外文翻译

- 格式:doc

- 大小:115.50 KB

- 文档页数:13

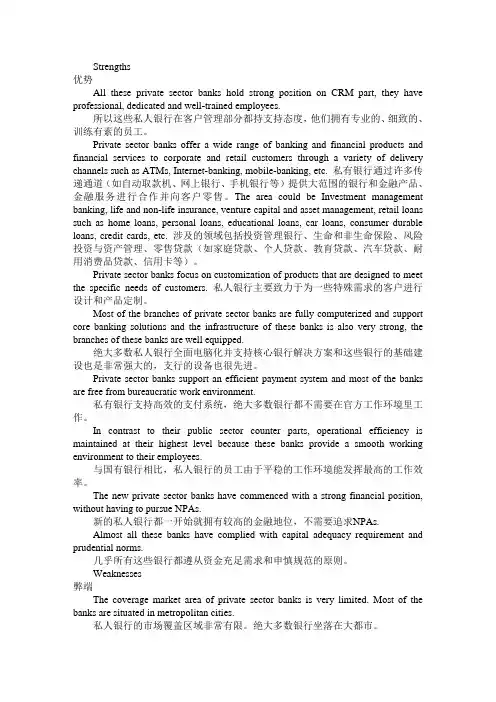

Strengths优势All these private sector banks hold strong position on CRM part, they have professional, dedicated and well-trained employees.所以这些私人银行在客户管理部分都持支持态度,他们拥有专业的、细致的、训练有素的员工。

Private sector banks offer a wide range of banking and financial products and financial services to corporate and retail customers through a variety of delivery channels such as ATMs, Internet-banking, mobile-banking, etc. 私有银行通过许多传递通道(如自动取款机、网上银行、手机银行等)提供大范围的银行和金融产品、金融服务进行合作并向客户零售。

The area could be Investment management banking, life and non-life insurance, venture capital and asset management, retail loans such as home loans, personal loans, educational loans, car loans, consumer durable loans, credit cards, etc. 涉及的领域包括投资管理银行、生命和非生命保险、风险投资与资产管理、零售贷款(如家庭贷款、个人贷款、教育贷款、汽车贷款、耐用消费品贷款、信用卡等)。

Private sector banks focus on customization of products that are designed to meet the specific needs of customers. 私人银行主要致力于为一些特殊需求的客户进行设计和产品定制。

因为学校对毕业论文中的外文翻译并无规定,为统一起见,特做以下要求:1、每篇字数为1500字左右,共两篇;2、每篇由两部分组成:译文+原文.3 附件中是一篇范本,具体字号、字体已标注。

外文翻译(包含原文)(宋体四号加粗)外文翻译一(宋体四号加粗)作者:(宋体小四号加粗)Kim Mee Hyun Director, Policy Research & Development Team,Korean Film Council(小四号)出处:(宋体小四号加粗)Korean Cinema from Origins to Renaissance(P358~P340) 韩国电影的发展及前景(标题:宋体四号加粗)1996~现在数量上的增长(正文:宋体小四)在过去的十年间,韩国电影经历了难以置信的增长。

上个世纪60年代,韩国电影迅速崛起,然而很快便陷入停滞状态,直到90年代以后,韩国电影又重新进入繁盛时期。

在这个时期,韩国电影在数量上并没有大幅的增长,但多部电影的观影人数达到了上千万人次。

1996年,韩国本土电影的市场占有量只有23.1%。

但是到了1998年,市场占有量增长到35。

8%,到2001年更是达到了50%。

虽然从1996年开始,韩国电影一直处在不断上升的过程中,但是直到1999年姜帝圭导演的《生死谍变》的成功才诞生了韩国电影的又一个高峰。

虽然《生死谍变》创造了韩国电影史上的最高电影票房纪录,但是1999年以后最高票房纪录几乎每年都会被刷新。

当人们都在津津乐道所谓的“韩国大片”时,2000年朴赞郁导演的《共同警备区JSA》和2001年郭暻泽导演的《朋友》均成功刷新了韩国电影最高票房纪录.2003年康佑硕导演的《实尾岛》和2004年姜帝圭导演的又一部力作《太极旗飘扬》开创了观影人数上千万人次的时代。

姜帝圭和康佑硕导演在韩国电影票房史上扮演了十分重要的角色。

从1993年的《特警冤家》到2003年的《实尾岛》,康佑硕导演了多部成功的电影。

毕业论文外文翻译格式毕业论文外文翻译格式在撰写毕业论文时,外文翻译是一个重要的环节。

无论是引用外文文献还是翻译相关内容,都需要遵循一定的格式和规范。

本文将介绍一些常见的外文翻译格式,并探讨其重要性和应用。

首先,对于引用外文文献的格式,最常见的是使用APA(American Psychological Association)格式。

这种格式要求在引用外文文献时,先列出作者的姓氏和名字的首字母,然后是出版年份、文章标题、期刊名称、卷号和页码。

例如:Smith, J. D. (2010). The impact of climate change on biodiversity. Environmental Science, 15(2), 145-156.在翻译外文文献时,需要注意保持原文的准确性和完整性。

尽量避免意译或添加自己的解释,以免歪曲原文的意思。

同时,还需要在翻译后的文献后面加上“译者”和“翻译日期”的信息,以便读者可以追溯翻译的来源和时间。

其次,对于翻译相关内容的格式,可以参考国际标准组织ISO(International Organization for Standardization)的格式。

这种格式要求在翻译相关内容时,先列出原文,然后是翻译后的文本。

例如:原文:The importance of effective communication in the workplace cannot be overstated.翻译:工作场所有效沟通的重要性不容忽视。

在翻译相关内容时,需要注意保持原文的意思和语气。

尽量使用准确的词汇和语法结构,以便读者能够理解和接受翻译后的内容。

同时,还需要在翻译后的文本后面加上“翻译者”和“翻译日期”的信息,以便读者可以追溯翻译的来源和时间。

此外,对于长篇外文文献的翻译,可以考虑将其分成若干章节,并在每个章节前面加上章节标题。

这样可以使读者更容易理解和阅读翻译后的内容。

毕业设计外文资料翻译原文题目:The Design and Retorfit of Buildings for Resistance to Blast-Induced Progressive Collapse 译文题目:建筑物的设计和改造抵抗由爆炸冲击引起的建筑物的连续倒塌院系名称:土木建筑学院专业班级:土木工程0303班学生姓名:吴建明学号:20034040332指导教师:白杨教师职称:讲师附件: 1.外文资料翻译译文;2.外文原文。

指导教师评语及成绩:签名: 2010年 4月 12日附件1:外文资料翻译译文译文标题(3号黑体,居中)×××××××××(小4号宋体,1.5倍行距)×××××××××××××××××××××××××××××××××××××××××××××××××××××××××××××××××××…………。

(要求不少于3000汉字)建筑物的设计和改造抵抗由爆炸冲击引起的建筑物的连续倒塌1.简介在近现代史中,极端的爆炸事件推动了现有的设计方法和规范重新评估冲击荷载对建筑结构和它们的居住着的影响。

外文翻译器外文翻译器外文翻译器(Machine Translation)是指使用计算机等技术对外文进行自动翻译的工具。

它利用计算机语言处理、人工智能和语言学等多个领域的知识和技术,将源语言(外文)自动转化为目标语言(母语)的过程。

外文翻译器可以帮助人们快速准确地将外文内容转化为自己熟悉的语言,提高工作效率和信息获取能力。

外文翻译器的研究和发展始于上世纪40年代,最早采用的是基于规则的翻译方法,即根据语法规则和词汇库对源语言进行分析和转换。

然而,这种方法存在很多限制,因为语法和词汇库可能无法覆盖所有的语言特点和用法,导致翻译结果不准确和不流畅。

随着计算机技术和人工智能的发展,神经网络机器翻译(Neural Network Translation)成为外文翻译器的主流方法。

这种方法利用大规模平行语料库训练神经网络模型,通过模仿人类学习语言的方式自动学习源语言和目标语言之间的映射关系。

神经网络机器翻译能够更好地处理语法结构和上下文信息,翻译结果更加准确和自然。

除了神经网络机器翻译,外文翻译器还可以采用统计机器翻译(Statistical Machine Translation)等其他方法。

统计机器翻译利用大量的双语语料进行统计分析,找到最佳的翻译候选,然后根据概率模型对其进行排序和选择。

虽然统计机器翻译在一定程度上改善了翻译质量,但由于依赖于大量的语料库,对于某些语言和领域的翻译效果仍然不理想。

当前外文翻译器的发展已经进入了深度学习时代,融合了自然语言处理、深度学习和人工智能的多种技术手段。

深度学习通过建立多层神经网络模型,能够从大规模语料中自动学习和提取特征,进一步提升了翻译质量和效率。

此外,人工智能的发展还带来了一系列辅助工具,如术语提取、句子结构分析和语音识别等,能够进一步提高翻译的准确性和流畅度。

虽然外文翻译器在很大程度上改善了翻译效率和准确性,但由于语言本身的复杂性和多义性,完全依靠机器翻译仍然存在一些局限性。

论文外文翻译指导日志

翻译要求:

