with a beta of 1.8.SOLUTION: By definition:β = cov/σ2Mρ = covσrσMTherefore, β = ρσr/σM. The beta of Rodman stock is therefore .9x.3/.2 = 1.35.The beta of a portfolio is a weighted average of the betas of the component securities. Let A be a fraction of the portfolio invested in Rodman stock to produce a beta of 1.8. Then we have:1.35A + (1-A) = 1.8.35A = .8A = 2.286So the portfolio would have to have 228.6% invested in Rodman stock and a short position in the market portfolio equal to 128.6%.11. The current price of a share of stock in the Vo Giap Clothing Company of Vietnam is 50 dong and its expected yield over the year is 14%. The market risk premium in Vietnam is 8% and the riskless interest rate 6%. What would happen to the stock’s current price if its expected future payout remains co nstant while the covariance of its rate of return with the market portfolio falls by 50%?SOLUTION:Deduce that the expected future price of a share of Vo Giap is 57 dong, so that a reduction in this stock’s beta of 50% implies, by the security market relation, that the required yield on Vo Giap is now 10%, so that its current share price rises by 3.64% toa new value of 51.82 dong.12. Suppose that you believe that the price of a share of IBM stock a year from today will be equal to the sumof the price of a share of General Motors stock plus the price of a share of Exxon, and further you believethat the price of a share of IBM stock in one year will be $100 whereas the price of a share of General Motors today is $30. If the annualized yield on 91-day T-bills (the riskless rate you use) is 5%, the expected yield on the market is 15%, the variance of the market portfolio is 1, and the beta of IBM is 2, what price would you be willing to pay for one share of Exxon stock today?SOLUTION:Expected return = .05 + 2(.15 - .05) = 25%; (100 - x)/x = .25 → x = $80Deduce that the current price of a share of IBM stock is $80, so that the upper bound on the price of a share of Exxon is ($80 -$30 = $50).13. Ascertain whether the following quotation is true or false, and state why:“When arbitrage is absent from financial markets, and investors are each concerned with only the risk and return to their portfolios, then each investor can eliminate all the riskiness of his investments through diversification, and as a consequence the expected yield on each available asset will depend only on the covariance of its yield with the covariance of the yield on the diversified portfolio of risky assets each investor holds.”SOLUTION:False. You cannot eliminate all risk through diversification, only the unsystematic risk.Application of CAPM to Measuring Portfolio Performance14. During the most recent 5-year period, the Pizzaro mutual fund earned an average annualized rate of return of 12% and had an annualized standard deviation of 30%. The average risk-free rate was 5% per year. The average rate of return in the market index over that same period was 10% per year and the standard deviation was 20%. How well did Pizzaro perform on a risk-adjusted basis?SOLUTION:Compute the ratio of average excess return to standard deviation for Pizzaro and compare it to that of the market portfolio: Pizzaro risk-adjusted performance ratio = (.12-.05)/.30 = .233Market portfolio risk-adjusted performance ratio = (.1-.05)/.2 = .250So, on a risk-adjusted basis, Pizzaro did worse than the market index.Challenge ProblemCAPM with only 2 Risky Assets15. There are only two risky assets in the economy: stocks and real estate and their relative supplies are 50% stocks and 50% real estate. Thus, the market portfolio will be half stocks and half real estate. The standard deviations are .20 for stocks, .20 for real estate, and the correlation between them is 0. The coefficient of relative risk aversion of the average market participant (A) is 3. r f is .08 per year.a.According to the CAPM what must be the equilibrium risk premium on the market portfolio, on stocks,and on real estate?b.Draw the Capital Market Line. What is its slope? Where is the point representing stocks located relativeto the CML?c.Draw the SML. What is its formula? Where is the point representing stocks located relative to the SML? SOLUTION: a.The market portfolio consists of half stocks and half real estate. It has a standard deviation of .1414, computedas follows:σ2M = w2σ2s + (1-w)2σ2r+ 2 w(1-w) cov s,rσ2M = 2 x (1/2)2 .22 = .02σM = .1414The equilibrium risk premium on the market portfolio is E(r M)-r f = Aσ2M = 3x.02 = .06.The market portfolio’s expected rate of return is also a weighted average of the expected rates of return on stocks and real estate, where the weights are each 1/2. Stocks and real estate must have the same risk premiumbecause they have the same standard deviation and correlation with the market. Therefore the risk premium on stocks and real estate must be .06, the same as the market portfolio’s risk premium.b.The slope of the CML is .06/.1414 = .424. The point representing stocks is M, it is to the right of the CML.equaling to 1.The formula is: E(r) = r f + (E(r M) –r f).。

