巴基斯坦进口清关所需要资料及税款计算公式

- 格式:doc

- 大小:36.00 KB

- 文档页数:1

巴基斯坦税费简介工程项目在巴基斯坦涉及的主要税种简介章节2 –工程项目在巴基斯坦涉及的主要税种简介工程项目在巴基斯坦涉及的主要税种简介根据巴基斯坦当地的相关法律规定,外国企业在巴基斯坦境内开展EPC合同中规定的相关经营活动,必须要在当地建立商业实体。

根据实际需要,贵司可以考虑选择的商业实体形式有分公司和子公司(私人有限公司)两种。

一般情况下,外国企业在巴基斯坦设立子公司的形式或分公司的形式从事EPC工程项目涉及以下主要税种:般情况下外国企业在巴基斯坦设立子公司的形式或分公司的形式从事–企业所得税(Tax on Corporate Income)–利润汇回预提税(Withholding Tax on Profit Distribution)增值税(Value Added Tax)–(Value Added Tax)–个人所得税(Tax on Personal income)–社会保险(Social Security) (社会保险不属于税项,但作为雇主的一项成本,我们将其包含在税种简介中)–员工福利基金(Workers’ Welfare Fund)–其他税种(主要包括关税、联邦消费税、印花税等)工程项目在巴基斯坦涉及的主要税种简介章节2 –工程项目在巴基斯坦涉及的主要税种简介企业所得税在巴基斯坦从事商业经营活动的居民企业和非居民企业(在特定条件下)需要在巴基斯坦缴纳企业所得税收入的性质支付对象预提税税率(在特定条件下)需要在巴基斯坦缴纳企业所得税。

目前巴基斯坦有两种所得税征收制度:净利润制度(NIB)和最终税负制度(FTR)。

–一般而言,巴基斯坦所得税纳税人需要以净利润为基技术服务费和特许权使用费非居民企业15%执行合同取得的收入(包括施工、组装、安装等)居民/非居民企业6%产品销售居民企业 3.5%础计算应税所得并按照35%的税率缴纳所得税;–但是从事特定行业的纳税人需要根据最终税负制度缴纳所得税,其中居民企业(如外国企业当地投资设立的子公司)必须按照最终税负制度缴税,而非居民企股息收入(包括分公司向总公司的利润汇回)居民/非居民企业10%商品进口居民/非居民企业3% 至5%出业(如外国企业在巴基斯坦的分公司)可以选择按照此制度缴税;在最终税负制度下,纳税人需要在取得相关收入时缴纳预提税(由支付人扣缴),并作为所得税最终税负,而无需就相关收入再额外计算缴纳所得税,但相应的也不能对相关经营费用进行扣除。

进口关税计算公式导言进口关税是国家对进口商品征收的一种税收形式。

它既可以作为保护国内产业的手段,也可以作为调节贸易平衡的工具。

进口关税的计算方法直接关系到企业和个人的进口成本,因此了解和掌握进口关税的计算公式对于进口贸易行业非常重要。

本文将介绍进口关税的基本概念和计算公式。

一、进口关税的基本概念进口关税是指国家根据贸易法规定,对进口商品征收的税费。

它主要包括关税税率和关税计算基数两个方面。

关税税率是对进口商品征收的税率,通常以百分比来表示。

关税计算基数是指进口商品的完税价格,即商品的成交价格加上海关处理费、保险费和运费等相关费用。

进口关税的计算公式一般为:进口关税=关税计算基数×关税税率二、关税计算公式的说明1. 关税计算基数的确定关税计算基数由进口商品的完税价格组成。

完税价格是指商品在境外出口国家的销售价格,需要加上一些相关费用。

这些相关费用包括海关处理费、保险费和运费等。

海关处理费是指处理进口商品所需的相关费用,包括检验、检疫、清关等。

保险费是进口商品在运输过程中所需的保险费用。

运费是指商品从出口国家到进口国家所需的运输费用。

这些费用的加入,可以更准确地反映出进口商品的真实成本。

2. 关税税率的确定关税税率是根据国家贸易政策和国际贸易协定等因素来确定的。

关税税率通常以百分比来表示,并根据不同的商品分类进行规定。

在世界贸易组织框架下,各国之间签订了多项贸易协定和自由贸易协定,这些协定对于关税税率的确定有一定的规定。

因此,在进口商品时,需要根据商品的分类和相关贸易协定来确定关税税率。

3. 进口关税的计算根据以上说明,可以将进口关税的计算公式简化为:进口关税=完税价格×关税税率。

当然,在实际操作中,可能还需要考虑其他因素,如加工贸易、特殊关税减免等。

这些因素将根据具体情况来确定具体的计算方法。

三、进口关税计算的实际应用进口关税的计算方法直接影响着进口商品的成本和价格,因此在进口贸易中有着极其重要的应用价值。

报关员- 进出口税费的计算及公式进出口税费的计算海关征收的关税、进口环节税、滞纳金、滞报金、监管手续费等一律以人民币计征。

进出口货物的成交价格如以外币计价的,应当由海关按照填发《海关专用缴款书》和《海关行政事业收费专用票据》之日国家外汇管理部门公布的《人民币外汇牌价表》的买卖中间价,折合成人民币后计征。

提前报关的转关货物,其汇率以指运地海关接收到进境地海关传输的转关放行信息之日的计算机系统中的汇率计算。

如运输途中汇率发生重大调整的,以转关货物运抵指运地海关之日的汇率计算。

海关征收的税费是以人民币征收,计算税款前要将审核的完税价格折算成人民币;完税价格计算至分,元以下的四舍五入;税额计算到分,分以下四舍五入;税款的起征点为人民币50元。

一、进出口关税计算(一)进口关税税款的计算,目前我国对进口关税采用的计征标准有:从价关税、从量关税和复合关税3种。

1.从价关税(1)从价关税是以进口货物的完税价格作为计税依据,以应征税额占货物完税价格的百分比作为税率,货物进口时,以此税率和实际完税价格相乘计算应征税额。

(2)计算公式:正常征收的进口关税税额=完税价格*法定进口关税税率减税征收的进口关税税额=完税价格*减按进口关税税率(3)计算程序:①按照归类原则确定税则归类,将应税货物归入恰当的税目税号;②根据原产地规则,确定应税货物所适用的税率;③根据完税价格审定办法和规定,确定应税货物的完税价格;④根据汇率使用原则,将外币折算成人民币;⑤按照计算公式正确计算应征税款。

(4)计算实例实例一:国内某公司向香港购进日本皇冠牌轿车10辆,成交价格共为FOB香港120,000.00美元,实际支付运费5,000美元,保险费800美元。

已知汽车的规格为4座位,汽缸容量2,000cc,外汇折算率1美元二人民币8.2元,要求计算进口关税。

[计算方法)确定税则归类,汽缸容量2,000cc的小轿车归入税目税号8703.2314;原产国日本适用最惠国税率43.8%;审定完税价格为125,800美元(120,000.00美元+5,000美元+800美元);将外币价格折算成人民币为1,031,560.00元;正常征收的进口关税税额二完税价格X法定进口关税税率=1,031,560X43.8%=451,823.28(元)实例二:国内某远洋渔业企业向美国购进国内性能不能满足需要的柴油船用发动机2台,成交价格为CIF境内目的地口岸680,000.00美元。

关税怎么计算现在我们的对外贸易还是很发达的,涉及进⼝和出⼝贸易的,这样的话就是需要申报缴纳关税的,⼀般分为进⼝和出⼝关税的,税率是不同的,分为⼏种情况的,下⾯就由店铺⼩编给⼤家讲解⼀下有关海关关税的计算⽅法等法规。

关税怎么计算计算关税的相关公式1.从价税,适⽤于:⼀般的(出)⼝货物计算公式:应纳税额=应税进(出)⼝货物数量*单位完税价格*适⽤税率2.从量税,适⽤于:进⼝啤酒、原油等计算公式:应纳税额=应税进⼝货物数量*关税单位税额3.复合税,适⽤于:进⼝⼴播⽤录录像机、⽅像机、摄像机等计算公式:应纳税额=应税进⼝货物数量*关税单位税额+应税进⼝货物数量*单位完税价格*适⽤税率4.滑准税,适⽤于:进⼝规定适⽤滑准税的商品计算公式:进⼝商品价格越⾼。

(⽐例)税率越低;税率与商品进⼝价格反⽅向变动。

海关监管货物说明海关监管货物是指所有进出境货物,包括海关监管时限内的进出⼝货物,过境货物、转运货物、通运货物,特定减免税货物,以及暂时进出⼝货物、保税货物和其他尚未办结海关⼿续的进出境货物。

(1)⾃向海关申报起到出境⽌的出⼝货物;(2)⾃进境起到办结海关⼿续⽌的进⼝货物;(3)⾃进境起到出境⽌的过境、转运和通运的货物按货物进出境的不同⽬的划分,可以分成五⼤类:1.⼀般进出⼝货物。