1、选定外文文献后先给指导老师看,得到老师的确认通过后方可翻译。

2、选择外文翻译时一定选择外国作者写的文章,可从学校中知网或者外文数据库下载。

3、外文翻译字数要求3000字以上,从外文文章起始处开始翻译,不允许从文章中间部分开始翻译,翻译必须结束于文章的一个大段落。

参考文献是在学术研究过程中,对某一著作或论文的整体的参考或借鉴。

征引过的文献在注释中已注明,不再出现于文后参考文献中。

外文参考文献就是指论文是引用的文献原文是国外的,并非中国的。

原文就是指原作品,原件,即作者所写作品所用的语言。

如莎士比亚的《罗密欧与朱丽叶》原文是英语。

译文就是翻译过来的文字,如在中国也可以找到莎士比亚《罗密欧与朱丽叶》的中文版本,这个中文版本就称为译文。

主要标准

翻译是语际交流过程中沟通不同语言的桥梁。

一般来说,翻译的标准主要有两条:忠实和通顺。

忠实

是指忠实于原文所要传递的信息,也就是说,把原文的信息完整并且准确地表达出来,使译文读者得到的信息与原文读者得到的信息大致相同。

通顺

是指译文规范、明白易懂,没有文理不通、结构混乱、逻辑不清的现象。

外文翻译范例在全球化日益加深的今天,外文翻译的重要性愈发凸显。

无论是学术研究、商务交流,还是文化传播,准确而流畅的外文翻译都起着至关重要的桥梁作用。

下面为大家呈现几个不同领域的外文翻译范例,以帮助大家更好地理解和掌握外文翻译的技巧与要点。

一、科技文献翻译原文:The development of artificial intelligence has brought about revolutionary changes in various fields, such as healthcare, finance, and transportation译文:人工智能的发展给医疗保健、金融和交通运输等各个领域带来了革命性的变化。

在这个范例中,翻译准确地传达了原文的意思。

“artificial intelligence”被准确地翻译为“人工智能”,“revolutionary changes”翻译为“革命性的变化”,“various fields”翻译为“各个领域”,用词准确、贴切,符合科技文献严谨、客观的语言风格。

二、商务合同翻译原文:This Agreement shall commence on the effective date and shall continue in force for a period of five years, unless earlier terminated in accordance with the provisions herein译文:本协议自生效日起生效,并将持续有效五年,除非根据本协议的规定提前终止。

商务合同的翻译需要格外注重准确性和专业性。

上述译文中,“commence”翻译为“生效”,“in force”翻译为“有效”,“terminated”翻译为“终止”,清晰准确地表达了合同条款的含义,避免了可能的歧义。

三、文学作品翻译原文:The sun was setting, painting the sky with hues of orange and pink, as if nature were a master artist at work译文:太阳正在西沉,把天空涂成了橙色和粉色,仿佛大自然是一位正在创作的艺术大师。

