Advanced Accounting, 11e (Beams/Anthony/Bettinghaus/Smith)

Chapter 8 Consolidations - Changes in Ownership Interests

Multiple Choice Questions

1) Which of the following is correct? The direct sale of additional shares of stock at book value per share to only the parent company from a subsidiary

A) decreases the parent's interest and decreases the noncontrolling shareholders' interest.

B) decreases the parent's interest and increases the noncontrolling shareholders' interest.

C) increases the parent's interest and increases the noncontrolling shareholders' interest.

D) increases the parent's interest and decreases the noncontrolling shareholders' interest.

Answer: D

Objective: LO3

Difficulty: Moderate

Use the following information to answer the question(s) below.

On December 31, 2010, Giant Corporation's Investment in Penguin Corporation account had a balance of $500,000. The balance consisted of 80% of Penguin's $625,000 stockholders' equity on that date. Giant owns 80% of Penguin. On January 2, 2011, Penguin increased its outstanding common stock from 15,000 to 18,000 shares.

2) Assume that Penguin sold the additional 3,000 shares directly to Giant for $150,000 on January 2, 2011. Giant's percentage ownership in Penguin immediately after the purchase of the additional stock is

A) 66-2/3%.

B) 80%.

C) 83-1/3%.

D) 86-2/3%

Answer: C

Explanation: C) (Parent had 80% of 15,000 shares, or 12,000 shares. They now hold 15,000 of 18,000 shares) = 83.33%

Objective: LO3

Difficulty: Moderate

3) Assume that Penguin sold the additional 3,000 shares to outside interests for $150,000 on January 2, 2011. Giant's percentage ownership immediately after the sale of additional stock would be

A) 66-2/3%.

B) 75%.

C) 80%.

D) 83-1/3%.

Answer: A

Explanation: A) (12,000 shares/18,000 shares) = 66.67%

Objective: LO3

Difficulty: Moderate

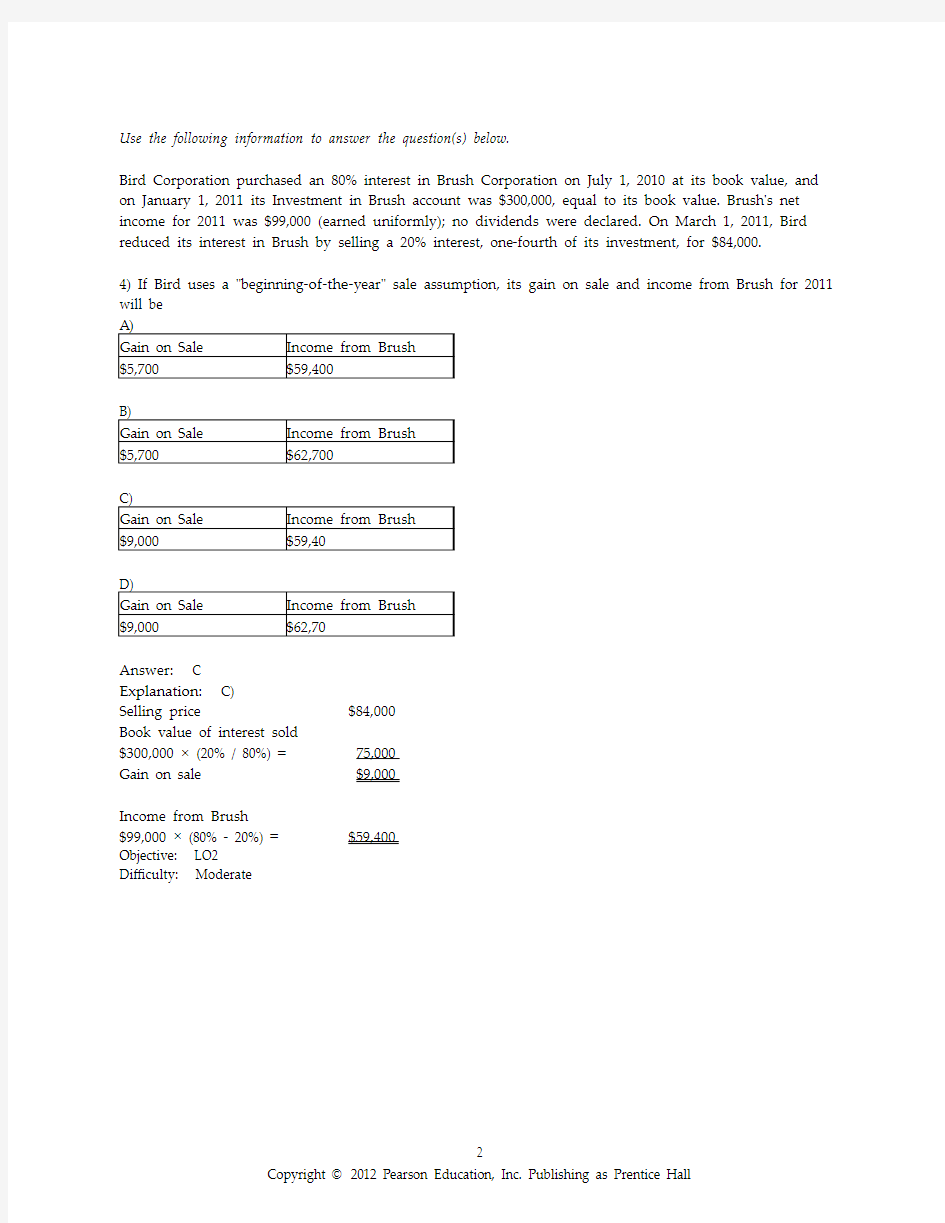

Use the following information to answer the question(s) below.

Bird Corporation purchased an 80% interest in Brush Corporation on July 1, 2010 at its book value, and on January 1, 2011 its Investment in Brush account was $300,000, equal to its book value. Brush's net income for 2011 was $99,000 (earned uniformly); no dividends were declared. On March 1, 2011, Bird reduced its interest in Brush by selling a 20% interest, one-fourth of its investment, for $84,000.

4) If Bird uses a "beginning-of-the-year" sale assumption, its gain on sale and income from Brush for 2011 will be

Answer: C

Explanation: C)

Selling price $84,000

Book value of interest sold

$300,000 × (20% / 80%) =75,000

Gain on sale $9,000

Income from Brush

$99,000 × (80% - 20%) =$59,400

Objective: LO2

Difficulty: Moderate

5) If Bird uses the "actual-sale-date" sales assumption, its gain on the sale and income from Brush for 2011 will be

Answer: B

Explanation: B)

Selling price $84,000

Book value of interest sold:

Beginning balance $300,000

Income for 2 months

$99,000 x 1/6 × 80% =13,200

Adjusted book value 313,200

Percentage of interest sold 1/4

Book value applied 78,300 78,300

Gain on sale $5,700

Income from Brush:

Jan 1 - Mar 1 $99,000 × 2/12 × 80% =$13,200

Mar 1 - Dec 31 $99,000 × 10/12 × 60% =49,500

Income from Brush $62,700

Objective: LO2

Difficulty: Moderate

6) Jersey Company acquired 90% of York Company on April 1, 2011. Both Jersey Company and York Company have December 31 fiscal year ends. Under current GAAP, which of the following statements is false?

A) The consolidated income statement in 2011 should not include York's revenues and expenses prior to April 1, 2011.

B) When preparing consolidating work papers in 2011, York's revenues prior to April 1, 2011 are eliminated.

C) York's earnings prior to April 1, 2011 should appear as a deduction on the consolidated income statement in 2011.

D) The consolidated income statement in 2011 should include York's revenues and expenses after April 1, 2011.

Answer: C

Objective: LO1

Difficulty: Moderate

7) Utah Company holds 80% of the stock of a subsidiary company. The subsidiary issues 100 additional shares of stock to Utah Company at a price above book value per share. The subsidiary does not issue any additional shares at the same time. How will Utah Company record the purchase?

A) Utah Company records a gain on sale of stock.

B) Utah Company increases additional paid-in capital.

C) Utah Company decreases additional paid-in capital.

D) Utah Company assigns any excess cost over book value acquired to increase undervalued identifiable assets or goodwill as appropriate.

Answer: D

Objective: LO3

Difficulty: Moderate

Use the following information to answer the question(s) below.

Goldberg Corporation owned a 70% interest in Savannah Corporation on December 31, 2010, and Goldberg's Investment in Savannah account had a balance of $3,900,000. Savannah's stockholders' equity on this date was as follows:

Capital stock, $10 par value $3,000,000

Retained Earnings 2,400,000

Total Stockholders' Equity $5,400,000

On January 1, 2011, Savannah issues 80,000 new shares of common stock to Goldberg for $16 each.

8) What is Goldberg's percentage ownership in Savannah after Savannah issues its stock to Goldberg?