指从境外进⼝,办结海关⼿续直接进⼊国内⽣产或流通领域的进⼝货物,及按国内商品申报,办结出⼝⼿续到境外消费的出⼝货物。

2.保税货物。

指经海关批准未办理纳税⼿续⽽进境,在境内储存、加⼯、装配后复运出境的货物。

此类货物⼜分为保税加⼯货物和保税物流货物两类。

3.特定减免税货物。

指经海关依据有关法律准予免税进⼝的⽤于特定地区、特定企业、有特定⽤途的货物。

4.暂准进出境货物。

指经海关批准,凭担保进境或出境,在境内或境外使⽤后,原状复运出境或进境的货物。

5.其他进出境货物。

指由境外启运,通过中国境内继续运往境外的货物,以及其他尚未办结海关⼿续的进出境货物。

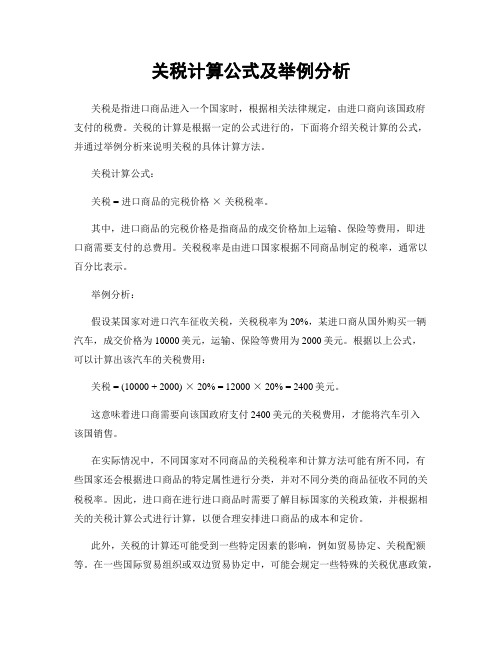

关税计算公式及举例分析关税是指进口商品进入一个国家时,根据相关法律规定,由进口商向该国政府支付的税费。

关税的计算是根据一定的公式进行的,下面将介绍关税计算的公式,并通过举例分析来说明关税的具体计算方法。

关税计算公式:关税 = 进口商品的完税价格×关税税率。

其中,进口商品的完税价格是指商品的成交价格加上运输、保险等费用,即进口商需要支付的总费用。

关税税率是由进口国家根据不同商品制定的税率,通常以百分比表示。

举例分析:假设某国家对进口汽车征收关税,关税税率为20%,某进口商从国外购买一辆汽车,成交价格为10000美元,运输、保险等费用为2000美元。

根据以上公式,可以计算出该汽车的关税费用:关税 = (10000 + 2000) × 20% = 12000 × 20% = 2400美元。

这意味着进口商需要向该国政府支付2400美元的关税费用,才能将汽车引入该国销售。

在实际情况中,不同国家对不同商品的关税税率和计算方法可能有所不同,有些国家还会根据进口商品的特定属性进行分类,并对不同分类的商品征收不同的关税税率。

因此,进口商在进行进口商品时需要了解目标国家的关税政策,并根据相关的关税计算公式进行计算,以便合理安排进口商品的成本和定价。

此外,关税的计算还可能受到一些特定因素的影响,例如贸易协定、关税配额等。

在一些国际贸易组织或双边贸易协定中,可能会规定一些特殊的关税优惠政策,例如降低关税税率、免除关税等,以促进贸易自由化和促进经济发展。

因此,进口商还需要考虑这些因素,并结合实际情况进行关税的计算和申报。

总之,关税是国际贸易中不可或缺的一环,其计算方法是根据一定的公式和相关政策进行的。

通过以上的公式和举例分析,我们可以更好地理解关税的计算方法,并在实际的进口贸易中进行合理的成本控制和风险管理。

希望本文能对读者有所帮助,谢谢阅读!。

销售税是联邦政府根据《销售税法案1990》针对货物(包括进口)和服务的销售供应征收的一种税。

*概念梳理进项税(Input Tax):进项税额是税号注册人对他所购买或取得的应税商品和劳务支付的税款。

销项税(Output Tax):销售或供应货物或服务时征收的销售税。

消费税的调整(增值税):以商品(含应税劳务)在流转过程中产生的增值额作为计税依据而征收的一种流转税。

公式:销项税-进项税:进项税额调整是指从销项税中扣除进项税额,达到纳税人应纳税额的净额。

由于销售税是一种增值税,在每一个增值阶段都要征收。

为避免双重征税,对进项税进行调整,计算出正确的政府应纳税额。

例:如果一个注册的人购买了成本为100卢比的商品,而他/她被收取15%(即为15卢比)的销售税(进项税),那么他的总购买价就会变成115卢比。

如果后来他/她以200卢比的价格销售货物,并收取15%(即30卢比)作为销项税,则他的总销售价格将变为230卢比。

此时他/她的应税款额即增值税为:30-15=15卢比。

* Sales Tax Records 销售税记录税号注册人须在经营过程中,用英文或乌尔都语对所有提供、购买或进口的商品和服务进行记录。

* Record of Sales 销售记录销售记录应注明提供的货物或服务的下列细节:description; 描述quantity; 数量value; 价值name and address of the customer; 客户名称和地址amount of tax charged 收取的税额文章内容摘自《Sales Tax Guide(Taxpayer's Facilitation Guide) Brochure 015 January,2008》,仅供参考。

各国进⼝所需清关⽂件和产地证(外贸篇)1、⼀般产地证(C/O),⼀般原产地证是证明货物原产于某⼀特定国家或地区,享受进⼝国正常关税(最惠国)待遇的证明⽂件,它的适⽤范围是:征收关税、贸易统计、歧视性数量限制、反倾销和反补贴、原产地标记、政府采购等⽅⾯。

任何国家都可以做CO。

全称:CERTIFICATE OF ORIGIN 。

2、FORM A普惠制原产地证明书,是具有法律效⼒的我国出⼝产品在给惠国税率基础上进⼀步减免进⼝关税的官⽅凭证。

世界给予我国优惠的国家有38个(也就是说,只有出⼝到这些国家才做F/A):欧盟27国(⽐利时、丹麦、英国、德国、法国、爱尔兰、意⼤利、卢森堡、荷兰、希腊、葡萄⽛、西班⽛、奥地利、芬兰、瑞典、波兰、捷克、斯洛伐克、拉脱维亚、爱沙尼亚、⽴陶宛、匈⽛利、马⽿他、塞浦路斯、斯洛⽂尼亚、保加利亚、罗马尼亚)、挪威、瑞⼠、⼟⽿其、俄罗斯、⽩俄罗斯、乌克兰、哈萨克斯坦、⽇本、加拿⼤、澳⼤利亚和新西兰。

全称:GENERALIZED SYSTEM OF PREFERENCES CERTIFICATEOFORIGIN 。

3、FORM E 是中国-东盟⾃贸区使⽤的优惠性原产地证书。

⽬前,我国对外签发FORM E证书的国家包括⽂莱、柬埔寨、印度尼西亚、⽼挝、马来西亚、缅甸、菲律宾、新加坡、泰国、越南10国。

FORM D 是东盟⾃贸区原产地证书。

(FORM D等于FORM E,⼀般国外喜欢叫FORM D) 。

4、中国—智利⾃由贸易区原产地证书(FORM F) 中华⼈民共和国政府和智利共和国政府⾃由贸易协定 ,单个中国-智利⾃贸区FORM F原产地证书!5、《〈中国与巴基斯坦⾃由贸易区〉优惠原产地证明书》(FORM P) 对巴基斯坦可以签发《〈中国与巴基斯坦⾃由贸易区〉优惠原产地证明书》,2006年1⽉1⽇起双⽅先期实施降税的3000多个税⽬产品,分别实施零关税和优惠关税.原产于中国的486个8位零关税税⽬产品的关税将在2年内分3次逐步下降,2008年1⽉1⽇全部降为`零,原产于中国的486个8位零关税税⽬产品实施优惠关税,平均优惠幅度为22%.给予关税优惠的商品其关税优惠幅度从1%到10%不等。

进出口税费的计算与缴纳实例1. 引言进出口业务在国际贸易中扮演着重要角色,但在进行进出口业务时,需要了解和计算相关的税费,以确保交易的合法性和利润。

本文将以进出口税费的计算与缴纳实例为主题,介绍进出口税费的计算方法和实际操作。

2. 进口税费的计算与缴纳2.1 进口税费的种类进口税费主要包括关税、增值税和消费税等。

关税是根据商品的类别和产地等因素确定的,增值税和消费税是根据商品的价值确定的。

进口税费的类型和税率根据国家和地区的政策而有所不同。

2.2 进口税费的计算公式进口税费的计算公式如下:总进口税费 = 关税 + 增值税 + 消费税其中,关税的计算公式为:关税 = 关税税率 × (进口商品的完税价格 + 运费 + 保险费)增值税的计算公式为:增值税 = (进口商品的完税价格 + 关税 + 运费 + 保险费) × 增值税税率消费税的计算公式为:消费税 = (进口商品的完税价格 + 关税 + 运费 + 保险费) × 消费税税率进口税费的缴纳通常由进口商负责。

