本文摘自商业周刊第期生活专刊.

- 格式:ppt

- 大小:2.01 MB

- 文档页数:19

Consumer Perceptions of Price, Quality, and Value: A Means-End Model and Synthesis of EvidenceAuthor(s): Valarie A. ZeithamlSource: The Journal of Marketing, Vol. 52, No. 3 (Jul., 1988), pp. 2-22Published by: American Marketing AssociationStable URL: /stable/1251446Accessed: 21/05/2010 10:20Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use.Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at/action/showPublisher?publisherCode=ama.Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact support@.American Marketing Association is collaborating with JSTOR to digitize, preserve and extend access to TheJournal of Marketing.。

华尔街日报体范文Title: The Impact of Globalization on Financial Markets: A Wall Street Journal PerspectiveIntroduction:Globalization has become an increasingly influential force in shaping the world's financial markets. As countries integrate and economies interconnect, Wall Street Journal has closely observed the profound effects of globalization on the financial sector. This article will discuss the key aspects of globalization and their far-reaching impacts on Wall Street and global financial dynamics. The Globalization Wave:In recent decades, globalization has gained considerable momentum, fueled by advancements in technology, trade liberalization policies, and increased cross-border investments. This wave of globalization has resulted in the convergence of financial markets worldwide, facilitating unprecedented access to international markets.Market Integration:The financial markets' integration has brought about numerous benefits for Wall Street players. Investors now have access to a broader range of investment opportunities, diversifying risk and potentially increasing returns. Moreover, companies can easily tap into global capital markets, raising funds to support expansion and development.FDI and Capital Flows:Foreign direct investment (FDI) and substantial cross-bordercapital flows have become integral components of the global financial landscape. Multinational corporations and institutional investors are increasingly exploring opportunities across borders, transferring capital to regions with high growth potential. This capital mobility has allowed Wall Street to channel investments into emerging markets, not only stimulating their economic growth but also generating profitable opportunities for investors. Regulatory Challenges:While globalization brings undeniable benefits, it also poses significant challenges. Cooperation among regulatory bodies becomes essential to maintain stability and avoid systemic risks. Wall Street Journal has closely monitored instances where regulatory gaps have been exploited, leading to financial crises that reverberate globally. Such examples highlight the need for stronger cross-border regulatory coordination to ensure financial market stability.Technology and Financial Innovation:Globalization and technological advancements go hand in hand, revolutionizing the financial sector. Wall Street Journal has documented the emergence of fintech start-ups, which offer disruptive innovations in payment systems, trading platforms, and risk assessment techniques. As technology continuously evolves, Wall Street embraces these developments to remain competitive and efficiently adapt to changing investor demands.Emerging Market Opportunities:The Journal recognizes that globalization has opened up new investment vistas in emerging markets. As developing economiesgrow, Wall Street's presence in these regions has expanded significantly. This presence not only facilitates capital flows and access to global markets but also helps drive economic development, job creation, and sustainable growth. Conclusion:Globalization has transformed Wall Street into a dynamic and interconnected financial powerhouse. Through its comprehensive coverage, the Wall Street Journal continues to shed light on the opportunities and challenges presented by global integration. As the world's economies become increasingly intertwined, it is imperative for financial institutions and regulators to navigate the global landscape prudently. Wall Street Journal serves as a reliable source for readers to comprehend the complex dynamics of globalization and make informed decisions in the ever-evolving global financial markets.。

生活中的市场营销学智慧树知到课后章节答案2023年下昆明理工大学昆明理工大学第一章测试1.市场营销的核心是()答案:交换2.从市场营销的角度看,市场就是()答案:具有购买欲望和支付能力的消费者3.站在经营者的角度,人们常常把卖方称之为(),而将买方称之为市场。

答案:产业4.从市场营销理论的角度而言,企业市场营销的最终目标是()答案:满足消费者的需求和欲望5.以“顾客需要什么,我们就生产供应什么”作为座右铭的企业属于()企业答案:市场营销导向型第二章测试1.对企业造成市场营销机会和形成环境威胁的外部因素称为()。

答案:宏观环境2.分析营销微观环境时,需要考虑的因素包括()。

答案:供应商;社会公众;消费者;企业自身;竞争者3.消费者行为信息的调研中,购买者和参与购买的人都是调研对象。

答案:对4.随机抽样是指根据自己的主观判断或标准去抽选样本。

答案:错5.营销学把市场中存在的各种尚未满足或者未能很好满足的需求称为营销机会。

答案:对第三章测试1.识别竞争者并非是一件简单容易的事,通常可从()来识别。

答案:产业和市场两个方面2.下列不属于市场领导者战略的是()答案:制定行业标准制定行业标准制定行业标准3.有能力对市场领导者采取攻击行动,有望夺取市场领导者地位的公司属于()答案:市场挑战者4.市场跟随者可以应用()的战略。

