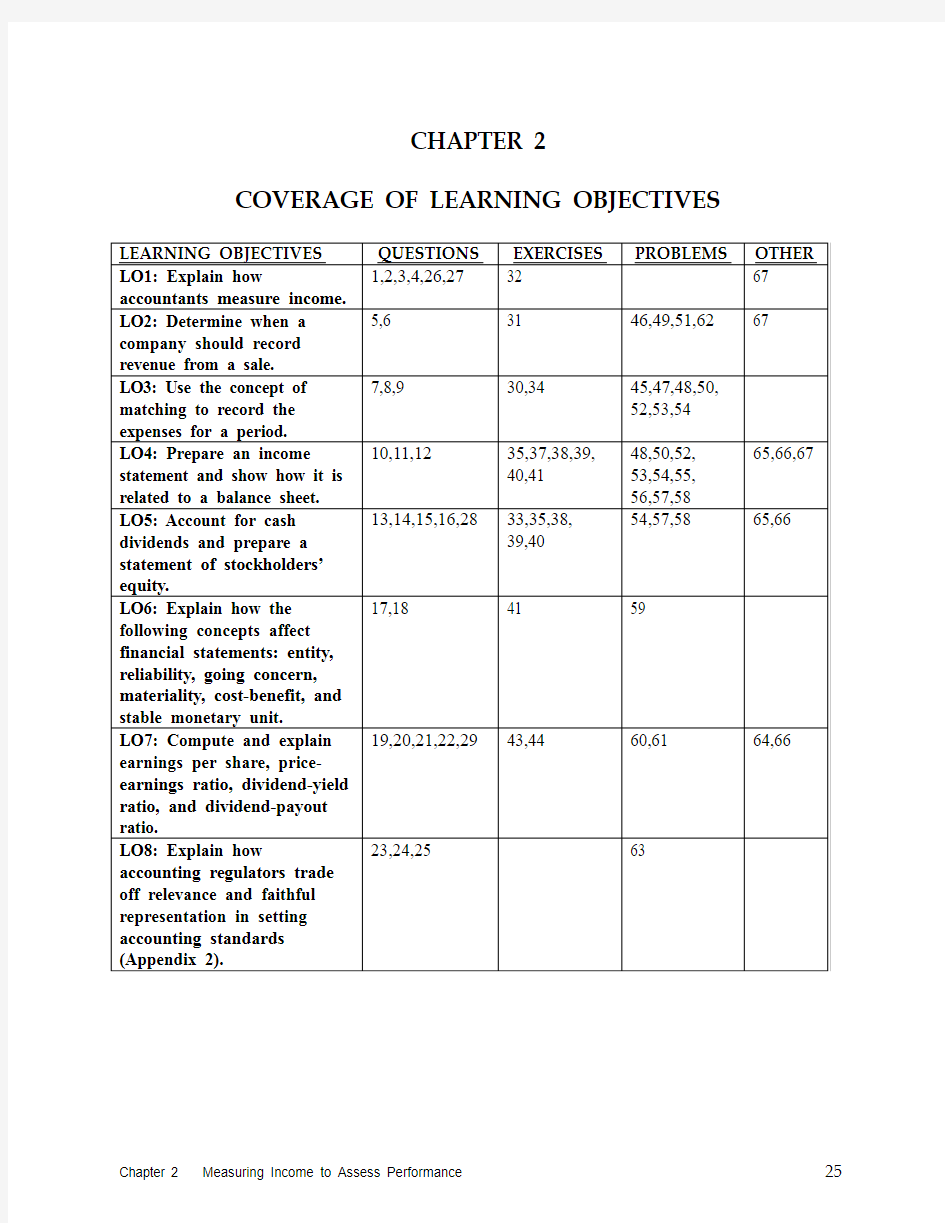

CHAPTER 2

COVERAGE OF LEARNING OBJECTIVES

Chapter 2 Measuring Income to Assess Performance 25

CHAPTER 2

2-1 The operating cycle depends on the nature of the company. It is the time it takes the company to use cash to acquire goods and services, to sell those goods and services to customers, and to collect cash from the sales.

2-2 A fiscal year is the year used for financial reporting. It may be the same as a calendar year, but often it is not. Many companies elect to begin and end a fiscal year at the low point in their annual business activity.

2-3 Expenses are reductions in stockholders’ equity; thus they may be accurately described as negative stockholders’ equity accounts.

2-4 The cash basis fails to match accomplishments with efforts. In particular, the cash basis fails to match revenues and expenses properly. Inventory may be bought and paid for in one period, and sold in the second with the collection from customers in a third period.

Accrual accounting matches revenue and cost of goods sold in the second period, although the cash outlay was in the first and the collection was in the third.

2-5 The two tests of revenue recognition are earning and realization (realized or realizable).

2-6 Revenue recognition is delayed when a company sells a magazine subscription because the company does not recognize revenue until it is earned by delivery of the magazines.

Revenue recognition is also delayed if collection of the account receivable is not reasonably certain, which means that it is not realized or realizable. This may happen with speculative land sales.

2-7 Product costs are naturally linked to revenues, while period costs support a company’s operations for a given period. Product costs become expenses when the company recognizes the related revenue. Period costs become expenses in the period in which they are incurred.

2-8 In theory, all expenses are goods and services that were first purchased as assets and that have now been utilized (used up) in the conduct of operations.

2-9 Managers acquire assets (goods and services) that are then either used instantaneously or at a later time. When the assets are used, they become expenses.

2-10 The balance sheet is a financial picture of a company at one point in time, like a snapshot.

In contrast, an income statement shows activity over a period of time. It shows the series of events that take a company from one “snapshot” (balance sheet) to another, just as a moving picture shows movement from one position to the next.

26

2-11 Synonyms for the income statement are statement of earnings, statement of operations, profit and loss (P&L) statement, and operating statement. A major reason to learn accounting is to be able to read real financial statements. Such statements contain a variety of terms that may differ from the one first leaned in an introductory accounting course. To be able to read and interpret the financial statements, users need to understand the terminology used, including synonyms used for the major accounting terms.

2-12 Managers are often optimistic and feel that things are bound to get better, so they do not like to report bad news. In addition, they may have bonuses or possible future promotions that depend on the financial reports, so they want the reports to be as good as possible. Finally, financial reports are often the “scorecard” for business success, and competitive managers want to report a high score.

2-13 Cash dividends are not necessary in the conduct of revenue-producing operations.

Therefore, they are not expenses but are distributions of assets to owners. These distributions are made possible because of profitable operations, but are not part of the profitable operations.

2-14 Retained earnings is a stockholders’ equity account (a residual claim against assets) not an asset account.

2-15 The statement of stockholders’ equity provides information on why the stockholders’ equity accounts changed during a given period. The three main items that affect stockholders’ equity are net income, transactions with s tockholders, and other comprehensive income—a catch-all category of all equity changes that are neither part of net income nor arise from transactions with owners.

2-16 No. An accounting entity can be a part of an organization, such as a division or department. It can also be an entire economy, such as national income accounting for the United States or another country.

2-17 Reliable data require convincing evidence that can be verified by independent auditors.

Accountants must make sure that data reported in the financial statements can be measured with enough accuracy to be useful to users of the statements.

2-18 Materiality means that items that are not large enough to influence users’ decisions can be omitted from the financial statements. Thus, you do not find pencils or paper clips listed among a company’s assets. Cost-benefit means, for example, that if the cost of measuring an item is greater than the value from knowing it, it can be omitted. Thus, the financial statements of a division of a company may not include an expense for any portion of the company president’s salary, even though the president spends time overseeing the division’s activities. It would simply be too costly for the president to account for each minute spent on each different activity he undertakes and there is no benefit to attempting to allocate the president’s salary to individual divisions. However, in the corporate financial statements, the president’s salary would be treated as an operating cost assigned to the corporation as a whole.

Chapter 2 Measuring Income to Assess Performance 27

2-19 No. One financial ratio, earnings per share (EPS), is presented on the income statement.

2-20 A high P-E ratio means that investors expect future earnings to significantly exceed current earnings. This is likely to be true for fast growing companies.

2-21 Two dividend ratios are as follows:

?Dividend-yield ratio—The amount of dividends paid per dollar invested in a stock at the current market price. The dividend-yield ratio is computed as Dividends per

share ÷ Market price per share.

?Dividend-payout ratio—The percentage of a company’s earnings that is paid out in dividends The dividend-payout ratio is computed as Dividends per share ÷ EPS.

2-22 No. A high dividend-payout ratio may be a bad sign. Companies with a high dividend-payout ratio tend to be slow-growing companies. They return a larger percentage of their income to shareholders because they do not have profitable investments for which to use the money.

2-23 Yes, accountants make many trade-offs between relevance and faithful representation.