进口商需要根据海关提供的进口税费计算结果,按规定的时间和方式缴纳相应的税款。

通常,进口商可选择自行办理进口税费的缴纳,或委托专业的报关公司代为办理。

3. 出口税费的计算与缴纳3.1 出口税费的种类出口税费主要包括关税和退税等。

关税是根据商品的类别和目的地等因素确定的,退税是根据商品的出口价值确定的。

3.2 出口税费的计算公式出口税费的计算公式如下:总出口税费 = 关税 - 退税出口税费的缴纳通常由出口商负责。

出口商需要根据海关提供的出口税费计算结果,按规定的时间和方式缴纳相应的税款。

通常,出口商可选择自行办理出口税费的缴纳,或委托专业的报关公司代为办理。

4. 进出口税费的实际操作4.1 进口税费的实际操作进口商在进行进口业务时,需要按照以下步骤进行进口税费的计算和缴纳:1.获取进口商品的完税价格,即商品的成交价格加上运费和保险费。

Chapter 98(SERVICES)Heading Description FED98.019801.1000 9801.2000 9801.3000 9801.4000 9801.5000 9801.60009801.7000 9801.9000Services provided or rendered by hotels, restaurants, marriage halls, lawns, clubsand caterers.Services provided or rendered by hotelsServices provided or rendered by restaurantsServices provided or rendered by marriage halls and lawnsServices provided or rendered by clubsServices provided or rendered by caterers, suppliers of food and drinksAncillary services provided or rendered by hotels, restaurants, marriage halls, lawns,caterersServices provided or rendered by messes and hostelsOther16% of the charges98.02 9802.1000 9802.2000 9802.3000 9802.4000 9802.5000 9802.9000Advertisements.Advertisement on T.V.Advertisement on radioAdvertisement on closed circuit T.V.Advertisement in newspapers and periodicalsAdvertisement on cable T.V networkOther16% of the charges98.03 9803.1000 9803.1100 9803.2000 9803.2100 9803.9000Facilities for travel.Travel by air of passengers within the territorial jurisdiction of Pakistan.Travel by air of passengers embarking on international journey from PakistanDomestic travel by trainInternational travel by trainOther16% of the charges98.04 9804.1000 9804.2000 9804.9000Services provided or rendered for inland carriage of goods.Carriage of goods by airCarriage of goods by trainOther16% of the charges98.05 9805.1000 9805.2000 9805.2100 9805.3000 9805.4000 9805.5000 9805.5100 9805.6000 9805.7000 9805.8000 9805.9000 9805.9100 9805.9200 9805.9090Services provided or rendered by persons authorized to transact business on behalfof others.Shipping agentsStevedoresShip management serviceFreight forwarding agentsCustoms agentsTravel agentsTour operatorsRecruiting agentsAdvertising agentsShip chandlersShare transfer agentSponsorship servicesBusiness support servicesOther16% of the charges9807.0000 Services provided or rendered by property developers and promoters. 16% of the charges 9808.0000 Courierservices. 16% of the charges9809.0000 Services provided or rendered by persons engaged in contractual execution of workor furnishing supplies.16% of the charges9810.0000 Services provided or rendered for personal care by beauty parlours/clinics,slimming clinics and others.16% of the charges 9811.0000 Services provided or rendered by laundries, dry cleaners. 16% of the chargesHeading Description FED98.12 9812.1000 9812.1100 9812.1200 9812.1210 9812.1220 9812.1300 9812.1400 9812.1500 9812.1600 9812.1700 9812.1710 9812.1720 9812.1910 9812.1920 9812.1930 9812.1940 9812.1950Telecommunication services.Telephone servicesFixed line voice telephone serviceWireless telephoneCellular telephoneWireless Local Loop telephoneVideo telephonePayphone cardsPre-paid calling cardsVoice mail serviceMessaging serviceShort Message service (SMS)Multimedia message service (MMS)Shifting of telephone connectionInstallation of telephone extensionProvision of telephone extensionChanging of telephone connectionConversion of NWD connection to non NWD or vice versa16% of the charges9812.1960 9812.1970 9812.1990 9812.2000 9812.2100 9812.2200 9812.2300 9812.2400 9812.2500 9812.2900 9812.3000 9812.4000 9812.5000 9812.5010 9812.5090 9812.6000 9812.6100 9812.6110 9812.6120 9812.6121 9812.6122 9812.6123 9812.6124 9812.6125 9812.6129Cost of telephone setRestoration of telephone connection OthersBandwidth servicesCopper line basedFibre-optic basedCo-axial cable basedMicrowave basedSatellite basedOthersTelegraphTelexTelefaxStore and forward fax servicesOthersInternet servicesInternet services including e-mail services Dial-up internet servicesBroadband services for DSL connection Copper line basedFibre-optic basedCo-axial cable basedWireless basedSatellite basedOthers9812.6130 9812.6140 9812.6190 9812.6200 9812.6210 9812.6220 9812.6230 9812.6240 9812.6250 9812.6290 9812.6300 9812.6310 9812.6320 9812.6390 9812.9000 9812.9100 9812.9200 9812.9300 9812.9400 9812.9410 9812.9490 9812.9500 9812.9090Internet/e-mail/Data/SMS/MMS services on WLL networksInternet/e-mail/Data/SMS/MMS services on cellular mobile networks OthersData Communication Network services (DCNS)Copper Line basedCo-axial cable basedFibre-optic basedWireless/Radio basedSatellite basedOthersValue added data servicesVirtual private Network service (VPN)Digital Signature serviceOthersAudiotext servicesTeletext servicesTrunk radio servicesPaging servicesVoice paging servicesRadio paging servicesVehicle tracking services.Burglar alarm services.OthersHeading Description FED98.139813.1000 9813.1100 9813.1200 9813.1300 9813.1400 9813.1500 9813.1600 9813.2000 9813.3000 9813.3010 9813.3020 9813.3030 9813.3090 9813.3900 9813.4000 9813.4100 9813.4200 9813.4300 9813.4400 9813.4500 9813.4600 Services provided or rendered by banking companies, insurance companies,cooperative financing societies, modarabas, musharikas, leasing companies,foreign exchange dealers, non-banking financial institutions and other personsdealing in any such services.Services provided or rendered in respect of insurance to a policy holder by an insurer,including a reinsurer.Goods insuranceFire insuranceTheft insuranceMarine insuranceLife insuranceOther insuranceServices provided or rendered in respect of advances and loansServices provided or rendered in respect of leasing.Financial leasingCommodity or equipment leasingHire-purchase leasingOtherServices provided or rendered in respect of musharika financingServices provided or rendered by banking companies in relation to:GuaranteeBrokerageLetter of creditIssuance of pay order and demand draftBill of exchangeTransfer of money including telegraphic transfer, mail transfer and electronic transfer16% of the charges9813.4700 9813.4800 9813.4900 9813.4910 9813.5000 9813.6000 9813.7000 9813.8000 9813.8100 9813.9000 Bank guaranteeBill discounting commissionSafe deposit lockersSafe vaultsIssuance, processing and operation of credit and debit cardsCommission and brokerage of foreign exchange dealings.Automated Teller Machine operations, maintenance and management.Service provided as banker to an issueOtherService provided or rendered by a foreign exchange dealer or exchange company or money changer98.14 9814.1000 9814.2000 9814.3000 9814.4000 9814.9000Services provided or rendered by architects, town planners, contractors, propertydevelopers or promoters, interior decorators.Architects or town plannersContractors of building (including water supply, gas supply and sanitary works), roads andbridges, electrical and mechanical works (including air conditioning), horticultural works,multi-discipline works (including turn-key projects) and similar other worksProperty developers or promotersLandscape designersOther16% of the charges98.15 9815.1000 9815.2000 9815.3000 9815.4000 9815.5000 9815.6000 9815.9000Services provided or rendered by professionals and consultants etc.Medical practitioners and consultantsLegal practitioners and consultantsAccountants and auditorsManagement consultantsTechnical, scientific, engineering consultantsSoftware or IT based system development consultantsOther consultants16% of the charges9816.0000 Services provided or rendered by pathological laboratories. 16% of the chargesHeading Description FED98.17 9817.1000 9817.2000 9817.3000 9817.4000 9817.9000Services provided or rendered by medical diagnostic laboratories including X-Rays,CT Scan, M.R. Imaging etc.Scientific laboratoriesMechanical laboratoriesChemical laboratoriesElectrical or electronic laboratoriesOther such laboratories16% of the charges98.18 9818.1000 9818.2000 9818.3000 9818.9000Services provided or rendered by specialized agencies.Security agencyCredit rating agencyMarket research agencyOther such agencies16% of the charges98.19 9819.1000 9819.1100 9819.1200 9819.1300 9819.1400 9819.2000 9819.3000 9819.4000 9819.5000 9819.6000 9819.7000 9819.8000 9819.9000 9819.9100 9819.9200 9819.9300 9819.9400 9819.9500 9819.9090 Services provided or rendered by specified persons or businesses.StockbrokersUnder writersIndentersCommission agentsPackersMoney exchangerRent a carPrize bond dealersSurveyorsDesignersOutdoor photographerArt painterCable TV operatorsAuctioneersPublic relations servicesManagement consultantsTechnical testing and analysis serviceService provided by a registrar to an issueOthers16% of the charges98.20 9820.1000 9820.2000 9820.3000 9820.4000 9820.9000Services provided or rendered by specialized workshops or undertakings.Auto-workshopsWorkshops for industrial machinery construction and earth-moving machinery or otherspecial purpose machinery etc.Workshops for electric or electronic equipments or appliances etc. including computerhardwareCar washing or similar service stations.Other workshops16% of the charges98.21 9821.1000 9821.2000 9821.3000 9821.4000 9821.5000 9821.9000Services provided or rendered in specified fields.Healthcare centres, gyms or physical fitness centres etc.Indoor sports and games centresBaby care centresBody massage centresPedicure centresSimilar other centers16% of the charges98.22 9822.1000 9822.2000 9822.3000 9822.4000 9822.9000Services provided or rendered for specified purposes.Fumigation servicesMaintenance or cleaning servicesJanitorial servicesDredging or desilting servicesOther similar services16% of the charges9823.0000 Franchiseservices 16% of the charges 9824.0000 Construction services 16% of the chargesChapter 99SPECIAL CLASSIFICATION PROVISIONSNotes.1. The provisions of this Chapter are not subject to the rule of specificity in General Interpretative Rule 3(a) and have over-riding effect onclassifications made under Chapters 1 to 97.2. Classification in Chapter 99 is subject to,-(i) determination of eight digit classification under a tariff item in chapter 1 to 97;(ii) determination of four digit classification under chapter 99 and fulfillment of conditions mentioned in the Chapter, Sub-chapters, Headings; and(iii) such other conditions, limitations and restrictions as Federal Board of Revenue or the Federal Government may impose from time to time.3. In case of sale or disposal of goods in violation of the prescribed condition, limitation or restriction, duty shall be recovered at the rates specifiedin Chapter 1 to 97 without prejudice to any other action required under the Customs Act, 1969.SUB-CHAPTER -IIMPORTS BY PRIVILEGED PERSONS, ORGANIZATIONS, AND OTHER DIGNITARIES.Note.1. For the purpose of sub-chapter 1, the following conditions shall apply:(i) The importer shall make a declaration on the bill of entry for exemption claimed.