2. WHAT CONSTITUTES FAIR DEALINGWEINBERGER v. UOP, INC.457 A.2d 701 (Del.Supr.19a3).MOORE, JUSTICE.This post-trial appeal was reheard en banc from a decision of the Court of Chancery. It was brought by the class action plaintiff below, a former shareholder of UOP, Inc., who challenged the elimination of UOP's minority shareholders by a cash-out merger between UOP and its majority owner, The Signal Companies, Inc. Originally, the defendants in this action were Signal, UOP, certain officers and directors of those companies, and UOP's investment banker, Lehman Brothers Kuhn Loeb, Inc. The present Chancellor held that the terms of the merger were fair to the plaintiff and the other minority shareholders of UOP. Accordingly, he entered judgment in favor of the defendants.Numerous points were raised by the parties, but we address only the following questions presented by the trial court's opinion:1) The plaintiffs duty to plead sufficient facts demonstrating the unfairness of the challenged merger;2) The burden of proof upon the parties where the merger has been approved by the purportedly informed vote of a majority of the minority shareholders;3) The fairness of the merger in terms of adequacy of the defendants' disclosures to the minority shareholders;4) The fairness of the merger in terms of adequacy of the price paid for the minority shares and the remedy appropriate to that issue; and5) The continued force and effect of Singer v. Magnavox Co., Del.Supr., 380 A.2d 969, 980 (1977), and its progeny.In ruling for the defendants, the Chancellor re-stated his earlier conclusion that the plaintiff in a suit challenging a cash-out merger must allege specific acts of fraud, misrepresentation or other items of misconduct to demonstrate the unfairness of the merger terms to the minority. We approve this rule and affirm it.The Chancellor also held that even though the ultimate burden of proof is on the majority shareholder to show by a preponderance of the evidence that the transaction is fair, it is first the burden of the plaintiff attacking the merger to demonstrate some basis for invoking the fairness obligation. We agree with that principle. However, where corporate action has been approved by an informed vote of a majority of the minority shareholders, we conclude that the burden entirely shifts ^ to the plaintiff to show that the transaction was unfair to the minority^- But in all this, the burden clearly remains on those relying on the vote to show that they completely disclosed all material facts relevant to the transaction.Here, the record does not support a conclusion that the minority stockholder vote was an informed one. Material information, necessary to acquaint those shareholders with the bargaining positions of Signal and UOP, was withheld under circumstances amounting to a breach of fiduciary duty. We therefore conclude that this merger does not meet the test of fairness, at least as we address that concept, and no burden thus shifted to the plaintiff by reason of the minority shareholder vote. Accordingly, we reverse and remand for further proceedings consistent herewith.In considering the nature of the remedy available under our law to minority shareholders in a cash-out merger, we believe that it is, and hereafter should be, an appraisal under 8 Del.C. § 262 as hereinafter construed. We therefore overrule Lynch v. Vickers Energy Corp., Del. Supr., 429 A.2d 497 (1981) {Lynch II) to the extent that it purports to limit a stockholder's monetary relief to a specific damage formula. But to give full effect to section 262 within the framework of the General Corporation Law we adopt a more liberal, less rigid and stylized, approach to the valuation process than has heretofore been permitted by our courts. While the present state of these proceedings does not admit the plaintiff to the appraisal remedy per se, the practical effect of the remedy we do grant him will be co-extensive with the liberalized valuation and appraisal methods we herein approve for cases coming after this decision.Our treatment of these matters has necessarily led us to a reconsideration of the business purpose rule announced in the trilogy of Singer A v. Magnavox Co., supra; Tanzer v. International General Industries, JT > Inc., DeL.Supr., 379 A.2d 1121 (1977); and Roland International Corp. v. Najjar, Del.Supr., 407 A.2d 1032 (1979). For the reasons hereafter set forth we consider that the business purpose requirement of these cases v J is no longer the law of Delaware.The facts found by the trial court, pertinent to the issues before us, are supported by the record, and we draw from them as set out in the Chancellor's opinion.Signal is a diversified, technically based company operating through various subsidiaries. Its stock is publicly traded on the New York, Philadelphia and Pacific Stock Exchanges. UOP, formerly known as Universal Oil Products Company, was a diversified industrial company engaged in various lines of business, including petroleum and petro-chemical services and related products, construction, fabricated metal products, transportation equipment products, chemicals and plastics, and other products and services including land development, lumber products and waste disposal. Its stock was publicly held and listed on the New York Stock Exchange.In 1974 Signal sold one of its wholly-owned subsidiaries for $420,000,000 in cash. See Gimbel v. Signal Companies, Inc., Del.Ch., 316 A.2d 599, aff’d, Del.Supr., 316 A.2d 619 (1974). While looking to invest this cash surplus, Signal became interested in UOP as a possible acquisition. Friendly negotiations ensued, and Signal proposed to acquire a controlling interest in UOP at a price of $19 per share. UOP's representatives sought $25 per share. In the arm's length bargaining that followed, an understanding was reached whereby Signal agreed to purchase from UOP 1,500,000 shares of UOP's authorized but unissued stock at $21 per share.This purchase was contingent upon Signal^ making a successful cash tender offer for 4,300,000 publicly held shares of UOP, also at a price of $21 per share. This combined method of acquisition permitted Signal to acquire 5,800,000 shares of stock, representing 50.5% of UOP's outstanding shares. The UOP board of directors advised the company's shareholders that it had no objection to Signal's tender offer at that price. Immediately before the announcement of the tender offer, UOP's common stock had been trading on the New York Stock Exchange at a fraction under $14 per share.The negotiations between Signal and UOP occurred during April 1975, and the resulting tender offer was greatly oversubscribed. However, Signal limited its total purchase of the tendered shares so that, when coupled with the stock bought from UOP, it had achieved its goalof becoming a 50.5% shareholderAlthough UOP’ board consisted of thirteen directors, Signal nominated and elected only six. Of these, five were either directors or employees of Signal. The sixth, a partner in the banking firm of Lazard Freres & Co., had been one of Signal's representatives in the negotiations and bargaining with UOP concerning the tender offer and purchase price of the UOP shares.However, the president and chief executive officer of UOP retired during 1975, and Signal caused him to be replaced by James V. Crawford, a long-time employee and senior executive vice president of one of Signal's wholly-owned subsidiaries. Crawford succeeded his predecessor on UOP's board of directors and also was made a director of Signal.By the end of 1977 Signal basically was unsuccessful in finding other suitable investment candidates for its excess cash, and by February 1978 considered that it had no other realistic acquisitions available to it on a friendly basis. Once again its attention turned to UOP.The trial court found that at the instigation of certain Signal management personnel, including William W. Walkup, its board chairman, and Forrest N. Shumway, its president, a feasibility study was made concerning the possible acquisition of the balance of UOP's outstanding shares. This study was performed by two Signal officers, Charles S. Arledge, vice president (director of planning), and Andrew J. Chitiea, senior vice president (chief financial officer). Messrs. Walkup, Shumway, Arledge and Chitiea were all directors of UOP in addition to their membership on the Signal board.Arledge and Chitiea concluded that it would be a good investment for Signal to acquire the remaining 49.5% of UOP shares at any price up to $24 each. Their report was discussed between Walkup and Shumway who, along with Arledge, Chitiea and Brewster L. Arms, internal counsel for Signal, constituted Signal's senior management. In particular, they talked about the proper price to be paid if the acquisition was pursued, purportedly keeping in mind that as UOP's majority shareholder, Signal owed a fiduciary responsibility to both its own stockholders as well as to UOP's minority. It was ultimately agreed that a meeting of Signal's Executive Committee would be called to propose that Signal acquire the remaining outstanding stock of UOP through a cash-out merger in the range of $20 to $21 per share.The Executive Committee meeting was set for February 28, 1978. As a courtesy, UOP's president, Crawford, was invited to attend, although he was not a member of Signal's executive committee. On his arrival, and prior to the meeting, Crawford was asked to meet privately with Walkup and Shumway. He was then told of Signal's plan to acquire full ownership of UOP and was asked for his reaction to the proposed price range of $20 to $21 per share. Crawford said he thought such a price would be "generous", and that it was certainly one which should be submitted to UOP's minority shareholders for their ultimate consideration. He stated, however, that Signal's 100% ownership could cause internal problems at UOP. He believed that employees would have to be given some assurance of their future place in a fully- owned Signal subsidiary. Otherwise, he feared the departure of essential personnel. Also, many of UOP's key employees had stock option incentive programs which would be wiped out by a merger. Crawford therefore urged that some adjustment would have to be made, such as providing a comparable incentive in Signal's shares, if after the merger he was to maintain his quality of personnel and efficiency at UOP.Thus, Crawford voiced no objection to the $20 to $21 price range, nor did he suggest that Signal should consider paying more than $21 per share for the minority interests. Later, at the Executive Committee meeting the same factors were discussed, with Crawford repeating the position he earlier took with Walkup and Shumway. Also considered was the 1975 tender offer andthe fact that it had been greatly oversubscribed at $21 per share. For many reasons, Signal's manage¬ment concluded that the acquisition of UOP's minority shares provided the solution to a number of its business problems.Thus, it was the consensus that a price of $20 to $21 per share would be fair to both Signal and the minority shareholders of UOP. Signal's executive committee authorized its management "to negotiate" with UOP "for a cash acquisition of the minority ownership in UOP, Inc., with the intention of presenting a proposal to [Signal's] board of directors * * * on March 6, 1978". Immediately after this February 28, 1978 meeting, Signal issued a press release stating: The Signal Companies, Inc. and UOP, Inc. are conducting negotiations for the acquisition for cash by Signal of the 49.5 per cent of UOP which it does not presently own, announced Forrest N. Shumway, president and chief executive officer of Signal, and James V. Crawford, UOP president. Price and other terms of the proposed transaction have not y et been finalized and would be subject to approval of the boards of directors of Signal and UOP, scheduled to meet early next week, the stockholders of UOP and certain federal agencies.The announcement also referred to the fact that the closing price of UOP's common stock on that day was $14.50 per share.Two days later, on March 2, 1978, Signal issued a second press release stating that its management would recommend a price in the range of $20 to $21 per share for UOP's 49.5% minority interest. This announcement referred to Signal's earlier statement that "negotiations" were being conducted for the acquisition of the minority shares.Between Tuesday, February 28, 1978 and Monday, March 6,1978, a total of four business days, Crawford spoke by telephone with all of UOP's non-Signal, i.e., outside, directors. Also during that period, Crawford retained Lehman Brothers to render a fairness opinion as to the price offered the minority for its stock. He gave two reasons for this choice. First, the time schedule between the announcement and the board meetings was short (by then only three business days) and since Lehman Brothers had been acting as UOP's investment banker for many years, Crawford felt that it would be in the best position to respond on such brief notice. Second, James W. Glanville, a long-time director of UOP and a partner in Lehman Brothers, had acted as a financial advisor to UOP for many years. Crawford believed that Glanville's familiarity with UOP, as a member of its board, would also be of assistance in enabling Lehman Brothers to render a fairness opinion within the existing time constraints.Crawford telephoned Glanville, who gave his