第十三章货币需求一、名词解释1. 货币需求2. 费雪交易方程式3. 预防动机4. 流动性陷阱5. 流动性偏好6. 货币需求函数7. 恒久性收入8. 持有货币的机会成本二、不定项选择1.在正常情况下,市场利率与货币需求成( )。

A、正相关B、负相关C、正负相关都可能D、不相关2. 根据凯恩斯流动性偏好理论,当预期利率上升时,人们就会( )。

A、抛售债券而持有货币B、抛出货币而持有债券C、只持有货币D、只持有债券3.M=KPY是属于( )的理论。

A、现金交易说B、现金余额说C、可贷资金说D、流动性偏好说4.以下( )属于弗里德曼的货币数量说。

A、利率是货币需求的重要决定因素。

B、人们资产选择的原则是效用极大化。

C、“恒久性收入”概念是一个不包括人力资本在内的纯物质化的概念。

D、货币数量说首先是一种货币需求理论,其次才是产出、货币收入或物价水平的理论。

5. 凯恩斯在其货币需求分析中,认为人们对货币的需求行为是由三种动机决定的:( )。

A、交易动机B、预防动机C、投机动机D、投资动机6. 下列属于货币需求函数中的机会成本变量的有:()。

A、债券的预期收益率B、股票的预期收益率C、实物资产的预期收益率D、货币本身的收益率7. 下列从微观角度分析货币需求的是()A、费雪方程式B、剑桥方程式C、凯恩斯货币需求模型D、费里德曼货币需求函数8. 在弗里德曼货币需求理论中,总财富分为()。

A、人力财富B、非人力财富C、现金财富D、资产财富三、判断题1. 货币需求就是人们持有货币的愿望,而不考虑人们是否有足够的能力来持有货币。

()2. 在现金余额说中,k为以货币形式持有的收入与财富占总收入与总财富的比例。

()3. 利率上升债券价格将会下降。

()4. 弗里德曼认为,在总财富中人力财富所占的比例越大,出于谨慎动机的货币需求越小。

()5. 名义货币需求与实际货币需求的区别在于是否剔除了物价变动的影响。

()四、简答题1. 简要比较费雪方程式与剑桥方程式。

《金融学》第十三章通货膨胀与通货紧缩—、单项选择题(本大题共20小题,每小题1分,共20分' 在每小题列出的四个备选答案中只有一个是最符合题目要求的,请将其代码分别填写在下列表格中。

错选、多选、漏选或未选记分X1 •通货膨胀表现为物价水平上涨,这里〃物价水平"是指A •个别商品物价B •地区商品物价C・一般物价水平 D •特种商品价格2•发生温和式通货膨胀时,特价水平大约在A・1%左右B・2.5%左右C・5左右D・10左右3. 大多数国家用来衡量通货膨胀的指标是A・消费物价指数B・批发物价指数C・工业物价指数D・国民生产总值平减指数4 •能够较为全面反映总体物价水平变化趋势的指标是A・消费物价指数B・批发物价指数C・工业物价指数D・国民生产总值平减指数5•关于"通货膨胀"描述正确的是A・通货膨胀就是物价上涨B. 通货膨胀就是货币供给过多C. 通货膨胀就是总体物价水平持续上涨D・通货膨胀就是总体物价水平持续明显上涨6. 认为通货膨胀的原因在于经济发展过程中社会总需求大于总供给,从而引起一般物价水平持续上涨”这种理论是A・需求拉上论B・成本推进论C结构失衡论D・外国输入论7. 把通货膨胀归咎于产品成本提高的是A・凯恩斯主义B・后凯恩斯学派C・现代货币主义D・马克思主义8・通货膨胀对策中,通过公开市场业务出售政府债券属于A・控制需求B・改善供给C・收入指数化政策D・紧缩性财政政策9. 通货膨胀对策中,冻结工资和物价属于A・控制需求B・改善供给C・收入指数化政策D・紧缩性财政政策10. 通货紧缩的特点是A.部分物价持续下跌B.总体物价持续下降C・地区价格差距拉大D・商品价格波动性加大口・通货膨胀的含义特别强调物价A・季节性波动 B.持续性上涨 C.规律性上涨 D.调节性上涨12 •出现抑制型通货膨胀的原因是A •价格双轨制B.市场定价 C.官方定价 D.行业定价13 •国际传播型通货膨胀的价格传导途径是A・商品进口B.商品出口 C.资本流入 D.资本流出14.通货膨胀对生产产生破坏作用的机理是A .商品供大于求 B.商品供不应求 C.价格异常波动D.价格的混舌闲扭曲15•当发生恶性通货膨胀时,公众应该更多地持有A .存款 B.证券 C.房地产D.黄金如果通货膨胀高于名义收益率,那么实际收益率A・大于零B.等于零C.小于零 D.无法确定17•当发生通货膨胀时,消费者最好A •增加消费 B.减少消费 C.信用消费 D.增加储蓄抑制通货膨胀采取的紧缩性货币政策是A・提高法定存款准备金 B.增加现钞发行C.降低提现率D.降低利率19.实行扩张的收入政策以缓解通货紧缩的矛盾,主要是增加A・高收入居民收入B.中等收入居民收入C低收入居民收入 D.中低收入居民收入20•在缓解通货紧缩问题而实施的扩张性财政政策中,能起到"立竿见影〃效果的是A •减少税收 B.提高税率 C.增加财政支出 D.减少财政开支二、多项选择题(本大题共10小题,每小题1.5分,共15分L在每小题列出的五个备选答案中有二至五个是符合题目要求的,请将其代码分别填写在下列表格中。