(ii) Any article other than a motor vehicle, sold or otherwise disposed of before the expiration of three years from its importation shall be liable topayment of customs duties, which would have been leviable at the time of importation.(iii) A motor vehicle shall not be sold or otherwise disposed of in Pakistan without payment of customs duties, which would have been leviable atthe time of importation as provided under the procedure prescribed therefor by the Board.PCT CODE Description CD (%)(1) (2)(3) 9901 Goods imported by various agencies of the United Nations under the United Nations (PrivilegesandImmunities) Act,1948(XX of 1948), as certified by the Ministry of Foreign Affairs, Government ofPakistan.9902 Goods imported by Diplomats/Embassies/ Consulates under the Diplomatic and Consular PrivilegesAct, 1972 (Act IX of 1972) as certified by the Ministry of Foreign Affairs, Government of Pakistan.9903 Goods imported by privileged personnel/organizations under grant-in-aid agreements signed by theEconomic Affairs Division (EAD) Government of Pakistan, duly concurred by the Federal Board ofRevenue.9904 Vehicles in CKD condition, imported by recognized local manufacturer for supply to diplomat,diplomatic mission, privileged person (as per model rules) and organizations etc eligible to import dutyfree vehicles subject to the procedure laid down by the Board.9905 Household articles and personal effects including vehicles and goods for donation to projectsestablished in Pakistan, imported by the rulers and following dignitaries of UAE and Qatar subject tothe conditions mentioned below and the conditions mentioned in sub-chapter notes:-Dignitaries of UAE1. H.H.Sheikh Khalifa Bin Zayed Al-Nahyan, Crown Prince of Abu Dhabi and Deputy SupremeCommander of UAE Armed Force.2. H.E.Sheikh Suroor Bin Mohammad Al-Nahyan, Chamberlain of the Presidential Court, Abu Dhabi.3. H.E.Sheikh Mohammad Bin Khalid Al-Nahyan, Member of the ruling family of Abu Dhabi.4. H.E.Sheikh Mubarak Bin Mohammad Al- Nahyan, Member of the ruling family of Abu Dhabi.5. H.E.Sheikh Sultan Bin Hamdan Al-Nahyan, Member of the ruling family of Abu Dhabi.6. H.H.General Sheikh Mohammad Bin Zayed Al-Nahyan Chief of Staff of UAE Armed Forces.7. H.E.Sheikh Tahnoum Bin Mohammad Al-Nahyan, Member of the ruling family of Abu Dhabi.8. H.E. Sheikh Rashid Bin Khalifa Al-Makhtoum, Member of the ruling family of Dubai.9. H.H.Sheikh Sultan Bin Zayed Al-Nahyan, Deputy Prime Minister of the UAE.10. H.H.Sheikh Hamdan Bin Zayed Al-Nahyan, Minister of State for Foreign Affairs, Government ofthe United Arab Emirates.11. H.H. Sheikh Muhammad Bin Rashid Al Maktoum, Vice President, Prime Minister, Minister ofDefence and Ruler of Dubai.12. H.H. Sheikh Hamdan Bin Rashid Al-Maktoum, Deputy Ruler of Dubai, Minister of Finance &Industry, UAE.13. H.H. Maj. Gen. Sheikh Ahmed Bin Rashid Al-Maktoum, Member of the Ruling Family of Dubai &Head of Central Military Command.14 H.H. Maj. Gen. Sheikh Nahyan Bin Zayed, Member of the Ruling Family of Abu Dhabi andCommander of Royal Guard.PCT CODE Description CD (%)(1) (2) (3) Dignitaries of Qatar: 1. H.E. Shaikh Faisal Bin Thani Bin Jassim Al-Thani 2. H.E. Shaikh Ali Bin Abdullah Bin Thani Al-Thani.3. H.E. Shaikh Abdullah Bin Jassim Bin Fahad Al-Thani.4. H.E. Shaikh Mubarak Bin Khalifa Bin Saud Al-Thani5. H.E. Shaikh Abdullah Bin Ali Bin Abdullah Al-Thani.6. H.E. Shaikh Abdul Rahman Bin Nasser Bin Jassim Al-Thani7. H.E.Shaikh Ali Bin Ahmed Al-Ahmed Al-Thani8. H.E.Shaikh Faisal Bin Jassim Bin Faisal Al-Thani(i) A complete list of all vehicles showing name of the owner, details of imports and present custodian etc shall be provided by UAE/Qatar Ambassador. This information shall be provided by 31-7-2004 showing comprehensive positions as on 31-12-2003.(ii) The list shall be updated every six months i.e. on 31st July and 31st January to show status as on 1st July & 1st January.(iii) UAE/Qatar Rulers must make and disclose alternate arrangements for maintenance of their fleet by their employees and not by any Pakistani posing as their agents or authorized representatives. (iv) UAE/Qatar Embassy should undertake that no Pakistani will be allowed use of their duty free vehicles and that they will abide by the true spirit in which this concession is available to the UAE/Qatar Rulers.(v) In order to avail the duty concession, an exemption certificate to this effect shall be issued by the Ministry of Foreign Affairs, Government of Pakistan9906 (i) Goods imported under the President’s Salary, Allowances and Privileges Act, 1975(Act LVIII of 1975).(ii) Goods imported under the Prime Minister’s Salary, Allowances and Privileges Order,1975 (ActLIX of 1975).(iii) Goods imported under the Governor’s Salary, Allowances and Privileges, Order,1975(President’s Order No.5 of 1975).(iv) Goods imported under the Acting Governer’s (Allowance and Privileges) Order,1978(President’s Order No.19 of 1978).(v) Furniture, and spare parts in respect of official cars, river craft or air craft imported orpurchased out of bond for the President, Prime Minister, Governor or Acting Governor.SUB-CHAPTER–IIIMPORT OF RELIEF GOODS, GIFTS, SAMPLESPCT CODE Description CD (%)(1) (2) (3) 9907 Goods imported for the President’s Fund for Afghan Refugees. Bonafide relief goods donated for the Afghan Refugees through the Chief Commissioner or the Provincial Commissioner of the Afghan Refugees subject to a certificate from the Chief Commissioner for the Afghan Refugees that the imported goods or equipment are menat for free distribution amongst Afghan Refugees or for relief wrok and that the same would not be sold or otherwise disposed of without the prior approval of the Federal Board of Revenue9908 Goods received as gift by Pakistani organizations from Church World Services or the Catholic Relief Services as are certified by the Ministry of Health, that these imports are made under agreements signed by the Government of Pakistan with the Church World Service and with the Catholic Relief Service9909 Articles, value of which does not exceed Rs.20,000/- per parcel, if imported through post or courier service as unsolicited gift parcel.9910 Samples of no commercial value imported by manufacturers subject to the following conditions:- a) raw materials and products of such dimensions/ specifications that are useless except for purposesof demonstration;b) articles of non-precious materials affixed to cards or put up as samples in the manner usual in thetrade provided that there is not more than one of each size or kind;c) raw materials and products, and articles thereof rendered useless, except for purposes ofdemonstration, by slashing, perforation, indelible marking or by any other effective method;d) products which cannot be put up as samples of no commercial value in accordance with clauses (a)to (c) and which consist of:(ot (2) oods of an individual value not exceeding US$ 100 or its equivalent in any1) non-consumable goods of an individual value not exceeding US$ 100 or its equivalent in anyher currency and provided there is not more than one sample of each kind or quality; and consumable g currency even if they consist wholly or partly of samples of the same kind or quality, provided the quantity and the manner in which they are put up preclude their being used otherwise than as samples9911 (i) R ted for free distribution among the victims of natural disaster or other catastrophe, as are certified by the authorized officer of Federal/Provincial Governmentelief goods dona (ii) Plant, machinery and equipment imported by way of donation for installation in the earthquakehit districts as certified by ERRA/National Disaster Management Authority.otepurpose of sub-chapter III the expression:(i) “Charitable Institution” and “Charitable non-profit m ans an institution approved for the purpose of section 2(36C) ofthe Income Tax Ordi (ii) “Gifts or Donations” include goods other y the donorsresiding abroad. However, ambulances received as gift or donati road shall be eligible for the benefit provided that the same are imported as per Serial No. 116 of Customs General Order No.12 of 2002, dated the 15th June, 2002; andPCT CODE CD (%) SUB-CHAPTER IIIIMPORTS BY CHARITABLE, EDUCATIONAL, SCIENTIFIC INSTITUTIONS AND HOSPITALS.N For the aking institution” me nance, 2001;than v of the First Schedule to the said Act, donated b ehicles of chapter 87on from ab (iii) “Competent Authority” means:(i) in case of educational and research institutions falling in the jurisdiction of the Federal Government, the Ministry of Education orMinistry of Science & Technology or any other relevant Ministry of the Federal Government;(ii) in case of an institution falling within the jurisdiction of a Provincial Government, the Director of Education or Technical Educationor PublicInstitution or any other relevant authority of the Provincial Government; andnized by the University Grants Commission, the Registrar of the University.(iii) in case of a university recogDescription(1) (2) (3)9912 Fo imported by Abdul Sattar Edhi Foundation and Bilques Edhi Foundation, subject tofu oor Edhi at the time of case may be, by Bilquis Edhi Foundation. (In the case of goods at serial No. 14,15,16, the words "Edhi Foundation" or "as the case may be , Bilquis on "are inscribed at some prominent place on the body of each vehicle, aeroplane or helicopter); .04)ze, bandages and similar articles (for example, er, poultices) impregnated or coated stances.(30.05) ods (30.06) 09)n apparatus (85.15) al or surgical usses; splints and other fracturey, hearing aids and other appliances which are worn or r a defect or disability(90.21)al uses, control panels and desks,(90.22).0 llowing goods rnishing of a certificate by Maulana Abdul Sattar Edhi son of Haji Abdul Shak import of each consignment to the effect that the goods are meant for use by Edi Foundation or, as the Edhi Foundati 1. Butter oil(04.05) 2. Rice(10.06) 3. Grains(10.07)4. Cooking oil(Chapter 15)5. Vitamins(29.36)6. Hormones.