A) 76.32%

B) 80.43%

C) 82.57%

D) 83.43%

Answer: A

Explanation: A) (210,000 + 80,000)/380,000

Objective: LO3

Difficulty: Moderate

9) On January 1, 2011, assume the fair values of Savannah's identifiable assets and liabilities equal book values. What is the change in the amount of goodwill associated with the issuance of 80,000 additional shares to Goldberg? (Use four decimal places.)

A) Increase goodwill $38,176.

B) Decrease goodwill $38,176.

C) Increase goodwill $384,000.

D) Decrease goodwill $384,000.

Answer: B

Explanation: B)

Savannah's equity after the issuance of

the new shares ($5,400,000 + $1,280,000) $6,680,000

Goldberg's ownership percentage 76.32%

Goldberg's share of Savannah's equity now $5,098,176

Goldberg's previous share of Savannah's equity ($5,400,000 × 70%) 3,780,000

Savannah's equity acquired in the purchase $1,318,176

Amount spent to acquire stock 1,280,000

Excess book value acquired over cost $ 38,176

Objective: LO3

Difficulty: Difficult

Use the following information to answer the question(s) below.

Great Corporation acquired a 90% interest in SOS Corporation at its $810,000 book value on December 31, 2010. A summary of the stockholders' equity for SOS at the end of 2010 and 2011 is as follows:

12/31/10 12/31/11

Capital stock, $10 par $600,000 $600,000

Additional paid-in capital 30,000 30,000

Retained Earnings 270,000 420,000

Total stockholders' equity $900,000 $1,050,000

On January 1, 2012, SOS sold 10,000 new shares of its $10 par value common stock for $45 per share. 10) If SOS sold the additional shares to the general public, Great's Investment in SOS account after the sale would be ________. (Use four decimal places.)

A) $945,000

B) $1,157,100

C) $1,225,000

D) $1,245,000

Answer: B

Explanation: B)

SOS's stockholders' equity prior to the stock issuance $1,050,000

Plus: Capital received from new stock issued 450,000

New stockholders' equity $1,500,000

Great's ownership (54,000/(60,000 + 10,000)) 77.14%

Great's adjusted investment in SOS $1,157,100

Objective: LO3

Difficulty: Moderate

11) If SOS sold the additional shares directly to Great, Great's Investment in SOS account after the sale would be

A) $1,350,000.

B) $1,395,000.

C) $1,425,000.

D) $1,500,000.

Answer: B

Explanation: B)

Investment balance at 12/31/2011

($1,050,000 × 90%) $945,000

Additional investment (10,000 shares × $45) 450,000

Investment account balance, 12/31/2011 $1,395,000

Objective: LO3

Difficulty: Moderate

12) Consider a sale of stock by a subsidiary to parties outside the consolidated entity. This transaction requires an adjustment of the parent's investment and additional paid-in capital accounts except when

A) the shares are sold below book value per share.

B) the shares are sold above book value per share.

C) the shares are sold at book value per share.

D) All of the above are correct.

Answer: C

Objective: LO3

Difficulty: Moderate

13) If a parent company and outside investors purchase shares of a subsidiary in relation to existing stock ownership (ratably), then

A) there will be an adjustment to additional paid-in capital if the stock is sold above book value.

B) there will be no adjustment to additional paid-in capital regardless whether the stock is sold above or below book value.

C) there will be an adjustment to additional paid-in capital if the stock is sold below book value.

D) there will be the elimination of a gain.

Answer: B

Objective: LO3

Difficulty: Easy

14) A subsidiary split its stock 2 for 1. Which of the following statements is false?

A) A stock split does not affect the amount of net assets of the subsidiary.

B) A stock split does not affect parent and noncontrolling interest ownership percentages.

C) A stock split does not affect consolidation procedures.

D) A 2 for 1 stock split decreases the number of shares outstanding.

Answer: D

Objective: LO3

Difficulty: Moderate

Use the following information to answer the question(s) below.

Bower Corporation purchased a 70% interest in Stage Corporation on June 1, 2010 at a purchase price of $350,000. On June 1, 2010, the book values of Stage's assets and liabilities were equal to fair values. On June 1, 2010, Stage's stockholders' equity consisted of $290,000 of Common Stock and $210,000 of Retained Earnings. All cost-book differentials were attributed to goodwill.

During 2010, Stage earned $120,000 of net income, earned uniformly throughout the year and paid $6,000 of dividends on March 1 and another $6,000 on September 1.

15) Noncontrolling interest share for 2010 is

A) $21,000.

B) $32,400.

C) $36,000.

D) $50,000.

Answer: A

Explanation: A) ($120,000 × 7/12 × 30%)

Objective: LO2

Difficulty: Moderate

16) Preacquisition income for 2010 is

A) $50,000.

B) $35,000.

C) $44,000.

D) $36,000.

Answer: A

Explanation: A) ($120,000 × 5/12)

Objective: LO2

Difficulty: Moderate

17) Anthony Company declared and paid $20,000 of dividends during 2011. The schedule of dividends follows:

Date Dividend Declared & Paid Amount Paid

March 31, 2011 $5,000

June 30, 2011 $5,000

September 30, 2011 $5,000

December 31, 2011 $5,000

Anthony Company was acquired on June 1, 2011 by Google Company. Google acquired 100 percent of Anthony Company. Both companies have a December 31 fiscal year end. What is the amount of preacquisition dividends in 2011?

A) 0

B) $5,000

C) $10,000

D) $15,000

Answer: B

Objective: LO1

Difficulty: Moderate

18) On April 1, 2011, Paramount Company acquires 100% of the outstanding stock of Yester Company on the open market. Paramount and Yester have December 31 fiscal year ends. Under GAAP, a consolidated income statement for the year ending December 31, 2011, will include

A) 100 percent of the revenues and expenses in 2011 of Yester Company after January 1, 2011.

B) no revenues and expenses in 2011 of Yester Company.

C) 80 percent of the revenues and expenses in 2011 of Yester Company.

D) 100 percent of the revenues and expenses in 2011 of Yester Company after April 1, 2011.

Answer: D

Objective: LO1

Difficulty: Moderate

19) The acquisition of treasury stock by a subsidiary from noncontrolling shareholders at a price above book value

A) decreases the parent's share of subsidiary book value and decreases the parent's ownership percentage.

B) decreases the parent's share of subsidiary book value and increases the parent's ownership percentage.

C) increases the parent's share of subsidiary book value and decreases the parent's ownership percentage.

D) increases the parent's share of subsidiary book value and increases the parent's ownership percentage. Answer: B

Objective: LO3

Difficulty: Moderate

20) A 15% stock dividend by a subsidiary causes

A) the parent company investment account to decrease.

B) the parent company investment account to remain the same.

C) the parent company investment account to increase.

D) the noncontrolling interest equity to increase.

Answer: B

Objective: LO3

Difficulty: Moderate

Exercises

1) At December 31, 2010, the stockholders' equity of Gost Corporation and its 80%-owned subsidiary, Tree Corporation, are as follows:

Gost Tree

Common stock, $10 par value $20,000 $12,000

Retained earnings 8,000 6,000

Totals $28,000 $18,000

Gost's Investment in Tree is equal to 80 percent of Tree's book value. Tree Corporation issued 225 additional shares of common stock directly to Gost on January 1, 2011 at $18 per share.

Required:

1. Compute the balance in Gost's Investment in Tree account on January 1, 2011 after the new investment is recorded.

2. Determine the increase or decrease in goodwill from Gost's new investment in the 225 Tree shares. Use four decimal places for the ownership percentage. Assume the fair values of Tree's assets and liabilities are equal to book values.

Answer:

Requirement 1

Cost of investment ($18,000 × 80%) $14,400

Plus: Purchase of 225 Tree shares at $18 on January 1, 2011 4,050

Investment account balance $18,450

Requirement 2

Tree's stockholders' equity at January 1, 2011 $18,000

Plus: Additional capital from the shares issued 4,050

Total stockholders' equity after issuance of the new shares $22,050

Gost's percentage

(960 + 225)/1425 =0.8316

Gost's share of Tree's equity after issuance $18,337

Gost's share of Tree's equity before stock issuance 14,400

Equity acquired in the purchase 3,937

Cost of interest acquired 4,050

Increase goodwill $ 113

Objective: LO3

Difficulty: Moderate

Goldberg Corporation, are as follows:

Godwin Goldberg

Common stock, $10 par value $20,000 $12,000

Retained earnings 8,000 6,000

Totals $28,000 $18,000

Godwin's Investment in Goldberg is equal to 80 percent of Goldberg's book value. Goldberg Corporation issued 225 additional shares of common stock directly to Godwin on January 1, 2011 at $28 per share. Required:

1. Compute the balance in Godwin's Investment in Goldberg account on January 1, 2011 after the new investment is recorded.

2. Determine the increase or decrease in goodwill from Godwin's new investment in the 225 Goldberg shares. Use four decimal places for the ownership percentage. Assume the fair value and book value of Goldberg's assets and liabilities are equal.

