会计学毕业论文中英文资料外文翻译文献

- 格式:docx

- 大小:55.69 KB

- 文档页数:12

云会计发展状况研究外文文献翻译最新译文XXX of the development of cloud accounting research。

focusing on the d from 2010 to 2015.The XXX discussing its XXX It then reviews the existing literature on cloud accounting。

including studies on n。

security。

privacy。

and performance。

The paper also XXX。

Finally。

XXX.译文:本文概述了云会计研究的发展情况,重点关注2010年至2015年期间。

文章首先定义了云会计并讨论了其潜在的优势和挑战。

接着,文章对现有的云会计文献进行了回顾,包括有关采用、安全、隐私和绩效的研究。

文章还确定了文献中的空白,并提出了未来研究的方向。

最后,文章讨论了云会计对会计实践和教育的影响。

With the rise of the。

and the rapid development of n and XXX。

XXX changes。

system are。

ork platforms。

interactive experiences。

and other fields are being pushed to the forefront。

XXX.XXX has only been around for a few short years。

but XXX of the market and is XXX。

The accounting industry is no n。

and accounting n and cloud XXX linked。

The cloud accounting concept appears more natural。

and its technical advantages of low cost。

. '. 原文:Introduction to Financial Management Sourse:Ryan Allis.Zero to one million.February 2008

Business financial management in the small firm is characterized, in many different cases, by the need to confront a somewhat different set of problems and opportunities than those confronted by a large corporation. One immediate and obvious difference is that a majority of smaller firms do not normally have the opportunity to publicly sell issues of stocks or bonds in order to raise funds. The owner-manager of a smaller firm must rely primarily on trade credit, bank financing, lease financing, and personal equity to finance the business. One, therefore faces a much more severely restricted set of financing alternatives than those faced by the financial vice president or treasurer of a large corporation. On the other hand, when small business financial management is concern, many financial problems facing the small firm are very similar to those of larger corporations. For example, the analysis required for a long-term investment decision such as the purchase of heavy machinery or the evaluation of lease-buy alternatives, is essentially the same regardless of the size of the firm. Once the decision is made, the financing alternatives available to the firm may be radically different, but the decision process will be generally similar. One area of particular concern for the smaller business owner lies in the effective management of working capital. Net working capital is defined as the difference between current assets and current liabilities and is often thought of as the "circulating capital" of the business. Lack of control in this crucial area is a primary cause of business failure in both small and large firms. The business manager must continually be alert to changes in working capital accounts, the cause of these changes and the implications of these changes for the financial health of the company. One convenient and effective method to highlight the key managerial requirements in this area is to view working capital in terms of its major components: (1) Cash and Equivalents This most liquid form of current assets, cash and cash equivalents (usually marketable securities or short-term certificate of deposit) requires constant supervision. A well planned and maintained cash budgeting system is essential to answer key questions such as: Is the cash level adequate to meet current expenses as they come due? What are the timing relationships between cash inflows and outflows? When will peak cash needs occur? What will be the magnitude of bank borrowing required to meet any cash shortfalls? When will this borrowing be necessary and when may repayment be expected? (2) Accounts Receivable Almost all businesses are required to extend credit to their customers. Key issues in this area include: Is the amount of accounts receivable reasonable in relation to sales? On the average, how rapidly are accounts receivable being collected? Which customers are "slow payers?" What action should be taken to speed collections where needed? (3) Inventories Inventories often make up 50 percent or more of a firm's current assets and therefore, are deserving of close scrutiny. Key questions which must be considered in this area include: Is the level of inventory reasonable in relation to sales and the operating characteristics of the business? . '. How rapidly is inventory turned over in relation to other companies in the same industry? Is any capital invested in dead or slow moving stock? Are sales being lost due to inadequate inventory levels? If appropriate, what action should be taken to increase or decrease inventory? (4) Accounts Payable and Trade Notes Payable In a business, trade credit often provides a major source of financing for the firm. Key issues to investigate in this category include: Is the amount of money owed to suppliers reasonable in relation to purchases? Is the firm's payment policy such that it will enhance or detract from the firm's credit rating? If available, are discounts being taken? What are the timing relationships between payments on accounts payable and collection on accounts receivable? (5) Notes Payable Notes payable to banks or other lenders are a second major source of financing for the business. Important questions in this class include: What is the amount of bank borrowing employed? Is this debt amount reasonable in relation to the equity financing of the firm? When will principal and interest payments fall due? Will funds be available to meet these payments on time? (6) Accrued Expenses and Taxes Payable Accrued expenses and taxes payable represent obligations of the firm as of the date of balance sheet preparation. Accrued expenses represent such items as salaries payable, interest payable on bank notes, insurance premiums payable, and similar items. Of primary concern in this area, particularly with regard to taxes payable, is the magnitude, timing, and availability of funds for payment. Careful planning is required to insure that these obligations are met on time.