答案:产品模仿5.市场补缺者竞争战略的关键是()。

答案:专业化第四章测试1.()差异的存在是市场细分的内在依据。

答案:客户需求2.不属于消费者市场细分变量的是()。

答案:采购方法3.企业开展目标营销的第二个步骤是()。

答案:目标市场选择4.()是设计公司的产品和形象,以求在目标顾客心目中占据一个独特位置的行动。

答案:市场定位5.如下图所示的目标市场战略是()。

答案:差异市场营销第五章测试1.在产品整体概念中最基本、最主要的部分是()。

答案:核心产品2.根据消费者购买习惯和特点,消费品一般区分为()。

行为金融学有限自利的例子行为金融学是一门研究人们在金融决策过程中的行为心理学科。

这门学科与传统金融学相比,更加注重个体的非理性行为以及市场的非效率性。

在行为金融学中,有一个重要的概念叫做有限自利(bounded self-interest)。

有限自利指的是个体在做决策时,虽然有着自身的利益诉求,但由于认知偏差和情绪因素的影响,导致其决策并非完全追求最大的个人利益。

在下面的文章中,我将为大家介绍两个典型的行为金融学有限自利的例子。

第一个例子是“损失厌恶”。

根据行为金融学的研究,人们对于损失的厌恶程度远大于同等金额的收益的满足感。

也就是说,人们往往会不愿意承担风险,而更愿意选择稳定的回报。

一个常见的例子是投资者对于股票市场的情绪反应。

当股票市场出现剧烈波动时,投资者往往会因为盈利的机会而犹豫不决,而一旦出现亏损,他们会迅速抛售股票以避免进一步损失。

这种行为背后的心理机制就是损失厌恶。

尽管在理性的视角下,应该追求最大的利益,但出于对损失的恐惧,人们更倾向于选择稳定的回报。

第二个例子是“过度自信”。

根据研究,人们往往会对自己的能力和知识水平过度自信,而忽视了风险和不确定性。

这种过度自信的现象在金融领域尤为明显。

例如,在股票市场中,投资者可能会过于相信自己的分析和预测,而忽视市场的真实情况。

这种过度自信使得投资者往往会对高风险高回报的投资机会持有过高的期望,进而导致决策的失误。

过度自信也表现在投资者不愿意听取他人的建议和意见,更倾向于自己的直觉和判断。

行为金融学的有限自利理论提供了一种解释金融决策背后心理机制的角度。

它向我们展示了人们在金融决策中的非理性行为,以及这种非理性行为可能对个人和市场造成的影响。

了解这些心理偏差,可以帮助我们更好地理解市场的波动和投资者的决策。

总结起来,行为金融学的有限自利概念揭示了人们在金融决策中的非理性行为。

通过引入损失厌恶和过度自信的例子,我们可以看到个体在决策过程中所受到的心理偏差。

华尔街日报体范文华尔街日报是全球知名的财经类报纸,其体裁多样,既包括新闻报道,也包括特写报道和评论文章。

下面是一个以华尔街日报为模板写的700字体裁为新闻报道的范文:标题:科技巨头争相进军电动汽车领域导语:近年来,科技巨头纷纷将目光投向了电动汽车领域。

亚马逊、苹果、谷歌等公司相继加入这一竞赛,成为了特斯拉的潜在竞争对手,引发了业界的广泛关注。

华尔街,日期——。

美国电动汽车制造商特斯拉的市场垄断地位或将面临挑战。

近年来,亚马逊、苹果、谷歌等科技巨头纷纷加大对电动汽车领域的投入,意图改变行业格局。

这一竞争激化不仅促使特斯拉加速创新,也为消费者提供了更多选择。

据了解,亚马逊正在积极开发自己的电动汽车。

这家电商巨头已与数家汽车制造商展开合作,计划推出一款以亚马逊品牌命名的电动SUV。

公司高层表示,亚马逊将通过整合其在物流和智能家居领域的优势,为电动汽车行业注入新的活力。

苹果则计划于今年发布自家品牌的电动汽车。

虽然苹果始终保持沉默,但据多位知情人士透露,苹果已与多家供应商和合作伙伴展开洽谈,目前已取得了初步进展。

分析人士认为,苹果进军电动汽车领域将进一步扩大其在科技行业的影响力。

谷歌也不甘落后,正在研发一款自动驾驶的电动汽车。

该公司表示,他们的目标是打造一款能够完全自动驾驶的电动汽车,极大地改善交通效率和安全性。

分析师认为,谷歌的技术优势将使他们在电动汽车领域占据有利地位。

然而,特斯拉并不惧怕这些竞争对手。

作为业内领先的电动汽车制造商,特斯拉已建立了庞大的销售网络和忠实的用户基础。

同时,公司不断创新,持续推出更具竞争力的产品。

特斯拉的创始人马斯克更是表示,公司将会在电动汽车领域继续保持领先地位。

总结:科技巨头们的进军,无疑将给电动汽车市场带来激烈的竞争。

消费者将有更多选择,行业创新也将加速推进。

然而,特斯拉凭借其坚实的市场地位和持续的创新,依然具备竞争优势。

电动车市场的未来,将充满变数和机遇。

主题:用中我的第二封备忘录“第一季度业绩”写于1991 年4 月11 日,主要讨论了市场的钟摆运动。

13 年后,重看当年的论述,我认为一个字都不用改。

证券市场的情绪波动如同钟摆运动。