Answer:

Requirement 1

Cost of investment ($18,000 × 80%) $14,400

Plus: Purchase of 225 Goldberg shares at $28 on January 1, 2011 6,300

Investment account balance $20,700

Requirement 2

Goldberg's stockholders' equity at January 1, 2011 $18,000

Plus: Additional capital from the shares issued 6,300

Total stockholders' equity after issuance of the new shares $24,300

Godwin's percentage

(960 + 225)/1425 =0.8316

Godwin's share of Goldberg's equity after issuance $20,208

Godwin's share of Goldberg's equity before stock issuance 14,400

Equity acquired in the purchase 5,808

Cost of interest acquired 6,300

Increase in goodwill $ 492

Objective: LO3

Difficulty: Moderate

Trompeter Corporation, are as follows:

Pearson Trompeter

Common stock, $10 par value $20,000 $12,000

Retained earnings 8,000 6,000

Totals $28,000 $18,000

Pearson's Investment in Trompeter is equal to 80 percent of Trompeter's book value. Trompeter Corporation issued 400 additional shares of common stock directly to Pearson on January 1, 2011 at $10 per share.

Required:

1. Compute the balance in Pearson's Investment in Trompeter account on January 1, 2011 after the new investment is recorded.

2. Determine the increase or decrease in goodwill from Pearson's new investment in the 400 Trompeter shares. Use four decimal places for the ownership percentage. Assume the fair value and book value of Trompeter's assets and liabilities are equal.

Answer:

Requirement 1

Cost of investment ($18,000 × 80%) $14,400

Plus: Purchase of 400 Trompeter shares at $10 on January 1, 2011 4,000

Investment account balance $18,400

Requirement 2

Trompeter's stockholders' equity at January 1, 2011 $18,000

Plus: Additional capital from the shares issued 4,000

Total stockholders' equity after issuance of the new shares $22,000

Pearson's percentage

(960 + 400)/1600 =0.85

Pearson's share of Trompeter's equity after issuance $18,700

Pearson's share of Trompeter's equity before stock issuance 14,400

Equity acquired in the purchase 4,300

Cost of interest acquired 4,000

Reduce goodwill or identifiable assets (Since no goodwill is

associated with the investment, should reduce overvalued

identifiable assets.) $ 300

Objective: LO3

Difficulty: Moderate

account balance was $900,000. On January 1, 2010, Twig's total stockholders' equity was $1,125,000.

During 2010, Twig uniformly earned $234,000 and paid dividends of $37,500 on April 1 and again on October 1. On August 1, 2010, Starling sold 30% of its investment in Twig for $262,500, thereby reducing its interest in Twig to 56%.

Required: Compute the following using the actual sales date assumption:

1. Gain or loss on sale.

2. Income from Twig for 2010.

3. Noncontrolling interest share for 2010.

Answer:

Preliminary computations

Investment balance, January 1 $900,000

Income from Twig ($234,000 x 7/12 × 80%) 109,200

Less: April 1 dividends ($37,500 × 80%) (30,000)

Book value at July 31, 2010 $979,200

Requirement 1

Proceeds from sale $262,500

Book value of interest sold

($979,200 × 30%) 293,760

Loss on sale $ (31,260)

Requirement 2

Income from Twig from Jan 1 through July 31

(from above) $109,200

Income from August 1 - December 31

($234,000 × 5/12 × 56%) 54,600

Income from Twig for 2010 $ 163,800

Requirement 3

Noncontrolling interest share:

Jan 1 to Jul 31 ($234,000 × 7/12 × 20%) $27,300

Aug 1 to Dec 31 ($234,000 × 5/12 × 44%) 42,900

Noncontrolling interest share $ 70,200

Objective: LO2

Difficulty: Moderate

balance was $2,100,000, consisting of 60% of Liptin's $3,500,000 of net assets.

During 2011, Liptin earned $300,000 uniformly and paid dividends of $110,000 on November 1. On October 1, 2011, Fly sold 10% of its investment in Liptin for $364,000, thereby reducing its interest in Liptin to 54%.

Required: Compute the following using the actual sales date assumption:

1. Gain or loss on sale.

2. Income from Liptin for 2011.

3. Noncontrolling interest share for 2011.

Answer:

Preliminary computations

Investment balance, January 1 $2,100,000

Income from Liptin ($300,000 × 9/12 × 60%) 135,000

Book value at September 30, 2011 $2,235,000

Requirement 1

Proceeds from sale $364,000

Book value of interest sold

($2,235,000 × 10%) 223,500

Gain on sale $140,500

Requirement 2

Income from Liptin from Jan 1

through September 30 (from above) $135,000

Income from October 1-December 31

($300,000 × 3/12 × 54%) 40,500

Income from Liptin for 2011 $175,500

Requirement 3

Noncontrolling interest share:

Jan 1 to Sep 30 ($300,000 × 9/12 × 40%) $90,000

Oct 1 to Dec 31 ($300,000 × 3/12 × 46%) 34,500

Noncontrolling interest share $124,500

Objective: LO2

Difficulty: Moderate

6) At December 31, 2012 year-end, Lapwing Corporation's investment in Ground Inc. was $200,000 consisting of 80% of Ground's $250,000 stockholders' equity on that date. On April 1, 2013, Lapwing sold 20% interest (one-fourth of its holdings) in Ground for $65,000. During 2013, Ground had net income of $75,000(earned uniformly) and on July 1, 2013, Ground paid dividends of $40,000. Lapwing uses the equity method to account for the investment.

Required:

1. What is the gain or loss on sale of the 20% interest?

2. Record the journal entries for Lapwing for the year ending December 31, 201

3. Use the actual-sale-date assumption.

Answer:

Requirement 1

Selling price $65,000

Book value of interest sold:

Beginning balance $200,000

Income for 3 months

$75,000 × 1/4 × 80% =15,000

Adjusted book value 215,000

Percentage of interest sold 25%

Book value applied 53,750 53,750

Gain on sale $11,250

Requirement 2 Debit Credit

April 1

Investment in Ground 15,000

Income from Ground 15,000

Cash 65,000

Investment in Ground 53,750

Gain from sale of investment in Ground 11,250

July 1

Cash ($40,000 × 60%) 24,000

Investment in Ground 24,000

December 31

Investment in Ground 33,750

Income from Ground 33,750

($75,000 × 60% × 9/12)

Objective: LO2

Difficulty: Moderate

7) At December 31, 2012 year-end, Arnold Corporation's investment in Oakes Inc. was $200,000 consisting of 80% of Oakes's $250,000 stockholders' equity on that date. On April 1, 2013, Arnold sold 20% interest (one-fourth of its holdings) in Oakes for $65,000. During 2013, Oakes had net income of $75,000 (earned uniformly) and on July 1, 2013, Oakes paid dividends of $40,000. Arnold uses the equity method to account for the investment.

Required:

1. What is the gain or loss on sale of the 20% interest?

2. Record the journal entries for Arnold for the year ending December 31, 201

3. Use the

beginning-of-the-year-sale-date assumption.

Answer:

Requirement 1

Selling price $65,000

Book value of interest sold:

Beginning balance $200,000

Percentage of interest sold 25%

Book value applied 50,000 50,000

Gain on sale $15,000

Requirement 2 Debit Credit

April 1

Cash 65,000

Investment in Oakes 50,000

Gain from sale of investment in Oakes 15,000

July 1

Cash ($40,000 × 60%) 24,000

Investment in Oakes 24,000

December 31

Investment in Oakes 45,000

Income from Oakes 45,000

($75,000 × 60%)

Objective: LO2

Difficulty: Moderate

8) Candy Corporation paid $240,000 on April 1, 2011 for all of the common stock of Bun Corporation in a business acquisition. On January 1, 2011, Bun's stockholders' equity was equal to $195,000. Bun's first quarter 2011 net income was $10,000 and first quarter 2011 dividends were $5,000. In 2011, preacquisition sales were $32,500 and preacquisition cost of sales was $22,500. (There were no other preacquisition expenses in 2011.) Dividends are paid quarterly on March 31, June 30, September 30 and December 31. Any excess cost over book value acquired is allocated to goodwill.

Additional information:

1. Candy sold equipment with a 5-year remaining useful life to Bun on July 1, 2011 for a gain of $10,000. Salvage value of the equipment is zero and both companies use the straight-line depreciation method.

2. Bun's accounts payable balance at December 31 includes $5,000 due to Candy from the sale of equipment.

3. Candy accounts for its investment in Bun using the equity method.

Complete the working papers to consolidate the financial statements of Candy and Bun Corporations for the year ending December 31, 2011.

Objective: LO1, 2 Difficulty: Difficult

9) Olson Corporation paid $62,000 to acquire 100% of Towing Corporation's outstanding voting common stock at book value on May 1, 2011. The stockholders' equity of Towing on January 1, 2011 consisted of $40,000 Capital Stock and $20,000 Retained Earnings. Towing's total dividends for 2011 were $6,000, paid equally on April 1 and October 1. Towing's net income was earned uniformly throughout 2011. In 2011, preacquisition sales were $10,000 and preacquisition expenses were cost of sales for $5,000. (There were no other preacquisition expenses in 2011.)