会计准那么外文文献及翻译-财务会计专业(含:英文原文及中文译文)文献出处:Buschhüter M, Striegel A. IAS 37 – Provisions, Contingent Liabilities and Contingent Assets[M]// Kommentar Internationale Rechnungslegung IFRS. Gabler, 2021:955-974.英文原文Accounting Standard (AS) 37Contingent Liabilities and Contingent AssetsBuschhüter M, Striegel AThis International Accounting Standard was approved by the IASC Board in July 1998 and became effective for financial statements covering periods beginning on or after 1 July 1999.Introduction1. IAS 37 prescribes the accounting and disclosure for all provisions, contingent liabilities and contingent assets, except:(a) those resulting from financial instruments that are carried at fair value;(b) those resulting from executory contracts, except where the contract is onerous. Executory contracts are contracts under which neither party has performed any of its obligations or both parties have partially performed their obligations to an equal extent;(c) those arising in insurance enterprises from contracts with policyholders;(d) those covered by another International Accounting Standard. Provisions2. The Standard defines provisions as liabilities of uncertain timing or amount. A provision should be recognised when, and only when:(a) an enterprise has a present obligation (legal or constructive) as a result of a past event; (b) it is probable (i.e. more likely than not) that an outflow of resources embodying economic benefits will be required to settle the obligation;(c) a reliable estimate can be made of the amount of the obligation. The Standard notes that it is only in extremely rare cases that a reliable estimate will not be possible.3. The Standard defines a constructive obligation as an obligation that derives from an enterprise's actions where:(a) by an established pattern of past practice, published policies or a sufficiently specific current statement, the enterprise has indicated to other parties that it will accept certain responsibilities; (b) as a result, the enterprise has created a valid expectation on the part of those other parties that it will discharge those responsibilities.4. In rare cases, for example in a law suit, it may not be clear whether an enterprise has a present obligation. In these cases, a past event is deemed to give rise to a present obligation if, taking account of all available evidence, it is more likely than not that a present obligation exists at thebalance sheet date. An enterprise recognises a provision for that present obligation if the other recognition criteria described above are met. If it is more likely than not that no present obligation exists, the enterprise discloses a contingent liability, unless the possibility of an outflow of resources embodying economic benefits is remote.5. The amount recognized as a provision should be the best estimate of the expenditu required to settle the present obligation at the balance sheet date, in other words, the amount that an enterprise would rationally pay to settle the obligation at the balance sheet date or to transfer it to a third party at that time.6. The Standard requires that an enterprise should, in measuring a provision: (a) take risks and uncertainties into account. However, uncertainty does not justify the creation of excessive provisions or a deliberate overstatement of liabilities;(b) discount the provisions, where the effect of the time value of money is material, using a pre-tax discount rate (or rates) that reflect(s) current market assessments of the time value of money and those risks specific to the liability that have not been reflected in the best estimate of the expenditure. Where discounting is used, the increase in the provision due to the passage of time is recognised as an interest expense;(c) take future events, such as changes in the law and technological changes, into account where there is sufficient objective evidence thatthey will occur; and(d) not take gains from the expected disposal of assets into account, even if the expected disposal is closely linked to the event giving rise to the provision.7. An enterprise may expect reimbursement of some or all of the expenditure required to settle a provision (for example, through insurance contracts, indemnity clauses or suppliers' warranties). An enterprise should:(a) recognise a reimbursement when, and only when, it is virtually certain that reimbursement will be received if the enterprise settles the obligation. The amount recognised for the reimbursement should not exceed the amount of the provision; and(b) recognise the reimbursement as a separate asset. In the income statement, the expense relating to a provision may be presented net of the amount recognised for a reimbursement. 8. Provisions should be reviewed at each balance sheet date and adjusted reflect thecurrent best estimate. If it is no longer probable that an outflow of resources embodying economic benefits will be required to settle the obligation, the provisioshould be reversed.9. A provision should be used only for expenditures for which the provision was originally recognised.Provisions - Specific Applications10. The Standard explains how the general recognition and measurement requirements for provisions should be applied in three specific cases: future operating losses; onerous contracts; and restructurings. Contingent Liabilities11. An enterprise should not recognise a contingent liability. , unless the12. A contingent liability is disclosed, as required by paragraph 86possibility of an outflow of resources embodying economic benefits is remote.13. Where an enterprise is jointly and severally liable for an obligation, the part of tobligation that is expected to be met by other parties is treated as a contingentThe enterprise recognises a provision for the part of the obligation for which an outflow of resources embodying economic benefits is probable, except in the extremely rare circumstances where no reliable estimate can be made.14. Contingent liabilities may develop in a way not initially expected. Therefore, theare assessed continually to determine whether an outflow of resources embodying probable. If it becomes probable that an outflow of economic benefits has become future economic benefits will be required for an item previously dealt with as a contingent liability, a provision is recognised in the financial statements of the period in which the change in probability occurs (except in the extremely rare circumstances where no reliable estimate can be made).Contingent Assets15. An enterprise should not recognise a contingent asset.16. Contingent assets usually arise from unplanned or other unexpected events that give rise to the possibility of an inflow of economic benefits to the enterprise. An example is a claim that an enterprise is pursuing through legal processes, where the outcome is uncertain. 17. Contingent assets are not recognised in financial statements since this may result in the recognition of income that may never be realised. However, when the realisation of income is virtually certain, then the related asset is not a contingent asset and its recognition is appropriate. 18. A contingent asset is disclosed, as required by paragraph 89 economic benefits is probable.19. Contingent assets are assessed continually to ensure that developments are appropriately reflected in the financial statements. If it has become virtually certain that an inflow of economic benefits will arise, the asset and the related income are recognised in the financial statements of the period in which the change occurs. If an inflow of economic benefits has become probable, an enterprise discloses the contingent asset.Measurement20. The amount recognised as a provision should be the best estimate of the expenditure required to settle the present obligation at the balance sheet date.21. The best estimate of the expenditure required to settle the present obligation is the amount that an enterprise would rationally pay to settle the obligation at the balance sheet date or to transfer it to a third party at that time. It will often be impossible or prohibitively expensive to settle or transfer an obligation at the balance sheet date. However, the estimate of the amount that an enterprise would rationally pay to settle or transfer the obligation gives the best estimate of the expenditure required to settle the present obligation at the balance sheet date. 22. The estimates of outcome and financial effect are determined by the judgement of the management of the enterprise, supplemented by experience of similar transactions and, in some cases, reports from independent experts. The evidence considered23. Uncertainties surrounding the amount to be recognised as a provision are dealt with by various means according to the circumstances. Where the provision being measured involves a large population of items, the obligation is estimated by weighting all possible outcomes by their associated probabilities. The name for thistatistical method of estimation is 'expected value'. The provision will therefore be different depending on whether the probability of a loss of a given amount is, for example, 60 per cent or 90 per cent. Where there is a continuous range of possible outcomes, and each point in that range is as likely as any other, the mid-point of thrange is used. 24. Where a single obligation is beingmeasured, the individual most likely outcome may be the best estimate of the liability. However, even in such a case, the enterprise considers other possible outcomes. Where other possible outcomes are either mostly higher or mostly lower than the most likely outcome, the best estimate will be a higher or lower amount. For example, if an enterprise has to rectify a serious fault in a major plant that it has constructed for a customer, the individual most likely outcome may be for the repair to succeed at the first attempt at a cost of1,000, but a provision for a larger amount is made if there is a significant chance that further attempts will be necessary.25. The provision is measured before tax, as the tax consequences of the provision, , Income Taxes. and changes in it, are dealt with under IAS 12,Income Taxes.Risks and Uncertainties26. The risks and uncertainties that inevitably surround many events and the best estimate of a circumstances should be taken into account in reachin the best estmeate of a provision.27. Risk describes variability of outcome. A risk adjustment may increase the amount at which a liability is measured. Caution is needed in making judgements under conditions of uncertainty, so that income or assets are not overstated and expenses or liabilities are not understated. However, uncertainty does not justify the creation of excessive provisions or adeliberate overstatement of liabilities. For example, if the projected costs of a particularly adverse outcome are estimated on a prudent basis, that outcome is not then deliberately treated as more probable than is realistically the case. Care is needed to avoid duplicating adjustments for risk and uncertainty with consequent overstatement of a provision. Present Value28. Where the effect of the time value of money is material, the amount ofa provision should be the present value of the expenditures expected to be required to settle the obligation.29. The discount rate (or rates) should be a pre-tax rate (or rates) that reflect(s) current market assessments of the time value of money and the risks specific to the liability. The discount rate(s) should not reflect risks for which future cash flow estimates have been adjusted. Future Events 30. Future events that may affect the amount required to settle an obligation should be reflected in the amount of a provision where there is sufficient objective evidence that they will occur.31. Expected future events may be particularly important in measuring provisions. For example, an enterprise may believe that the cost of cleaning up a site at the end of its life will be reduced by future changes in technology. The amount recognised reflects a reasonable expectation of technically qualified, objective observers, taking account of all available evidence as to the technology that will be available at the time of theclean-up. Thus it is appropriate to include, for example, expected cost reductions associated with increased experience in applying existing technology or the expected cost of applying existing technology to a larger or more complex clean-up operation than has previously been carried out. However, an enterprise does not anticipate the new technology for cleaning up unless it is supported by development of a completel sufficient objective evidence.32. The effect of possible new legislation is taken into consideration in measuring an existing obligation when sufficient objective evidence exists that the legislation is virtually certain to beenacted. The variety of circumstances that arise in practice makes it impossible to specify a single event that will provide sufficient, objective evidence in every case. Evidence is required both of what legislation will demand and of whether it is virtually certain to be enacted and implemented in due course. In many cases sufficient objective evidence will not exist until the new legislation is enacted.Expected Disposal of Assets33. Gains from the expected disposal of assets should not be taken into account in measuring a provision.34. Gains on the expected disposal of assets are not taken into account in measuring a provision, even if the expected disposal is closely linked to the event giving rise to the provision. Instead, an enterprise recognisesgains on expected disposals of assets at the time specified by the International Accounting Standard dealing with the assets concerned. Reimbursements35. Where some or all of the expenditure required to settle a provision is expected to be reimbursed by another party, the reimbursement should be recognised when, and only when, it is virtually certain that reimbursement will be received if the enterprise settles the obligation. The reimbursement should be treated as a separate asset. The amount recognised for the reimbursement should not exceed the amount of