钟摆摆动弧线的中央是钟摆的“中和”位置,钟摆却很少在这个位置停留。

它总是从弧线的一个极端向另一个极端运动。

但是,当钟摆接近任何一个极端时,或早或晚,总是不可避免地要回归中点。

正是在向极端运动的过程中,钟摆积聚了回归中点的能量。

我们做投资的市场中也存在一模一样的钟摆运动:•在喜与悲之间摆动、•在欢庆顺境与哀叹逆境之间摆动、•在高估与低估之间摆动。

钟摆运动是投资领域最可靠的规律之一,投资者的心理似乎大部分时间都在走极端,不知道什么是“用中”。

自从1991 年的这封备忘录发布后,我又有了很多新的感悟,但是我仍然认为上面节选的内容基本上揭示出了市场波动的本质。

我仍然认为周期不可避免、影响深远,是商业界和投资界最可靠的一条规律。

2001 年11 月,我写了一篇题为“不预测,只准备”(You Can’t Predict. You Can Prepare) 的备忘录。

这篇备忘录没在读者中引发什么反响,不过我个人认为这篇备忘录很重要。

我在其中讨论了影响投资者的周期:•经济大周期影响可能很深远,但它们的波动很平缓。

长期的经济周期波动呈现在图表上是很缓和的波动。

•商业周期受经济大周期波动的影响,看起来更明显,它随着消费者和企业增加与减少开支而起伏。

•盈利周期的波动是企业业务规模变化的放大,而企业的业务规模变化主要受经营杠杆和财务杠杆的双重影响。

•信用周期的波动比较剧烈,因为资本市场之门时而大敞四开,时而紧紧关闭。

•上述所有周期被投资者心理放大,造就了波动最为剧烈的市场周期。

证券价格被投资者心理波动左右,经常走极端、反应过度。

人人都知道上述周期,但不是谁都能说出来它们的本质和根源。

要清楚其根源和本质,我们要深入研究人的本性和情绪。

周期现象对我们的投资收益具有重大影响,周期不是大型投资机构的投资方式引起的,也不是物理学定律引发的,本文旨在阐明投资中的周期现象主要是因为人本身具有种种弱点而且容易走极端。

蝴蝶效应行为金融学案例说起“蝴蝶效应”,想必大家都不陌生。

这个名词最早是由一位气象学家创立,而在现如今它已经不单单被用来解释气象问题,还贯穿在经济、社会的各个领域。

在全球化的今天,世界联结成一体,事实上已经没有了所谓的孤岛,世界各国都存在着千丝万缕的经济联系,处于一个相互关联且极其复杂的系统中,一个微小的初始事件,就很有可能引起系统性的整体灾难。

2008年美国金融危机爆发,其“蝴蝶效应”引起全球金融市场剧烈震荡。

危机首先影响的是美国金融业,根据当时的公开数据显示,仅在2008年初,花旗集团市值缩水高达52%,摩根大通的市值则缩水了14%,同年9月,雷曼兄弟公司宣布破产,美国金融危机全面爆发,同时美国股市暴跌。

由于金融危机的乘数效应,实体经济也随之爆发了危机。

其带来的影响就是美国的消费者支出明显萎缩,制造业开始受到影响,失业率逐步上升,美国经济受到了严重破坏。

危机带来的伤害不会只让美国一家承受。

美国作为世界经济的火车头,当其内部发生严重金融危机时,这种影响就会不断地借助“蝴蝶效应”加以放大,并通过与世界的种种复杂经济关系传递给各个国家,最后,欧盟和亚洲经济也不可避免地遭受了重大损失。

时至今日,亚洲地区的一些典型的外贸出口企业依旧对此有着深刻的切肤之痛。

在当时,原有的外贸出口订单在极短的时间内突然彻底消失,企业一度在生死线上苦苦挣扎。

任何事物的发展都存在着一定的定数与变数,而事物在发展过程中其发展轨迹既有迹可循,也会捉摸不透,存在不可预测的“变数”,有时候还会适得其反。

而一个微小的变化能影响事物的发展和结局,恰恰也说明事物发展的复杂性。

就像海水潮汐的涨落一样,大浪不是分分钟就有的。

金融危机不会突然产生并爆发,而是随着各种问题的积累,才会最终酿成金融海啸。

如果不了解其中的环节和过程,也就无法深刻理解蝴蝶扇一下翅膀为什么会造成如此严重的后果。

其实说起来金融危机的苗头还是欧洲国家经济自我冒险的结果。

法国。

论现金是企业的“血液”摘要:企业若没有充足的现金就无法运转,更可能危及企业生存。

现金对于企业,就是立命之本。

失去了立命之本,再精妙的管理方案也只会付之东流。

一味盲目叫嚣企业利润几何、资金几许,而忽视现金管理的企业,终究逃脱不了一个命运,那就是凯恩司先生所说的最后我们都会死去。

关键字:现金企业破产管理市场中有这样一条黄金定律:不管企业卖出了多少产品,如果收不回钱,那么企业最终将会出局。

有的经理人经常说自己很忙,没有时间去考虑企业现金的问题。

但当你的公司没有钱付账单的时候,企业的经营状况就会恶化。

这时,哪怕一个小小的变动都会给你的企业带来灭顶之灾。

案例一:1975 年,美国最大的商业企业之一W.T.Grant宣告破产,而在其破产前一年,其营业净利润近1000 万美元,经营活动提供营运资金2000 多万元,银行贷款达6 亿美元,1973 年公司股票价格仍按其收益20 倍的价格出售!。