During 2011, Olson made sales of $10,000 to Towing at a gross profit of $3,000. One-half of this merchandise was inventoried by Towing at year-end, and one-half of the 2011 intercompany sales were unpaid at year-end 2011.

Olson sold equipment with a ten-year remaining useful life to Towing at a $2,000 gain on December 31, 2011. The straight-line depreciation method is used by both companies. The equipment has no salvage value.

Financial statements of Olson and Towing Corporations for 2011 appear in the first two columns of the partially completed consolidation working papers.

Complete the consolidating working papers for Olson Corporation and Subsidiary for the year ending December 31, 2011.

高级财务会计练习及答案 一租赁练习 一、单项选择题 1.在某项固定资产租赁合同中,租赁资产原账面价值为45万元,每年年末支付10万元租金,租赁期为5年,承租人无优惠购买选择权,租赁开始日估计资产余值为4万元,承租人提供资产余值的担保金额为3万元,另外担保公司提供资产余值的担保金额为1万元,则最低租赁付款额为()万元。 A.50 B.53 C.49 D.45 2.在售后租回交易形成融资租赁的情况下,对所售资产的售价与其账面价值之间的差额,应当采用的会计处理方法是( ) 。 A. 计入当期损益 B. 计入递延损益 C. 售价高于其账面价值的差额计入当期损益,反之计入递延损益 D. 售价高于其账面价值的差额计入递延损益,反之计入当期损益 3.甲公司采用融资租赁方式租入一台大型设备,该设备的入账价值为1200万元,租赁期为10年,与承租人相关的第三方提供的租赁资产担保余值为200万元,预计清理费用为50万元。该设备的预计使用年限为10年,预计净残值为120万元。甲公司采用年限平均法对该租入设备计提折旧。甲公司每年对该租入设备计提的折旧额为()。 A.105万元 B.108万元 C.113万元 D.120万元 4.租赁开始日是指()。 A、租赁协议日 B、租赁各方就主要租赁条款做出承诺日 C、租赁协议日与租赁各方就主要租赁条款做出承诺日中的较早者 D、租赁协议日与租赁各方就主要租赁条款做出承诺日中的较晚者 5.售后租回形成融资租赁的情况下,承租人每期确认未实现售后租回损益的摊销方法为()。 A、在租赁期内平均确定 B、按折旧进度 C、按租金支付比例 D、按实际利率法 二、多项选择题 1.下列项目不可以计入融资租入固定资产价值的有()。 A.支付的与租赁有关的印花税B.履约成本C.支付的有关人员差旅费D.支付的固定资产的安装费E.或有租金 2.融资租赁下,采用实际利率法分摊未确认融资费用时,下列表述正确的是( ) 。

高级财务会计第版练习 题答案 Last revised by LE LE in 2021

第1章所得税费用 一、单项选择题 1.【2014年注册会计师考试《会计》试题】甲公司本期的会计利润210万元,本期有国债收入10万元,本期有环保部门罚款20万元,另外,已知固定资产对应的递延所得税负债年初金额为20万元,年末金额为25万元。甲公司本期的所得税费用金额为( )万元。 A. 50 B. 60 C. 55 D. [答案]:C [解析]:应交所得税=[210-10+20-5/25%]*25%=50(万元),递延所得税负债的当期发生额=25-5=5(万元),所得税费用=50+5=55(万元)。 2.【2012年中级职称试题】2011年12月31日,甲公司因交易性金融资产和可供出售金融资产的公允价值变动,分别确认了10万元的递延所得税资产和20万元的递延所得税负债。甲公司当期应交所得税的金额为150万元。假定不考虑其他因素,该公司2011年度利润表“所得税费用”项目应列示的金额为()万元 A. 120 B. 140 C. 160 D. 180 【参考答案】B 二、多项选择题 1.【2012年中级职称试题】下列各项中,能够产生应纳税暂时性差异的有()。 A.账面价值大于其计税基础的资产 B.账面价值小于其计税基础的负债 C.超过税法扣除标准的业务宣传费 D.按税法规定可以结转以后年度的为弥补亏损 【参考答案】AB 2.【2010年注册会计师考试专业阶段试题】甲公司20×9年度涉及所得税的有关交易或事项如下:

(1)甲公司持有乙公司40%股权,与丙公司共同控制乙公司的财务和经营政策。甲公司对乙公司的长期股权投资系甲公司20×7年2月8日购入,其初始投资成本为3 000万元,初始投资成本小于投资时应享有乙公司可辨认净资产公允价值份额的差额为400万元。甲公司拟长期持有乙公司股权。根据税法规定,甲公司对乙公司长期股权投资的计税基础等于初始投资成本。 (2)20×9年1月1日,甲公司开始对A设备计提折旧。A设备的成本为8 000万元,预计使用10年,预计净残值为零,采用年限平均法计提折旧。根据税法规定,A设备的折旧年限为16年。假定甲公司A设备的折旧方法和净残值符合税法规定。 (3)20×9年7月5日,甲公司自行研究开发的B专利技术达到预定可使用状态,并作为无形资产入账。B专利技术的成本为4 000万元,预计使用10年,预计净残值为零,采用直线法摊销。根据税法规定,B专利技术的计税基础为其成本的150%。假定甲公司B专利技术的摊销方法、摊销年限和净残值符合税法规定。 (4)20×9年12月31日,甲公司对商誉计提减值准备1 000万元。该商誉系20×7年12月8日甲公司从丙公司处购买丁公司100%股权并吸收合并丁公司时形成的,初始计量金额为3 500万元,丙公司根据税法规定已经缴纳与转让丁公司100%股权相关的所得税及其他税费。根据税法规定,甲公司购买丁公司产生的商誉在整体转让或者清算相关资产、负债时,允许税前扣除。 (5)甲公司的C建筑物于20×7年12月30日投入使用并直接出租,成本为6 800万元。甲公司对投资性房地产采用公允价值模式进行后续计量。20×9年12月31日,已出租C建筑物累计公允价值变动收益为1 200万元,其中本年度公允价值变动收益为500万元。根据税法规定,已出租C建筑物以历史成本按税法规定扣除折旧后作为其计税基础,折旧年限为20年,净残值为零,自投入使用的次月起采用年限平均法计提折旧。甲公司20×9年度实现的利润总额为15 000万元,适用的所得税税率为25%。假定甲公司未来年度有足够的应纳税所得额用于抵扣可抵扣暂时性差异。 要求:根据上述资料,不考虑其他因素,回答下列第(1)小题至第(2)小题。

第一章 高级财务会计所依据的理论和采用的方法(B )。 A. 抛弃了原有的财会理论与方法 B. 是对原有财务会计理论和方法的修正 C. 沿用了原有财会理论和方法 D. 仍以四大假设为出发点 [ 答案解析] 高级财务会计是在对原财务会计理论与方法体系进行修正的基础上,对企业出现的特殊交易和事项进行会计处理的理论与方法的总称。 高级财务会计研究的对象是(A )。 A. 企业面临的特殊事项 B. 与中级财务会计一致 C. 对企业一般交易事项在理论与方法上的进一步研究 D. 企业所有的交易和事项 [ 答案解析] 高级财务会计处理的是企业面临的特殊事项。特殊事项是企业在经营的某一特定阶段或某一特定条件下出现的事项,如公司在频临破产状态下进行的清算或重组事项;跨国经营情况下的外币报表折算,等等。 高级财务会计产生的基础是( C )。 A. 货币计量假设的松动 B. 会计主体假设的松动 C. 以上都对 D. 持续经营假设与会计分期 假设的松动 [ 答案解析] 高级财务会计产生于会计所处的客观经济环境的变化,是客观经济环境发生变化引起会计假设松动后,人们对背离会计假设的特殊会计事项进行理论和方法研究的结果。 通货膨胀的产生使得( B )。 A. 持续经营假设产生松动 B. 货币计量假设产生松动 C. 会计分期假设产生松动 D. 会计主 体假设产生松动 [ 答题解析] 普遍的、持续性的通货膨胀,使得货币购买力不断下降,货币计量假设中隐含的币值稳定的假定严重脱离现实。 如果企业面临清算,投资者和债权人关心的将是资产的(B )和资产的偿债能力。 A. 历史成本 B. 可变现净值 C. 账面价值 D. 估计售价 [ 答题解析] 如果企业面临清算,投资者和债权人关心的将是资产的可变现净值和资产的偿债能力,按可变现净值计价才能提供决策有用的信息 企业面临破产清算和重组等特殊会计事项,正是(C )动摇的结果。 A. 会计主体假设和持续经营假设 B. 持续经营假设和货币计量假设 C. 持续经营假设和会计分期假设 D. 会计分期假设和货币计量假设