the provision.36. In the income statement, the expense relating to a provision may be presented net of the amount recognised for a reimbursement.37. Sometimes, an enterprise is able to look to another party to pay part or all of the expenditure required to settle a provision (for example, through insurance contracts, indemnity clauses or suppliers' warranties). The other party may either reimburse amounts paid by the enterprise or pay the amounts directly.38. In most cases the enterprise will remain liable for the whole of the amount in question so that the enterprise would have to settle the full amount if the third party failed to pay for any reason. In this situation, a provision is recognised for the full amount of the liability, and a separate asset for the expected reimbursement is recognised when it is virtuallycertain that reimbursement will be received if the enterprise settles the liability.39. In some cases, the enterprise will not be liable for the costs in question if the third party fails to pay. In such a case the enterprise has no liability for those costs and they are not included in the provision.40. As noted in paragraph 29,severally liable is a contingent liability to the extent that it is expected that the obligation will be settled by the other parties.Changes in Provisions41. Provisions should be reviewed at each balance sheet date and adjusted to reflect the current best estimate. If it is no longer probable that an outflow of resources embodying economic benefits will be required to settle the obligation, the provision should be reversed.42. Where discounting is used, the carrying amount of a provision increases in each period to reflect the passage of time. This increase is recognised as borrowing cost.Use of Provisions43. A provision should be used only for expenditures for which the provision was originally recognised.44. Only expenditures that relate to the original provision are set against it. Setting expenditures against a provision that was originally recognised for another purpose would conceal the impact of two different events.Future Operating Losses45. Provisions should not be recognised for future operating losses.46. Future operating losses do not meet the definition of a liability in paragraph 10.the general recognition criteria set out for provisions in paragraph 1447. An expectation of future operating losses is an indication that certain assets of the operation may be impaired. An enterprise tests these assets for impairment under IAS 36, Impairment of Assets.Onerous Contracts48. If an enterprise has a contract that is onerous, the present obligation under the contract should be recognised and measured as a provision. 49. Many contracts (for example, some routine purchase orders) can be cancelled without paying compensation to the other party, and therefore there is no obligation. Other contracts establish both rights and obligations for each of the contracting parties. Where events make such a contract onerous, the contract falls within the scope of this Standard and a liability exists which is recognised. Executory contracts that are not onerous fall outside the scope of this Standard. 50. This Standard defines an onerous contract as a contract in which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received under it. The unavoidable costs under a contract reflect the least net cost of exiting from the contract, which is the lower ofthe cost of fulfilling it and any compensation or penalties arising from failure to fulfil it.51. Before a separate provision for an onerous contract is established, an enterprise recognises any impairment loss that has occurred on assets dedicated to that contract(see IAS 36, Impairment of Assets). Restructuring52. The following are examples of events that may fall under the definition of restructuring: (a) sale or termination of a line of business; (b) the closure of business locations in a country or region or the relocation of business activities from one country or region to another; (c) changes in management structure, for example, eliminating a layer of management; (d) fundamental reorganisations that have a material effect on the nature and focus of the enterprise's operations.53. A provision for restructuring costs is recognised only when the general recognition are met. Paragraphs 72-83 set out how criteria for provisions set out in paragraph 14the general recognition criteria apply to restructurings.54. A constructive obligation to restructure arises only when an enterprise:(a) has a detailed formal plan for the restructuring identifying at least: (i) the business or part of a business concerned;(ii) the principal locations affected;(iii) the location, function, and approximate number of employees whowill be compensated for terminating their services;(iv) the expenditures that will be undertaken;(v) when the plan will be implemented;(b) has raised a valid expectation in those affected that it will carry out the restructuring by starting to implement that plan or announcing its main features to those affected by it. . Evidence that an enterprise has started to implement a restructuring plan would be provided, 55for example, by dismantling plant or selling assets or by the public announcement of the main features of the plan. A public announcement of a detailed plan to restructure constitutes a constructive obligation to restructure only if it is made in such a way and in sufficient detail (i.e. setting out the main features of the plan) that it gives rise to valid expectations in other parties such as customers, suppliers and employees (or their representatives) that the enterprise will carry out the restructuring.56. For a plan to be sufficient to give rise to a constructive obligation when communicated to those affected by it, its implementation needs to be planned to begin as soon as possible and to be completed in a timeframe that makes significant changes to the plan unlikely. If it is expected that there will be a long delay before the restructuring begins or that the restructuring will take an unreasonably long time, it is unlikely that the plan will raise a valid expectation on the part of others that theenterprise is at present committed to restructuring, because the timeframe allows opportunities for the enterprise to change its plans.57. A management or board decision to restructure taken before the balance sheet date does not give rise to a constructive obligation at the balance sheet date unless the enterprise has, before the balance sheet date:(a) started to implement the restructuring plan;(b) announced the main features of the restructuring plan to those affected by it in a sufficiently specific manner to raise a valid expectation in them that the enterprise will carry out the restructuring. In some cases, an enterprise starts to implement a restructuring plan, or announces its main features to those affected, only after the balance sheet date. Disclosure may be , Events After the Balance Sheet Date, if the restructuring is of required under IAS 10 such importance that its non-disclosure would affect the ability of the users of the financial statements to make proper evaluations and decisions.58. Although a constructive obligation is not created solely by a management decision, an obligation may result from other earlier events together with such a decision. For example, negotiations with employee representatives for termination payments, or with purchasers for the sale of an operation, may have been concluded subject only to board approval. Once that approval has been obtained and communicated to the other parties, the enterprise has a constructive obligation to restructure, if theconditions of paragraph 72 are met.. 59. In some countries, the ultimate authority is vested in a board whose membership gement (e.g. employees) includes representatives of interests other than those of managment.or notification to such representatives may be necessary before the board decision is taken. Because a decision by such a board involves communication to these representatives, it may result in a constructive obligation to restructure.60. No obligation arises for the sale of an operation until the enterprise is committed to the sale, i.e. there is a binding sale agreement.61. Even when an enterprise has taken a decision to sell an operation and announced that decision publicly, it cannot be committed to the sale until a purchaser has been identified and there is a binding sale agreement. Until there is a binding sale agreement, the enterprise will be able to change its mind and indeed will have to take another course of action if a purchaser cannot be found on acceptable terms. When the sale of an operation is envisaged as part of a restructuring, the assets of the operation , Impairment of Assets. When a sale is only are reviewed for impairme-ent under IAS 36part of a restructuring, a constructive obligation can arise for the other parts of the restructuring before a binding sale agreement exists.62. A restructuring provision should include only the direct expenditures arising form the restrict-uring,which are those that are both:(a) necessarily entailed by the restructuring; and(b) not associated with the ongoing activities of the enterprise.63. A restructuring provision does not include such costs as:(a) retraining or relocating continuing staff;(b) marketing; or(c) investment in new systems and distribution networks.These expenditures relate to the future conduct of the business and are not liabilities for restructuring at the balance sheet date. Such expenditures are recognised on the same basis as if they arose independently of a restructuring.64. Identifiable future operating losses up to the date of a restructuring are not included in a provision, unless they relate to an onerous contract as defined in paragraph 10. , gains on the expected disposal of assets are not taken65. As required by paragraph 51into account in measuring a restructuring provision, even if the sale of assets is envisaged as part of the restructuring.Disclosure66. For each class of provision, an enterprise should disclose:(a) the carrying amount at the beginning and end of the period;(b) additional provisions made in the period, including increases toexisting provisions; (c) amounts used (i.e. incurred and charged against the provision) during the period; (d) unused amounts reversed during the period; and(e) the increase during the period in the discounted amount arising from the passage of time and the effect of any change in the discount rate. Comparative information is not required67. An enterprise should disclose the following for each class of provision:(a) a brief description of the nature of the obligation and the expected timing of any resulting outflows of economic benefits;(b) an indication of the uncertainties about the amount or timing of those outflows. Where necessary to provide adequate information, an enterprise should disclose the major assumptions made concerning future events, as addressed in paragraph 48(c) the amount of any expected reimbursement, stating the amount of any asset that has been recognised for that expected reimbursement.68. Unless the possibility of any outflow in settlement is remote, an enterprise should disclose for each class of contingent liability at the balance sheet date a brief description of the nature of the contingent liability and, where practicable:;(a) an estimate of its financial effect, measured under paragraphs 36(b) an indication of the uncertainties relating to the amount or timing of any outflow; (c) the possibility of any reimbursement.69. In determining which provisions or contingent liabilities may be aggregated to form a class, it is necessary to consider whether the nature of the items is sufficiently similar for a single statement about them to fulfil the requirements of paragraphs 85(a)and (b) and 86(a) and (b). Thus, it may be appropriate to treat as a single class of provision amounts relating to warranties of different products, but it would not be appropriate to treat as a single class amounts relating to normal warranties and amounts that are subject to legal proceedings.70. Where a provision and a contingent liability arise from the same set of -86 in a circumstances, an enterprise makes the disclosures required by paragraphs 84 that shows the link between the provision and the contingent liability.71. Where an inflow of economic benefits is probable, an enterprise should disclose a brief description of the nature of the contingent assets at the balance sheet date, and, where practicable, an estimate of their financial effect, measured using the principles set out for provisions in paragraphs 3672. It is important that disclosures for contingent assets avoid giving misleading ndications of the likelihood of income arising.73 In extremely rare cases, disclosure of some or all of the information required by paragraphs 84-89 can be expected to prejudice seriously the position of the enterprise a dispute with other parties on the subject matterof the provision, contingent or contingent asset. In such cases, an enterprise need not disclose the information, but should disclose the general nature of the dispute, together with the fact that, and reason why, the information has not been disclosed. Transitional Provisions74. The effect of adopting this Standard on its effective date (or earlier) should be reported as an adjustment to the opening balance of retained earnings for the period in which the Standard is first adopted. Enterprises are encouraged, but not required, to adjust the opening balance of retained earnings for the earliest period presented and to restate comparative information. If comparative information is not restated, this fact should be disclosed. , Net Profit or Loss for the75. The Standard requires a different treatment from IAS 8requires Period, Fundamental Errors and Changes in Accounting Policies. IAS 8comparative information to be restated (benchmark treatment) or additional pro forma comparative information on a restated basis to be disclosed (allowed alternative reatment) unless it is impracticable to do so.。