assurance that Lehman Brothers had no conflicts that would prevent it from accepting the task. Glanville's immediate personal reaction was that a price of $20 to $21 would certainly be fair, since it represented almost a 50% premium over UOP's market price. Glanville sought a $250,000 fee for Lehman Brothers' services, but Crawford thought this too much. After further discussions Glanville finally agreed that Lehman Brothers would render its fairness opinion for $150,000.During this period Crawford also had several telephone contacts with Signal officials. In only one of them, however, was the price of the shares discussed. In a conversation with Walkup, Crawford advised that as a result of his communications with UOP's non-Signal directors, it was his feeling that the price would have to be the top of the proposed range, or $21 per share, if the approval of UOP's outside directors was to be obtained. But again, he did not seek any price higher than $21.Glanville assembled a three-man Lehman Brothers team to do the work on the fairness opinion. These persons examined relevant documents and information concerning UOP, including its annual reports and its Securities and Exchange Commission filings from 1973 through 1976, as well as its audited financial statements for 1977, its interim reports to shareholders, and its recent and historical market prices and trading volumes. In addition, on Friday, March 3, 1978, two members of the Lehman Brothers team flew to UOP's headquarters in Des Plaines, Illinois, to perform a "due diligence" visit, during the course of which they interviewed Crawford as well as UOP's general counsel, its chief financial officer, and other key executives and personnel.As a result, the Lehman Brothers team concluded that "the price of either $20 or $21 would be a fair price for the remaining shares of UOP". They telephoned this impression to Glanville, who was spending the weekend in Vermont.On Monday morning, March 6, 1978, Glanville and the senior member of the Lehman Brothers team flew to Des Plaines to attend the scheduled UOP directors meeting. Glanville looked over the assembled information during the flight. The two had with them the draft of a "fairness opinion letter" in which the price had been left blank. Either during or immediately prior to the directors' meeting, the two-page "fairness opinion letter" was typed in final form and the price of $21 per share was inserted.On March 6, 1978, both the Signal and UOP boards were convened to consider the proposed merger. Telephone communications were maintained between the two meetings. Walkup, Signal's board chairman, and also a UOP director, attended UOP's meeting with Crawford in order to present Signal's position and answer any questions that UOP's non-Signal directors might have. Arledge and Chitiea, along with Signal's other designees on UOP's board, participated by conference telephone. All of UOP's outside directors attended the meeting either in person or by conference telephone.First, Signal's board unanimously adopted a resolution authorizing Signal to propose to UOP a cash merger of $21 per share as outlined in a certain merger agreement, and other supporting documents. This proposal required that the merger be approved by a majority of UOP's outstanding minority shares voting at the stockholders meeting at which the merger would be considered, and that the minority shares voting in favor of the merger, when coupled with Signal's 50.5% interest would have to comprise at least two-thirds of all UOP shares. Otherwise the proposed merger would be deemed disapproved.UOP's board then considered the proposal. Copies of the agreement were delivered to the directors in attendance, and other copies had been forwarded earlier to the directors participating by telephone. They also had before them UOP financial data for 1974-1977, UOP's most recent financial statements, market price information, and budget projections for 1978. In addition they had Lehman Brothers' hurriedly prepared fairness opinion letter finding the price of $21 to be fair. Glanville, the Lehman Brothers partner, and UOP director, commented on the information that had gone into preparation of the letter.Signal also suggests that the Arledge-Chitiea feasibility study, indicating that a price of up to $24 per share would be a "good investment" for Signal, was discussed at the UOP directors' meeting. The Chancellor made no such finding, and our independent review of the record, detailed infra, satisfies us by a preponderance of the evidence that there was no discussion of this document at UOP's board meeting. Furthermore, it is clear beyond peradventure that nothing in that report was ever disclosed to UOP's minority shareholders prior to their approval of themerger.After consideration of Signal's proposal, Walkup and Crawford left the meeting to permit a free and uninhibited exchange between UOP's non-Signal directors. Upon their return a resolution to accept Signal's offer was then proposed and adopted. While Signal's men on UOP's board participated in various aspects of the meeting, they abstained from voting. However, the minutes show that each of them "if voting would have voted yes".On March 7, 1978, UOP sent a letter to its shareholders advising them of the action taken by UOP's board with respect to Signal's offer. This document pointed out, among other things, that on February 28, 1978 "both companies had announced negotiations were being conducted".Despite the swift board action of the two companies, the merger was not submitted to UOP's shareholders until their annual meeting on May 26, 1978. In the notice of that meeting and proxy statement sent to shareholders in May, UOP's management and board urged that the merger be approved. The proxy statement also advised:The price was determined after discussions between James V. Crawford, a director of Signal and Chief Executive Officer of UOP, and officers of Signal which took place during meetings on February 28, 1978, and in the course of several subsequent telephone conversations. (Emphasis added.)In the original draft of the proxy statement the word "negotiations" had been used rather than "discussions". However, when the Securities and Exchange Commission sought details of the "negotiations" as part of its review of these materials, the term was deleted and the word "discussions" was substituted. The proxy statement indicated that the vote of UOP's board in approving the merger had been unanimous. It also advised the shareholders that Lehman Brothers had given its opinion that the merger price of $21 per share was fair to UOP's minority. However, it did not disclose the hurried method by which this conclusion was reached.As of the record date of UOP's annual meeting, there were 11,488,302 shares of UOP common stock outstanding, 5,688,302 of which were owned by the minority. At the meeting only 56%, or 3,208,652, of the minority shares were voted. Of these, 2,953,812, or 51.9% of the total minority, voted for the merger, and 254,840 voted against it. When Signal's stock was added to the minority shares voting in favor, a total of 76.2% of UOP's outstanding shares approved the merger while only 2.2% opposed it.By its terms the merger became effective on May 26, 1978, and each share of UOP's stock held by the minority was automatically converted into a right to receive $21 cash.II.A.A primary issue mandating reversal is the preparation by two UOP directors, Arledge and Chitiea, of their feasibility study for the exclusive use and benefit of Signal. This document was of obvious significance to both Signal and UOP. Using UOP data, it described the advantages to Signal of ousting the minority at a price range of $21-$24 per share. Mr. Arledge, one of the authors, outlined the benefits to Signal:Purpose Of The Merger1) Provides an outstanding investment opportunity for Signal—(Better than any recent acquisition we have seen.)2) Increases Signal's earnings.3) Facilitates the flow of resources between Signal and its subsidiaries(Big factor—works both ways.)4) Provides cost savings potential for Signal and UOP.5) Improves the percentage of Signal's 'operating earnings' as opposed to 'holding company earnings'.6) Simplifies the understanding of Signal.7) Facilitates technological exchange among Signal's subsidiaries.8) Eliminates potential conflicts of interest.Having written those words, solely for the use of Signal it is clear from the record that neither Arledge nor Chitiea shared this report with their fellow directors of UOP. We are satisfied that no one else did either. This conduct hardly meets the fiduciary standards applicable to such a transaction * * *The Arledge-Chitiea report speaks for itself in supporting the Chancellor's finding that a price of up to $24 was a "good investment" for Signal. It shows that a return on the investment at $21 would be 15.7% versus 15.5% at $24 per share. This was a difference of only two-tenths of one percent, while it meant over $17,000,000 to the minority. Under such circumstances, paying UOP's minority shareholders $24 would have had relatively little long-term effect on Signal, and the Chancellor's findings concerning the benefit to Signal, even at a price of $24, were obviously correct. Levitt v. Bouvier, Del.Supr., 287 A.2d 671, 673 (1972).Certainly, this was a matter of material significance to UOP and its shareholders. Since the study was prepared by two UOP directors, using UOP information for the exclusive benefit of Signal, and nothing whatever was done to disclose it to the outside UOP directors or the minority shareholders, a question of breach of fiduciary duty arises. This problem occurs because there were common Signal-UOP directors participating, at least to some extent, in the UOP board's decision making processes without full disclosure of the conflicts they faced.7B.In assessing this situation, the Court of Chancery was required to:examine what information defendants had and to measure it against what they gave to the minority stockholders, in a context in which 'complete candor' is required. In other words, the limited function of the Court was to determine whether defendants had disclosed all information in their possession germane to the transaction in issue. And by 'germane' we mean, for present purposes, information such as a reasonable shareholder would consider important. in Priding whether. to sell or retain stock.* * ** * * Completeness, not adequacy, is both the norm and the mandate under present circumstances. Lynch v. Vickers Energy Corp., Del.Supr., 383 A.2d 278, 281 (1977) (Lynch /). This is merely stating in another way the long-existing principle of Delaware law that these Signal designated directors on UOP's board still owed UOP and its shareholders an uncompromising duty of loyalty. The classic language of Guth v. Loft, Inc., Del.Supr., 5 A.2d 503, 510 (1939), requires no embellishment:A public policy, existing through the years, and derived from a profound knowledge of human characteristics and motives, has established a rule that demands of a corporate officer or director, peremptorily and inexorably, the most scrupulous observance of his duty, not only affirmatively to protect the interests of the corporation committed to his charge, but also to refrainfrom doing anything that would work injury to the corporation, or to deprive it of. profit or advantage which his skill and ability might properly bring to it, or to enable it to make in the reasonable and lawful exercise of its powers. The rule that requires an undivided and unselfish loyalty to the corporation demands that there shall be no conflict between duty and self-interest. Given the absence of any attempt to structure this transaction on an arm's length basis, Signal cannot escape the effects of the conflicts it faced, particularly when its designees on UOP's board did not totally abstain from participation in the matter. There is no "safe harbor" for such divided loyalties in Delaware. When directors of a Delaware ^ corporation are on both sides of a transaction, they are required to demonstrate their utmost good faith and the most scrupulous inherent P fairness of the bargain. Gottlieb v. Heyden Chemical Corp., Del.Supr., 91 A.2d 57, 57-58 (1952). The requirement of fairness is unflinching in v rP y demand that where one stands on both sides of a transaction, he has the burden of establishing its entire fairness, sufficient to pass the test of careful scrutiny by the courts. Sterling v. Mayflower Hotel Corp., N, Del.Supr., 93 A.2d 107, 110 (1952); Bastian v. Bourns, Inc., Del.Ch., 256 A.2d 680, 681 (1969), aff’d, Del.Supr., 278 A.2d 467 (1970); David J. Greene & Co. v. Dunhill International Inc., Del.Ch., 249 A.2d 427, 431 (1968).There is no dilution of this obligation where one holds dual or multiple directorships, as in a parent-subsidiary context. Levien v. Sinclair Oil Corp., Del.Ch., 261 A.2d 911, 915 (1969). Thus, individuals who act in a dual capacity as directors of two corporations, one of whom is parent and the other subsidiary, owe the same duty of good management to both corporations, and in the absence of an independent negotiating structure (see note 7, supra), or the directors' total abstention from any participation in the matter, this duty is to be exercised in light of what is best for both companies. Warshaw v. Calhoun, Del. Supr., 221 A.2d 487, 492 (1966). The record demonstrates that Signal has not met this obligation.。