Although both are desirable, sometimes it is necessary to sacrifice some of one to gain much of the other. A major trade-off is between market values, which are often more relevant but may raise questions about faithful representation, and historical costs, which faithfully represent an event but may be less relevant.

2-24 The two main characteristics that make accounting information relevant are predictive value—meaning that it helps users form their expectations about the future—and confirmatory value—meaning that it can confirm or contradict existing expectations.

2-25 These criteria support faithful representation. They help ensure that information truly captures the economic substance of the transactions, events, or circumstances it describes. 2-26 A year is a long time to wait for new information about a company’s performance.

Preparing full financial statements is time consuming and costly. Quarterly financial disclosures are less complete than annual ones, but they represent a balanced answer to how often and how complete information should be. Within companies, managers get financial reports daily, weekly, or monthly depending on their needs. In different countries the tradition and the identity of investors have led to different customs. The United States relies on public ownership of companies and needs a system to keep large numbers of investors adequately informed. In countries where more of the ownership is closely held and more of the liabilities are bank financed, there is less need for frequent public disclosure.

2-27 The real choice is not between the cash basis and the accrual basis. We can have either one, but they provide very different information. The accrual-basis income statement is a better measure of overall performance over an accounting period. The cash-basis income statement provides better information about the risks of running out of cash. In the end, our choice between the two would depend on the question we are trying to answer.

28

2-28 The stock price should drop by the amount of the dividend per share. Just before the dividend, the stock is worth whatever it will be worth after the dividend plus the amount of the dividend. The chapter does not address details of exactly when rights to a dividend are created, when they accompany the sale of a share, or when they are retained by the seller. These issues are covered in the owners’ equity chapter (Chapter 10).

2-29 Many investors would say that it does not matter because the security markets are efficient and the P-E ratios reflect the expected growth rates of future earnings for each firm. High-growth firms have high P-E ratios and low-growth firms have lower ones.

Other investors would sort into two groups. Each group of investors believes the market tends to systematically misvalue firms, but they disagree on the nature of the market’s “error.” Value investors believe that the market undervalues good low-growth, low P-E firms and therefore buy them. Growth investors believe that the market undervalues good high-growth, high P-E firms and therefore buy them. Empirically, we can find periods of time when value investors have had better results from their investments than growth investors and vice versa. The bottom line is that investing based on P-E ratios alone is never a good idea, although they are an important descriptor of what the market perceptions of a company are at a moment in time.

2-30 (10 min.)

Balance Sheet Income Statement

3. Accumulated deficit 1. Sales

4. Unexpired costs—asset 2. Net earnings

5. Prepaid expenses—asset 7. Statement of earnings

6. Accounts receivable—asset 8. Used up costs—expense

12. Retained earnings 9. Net profits

14. Statement of financial condition 10. Net income

16. Statement of financial position 11. Revenues

13. Expenses—expense

15. Statement of income

17. Operating statement

18. Cost of goods sold—expense

2-31 (5-10 min.)

The dealer is confused. As used by accountants, revenue is a gross amount earned from sales to customers. For example, sales and revenues are synonyms. Revenue is not “the bottom line” in accountants’ minds. “The bottom line” is net income, that is, revenue minus all expenses. The dealer has $280,000 revenue per month, not income.

Of course, many people use “bottom line” in a nontechnical sense to mean the important or significant result—the result that really matters. For example, “the bottom line is not how much you earn but how much you keep.”

Chapter 2 Measuring Income to Assess Performance 29

2-32 (10 min.)

1. On the cash basi s, Yankton’s net income would be as follows:

Revenue (cash received) $190,000*

Expenses 175,000

Net income $15,000

* Beginning receivables + Credit sales – Cash collections = Ending receivables

$60,000 + 240,000 – Cash collections = $110,000

$60,000 + 240,000 – 110,000 = Cash collections = $190,000

2. On an accrual basis, Yankton’s net income would be as follows:

Revenue (sales) $240,000

Expenses 175,000

Net income $ 65,000

3. The $65,000 net income on the accrual basis is generally the most relevant for assessing

Yankton’s performance. It gives credit for all $240,000 of sales because, provided the

accounts receivable are likely to be received (which is one criterion for the accrual

recognition of revenue), Yankton has created value from all the sales, not just those for

which cash has been received.

2-33 (15-20 min.)

The theme of this solution is that retained earnings is not a pot of cash awaiting distribution to stockholders.

1. Cash $1,000 Paid-in capital $1,000

2. Cash $ 400 Paid-in capital $1,000

Inventory 600

Total $1,000

Note in both Requirements 1 and 2 that the ownership equity is fundamentally a claim against the total assets (in the aggregate). For example, none of the shareholders have a specific claim on cash, and none have a specific claim on inventory. Instead, they all have an undivided claim against (or interest in) all of the assets.

30

3. Cash $1,150 Paid-in capital $1,000

Retained earnings 150

Total $1,150 Retained Earnings is part of stockholders’equity. Even though Cash and Retained Earnings have increased by identical amounts compared to number 1, the retained earnings is fundamentally a general claim against total assets (just as paid-in capital is a general claim). Retained earnings is the net rise in ownership claim attributable to profitable operations. However, the assets themselves should not be confused with the claims against the assets.

4. Cash $ 50 Paid-in capital $1,000

($1,150 – $300 – $800) Retained earnings 150 Inventory 300

Equipment 800

Total $1,150 Total $1,150

The same explanation applies here as in Requirement 3. However, Transaction 4 should clarify the lack of a specific link between retained earnings (and paid-in capital) and any particular assets. The ownership claims are general, not specific.

5. Cash $ 50 Account payable $ 500

Inventory Paid-in capital 1,000 ($300 + $500) 800 Retained earnings 150 Equipment 800

Total $1,650 Total $1,650

The meaning of retained earnings was explained above. Purchases on “open account”

usually create a general liability; that is, the trade creditors usually hold only general claims against the total assets, not specific claims against particular assets (such as mortgages on buildings). In sum, both the creditors and the owners hold general claims against the assets. Of course, if the corporation is liquidated (all assets converted to cash to be distributed to claimants), the creditors’ general claims must be satisfied before the owners get one dollar. Thus, the stockholders are said to have a residual claim or residual interest.

2-34 (15-25 min.)

See Exhibit 2-34 on the following page.

Chapter 2 Measuring Income to Assess Performance 31

2-35 (15-20 min.)

1. First calculate stockholders’ equity from the asset and liability amounts given.

Assets –Liabilities = Stockholders’ equity Dec. 31: £126,000 –£55,000 = £71,000

Jan. 1: 110,000 – 50,000 = 60,000

Change: £ 16,000 –$ 5,000 = £11,000

Note that the £16,000 asset increase less the £5,000 liability increase yields the increase in stockholders’ equity of £11,000.

2. We can use knowledge of what changes stoc kholders’ equity to “deduce” the amount of

net income. Net income increases stockholders’equity and dividends decrease stockholders’ equity.

Beginning stockholders’ equity + net income – dividends = ending stockholders’ equity £60,000 + net income – £5,000 = £71,000

net income = £71,000 + £5,000 – £60,000

= £16,000

3. Sales – Cost of goods sold – Operating expense = Net income

£354,000 –Cost of goods sold – £200,000 = £16,000

–Cost of goods sold = £16,000 + £200,000 –£354,000

Cost of goods sold = £138,000

2-36 (15 min.)

The cash balance on June 30 was $55,000, as shown in the balance sheet equation

transactions in Exhibit 2-36 on the next page. The cash balance is the only beginning or ending balance that is available from the data.

2-37 (10-15 min.)

1. The name of the statement is antiquated. It should be titled income statement (or

statement of earnings, statement of operations, or operating statement).

2. The line with the date should not be for an instant of time but for an indicated span of

time: a year, a quarter, or a month ending on December 31, 20X0.

3. Increases in market values of land and buildings are not recognized under U. S. GAAP.

4. Dividends are not expenses and are not deducted before net profit is computed.

5. The appropriate deduction is the cost of goods sold, not the cost of the cars purchased.

6. The bottom line should be titled net income or net earnings.

7. The cost of the products sold is usually listed right after revenue, not near the bottom of

the statement.

8. Although it is not the major point of the problem, the income statement has apparently

omitted some expenses; for example, neither rent nor depreciation is shown. As a minimum, one or the other would ordinarily be included.

Chapter 2 Measuring Income to Assess Performance 33

2-38 (5-10 min.) Amounts are in millions.

1.

Revenues $3,275.4

Expenses 3,462.1

Net income (loss) $ (186.7)

Beginning retained earnings $250.5

+ Net income (loss) (186.7)

– Dividends ?

Ending retained earnings $ 63.8

2. Dividends = $6

3.8 – $250.5 + $186.7 = $0

2-39 (20-30 min.) Amounts are in thousands of dollars.