高级财务会计练习及答 案 内部编号:(YUUT-TBBY-MMUT-URRUY-UOOY-DBUYI-0128)

高级财务会计练习题 一、判断题 1.(√)企业合并最主要的原因通常是扩大规模,获取经济利益。 2.(×)吸收合并中,参与合并各方的法律地位均丧失。解释:吸收合并是 一家企业保留法人资格,其他企业随着合并而消失。 3.(√)新设合并中,被合并的公司均丧失法律地位。解释:是几家公司协 议合并共同组成一家新企业。 4.(√)控股合并主要表现为一家公司取得另一家公司的全部或部分有表决 权资本,两公司仍保留其法律地位。 5.(×)在购买法下,如果支付的总成本高于净资产的公允市价,应将其差 额确认为一项费用,计入当期损益。解释:应作为商誉处理。 6.(√)在权益集合法下,参与合并的企业各自的会计报表均保持原来的账 面价值。解释:所谓权益结合法,以发行股票的方式与参与合并的企业的股东间的普通股的交换。 7.(×)当子公司所有者权益为负数时,母公司对其权益性资本投资数额为 0。在这种情况下,不应当将这一子公司纳入合并范围。 8.(√)确定合并会计报表的编制范围的关键取决于是否对被投资公司具有 实质意义上的控制,而不是完全取决于是否拥有被投资公司半数以上的权益性资本。解释:凡能够为母公司所控制的被投资企业都属于控制范围 9.(×)母公司拥有半数以上权益性资本的所有被投资企业,均应纳入合并 报表内。 10.(×)子公司的本期净利润就是母公司的投资收益。

11.(×)若集团内部不曾发生内部交易,则合并报表就是个别报表的加总。 12.(×)对于子公司相互之间发生的内部交易,在编制合并报表时不需要进 行抵销处理。 13.(√)从企业集团整体来看,集团内部企业之间的商品购销活动实际上相 当于一个企业内部物资调拨活动,既不会实现利润,也不会增加商品价值,因此,应当将存货价值中包含的未实现内部销售利润予以抵销。 14.(×)合并商誉是指企业合并中,购买方所支付的购买价格高于被购买企 业净资产所产生的差额,包括被购买企业净资产与其账面价值之间的差额。 解释:购买价格高于公允价值的部分 15.(√)“少数股东权益”项目反映母公司以外的其他投资者在子公司中的 权益,表示其他投资者在子公司中的权益。 16.(×)当本期内部应收账款的数额与上期内部应收账款的数额相等时, 对坏账准备不需要进行抵销处理。解释:借:坏账准备贷:期初未分配利润17.(×)未实现内部销售利润不论是从企业集团来说,还是从集团内的销售 企业和购买企业来说,都是未实现的利润。 18.(×)若集团内部的应收账款和应付账款产生于以前年度,则债权企业对 该项应收账款的坏账准备也是以前年度计提的,因此当年就不需要对坏账准备进行抵销。 19.(√)控股合并主要表现为一家公司取得另一家公司的全部或部分有表决 权资本,两公司仍保留其法律地位。 20.(×)在购买法下,企业发行股票所取得的资产,应按资产的账面价值计 价。解释:公允市价反映。

绝密★考试结束前 全国2015年4月高等教育自学考试 高级财务会计试题 课程代码:《00159》 请考生按规定用笔将所有试题的答案涂、写在答题纸上。 选择题部分 注意事项: 1. 答题前,考生务必将自己的考试课程名称、姓名、准考证号用黑色字迹的签字笔或钢笔填写在答题纸规定的位值上。 2. 每小题选出答案后,用2B铅笔把答题纸上对应题目的答案标号涂黑。如需改动,用橡皮擦干净后,在选涂其他答案标号。不能答在试题卷上。 一、单项选择题(本大题共20小题,每小题1分,共20分)在每小题列出的四个备选项中只有一个是符合题目要求的,请将其选出并将“答题纸”的相应代码涂黑。错涂、多涂或未涂均无分? 1. 根据我国企业会计准则规定,对外币资产负债表进行折算时,“实收资本”项目应采用的折算汇率是( D ) A.期初汇率 B.平均汇率 C.交易发生时即期汇率 D.资产负债表日即期汇率 2. 下列各项支出中,在计算应纳税所得额时允许税前扣除的是( B ) A税收滞纳金 B.非公益性捐赠 C.未经核定的准备金支出 D.按照税法规定计算的固定资产折旧 3. 下列上市公司披露的报告中,必须经注册会计师审计的是( B ) A.临时报告 B.月度财务报告 C.季度财务报告 D.年度财务报告 4. 根据我国企业会计准则规定,不要求企业在中期财务报告中单独披兹的是( B )A利润表 B.资产负债表 C.现金流量表 D.所有者权益变动表 5. 下列各项中,在确定融资租入资产入账价值时不需要考虑的是( B ) A.租赁资产未担保余值 B.最低租赁付款额现值 C.承租人发生的初始直接费用 D.租货开始日租赁资产公允价值 6. 根据我国企业会计准则规定,出租人分配未实现融资收益应采用的方法是( B ) A.工作里法 B.实际利率法 C.年数总和法 D.双倍余额递减法 7. 下列关于权益工具的说法中,正确的是( C ) A. 权益工具包括可转换愤券 B. 权益工具不包括认股权证 C. 权益工具是能证明拥有某个企业剩余权益的合同 D. 从发行方看,权益工具是与股权投资相同性质的合同

《高级财务会计》综合练习题 一、单项选择题 1.甲公司和乙公司同为A集团的子公司。甲公司于2009年1月1日以银行存款12 000万元取得乙公司70%的股份,2009年1月1日,乙公司所有者权益的账面价值为20 000万元,可辨认净资产公允价值为24 000万元。甲公司为进行企业合并支付审计费等直接费用30万元。2009年1月1日甲公司应确认的资本公积为()万元。 A.2000 B.0 C.4 800 D.1970 2.依据企业会计准则的规定,下列有关企业合并的表述中,不正确的是()。 A.同一控制下的企业合并中,合并成本是购买方为取得对被购买方的控制权支付对价的公允价值及各项直接相关费用之和 B.受同一母公司控制的两个企业之间进行的合并,通常属于同一控制下的企业合并 C.同一控制下的控股合并发生当期,合并方于期末编制合并利润表时应包括被合并方自合并当期期初至期末的净利润 D.企业合并是将两个或两个以上单独的企业合并形成一个报告主体的交易或事项 3.按照我国企业会计准则的规定,非同一控制下企业合并在购买日一般只需要编制()。 A.合并利润表 B.合并所有者权益变动表 C.合并资产负债表 D.合并现金流量表 4.下列项目中,C公司应纳入A公司合并围的情况是()。 A.A公司拥有B公司60%的权益性资本,A公司直接拥有C公司20%的权益性资本,B公司拥有C公司40%的权益性资本 B.A公司拥有C公司43%的权益性资本 C.A公司拥有B公司70%的权益性资本,B公司拥有C公司40%的权益性资本 D.A公司拥有B公司50%的权益性资本,B公司拥有C公司100%的权益性资本 5.子公司上期用20 000元将母公司成本为16 000元的货物购入,全部形成期末存货,本期销售其中的70%,售价18 000元;子公司本期又用 40 000元将母公司成本为34 000元的货物购入,没有销售,全部形成存货。则期末存货中包含的未实现部销售损益是()。 A.6 000 B.7 200 C.1 200 D.4 000 6.母公司在编制合并现金流量表时,下列各项中,会引起筹资活动产生的现金流量发生增减变动的是()。 A.子公司购买少数股东的固定资产支付的现金 B.子公司向少数股东出售无形资产收到的现金 C.子公司依法减资支付给少数股东的现金 D.子公司购买少数股东发行的债券支付的现金 7.母公司期初期末对子公司应收款项余额分别是200万元和150万元,母公司始终按应收款项余额的5‰提取坏账准备,则母公司期末编制合并报表时,因抵消部应收款项而影响的期初未分配利润金额是()万元。 A.0 B.0.25 C.0.75 D.1 8.甲公司2008年12月31日融资租入一台设备,设备的公允价值为490万元,租赁期4年,每年年末支付租金150万元,按租赁合同规定的利率折合的现值为540万元,甲公司在租赁谈判过程中发生手续费、律师费等合计10万元。则在租赁期开始日,租赁资产的入账价值是()万元。 A.540 B.500 C.510 D.600 9.承租人对融资租入的资产采用公允价值作为入账价值的,分摊未确认融资费用所采用的分摊率是()。 A.出租人出租资产的无风险利率 B.使最低租赁付款额的现值与租赁资产公允价值相等的折现率 C.银行同期贷款利率 D.租赁合同中规定的利率 10.某企业以融资租赁方式租入固定资产一台,租期4年,租赁开始日租赁资产公允价值为300万元,最低租赁付