DOI10.1007/s10711-012-9699-zORIGINAL PAPERParking garages with optimal dynamicsMeital Cohen·Barak WeissReceived:19January2011/Accepted:22January2012©Springer Science+Business Media B.V.2012Abstract We construct generalized polygons(‘parking garages’)in which the billiard flow satisfies the Veech dichotomy,although the associated translation surface obtained from the Zemlyakov–Katok unfolding is not a lattice surface.We also explain the difficulties in constructing a genuine polygon with these properties.Keywords Active vitamin D·Parathyroid hormone-related peptide·Translation surfaces·Parking garages·Veech dichotomy·BilliardsMathematics Subject Classification(2000)37E351Introduction and statement of resultsA parking garage is an immersion h:N→R2,where N is a two dimensional compact connected manifold with boundary,and h(∂N)is afinite union of linear segments.A parking garage is called rational if the group generated by the linear parts of the reflections in the boundary segments isfinite.If h is actually an embedding,the parking garage is a polygon; thus polygons form a subset of parking garages,and rationals polygons(i.e.polygons all of whose angles are rational multiples ofπ)form a subset of rational parking garages.The dynamics of the billiardflow in a rational polygon has been intensively studied for over a century;see[7]for an early example,and[5,10,13,16]for recent surveys.The defi-nition of the billiardflow on a polygon readily extends to a parking garage:on the interior of N the billiardflow is the geodesicflow on the unit tangent bundle of N(with respect to the pullback of the Euclidean metric)and at the boundary,theflow is defined by elastic reflection (angle of incidence equals the angle of return).Theflow is undefined at thefinitely many M.Cohen·B.Weiss(B)Ben Gurion University,84105Be’er Sheva,Israele-mail:barakw@math.bgu.ac.ilM.Cohene-mail:comei@bgu.ac.ilpoints of N which map to‘corners’,i.e.endpoints of boundary segments,and hence at thecountable union of codimension1submanifolds corresponding to points in the unit tangentbundle for which the corresponding geodesics eventually arrive at corners in positive or neg-ative time.Since the direction of motion of a trajectory changes at a boundary segment viaa reflection in its side,for rational parking garages,onlyfinitely many directions of motionare assumed.In other words,the phase space of the billiardflow decomposes into invarianttwo-dimensional subsets corresponding tofixing the directions of motion.Veech[12]discovered that the billiardflow in some special polygons exhibits a strikingly he found polygons for which,in any initial direction,theflow is eithercompletely periodic(all orbits are periodic),or uniquely ergodic(all orbits are equidistrib-uted).Following McMullen we will say that a polygon with these properties has optimaldynamics.We briefly summarize Veech’s strategy of proof.A standard unfolding construc-tion usually attributed to Zemlyakov and Katok[15]1,associates to any rational polygon Pa translation surface M P,such that the billiardflow on P is essentially equivalent to thestraightlineflow on M P.Associated with any translation surface M is a Fuchsian group M,now known as the Veech group of M,which is typically trivial.Veech found M and P forwhich this group is a non-arithmetic lattice in SL2(R).We will call these lattice surfaces and lattice polygons respectively.Veech investigated the SL2(R)-action on the moduli space of translation surfaces,and building on earlier work of Masur,showed that lattice surfaces haveoptimal dynamics.From this it follows that lattice polygons have optimal dynamics.This chain of reasoning remains valid if one starts with a parking garage instead of apolygon;namely,the unfolding construction associates a translation surface to a parkinggarage,and one may define a lattice parking garage in an analogous way.The arguments ofVeech then show that the billiardflow in a lattice parking garage has optimal dynamics.Thisgeneralization is not vacuous:lattice parking garages,which are not polygons,were recentlydiscovered by Bouw and Möller[2].The term‘parking garage’was coined by Möller.A natural question is whether Veech’s result admits a converse,i.e.whether non-latticepolygons or parking garages may also have optimal dynamics.In[11],Smillie and the sec-ond-named author showed that there are non-lattice translation surfaces which have optimaldynamics.However translation surfaces arising from billiards form a set of measure zero inthe moduli space of translation surfaces,and it was not clear whether the examples of[11]arise from polygons or parking garages.In this paper we show:Theorem1.1There are non-lattice parking garages with optimal dynamics.An example of such a parking garage is shown in Fig.1.Veech’s work shows that for lattice polygons,the directions in which all orbits are periodicare precisely those containing a saddle connection,i.e.a billiard path connecting corners ofthe polygon which unfold to singularities of the corresponding surface.Following Cheunget al.[3],if a polygon P has optimal dynamics,and the periodic directions coincide with thedirections of saddle connections,we will say that P satisfies strict ergodicity and topologicaldichotomy.It is not clear to us whether our example satisfies this stronger property.As weexplain in Remark3.2below,this would follow if it were known that the center of the regularn-gon is a‘connection point’in the sense of Gutkin,Hubert and Schmidt[8]for some nwhich is an odd multiple of3.Veech also showed that for a lattice polygon P,the number N P(T)of periodic strips on P of length at most T satisfies a quadratic growth estimate of the form N P(T)∼cT2for a positive constant c.As we explain in Remark3.3,our examples also satisfy such a quadratic growth estimate.1But dating back at least to Fox and Kershner[7].Fig.1A non-lattice parkinggarage with optimal dynamics.(Here 2/n represents angle 2π/n )It remains an open question whether there is a genuine polygon which has optimal dynam-ics and is not a lattice polygon.Although our results make it seem likely that such a polygon exists,in her M.Sc.thesis [4],the first-named author obtained severe restrictions on such a polygon.In particular she showed that there are no such polygons which may be constructed from any of the currently known lattice examples via the covering construction as in [11,13].We explain these results and prove a representative special case in §4.2PreliminariesIn this section we cite some results which we will need,and deduce simple consequences.For the sake of brevity we will refer the reader to [10,11,16]for definitions of translation surfaces.Suppose S 1,S 2are compact orientable surfaces and π:S 2→S 1is a branched cover.That is,πis continuous and surjective,and there is a finite 1⊂S 1,called the set of branch points ,such that for 2=π−1( 1),the restriction of πto S 2 2is a covering map of finite degree d ,and for any p ∈ 1,#π−1(p )<d .A ramification point is a point q ∈ 2for which there is a neighborhood U such that {q }=U ∩π−1(π(q ))and for all u ∈U {q },# U ∩π−1(π(u )) ≥2.If M 1,M 2are translation surfaces,a translation map is a surjective map M 2→M 1which is a translation in charts.It is a branched cover.In contrast to other authors (cf.[8,13]),we do not require that the set of branch points be distinct from the singularities of M 1,or that they be marked.It is clear that the ramification points of the cover are singularities on M 2.If M is a lattice surface,a point p ∈M is called periodic if its orbit under the group of affine automorphisms of M is finite.A point p ∈M is called a connection point if any seg-ment joining a singularity with p is contained in a saddle connection (i.e.a segment joining singularities)on M .The following proposition summarizes results discussed in [7,9–11]:Proposition 2.1(a)A non-minimal direction on a translation surface contains a saddle connection.(b)If M 1is a lattice surface,M 2→M 1is translation map with a unique branch point,then any minimal direction on M 2is uniquely ergodic.(c)If M2→M1is a translation map such that M1is a lattice surface,then all branchpoints are periodic if and only if M2is a lattice surface.(d)If M2→M1is a translation map with a unique branch point,such that M1is a latticesurface and the branch point is a connection point,then any saddle connection direction on M2is periodic.Corollary2.2Let M2→M1be a translation map such that M1is a lattice surface with a unique branch point p.Then:(1)M2has optimal dynamics.(2)If p is a connection point then M2satisfies topological dichotomy and strict ergodicity.(3)If p is not a periodic point then M2is not a lattice surface.Proof To prove(1),by(b),the minimal directions are uniquely ergodic,and we need to prove that the remaining directions are either completely periodic or uniquely ergodic. By(a),in any non-minimal direction on M2there is a saddle connectionδ,and there are three possibilities:(i)δprojects to a saddle connection on M1.(ii)δprojects to a geodesic segment connecting the branch point p to itself.(iii)δprojects to a geodesic segment connecting p to a singularity.In case(i)and(ii)since M1is a lattice surface,the direction is periodic on M1,hence on M2as well.In case(iii),there are two subcases:ifδprojects to a part of a saddle connec-tion on M1,then it is also a periodic direction.Otherwise,in light of Proposition2.1(a),the direction must be minimal in M1,and hence,by Proposition2.1(b),uniquely ergodic in M2. This proves(1).Note also that if p is a connection point then the last subcase does not arise, so all directions which are non-minimal on M2are periodic.This proves(2).Statement(3) follows from(c).We now describe the unfolding construction[7,15],extended to parking garages.Let P=(h:N→R2).An edge of P is a connected subset L of∂N such that h(L)is a straight segment and L is maximal with these properties(with respect to inclusion).A vertex of P is any point which is an endpoint of an edge.The angle at a vertex is the total interior angle, measured via the pullback of the Euclidean metric,at the vertex.By convention we always choose the positive angles.Note that for polygons,angles are less than2π,but for parking garages there is no apriori upper bound on the angle at a vertex.Since our parking garages are rational,all angles are rational multiples ofπ,and we always write them as p/q,omitting πfrom the notation.Let G P be the dihedral group generated by the linear parts of reflections in h(L),for all edges L.For the sake of brevity,if there is a reflection with linear part gfixing a line parallel to L,we will say that gfixes L.Let S be the topological space obtained from N×G P by identifying(x,g1)with(x,g2)whenever g−11g2fixes an edge containing h(x).Topologically S is a compact orientable surface,and the immersions g◦h on each N×{g}induce an atlas of charts to R2which endows S with a translation surface structure.We denote this translation surface by M P,and writeπP for the map N×G P→M P.We will be interested in a‘partial unfolding’which is a variant of this construction,in which we reflect a parking garage repeatedly around several of its edges to form a larger parking garage.Formally,suppose P=(h:N→R2)and Q=(h :N →R2)are parking garages.For ≥1,we say that P tiles Q by reflections,and that is the number of tiles,if the following holds.There are maps h 1,...h :N→N and g1,...,g ∈G P(not necessarily distinct)satisfying:(A)The h i are homeomorphisms onto their images,and N = h i (N ).(B)For each i ,the linear part of h ◦h i ◦h −1is everywhere equal to g i .(C)For each 1≤i <j ≤ ,let L i j =h i (N )∩h j (N )and L =(h i )−1(L i j ).Then (h j )−1◦h i is the identity on L ,and L is either empty,or a vertex,or an edge of P .If L is an edge then h i (N )∪h j (N )is a neighborhood of L i j.If L i j is a vertex then there is a finite set of i =i 1,i 2,...,i k =j such that h i s (N )contains a neighborhood of L i j ,and each consecutive pair h i t (N ),h i t +1(N )intersect along an edge containing L i j .V orobets [13]realized that a tiling of parking garages gives rise to a branched cover.More precisely:Proposition 2.3Suppose P tiles Q by reflections with tiles,M P ,M Q are the correspond-ing translation surfaces obtained via the unfolding construction,and G P ,G Q are the cor-responding reflection groups.Then there is a translation map M Q →M P ,such that the following hold:(1)G Q ⊂G P .(2)The branch points are contained in the G P -orbit of the vertices of P .(3)The degree of the cover is [G P :G Q ].