The basic relations used in these problems are as follows:

Revenues – Expenses = Net income

Assets = Liabilities + Stockholders’ equity

Beginning retained earnings + Net income – Dividends = Ending retained earnings

Beginning paid-in-capital + additional investment = Ending paid-in-capital.

1. E = 165 – 125 = 40

D = 30 + 40 = 70

C = 15 because there were no additional investments by stockholders

A = 80 – 15 – 30 = 35; or 80 – (15 + 30) = 35

B = 95 – 15 – 70 = 10; or 95 – (15 + 70) = 10

2. K = 20 + 200 = 220

J = 60 + 20 – 7 = 73

H = 10 + 40 = 50

F = 60 + 10 + 90 = 160

G = 280 – 73 – 50 = 157

3. P = 280 – 250 = 30

Q = 120 + 30 – 130 = 20

N = 85 – 35 = 50

L = 105 + 50 + 120 = 275

M = 95 + 85 + 130 = 310

2-40 (10-15 min.)

This is straightforward. Computations are in millions of dollars:

A = 23,185 – 6,406 = 16,779

B = 11,203 – 646 = 10,557

C = 962 + 646 – 420 = 1,188

D = 17,890+ 7,069 = 24,959

Chapter 2 Measuring Income to Assess Performance 35

2-41 (10 min.)

1. Companies choose what details to report based partly on materiality. A $250,000

investment is definitely material to Dayton Service Stations. It is 27% of its total assets

before the investment. However, it is not necessarily material to ExxonMobil—it is a

very small fraction of 1% of its total assets and even a smaller fraction of its net income.

2. A key question a company must ask is whether a potential investor would find the

information relevant for assessing the position and prospects of the company. The

investment would certainly be an important factor in assessing Dayton Service Stations,

but it would be so small as to be insignificant for assessing ExxonMobil.

2-42 (10-15 min.)

1. Income statement or operating statement is used instead of statement of income and

expenses.

2. The end of the fiscal year is typically identified.

3. The terms income or profit are used rather than surplus (and net income rather than net

surplus).

4.The term loss is used instead of deficit.

5. A profit-seeking organization would not receive a subsidy.

2-43 (10-15 min.)

This problem demonstrates how financial statements provide information for investor decisions. These ratios are compared with other companies in the industry and with the company’s ratios through the years.

1. EPS = £364,000,000 ÷ 1,611,000,000 = £0.226

2. P-E = £6.000 ÷ £0.226 = 26.5

3. Dividend Yield = (£295 ÷ 1,611) ÷ £6.000 = 3.1%

4. Dividend Payout = (£295 ÷ 1,611) ÷ £0.226 = 81%

36

2-44 (10-15 min.)

1. $23,931,000,000 ÷ $11.74 = 2,038,415,673 average shares

2. $11.74 × .2155 = $2.53; this is much less than the $11.74 EPS.

3. (a) $2.53 ÷ $76.50 = 3.3% dividend yield

(b) $76.50 ÷ $11.74 = 6.5 P-E ratio

2-45 (20-30 min.)

1 and 2. See Exhibit 2-45 on the following page.

3. R. J. SEN CORPORATION

Income Statement

For the Month Ended June 30, 20X0

Accrual Basis Cash Basis

Sales $115,000 Revenue (cash collected

from customers*) $ 45,000 Deduct: Cost of Expenses (cash disbursed

goods sold 60,000 for merchandise) 85,000

Net cash used by

Net income $ 55,000 operating activities $(40,000)

*The entire revenue is cash sales. If any cash had been collected from credit customers during June, it would be added here.

The accrual basis provides a better measure of the economic accomplishments and efforts of the entity. The cash basis is inferior because it fails to recognize revenue as earned (the sales on credit), and it often recognizes expenses before they help generate revenues (for example, inventory acquired but not sold). Note that the June 28 acquisition of inventory on open account is irrelevant under both the accrual and cash basis.

Chapter 2 Measuring Income to Assess Performance 37

1. The first two items in the first sentence of the footnote (i.e., reference to persuasive

evidence of an arrangement and delivery) relate to the earning of the revenue, and the last two (i.e., fee fixed and determinable and collectability probable) relate to its realization.

Microsoft used to recognize revenue on products licensed to OEMs when the OEMs

shipped product to customers, based on the assumption that Microsoft does not earn the revenue until the product actually is sent to a final customer. However, a change in

licensing earlier this decade made it possible to regard revenue as earned when Microsoft ships product to the OEMs. The licensing agreement may have been changed to make the OEMs more responsible for the products after Microsoft ships them. Microsoft decided not to wait until the OEM delivers product to customers to regard the revenue as earned;

instead, it is deemed earned at the time Microsoft ships it. This accelerates Microsoft’s recognition of revenues.

2. Multi-year licensing agreements are treated as a magazine publisher would treat a

subscription. The revenue is not earned until the customer uses the software for which it has a licensing agreement. Therefore, revenue recognition is spread over the life of the

license.

3. Revenue related to games published by third parties is recognized when the games are

manufactured, not when they are shipped to customers. Microsoft must believe that it

sells the right to manufacture the games, and as soon as the manufacturing process is

complete its revenue-earning process is complete.

Chapter 2 Measuring Income to Assess Performance 39

1. See Exhibit 2-47 on the following page.

Transactions 8 to 11 illustrate the culmination of the asset acquisition-asset expiration sequence: that is, most assets are “stored” as “unexpired” or “prepaid” costs that are expected to benefit future operations (inventory, prepaid rent, prepaid insurance and equipment). As these assets are “used up” or “expire,” they become expenses or “expired costs.”

2. MONTERO COMPANY

Income Statement

For the Month Ended July 31, 20X2

Sales $205,000

Deduct expenses:

Cost of goods sold $160,000

Rent 5,000

Depreciation 2,000

Insurance 1,000

Total expenses 168,000

Net income $ 37,000

3. MONTERO COMPANY

Balance Sheet

July 31, 20X2

Liabilities and

Assets Stockholders’ Equity

Liabilities:

Cash $ 126,000 Note payable $ 60,000 Accounts receivable 140,000 Accounts payable 110,000 Merchandise inventory 65,000 Total liabilities 170,000 Prepaid rent 55,000 Stockholders’ equity:

Prepaid insurance 23,000 Paid-in capital 300,000 Equipment 98,000 Retained earnings 37,000

Total stockholders’ equity 337,000 Total assets $507,000 Total liab. and stk. equity $507,000 40

2-48 (35-40 min.)

1. See Exhibit 2-48 on the following page.

2. BEKELE COMPANY

Balance Sheet

April 30, 20X2

Liabilities and

Assets Stockholders’ Equity

Liabilities:

Cash $106,000 Note payable $ 24,000 Accounts receivable 57,000 Accounts payable 5,000 Merchandise inventory 43,000 Total liabilities 29,000 Prepaid rent 4,000 Stockholders’ equity:

Equipment and fixtures 35,000 Paid-in capital $200,000

Retained earnings 16,000

Total stk. equity $216,000 Total $245,000 Total $245,000

BEKELE COMPANY

Income Statement

For the Month Ended April 30, 20X0

Sales revenue $100,000

Deduct expenses:

Cost of goods sold $37,000

Wages and sales commissions 34,000

Rent ($2,000 + $10,000) 12,000

Depreciation 1,000

Total expenses 84,000 Net Income $16,000 3. Most businesses tend to have net losses during their infant mont hs, so Bekele’s ability

to show a net income for April is impressive. Indeed, the rate of return on beginning

investment is ($16,000 ÷ $200,000) = 8% per month, or 96% per year. Bekele also has

high stockholders’ equity compared to its liabilities, quite a high cash balance, and

flexibility because most assets are either in cash or will be turned into cash relatively

quickly. Many other points can be raised, including the problem of maintaining an

“optimum” cash balance so that creditors can be paid neither too quickly nor too slowly.

See the next solution also.

42

2-49 (5-10 min.)

Cash Inflows:

Cash sales $ 25,000

Cash collected from credit customers 18,000

Cash disbursements:* 43,000 Disbursements for merchandise $(75,000)**

Disbursements for rent, wages,

and sales commissions (50,000)***

Total cash disbursements 125,000

Net cash outflow for operations $(82,000) *Some students will also include the $12,000 cash paid to purchase equipment as a cash outflow. This is consistent with a strict cash-basis of accounting.

**$45,000 + $30,000

*** $6,000 + $10,000 + $34,000

The accrual basis provides a more accurate measure of economic performance. If the two revenue recognition criteria are met (earning and realization), the $100,000 measure of revenue on the accrual basis is preferred to the $43,000 measure of cash receipts for measuring economic performance, and the $84,000 measure of costs is preferred to the $125,000 measure of cash disbursements. The $16,000 net income is a more accurate measure of total accomplishments for April than is the $82,000 net cash outflow for operations.