该企业破产的原因就在于公司早在破产前 5 年的现金流量净额已经出现了负数,虽然有高额的利润,公司的现金不能支付巨额的生产性支出与债务费用,最后导致成长性破产。

案例二:某活动公司,刚成立半年就接了一个国内知名品牌的百万大单。

因为客户是知名企业,在付款方式上,他们接受了预付款30%,其余70%活动结束后2 个月付清的苛刻要求。

活动轰轰烈烈的开始了,该活动公司的财务也陷入了危机,因为活动的费用支出高达合同金额的70%,而客户才先付了30%,这就意味着40%的费用要该活动公司提前垫付。

而这40%就是小40 万啊!40 万对于一个刚成立的小公司来讲,是多么大的一笔数字!幸亏几位公司股东及时把自己的房子抵押了,获得了贷款,解决了危机。

案例三:江龙控股是一家集研发、生产、加工和销售于一体的大型印染企业,在短短两三年时间内,迅速成为中国最大印染企业——浙江江龙控制集团有限公司,然而,2008 年下半年,江龙控股却突然出现了危机,其倒塌速度之快也同样让人叹为观止,究其根源,出问题的地方还是企业现金。

据美国《商业周刊》网络版5月14日文章称,眼下对于中国上海和深圳两个证券交据美国《商业周刊》网络版5月14日文章称,眼下对于中国上海和深圳两个证券交易所正在形成股市泡沫的担忧确实非常严重。

越来越多的普通中国人动用储蓄账户,参与炒股。

中国已陷入历史上前所未有的股市狂热,这几乎是不争的事实。

今年第一季度,股民新开账户超过850万。

迅速致富的愿望无疑是这轮股市狂热的主要动力。

但是,对于中国家庭来说这或许也是理性之举。

对于一个已经呈现出过热迹象的经济来说,中国的利率实在太低。

而M2货币供应量的增长和银行贷款则是中国央行行长周小川及其他金融领导人的担忧。

但是,中国人民银行不可能再采取更有力的升息措施了,因为那将有悖于其它政策目标,比如为银行提供一个良好的利润缓冲,设法给巨额资本流入降温。

中国确实存在货币问题:涌入大陆的资本确实太多了。

2006年,这个世界上增长最快的经济体实现了创记录的全球贸易顺差,大约为2170亿美元,经常账户盈余达2490亿美元。

5月11日,标准渣打银行高级经济学家斯蒂芬格林预测中国的贸易顺差今年将急剧上升到3700亿美元,而经常账户盈余将冲至4000亿美元,或是占中国国内生产总值的12.8%左右。