高级财务会计习题答案 Prepared on 22 November 2020

《高级财务会计》习题答案 第一章非货币资产交换 1、2007年5月,A公司以其一直用于出租的一幢房屋换入B公司生产的办公家具准备作为办公设备使用,B公司则换入的房屋继续出租。交换前A公司对该房屋采用成本模式进行后续计量,该房屋的原始成本为500 000元,累计已提折旧180 000元,公允价值为400 000元,没有计提减值准备;B公司换入房屋后继续采用成本模式进行计量。B公司办公家具账面价值为280 000元,公允价值与计税价格均为300 000元,适用的增值税税率为17%,B公司另外支付A公司49 000元的补价。假设交换不涉及其他的相关税费。 要求:分别编制A公司和B公司与该资产交换相关的会计分录。 A公司的会计处理: 49 000/400 000=%,所以交换属于非货币资产交换。 换入设备的入账价值=400 000-(300 000×17%)-49 000=300 000元 换出资产应确认的损益=400 000-320 000=80 000元 借:固定资产清理 320 000 累计折旧 180 000 贷:投资性房地产 500 000 借:固定资产——办公设备 300 000 银行存款 49 000 应交税金—增值税(进项) 51 000 贷:固定资产清理 320 000

其他业务收入(投资性房地产收益) 80 000 B公司的会计处理 换入设备的入账价值=300 000+300 000×17%+49 000=400 000元 换出资产应确认的损益=300 000-280 000=20 000元 借:投资性房地产 400 000 贷:主营业务收入 300 000 应交税金——增值税(销项) 51 000 银行存款 49 000 借:主营业务成本 280 000 贷:库存商品 280 000 2、2007年9月,X公司生产经营出现现金短缺,为扭转财务困境,遂决定将其正在建造的一幢办公楼及购买的办公设备与Y公司的一项专利技术及其对Z公司的一项长期股权投资进行交换。截止交换日,X公司办公楼的建设成本为900 000元。办公设备的账面价值为600 000元,公允价值为620 000元;Y公司的专利技术的账面价值为400 000元,长期股前投资的账面价值为600 000元。由于正在建造的办公楼的完工程度难以合理确定,Y公司的专利技术为新开发的前沿技术,Z公司是非上市公司,因而X公司在建的办公楼、Y公司的专利技术和对Z公司的长期股权投资这三项资产的公允价值均不能可靠计量。Y公司另支付X公司300 000元补价。假设该资产交换不涉及相关税费。 要求:分别编制X公司和Y公司与该资产交换相关的会计分录。 X公司的会计处理: 因为公允价值均不能可靠计量,所以采用账面价值计量换入资产。

一、单项选择题(本大题共20小题,每小题1分,共20分)在每小题列出的四个备选项中只有一个是符合题目要求的,请将其代码填写在题后的括号内。错选、多选或未选均无分。 1、下列合并财务报表中,需要在控制权取得日编制的是(C )。 A. 合并利润表 B. 合并现金流量表 C. 合并资产负债表 D. 合并所有者权益变动表 2、下列不属于基础金融工具的是(C )。 A. 银行存款 B. 应收账款 C. 商品期货 D. 其他应收款 3、清算会计的计量基础是(B )。 A. 历史成本 B. 变现价值 C. 预计净残值 D. 现行重置成本 4、有关企业合并的说法中,正确的是(C )。 A. 企业合并必然形成长期股权投资 B. 同一控制下的企业合并就是吸收合并 C. 控股合并的结果是形成母子公司关系 D. 企业合并的结果是取得被合并方净资产 5、对于非同一控制下的吸收合并,合并方对合并商誉的下列账务处理方法中符合我国现行会计准则的是( A )。 A. 单独确定商誉,不予以摊销 B. 确认为一项无形资产并分期摊销 C. 计入“长期股权投资”的账面价值 D. 调整减少吸收合并当期的股东权益 6、2010年某企业利润总额为800万元,当年发生应纳税暂时性差异120万元,发生可抵扣暂时性差异170万元,适用的所得税税率为25%,则该企业2010年所得税费用为(B )A.187.5万元 B.200万元 C.212.5万元 D.272.5万元 7、关于承租人融资租赁业务发生的初始直接费用,下列说法中正确的是(D )。 A. 计入管理费用 B. 计入财务费用 C. 计入营业外支出 D. 计入租入资产的价值 8、资产负债表日,衍生金融工具公允价值低于其账面余额的差额,应贷记“衍生工具”科目,应借记的科目是(A )。 A. 公允价值变动损益 B. 套期损益 C. 汇兑损益 D. 投资收益 9、2011年12月31日,某企业融资租入一台设备,租赁开始日租赁资产公允价值为300万元最低租赁付款额为420万元,按出租人的租赁内含利率折成的现值为320万元,则在租赁开始日,租赁资产的入账价值、未确认融资费用分别是(B )万元。 A. 320、100 B. 300、120 C. 420、0 D. 320、0 10、甲公司合并乙公司,合并后甲公司拥有乙公司资产并承担其债务,乙公司法人资格随合并而注销,这种合并方式是( C )。 A. 横向合并 B. 新设合并 C. 吸收合并 D. 控股合并 11、2010年7月1日,甲公司向乙公司股东发行股票1200万股吸收合并乙公司,股票面值1元,发行价格为3元,合并日乙公司可辨认净资产的账面价值为3000万元,公允价值为3200万元,该合并为非同一控制下企业合并,则甲公司应确认的合并商誉是(B )。 A. —800万元 B. 400万元 C. 600万元 D. 1800万元 12、以一定单位的外币为标准折合成一定数额的本国货币的汇率标价方法是(C )。 A. 市场标价法 B. 总额标价法 C. 直接标价法 D. 间接标价法 13、2010年6月,母公司将成本为60万元的存货以85万元的价格销售给子公司,子公司销售其中的40%,售价45万元,则期末编制合并财务报表时,编制的抵销分录中不涉及的财务报表项目是(D )。 A. 存货 B. 营业收入 C. 营业成本 D. 未分配利润

高级财务会计的试题及答案 一、单项选择题(在每小题的四个备选答案中,选出一个正确答案,并将正确答案的序号填在题干的括号内。每小题1.5分,共15分) 1.在下列各项业务中,可以归为多层次结构会计主体的特殊会计业务是( ) A.通货膨胀会计 B.企业合并 C.期货交易 D.股份上市公司信息披露 2.某国有企业整体改组为上市公司,经评估确认的账面净资产为8000万元,其中股本5000万元。发起人的股份额占新组建公司总股本额的80%,其余向公众募集。新组建公司注册资本为6000万元,折股倍数为( ) A. 166.67% B. 60% C. 104.17% D. 106.67% 3.市盈率等于普通股股票的( )与每股盈利之间的比例。 A.每股面值 B.每股设定价值 C.每股账面价值 D.每股市价 4.对于融资租赁性质的回租业务,承租人(兼销货方)所取得的销售收入超过资产账面净值的差额,应作为( ) A.当期损失 B.递延收益 C.财务费用 D.营业收入 5.房地产企业对外转让、销售和出租开发产品等取得的收入应计入( )科目。 A.其他业务收入 B.经营收入 C.营业外收入 D.销售利润 6.我国外币报表折算采用( ) A.时态法 B.货币与非货币性项目法 C.现行汇率法 D.流动与非流动性项目法 7.直接标价法下,汇率上升,企业拥有( )会产生汇兑收益。 A.货币性资产 B.外币货币性资产 C.货币性负债 D.外币货币性负债 8.关于权益集合法,下列哪种说法是错误的( ) A.参与合并企业资产、负债和所有者权益以账面价值计价 B.企业合并通过股票交换 C.留存收益不予以合并 D.一般适用于吸收合并和创立合并 9.房地产会计中开发产品成本采用( )核算。

