Related Classifications

Hospice Facilities

Hospitals - General Care

Nursing Homes

Pharmacies

Rehabilitation Facilities - Physical Restoration

Special Exposures

Administration of drugs

Lifting residents or heavy items

Pets

Pools, whirlpools, and exercise equipment

Privacy

Substandard facilities of care

Unqualified personnel

RISK DESCRIPTION

A rapidly growing segment of the United States population is the elderly. In 1996, there were 34 million people over the age of 65, representing 13% of the nation's total population. By the year 2020, this age group is projected to nearly double in number and account for 20% of the total population. This increase has produced a large and growing number of senior citizens requiring medical oversight and formalized care. Assisted living facilities are designed to meet these increasing demands. These facilities combine the advantages of independent housing, supportive services, and social activities. They offer individual apartments or rooms, meals, housekeeping and laundry services, transportation, assi stance with basic activities of daily living (ADLs) and instrumental activities of daily living (e.g., bathing, eating), along with ongoing health and activity supervision.

Assisted living is an umbrella term for a wide range of new living settings where nursing home-eligible people live and receive care. However, while some persons may refer to assisted living facilities as nursing homes, they are not similar types of facilities; they offer different services, often to a different population. While both facilities offer medical services, nursing homes are designed to provide long-term health care and social services to the elderly, chronically ill, or convalescent persons. Assisted living facilities are designed specifically for elderly citizens, whereas nursing homes may house both elderly and young persons (i.e., those with chronic medical problems or severely injured individuals who are in need of 24-hour care). The goal of nursing home care is to provide care and treatment to restore and maintain the patient's highest level of physical, mental, and social well-being by providing round-the- clock health care services. The goal of assisted living is to help individuals live as independently as possible. This classification will focus solely on assi sted living facilities. For more in formation on nursing home care, refer to the Nursing Homes classification.

Currently, assisted living facilities are state regulated. Facility providers are chosen to work with state agencies to help establish quality standard, measurement, and monitoring approaches. Each of the 50 state departments of social services or public health responsible for licensing assisted living facilities has

different parameters and restrictions, as well as different names for the residences. Currently, there are 26 different terms commonly used throughout the United States, including such designations as residential care, personal care, boarding facilities, catered living, retirement homes, homes for adults, and adult congregate living care. While these various facilities may be referred to as assisted living facilities, each often offers its own unique type of services. The majority of states have existing licensing regulations using the term "assisted living"; for the purposes of this classification, all such residences will be referred to as assisted living facilities.

In 1996, people reaching the age of 65 had an average life expectancy of 82.7 years, which is 3.4 years more than their expectancy in 1960. While such recent medical advances as new medicatio ns, surgeries, and life-sustaining equipment have extended the human life span, an increase in the elderly population has brought forth a need for a disproportionately large share of medical services and assistance with daily activities. According to the U.S. Administration on Aging, daily living activities include eating, getting around in one's home, dressing, and bathing oneself. These older individuals sometimes need help with ADLs, and assisted living facilities are designed to provide the necess ary support.

Diseases related to dementia (i.e., ailments that affect the brain and alter memory, thinking, and actions, such as Alzheimer's disease) have affected life expectancies, and those suffering from such illnesses require the sort of increased care that assisted living facilities offer. Other factors contributing to the growth of such facilities include the fact that older persons now have higher incomes (over 53% of the U.S. elderly have incomes topping $15,000 a year and nearly 35% have an annual income of $25,000) allowing individuals to afford living in these residences; and the emergence of managed care and integrated delivery health care systems. Additionally, with more women entering the workforce, the number of family members able to care for aging relatives has decreased. It is estimated that more than 25% of seniors do not have relatives to whom they can turn for support in their later years.

Assisted living facilities debuted in the U.S. in the 1980s. These institutions were patterned after Dutch and Scandinavian systems egularly by the facility, and as the resident's condition indicates. The resident, his or her family, or another party responsible for the resident, play a role in the service plan's development by aiding the facility's personnel in determining what types of services and level of care the resident needs.

The resident may be placed in a particular level of care, if the facility offers such di stinct tiers. Examples

of these care tiers may include a level of minimal assistance where residents are only given direction on activities, meals, and medications; a stand-by assistance level where they are provided minimal hands-on assistance with dressing, 24-hour care, medications, meals, and direction on activities; and a hands-on assistance level where they receive aid in activities of daily living, help with incontinent care, diabetic monitoring, plus all other assi stance from the previously-mentioned levels.

Assisted living facilities typically do not provide continuous skilled nursing care. The facility should assure that prompt and appropriate medical, health, and dental care services are administered when required. The health care of each resident is under the supervision of the resident's chosen ph ysician. Residents suffering from temporary incapacity due to illness, injury, or recuperation from surgery may be allowed to remain in the facility if appropriate services can be provided or be readmitted to a hospital, if necessary.

Many elderly citizens are turning to assisted living facilities because they find them more appropriate and cost-efficient than other residences or facilities for the elderly, such as nursing homes or adult daycares. Compared to conventional nursing home care, assisted living facilities are 20% to 30% less expensive. More than 90% of the sector's revenues are generated from private pay. In 1998, assisted living facilities comprised a nearly $17 billion industry, which is projected to climb to over $23 billion by the year 2000. National expenditures for skilled nursing and home health care increased from $36 billion in 1985 to $106 billion in 1995 - expenditures that accounted for 11% of all health care costs in the U.S. Assisted living facilities offer the appropriate level of care for seniors at 25% to 50% less than the cost of a skilled nursing facility.