这对发展中经济体而言确实是一个令人震惊的数字,而且必然会给主要贸易伙伴造成巨额逆差,特别是美国。

格林提出,北京的决策者只有付出巨大努力才能防止这个现象发生。

控制这些数字,更不用说中国的股市狂热了,两种最明显的办法就是允许人民币大幅升值,同时真正严格控制利率。

对于一个有着如此巨大的就业需求的经济体来说,这完全是不切实际的想法。

为了吸收新的劳动者,中国每年大约必须创造1000万至1500万个就业岗位。

除此之外,中国的综合经济增长和就业都严重依赖出口部门。

中国劳动和社会保障部5月10日估计,如果人民币升值5%至10%,那么出口部门就业岗位将减少350万个,并危及1000万个农民的利益。

因此北京不大可能改变现行的限制性货币政策,即保持人民币对美元的低估现状。

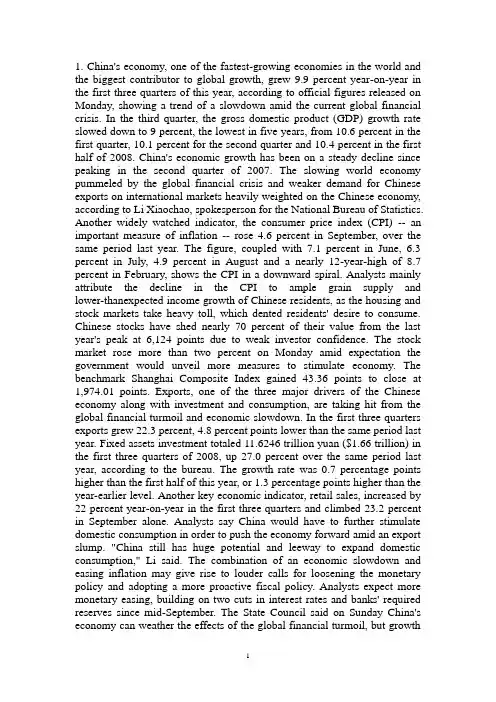

1. China's economy, one of the fastest-growing economies in the world and the biggest contributor to global growth, grew 9.9 percent year-on-year in the first three quarters of this year, according to official figures released on Monday, showing a trend of a slowdown amid the current global financial crisis. In the third quarter, the gross domestic product (GDP) growth rate slowed down to 9 percent, the lowest in five years, from 10.6 percent in the first quarter, 10.1 percent for the second quarter and 10.4 percent in the first half of 2008. China's economic growth has been on a steady decline since peaking in the second quarter of 2007. The slowing world economy pummeled by the global financial crisis and weaker demand for Chinese exports on international markets heavily weighted on the Chinese economy, according to Li Xiaochao, spokesperson for the National Bureau of Statistics. Another widely watched indicator, the consumer price index (CPI) -- an important measure of inflation -- rose 4.6 percent in September, over the same period last year. The figure, coupled with 7.1 percent in June, 6.3 percent in July, 4.9 percent in August and a nearly 12-year-high of 8.7 percent in February, shows the CPI in a downward spiral. Analysts mainly attribute the decline in the CPI to ample grain supply and lower-thanexpected income growth of Chinese residents, as the housing and stock markets take heavy toll, which dented residents' desire to consume. Chinese stocks have shed nearly 70 percent of their value from the last year's peak at 6,124 points due to weak investor confidence. The stock market rose more than two percent on Monday amid expectation the government would unveil more measures to stimulate economy. The benchmark Shanghai Composite Index gained 43.36 points to close at 1,974.01 points. Exports, one of the three major drivers of the Chinese economy along with investment and consumption, are taking hit from the global financial turmoil and economic slowdown. In the first three quarters exports grew 22.3 percent, 4.8 percent points lower than the same period last year. Fixed assets investment totaled 11.6246 trillion yuan ($1.66 trillion) in the first three quarters of 2008, up 27.0 percent over the same period last year, according to the bureau. The growth rate was 0.7 percentage points higher than the first half of this year, or 1.3 percentage points higher than the year-earlier level. Another key economic indicator, retail sales, increased by 22 percent year-on-year in the first three quarters and climbed 23.2 percent in September alone. Analysts say China would have to further stimulate domestic consumption in order to push the economy forward amid an export slump. "China still has huge potential and leeway to expand domestic consumption," Li said. The combination of an economic slowdown and easing inflation may give rise to louder calls for loosening the monetary policy and adopting a more proactive fiscal policy. Analysts expect more monetary easing, building on two cuts in interest rates and banks' required reserves since mid-September. The State Council said on Sunday China's economy can weather the effects of the global financial turmoil, but growthwill decline as business profits and public revenues slow. In a statement at the end of an executive meeting presided by Premier Wen Jiabao, it said the global turmoil and economic instability will have a "gradual" effect on the country. It said China's economic growth will slow along with corporate profits and public revenues, and as capital markets continue to fluctuate. "Unfavorable international factors and the serious natural disasters at home have not changed the basic growth situation of our country's economy," said the statement posted on a government website. "Our country's economic growth has the ability and vigor to resist risks." China must "adopt flexible and cautious macroeconomic policies" to maintain stable growth, the statement said. The State Council said that in the fourth quarter, China should focus on developing the rural economy, while striving to control inflation. Global Financial Crisis:全球金融危机international market 国际市场gross domestic product 国内生产总值consumer price index 消费者物价指数housing and stock markets 房地产和证劵市场investor confidence 投资者信心stimulate economy 刺激经济easing inflation 缓解通货膨胀investment and consumption maintain stable growth投资和消费保持稳定增长2. Macroeconomics is a sub-field of economics that examines the behavior of the economy as a whole, once all of the individual economic decisions of companies and industries have been summed. Economy-wide phenomena considered by macroeconomics include Gross Domestic Product and how it is affected by changes in unemployment, national income, rate of growth, and price levels. In contrast, microeconomics is the study of the economic behaviour and decision-making of individual consumers, firms, and industries. Macroeconomics can be used to analyze how to influence government policy goals such as economic growth, price stability, full employment and the attainment of a sustainable balance of payments. Macroeconomics is sometimes used to refer to a general approach to economic reasoning, which includes long term strategies and rational expectations in aggregate behavior. Until the 1930s most economic analysis did not separate out individual economics behavior from aggregate behavior. With the Great Depression of the 1930s, suffered throughout the developed world at the time, and the development of the concept of national income and product statistics, the field of macroeconomics began to expand.Particularly influential were the ideas of John Maynard Keynes, who formulated theories to try to explain the Great Depression. Before that time, comprehensive national accounts, as we know them today, did not exist . One of the challenges of economics has been a struggle to reconcile macroeconomic and microeconomic models. Starting in the 1950s, macroeconomists developed micro-based models of macroeconomic behavior. Dutch economist Jan Tinbergen developed the first comprehensive national macroeconomic model, which he first built for the Netherlands and later applied to the United States and the United Kingdom after World War II. The first global macroeconomic model, Wharton Econometric Forecasting Associates LINK project, was initiated by Lawrence Klein and was mentioned in