购并日后的合并财务报表习题 一、判断题 10分 1.母公司在报告期内因同一控制下企业合并增加的子公司,编制合并资产负债表时,不应当调整合并资产负债表的期初数。()2.母公司因非同一控制下企业合并增加的子公司,编制合并资产负债表时,应当调整合并资产负债表的期初数。()3.母公司在报告期内处置子公司,应当将该子公司期初至处置日的收入、费用、利润纳入合并利润表。 4.子公司所有者权益中不属于母公司的份额,应当作为少数股东权益,在合并资产负债表中负债与所有者权益项目之间以“少数股东权益”项目列示。() 5. 为编制合并财务报表,集团内部公司间的所有交易和往来业务的抵销应分别计入母子公司的账簿中。 6.根据稳健性原则,编制合并财务报表中,只应抵销集团内部因销售而产生的未实现收益,而不应抵销集团内部因销售而产生的未实现损失。() 7.从企业集团来看,内部交易形成的期末存货的账面价值一般等于持有该存货的企业账面价值。() 8. 母公司以高于成本的价格向子公司出售一台设备,编制合并报表中,应抵销子公司多计提的折旧。() 9. 合并报表中,母公司对子公司的长期股权投资与母公司在子公司所有者权益中所享有的份额应当相互抵销,不需抵销相应的长期股权投资减值准备。()10、为编制合并财务报表,集团内部公司间的所有交易和往来业务都应抵销。() 二、单项选择题 14分 1.甲公司通过定向增发普通股,取得乙公司30%的股权。该项交易中,甲公司定向增发股份的数量为1000万股(每股面值1元,公允价值为2元),发行股份过程中向证券承销机构支付佣金及手续费共计50万元。除发行股份外,甲公司还承担了乙公司原股东对第三方的债务500万元。取得投资时,乙公司股东大会已通过利润分配方案,甲公司可取得120万元。乙公司的可辨认净资产公允价值为8000万元。甲公司对乙公司长期股权投资的初始投资成本为()。 A.2550万元万元 C.2380万元万元 2.承上题,甲公司对乙公司长期股权投资的入账价值为()。 A.2430万元万元 C.2380万元万元 3. 甲、乙公司此前无关联关系。20×7年2月26日,甲公司以账面价值为3000万元、公允价值为3600万元的非货币性资产为对价,自集团公司处取得对乙公司60%的股权,相关手续已办理;当日乙公司账面净资产总额为5200万元、公允价值为6300万元。20×7年3月29日,乙公司宣告发放20×6年度现金股利500万元。不考虑其他因素影响。20×7年3月31日,甲公司对乙公司长期股权

中央电大高级财务会计 一、单项选择题(每小题2分,共20分) 1.高级财务会计研究的对象是(B.企业特殊的交易和事项 )。 2.同一控制下的企业合并中,合并方为进行企业合并发生的各项直接相关费用,包括为进行企业合并而支付的审计费用、评估费用、法律费用等,应当于发生时计入( A.管理费用)。 3.甲公司拥有乙公司90%的股份,拥有丙公司50%的股份,乙公司拥有丙公司25%的股份,甲公司拥有丙公司股份为( B.75% )。 4.关于非同一控制下企业合并的会计处理,下列说法中不正确的是( C.购买方在购买日对作为企业合并对价付出的资产、发生或承担的负债应当按照账面价值计量,不确认损益 )。 5.下列关于抵销分录表述正确的是( D.编制抵销分录是用来抵销集团内部经济业务事项对个别财务报表的影响 )。 6.股权取得日后各期连续编制合并财务报表时(B.仍要考虑以前年度企业集团内部业务对个别财务报表产生的影响)。 7.母公司期初期末对子公司应收款项余额分别是250万元和200万元,母公司始终按应收款项余额5‰提取坏账准备,则母公司期末编制合并财务报表抵销内部应收款项计提的坏账准备分录是(D )。 D.借:应收账款——坏账准备 12 500 贷:未分配利润——年初 12 500 借:资产减值损失 2 500 贷:应收账款——坏账准备 2 500 8.现行成本会计计量模式是(C.现行成本/名义货币)。 9.在时态法下,按照即期汇率折算的财务报表项目是( B.按市价计价的存货 )。 10.A公司从B公司融资租入一条设备生产线,其公允价值为500万元,最低租赁付款额为600万元,假定按出租人的租赁内含利率折成的现值为520万元,则在租赁开始日,租赁资产的入账价值、未确认融资费用分别是( A.500、100 )万元。 二、多项选择题(每小题2分,共10分) 1.非同一控制下的企业合并,企业合并成本包括(ABCDE )。 A.企业合并中发生的各项直接相关费用 B.购买方为进行企业合并支付的现金 C.购买方为进行企业合并付出的非现金资产的公允价值 D.购买方为进行企业合并发行的权益性证券在购买日的公允价值 E.购买方为进行企业合并发行或承担的债务在购买日的公允价值 2.编制合并财务报表应具备的基本前提条件为( ABCD )。 A.统一母公司与子公司的财务报表决算日和会计期间 B.按权益法调整对子公司的长期股权投资 C.统一母公司和子公司的编报货币 D.统一母公司和子公司采用的会计政策 E.对子公司的长期股权投资采用权益法核算 3.甲公司是乙公司的母公司,20×8年末甲公司应收乙公司账款为800万元,20×9年末甲公司应收乙公司账款为900万元。甲公司坏账准备计提比例均为10%。对此,编制20×9年合并报表工作底稿时应编制的抵销分录有( ABC )。 A.借:应付账款 9 000 000 贷:应收账款 9 000 000 B.借:应收账款——坏账准备 800 000 贷:未分配利润——年初 800 000 C.借:应收账款——坏账准备100 000 贷:资产减值损失 100 000

全国2011年1月自学考试高级财务会计试题及答案 课程代码:00159 一、单项选择题(本大题共20小题,每小题1分,共20分) 在每小题列出的四个备选项中只有一个是符合题目要求的,请将其代码填写在题后的括号内。 错选、多选或未选均无分。 1.采用货币性与非货币性项目法对外币财务报表进行折算时,下列项目中应按现行汇率折算的是( ) A.存货 B.应收账款 C.固定资产 D.实收资本 2.我国企业会计准则要求采用的所得税会计核算方法是( ) A.利润表法 B.应付税款法 C.资产负债表递延法 D.资产负债表债务法 3.下列上市公司定期报告中,必须经注册会计师审计的是( ) A.月度报告 B.季度报告 C.中期报告 D.年度报告 4.在中期财务报告中,不应 ..提供的前期比较财务报表是( ) A.本中期末和上年度末的资产负债表 B.年初至本中期末的、上年年初至可比本中期末的现金流量表 C.本中期的、年初至本中期末以及上年度可比较期间的利润表 D.本中期的、年初至本中期末以及上年度可比较期间的所有者权益变动表 5.甲公司以经营租赁方式将一栋办公楼出租,租约规定,租期三年,第一年末支付租金25万元,第二年末支付租金45万元,第三年末支付租金50万元。租赁期满后,甲公司收回办公楼。甲公司第一年应确认的租金收入为( ) A.25万元 B.40万元 C.45万元 D.50万元 6.下列不属于 ...金融资产的是( ) A.银行存款 B.应收账款 C.债权投资 D.权益工具 7.在资产负债表日,对于衍生金融工具的公允价值高于其账面余额的差额,应借记的账户为衍生工具,贷记的账户为( ) A.投资收益 B.套期损益 C.汇兑损益 D.公允价值变动损益

高级财务会计期末考试试题 一、名词解释(每题3分,共9分) 1.少数股东权益 2.现行汇率法 3.应追索资产 二、单项选择题(从下列每小题的四个选项中,选出一个正确的,请将正确答案的序号填在括号内,每小题2分。共20分) 1.购买企业在确定所承担的负债的公允价值时,一般应按( )确定。 A.可变现净值B.账面价值 C.重置成本D.现行市价 2.在连续编制合并会计报表的情况下,上期抵销内部应收账款额计提的坏账准备对本期的影响时,应编制的抵销分录为( )。 A.借:坏账准备B.借:坏账准备 贷:管理费用贷:期初未分配利润 C.借:期初未分配利润D.借:管理费用 贷:坏账准备贷:坏账准备 3. 在连续编制合并会计报表的情况下,上期已抵销的内部购进存货包含的未实现内部销售利润,在本期应当进行的抵销处理为( )。

A. 借:期初未分配利润B.借:期初未分配利润 贷:主营业务成本贷:存货 C.借:主营业务收入D.借:主营业务收入 贷:主营业务成本贷:存货 4.在货币项目与非货币项目法下,按历史汇率折算的会计报表项目是( )。 A. 存货B.应收账款 C. 长期借款D.货币资金 5.在时态法下,按照历史汇率折算的会计报表项目是( )。 A.按市价计价的存货 B.按成本计价的长期投资 C.应收账款 D.按市价计价的长期投资 6.期货投资企业根据期货经纪公司的结算单据,对已实现的平仓盈利应编制的会计分录是( )。 A. 借:期货保证金B.借:长期股权投资 贷:期货损益贷:期货损益 C.借:应收席位费D.借:期货保证金 贷:期货损益贷:财务费用 7.企业在期货交易所取得会员资格,所交纳的会员资格费应作为( )。 A.管理费用B.长期股权投资 C.期货损益D.会员资格费 8.下列体现财务资本保全的会计计量模式是( )。 A.历史成本/名义货币单位 B.历史成本/不变购买力货币单位