44

2016年10月高等教育自学考试全国统一命题考试 高级财务会计试卷 一、单项选择题 1、某企业的记账本位币为美元,根据我国会计准则规定,下列说法中错误的是( C ) A.该企业日常核算使用的货币为美元 B.该企业的财务报表需要折算为人民币 C.该企业以美元计价和结算的交易属于外币交易 D.该企业以人民币计价和结算的交易不属于外币交易 2、根据我国会计准则规定,企业实际收到的外币投资额在折算为记账本位币时,应采用的汇率是( B ) A.合同约定汇率 B.交易发生日即期汇率 C.资产负债表日即期汇率 D.交易发生日即期汇率的近似汇率 3、甲、乙公司均为房地产开发企业,甲公司与乙公司进行合并,合并后的法人资格均保留,这种合并方式称为( A ) A.横向合并 B.新设合并 C.纵向合并 D.混合合并 4、企业集团内部甲子公司以发行股票方式对乙子公司进行吸收合并,在合并过程中为发行股票而发生的佣金等相关费用,应于发生时计入(C ) A.财务费用 B.管理费用 C.资本公积 D.投资收益 5、编制合并财务报表时,下列各项中不属于子公司必须提供的资料是(A ) A.子公司管理人员的薪酬 B.子公司与母公司不一致的会计期间的说明 C.子公司所有者权益变动和利润分配的相关情况 D.子公司采用的与母公司不一致的会计政策及其影响金额 6、非同一控制下的控股合并中,如果合并日被合并企业固定资产的公允价值高于其账面价值,在编制控制权取得日后首期合并财务报表时,正确的处理方法是( C ) A.在账簿中将固定资产的账面价值调整为公允价值并增加资本公积 B.在账簿中将固定资产的账面价值调整为公允价值并增加营业外收入

第二章货币资金 (一)单项选择题 1.不包括在现金使用范围内的业务是()。D A.支付职工福利费 B.结算起点以下的零星支出 C.向个人收购农副产品 D.支付银行借款利息 2.结算起点以下的零星支出的结算起点是()。 C A.1500元 B.500元 C.1000元 D.2000元 3.不包括在广义现金范围内的项目是()。D A.银行存款 B.个人支票 C.保付支票 D.职工借款欠条 保付支票为了避免出票人开空头支票,收款人或持票人可以要求付款行在支票上加盖“保付”印记,以保证到时一定能得到|银行付款。 4.实行定额备用金制度,报销时的会计分录是()。 A A.借记"管理费用",贷记"库存现金" B.借记"备用金",贷记"库存现金" C.借记"管理费用",贷记"备用金" D.借记"库存现金",贷记"备用金" 5.确定企业库存现金限额时,考虑的天数最多不能超过()。 C A.5天 B.1O天 C.15天 D.8天 6.在企业开立的诸多账户中,可以办理提现业务,以发放工资的是()。D A.专用存款账户 B.一般存款账户 C.临时存款账户 D.基本存款账户 7.在企业的银行账户中,不能办理现金支取的账户是()。D A.基本存款账户 B.临时存款账户 C.专用存款账户 D.一般存款账户 8.银行汇票的提示付款期限为自出票日起()。 A A.l个月 B. 3个月 C.4个月 D.6个月 9.银行本票的提示付款期限自出票日起最长不超过()。 A A.2个月 B.6个月 C.l个月 D.3个月 10.支票的提示付款期限为自出票日起()。 A A.10天 B.5天 C.3天 D.6天 11.在下列项目中,不属于其他货币资金的是()。 A A.向银行申请的银行承兑汇票

此文档下载后即可编辑 (1)出售产品5件,价款600元,增值税102元,收到现金702元。借:库存现金702 贷:主营业务收入600 应交税费-----应交增值税(销项税额)102 (2)厂办主任王平因公外出,预借差旅费1500元,以现金支付。 借:其他应收款------备用金(王平)1500 贷:库存现金1500 (3)职工李红交回欠款500元。 借:库存现金500 贷:其他应收款-------其他应收暂付款(李红)500 4 大明公司现金清查,发现短缺360元,经查实,其中160元属于出纳员小王的责任,应由其赔偿,赔款尚未收到,另外200元无法查明原因,经批准作为管理费用处理。 借:待处理财产损溢-----待处理流动资产损溢360 贷:库存现金360 借:其他应收款------其他应收暂付款(小王)160 管理费用200 贷:待处理财产损溢-----待处理流动资产损溢360 5大明公司现金清查,发现库存现金溢余270元,经查实200元为多收A公司货款,其中70元无法查明原因,经批准作为营业外收入。 借:库存现金270

贷:待处理财产损溢-----待处理流动资产损溢270 借:待处理财产损溢-----待处理流动资产损溢270 贷:其他应付款-----其他应付暂收款(A公司) 200 营业外收入70 6大明公司收回A公司以转账支票偿还前欠货款1.8万元 借:银行存款18000 贷:应收账款-----A公司18000 7大明公司前欠天一公司货款15万元,现以信汇方式付款 借:应付账款-----天一公司150000 贷:银行存款150000 8甲企业为增值税一般纳税人,向银行申请办理银行汇票用以购买原材料,将款项250 000元交存银行转作银行汇票存款。根据银行盖章退回的申请书存根联: 借:其他货币资金——银行汇票存款250 000 贷:银行存款250 000 9甲企业购入原材料一批,取得的增值税专用发票上的原材料价款为200 000元,增值税税额为34 000元,已用银行汇票办理结算。 借:原材料200 000 应交税费——应交增值税(进项税额)34 000 贷:其他货币资金——银行汇票存款234 000 10甲企业于3月5日向银行申领信用卡,向银行交存50 000元。 借:其他货币资金——信用卡存款50 000

自学考试高级财务会计试题

全国10月高等教育自学考试 高级财务会计试题 课程代码:00159 一、单项选择题(在每小题的四个备选答案中选出一个正确答案,并将其号码填在题干的括号内。每小题1分,共20分) 1.财务会计以对外报告为主要目标,以( )为最终目的。 A.编制企业通用会计报表 B.强化企业内部管理 C.建立企业内部控制制度 D.规范企业会计核算 2.期末编制资产负债表时,可列示在资产负债表流动负债“其它负债”项目中的是( ) A.“递延升水”帐户的借方余额 B.“递延升水”帐户的贷方余额 C.“递延贴水”帐户的借方余额 D.“汇兑损益”帐户的借方余额 3.采用纳税影响会计法时,企业一定会计期间发生的时间性差异的所得税影响金额,在期末时应当在资产负债表反映的项目是( ) A.其它应付款 B.其它应收款

C.递延税款 D.应交税金 4.采用递延法核算所得税时,以前各期发生的而在本期转销的各项时间性差异影响纳税的金额,按照( )计算转销。 A.现行税率 B.新税率 C.原发生时的税率 D.平均税率 5.以融资租赁为主并以专业公司从事业务活动为特点的租赁是( ) A.古代租赁 B.近代租赁 C.现代租赁 D.当代租赁 6.租赁公司以承租人身份与设备供货厂商直接签订租赁合同,租赁公司再以出租人的身份与用户签订转租合同的租赁业务,是属于( ) A.售后租赁业务 B.经营租赁业务 C.转租赁业务 D.融资租赁业务 7.“未实现租赁收益”科目,是出租人为核算其融资租赁业务而设置的( )类会计科目。 A.资产 B.负债 C.收入 D.所有者权益

8.下列行为,不属于房地产开发行为的是( ) A.征用土地 B.土地使用权的转让 C.折迁安置 D.委托规划设计 9.企业从事土地开发经营活动中获得的土地使用权,应当( ) A.计入期间费用 B.计入受益开发产品成本 C.作为无形资产核算 D.计入资本公积 10.在房地产企业会计核算中,“销售费用”科目期末( ) A.可能没有余额 B.可能有借方余额 C.可能有贷方余额 D.一定没有余额 11.采有购买法编制控制权取得日合并会计报表时,母公司购买子公司的成本与子公司帐面价值之间的差额作为( ) A.实收资本处理 B.合并价差处理