his citation for the Nobel Memorial Prize in Economics in 1980. Macroeconomics 宏观经济学Price stability 价格稳定balance ofpayments 国际收支平衡表individual economics behavior 个体经济行为product statistics 产品统计individual economic decisions 个体经济决策full employment 充分就业rational expectations 理性预期long termstrategies 长期战略microeconomic models 微观经济模型3.The annual review of American company board practices by Korn/Ferry, a firm of 3. headhunters, is a useful indicator of the health of corporate governance. This year’s review, published on November 12th, shows that the Sarbanes-Oxley act, passed in 2002 to try to prevent a repeat of corporate collapses such as Enron’s and WorldCom’s, has had an impact on the boardroom--albeit at an average implementation cost that Korn/Ferry estimates at $5.1m per firm.Two years ago, only 41% of American firms said they regularly held meetings of directors without their chief executive present; this year the figure was 93%. But some things have been surprisingly unaffected by the backlash against corporate scandals. For example, despite a growing feeling that former chief executives should not sit on their company’s board, the percentage of American firms where they do has actually edged up, from 23% in 2003 to 25% in 2004. Also, disappointingly few firms have split the jobs of chairman and chief executive. Another survey of American boards published this week, by A.T. Kearney, a firm of consultants, found that in 2002 14% of the boards of S&P 500 firms had separated the roles, and a further 16% said they planned to do so. But by 2004 only 23% overall had taken the plunge. A survey earlier in the year by consultants at McKinsey found that 70% of American directors and investors supported the idea of splitting the jobs, which is standard practice in Europe. Another disappointment is the slow progress in abolishing "staggered" boards--oneswhere only one-third of the directors are up for re-election each year, to three-year terms. Invented as a defence against takeover, such boards, according to a new Harvard Law School study by Lucian Bebchuk and Alma Cohen, are unambiguously "associated with an economically significant reduction in firm value".corporate governance 企业管制splitting the jobs 分裂的工作4.taken the plunge 采取果断行动corporate scandals 公司丑闻4. The dollar's tumble this week was attended by predictable shrinks from the markets; but as it fell to a 20-month low of $1.32 against the euro, the only real surprise was that it had not slipped sooner. Indeed, there are good reasons to expect its slide to continue, dragging it below the record low of $1.36 against the euro that it hit in December 2004. The recent decline was triggered by nasty news about the American economy. New figures this week suggested that the housing market's troubles are having a wider impact on the economy. Consumer confidence and durable-goods orders both fell more sharply than expected. In contrast, German business confidence has risen to a 15-year high. There are also mounting concerns that central banks in China and elsewhere, which have been piling up dollars assiduously for years, may start selling. So, contrary to popular perceptions, America's economy has not significantly outperformed Europe's in recent years. Since 2000 its structural budget deficit (after adjusting for the impact of the economic cycle) has widened sharply, while American households' saving rate has plunged, causing the current-account deficit to swell. Over the same period, the euro-area economies saw no fiscal stimulus and household saving barely budged. Yet cyclical factors only partly explain why the dollar has been strong. At bottom, its attractiveness is based more on structural factors---or, more accurately, on an illusion about structural differences between the American and European economies. The main reason for the dollar's strength has been the widespread belief that the American economy vastly outperformed the world's other rich country economies in recent years. But the figures do not support the hypothesis. Sure, America's GDP growth has been faster than Europe's, but that is mostly because its population has grown more quickly too. Official figures of productivity growth, which should in theory be an important factor driving currency movement, exaggerate America's lead. If the two are measured on a comparable basis, productivity growth over the past decade has been almost the same in the euro area as it has in America. Even more important, the latest figures suggest that, whereas productivity growth is now slowing in America, it is accelerating in the euro zone. America's growth, thus, has been driven by consumer spending. That spending, supported by dwindling saving and increased borrowing, is clearly unsustainable; and the consequent economic and financial imbalances must inevitably unwind. As that happens, thecountry could face a prolonged period of slower growth. As for Europe, the old continent is hobbled by inflexible product and labor markets. But that, paradoxically, is an advantage: it means the place has a lot of scope for improvement. Some European countries are beginning to contemplate (and, to a limited extent, undertake) economic reforms. If they push ahead, their growth could actually speed up over the comingyears. Once investors spot this, they are likely to conclude that the euro is a better bet than the dollar. dollar's tumble 美元下跌durable-goods 耐用商品popular perceptions 流行观点structural budget 结构性预算current-account deficit 现有项目赤字currency movement 资本流通comparable basis 可比基础consumer spending 消费性开支financial imbalances 财政失衡inflexible product 缺乏弹性的产品labor markets 劳力市场5. At its heart, logistics deals with satisfying the customer. This implies that management must first understand what those requirements are before a logistics strategy can be developed and implemented to meet them. Customer service is the most important output of an organization’s logistics system. In a more practical sense, logistics refers to the systematic management of the various activities required to move benefits from their point of production to the customer. Often these benefits are in the form of a tangible product that must be manufactured and moved to the user; sometimes these benefits are intangible and are known as services. They too must be produced and made available to the final customer. But logistics encompasses much more than just the transport of goods. The concept of benefits is a multifaceted one that goes beyond the product or service itself to include issues regarding timing, quantity, supporting services, location and cost. So a basic definition of logistics is the continuous process of meeting customer needs by ensuring the availability of the fight benefits for t he right customer, in the