(29.37)7. Pencillin (29.41) s(308. Medicament9. Waddings, gua dressings, adhesive plast ical sub with pharmaceut 10. Pharmaceutical go .11. Worn clothing(6312. Wireless transmissio 13. Wireless reception apparatus.(85.27) 14. Ambulances.(87.03)15. Mobile radiological units(87.05)16. Helicopters, aeroplanes (88.02)d aeroplanes (Respective headings) 17. Parts of helicopters an 18. Instruments and appliances used in medic sciences.(90.18)s, including crutches, surgical belts and tr 19. Orthopaedic appliance appliances, artificial parts of the bod carried, or implanted in the body, to compensate fo 20.Apparatus based on the use of X-rays for medical or surgic like screens, examination or treatment tables, chairs and the 9913 eived by a charitable non-profit making hospital or institution, solely for the (i) (ii) o the respective Collector ofGifts or donations rec purpose of advancing the declared objectives of such hospital or institution, subject to the following conditions, namely:-no condition is attached to the gift or donation by the donor and the receiving institution or hospitalis at liberty to use the same in accordance with its declared objectives; andthe receiving institution or hospital furnishes an undertaking in writing t Customs to the effect that such gifts or donations will not be sold, utilized or disposed of otherwise than for the purpose for which the same have been received and binds itself to pay the leviable duties in the event of a breach of the undertaking.9914 Equipment, apparatus, reagents, disposables and spares, imported by: -(i) charitable non profit making institutions operating hospitals of fifty beds or more; and(ii) hospitals run by the Federal Government or a Provincial Government,-Subject to the following conditions: -(a) the importing institution or hospital furnishes an undertaking in writing to the respective Collector ofCustoms to the effect that such equipment, apparatus, reagents, disposable and spares will not besold, utilized or disposed of otherwise than for the purpose for which the same have been importedand binds itself to pay the leviable duty and sales tax in the event of breach of the undertaking.(b) the importing institution operating a hospital of fifty beds or more shall furnish a proof thereof to thesatisfaction of the respective Collector of Customs.9915 Goods imported by or donated to non profit making educational and research institutions subject to thefollowing conditions:(i) the imported goods have an educational and scientific character;(ii) the importing or receiving institutions are recognized, aided or run by the Federal Government ora Provincial Government, a City Government or a District Government;(iii) the importing or receiving institution shall produce a certificate from the competent authority that –(a) goods of equivalent educational and scientific value are not produced in Pakistan; and(b) the imported goods will be used exclusively under the control and responsibility of the importing orreceiving institution.SUB-CHAPTER-IVIMPORT OF REPLACEMENT GOODSPCT CODE Description CD (%)(1) (2) (3) 9916 Goods supplied free of cost as replacement of identical goods previously imported including goodsimported within warranty period not exceeding one year or such extended period as allowed by theCollector of Customs, subject to the following conditions:-(i)the goods were imported in pursuance of firm contract of sale, and not under a contract of sale orreturn, on approval; on consignment for sale or on similar terms;(ii) the goods at the time of importation were not in accordance with the terms of contract in respect oftheir description, quality, state or condition or had been damaged or defected;(iii) the goods were not used except in circumstances in which limited use was indispensable to revealany inherent defect in the imported goods or to establish that they do not conform to the conditions ofthe contract;(iv) if the goods are returned abroad, they are returned to the supplier and if they are not returned,they are deposited with customs for further disposal.SUB-CHAPTER-VIMPORTS MADE BY THE UNITS LOCATED IN EXPORTS PROCESSING ZONES (EPZ)PCT CODE Description CD (%)(1) (2) (3) 9917 Goods imported into and exported (except to tariff area of Pakistan) from the Export Processing Zonesestablished under the Export Processing Zone Authority Ordinance, 1980 (IV of 1980) and anyenactment relating to Gwadar Special Economic Zone, subject to such conditions, limitations andrestrictions as the Federal Board of Revenue may impose from time to time.SUB-CHAPTER-VITEMPORARY IMPORT OR EXPORTPCT CODE Description CD (%)(1) (2) (3) 9918 Goods not produced or manufactured in Pakistan which are re-imported by industrial concerns afterhaving been exported and have not undergone any process outside Pakistan since their exportation.In case the goods have undergone any alterations, renovations, addition or repairs prior to their re-import into Pakistan, the cost incurred on such alterations, renovations, additions or repairs (excludingthe element of freight and other incidentals) shall be liable to duty as leviable under its respective PCTheading determined at the time of original import provided the machinery was exported under acontract of alteration, renovation, adddition or repairs and that the supplier and the receiver as well asthe make, model, weight and other specifications remain the same as were at the time of the originalimport of the goods.9919 Goods mentioned below, imported temporarily for a period not exceeding 6 months into Pakistan witha view to subsequent exportation, subject to furnishing of bank guarantee or other security/guaranteeas determined by Federal Board of Revenue equivalent to customs duty chargeable at the ratesspecified in Chapter 1 to 97 of the lst Schedule to the Act for such goods and other taxes leviablethereon.1. Packing material used or required to be used as external or internal covering of goods, or asholders of goods, or as holders on which goods rolled, wound or attached provided such material donot change their original shape or form. Packing material if imported filled, it may be re-exportedempty, and if imported empty it may be re-exported filled.2. Machinery and equipment for repair imported by manufacturer or authorized agents based inPakistan, representing foreign manufacturers duly registered with the Sales Tax Authorities, having inhouse facility for repair, Refurbishment or value addition of machinery.3. Professional equipment imported by scientists, IT experts, technicians, doctors, engineers, etc.either imported in their own name or in the name of the company in Pakistan for which these areimported.4. Tubes or cops of metal plastic or other durable material which are imported wrapped with yarn.5. Goods imported for demonstration , display, test or trial purposes.6. Dry fruits imported from Afghanistan.9920 Goods mentioned below, imported temporarily into Pakistan with a view to subsequent exportation,subject to furnishing of undertaking/bond by the importers as well as their sponsoring Ministry/Department/ Embassy:1. Excavation equipment and consumable stores imported by a foreign archaeological mission towhom a license for archaeological excavation has been granted by the Federal Government or aProvincial Government.2. Scientific and educational equipment imported for Scientific, educational or cultural seminars inPakistan on the recommendation of the concerned Ministry.3. Goods imported for display at international or single country exhibition organized by foreignmissions or imported by or through the Ministry of Commerce or the Ministry of Foreign Affairs.4. Machinery imported by the representatives of foreign commercial firms for demonstration purposesimported by or through the Ministry of Commerce or the Ministry of Foreign Affairs.5. Equipment and materials imported by foreign nationals such as journalists, press photographers,members of television teams, broadcasting units and film companies subject to endorsement on theirpassports. The duties shall be charged if such importer fails to prove their re-export at the time ofdeparture.6. Equipment, materials and special food stuff imported by mountaineering expeditions. In case theequipment and material is not exported the expeditions may donate such equipment and produce acertificate from the Secretary of that club to the effect that the equipment and material so imported hasbeen donated by that expedition to that club. Special food stuff can however, be consumed by them.9921 Container for transportation of cargo (PCT No.86.09) if imported by the shipping companies for useon board the ships and for transportation of cargo to and from inland container depots or containerfreight stations subject to the furnishing of indemnity bond by the shipping lines, equal to the amountof duty and taxes to the respective Collector of Customs. The indemnity bond is to be discharged onreceipt of proof of export of the containers.9922 Ship spares, stores and equipment imported for use in ships registered in Pakistan under theMerchant Shipping Act, 1923 (XXI of 1923) subject to the condition that the importer satisfies therespective Collector of Customs that the items imported would be used by such vessels.SUB-CHAPTER-VIIMISCELLANEOUSPCT CODE Description CD (%)(3)(1) (2)9923 Currency Notes, unused stamps 09924 Eyecornea 0machines, hemodialyzers, A.V. fistula needles, hemodialysis fluids &hemodialysiskidneys,9925 Artificialpowder, blood tubing tines for dialysis, reverse osmosis plants for dialysis, double lumen catheter fordialysis, catheters for renal failure patients, peritoneal dialysis solution and cardiac catheters.9926 Machinery and equipment, not manufactured locally, namely navigational equipment, fish finders,storage and handling equipment, if imported by fish farming or catching stage operators, who willenjoy the status of indirect exporters.9927 Pharmaceutical raw materials if imported for manufacture of contraceptives in accordance with theinput out put ratios determined by the Directorate of Input Output Co-efficient Organization.Contraceptives and accessories thereof.9928 Omitted.。