全国自考高级财务会计试题及答案

10月高等教育自学考试全国统一命题考试 高级财务会计试卷 一、单项选择题 1、某企业的记账本位币为美元,根据中国会计准则规定,下列说法中错误的是( C ) A.该企业日常核算使用的货币为美元 B.该企业的财务报表需要折算为人民币 C.该企业以美元计价和结算的交易属于外币交易 D.该企业以人民币计价和结算的交易不属于外币交易 2、根据中国会计准则规定,企业实际收到的外币投资额在折算为记账本位币时,应采用的汇率是( B ) A.合同约定汇率 B.交易发生日即期汇率 C.资产负债表日即期汇率 D.交易发生日即期汇率的近似汇率 3、甲、乙公司均为房地产开发企业,甲公司与乙公司进行合并,合并后的法人资格均保留,这种合并方式称为( A ) A.横向合并 B.新设合并 C.纵向合并 D.混合合并 4、企业集团内部甲子公司以发行股票方式对乙子公司进行吸收合并,在合并过程中为发行股票而发生的佣金等相关费用,应于发生时计入(C ) A.财务费用 B.管理费用 C.资本公积 D.投资收益 5、编制合并财务报表时,下列各项中不属于子公司必须提供的资料是(A ) A.子公司管理人员的薪酬 B.子公司与母公司不一致的会计期间的说明 C.子公司所有者权益变动和利润分配的相关情况 D.子公司采用的与母公司不一致的会计政策及其影响金额 6、非同一控制下的控股合并中,如果合并日被合并企业固定资产的公允价值高于其账面价值,在编制控制权取得日后首期合并财务报表时,正确的处理方法是( C ) A.在账簿中将固定资产的账面价值调整为公允价值并增加资本公积 B.在账簿中将固定资产的账面价值调整为公允价值并增加营业外收入

中级财务会计第二章:货币资金 1货币资金:是企业在生产经营过程中停留在货币形态的那部分资金,是可以立即投入流通,用以购买商品或 劳务,或用以偿还债务的交换媒介物。货币资金是企业资产中流动性最强的一类(包括现金、银行存款和其他 货币资金) 2现金的管理与核算 现金的定义:是指存于企业用于日常零星开支的现钞。广义的现金包括库存现金、银行活期存款、银行本 票、银行汇票、信用证存款、信用卡存款等内容;狭义的现金即库存现金。 现金的使用范围:企业可以使用现金的范围主要包括: (1)职工工资、津贴;(2)个人劳动报酬; (3)根据国家规定颁发给个人的科学技术、文化艺术、体育等各种奖金; (4)各种劳保、福利费用以及国家规定的对个人的其他支岀等; (5)向个人收购农副产品和其他物资的价款;(6)岀差人员必须随身携带的差旅费; (7)结算起点(现行规定为1 000元)以下的零星支岀;(8)中国人民银行确定需要支付现金的其他支岀。库存现金限额P54 (1)企业的库存现金限额由其开户银行根据实际需要核定,一般为三至五天的零星开支需要量。 (2)边远地区和交通不便地区的企业,库存现金限额可以多于五天,但不能超过十五天的日常零星开支量。 (3)企业必须严格按规定的限额控制现金结余量,超过限额的部分,必须及时送存银行,库存现金低于限额 时,可以签发现金支票从银行提取现金,以补足限额。 现金日常收支管理P54 (1)现金收入应于当日送存银行,如当日送存银行确有困难,由银行确定送存时间;(余款当日送存) (2)企业可以在现金使用范围内支付现金或从银行提取现金,但不得从本单位的现金收入中直接支付(坐支),因特殊情况需要坐支现金的,应当事先报经开户银行审查批准,由开户银行核定坐支范围和限额。企业 应定期向开户银行报送坐支金额和使用情况;(不许____________ (3)企业从银行提取现金时,应当在取款凭证上写明具体用途,并由财会部门负责人签字盖章后,交开户银行审核后方可支取;(支票填写规范) (4)贯彻“九不准”的规定 3银行存款开户管理与核算 银行存款开户管理 (1)基本存款户:是企业办理日常结算及现金支取的账户,按照规定,企业发放工资、奖金等需要支取的现金,只能通过基本存款账户办理。 (2)一般存款户:是企业为了业务方便在银行或金融机构开立的基本存款户以外的账户,该类账户主要用于银行借款的转存以及与开立基本存款账户的企业不在同一地点的附属非独立核算的单位开立的账户,按规 定,企业可以通过一般存款户办理转账结算和现金缴存,但不得支取现金。 (3)临时存款户:是因企业的临时业务活动需要而开立的暂时性账户,企业可以通过此类账户办理转账结算以及按照现金管理的规定办理现金收付。 (4)专用存款户:是企业因特定用途需要开立的具有特定用途的账户 银行存款结算管理P61 四票(支票、银行汇票、商业汇票和银行本票)、一卡(信用卡)、三方式(托收承付、委托收款和汇兑)、一证(信用证)、一款(存岀投资款) 支票:含义一一是岀票人(银行的存款人)签发的,委托办理支票存款业务的银行在见票时无条件支付确定金额给收款人或持票人的票据。 特点一一①现金支票(只能从银行提现)、转账支票(只能从银行转账)、普通支票②有效期:不超过10

财务会计分录题及答案集团档案编码:[YTTR-YTPT28-YTNTL98-UYTYNN08]

(1)出售产品5件,价款600元,增值税102元,收到现金702元. 借:库存现金 702 贷:主营业务收入 600 应交税费-----应交增值税(销项税额)102 (2)厂办主任王平因公外出,预借差旅费1500元,以现金支付. 借:其它应收款------备用金(王平) 1500 贷:库存现金 1500 (3)职工李红交回欠款500元. 借:库存现金 500 贷:其它应收款-------其它应收暂付款(李红) 500 4 大明公司现金清查,发现短缺360元,经查实,其中160元属于出纳员小王责任,应由其赔偿,赔款尚未收到,另外200元无法查明原因,经批准作为管理费用处理. 借:待处理财产损溢-----待处理流动资产损溢 360 贷:库存现金 360 借:其它应收款------其它应收暂付款(小王) 160 管理费用 200 贷:待处理财产损溢-----待处理流动资产损溢 360 5大明公司现金清查,发现库存现金溢余270元,经查实200元为多收A公司货款,其中70元 无法查明原因,经批准作为营业外收入. 借:库存现金 270 贷:待处理财产损溢-----待处理流动资产损溢 270 借:待处理财产损溢-----待处理流动资产损溢 270 贷:其它应付款-----其它应付暂收款 (A公司) 200 营业外收入 70 6大明公司收回A公司以转账支票偿还前欠货款1.8万元 借:银行存款 18000 贷:应收账款 -----A公司 18000 7大明公司前欠天一公司货款15万元,现以信汇方式付款 借:应付账款-----天一公司 150000

高级财务会计第版练习 题答案 Revised by Chen Zhen in 2021

第1章所得税费用 一、单项选择题 1.【2014年注册会计师考试《会计》试题】甲公司本期的会计利润210万元,本期有国债收入10万元,本期有环保部门罚款20万元,另外,已知固定资产对应的递延所得税负债年初金额为20万元,年末金额为25万元。甲公司本期的所得税费用金额为( )万元。 A. 50 B. 60 C. 55 D. [答案]:C [解析]:应交所得税=[210-10+20-5/25%]*25%=50(万元),递延所得税负债的当期发生额=25-5=5(万元),所得税费用=50+5=55(万元)。 2.【2012年中级职称试题】2011年12月31日,甲公司因交易性金融资产和可供出售金融资产的公允价值变动,分别确认了10万元的递延所得税资产和20万元的递延所得税负债。甲公司当期应交所得税的金额为150万元。假定不考虑其他因素,该公司2011年度利润表“所得税费用”项目应列示的金额为()万元 A. 120 B. 140 C. 160 D. 180 【参考答案】B 二、多项选择题 1.【2012年中级职称试题】下列各项中,能够产生应纳税暂时性差异的有()。 A.账面价值大于其计税基础的资产 B.账面价值小于其计税基础的负债 C.超过税法扣除标准的业务宣传费 D.按税法规定可以结转以后年度的为弥补亏损 【参考答案】AB 2.【2010年注册会计师考试专业阶段试题】甲公司20×9年度涉及所得税的有关交易或事项如下: (1)甲公司持有乙公司40%股权,与丙公司共同控制乙公司的财务和经营政策。甲公司对乙公司的长期股权投资系甲公司20×7年2月8日购入,其初始投资成本为3 000万元,初始投资成本小于投资时应享有乙公司可辨认净资产公允价值份额的差额为400万元。甲公司拟长期持有乙公司股权。根据税法规定,甲公司对乙公司长期股权投资的计税基础等于初始投资成本。 (2)20×9年1月1日,甲公司开始对A设备计提折旧。A设备的成本为8 000万元,预计使用10年,预计净残值为零,采用年限平均法计提折旧。根据税法规定,A设备的折旧年限为16年。假定甲公司A设备的折旧方法和净残值符合税法规定。 (3)20×9年7月5日,甲公司自行研究开发的B专利技术达到预定可使用状态,并作为无形资产入账。B专利技术的成本为4 000万元,预计使用10年,预计净残值为零,采用直线法摊销。根据税法规定,B专利技术的计税基础为其成本的150%。假定甲公司B专利技术的摊销方法、摊销年限和净残值符合税法规定。 (4)20×9年12月31日,甲公司对商誉计提减值准备1 000万元。该商誉系20×7年12月8日甲公司从丙公司处购买丁公司100%股权并吸收合并丁公司时形成的,初始计量金额为3 500万元,丙公司根据税法规定已经缴纳与转让丁公司100%股权相关的所得税及其他税费。根据税法规定,甲公司购买丁公司产生的商誉在整体转让或者清算相关资产、负债时,允许税前扣除。 (5)甲公司的C建筑物于20×7年12月30日投入使用并直接出租,成本为6 800万元。甲公司对投资性房地产采用公允价值模式进行后续计量。20×9年12月31日,已出租C建筑物累计公允价值变动收益为1 200万元,其中本年度公允价值变动收益为500万元。根据税法规定,已出租C建筑物以历史成本按税法规定扣除折旧后作为其计税基础,折旧年限为20年,净残值为零,自投入使用的次月起采用年限平均法计提折旧。甲公司20×9年度实现的利润总额为15 000万元,适用的所得税税率为25%。假定甲公司未来年度有足够的应纳税所得额用于抵扣可抵扣暂时性差异。 要求:根据上述资料,不考虑其他因素,回答下列第(1)小题至第(2)小题。 (1)下列各项关于甲公司上述各项交易或事项会计处理的表述中,正确的有()。 A.商誉产生的可抵扣暂时性差异确认为递延所得税资产 B.无形资产产生的可抵扣暂性差异确认为递延所得税资产 C.固定资产产生的可抵扣暂时性差异确认为递延所得税资产