IMPLEMENTING ENVIRONMENTAL COSTACCOUNTING IN SMALL AND MEDIUM-SIZEDCOMPANIES1.ENVIRONMENTAL COST ACCOUNTING IN SMESSince its inception some 30 years ago, Environmental Cost Accounting (ECA) has reached a stage of development where individual ECA systems are separated from the core accounting system based an assessment of environmental costs with (see Fichter et al., 1997, Letmathe and Wagner , 2002).As environmental costs are commonly assessed as overhead costs, neither the older concepts of full costs accounting nor the relatively recent one of direct costing appear to represent an appropriate basis for the implementation of ECA. Similar to developments in conventional accounting, the theoretical and conceptual sphere of ECA has focused on process-based accounting since the 1990s (see Hallay and Pfriem, 1992, Fischer and Blasius, 1995, BMU/UBA, 1996, Heller et al., 1995, Letmathe, 1998, Spengler and H.hre, 1998).Taking available concepts of ECA into consideration, process-based concepts seem the best option regarding the establishment of ECA (see Heupel and Wendisch , 2002). These concepts, however, have to be continuously revised to ensure that they work well when applied in small and medium-sized companies.Based on the framework for Environmental Management Accounting presented in Burritt et al. (2002), our concept of ECA focuses on two main groups of environmentally related impacts. These are environmentally induced financial effects and company-related effects on environmental systems (see Burritt and Schaltegger, 2000, p.58). Each of these impacts relate to specific categories of financial and environmental information. The environmentally induced financial effects are represented by monetary environmental information and the effects on environmental systems are represented by physical environmental information. Conventional accounting deals with both – monetary as well as physical units – but does not focus on environmental impact as such. To arrive at a practical solution to the implementation of E CA in a company’s existing accounting system, and to comply with the problem of distinguishing between monetary and physical aspects, an integrated concept is required. As physical information is often the basis for the monetary information (e.g. kilograms of a raw material are the basis for the monetary valuation of raw material consumption), the integration of this information into the accounting system database is essential. From there, the generation of physical environmental and monetary (environmental) information would in many cases be feasible. For many companies, the priority would be monetary (environmental) information for use in for instance decisions regarding resource consumptions and investments. The use of ECA in small andmedium-sized enterprises (SME) is still relatively rare, so practical examples available in the literature are few and far between. One problem is that the definitions of SMEs vary between countries (see Kosmider, 1993 and Reinemann, 1999). In our work the criteria shown in Table 1 are used to describe small and medium-sized enterprises.Table 1. Criteria of small and medium-sized enterprisesNumber of employees TurnoverUp to 500employees Turnover up to EUR 50mManagement Organization- Owner-cum-entrepreneur -Divisional organization is rare- Varies from a patriarchal management -Short flow of information style in traditional companies and teamwork -Strong personal commitmentin start-up companies -Instruction and controlling with- Top-down planning in old companies direct personal contact- Delegation is rare- Low level of formality- High flexibilityFinance Personnel- family company -easy to survey number of employees- limited possibilities of financing -wide expertise-high satisfaction of employeesSupply chain Innovation-closely involved in local -high potential of innovationeconomic cycles in special fields- intense relationship with customersand suppliersKeeping these characteristics in mind, the chosen ECA approach should be easy to apply, should facilitate the handling of complex structures and at the same time be suited to the special needs of SMEs.Despite their size SMEs are increasingly implementing Enterprise Resource Planning (ERP) systems like SAP R/3, Oracle and Peoplesoft. ERP systems support business processes across organizational, temporal and geographical boundaries using one integrated database. The primary use of ERP systems is for planning and controlling production and administration processes of an enterprise. In SMEs however, they are often individually designed and thus not standardized making the integration of for instance software that supports ECA implementation problematic. Examples could be tools like the “eco-efficiency” approach of IMU (2003) or Umberto (2003) because these solutions work with the database of more comprehensive software solutions like SAP, Oracle, Navision or others. Umberto software for example (see Umberto, 2003) would require large investments and great background knowledge of ECA – which is not available in most SMEs.The ECA approach suggested in this chapter is based on an integrative solution –meaning that an individually developed database is used, and the ECA solution adopted draws on the existing cost accounting procedures in the company. In contrast to other ECA approaches, the aim was to create an accounting system that enables the companies to individually obtain the relevant cost information. The aim of the research was thus to find out what cost information is relevant for the company’s decision on environmental issues and how to obtain it.2.METHOD FOR IMPLEMENTING ECASetting up an ECA system requires a systematic procedure. The project thus developed a method for implementing ECA in the companies that participated in the project; this is shown in Figure 1. During the implementation of the project it proved convenient to form a core team assigned with corresponding tasks drawing on employees in various departments. Such a team should consist of one or two persons from the production department as well as two from accounting and corporate environmental issues, if available. Depending on the stage of the project and kind of inquiry being considered, additional corporate members may be added to the project team to respond to issues such as IT, logistics, warehousing etc.Phase 1: Production Process VisualizationAt the beginning, the project team must be briefed thoroughly on the current corporate situation and on the accounting situation. To this end, the existing corporate accounting structure and the related corporate information transfer should be analyzed thoroughly. Following the concept of an input/output analysis, how materials find their ways into and out of the company is assessed. The next step is to present the flow of material and goods discovered and assessed in a flow model. To ensure the completeness and integrity of such a systematic analysis, any input and output is to be taken into consideration. Only a detailed analysis of material and energy flows from the point they enter the company until they leave it as products, waste, waste water or emissions enables the company to detect cost-saving potentials that at later stages of the project may involve more efficient material use, advanced process reliability and overview, improved capacity loads, reduced waste disposal costs, better transparency of costs and more reliable assessment of legal issues. As a first approach, simplified corporate flow models, standardizedstand-alone models for supplier(s), warehouse and isolated production segments were established and only combined after completion. With such standard elements and prototypes defined, a company can readily develop an integrated flow model with production process(es), production lines or a production process as a whole. From the view of later adoption of the existing corporate accounting to ECA, such visualization helps detect, determine, assess and then separate primary from secondary processes. Phase 2: Modification of AccountingIn addition to the visualization of material and energy flows, modeling principal and peripheral corporate processes helps prevent problems involving too high shares of overhead costs on the net product result. The flow model allows processes to be determined directly or at least partially identified as cost drivers. This allows identifying and separating repetitive processing activity with comparably few options from those with more likely ones for potential improvement.By focusing on principal issues of corporate cost priorities and on those costs that have been assessed and assigned to their causes least appropriately so far, corporate procedures such as preparing bids, setting up production machinery, ordering (raw) material and related process parameters such as order positions, setting up cycles of machinery, and order items can be defined accurately. Putting several partial processes with their isolated costs into context allows principal processes to emerge; these form the basis of process-oriented accounting. Ultimately, the cost drivers of the processes assessed are the actual reference points for assigning and accounting overhead costs. The percentage surcharges on costs such as labor costs are replaced by process parameters measuring efficiency (see Foster and Gupta, 1990).Some corporate processes such as management, controlling and personnel remain inadequately assessed with cost drivers assigned to product-related cost accounting. Therefore, costs of the processes mentioned, irrelevant to the measure of production activity, have to be assessed and surcharged with a conventional percentage.At manufacturing companies participating in the project,computer-integrated manufacturing systems allow a more flexible and scope-oriented production (eco-monies of scope), whereas before only homogenous quantities (of products) could be produced under reasonable economic conditions (economies of scale). ECA inevitably prevents effects of allocation, complexity and digression and becomes a valuable controlling instrument where classical/conventional accounting arrangements systematically fail to facilitate proper decisions. Thus, individually adopted process-based accounting produces potentially valuable information for any kind of decision about internal processing or external sourcing (e.g. make-or-buy decisions).Phase 3: Harmonization of Corporate Data – Compiling and Acquisition On the way to a transparent and systematic information system, it is convenient to check core corporate information systems of procurement and logistics, production planning, and waste disposal with reference to their capability to provide the necessary precise figures for the determined material/energy flow model and for previously identified principal and peripheral processes. During the course of the project, a few modifications within existing information systems were, in most cases, sufficient to comply with these requirements; otherwise, a completely new softwaremodule would have had to be installed without prior analysis to satisfy the data requirements.Phase 4: Database conceptsWithin the concept of a transparent accounting system, process-based accounting can provide comprehensive and systematic information both on corporate material/ energy flows and so-called overhead costs. To deliver reliable figures over time, it is essential to integrate a permanent integration of the algorithms discussed above into the corporate information system(s). Such permanent integration and its practical use may be achieved by applying one of three software solutions (see Figure 2).For small companies with specific production processes, an integrated concept is best suited, i.e. conventional andenvironmental/process-oriented accounting merge together in one common system solution.For medium-sized companies, with already existing integrated production/ accounting platforms, an interface solution to such a system might be suitable. ECA, then, is set up as an independent software module outside the existing corporate ERP system and needs to be fed data continuously. By using identical conventions for inventory-data definitions within the ECA software, misinterpretation of data can be avoided.Phase 5: Training and CoachingFor the permanent use of ECA, continuous training of employees on all matters discussed remains essential. To achieve a long-term potential of improved efficiency, the users of ECA applications and systems must be able to continuously detect and integrate corporate process modifications and changes in order to integrate them into ECA and, later, to process them properly.。