2011年自考高级财务会计押密试题及答案(3) 一、单项选择题 1.外币交易与折算业务属于 (A.各类企业均可能发生的特殊会计业务) 2.下列业务属于企业在特殊时期的特殊会计业务的是 (B.企业清算 ) 3.外币业务会计和物价变动会计的产生,形成的结果是 (D.货币计量假设的松动) 4.在单一交易观点下,外币业务按记账本位币反映的购货成本或销售收入,最终取决于它们的 ( ) A.结算日汇率 5.企业在采用外币业务发生时的市场汇率作为折算汇率的情况下,将人民币兑换成外币时所产生的汇兑损益,是指 (B.银行卖出价与当日市场汇率之差所引起的折算差额 ) 6.当负债的账面价值小于其计税基础时,会产生 (D.应纳税暂时性差异) 7.股份有限公司申请股票上市,公司股本总额应不少于 (C.3 000万元) 8.下列不属于上市公司披露信息的内容是 (A.公司管理办法) 9.租赁业务按其目的不同分为 (C.经营租赁和融资租赁 ) 10.在经营租赁性质的售后回租业务中,承租人因出售资产而获取的收入超过资产账面净额的差额,应作为 ( ) A.营业外收入 11.下列关于创立合并表述正确的是 (D.创立合并是指两个或两个以上的企业协议组成一个新的企业) 12.以是否形成控制作为确定合并范围标准,是运用了合并报表中的 (C.母公司理论) 13.下列子公司中,应排除在其母公司合并会计报表合并范围之外的是 ( ) C.准备近期售出而短期持有其半数以上权益性资本的子公司 14.在连续编制合并报表的情况下,由于上年坏账准备抵消而应调整年初未分配利润的金额为 ( ) C.上年度抵消的内部应收账款计提的坏账准备的数额 15.下列项目属于货币性权益性质的是 (C.优先股) 16.假设同生公司2002年6月20购置固定资产的成本为200 000元,当时物价指数为150,2008年12月31日一般物价指数为310,编制2008年一般物价水平资产负债表时,该固定资产调整后的金额为 ( ) B.413 333.33 采集者退散 17.下列有关现时成本会计报表的说法中,不正确的是 (A.报告期末以等值货币为计价单位) 18.以下属于现时成本会计账户体系中专门设置的特有会计科目是 (A.增补折旧费) 19.企业进入破产清算后,废止的会计原则是 (B.可比性原则) 20.下列属于“清算损益”账户核算内容的是 (B.清算期间处置资产发生的损益) 二、多项选择题。 21.下列属于复合会计主体的特殊会计业务的有 ( ) A.母子公司之间内部往来的会计业务D.破产清算的会计业务 E.企业合并的会计业务 22.以下不属于某企业关联方关系存在形式的有 ( ) A.与该企业共同控制合营企业的合营者C.与该企业发生日常往来的政府部门 D.该企业的供应商

《高级财务会计》习题答案 第一章非货币资产交换 1、2007年5月,A公司以其一直用于出租的一幢房屋换入B公司生产的办公家具准备作为办公设备使用,B公司则换入的房屋继续出租。交换前A公司对该房屋采用成本模式进行后续计量,该房屋的原始成本为500 000元,累计已提折旧180 000元,公允价值为400 000元,没有计提减值准备;B公司换入房屋后继续采用成本模式进行计量。B公司办公家具账面价值为280 000元,公允价值与计税价格均为300 000元,适用的增值税税率为17%,B公司另外支付A公司49 000元的补价。假设交换不涉及其他的相关税费。 要求:分别编制A公司和B公司与该资产交换相关的会计分录。 A公司的会计处理: 49 000/400 000=12.25%,所以交换属于非货币资产交换。 换入设备的入账价值=400 000-(300 000×17%)-49 000=300 000元 换出资产应确认的损益=400 000-320 000=80 000元 借:固定资产清理320 000 累计折旧180 000 贷:投资性房地产500 000 借:固定资产——办公设备300 000 银行存款49 000 应交税金—增值税(进项)51 000 贷:固定资产清理320 000 其他业务收入(投资性房地产收益)80 000 B公司的会计处理 换入设备的入账价值=300 000+300 000×17%+49 000=400 000元 换出资产应确认的损益=300 000-280 000=20 000元 借:投资性房地产400 000 贷:主营业务收入300 000 应交税金——增值税(销项)51 000 银行存款49 000 借:主营业务成本280 000 贷:库存商品280 000 2、2007年9月,X公司生产经营出现现金短缺,为扭转财务困境,遂决定将其正在建造的一幢办公楼及购买的办公设备与Y公司的一项专利技术及其对Z公司的一项长期股权投资进行交换。截止交换日,X公司办公楼的建设成本为900 000元。办公设备的账面价值为600 000元,公允价值为620 000元;Y公司的专利技术的账面价值为400 000元,长期股前投资的账面价值为600 000元。由于正在建造的办公楼的完工程度难以合理确定,Y公

高级财务会计习题 第一章绪论 一、单项选择题 1.高级财务会计所依据的理论和采用的方法是(C )。 A.沿用了原有财会理论和方法. B.仍以四大假设为出发点 C.是对原有财务会计理论和方法的修正 D.抛弃了原有的财会理论与方法 2.高级财务会计研究的对象是( B )。 A.企业所有的交易和事项 B.企业面临的特殊事项 C.对企业一般交易事项在理论与方法上的进一步研究 D.与中级财务会计一致 3.高级财务会计产生的基础是( D )。 A.会计主体假设的松动 B.持续经营假设与会计分期假设的松动 C.货币计量假设的松动 D.以上都对 4.通货膨胀的产生使得( D )。 A.会计主体假设产生松动 B.持续经营假设产生松动 C.会计分期假设产生松动 D.货币计量假设产生松动 5.如果企业面临清算,投资者和债权人关心的将是资产的( B )和资产的偿债能力。A.历史成本 B.可变现净值 C.账面价值 D.估计售价 6.企业面临破产清算和重组等特殊会计事项,正是( C )松动的结果。 A.会计主体假设和持续经营假设 B.持续经营假设和货币计量假设 C.持续经营假设和会计分期假设 D.会计分期假设和货币计量假设 二、多项选择题 1.高级财务会计产生的基础是( ABCDE )。 A.会计主体假设松动 B.会计所处客观经济环境变化 C.持续经营假设松动 D.会计分期假设松动 E.货币计量假设松动 2.高级财务会计中的破产清算会计和重组会计正是( AC )松动的结果。 A.持续经营假设 B会计主体假设 C.会计分期假设 D.货币计量假设 E.币值稳定 3.破产会计主要研究(ABCDE )以及破产会计报告体系的构成与编制。 A.破产资产确认与计量 B.破产债务确认与计量 C.清算净资产确认与计量 D.清算损益确认与计量 E.破产企业债务清偿顺序的确定 4.在会计学中,属于财务会计领域的有( ABC )。A.会计学原理 B.高级财务会计 C.中级财务会计 D.管理会计 E.财务管理 三、判断题 1.高级财务会计是在对原财务会计理论与方法体系进行修正的基础上,对企业出现的特殊

【财务会计】高级财务会计习题 答案完整版 xxxx年xx月xx日 xxxxxxxx集团企业有限公司 Please enter your company's name and contentv

第一章 1. (1)此项租赁属于经营租赁。因为此项租赁未满足融资租赁的任何一项标准。(2)甲公司有关会计分录: ①2008年1月1日 借:长期待摊费用80 贷:银行存款80 ②2008年12月31日 借:管理费用100(200÷2=100)贷:长期待摊费用40 银行存款60 ③2009年12月31日 借:管理费用100 贷:长期待摊费用40 银行存款60 (3)乙公司有关会计分录: ①2008年1月1日, 借:银行存款80 贷:应收账款80 ②2008年、2009年12月31日, 借:银行存款60 应收账款40 贷:租赁收入100(200/2=100)

(1)此项租赁属于经营租赁。因为此项租赁未满足融资租赁的任何一项标准。(2)甲公司有关会计分录: ①2008年1月1日 借:长期待摊费用80 贷:银行存款80 ②2008年12月31日 借:管理费用60 (120÷2=60) 贷:长期待摊费用40 银行存款20 ③2009年12月31日 借:管理费用60 贷:长期待摊费用40 银行存款20 (3)乙公司有关会计分录: ①2008年1月1日 借:银行存款80 贷:应收账款80 ②2008年12月31日 借:银行存款20 应收账款40 贷:租赁收入60 (120÷2=60) ③2009年12月31日 借:银行存款20 应收账款40

3. (1)改良工程领用原材料 借:在建工程421.2 贷:原材料360 应交税费――应交增值税(进项税额转出) 61.20 (2)辅助生产车间为改良工程提供劳务 借:在建工程38.40 贷:生产成本――辅助生产成本38.40 (3)计提工程人员职工薪酬 借:在建工程820.8 贷:应付职工薪酬820.8 (4)改良工程达到预定可使用状态交付使用 借:长期待摊费用1280.4 贷:在建工程1280.4 (5)2009年度摊销长期待摊费用会计 因生产线预计尚可能使用年限为6年,剩余租赁期为5年,因此,应按剩余租赁期5年摊销。借:制造费用256.08 (1280.4÷5) 贷:长期待摊费用256.08 4. 1.2007 年12 月1 日 2.2008 年1 月1 日 3.2007 年12 月1 日