第二章货币资金 一、单项选择题 1.不属于其他货币资金的是()。 A.在途货币 B.存出投资款 C.外币存款 D.银行汇票存款 2.除现金流量表以外,我国会计上所界定的现金概念指的是企业的()。 A.库存现金 B.银行存款 C.其他货币资金 D.有价证券 3.企业平时若发现现金长款,在查明原因以前应计入()。 A.营业外收入 B.其他业务收入 C.其他应付款 D.应付账款 4.企业平时若发现现金短款,在查明原因以前应计入()。 A.营业外支出 B.其他业务成本 C.其他应收款 D.应收账款 5.除中国人民银行另有规定外,支票的提示付款期限一般为自出票日起()。 A.7天 B.10天 C.15天 D.20天 6.既可用于同城结算,又可用于异地结算的结算方式是()。 A.汇兑 B.银行本票 C.委托收款 D.支票 7.商业汇票承兑期限由交易双方商定,最长不超过()个月。 A.九 B.三 C.六 D.十二 8.不正确的说法是()。 A.企业收入现金应于当日送存开户银行 B.企业与其他单位的经济往来,除在规定的范围可以使用现金外,应通过开户银行进行转账结算 C.企业可用现金收入支付现金支出 D.企业从开户银行提取现金必须写明真实用途 二、多项选择题 1.符合现金管理有关规定的事项是()。 A.企业对于当日送存现金有困难的,由开户银行确定送存时间 B.因特殊情况还需要坐支现金的,应当事先报经开户银行审批 C.企业从开户银行提取现金,应由本单位出纳人员签字盖章 D.如果现金长短款是由于单据丢失或记账产生的差错,应补办手续入账或更正错误 2.货币资金管理和控制的原则有()。 A.职责分工 B.交易分开 C.内部稽核 D.定期换岗

会计分录练习题及答案 一、东方公司为增值税一般纳税人工业企业,2001年月12月份发生下列业务: 1、开出现金支票从银行提取现金2000元备用; 借:库存现金 2000 贷:银行存款 2000 2、用现金支付生产车间办公用品费440元; 借:制造费用 440 贷:库存现金 440 3、收到盛达公司前欠货款80000元,存入银行; 借:银行存款 80000 贷:应收账款---盛达公司 80000 4、向前进工厂销售A产品一批,不含增值税的售价为100000元,增值税17000元,款项尚未收到; 借:应收账款---前进工厂 117000 贷:主营业务收入 100000 应交税费—应交增值税(销项税) 17000 5、接到开户银行的通知,收到光明公司前欠货款150000元; 借:银行存款 150000 贷:应收账款---光明工厂 150000 6、向大华公司销售B产品一批,不含增值税的售价为200000元,增值税为34000元,合计234000元, 当即收到大华公司签发并承兑的面值为234000元,期限为三个月的商业汇票一张; 借:应收票据--大华公司 234000 贷:主营业务收入 200000 应交税费—应交增值税(销项税额) 34000 7、接到开户银行的通知,胜利工厂签发并承兑的商业汇票已到期,收到胜利工厂支付的票据款120000元; 借:银行存款 120000 贷:应收票据--胜利工厂 120000 8、向宏达公司购买一批甲材料,按合同规定,东方公司用银行存款预付购货款50000元; 借:预付账款--宏达公司 50000 贷:银行存款 50000 9、接上题,收到宏达公司发来的甲材料一批,增值税专用发票上注明的买价为80000元,增值税为13600 元,合计93600元。扣除预付款50000元,余额43600元东方公司用银行存款支付,甲材料已验收入库; 借:原材料—甲材料 80000 应交税费—应交增值税(进项税额) 13600 贷:预付账款--宏达公司 93600 借:预付账款 43600 贷:银行存款 43600 10、厂部办公室张强因公出差,预借差旅费800元,付以现金; 借:其他应收款--张强 800 贷:库存现金 800 11、张强出差回来,向公司报销差旅费700元,余款交回现金; 借:管理费用 700 库存现金 100 贷:其他应收款--张强 800 12、向科达公司购进甲材料一批,增值税专用发票上注明的买价为500000元,增值税85000元,价税合计

2018 年 4 月高等教育自学考试全国统一命题考试 高级财务会计试卷 ( 课程代码 00159) 本试卷共7 页,满分l00 分,考试时间l50 分钟。 考生答题注意事项: 1.本卷所有试题必须在答题卡上作答。答在试卷上无效,试卷空白处和背面均可作草稿纸。2.第一部分为选择题。必须对应试卷上的题号使用2B 铅笔将“答题卡”的相应代码涂黑。3.第二部分为非选择题。必须注明大、小题号,使用0. 5 毫米黑色字迹签字笔作答。4.合理安排答题空间, 超出答题区域无效。 第一部分选择题 一、单项选择题:本大题共20 小题,每小题 l 分,共 20 分。在每小题列出的备选项中只有一 项是最符合题目要求的,请将其选出。 1.根据我国会计准则规定,外币应付账款由于汇率变动所产生的汇兑差额应计入 A .财务费用B.库存商品 C.投资收益D.主营业务收入 2.采用货币与非货币项目法对外币财务报表进行折算时,下列项目中应按现行汇率折算的是 A .存货B.无形资产C.应收账款D.实收资本 3.两家或两家以上的企业联合成立一个新的企业,用新企业的股份交换原来各企业的股份,这一合并按照法律形式分类属于 A .新设合并B.吸收合并C.控股合并D.混合合并 4.下列各项中,不属于同一控制下企业合并表外披露内容的是 A.同一控制下企业合并的判断依据 B.合并合同或协议中约定的将承担的或有负债情况 C.被合并方上一会计年度资产负债表日以及合并日的公允价值 D.被合并方自合并当期期初至合并日的收入、净利润和现金流量等情况 5.编制合并财务报表时,将非全资子公司的少数股东权益视为整个集团的负债,少数股东享有的净收益视为一项费用,这一处理体现的合并理论是 A .实体理论B.母公司理论C.子公司理论D.所有权理论 6.下列各项中,不属于合并财务报表编制原则的是 A .一体性原则8.真实性原则 C .汇总性原则D.以个别财务报表为基础 7.如果乙公司是甲公司同一控制下的非全资子公司,则下列各项影响合并财务报表中 少数股东权益数额的是 A .乙公司的赊销政策B.甲公司实现的净利润

2018年高级财务会计试题及答案 第1题:并购方在并购完成后,可能无法使整个企业集团产生经营协同效应、财务 协同效应、市场份额效应,难以实现规模经济和经验共享互补的风险是指(A). A.营运风险 B.信息风险 C.融资风险 D.体制风险 第3题:下列企业价值估价方法中,哪项属于市场价值法?(D) A.期权定价模型 B.折现现金流量模型 C.经济利润模式

D.托宾的Q模型 第5题:资本经营效果的评价人应该是(B). A.经营者 B.出资人 C.监事会 D.企业职工 第7题:某分公司目前总资产为1750万元、年利润为200万元,其总公司的资A人 本为9?则该分公司的剩余收益为(A)。 A.42.5万元

B.250万元 C.1732万元 D.4250万元 第9题:下列关于控股式企业集团,说法不正确的是(D)。 A.设立目的是为了掌握子公司的股份 B.设立目的是为控制子公司的股权 大.母公司不直接参与子公司生产经营活动 D.母公司既从事股权控制,又直接进行生产经营 第11题:企业集团财务公司最本质的功能是(A)。 A.融资中心