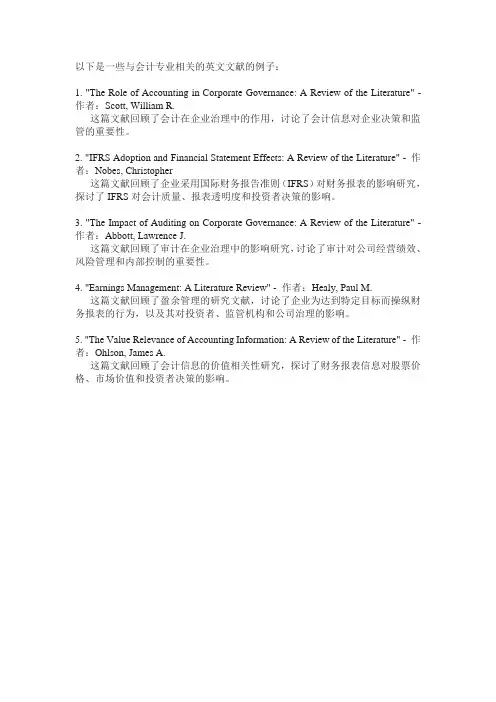

以下是一些与会计专业相关的英文文献的例子:1. "The Role of Accounting in Corporate Governance: A Review of the Literature" - 作者:Scott, William R.这篇文献回顾了会计在企业治理中的作用,讨论了会计信息对企业决策和监管的重要性。

2. "IFRS Adoption and Financial Statement Effects: A Review of the Literature" - 作者:Nobes, Christopher这篇文献回顾了企业采用国际财务报告准则(IFRS)对财务报表的影响研究,探讨了IFRS对会计质量、报表透明度和投资者决策的影响。

3. "The Impact of Auditing on Corporate Governance: A Review of the Literature" - 作者:Abbott, Lawrence J.这篇文献回顾了审计在企业治理中的影响研究,讨论了审计对公司经营绩效、风险管理和内部控制的重要性。

4. "Earnings Management: A Literature Review" - 作者:Healy, Paul M.这篇文献回顾了盈余管理的研究文献,讨论了企业为达到特定目标而操纵财务报表的行为,以及其对投资者、监管机构和公司治理的影响。

5. "The Value Relevance of Accounting Information: A Review of the Literature" - 作者:Ohlson, James A.这篇文献回顾了会计信息的价值相关性研究,探讨了财务报表信息对股票价格、市场价值和投资者决策的影响。