(4)Let z ∈M P be a point which is represented (as an element of N ×{1,...,r })by(x ,k )with x a vertex in P with angle m n (where gcd (m ,n )=1).Let (y i )⊂M Q be the pre-images of z,with angles k i m n in Q .Then z is a branch point of the cover if and only if k i n for some i.Proof Assertion (1)follows from the fact that Q is tiled by P .Since this will be impor-tant in the sequel,we will describe the covering map M Q →M P in detail.We will map (x ,g )∈N ×G Q to πP (x ,gg i )∈M P ,where x =h i (x ).We now check that this map is independent of the choice of x ,i ,and descends to a well-defined map M Q →M P ,which is a translation in charts.If x =h i (x 1)=h j (x 2)then x 1=x 2since (h i )−1◦h j is the identity.If x is in the relative interior of an edge L i j thenπP (x ,gg i )=πP (x ,gg j )(1)since (gg i )−1gg j =g −1i g j fixes an edge containing h (x 1).If x 1is a vertex of P then one proves (1)by an induction on k ,where k is as in (C).This shows that the map is well-defined.We now show that it descends to a map M Q →M P .Suppose (x ,g ),(x ,g )are two points in N ×G Q which are identified in M Q ,i.e.x ∈∂N is in the relative interior of an edge fixed by g −1g .By (C)there is a unique i such that x is in the image of h i .Thus (x ,g )maps to (x ,gg i )and (x ,g )maps to (x ,g g i ),and g −1i g −1g g i fixes the edge through x =g −1i (x ).It remains to show that the map we have defined is a translation in charts.This follows immediately from the chain rule and (B).Assertion (2)is simple and left to the reader.For assertion (3)we note that M P (resp.M Q )is made of |G P |(resp. |G Q |)copies of P .The point z will be a branch point if and only if the total angle around z ∈M P differs from the total angle around one of the pre-images y i ∈M Q .The total angle at a singularity corresponding to a vertex with angle r /s (where gcd (r ,s )=1)is 2r π,thus the total angle at z is 2m πand the total angle at y i is 2k i m πgcd (k i ,n ).Assertion (4)follows.3Non-lattice dynamically optimal parking garagesIn this section we prove the following result,which immediately implies Theorem1.1: Theorem3.1Let n≥9be an odd number divisible by3,and let P be an isosceles triangle with equal angles1/n.Let Q be the parking garage made of four copies of P glued as in Fig.1, so that Q has vertices(in cyclic order)with angles1/n,2/n,3/n,(n−2)/n,2/n,3(n−2)/n. Then M P is a lattice surface and M Q→M P is a translation map with one aperiodic branchpoint.In particular Q is a non-lattice parking garage with optimal dynamics.Proof The translation surface M P is the double n-gon,one of Veech’s original examples of lattice surfaces[12].The groups G P and G Q are both equal to the dihedral group D n.Thus by Proposition2.3,the degree of the cover M Q→M P is four.Again by Proposition2.3, since n is odd and divisible by3,the only vertices which correspond to branch points are the two vertices z1,z2with angle2/n(they correspond to the case k i=2while the other vertices correspond to1or3).In the surface M P there are two points which correspond to vertices of equal angle in P(the centers of the two n-gons),and these points are known to be aperiodic [9].We need to check that z1and z2both map to the same point in M P.This follows from the fact that both are opposite the vertex z3with angle3/n,which also corresponds to the center of an n-gon,so in M P project to a point which is distinct from z3. Remark3.2As of this writing,it is not known whether the center of the regular n-gon is a connection point on the double n-gon surface.If this turns out to be the case for some n which is an odd multiple of3,then by Corollary2.2(2),our construction satisfies strict ergodicity and topological dichotomy.See[1]for some recent related results.Remark3.3Since our examples are obtained by taking branched covers over lattice surfaces, a theorem of Eskin et al.[6,Thm.8.12]shows that our examples also satisfy a quadratic growth estimate of the form N P(T)∼cT2;moreover§9of[6]explains how one may explicitly compute the constant c.4Non-lattice optimal polygons are hard tofindIn this section we present results indicating that the above considerations will not easily yield a non-lattice polygon with optimal dynamics.Isolating the properties necessary for our proof of Theorem3.1,we say that a pair of polygons(P,Q)is suitable if the following hold:•P is a lattice polygon.•P tiles Q by reflections.•The corresponding cover M Q→M P as in Proposition2.3has a unique branch point which is aperiodic.In her M.Sc.thesis at Ben Gurion University,thefirst-named author conducted an exten-sive search for a suitable pair of polygons.By Corollary2.2,such a pair will have yielded a non-lattice polygon with optimal dynamics.The search begins with a list of candidates for P,i.e.a list of currently known lattice polygons.At present,due to work of many authors, there is a fairly large list of known lattice polygons but there is no classification of all lattice polygons.In[4],the full list of lattice polygons known as of this writing is given,and the following is proved:Theorem4.1(M.Cohen)Among the list of lattice surfaces given in[4],there is no P for which there is Q such that(P,Q)is a suitable pair.The proof of Theorem4.1contains a detailed case-by-case analysis for each of the differ-ent possible P.These cases involve some common arguments which we will illustrate in this section,by proving the special case in which P is any of the obtuse triangles investigated byWard[14]:Theorem4.2For n≥4,let P=P n be the(lattice)triangle with angles1n,12n,2n−32n.Then there is no polygon Q for which(P,Q)is a suitable pair.Our proof relies on some auxiliary statements which are of independent interest.In all of them,M Q→M P is the branched cover with unique branch point corresponding to a suitable pair(P,Q).These statements are also valid in the more general case in which P,Q are parking garages.Recall that an affine automorphism of a translation surface is a homeomorphism which is linear in charts.We denote by Aff(M)the group of affine automorphisms of M and by D:Aff(M)→GL2(R)the homomorphism mapping an affine automorphism to its linear part.Note that we allow orientation-reversing affine automorphisms,i.e.detϕmay be1 or−1.We now explain how G P acts on M P by translation equivalence.LetπP:N×G P→M P and S be as in the discussion preceding Proposition2.3,and let g∈G P.Since the left action of g on G is a permutation and preserves the gluing ruleπP,the map N×G P→N×G P sending(x,g )to(x,g−1g )induces a homeomorphismϕ:S→S and g◦h◦ϕis a translation in charts.Thus g∈G P gives a translation isomorphism of M P,and similarly g∈G P gives a translation isomorphism of M Q.Lemma4.3The branch point of the cover p:M Q→M P isfixed by G Q.Proof Since G Q⊂G P,any g∈G Q induces translation isomorphisms of both M P and M Q.We denote both by g.The definition of p given in thefirst paragraph of the proof of Proposition2.3shows that p◦g=g◦p;namely both maps are induced by sending (x ,g )∈N ×G Q toπP(x,gg g i),where x =h i(x).Since the cover p has a unique branch point,any g∈G Q mustfix it. Lemma4.4If an affine automorphismϕof a translation surface has infinitely manyfixed points then Dϕfixes a nonzero vector,in its linear action on R2.Proof Suppose by contradiction that the linear action of Dϕon the plane has zero as a uniquefixed point,and let Fϕbe the set offixed points forϕ.For any x∈Fϕwhich is not a singularity,there is a chart from a neighborhood U x of x to R2with x→0,and a smaller neighborhood V x⊂U x,such thatϕ(V x)⊂U x and when expressed in this chart,ϕ|V x is given by the linear action of Dϕon the plane.In particular x is the onlyfixed point in V x. Similarly,if x∈Fϕis a singularity,then there is a neighborhood U x of x which maps to R2 via afinite branched cover ramified at x→0,such that the action ofϕin V x⊂U x covers the linear action of Dϕ.Again we see that x is the onlyfixed point in V x.By compactness wefind that Fϕisfinite,contrary to hypothesis. Lemma4.5Suppose M is a lattice surface andϕ∈Aff(M)has Dϕ=−Id.Then afixed point forϕis periodic.Proof LetF1={σ∈Aff(M):Dσ=−Id}.Thenϕ∈F1and F1isfinite,since it is a coset for the group ker D which is known to be finite.Let A⊂M be the set of points which arefixed by someσ∈F1.By Lemma4.4this is afinite set,which contains thefixed points forϕ.Thus in order to prove the Lemma,it suffices to show that A is Aff(M)-invariant.Letψ∈Aff(M),and let x∈A,so that x=σ(x)with Dσ=−Id.Since-Id is central in GL2(R),D(σψ)=D(ψσ),so there is f∈ker D such thatψσ=fσψ.Thereforeψ(x)=ψσ(x)=fσψ(x),and fσ∈F1.This proves thatψ(x)∈A.Remark4.6This improves Theorem10of[8],where a similar conclusion is obtained under the additional assumptions that M is hyperelliptic and Aff(M)is generated by elliptic ele-ments.The following are immediate consequences:Corollary4.7Suppose(P,Q)is a suitable pair.Then•−Id/∈D(G Q).•None of the angles between two edges of Q are of the form p/q with gcd(p,q)=1and q even.Proof of Theorem4.2We will suppose that Q is such that(P,Q)are a suitable pair and reach a contradiction.If n is even,then Aff(M P)contains a rotation byπwhichfixes the points in M P coming from vertices of P.Thus by Lemma4.5all vertices of P give rise to periodic points,contradicting Proposition2.1(c).So n must be odd.Let x1,x2,x3be the vertices of P with corresponding angles1/n,1/2n,(2n−3)/2n. Then x3gives rise to a singularity,hence a periodic point.Also using Lemma4.5and the rotation byπ,one sees that x2also gives rise to a periodic point.So the unique branch point must correspond to the vertex x1.The images of the vertex x1in P give rise to two regular points in M P,marked c1,c2in Fig.2.Any element of G P acts on{c1,c2}by a permutation, so by Lemma4.3,G Q must be contained in the subgroup of index twofixing both of the c i. Let e1be the edge of P opposite x1.Since the reflection in e1,or any edge which is an image of e1under G P,swaps the c i,we have:e1is not a boundary edge of Q.(2) We now claim that in Q,any vertex which corresponds to the vertex x3from P is alwaysdoubled,i.e.consists of an angle of(2n−3)/n.Indeed,for any polygon P0,the group G P0 is the dihedral group D N where N is the least common multiple of the denominators of theangles at vertices of P0.In particular it contains-Id when N is even.Writing(2n−3)/2n in reduced form we have an even denominator,and since,by Corollary4.7,−Id/∈G Q,in Q the angle at vertex x3must be multiplied by an even integer2k.Since2k(2n−3)/2n is bigger than2if k>1,and since the total angle at a vertex of a polygon is less than2π,we must have k=1,i.e.any vertex in Q corresponding to the vertex x3is always doubled.This establishes the claim.It is here that we have used the assumption that Q is a polygon and not a parking garage.Fig.2Ward’s surface,n=5Fig.3Two options to start the construction ofQThere are two possible configurations in which a vertex x3is doubled,as shown in Fig.3. The bold lines indicate lines which are external,i.e.boundary edges of Q.By(2),the con-figuration on the right cannot occur.Let us denote the polygon on the left hand side of Fig.3by Q0.It cannot be equal to Q,since it is a lattice polygon.We now enlarge Q0by adding copies of P step by step,as described in Fig.4.Without loss of generality wefirst add triangle number1.By(2),the broken line indicates a side which must be internal in Q.Therefore,we add triangle number 2.We denote the resulting polygon by Q1.One can check by computing angles,using thefact that n is odd,and using Proposition2.3(4)that the cover M Q1→M P will branch overthe points a corresponding to vertex x2.Since the allowed branching is only over the points corresponding to x1,we must have Q1 Q,so we continue the construction.Without loss of generality we add triangle number3.Again,by(2),the broken line indicates a side which must be internal in Q.Therefore,we add triangle number4,obtaining Q2.Now,using Prop-osition2.3(4)again,in the cover M Q2→M P we have branching over two vertices u andv which are both of type x1and correspond to distinct points c1and c2in M P.This implies Q2 Q.Fig.4Steps of the construction of QSince both vertices u and v are delimited by2external sides,we cannot change the angle to prevent the branching over one of these points.This means that no matter how we continue to construct Q,the branching in the cover M Q→M P will occur over at least two points—a contradiction.Acknowledgments We are grateful to Yitwah Cheung and Patrick Hooper for helpful discussions,and to the referee for a careful reading and helpful remarks which improved the presentation.This research was supported by the Israel Science Foundation and the Binational Science Foundation.References1.Arnoux,P.,Schmidt,T.:Veech surfaces with non-periodic directions in the tracefield.J.Mod.Dyn.3(4),611–629(2009)2.Bouw,I.,Möller,M.:Teichmüller curves,triangle groups,and Lyapunov exponents.Ann.Math.172,139–185(2010)3.Cheung,Y.,Hubert,P.,Masur,H.:Topological dichotomy and strict ergodicity for translation surfaces.Ergod.Theory Dyn.Syst.28,1729–1748(2008)4.Cohen,M.:Looking for a Billiard Table which is not a Lattice Polygon but satisfies the Veech dichotomy,M.Sc.thesis,Ben-Gurion University(2010)/pdf/1011.32175.DeMarco,L.:The conformal geometry of billiards.Bull.AMS48(1),33–52(2011)6.Eskin,A.,Marklof,J.,Morris,D.:Unipotentflows on the space of branched covers of Veech surfaces.Ergod.Theorm Dyn.Syst.26(1),129–162(2006)7.Fox,R.H.,Kershner,R.B.:Concerning the transitive properties of geodesics on a rational polyhe-dron.Duke Math.J.2(1),147–150(1936)8.Gutkin,E.,Hubert,P.,Schmidt,T.:Affine diffeomorphisms of translation surfaces:Periodic points,Fuchsian groups,and arithmeticity.Ann.Sci.École Norm.Sup.(4)36,847–866(2003)9.Hubert,P.,Schmidt,T.:Infinitely generated Veech groups.Duke Math.J.123(1),49–69(2004)10.Masur,H.,Tabachnikov,S.:Rational billiards andflat structures.In:Handbook of dynamical systems,vol.1A,pp.1015–1089.North-Holland,Amsterdam(2002)11.Smillie,J.,Weiss,B.:Veech dichotomy and the lattice property.Ergod.Theorm.Dyn.Syst.28,1959–1972(2008)Geom Dedicata12.Veech,W.A.:Teichmüller curves in moduli space,Eisenstein series and an application to triangularbilliards.Invent.Math.97,553–583(1989)13.V orobets,Y.:Planar structures and billiards in rational polygons:the Veech alternative.(Russian);trans-lation in Russian Math.Surveys51(5),779–817(1996)14.Ward,C.C.:Calculation of Fuchsian groups associated to billiards in a rational triangle.Ergod.TheoryDyn.Syst.18,1019–1042(1998)15.Zemlyakov,A.,Katok,A.:Topological transitivity of billiards in polygons,Math.Notes USSR Acad.Sci:18:2291–300(1975).(English translation in Math.Notes18:2760–764)16.Zorich,A.:Flat surfaces.In:Cartier,P.,Julia,B.,Moussa,P.,Vanhove,P.(eds.)Frontiers in numbertheory,physics and geometry,Springer,Berlin(2006)123。