quantity and condition desired by that customer, at the time and place the customer wants them, all for a price the buyer is willing to pay. These concepts apply equally well to for-profit industries and non-profit organizations. However, logistics can mean different things to different organization. Some firms are more concerned with producing the benefits: their management focus is on the flow of raw materials into the production process rather than on delivering the final goods to the user. Some companies are much more concerned with the flow of finished goods from the end of the production line to the customer. Logistics in this situation is sometimes referred to as physical distribution. Finally, somefirms view logistics as embracing both material management and physical distribution tasks into a single supply chain that links the customer with all aspects of the firm, sometimes it is referred to as supply chain management. logistics strategy 物流战略tangible product 有型产品continuous process 连续过程final goods 最终产品physical distribution 物资调运single supply chain单一供应链supply chain management 连锁供应管理系统Global house pricesHome truthsOur latest round-up shows that many housing markets are still in the dumpsTHE house-price boom that preceded the financial crisis was remarkable for its scope and scale. With a very few exceptions, there seemed only one way for prices to go: up. Things have been more diverse since, and our latest review of house prices is a picture with dramatic chiaroscuro. A brightening outlook for America stands out against the darkening tones of the beleaguered economies on the periphery of the euro area.In the countries we track, house prices are rising and falling in equal numbers. Over the past year prices have jumped most in Hong Kong (see table), prompting further government efforts to cool the market. They have dropped by 9.3% in Spain, the heaviest faller. The overall trend is down, however, since in three of the countries where prices are rising they are doing so at a slower pace than a year ago—in Canada, for example, they are up by 3.3% compared with 7.1% 12 months ago.A similar diversity characterises valuations. To gauge whether homes are cheap or expensive we use two measures, both of which compare current estimates with a long-run average (in most countries, going back to 1975). This average is our benchmark for “fair value”.The first gauge is a price-to-rents ratio. This is analogous to theprice-earnings ratio used for equities, with the rents going to property investors (or saved by homeowners) equivalent to corporate profits. The measure displays a massive range, from a whopping 78% overvaluation in Canada to an undervaluation of 37% in Japan. The other measure, the ratioof prices to disposable income per person, stretches from a 35% overvaluation in France to a 36% undervaluation, again in Japan. America’s housing-market revival looks sustainable in part because the sharp correction in house prices over the past few years has made homes cheap by historical standards. A year ago house prices were still falling, by 3.6%. There has been a turnaround since: the latest data show prices rising by 4.3%. But based on the ratio of prices to rents, houses are still 7% undervalued; judged by the price-to-income ratio, they are 20% below fair value. It also helps that mortgage rates are at historic lows and are likely to stay that way, since the Federal Reserve has promised to keep an extremely loose monetary stance for the next couple of years.Homeowners may be coming up for air in America, but their plight is deepening across much of Europe. The agony is most acute in Spain, where declines have gathered momentum (the 9.3% fall in our latest round-up follows a drop of 5.5% the previous year). Other big euro-zone economies are also heading in the wrong direction. In Italy and the Netherlands the pace of decline has quickened; in France prices are now edging down after a brief recovery.European valuations are most stretched in France, by as much as 50% judging by rents and by 35% on the basis of incomes. This compares with around 20% overvaluation on both counts in Spain, despite the price falls to date. But any house-price collapse in France is likely to be modest compared with Spain’s. Spain’s bust reflects a massive oversupply of housing built in the construction boom, and an unemployment rate that rose to 26.6% in November, the highest in Europe. France’s unemployment rate has edged up to 10.5% but that is in a different league to Spain’s; its banks are in better shape than Spanish ones, too.The anomaly among Europe’s big economies is Germany, where house prices are rising by a restrained 2.7%, the same pace as a year earlier. Thanks to their good fortune in missing the housing party before the financial crisis, German homeowners have a decent chance of making further gains. Homes there are 17% undervalued compared with historical averages on both our measures. German purchasers can benefit fromrock-bottom borrowing costs, unlike their counterparts in peripheral Europe. One of the lowest rates of unemployment (5.4%) in Europe further underpins the housing market.British house prices have posted only modest overall declines over the past five years (although rising rents and incomes have also helped bring things closer to fair value). But the British market may do rather better thanstill-stretched valuations suggest. For one thing, it does not suffer from the glut of empty homes that has created ghost towns in Ireland and Spain. Andaccording to the Bank of England’s latest credit-conditions survey lenders are more willing to make mortgage finance available than at any time since the financial crisis. The number of mortgage approvals for new purchases is at its highest for almost a year.Overvaluation is especially marked in Canada, particularly with respect to rents (78%) but also in relation to income (34%). Mark Carney, the country’s central-bank governor, who is soon to jump ship to join the Bank of England, where he takes over from Sir Mervyn King in July, may have shown good market timing with his move to London as well as a deft hand in negotiating his lavish remuneration. Singapore and Hong Kong also look vulnerable to a correction, given the overvaluation on their price-to-rents ratios.Misalignments with our gauges of fair value can persist for a long time, of course. That may spare countries where house prices have clearly overshot from a painful bust, but it may also mean that some markets end up mimicking Japan’s long descent and badly undershoot. At some point, central banks will have to take away the balm of easy money. If housing markets remain so fragile when they are getting so much help, they may break when it is removed.。