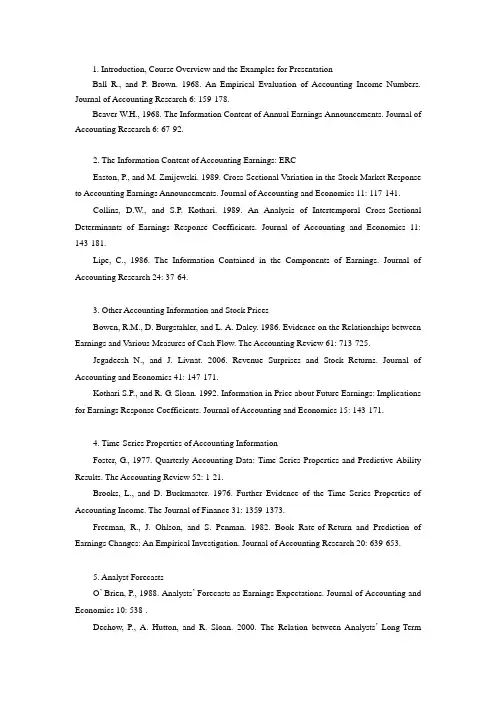

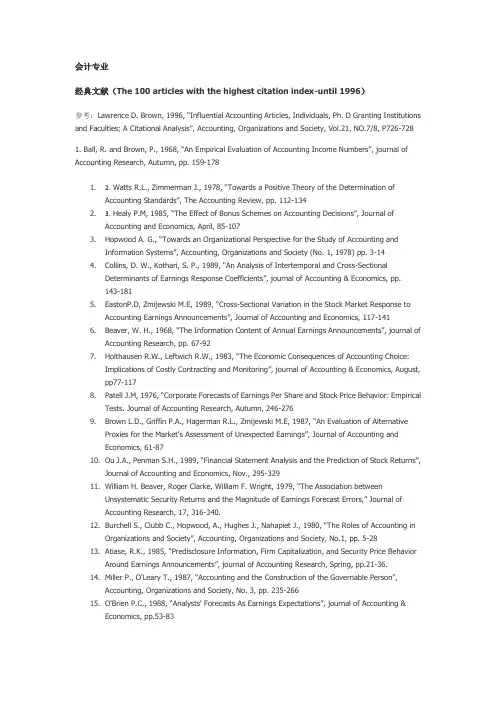

1. Introduction, Course Overview and the Examples for PresentationBall R., and P. Brown. 1968. An Empirical Evaluation of Accounting Income Numbers. Journal of Accounting Research 6: 159-178.Beaver W.H., 1968. The Information Content of Annual Earnings Announcements. Journal of Accounting Research 6: 67-92.2. The Information Content of Accounting Earnings: ERCEaston, P., and M. Zmijewski. 1989. Cross-Sectional Variation in the Stock Market Response to Accounting Earnings Announcements. Journal of Accounting and Economics 11: 117-141.Collins, D.W., and S.P. Kothari. 1989. An Analysis of Intertemporal Cross-Sectional Determinants of Earnings Response Coefficients. Journal of Accounting and Economics 11: 143-181.Lipe, C., 1986. The Information Contained in the Components of Earnings. Journal of Accounting Research 24: 37-64.3. Other Accounting Information and Stock PricesBowen, R.M., D. Burgstahler, and L. A. Daley. 1986. Evidence on the Relationships between Earnings and Various Measures of Cash Flow. The Accounting Review 61: 713-725.Jegadeesh N., and J. Livnat. 2006. Revenue Surprises and Stock Returns. Journal of Accounting and Economics 41: 147-171.Kothari S.P., and R. G. Sloan. 1992. Information in Price about Future Earnings: Implications for Earnings Response Coefficients. Journal of Accounting and Economics 15: 143-171.4. Time-Series Properties of Accounting InformationFoster, G., 1977. Quarterly Accounting Data: Time-Series Properties and Predictive-Ability Results. The Accounting Review 52: 1-21.Brooks, L., and D. Buckmaster. 1976. Further Evidence of the Time Series Properties of Accounting Income. The Journal of Finance 31: 1359-1373.Freeman, R., J. Ohlson, and S. Penman. 1982. Book Rate-of-Return and Prediction of Earnings Changes: An Empirical Investigation. Journal of Accounting Research 20: 639-653.5. Analyst ForecastsO’ Brien, P., 1988. Analysts’ Forecasts as Earnings Expectations. Journal of Accounting and Economics 10: 538-.Dechow, P., A. Hutton, and R. Sloan. 2000. The Relation between Analysts’Long-TermEarnings Forecasts and Stock Price Performance Following Equity Offering. Contemporary Accounting Research 17: 1-32.Irvine, P.J. 2004. Analysts’ Forecasts and Brokerage-Firm Trading. The Accounting Review 79: 125-149.6. Earning Management: Part IBurgstahler, D., and I.D.Dichev. 1997. Earnings Management to Avoid Earnings Decreases and Losses. Journal of Accounting and Economics 24: 99-126.Matsumoto, D. 2002. Management’s Incentives to Avoid Negative Earning Surprises. The Accounting Review 77: 483-514.Jones, J. 1991. Earnings Management during Import Relief Investigations. Journal of Accounting Research 29: 193-228.7. Earning Management: Part IIDeFond, M.L., and J. Jiambalvo. 1994. Debt Covenant Violation and Manipulation of Accruals. Journal of Accounting and Economics 17: 145-176.Gramlich, J.D., M.L. McAnally, and J. Thomas. 2001. Balance Sheet Management: The Case of Short-Term Obligations Reclassified ad Long-Term Debt. Journal of Accounting Research 39: 283-295.Daniel, N.D., D.J. Denis, and L. Naveen. 2008. Do Firms Manage Earnings to Meet Dividend Thresholds? Journal of Accounting and Economics 45: 2-26.8. Management Disclosures and Disclosure QualityBotosan, C., 1997. Disclosure Level and the Cost of Equity Capital. The Accounting Review 72: 323-349.Skinner, D. 1994. Why Do Firms V oluntarily Disclose Bad News? Journal of Accounting Research 32: 38-60.Lang M.H., and R.J. Lundholm. 1996. Corporate Disclosure Policy and Analyst Behavior. The Accounting Review 71: 467-492.9. Financial Accounting: an International View(3学时)Ball, R., S.P. Kothari, and A. Robin. 2000. The Effect of International Institutional Factors on Properties of Accounting Earnings. Journal of Accounting and Economics 29: 1-51.Morck, R., B. Yeung, and W. Yu. 2000. The information Content of Stock Markets: Why DoEmerging Markets Have Synchronous Stock Price Movements? Journal of Financial Economics 58: 215-260.Lang, M., J.S. Ready, and M.H. Yetman. 2003. How Representative Are Firms that Are Cross-Listed in the United States? An Analysis of Accounting Quality. Journal of Accounting Research 41: 363-386.参考书目[加]威廉姆·司可脱著,陈汉文译,《财务会计理论》,机械工业出版社。

附件9:XXX科技学院学生毕业设计(论文)外文译文院(系)专业班级学生姓名XXX学号XXX文章来源:玛利亚卡门惠安库扎大学,亚历山大雅西,罗马尼亚金融危机下的公允价值会计摘要:2008年9月的金融风暴直击美国经济核心,并且迅速蔓延到世界各地,引发了对使用外来衍生金融工具和公允价值会计的激烈辩论。

或多或少受此次危机影响的银行﹑保险管理人员,审计师和政界人士就这一主题多次在新闻头版发表不同意见,本文的目的是审查金融市场的现状,使我们了解到公允价值会计及衍生品在预防这些巨大的丑闻时的重要性,制定准则。

同时阐述支持或反对使用公允价值和信用衍生产品的意见并提出应对未来金融危机的解决办法。

关键词:次贷危机金融衍生产品公允价值一、引言安然危机震撼了美国经济的核心。

监管机构在2000年初发行规则,以方便投资者了解公司资产的价值,并减少(至少部分减少)结构性融资的复杂性。

当时,一个最佳的解决方案似乎是合理价值会计,它旨在披露更具相关性和有价值的报告。

监管机构认为,鼓励公平价值的透明度和可比性,将有助于恢复投资者对金融市场及其机构的信任。

安然事件之后,美国的标准制定者-财务会计标准委员会( FASB )已行使任务,发出的公允价值测量标准(联邦反垄断局第157条)。

根据这一标准,资产必须属于这三类之一,如何分类取决于其相对流动性:1级,包括最流动资产,其价值源于在活跃市场的价格;2级,包括使用可观察市场的市场数据;3级,包括最难计量的资产的公允价值计量不可观察,只有通过以内部模式和估算为基础的价格。

正是这个第三级别提高了在没有市场参考价时有关强制使用市场价值为交易或金融资产/负债的计价模式。

关于公允价值会计的争论再度引发了新闻界把责任归咎于彻底崩溃的住房抵押贷款证券的市场和住房信贷市场1由于缺乏市场流动性产生了上述银行家,责任再次放在公允价值会计,但奇怪的1因为没有流动性的市场,这里第三级最具争议,它有关强制使用以市场价值为交易、金融资产或负债。