金融学(本)第十三章的形考题及答案注意:选项(abcd)后面数字是一道题对这题的的评分,也就是答案,如果是0,是错误的,.就不要选择。

top/第十三章--单选题单选题在货币政策目标的选择的争论中,主张单一目标论的观点认为,()应该作为货币政策的唯一目标。

A. 稳定物价100B. 充分就业0C. 经济增长0D. 稳定汇率0单选题货币政策可选择的操作指标主要包括()。

A. 基础货币和利率0B. 准备金和利率0C. 超额准备金和再贴现率0D. 准备金和基础货币100单选题下列变量中不可作为货币政策中介指标的金融变量是()。

A. 同业拆借利率0B. 汇率0C. 货币供应量0D. 再贴现利率100单选题目前,我国以下各种利率中不由中央银行规定的是()。

A. 银行间同业拆借利率100B. 再贴现率0C. 商业银行存贷款基准利率0D. 专项贷款利率0单选题中央银行在其与商业银行的往来中,对商业银行的季度贷款额度附加规定,否则中央银行便削减甚至停止向商业银行提供再贷款,这种政策手段称为()。

A. 道义劝告0B. 再贷款和再贴现0C. 窗口指导100D. 信用控制0单选题凯恩斯主义和货币主义的在货币传导机制中的争论主要集中在对()认识的不同。

A. 货币需求的利率弹性100B. 总需求的利率弹性0C. 货币的真实余额效应0D. 货币流通速度的稳定性0单选题下列可能影响货币政策内部时滞的因素是()。

A. 货币政策流通速度的变化0B. 中央银行需要采取行动的认识时间100C. 非金融部门微观主体的预期0D. 金融机构信贷活动的速度0单选题下列何种政策配合可以对经济结构进行调节,一方面保持物价水平和总产出的稳定,另一方面使得政府投资下降,私人投资上升。

()A. 紧财政和紧货币的政策0B. 松财政和松货币的政策0C. 紧财政和松货币的政策100D. 松财政和紧货币的政策0单选题在货币政策最终目标中,相互之间关系一致的是()。