进口清关业务中缴纳税费流程在进口清关的时候啊,缴纳税费可是个挺重要的事儿呢。

这就像是你进一个游乐场,得先买门票才能痛痛快快玩里面的项目一样。

一、税费种类。

咱先得知道都有啥税费要交呀。

1. 关税。

关税呢,就像是给进口商品交的“入场费”。

不同的商品,它的关税税率可不一样哦。

这是根据商品的种类、原产地等好多因素来定的。

比如说,有些奢侈品的关税可能就会高一些,因为它们比较贵嘛。

像从某些国家进口的高级化妆品,关税可能就会让这个化妆品的成本一下子增加不少呢。

这就像是你在游乐园里玩那些特别刺激的高级项目,门票自然就贵些啦。

2. 增值税。

增值税呀,是在商品流转过程中征收的一种税。

进口的商品也逃不掉呢。

它是按照货物的增值额来征收的。

简单来说,就是这个商品到了咱们国内,它可能经过加工或者直接就销售了,那这个过程中产生的增值部分就得交增值税。

这就好比你在游乐园里买了个小纪念品,然后你转手卖给别人赚了点钱,那这个赚钱的部分就得交点税啦。

3. 消费税。

有些特定的商品还得交消费税呢。

像烟酒这种对身体有特殊影响的商品,或者是那些高档的珠宝首饰、豪华小汽车之类的。

消费税就是为了调节消费结构,引导大家合理消费的。

这就像游乐园里有些特别热门的项目,因为太火爆了,所以还得额外收点费用来调节一下人数一样。

二、税费计算。

知道了要交啥税,那咋计算呢?这可有点小复杂哦。

关税的计算一般是按照商品的完税价格乘以关税税率。

完税价格呢,不是简单的商品在国外的价格,而是要按照海关的规定来确定的。

比如说,它可能要加上运费啊、保险费之类的。

增值税的计算呢,是在关税完税价格加上关税的基础上,再乘以增值税税率。

消费税的计算又根据不同的商品有不同的计算方法,有的是从价计征,有的是从量计征,还有的是复合计征呢。

这就像你在游乐园里算自己玩项目总共要花多少钱一样,得根据不同项目的收费规则来算,有点头疼,但是搞清楚了就还好啦。

三、缴纳流程。

1. 申报。

进口商得先向海关申报进口货物的情况。

作者: 杨胜[1]

作者机构: [1]中国工商银行卡拉奇分行营业部

出版物刊名: 中国外汇

页码: 23-25页

年卷期: 2020年 第10期

主题词: 中资企业;同类商品;海关申报;数据库查询;贸易物流;巴基斯坦;一带一路;商品单价;

摘要:巴央行明确规定,由银行对进出口商品单价进行审核。

但由于受到行业知识的限制,银行一般会通过海关申报数据库查询同类商品的历史报关价格来进行对比、审核。

“一带一路”大背景下,越来越多的中资企业开始到巴基斯坦投资,期望在这片热土中寻找新的商机。

进出口清关作为工程和贸易物流的关键部分,是大多数赴巴中资企业必经环节。

然而巴基斯坦清关流程对外界一直是“犹抱琵琶半遮面”。

进口清关代理费用计算公式进口商品的清关代理费用是指进口商在国外采购商品后,通过清关代理公司进行报关、报检、缴税等流程的费用。

这些费用包括了代理公司的服务费、报关费、报检费、保险费等各项费用。

对于进口商来说,了解清关代理费用的计算公式是非常重要的,可以帮助他们在采购商品时更好地控制成本。

本文将介绍进口清关代理费用的计算公式,并且对其中的各项费用进行详细解析。

清关代理费用的计算公式通常包括以下几个部分,服务费、报关费、报检费、保险费等。

下面我们将对每一项费用进行详细介绍,并给出相应的计算公式。

1. 服务费。

清关代理公司的服务费是指他们为进口商提供的报关、报检、缴税等服务的费用。

服务费通常是按照货物的价值或者数量来计算的,计算公式如下:服务费 = 货物价值×服务费率。

其中,货物价值是指进口商品的成交价格,服务费率是由清关代理公司根据不同的情况来确定的,通常是一个百分比。

2. 报关费。

报关费是指清关代理公司为进口商办理报关手续所收取的费用。

报关费的计算公式如下:报关费 = 报关商品数量×单个商品报关费用。

报关商品数量是指进口商品的数量,单个商品报关费用是由清关代理公司根据不同的情况来确定的。

3. 报检费。

报检费是指清关代理公司为进口商办理报检手续所收取的费用。

报检费的计算公式如下:报检费 = 报检商品数量×单个商品报检费用。

报检商品数量是指进口商品的数量,单个商品报检费用是由清关代理公司根据不同的情况来确定的。

4. 保险费。

保险费是指清关代理公司为进口商购买货物保险所收取的费用。

保险费的计算公式如下:保险费 = 货物价值×保险费率。

其中,货物价值是指进口商品的成交价格,保险费率是由保险公司根据不同的情况来确定的,通常是一个百分比。

除了上述几项费用之外,清关代理费用还可能包括一些其他费用,比如货物仓储费、运输费等。

这些费用的计算公式也可以根据具体情况来确定。

在实际操作中,清关代理费用的计算还需要考虑到一些其他因素,比如货物的种类、来源国家、目的地国家、运输方式等。

进口关税计算方式是怎样的小编希望进口关税计算方式是怎样的这篇文章对您有所帮助, 如有必要请您下载收藏以便备查, 接下来我们继续阅读。

随着我国经济的快速发展, 越来越多的企业加入到进出口贸易的行列中, 国家为了保护国内的商品, 制定了相关的规定, 要求商品在进出口的过程中都需要缴纳关税。

那进口关税计算方式是怎样的?小编为您整理了以下内容, 相信会对您有所帮助。

进口关税计算方式计算进口关税税款的基本公式是:进口关税税额=完税价格×进口关税税率在计算关税时应注意以下几点:1、进口税款缴纳形式为人民币。

进口货物以外币计价成交的, 由海关按照签发税款缴纳证之日国家外汇管理部门公布的人民币外汇牌价的买卖中间价折合人民币计征。

人民币外汇牌价表未列入的外币, 按国家外汇管理部门确定的汇率折合人民币。

2、完税价格金额计算到元为止, 元以下四舍五入。

完税税额计算到分为止, 分以下四舍五入。

3、一票货物的关税税额在人民币50元以下的免税。

进口货物的成交价格, 因有不同的成交条件而有不同的价格形式, 常用的价格条款, 有FOB、CFR、CIF三种。

现根据三种常用的价格条款分别举例介绍进口税款的计算。

(一)以CIF成交的进口货物, 如果申报价格符合规定的“成交价格”条件, 则可直接计算出税款举例如下:某公司从德国进口钢铁盘条100 000千克, 其成交价格为CIF天津新港125 000美元, 求应征关税税款是多少?已知海关填发税款缴款书之日的外汇牌价:100美元=847.26人民币元(买入价)100美元=857.18人民币元(卖出价)税款计算如下:(1)审核申报价格, 符合“成交价格”条件, 确定税率:钢铁盘条归入税号7310, 进口关税税率为15%。