外文翻译格式

外语翻译通常需要遵循一定的格式,以确保翻译内容的准确性和易读性。

以下是一个700字外文翻译的通用格式示例:

1. 标题:翻译的内容的标题,通常与原文标题保持一致,居中显示。

2. 原文:原文内容,可将原文段落编号,并保留原文格式,如段落缩进或列表。

3. 译文:相关段落的翻译内容,与原文一一对应,并保持相同的段落编号和格式。

4. 术语翻译:将翻译中使用的特定术语或固定表达进行解释和翻译,避免出现歧义。

5. 校对与审校:对翻译内容进行校对和审校,确保翻译准确无误。

6. 结论:对整个翻译内容进行总结和评价,提出自己的观点和见解。

7. 参考文献:如有需要,列出翻译过程中所参考的文献或资料。

8. 附录:如有需要,可在翻译后添加附录,补充相关资料或说明。

注意事项:

- 翻译应遵循专业的术语和语法规范,尽量保持翻译内容的准确性。

- 可根据需要调整段落的分配和序号,以符合原文和翻译内容的逻辑结构。

- 保持翻译格式的统一和美观,使用合适的字体和字号,并注意标点符号的使用。

- 翻译结束后,应进行校对和审校,以确保翻译质量的准确性和流畅性。

总之,一个700字外文翻译的格式应该清晰明了,结构合理,准确无误,并能为读者提供一个清晰且易于理解的翻译内容。

Hotel Management System IntegrationServices1.IntroductionIt is generally accepted that the role of the web services in businesses is undoubtedly important. More and more commercial software systems extend their capability and power by using web services technology. Today the e-commerce is not merely using internet to transfer business data or supporting people to interact with dynamic web page, but are fundamentally changed by web services. The World Wide Web Consortium's Xtensible Markup Language (XML) and the Xtensible Stylesheet Language (XSL) are standards defined in the interest of multi-purpose publishing and content reuse and are increasingly being deployed in the construction of web services. Since XML is looked as the canonical message format, it could tie together thousands of systems programmed by hundreds of programming languages. Any program can be mapped into web service, while any web service can also be mapped into program. In this paper, we present a next generation commercial system in hotel industry that fully integrates the hotel Front Office system, Property Management System, Customer Relationship Management System, Quality Management system, Back Office system and Central Reservations System distributed in different locations. And we found that this system greatly improves both the hotel customer and hotel officer’s experiences in the hotel business work flow. Because current technologies are quite mature, it seems no difficulty to integrate the existing system and the new coming systems (for example, web-based applications or mobile applications). However, currently in hotel industry there are few truly integrated systems used because there are so many heterogeneous systems already exist and scalability, maintenance, price, security issues then become huge to be overcome. From our study on Group Hotel Integration Reservation System (GHIRS), there are still challenges to integrate Enterprise Information System (EIS), Enterprise Information Portal system (EIP), Customer Relationship Management system (CRM) and Supply Chain Management system (SCM) together because of standardization, security and scalability problems, although GHIRS is one of few integration solutions to add or expand hotel software system in any size of hotel chains environment.We developed this system to integrate the business flow of hotel management by using webservices and software integration technologies. In this paper, firstly we describe a scenario of hotel reservation and discuss the interaction between GHIRS and human. Secondly we analyze details of design and implementation of this system. The result and implications of the studies on the development of GHIRS are shown in the later part. Finally we discuss some problems still need to be improved and possible future directions of development.2. Hotel Reservation: A Business Case StudyOur initial thinking to develop GHIRS is to minimize the human interaction with the system. Since GHIRS is flexible and automated, it offers clear benefits for both hotel customers and hotel staff, especially for group hotel customers and group hotel companies. Group hotel companies usually have lots of hotels, restaurants, resorts, theme parks or casinos in different locations. For example, Shangri-La group has hundreds of hotels in different countries all over the world. These groups have certain customers who prefer to consume in hotels belong to the same group because they are membership of the group and can have individual services.The first step of a scenario of hotel reservation is that the consumer plans and looks for a hotel according the location, price or whatever his criteria and then decides the hotel. Then he makes a reservation by telephone, fax, internet, or mail, or just through his travel agent. When hotel staff receives the request, they first look if they can provide available services. If there is enough resource in the hotel, they prepare the room, catering and transportation for the request and send back acknowledgement. At last the guest arrives and checks in. The business flow is quite simple; however, to accomplish all these tasks is burdensome for both the consumer side and the hotel side without an efficient and integrated hotel management system.Telephone may be a good way to make a reservation because it is beyond the limit of time and space. Guests can call hotels at any time and any place. However, it costs much when the hotel is far away from the city where guest lives; especially the hotel locates in a different country. Moreover, if there is a group of four or five people to make reservation together, it would take a long time for hotel staff to record all the information they need. Making reservation by travel agent saves consumers’ time and cost, but there is still millions of work for agent to do. They gather the requirements from consumers, then distribute to proper destination hotels. Becausethese hotels don’t use a same system (these thousand s of hotels may use hundreds of management systems), someone, agent or hotel staff, must face the problem how to handle information from different sources with different hotel management systems to different destinations.Web service becomes the tool to solve these problems. Our web services integrate the web server and hotel management system together, and everyone gets benefit. Booking a room easily anywhere and anytime becomes possible by using GHIRS. Consumer browses websites and finds hotel using his PC, PDA or mobile phone (W AP supported), after his identity is accepted, he can book a reservation. Two minutes later he can get the acknowledgement from the hotel by mobile phone text message or multimedia message, or email sent to his email account or just acknowledgement on the dynamic web page, if he hasn’t leave the website. The response time may take a little longer because when the hotel receives the quest, in some circumstance, hotel staff should check if there is clean and vacant room left. The web service is a standard interface that all travel agents can handle, gather and distribute the reservation information easily through internet. When the reservation request is acknowledged, hotel staff prepares the room, catering, and transportation for guests. Since the information already stored in the database, every part in the hotel chains can share it and work together properly. For example, staff in front office and housekeeping department can prepare room for guests according to the data, staff in back office can stock material for catering purpose and hotel manager can check business report in Enterprise Information Portal integrated with GHIRS by his browser. Then room rent-ratio reports, room status reports, daily income reports and other real time business reports are generated. Managers of the group can access any report of any hotel by the system. In the later part of this paper, we will show how consumers, agents, and hotel staff can efficiently work together by GHIRS.GHIRS is scalable for small-to-large hotel chains and management companies, especially good for hotel group. It truly soars with seamless connectivity to global distribution systems thereby offering worldwide reservation access. It also delivers real-time, on line reservations via the Internet.3. Integration of Hotel Management SystemGHIRS is developed on the base of an existed hotel management system called FoxhisTM.FoxhisTM shares the largest part of software market in hotel industry in China. FoxhisTM version 5 has distributed Client/Server architecture that the server runs SCO-UNIX and client runs Microsoft Windows and it use Sybase database on UNIX. The system includes Front Office system, Property Management system, Quality Management system, Human Resource Management system, Enterprise Information Portal system (EIP), Customer Relationship Management system (CRM) and Supply Chain Management system (SCM).This system is largely based on intranet environment. Most of the work is done in a single hotel by the hotel staff. It’s no customer self-service. If a consumer wants to book a room, hotel staff in local hotel must help the guest to record his request, although FoxhisTM system already done lots of automatic job.When the systems are deployed in different hotels that are parts of a group, sharing data becomes a problem. Just as an example, if the group has ten hotels, there would be at least ten local databases to store the consumers’ data. Because hotels need real time respond of the system, so these ten hotels can’t deploy a central database that does not locate in the same local network. Thus one guest may have different records in different hotels and the information cannot be shared. By web services as an interface, these data can be exchanged easily.Recall that our initial thinking to deploy GHIRS is to save hotel staff, travel agents and consumers’labor work the system is to link all the taches of hotel business chains. Figure1 shows how consumers, agents, hotel staff cooperate together efficiently with the system.Consumers could be divided into two categories. One is member of hotel group, who holds different classes of memberships and gains benefits like discount or special offers. These consumers usually contribute a lar ge part of the hotel’s profit then are looked as VIP. The hotel keeps their profiles, preferences and membership account status. The other category is common guest. All these two kinds of guests and travel agents who may trade with many other hotels face the web-based interface that let them to make a reservation. For common guest, the system just requires him to input reservation information such as guest name, contact information, arrival and departure the system. The central processing server then distributes the information to appropriate hotel. Since web services technology is so good for submitting documents to long running business process flows, hotel staff could easily handle this data in andout of database management system and application server. As the membership of hotel, a user just inputs his member id and password, room information, arrival and departure date, then finish the request. Because hotels keep members’ profile, and systems exchange profile across all hotels of the group by web serv ices, hotel staff in different hotels could know the guest’s individual requirement and provide better services.The agents work for consumers get benefits from GHIRS as well. They may also keep the consumers’ profile and the web services interface is op en to them, it is easy to bridge their system to hotel management system. Before GHIRS is deployed, the agents should separate and process the reservation data and distribute them to different hotels, which is an onerous job. But now the agents could just press one button and all the hotel reservation is sent to destination.Hotel staff receives all request from different sources. Some policies are applied to response the request. For example, some very important guest’s request is passed automatically wi thout confirmation, the guest could get acknowledgement in very short time. The request triggers all chains of the hotel business flow and all the preparation work is done before his arrival. But for the common customer, hotel staff would check on the anticipate date if there is vacant and clean rooms available. Because all the FoxhisTM components are integrated together, staff users needn’t change computer interface to check he room status. If it is a valid request with enough guests’ information and there is enough room left, a confirmation is sent back. If there is not enough vacant room, hotel staff will ask if guest would like to wait a time or transfer to other hotels in the hotel group or alliance hotels. In order to transfer guest’s request, data flow s from local database to the central server through local web server, then it is passed to another hotels database by web services interface.Today there are lots of platforms that could provide capabilities to integrate different system and offer other features such as security and work load balancing. The two main commercial products are Java2 Enterprise Edition (J2EE) and . They offer pretty much the same laundry of list of features, albeit in different ways. We choose .NET platform as our programming environment, however, here we don’t advocate which platform is better or not. Our target is to integrate these decentralized and distributed systems together. In fact, both of these platforms support XML and SOAP to accomplish our task.We use Microsoft Internet Information Services (IIS) as web server and Sybase databaseserver. The firewalls separate the local networks from the public networks. This is very important from the security point of view. Each hotel of the group has a database server, an application server and a web server to deploy this multi-tier system that includes the user interface presentation tier, business presentation tier, business logical tier, and the data access tier. C# is adopted as the programming language for the core executable part. XML is the data exchange standard format.From:/link?url=u5PQlr59n0dA VI-V09htSseEFFmyLzwI5P7AR42ULwI7 okjG08MmwqYRvV_LbVYnj6XcxiEVbS5xlTpOhidIDdIrYo-h_3dU-v7QNgTtmMm酒店管理系统集成服务1.简介人们普遍认为,网络服务角色在企业中无疑是重要的。