(Cushing)——WTI 原油唯一交割地点的储存容量出现了危险的短缺,交易员和投资者感到焦虑,冲动之下急于卖出。

《华尔街日报》的一篇报道指出:“投资者和交易员不愿接收石油,以至于他们愿意付钱给其他人,让他们接收这些石油。

”“对储存能力不足的恐慌,导致人们急于抛售期货合约,”怀俄明大学石油和天然气经济学教授查尔斯·梅森(Charles F. Mason)说,“如果你签订期货合同,那么就有义务在特定时点交付产品,但你要有时间为此做计划……我们在这里看到的是,那些持有期货合约的人,有权力在某个时间点获得原油,但他们没有地方存放,因为存储能力已经满了。

也许他们在等待,希望事情会有所缓和,结果事与愿违,所以他们非常恐慌。

”出人意料的价格暴跌,强化了供应过剩的程度,沃顿商学院金融学教授杰里米·西格尔(Jeremy Siegel)表示: “这是交易员对俄克拉荷马州库欣存储能力的严重错估,否则,人们为什么会购买长期合约?”新冠肺炎疫情以前所未有的方式重创了石油市场。

“能源分析人士非常善于解释,如果某些冲击真的发生,会如何影响石油市随着消费需求的急剧下降,冠状病毒大流行为石油行业创造了一个艰难的新世界。

4月中旬,4月21日到期的美国基准原油——西德克萨斯中质原油(WTI)期货合约价格转为每桶-37.63美元。

现货价格也跌破零,恐慌的石油生产商和交易商抛售了大量期货合约。

北海地区基准原油布伦特(Brent)的价格也现下跌,不过仍维持在正区间。

4月底开始,基准WTI 原油价格又开始回升(至6月上旬,已升至每桶38美元左右)。

然而,短暂的负价格的确使这个行业遇到了新的问题,问题已不仅是新冠肺炎疫情将在多长时间内以及在多大程度上降低对原油的需求。

对石油生产商来说,油价下跌让他们一度担心要花钱让买家购买其石油。

现在,他们面临更长期的担忧,比如削减产量,关闭生产井,推迟新开井,推迟勘查。

许多公司将面临申请破产或在一波整合浪潮中被收购。

三明治效应案例三明治效应,又称为三明治效果,是指在一段时间内,一个国家或地区的经济增长速度放缓,然后再次加速增长的现象。

这一术语最早由美国经济学家阿瑟·奥肯在20世纪50年代提出,用来描述美国经济在20世纪30年代经历了一次持续了10年之久的经济衰退之后,再次迅速复苏的情况。

三明治效应通常是由于一些结构性变化或者政策调整所导致的,而这些变化或者调整往往需要一定的时间才能够产生显著的效果。

一个典型的三明治效应案例就是中国的经济发展。

在上世纪70年代末至80年代初,中国实行了改革开放政策,经济开始逐渐向市场经济转型。

然而,由于历史遗留问题和体制机制不完善,中国的经济增长一度放缓,甚至出现了通货膨胀等问题。

但是随着改革开放政策的不断深化和完善,中国的经济再次迎来了快速增长的时期,成为世界上经济增长最快的国家之一。

另一个典型的案例是日本的经济发展。

20世纪80年代,日本经济曾经处于高速增长期,被誉为亚洲四小龙之一。

然而,随着泡沫经济的破灭,日本经济陷入了长达20年的低增长期,甚至出现了通货紧缩的情况。

然而,日本政府通过一系列的经济政策和结构性改革,逐渐使经济走出低迷,再次实现了增长。

三明治效应案例不仅仅局限于国家层面,也可以在企业和行业中找到。

比如,诺基亚公司曾经是全球手机市场的霸主,然而随着智能手机的兴起,诺基亚的市场份额迅速下滑。

但是诺基亚通过不断创新和转型,重新找到了自己在智能手机市场中的位置,实现了再次崛起。

总的来说,三明治效应案例告诉我们,经济增长和发展往往不是一帆风顺的,会经历起伏和波动。

但是只要我们能够及时调整政策、改革体制,不断创新,就有可能实现再次复苏和增长。

这也给我们一个启示,就是在面对困难和挑战的时候,不要轻易放弃,要有信心和勇气,相信只要我们坚持努力,就一定能够迎来新的机遇和发展。

未曾注意到的价值沃伦·巴菲特说,价格是你付出的,价值是你得到的。

那么,什么是价值?什么才能为公司创造价值?你可以回答说是“经济护城河”,这没有错。

而当我确认什么才是公司高价值的时候,实际上就是说,它有助于改善公司的绩效,或是有利于公司完全区别于其竞争对手,这就是公司的价值。

你可能对其视而不见,但是它却能够满足顾客的需求,为企业创造价值,并使企业在竞争中出乎其类而拔乎其萃。

以下列举两个例子,看看这两家公司是如何创造“价值”的。

第一个案例:美铝公司。

美铝公司是世界铝生产制造业的领导者,致力于生产铝这种具有可持续性的产品,其主要产品包括压延产品、轮毂、锻件、紧固件系统、精密铸件以及建筑系统领域的解决方案等,其技术还涉及包括钛镍超级合金在内的其他轻金属。

不过,1991年当保罗·奥尼尔入主美铝时,美铝已经是老态龙钟而步履蹒跚了。

因此奥尼尔需要“突飞猛进的实质性改进”。

他认为必须以安全性推动企业飞跃,超越竞争对手。

他将目光投向最基础最实在的东西——安全。

“安全”这个词在今天最平常不过了,但在那时却少有人提高到战略的层面上。

许多企业天天喊着“安全生产”之类的口号,实际上却安全事故不断。

奥尼尔重新审视了安全对公司的重要性,认为,安全是一个表明企业经营业绩如何或是可能会如何的首要问题。

因此他要求安全的任务必须包括如下几点:1、确认安全的工作环境,避免员工驾车时参加电话会议等。

2、穿戴安全服饰,要求员工在工作期间必须佩戴硬质头盔和穿放热工作服。

3、为不同岗位配备具有相应资历的人员,减少人员错配情况的发生。

美铝始终把工作与“零工伤”结合在一起的思想,深入到每个员工的内心深处。

奥尼尔就任时,美铝百人重伤事故为1.44人次,这已经优于整个美国制造业的4.73人次。

奥尼尔就任后,其伤病事故率更是减少至0.75人次,这对于像美铝这样采矿和熔炼类的企业来说,绝对是不可思议的。

美铝对安全生产的高度重视为提高员工的士气带来了显著效果,反过来也提高了企业的经营绩效,为公司在劳动力就业市场上赢得声誉。