(2)根据填发税款缴款书日的外汇牌价, 将货价折算人民币。

当天外汇汇价为:外汇买卖中间价100美元=(847.26+857.18)÷2=852.22人民币元即1美元=8.5222人民币元完税价格=125 000×8.5222=1 065 275人民币元(3)计算关税税款即:1 065 275元人民币×15%=159 791.25人民币元(二)FOB和CFR条件成交的进口货物, 在计算税款时应先把进口货物的申报价格折算成CIF价, 然后再按上述程序计算税款举例如下:我国从国外进口一批中厚钢板共计200,000公斤, 成交价格为FOB伦敦2.5英镑/公斤, 已知单位运费为0.5英镑, 保险费率为0.25%, 求应征关税税款是多少?已知海关填发税款缴款书之日的外汇牌价:1英镑=11.2683人民币元(买入价)1英镑=11.8857人民币元(卖出价)(1)根据填发税款缴款书日的外汇牌价, 将货价折算人民币。

进口关税计算1. 什么是进口关税?进口关税是指各国政府对进口商品征收的税费。

它是一种外贸政策工具,旨在保护国内产业、调整外贸结构、维护国家安全等方面起到作用。

进口关税的计算方法因国家和进口商品的种类而异,本文将介绍进口关税的常见计算方法及示例。

2. 进口关税计算方法进口关税的计算通常基于商品的完税价格,即商品的海外出口价格。

计算方法涉及税率和完税价格,具体步骤如下:1.确定商品的海关编码:每种商品都有一个唯一的海关编码,用于分类和定价。

通常,海关编码可在海关网站或商品清单中查找。

2.查询税率:根据商品的海关编码,查询适用于该商品的税率表。

不同国家的税率表可能有所不同,因此应选择适用于进口目的国的税率表。

3.计算完税价格:完税价格是商品的海外出口价格,通常包括商品价格、运输费用、保险费用等。

4.计算进口关税:使用下述公式计算进口关税:进口关税 = 完税价格 × 税率注:某些情况下,还可能涉及到一些特定的减免措施或缴纳其他附加费用。

3. 进口关税计算示例为了更好地理解进口关税的计算方法,我们以一批进口手机为例进行计算。

假设货物的海关编码为8517.12.00,税率为10%,完税价格为1,000美元。

根据上述计算方法,我们可以进行进口关税的计算如下:步骤1:确定商品的海关编码为8517.12.00。

步骤2:查询税率表,得知该海关编码的商品税率为10%。

步骤3:完税价格为1,000美元。

步骤4:使用公式计算进口关税:进口关税 = 1,000美元 × 10% = 100美元因此,这批进口手机的进口关税为100美元。

4. 进口关税的影响进口关税的高低直接影响着商品的进口成本和国际贸易的竞争力。

较低的进口关税可以促进国际贸易的发展,增加消费者的选择,并降低商品价格。

然而,过高的进口关税可能会导致商品价格上涨,增加企业的负担,限制进口市场的开放程度。

因此,各国政府在制定进口关税政策时需要综合考虑国内产业发展、国际竞争力和消费者权益等多方面因素,并根据实际情况进行调整。

进⼝关税税率怎么算进⼝关税属于我国应征税的范围,我国的税收的特点⼀般是⽆偿性,固定性以及强制性。

⽬的在于将收取的预收充当国库。

下⾯店铺⼩编来为你介绍相关知识,希望对你有所帮助。

⼀、进⼝增值税计算⽅法:进⼝增值税计算公式:进⼝增值税=(关税完税价格+关税)/(1-消费税率)×增值税率需要注意的是,进⼝货物增值税的组成计税价格中已包括已纳关税税额,如果进⼝货物属于消费税应税消费品,其组成计税价格中还要包括进⼝环节已纳消费税税额。

⼆、进⼝关税计算⽅法有以下⼏种:1、从价从价税是按进出⼝货物的价格为标准计征关税。

这⾥的价格不是指成交价格,⽽是指进出⼝商品的完税价格。

因此,按从价税计算关税,⾸先要确定货物的完税价格。

从价税额的计算公式如下:应纳税额=应税进出⼝货物数量×单位完税价格×适⽤税率2、从量从量关税是依据商品的数量、重量、容量、长度和⾯积等计量单位为标准来征收关税的。

它的特点是不因商品价格的涨落⽽改变税额,计算⽐较简单。

从量关税额的计算公式如下:应纳税额=应税进⼝货物数量×关税单位税额3、复合复合税亦称混合税。

它是对进⼝商品既征从量关税⼜征从价关税的⼀种办法。

⼀般以从量为主,再加征从价税。

混合税额的计算公式如下:应纳税额=应税进⼝货物数量×关税单位税额+应税进⼝货物数量×单位完税价格×适⽤税率4、滑准滑准税是指关税的税率随着进⼝商品价格的变动⽽反⽅向变动的⼀种税率形式,即价格越⾼,税率越低,税率为⽐例税率。

因此,实⾏滑准税率,进⼝商品应纳关税税额的计算⽅法,与从价税的计算⽅法相同。

其计算公式如下:应纳关税税额=T1、2×P×汇率5、特别特别关税的计算公式如下:特别关税=关税完税价格×特别关税税率进⼝环节消费税=进⼝环节消费税完税价格×进⼝环节消费税税率进⼝环节消费税完税价格=(关税完税价格+关税+特别关税)/(1-进⼝环节消费税税率)进⼝环节增值税=进⼝环节增值税完税价格×进⼝环节增值税率进⼝环节增值税完税价格=关税完税价格+关税+特别关税+进⼝环节消费税三、进⼝关税进⼝关税是⼀个国家的海关对进⼝货物和物品征收的关税。

进出⼝税费的⼏个计算公式 (⼀)进⼝关税计算 从价进⼝货物应纳关税款=进⼝货物完税价格×适⽤的进⼝关税税率 进⼝货物完税价格=CIF=(FOB价格+运费)/(1-保险费率) =CFR价格/(1-保险费率) 从量进⼝货物应纳关税款=进⼝货物数量×适⽤的单位税额 复合进⼝货物应纳关税款=从价部分关税额+从量部分关税额 =进⼝货物完税价格×适⽤的关税额+进⼝货物数量×适⽤的单位税额 (⼆)进⼝环节税税款计算 l 从价应纳消费税额=从价消费税计税价格×消费税从价税率 从价消费税计税价格=(进⼝货物完税价格+进⼝关税税额)/(1-从价消费税税率) l 从量应纳消费税额=进⼝货物数量×消费税从量税率 复合应纳消费税额=从价部分消费税额+从量部分消费税额=从价消费税计税价格×消费税从价税率+进⼝货物数量×消费税从量税率 l 我国的增值税都是从价税,根据进⼝货物是否应缴消费税,分以下两种情况: 1、应征消费税的进⼝货物增值税=增值税计税价格×增值税税率 应征消费税的增值税计税价格=进⼝货物完税价格+进⼝关税税额+消费税税额=进⼝货物完税价格+进⼝货物完税价格×进⼝关税税率+从价/从量/复合消费税税额 2、不征消费税的进⼝货物增值税=增值税计税价格×增值税税率 不征消费税的增值税计税价格=进⼝货物完税价格+进⼝关税税额 (三)出⼝关税计算 出⼝货物应纳关税额=出⼝货物完税价格×出⼝关税税率 出⼝货物完税价格=FOB价格/(1+出⼝关税税率) 减税出⼝货物关税额=出⼝货物完税价格×减按出⼝关税税率 减税出⼝货物完税价格=FOB价格/(1+出⼝关税税率) (四)船舶吨税税款计算 船舶吨税按注册净吨位计算,尾数按四舍五⼊原则,半吨以下免征尾数,半吨以上按⼀吨计征 应征船舶吨税=净吨位×船舶吨税税率=船舶有效容积×吨/⽴⽅⽶×船舶吨税税率 (五)滞纳⾦计算 按照规定,关税、进⼝环节增值税和消费税、船舶吨税的纳税⼈或其代理⼈,未在规定时间内缴纳税款构成滞纳的,应照章缴纳滞纳⾦。

51ECONOMIC & TRADE UPDATE引言自2013年以来,为解决巴基斯坦电力日渐突出的供应不足问题,巴政府采取一系列措施,加大对电力业的投入,并鼓励和吸引外商和民间投资电力领域。

同时随着我国“一带一路”、“中巴经济走廊”政策的实施,我国在巴投资建设电站项目、巴方投资电站以及我国电力施工企业以EPC模式承包建设巴国电站项目逐渐增多,比如巴基斯坦卡西姆港2×660MW超临界燃煤电站、华能山东如意萨希瓦尔2×660MW燃煤电站、巴方在旁庶普省投资建设的3台GE公司9H级燃机联合循环电站等。

由于巴国工业化程度不高,电站建设的大部分设备、材料需要从国外进口,进口清关政策和相关税费对项目经济技术分析、成本测算、投标报价、建设和运营期间成本控制均有较大的影响。

笔者通过对巴基斯坦海关电站进口政策进行研究和分析,并从在巴电站建设的多年实践经验出发,编写此篇巴基斯坦电站工程物资进口概要,以期对在巴进行电站投资、项目建设投标和从事建设、运营业务的企业单位提供参考和借鉴。

巴基斯坦电站工程物资进口清关概要王伟民【摘 要】巴基斯坦海关进口清关税费的种类多、税率高,为推动电力行业发展,政府制定了一系列的电站设备材料进口清关税费优惠政策和适用条件,本文对巴基斯坦海关电站进口政策进行研究和分析,并对进口清关实践中需要注意的重要事项进行了归纳,以期对在巴进行电站投资、项目建设投标和从事建设、运营业务的企业单位提供参考和借鉴。