B.信贷中心 C.结算中心 D.投资中心 第13题:企业价值型管理更关注企业的(B)。 A.利润管理 B.现金流量管理 C.收益管理 D.风险管理 第15题:处于初创期企业的筹资战略应为(D)。 A.相对稳健型的筹资战略

B.激进型的筹资战略 C.高负债率的筹资战略 D.权益资本型的筹资战略 第17题:并购企业测算并购后使被并购企业健康发展而需支付的成本,称为(A)。 A.整合与营运成本 B.并购完成成本 C.并购退出成本 D.并购机会成本 第19题:最能反映各部门在权限和可控范围内有效利用各种资源、不断提高经济

2015年10月高级财务会计真题 一、单项选择题(本大题共20小题,每小题1分,共20分)在每小题列出的四个备选项中只有一个是符合题目要求的,请将其代码填写在题后的括号内。错选、多选或未选均无分。 1.对于以人民币作为记账本位币的企业,下列交易或事项中,不属于外币交易的是()。 A.以80万元人民币兑换美元 B.以20万美元购入原材料一批 C.为建造一项固定资产借款2000万美元 D.以60万元人民币支付美国子公司员工的薪酬 【答案】D 【解析】外币交易,以非记账本位币计价或者结算的交易,通常包括,买入或者卖出以外币 计价的商品或者劳务;借入或者借出外币资金;其他以外币计价或者结算的交易。 2.下列外币报表折算方法中,最有利于保持原外币报表各项目之间比例关系的是()。 A.时态法 B.现行汇率法 C.流动与非流动项目法 D.货币性与非货币性项目法 【答案】B 【解析】流动与非流动项目法,将资产负债表项目按其流动性划分为流动性项目与非流动项目两大类;货币与非货币性项目,将资产负债表项目划分为货币性项目与非货币性项目;现行汇率法,单一汇率法,采用资产负债表的现行汇率,保持附属公司财务报表原来表述的财务成果和不同报表项目之间的财务比例关系;时态法,也称时间量度法,是指依据资产和负债项目的计价时间分别采用现行汇率或历史汇率。 3.某企业2013年度利润总额为2000万元,其中包括本年收到的国库券利息收入20万元,全年实发工资600万元,均为税法认定的合理职工薪酬,企业所得税税率为25%。假设不考虑其他因素,该企业2013年应交所得税为()。A.345万元 B.495万元 C.500万元 D.505万元 【答案】A 【解析】(2000-20-600)×25%=345万 免税收入:国债利息收入;符合条件的居民企业之间的股息、红利等权益性投资收益;在中国境内设立机构、场所的非居民企业从居民企业取得与该机构、场所

绝密★ 考试结束前 全国2013年10月高等教育自学考试高级财务会计课程代码:00159 选择题部分 1.某公司外币业务采用交易发生日的即期汇率进行折算,按月计算汇兑损益。5月20日因销售产品发生应收账款500万欧元,当日即期汇率为1欧元=10.30元人民币。5月31日的即期汇率为1欧元=10.28元人民币;6月1目的即期汇率为1欧元= 10.32元人民币;6月30日的即期汇率为1欧元=10.35元人民币。7月10日收到该应收账款,当日即期汇率为1欧元=10.34元人民币。该公司6月份应当确认的汇兑收益为人民币(D) 1-28 A.10万元B.15万元 C.25万元D.35万元 计算:资产类项目汇兑损益=期末按市场汇率调整额-期末账面余额 =500万*10.35-500万*10.28=35万 2.我国企业对境外经营的财务报表进行折算时,产生的外币报表折算差额应当(D)1-50 A.作为递延收益列示B.在相关资产类项目下列示 C.在相关负债类项目下列示D.在所有者权益项目下单独列示 3.2010年7月10日,某企业购入一项可供出售金融资产,取得成本为500万元,2010年12月31日其公允价值为400万元。所得税税率为25%。2010年年末该项金融资产对所得税影响的会计处理为(B) 2-96 A.应确认递延所得税负债25万元B.应确认递延所得税资产25万元 C.应转回递延所得税资产25万元D.应转回递延所得税负债25万元 4.下列各项中,不属于 上市公司信息披露内容的是(D)3-128 ... A.招股说明书B.年度报告 C.上市公告书D.公司管理办法 5.下列各项中,属于上市公告书但不属于招股说明书主要内容的是(C)3-129 A.发起人简况B.筹资的目的 C.同业竞争与关联交易D.成立以来的生产经营状况 6.关于经营租赁业务承租人的会计处理,下列做法中正确的是(C)4-197 A.对租入的固定资产视同自有资产计提折旧 B.承租人发生的初始直接费用应计入租入资产成本 C.在租赁开始日租入资产不作为本企业资产计价入账 D.在实际发生或有租金时,应将或有租金计入资本公积 7.下列项目中,属于基础金融工具的是(A)5-230 A.银行存款B.固定资产 C.无形资产D.生物资产 金融期权的是(B)5-234 8.下列项目中,不属于 ...

1、正确答案是:A公司购买B公司20%的股权 2、正确答案是:M公司=N公司+P公司 3、正确答案是:购买合并、股权联合合并 4、正确答案是:控股合并 5、正确答案是:参与合并的企业在合并前后均受同一方或相同的多方最终控制且该控制并非暂时性的 6、正确答案是:购买方为进行企业合并发生的各项直接相关费用也应当计入企业购买成本 7、正确答案是:按照合并日被合并方的账面价值计量 8、正确答案是:400 9、正确答案是:账面价值 10、正确答案是:管理费用 11、正确答案是:存货按照现行重置成本确定 12、正确答案是:在控股合并的情况下,应体现在合并当期的个别利润表 13、正确答案是:1000 14、吸收合并, 控股合并, 新设合并 15、通过法律或协议,获得决定其他企业财务和经济政策的权利, 获得任命或解除其他企业董事会或类似机构大多数成员的权力, 获得其他企业董事会或对等决策团体会议中多数席位的权利, 一个企业的公允价值大大地超过其他参与合并企业的公允价值,则具有较大公允价值的企业是购买方, 如果企业合并是通过以现金换取有表决权的股份来实现,放弃现金的企业是购买方 16、非同一控制下的吸收合并,购买方在购买日应当按照合并中取得的被购买方各项可辨认资产、负债的公允价值确定其入账价值,确定的企业合并成本与取得被购买方可辨认净资产公允价值的差额,应确认为商誉或计入当期损益, 非同一控制下的控股合并,母公司在购买日编制合并资产负债表时,对于被购买方可辨认资产、负债应当按照合并中确定的公允价值列示, 企业合并成本大于合并中取得的被购买方可辨认净资产公允价值份额的差额,确认为合并资产负债表中的商誉, 企业合并成本小于合并中取得的被购买方可辨认净资产公允价值份额的差额,在购买日合并资产负债表中调整盈余公积和未分配利润, 合并方为进行企业合并发生的各项直接相关费用,包括为进行企业合并而支付的审计费用、评估费用、法律服务费用等,于发生时计入管理费用 17、企业合并协议已获股东大会通过, 参与合并各方已办理了必要的财产交接手续, 企业合并事项需要经过国家有关部门审批的,已取得有关主管部门的批准, 合并方或购买方实际上已经控制了被合并方或被购买方的财务和经营政策,并享有相应的利益及承担风险, 合并方或购买方已支付了合并价款的大部分(一般应超过50%),并且有能力支付剩余款项18、非同一控制下的企业合并,购买方为进行企业合并发生的各项直接相关费用应当计入当期损益, 同一控制下的企业合并,合并方为进行企业合并发生的各项直接相关费用,应当于发生时计入当期损益 19、合并方取得的资产和负债应当按照合并日被合并方的账面价值计量, 以支付现金、非现金资产作为合并对价的,发生的各项直接相关费用计入管理费用, 合并方取得净资产账面价值与支付的合并对价账面价值的差额调整资本公积 20、为进行合并而发生的法律服务费用, 为进行合并而发生的会计审计费用, 为进行合并而发生的咨询费、评估费用等 21、购买方为进行企业合并支付的现金, 购买方为进行企业合并付出的非现金资产的公允价值, 购买方为进行企业合并发行的权益性证券在购买日的公允价值, 购买方为进行企业合并发行或承担的债务在购买日的公允价值