知网外文翻译

知网外文翻译是指将英语及其他外语的文献,通过专业的翻译技

巧转化为中文文献的服务。

这是因为在学术研究中,英语和其他外语

文献的数量和质量都非常丰富,但由于我国大部分学者和研究者的语

言能力有限,无法阅读和理解这些文献。

因此,知网外文翻译成为了

他们获取信息的必要渠道。

关于知网外文翻译,其主要途径为:

1.在线翻译

使用在线翻译软件或一些自动翻译网站进行翻译。

但是,由于机器翻

译的精度和质量有限,翻译结果常常出现语义不通、用词不当等问题,难以满足学术研究的要求。

2.人工翻译

通过手动翻译,将外文文献翻译为中文文献。

相比于机器翻译,人工

翻译可以更好地保持语言和内容的准确性,更加符合学术研究的要求。

在进行知网外文翻译的过程中,一些需要注意的问题:

1.翻译者的语言能力必须达到一定水平,既要熟练掌握源语言也

要精通目标语言。

2.翻译者需要了解源文背景知识和研究领域的专业术语等。

3.翻译需要准确无误,同时要保持原文的风格和语调。

总之,在知网外文翻译方面,应该选择专业的翻译机构进行翻译,以保证翻译质量和准确性。

同时,学术研究者应该对翻译结果进行审

查和修订,确保翻译结果符合学术要求。

知网外文翻译是学术研究的必要手段之一,通过专业的翻译,可

以帮助学者和研究者更好地获取全球最新的学术成果,拓宽知识视野,提高学术水平。

因此,我们应该加强对知网外文翻译的认识,选择优

秀的翻译机构,提高我们的学术水平。

嘉兴学院毕业论文(设计)外文翻译撰写格式规范一、外文翻译形式要求1、要求本科生毕业论文(设计)外文翻译部分的外文字符不少于1.5万字, 每篇外文文献翻译的中文字数要求达到2000字以上,一般以2000~3000字左右为宜。

2、翻译的外文文献应主要选自学术期刊、学术会议的文章、有关著作及其他相关材料,应与毕业论文(设计)主题相关,并作为外文参考文献列入毕业论文(设计)的参考文献。

3、外文翻译应包括外文文献原文和译文,译文要符合外文格式规范和翻译习惯。

二、打印格式嘉兴学院毕业论文(设计)外文翻译打印纸张统一用A4复印纸,页面设置:上:2.8;下:2.6;左:3.0;右:2.6;页眉:1.5;页脚:1.75。

段落格式为:1.5倍行距,段前、段后均为0磅。

页脚设置为:插入页码,居中。

具体格式见下页温馨提示:正式提交“嘉兴学院毕业论文(设计)外文翻译”时请删除本文本中说明性的文字部分(红字部分)。

嘉兴学院本科毕业论文(设计)外文翻译题目:(指毕业论文题目)学院名称:服装与艺术设计学院专业班级:楷体小四学生姓名:楷体小四一、外文原文见附件(文件名:12位学号+学生姓名+3外文原文.文件扩展名)。

二、翻译文章翻译文章题目(黑体小三号,1.5倍行距,居中)作者(用原文,不需翻译,Times New Roman五号,加粗,1.5倍行距,居中)工作单位(用原文,不需翻译,Times New Roman五号,1.5倍行距,居中)摘要:由于消费者的需求和汽车市场竞争力的提高,汽车检测标准越来越高。

现在车辆生产必须长于之前的时间并允许更高的价格进行连续转售……。

(内容采用宋体五号,1.5倍行距)关键词:汽车产业纺织品,测试,控制,标准,材料的耐用性1 导言(一级标题,黑体五号,1.5倍行距,顶格)缩进两个字符,文本主体内容采用宋体(五号),1.5倍行距参考文献(一级标题,黑体五号, 1.5倍行距,顶格)略(参考文献不需翻译,可省略)资料来源:AUTEX Research Journal, V ol. 5, No3, September 2008*****译****校(另起一页)三、指导教师评语***同学是否能按时完成外文翻译工作。

论文写作中的外文翻译一、引言在如今全球化的时代,全球各个领域的学术研究都离不开海量的国际文献阅读。

然而,对于非英语母语的研究者来说,理解和运用外文文献成为了一个常见的挑战。

本文将探讨论文写作中外文翻译的重要性、技巧和对于学术研究的影响。

二、外文翻译的重要性1. 探索全球化的学术前沿外文翻译是获得国际学术研究成果的主要途径之一。

通过阅读和翻译外文文献,研究者可以了解全球学术前沿,并在自己的研究中借鉴和应用国际领先的研究成果,从而提高论文的质量和学术水平。

2. 拓宽研究视野翻译外文文献能够帮助研究者拓宽自己的研究视野。

不同国家和地区的学术界存在着不同的研究思路和方法,通过翻译外文文献,研究者可以深入了解其他学术领域的研究思想,为自己的研究提供新的思路和视角。

三、外文翻译的技巧1. 字典和翻译工具的运用在进行外文翻译时,合理利用字典和翻译工具是提高翻译效率和准确性的重要手段。

目前,市面上存在着众多的在线翻译工具和专业字典,研究者可以结合使用这些工具来更好地理解和翻译外文文献。

2. 上下文理解的重要性在进行外文翻译时,不仅需要理解每个词语的字面意思,更需要理解其在上下文中的含义。

上下文的语言环境会影响某个词的具体意思,因此,在进行翻译的过程中,研究者要通过上下文的分析来准确理解和翻译外文文献。

3. 注意语法和语义的转换不同语言之间存在着语法和语义的差异,研究者在进行外文翻译时需要注意将原文的语法和语义转换成适合目标语言的表达方式。

例如,英语中的被动语态在中文中要转换为主动语态,翻译时需要灵活运用语言表达的规则。

四、外文翻译对学术研究的影响1. 提高学术研究的质量外文翻译能够使研究者更深入地理解和掌握国际学术研究成果,为自己的学术研究提供新的思路和方法。

通过引用国际文献,研究者能够提高论文的可信度和学术价值,从而提高自己的研究质量。

2. 增强跨文化的交流和合作外文翻译能够促进国际学术界的跨文化交流和合作。