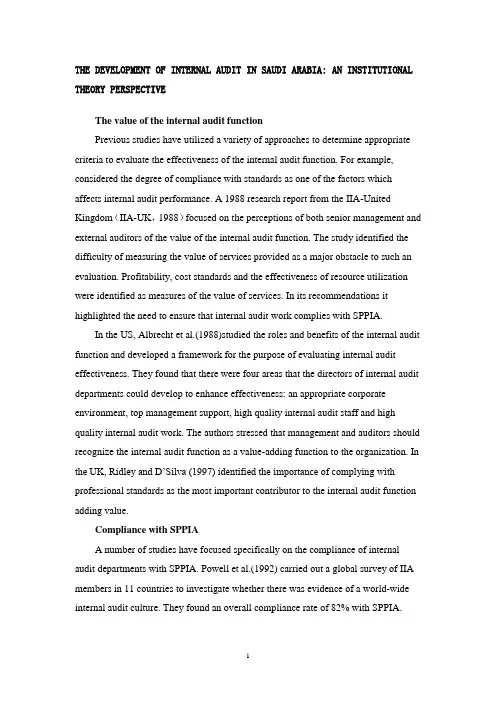

THE DEVELOPMENT OF INTERNAL AUDIT IN SAUDI ARABIA: AN INSTITUTIONAL THEORY PERSPECTIVEThe value of the internal audit functionPrevious studies have utilized a variety of approaches to determine appropriate criteria to evaluate the effectiveness of the internal audit function. For example, considered the degree of compliance with standards as one of the factors which affects internal audit performance. A 1988 research report from the IIA-United Kingdom(IIA-UK,1988)focused on the perceptions of both senior management and external auditors of the value of the internal audit function. The study identified the difficulty of measuring the value of services provided as a major obstacle to such an evaluation. Profitability, cost standards and the effectiveness of resource utilization were identified as measures of the value of services. In its recommendations it highlighted the need to ensure that internal audit work complies with SPPIA.In the US, Albrecht et al.(1988)studied the roles and benefits of the internal audit function and developed a framework for the purpose of evaluating internal audit effectiveness. They found that there were four areas that the directors of internal audit departments could develop to enhance effectiveness: an appropriate corporate environment, top management support, high quality internal audit staff and high quality internal audit work. The authors stressed that management and auditors should recognize the internal audit function as a value-adding function to the organization. In the UK, Ridley and D’Silva (1997) identified the importance of complying with professional standards as the most important contributor to the internal audit function adding value.Compliance with SPPIAA number of studies have focused specifically on the compliance of internal audit departments with SPPIA. Powell et al.(1992) carried out a global survey of IIA members in 11 countries to investigate whether there was evidence of a world-wide internal audit culture. They found an overall compliance rate of 82% with SPPIA.This high percentage prompted the authors to suggest that SPPIA provided evidence of the internationalization of the internal audit profession.A number of studies have focused on the SPPIA standard concerned with independence.Clark et al.(1981) found that the independence of the internal audit department and the level of authority to which internal audit staff report were the two most important criteria influencing the objectivity of their work. Plumlee (1985) focused on potential threats to internal auditor objectivity, particularly whether participation in the design of an internal control system influenced judgements as to the quality and effectiveness of that system. Plumlee found that such design involvement produced bias that could ultimately threaten objectivity.The relationship between the internal audit function and company management more generally is clearly an important factor in determining internal auditor objectivity. Harrell et al. (1989) suggested that perceptions of the views and desires of management could influence the activities and judgement of internal auditors. Also, they found that internal auditors who were members of the IIA were less likely to succumb to such pressure.Ponemon (1991) examined the question of whether or not internal auditors will report sensitive issues uncovered during the course of their work. He concluded that the three factors affecting internal auditor objectivity were their social position in the organization, their relationship with management and the existence of a communication channel to report wrongdoing.Internal audit research in Saudi ArabiaTo date there has been relatively little research about internal audit in the Saudi Arabian corporate sector, exceptions, however, are Asairy (1993)and Woodworth and Said (1996). Asairy (1993)sought to evaluate the effectiveness of internal audit departments in Saudi joint-stock companies. He studied departments in 38 companies using questionnaire responses from the directors of internal audit departments, senior company management, and external auditors. The result of this study revealed that one significant factor in the perceived success of internal audit was its independence from other corporate activities. The service provided by the internal audit department was affected by the support it received from the management, other employees andexternal auditors. The education, training, experience and professional qualifications of the internal auditors influenced the effectiveness of internal audit. On the basis of his study, Asairy (1993) recommended that all joint-stock companies, should have an internal audit function, and that internal auditing should be taught as a separate course in Saudi Universities.Woodworth and Said (1996)sought to ascertain the views of internal auditors in Saudi Arabia as to whether there were differences in the reaction of auditees to specific internal audit situations according to the nationality of the auditee. Based on 34 questionnaire responses from members of the IIA Dhahran chapter, they found there were no significant differences between the different nationalities. The internal auditors did not modify their audit conduct according to the nationality of the auditee and cultural dimensions did not have a significant impact on the results of the audit.Given the importance of complying with SPPIA, the professional and academic literature emphasizes the importance of the relationship between the internal audit department and the rest of the organization in determining the success or otherwise of internal audit departments (Mints,1972;Flesher,1996;Ridley & Chambers,1998 and Moeller & Witt,1999). This literature focuses on the need for co-operation and teamwork between the auditor and auditee if internal auditing is to be effective.Bethea (1992) suggests that the need for good human relations’ skills is important because internal auditing creates negative perceptions and negative attitudes. These issues are particularly important in a multicultural business environment such as Saudi Arabia where there are significant differences in the cultural and educational background of the auditors and auditees Woodworth and Said (1996).ResultsReasons for not having an internal audit departmentOf the 92 company interviews examining the reasons why companies do not have an internal audit function, the most frequent response from 52 companies (57%) was that reliance on the external auditor enabled the company to obtain the benefits that might be obtained from internal audit. Typically, interviewees argued that the external auditor is better, more efficient and saves money. Interviews with theexternal auditors revealed that client companies could not distinguish clearly between the work and roles of internal and external audit. For example, one external auditor said,there is a misperception of what the external auditor does, they think the external auditor does everything for the company and must discover any problem.Having said this, one external auditor doubted that an internal audit function would add value in all circumstances. When referring to the internal control system he stated,as long as they are happy with the final output, I think the internal audit function will not add value. External auditing eventually will highlight any significant internal control weakness.The second most frequent reason mentioned by interviewees (23 firms, 25%) for not operating an internal audit department was the cost/benefit trade-off. Specifically, 17 firms considered that the small size of the company and the limited nature of its activities meant that it would not be efficient for them to have an internal audit department. The external auditors interviewed were of the opinion that the readily identifiable costs as compared with the more difficult to measure benefits was a factor contributing to this decision.A number of other reasons were given by interviewees for not having an internal audit department. As a consequence of the high costs of conducting internal audit activities, 14 firms used employees who were not within a separate internal audit department to carry out internal audit duties. Eight companies did not think there was a need for internal audit because they believed their internal control systems were sufficient to obviate the need for internal audit. Five companies did not think that internal audit was an important activity and three felt that their type of the business did not require internal audit. Three respondents mentioned that they did not operate an internal audit department because professional people could not be found to run the department, and six companies did not provide a reason for not having an internal audit department. In 10 companies an internal audit department had been established but was no longer operating because of difficulties in recruiting qualified personneland changes in the organization structure. Having said this, eight companies without an internal audit department were planning to establish one in the future.The independence of internal audit departmentsCommentators and standard setters identify independence as being a key attribute of the internal audit department. From the questionnaire responses 60 (77%) of the internal audit departments stated that there was a written document defining the purpose, authority and responsibility of the department. In nearly all instances where there was such a document the terms of reference of the internal audit department had been agreed by senior management (93%), the document identified the role of the internal audit department in the organization, and its rights of access to individuals, records and assets (97%), and the document set out the scope of internal auditing (90%). Respondents were asked to assess the extent to which the relevant document was consistent with the specific requirements of SPPIA. In those departments where such a document existed 27 (45%) claimed full compliance with SPPIA, 23 (38%) considered their document to be partially consistent with SPPIA. In more thanone-third of the departments surveyed either no such document existed (n=18, 23%) or the respondent was not aware whether or not the document complied with SPPIA (n=10, 13%).SPPIA suggests that independence is enhanced when t he organization’s board of directors concurs with the appointment or removal of the director of the internal audit department, and that the director of the internal audit department is responsible to an individual of suitable seniority within the organization. It is noticeable that in 47 companies (60%) their responsibilities with regard to appointment, removal and the receipt of reports lay with non-senior management, normally a general manager. SPPIA recommends that the director of the internal audit department should have direct communication with the board of directors to ensure that the department is independent, and provides a means for the director of internal auditing and the board of directors to keep each other informed on issues of mutual interest. The interviews with directors of internal audit departments showed that departments tended to report to general managers rather than the board of directors. Further evidence of the lack ofaccess to the board of directors was provided by the questionnaire responses showing that in almost half the companies, members of the internal audit department have never attended board meetings and in only two companies did attendance take place regularly.Unrestricted access to documentation and unfettered powers of enquiry are important aspects of the independence and effectiveness of internal audit. The questionnaire responses revealed that 34 (44%) internal audit directors considered that they did not have full access to all necessary information. Furthermore, a significant minority (n=11, 14%) did not believe they were free, in all instances, to report faults, frauds, wrongdoing or mistakes. A slightly higher number (n=17, 22%) considered that the internal audit function did not always receive consistent support from senior management.SPPIA identifies that involvement in the design, installation and operating of systems is likely to impair internal auditor objectivity. Respondents were asked how often management requested the assistance of the internal audit department in the performance of non-audit duties. In 37 internal audit departments (47%) surveyed such requests were made sometimes, often or always, and only 27 (35%) departments never participated in these non-audit activities. The interviews revealed that in some organizations internal audit staff was used regularly to cover for staff shortages in other departments.。