会计分录练习题及参考答案 一、练习工业企业供应过程主要经济业务的核算 1 ) 1 日,购入甲材料一批,价款为 100000元,增值 税税率为17% ,税额为17000 元,全部款项已用银行存款支付,材料已验收入库。 借:原材料 --- 甲材料 1 00000 应交税金 --- 应交增值税(进项税额)17000 贷:银行存款117000 2 ) 5 日,购入乙材料一批,增值税专用发票注明的价款为 元,增值税额为34000 元,企业开出商业承 200000 兑汇票一张,票面金额为234000元,材料尚在运输 途中。 借:在途物资 --- 乙材料200000 应交税金 --- 应交增值税(进项税额)34000 贷:应付票据234000 93600 元,材料已验收入库,款项未付(假设不考虑增值税) 3 ) 8 日,购入丙材料一批,价款为合计为 借:原材料 --- 丙材料93 600 贷:应付账款93600 要求:对上述业务作账务处理 二、练习工业企业生产过程主要经济业务的核算 7年 10 月份发生以下有关经济业务 1 )本月仓库共发出甲材料44000 元,其中生产 A 产品领用 16000 元,生产 B 产品领用 11800 元,车间管理 部门耗用 1200 元,行政管理部门耗用 9000 元,对外发出委托加工物资 5000 元,销售部门领用 1000 元。 借:生产成本 --- A 产品16000 ---B 产品11800 制造费用1200 管理费用9000 委托加工物资5000 销售费用1000 贷:原材料 --- 甲材料44000 2 )计提本月职工工资 55000 元,其中 A 产品生产工人工资 23000 元, B 产品生产工人工资 15000 元,车 间管理人员工资2900 元,行政管理人员工资 4100 元,销售部门人员10000 元。 借:生产成本 --- A 产品23000 ---B 产品15000 制造费用2900 管理费用4100 销售费用10000 贷:应付职工薪酬 --- 工资55000 3 )按职工工资总额的 14% 计提职工福利费。(注:具体分配金额按照上题金额分配) 借:生产成本 --- A 产品3220 ---B 产品2100 第1 页共9 页

全国2011年1月自学考试高级财务会计试题及答案 课程代码:00159 一、单项选择题(本大题共20小题,每小题1分,共20分) 在每小题列出的四个备选项中只有一个是符合题目要求的,请将其代码填写在题后的括号内。 错选、多选或未选均无分。 1.采用货币性与非货币性项目法对外币财务报表进行折算时,下列项目中应按现行汇率折算的是( ) A.存货 B.应收账款 C.固定资产 D.实收资本 2.我国企业会计准则要求采用的所得税会计核算方法是( ) A.利润表法 B.应付税款法 C.资产负债表递延法 D.资产负债表债务法 3.下列上市公司定期报告中,必须经注册会计师审计的是( ) A.月度报告 B.季度报告 C.中期报告 D.年度报告 4.在中期财务报告中,不应 ..提供的前期比较财务报表是( ) A.本中期末和上年度末的资产负债表 B.年初至本中期末的、上年年初至可比本中期末的现金流量表 C.本中期的、年初至本中期末以及上年度可比较期间的利润表 D.本中期的、年初至本中期末以及上年度可比较期间的所有者权益变动表 5.甲公司以经营租赁方式将一栋办公楼出租,租约规定,租期三年,第一年末支付租金25万元,第二年末支付租金45万元,第三年末支付租金50万元。租赁期满后,甲公司收回办公楼。甲公司第一年应确认的租金收入为( ) A.25万元 B.40万元 C.45万元 D.50万元 6.下列不属于 ...金融资产的是( ) A.银行存款 B.应收账款 C.债权投资 D.权益工具 7.在资产负债表日,对于衍生金融工具的公允价值高于其账面余额的差额,应借记的账户为衍生工具,贷记的账户为( ) A.投资收益 B.套期损益 C.汇兑损益 D.公允价值变动损益

高级财务会计 单选题 数字开头找数字后第1个汉字的字母■ 符号/字母开头■ ☆:9、甲公司将一暂时闲置不用的机器设备租给乙公司使用,则甲公司在获得租金收入时,应借记“银行存款”,贷记(D、“其它业务收入”)。 ☆“少数股东权益”项目反映除母公司以外的其他投资者在子公司的权益,表示其他投资者在子公司所有者权益中所拥有的份额。在我国“少数股东权益”项目在合并资产负债表中应当A在所有者权益类项目下单独列示 ☆A公司2007年12月31日将账面价值2000万元的一条设备以3000万元的价格出售经任凭公司,并立即以融资租赁方式向该公司租入该生产线,租期10年,使用年限15年,期满归还设备。租回后入账价值2500万元,则2007年固定资产折旧费用C150万元☆A公司从B公司融资租入一条生产线,其公允价值500万元,最低租赁付款额600万元,假定按出租人的内含利率折成现值520万元,则在租赁开始日,租赁资产的入账价值、未确认融资费用分别是A 500、100万元 ☆A公司是B公司的母公司,在20x7年末的资产负债表中,A公司的存存货为1100万元,B公司则是900万元。当年9月12日A公司向B公司销售商品,售价为80万元,商品成本为60万元,B公司当年售出了其中的40%,则合并后的存货项目的金额为C 1988万元 ☆A公司为B公司的母公司,20x8年5月B公司从A公司购入的150万元存货,本年全部没有实现销售,期末该批存货的可变现净值为105万元,B公司计提了45万元的存货跌价准备,A公司销售该存货的成本120万元,20x8年末在A公司编制合并财务报表时对该准备项目所作的抵消处理为C借:存货—存贷跌价准备300000 贷:资产减值损失300000 ☆A公司为母公司,B公司为子公司,年末A公司“应收账款-B公司”的余额为100000元,其坏账准备提取率为10%,编制合并财务报表时应编制的抵销分录是D借:应收账款-坏账准备10000贷:资产减值损失10000 ☆A公司向B租赁公司融资租入一项固定资产,在以下利率均可获知的情况下,A公司计算最低租赁付款额现值应采用(A、B公司的租赁内含利率)。 ☆A公司以公允价值16000万元,账面价值为10000万元的无形资产作为对价对B公司进行吸收合并,购买日B公司资产情况如表:A公司和B 公司不存在关联方关系。A企业吸收合并产生产商誉为B 1000万元 ☆A公司于2008年9月1日以账面价值7000万元、公允价值9000万元的资产交换甲公司对B公司100%的股权,使B成为A的全资子公司,另发生直接相关税费60万元,为控股合并,购买日B公司可辨认净资产公允价值为8000万元。假如合并各方没有关联关系,A公司合并成本和“长期股权投资”的初始确认为(B、90609060)。 ☆A租赁公司将一台设备以融资租赁方式租赁给B公司。签订合同,该设备租期件,届满B公司归还A公司。每6个月月末支付租金800万元,B公司担保资产余值为460万元,B公司的母公司担保的资产余值为680万元,另外担保公司担保680万元,未担保余值为220万元,则最低租赁付款额为D 7540万元 ☆B公司为A公司的全资子公司,20x7年3月,A公司以1200万元的价格(不含增值税额)将其生产的设备销售给B公司作为管理用固定资产。 该设备的生产成本为1000万元。B公司采用直线法对该设备提折旧。该设备预计使用年限为10年。预计净残值为零。编制20X7年合并财务报表时,因该设备相关的未实现内部销售利润的抵消而影响合并净利润的金额为B 185万元 ☆M公司拥有N公司70%的股权,M公司向N公司销售商品一批,N公司尚未将其销售,此销售行为称为(顺销),在编制抵消分录时应(全部消除)。 A ■ ☆按清算原因不同,企业清算可分为(解散清算、破产清算和撤消清算)。 ☆按照新准则规定,承租人分摊未确认融资费用时,应采用的方法是A实际利率法 B ■ ☆编制合并报表的依据是纳入合并报表范围内的子公司的(个别会计报表)。 ☆编制合并报表时对子公司的权益性投资一般采用(权益法)进行核算。 ☆编制合并财务报表的依据是纳入合并财务报表合并范围内的子公司的D个别财务报表 ☆编制合并财务报表时,最关键的一步是(编制合并工作底稿)。 ☆编制合并财务报表时,最关键一步是D编制合并工作底稿 ☆编制合并财务报表时编制的有关母公司投资收益和子公司期初未分配利润与子公司本期利润分配和期末未分配编制利润的抵消分录正确的是D借:投资收益;未分配利润-年初贷:提取盈余公积;对所有者(股东)的分配;未分配利润-年末 ☆不属于企业特殊经济事项的是B无形资产核算 C ■ ☆采用货币性与非货币性项目法,资产负债表中留存收益项目C为轧算的平衡数 ☆采用现行汇率法,对资产负债表项目采用历史汇率折算的项目是C股本 ☆采用销售租赁的销售收入,存在未担保余值的情况下,应该是出租方的B最低租赁收款额现值 ☆承租人采用融资租赁方式租人一台设备,该设备尚可使用年限为10年,租赁期为8年,承租人租赁期满时以1万元的购价优惠购买该设备,该设备在租赁期满时的公允价值为30万元。则该设备计提折旧的期限为(10年)。