【关键词】清关 ;巴基斯坦;电站;减免税一、巴电站物资进口清关税费及政策(一)进口主要税种及介绍序号税种税率计税基础1CD关税不适用减免税时:3%-35%适用减免税时:3%或5%1、计税基础=发票货值CFR+保险金额+港杂费2、根据巴基斯坦海关法中5th schedule规定,如项目建设方与巴基斯坦政府私营电力和基础设施委员(PPIB)签署协议,属于水电部(WAPDA)项目,以业主名义进口,关税减免为5%,部分物资起征税率为3%2ACD附加关税3%1、计税基础=发票货值CFR+保险金额+港杂费 2、海关按货物性质确定是否征收,正式电站工程设备材料通常不征收附加关税3RD反倾销税5%及以上1、计税基础=发票货值CFR+保险金额+港杂费 2、海关按货物报关价格和市场价格确定是否征收,正式电站工程设备材料通常不征收附加关税4ST销售税17%1、计税基础=发票货值CFR+保险金额+港杂费+关税+ACD额外关税+反倾销税2、根据巴基斯坦销售税法中6th schedule,项目建设方与巴基斯坦政府私营电力和基础设施委员(PPIB)签署协议,属于水电部(WAPDA)项目,以业主名义进口,销售税减免为0%5AST附加销售税1%1、计税基础=发票货值CFR+保险金额+港杂费+关税+ACD额外关税+反倾销税2、进口商进口自用的物资通常不征收此税种,正式电站工程设备材料通常不征收附加关税6IT所得税0 ̄5.50%1、计税基础=发票货值CFR+保险金额+港杂费+关税+ACD额外关税+反倾销税+销售税2、进口自用物资时(即承包商设备、材料),中国国企、政府机构等出具中国驻伊斯兰堡大使馆的国企证明,此所得税可申请减免为0%;中国私营企业可减免到5.5%3、当地企业业主可向财务部FBR申请减免为0%7EXCISE信德省/旁庶普地方税0.9%-1.15%1、计税基础=发票货值CFR+保险金额+港杂费2、此税为地方税,由当地政府来确定是否征收,目前海运、空运等运输方式在信德省和旁庶普省均征收此税种,没有减免政策52ECONOMIC & TRADE UPDATE(二)电站项目物资进口优惠政策的详析1、关税(Customs Duty, 简写CD)的优惠政策根据最新的巴基斯坦2017-2018年度海关法The Fifth Schedule,与电力相关的减免关税共有4个类别,如下:第9项,(1)使用油、气、煤、潮汐能源发电的新建、现代化改造、更换或扩建项目,并且与巴基斯坦政府签订了相关执行协议,包括在建项目,关税减至3%,5%。

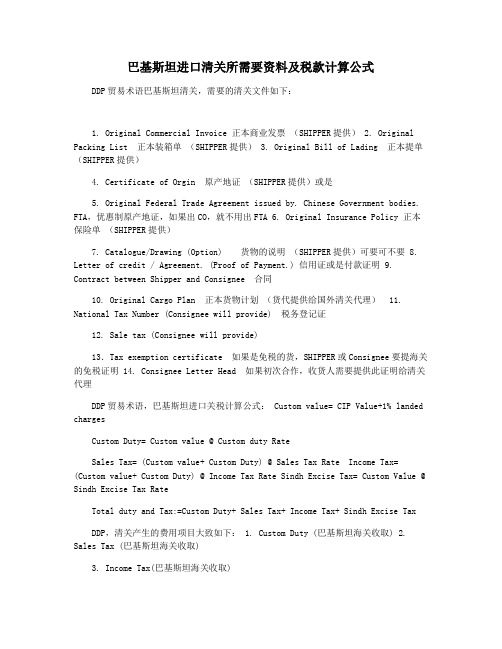

巴基斯坦进口清关所需要资料及税款计算公式DDP贸易术语巴基斯坦清关,需要的清关文件如下:1. Original Commercial Invoice 正本商业发票(SHIPPER提供)2. OriginalPacking List 正本装箱单(SHIPPER提供) 3. Original Bill of Lading 正本提单(SHIPPER提供)4. Certificate of Orgin 原产地证(SHIPPER提供)或是5. Original Federal Trade Agreement issued by. Chinese Government bodies. FTA,优惠制原产地证,如果出CO,就不用出FTA6. Original Insurance Policy 正本保险单(SHIPPER提供)7. Catalogue/Drawing (Option) 货物的说明(SHIPPER提供)可要可不要 8.Letter of credit / Agreement. (Proof of Payment.) 信用证或是付款证明 9.Contract between Shipper and Consignee 合同10. Original Cargo Plan 正本货物计划(货代提供给国外清关代理) 11.National Tax Number (Consignee will provide) 税务登记证12. Sale tax (Consignee will provide)13.Tax exemption certificate 如果是免税的货,SHIPPER或Consignee要提海关的免税证明 14. Consignee Letter Head 如果初次合作,收货人需要提供此证明给清关代理DDP贸易术语,巴基斯坦进口关税计算公式: Custom value= CIP Value+1% landedchargesCustom Duty= Custom value @ Custom duty RateSales Tax= (Custom value+ Custom Duty) @ Sales Tax Rate Income Tax=(Custom value+ Custom Duty) @ Income Tax Rate Sindh Excise Tax= Custom Value @Sindh Excise Tax RateTotal duty and Tax:=Custom Duty+ Sales Tax+ Income Tax+ Sindh Excise TaxDDP,清关产生的费用项目大致如下: 1. Custom Duty (巴基斯坦海关收取) 2.Sales Tax (巴基斯坦海关收取)3. Income Tax(巴基斯坦海关收取)4. Excise & Taxation Officer (巴基斯坦海关收取)5. Wharfage (码头费)6. Bill of Entry Charges (文件费)7. Amendment Fees Paid to Customs (if have) 改单费(如果产生) 8.Devaninig Charges M/s. Cosco Saeed Karachi 拆箱费(如果产生) 9. T.H.C Charges Paid to M/s. Cosco Saeed 码头操作费10. Registration Fees at Customs/KPT 如果港区,办理KPT费用11. Customs Examination, Assessment Port Formalties & Completion 海关查验费12. Commission 国外货代给他们报关代理的佣金(如跟货代已谈清关费用,可拒付)13. 16% sales tax of commission国外货代给他们报关代理的佣金(如跟货代已谈清关费用,可拒付)感谢您的阅读,祝您生活愉快。

DDP贸易术语巴基斯坦清关,需要的清关文件如下:

1. Original Commercial Invoice 正本商业发票(SHIPPER提供)

2. Original Packing List 正本装箱单(SHIPPER提供)

3. Original Bill of Lading 正本提单(SHIPPER提供)

4. Certificate of Orgin 原产地证(SHIPPER提供)或是

5. Original Federal Trade Agreement issued by. Chinese Government

bodies. FTA,优惠制原产地证,如果出CO,就不用出FTA

6. Original Insurance Policy 正本保险单(SHIPPER提供)

7. Catalogue/Drawing (Option) 货物的说明(SHIPPER提供)可要可不要

8. Letter of credit / Agreement. (Proof of Payment.) 信用证或是付款证明

9. Contract between Shipper and Consignee 合同

10. Original Cargo Plan 正本货物计划(货代提供给国外清关代理)

11. National Tax Number (Consignee will provide) 税务登记证

12. Sale tax (Consignee will provide)

13.Tax exemption certificate 如果是免税的货,SHIPPER或Consignee要提海关的免税证明14. Consignee Letter Head 如果初次合作,收货人需要提供此证明给清关代理

DDP贸易术语,巴基斯坦进口关税计算公式:

Custom value= CIP Value+1% landed charges

Custom Duty= Custom value @ Custom duty Rate

Sales Tax= (Custom value+ Custom Duty) @ Sales Tax Rate

Income Tax= (Custom value+ Custom Duty) @ Income Tax Rate

Sindh Excise Tax= Custom Value @ Sindh Excise Tax Rate

Total duty and Tax:=Custom Duty+ Sales Tax+ Income Tax+ Sindh Excise Tax

DDP,清关产生的费用项目大致如下:

1.Custom Duty (巴基斯坦海关收取)

2.Sales Tax (巴基斯坦海关收取)

3.Income Tax(巴基斯坦海关收取)

4.Excise & Taxation Officer (巴基斯坦海关收取)

5.Wharfage (码头费)

6.Bill of Entry Charges (文件费)

7.Amendment Fees Paid to Customs (if have) 改单费(如果产生)

8.Devaninig Charges M/s. Cosco Saeed Karachi 拆箱费(如果产生)

9.T.H.C Charges Paid to M/s. Cosco Saeed 码头操作费

10.Registration Fees at Customs/KPT 如果港区,办理KPT费用

11.Customs Examination, Assessment Port Formalties & Completion 海关查验费

mission 国外货代给他们报关代理的佣金(如跟货代已谈清关费用,可拒付)

13.16% sales tax of commission国外货代给他们报关代理的佣金(如跟货代已谈清关费用,

可拒付)。