货币金融学·第十三章利息理论引言利息是货币金融学中一个重要的概念,涉及到资金的借贷和投资等方面。

在第十三章中,我们将对利息理论进行详细的探讨。

本文将从利息的定义、影响利息的因素以及利息理论的发展等方面进行介绍,以帮助读者更好地理解和掌握利息理论。

利息的定义利息是指在借贷资金的过程中,贷方向借方收取的一定的费用。

在现代货币经济中,利息是货币资金的价格,反映了资金的使用价值。

利息的支付方式通常有两种,即正回现和负回现。

正回现是指在借贷期限结束时一次性支付全部利息和本金,负回现则是在借贷期限内按一定时间间隔支付利息,到期一次性支付全部本金。

影响利息的因素利息的形成和决定受到多种因素的影响,下面将介绍一些主要的因素:1. 供求关系资金的供求关系是影响利息的关键因素之一。

当资金供应相对紧缺,需求相对旺盛时,利率往往会上升;反之,当资金供应相对充裕,需求相对不旺时,利率会下降。

2. 通货膨胀率通货膨胀率也对利息产生影响。

通常情况下,通货膨胀率越高,利率越高。

这是因为通货膨胀会导致货币贬值,借款人在还款时所偿还的债务相对减少,因此,贷款人要求较高的利息来弥补货币贬值所带来的损失。

3. 政府政策政府的货币政策也是影响利率的重要因素。

通过调整货币供应量和利率,政府可以影响市场上资金的供求关系,从而对利率产生调控作用。

4. 风险风险水平也会对利息产生影响。

一般来说,风险越高,利息也会越高,以作为对风险的补偿。

借款人的信用状况、还款能力以及所进行的投资项目等都会对风险水平产生影响。

利息理论的发展随着时间的推移和学术研究的不断深入,人们对于利息的理解和认识也在不断演化。

以下是一些利息理论的发展概述:1. 时期结构理论时期结构理论强调了长期利率和短期利率之间的关系。

根据时期结构理论,长期利率通常会高于短期利率,这是因为长期借款涉及到更多的风险,借款人要求更高的利率来对冲风险。

2. 流动性偏好理论流动性偏好理论认为,人们通常更倾向于持有流动性较高的资产,而非流动性较高的资产。

金融学第十三章1、再贴现率的调整主要着眼于短期供求均衡,存在一定的局限性。

下列不属于其局限性的是()。

A. 能避免金融机构的道德风险 B. 是中央银行利率 C. 主动权并非只在中央银行 D. 调节作用有限正确答案是:能避免金融机构的道德风险2、下列利率中不由中央银行规定的利率是()。

A. 商业银行存贷款基准利率 B. 再贴现率 C. 专项贷款利率 D. 银行间同业拆借利率知识点提示:我国货币政策操作指标与中介指标。

参见教材本章第二节。

正确答案是:银行间同业拆借利率3、属于间接信用控制的其他货币政策工具是()。

A. 规定金融机构流动性比率 B. 道义劝告 C. 采用信用配额 D. 规定利率限额反馈知识点提示:其他货币政策工具。

参见教材本章第三节。

正确答案是:道义劝告4、保持()稳定是保证市场经济中价格机制发挥作用的前提。

A. 利率 B. 币值 C. 汇率 D. 国际收支正确答案是:币值5、在关于货币政策传导机制的理论中,托宾提出着名的Q 理论,归属于()。

A. 汇率传导论 B. 信贷传导论 C. 货币传导论 D. 金融价格传导论知识点提示:货币政策传导机制的理论分析。

参见教材本章第四节。

正确答案是:金融价格传导论6、公开市场业务政策的优越性有()。

A. 主动性强 B. 灵活性强 C. 调控效果和缓,震动性小 D. 影响范围广 E. 告示效应强知识点提示:一般性货币政策工具。

参见教材本章第三节。

正确答案是:主动性强, 灵活性强, 调控效果和缓,震动性小, 告示效应强7、其他货币政策工具中,属于直接信用控制的是()。

A. 采用信用配额 B. 不动产信用控制 C. 规定金融机构流动性比率 D. 规定利率限额 E. 直接干预知识点提示:其他货币政策工具。

参见教材本章第三节。

正确答案是:采用信用配额, 规定金融机构流动性比率, 规定利率限额, 直接干预8、下列属于选择性货币政策工具的是()。

A. 不动产信用控制 B. 消费信用控制 C. 优惠利率 D. 预缴进口保证金 E. 证券市场信用控制知识点提示:选择性货币政策工具。

参见教材本章第三节。

正确答案是:不动产信用控制, 消费信用控制, 优惠利率, 预缴进口保证金, 证券市场信用控制9、1994 年《国务院关于金融体制改革的决定》明确提出,我国货币政策中介指标主要包括()。

A. 货币供应量 B. 信用总量 C. 商业银行贷款总量 D. 同业拆借利率 E. 银行超额准备金率知识点提示:我国货币政策的操作指标与中介指标。

参见教材本章第二节。

正确答案是:货币供应量, 信用总量, 同业拆借利率, 银行超额准备金率10、货币政策目标包括()。

A. 金融稳定

B. 充分就业

C. 经济增长

D. 国际收支平衡

E. 稳定币值知识点提示:货币政策的目标。

参见教材本章第一节。

正确答案是:金融稳定, 充分就业, 经济增长, 国际收支平衡, 稳定币值11、利率作为货币政策的中介指标,优点是可测性和相关性都较强,但抗干扰性较差。

对错知识点提示:可作为中介指标的金融变量。

参见教材本章第二节。

正确的答案是“对”。

12、从中央银行采取行动到对政策目标产生影响所经过的时间称之为行动时滞。

对错知识点提示:货币政策时滞。

参见教材本章第四节。

答

案解析:是外部时滞。

正确的答案是“错”。

13、货币传导论认为,货币政策操作以后,传导主要是通过金融资产价格和信贷渠道完成。

对错知识点提示:货币政策传导机制的理论分析。

参见教材本章第四节。

答案解析:货币传导论认为主要通过货币量的变化传导。

正确的答案是“错”。

14、菲利普斯曲线表明物价稳定和充分就业这两个货币政策目标之间存在此消彼长的关系;但是,自然律假说反对这种观点,提出物价稳定和充分就业之间并不矛盾。

对错知识点提示:货币政策诸目标的关系。

参见教材本章第一节。

正确的答案是“对”。

15、量化宽松的货币政策以利率是零或负值为基本特征。

对错知识点提示:量化宽松的货币政策。

参见教材本章第五节。

答案解析:量化宽松的货币政策以“货币数量扩张”为主要特征。

正确的答案是“错”。