原文题目:《评述教育会计专业》作者:迈克尔卡夫金原文出处:School of Accounting and Finance, University of Wollongong,Wollongong, Australia会计教育会计教育。

一般来说,从业者似乎已不愿想改变- 要离开自己的舒适区- 慢,并已承认在与伦理,环境恶化,全球化相关的地区更广泛的社会问题所提出的问题,增加业务的复杂性和其他一些因素我写我的一些挫折(卡夫金,1981 年)和左新西兰追求我在澳大利亚的学习和职业生涯。

我后来成为澳大利亚的主要会计机构教育委员会主席。

在这种角色我曾与新西兰身体的教育委员会的领导组织,并得到非常积极的态度,他们与澳大利亚的机构都对促进更“圆”大学会计教育方案(其中大部分出自从业者,学者的鼓励!)。

最近在新西兰旅行,我一直很失望,观察什么似乎是一个这样做的目的完全逆转; 重点放在,由新西兰的专业团体,纯粹的技术能力,他们迫使大学遵守这一点- 复仇的bean 柜台?什么也令人失望对我来说是由学术带头人的决心明显缺乏,使专业团体的“决定” 什么通行证作为会计教育法规,如会计死记硬背。

我观察到有什么事我当作一个高级学者讨好自己的专业机构,而不是促进学科发展,将在二十一世纪更广泛的社会需要的知识要点。

因此,我的评论是针对试图界定什么是专业会计师- 毫无疑问,很多人可能不同意。

我的目的是展示合作的重要性,而不是怀疑和无知的需要和应具有什么样的会计专业的各个部分努力。

我并不想冒犯各位同事,而是试图提供一个什么样的我的看法是会计面临的问题和强调纪律,前进的方向,通过所有这些谁认为,在解决方案协助资讯科技合作是批判极大的社会问题。

从业人员有一个会计的执业类别广泛的业余爱好,所以任何评论,我所做的非常广泛的推广。

传统上,从业者已被注册会计师,会计师或公共部门私营会计师,但随着业务的日益复杂和商业机构在最近的时代,这些分类的界线变得越来越模糊。

The Impact of Cash Budgets on Poverty Reduction in Zambia: A Case Study of the Conflict between Well-Intentioned Macroeconomic Policy and Service Delivery to the Poor Hinh T. Dinh World Bank Abebe Adugna World Bank C. Bernard Myers World Bank October 2002 World Bank Policy Research Working Paper No. 2914 Abstract: Facing runaway inflation and budget discipline problems in the early 1990s, the Zambian government introduced the so-called cash budget in which government domestic spending is limited to domestic revenue, leaving no room for excess spending. Dinh, Adugna, and Myers review Zambia's experience during the past decade, focusing on the impact of the cash budget on poverty reduction. They conclude that after some initial success in reducing hyperinflation, the cash budget has largely failed to keep inflation at low levels, created a false sense of fiscal security, and distracted policymakers from addressing the fundamental issue of fiscal discipline. More important, it has had a deeply pernicious effect on the quality of service delivery to the poor. Features inherent to the cash budgeting system facilitated a substantial redirection of resources away from the intended targets, such as agencies and ministries that provide social and economic services. The cash budget also eliminated the predictability of cash releases, making effective planning by line ministries difficult. Going forward, Zambia must adopt measures that over time will restore the commitment to budget discipline and shelter budget execution decisions from the pressures of purely short-term exigencies. This paper - a product of the Poverty Reduction and Economic Management Division 1, Africa Region - is part of a larger effort in the region to review public expenditure management. Number of Pages in PDF File: 34 working papers series Download This PaperDecember 21, 2004Date posted: D ecember 21, 20042 Principles of Cash Management from IndianManagement Thought: ThirukkuralChendrayan ChendroyaperumalAnna University of Technology Chennai - Saveetha Engineering College; Deceased June 9, 2008Abstract: Wise management of cash is essential for the survival and success of any business organization. Textbooks prescribe a set of principles for successful management of cash, a key component of working capital but the least productive for the firm holding it. This paper attempts to highlight the principles of cash management propounded in Thirukkural - an Indian work on management written more than 2000 years ago but very relevant, practicable and consistent with that of the modern thought!Number of Pages in PDF File: 6Keywords: Cash Management, Working Capital, Financial Management, ThirukkuralJEL Classification: G11, G15, G31working papers series3 Management Accounting Systems Adoption Decisions:Evidence and Performance Implications from StartupCompaniesTony DavilaUniversity of Navarra - IESE Business School George FosterStanford Graduate School of Business October 2004Stanford GSB Research Paper No. 1874 Abstract: Adopting management accounting systems are important events in the life of young and growing companies. Using a sample of 78 startup companies, we document cross-sectional differences in the adoption of operating budgets as well as seven other management accounting systems. We find that our proxies for agency costs, perceived benefits and costs, complexity of the firm, and culture explain cross-sectional differences in time-to-adoption of budgets. In particular, the presence of venture capital, CEO experience, firm size, and the culture of the organization are associated with this adoption decision. We further investigate the effect of hiring a financial manager as an endogenous variable. In the first stage of a two-stage model, we find that CEO total experience, the presence of venture capital funds, culture, and firm size are associated with cross-sectional variation in this hiring decision. When treating this decision as endogenous, time to hiring a financial manager is unrelated to operating budget adoption. The paper also examines the association between the time-to-adoption of operating budgets and company performance. We find a significant increase in the size of the company around the adoption of operating budgets; moreover faster adoption of operating budgets is associated with faster growing companies. We extend the findings to additional management accounting systems including: cash budgets, variance analysis, operating expense approval policies, capital expenditure approval policies, product profitability, customer profitability, and customer acquisition costs. The influence of industry choice (biotechnology, information technology, or non-tech) is examined in each stage of the research.Number of Pages in PDF File: 47Keywords: Management accountingJEL Classification: G34, G31, M40, M46working papers series 。