Assisted living facility costs vary greatly, depending on the type of residence, room size, and types of services required by residents. Private funds pay for 90% of assisted living services; the remaining 10% are covered by Supplemental Security Income (SSI), Social Security Block Grants, and other entitlement programs. In addition, several private health and long-term care insurance policies include assisted

living/residential care coverage. In 1998, 35 states reimbursed, or planned to reimburse, services in assisted living or board-and-care facilities as a Medicaid service. According to the American Health Care Association, 42% of all facilities receive state program assistance for residents. Currently, many states are

experimenting with expanding assisted living to low-income seniors through waivers to the federal Medicaid program.

The typical profile of an assisted living resident is a senior aged 75 or older (the average age for women is 84 and for men is 81) who meets the entry criteria of having at least $25,000 in annual net income, no combative or disruptive behaviors, and the ability to pay monthly housing rental fees of $2,000 or more. The average per-diem rate for the industry is $72; it is approximately $91 for residents in an Alzheimer's disease facility. Assisted living costs range from between $985 and $1,500 per month to $3,700 per month for a private 2-bedroom suite with minimal to moderate levels of personal care. Residents generally have personal assets ranging from $100,000 to nearly $300,000.

Conversely, as needs change, elderly people may relocate from assisted living residences. According to the National Center for Assisted Living, the majority of residents leave facilities because they are in need of a higher level of medical care. In 1998, the following were leading reasons why residents moved out of assisted living facilities: 43% went to a nursing facility; 22% died; 13% returned to their homes; 11% went to a hospital; 9% relocated to another assisted living residence; and 3% went to other settings. The average length of stay for an assisted living facility resident is three years.

Consolidation of assisted living facilities is one reason for the industry's increase. This continuing trend is a result of dominant companies (e.g., hotel chains and major corporations) seeking to strengthen their presence in specific geographic regions. Most of these acqui sitions have been for individual properties and small clusters of properties. Recently, however, there has been a growing number of acquisitions of entire public assisted living companies. The majority of the largest multi-facility providers are publicly held and managed as for-profit businesses. In 1997, 54% of assisted living facilities were part of a larger multi-facility organization with 10 or more residences; 25% were part of multi-facility organizations of 2 to 9 facilities; and 20% were single or stand-alone facilities. According to the Assisted Living Federation of America, in 1996, 85% of assisted living residences were for-profit, while 15% were not-for-profit facilities.

Assisted living facilities are located in rural, suburban, and urban areas in all 50 states. Facility developers have identified several locations as the highest selected regions due to favorable demographics and the relative absence of regulatory impediments in those states. In addition to the District of Columbia, these regions include: Florida, Texas, New Jersey, Pennsylvania, California, North Carolina, Washington, and Ohio. Most assisted living facilities are freestanding; however, they may also be part of a continuing-care retirement community, seniors' apartment co mplex, or wing or floor of a nursing home. The facilities may also be renovated schools or converted hotels, motels, or nursing homes. Facilities vary in terms of size. The average size of an assisted living residence is 43 units; however, facilities may range from 3 units to over 200 individual living quarters. The average number of residents in a facility is 40; however, small, homelike facilities typically house 3 to 12 residents, while large, full-service communities may accommodate 600 to 800 persons.

Assisted living facilities generally consist of a lobby, kitchen, administrative offices, medical and treatment areas, a common dining room, employee lounges, restrooms, and a parking lot. Common areas may include sun porches, a veranda, a library, a billiards room, television rooms, gardens, a beauty

parlor/barber shop, and fitness rooms. Individual units or shared rooms may be clustered in groupings of six to eight, and they vary in size from one room to a full apartment. Full apartments generally contain a bedroom, bath, closets, and kitchenette. These units often open in a suite-like fashion into a common sitting area or small living room.

Assisted living facilities generally operate 24 hours a day, 7 days a week; however, administrative offices are typically open from 9 a.m. to 5 p.m., Monday through Friday. Most facilities place no restrictions on visitors, who are generally allowed on the premises at any time. In addition, many insureds also allow residents to have overnight guests.

The number of personnel employed by assisted living facilities varies, depending on the size of the organization. Some states have requirements as to the number of staff needed in the facilities. For example, Alabama requires that there be one staff member per six residents in assisted living facilities at all times. Typically, a facility may hire anywhere from 10 to over 50 employees, including administrators, nurses, direct care staff (e.g., certified nursing assistants, certified home health as sistants), food service personnel, therapy consultants, activities coordinators, dietary consultants/dietitians, clerical staff, billing personnel, and housekeeping and maintenance workers. The ages of the workers vary; some may be as young as 16, while others may be over the age of 65. Some facilities hire temporary or part-time employees, such as students, during the summer; others have volunteers who assi st personnel and aid residents in such areas

as writing letters, reading, and providing companionship.

While assisted living facilities continue to prosper, there are several primary concerns that plague the industry: licensing delays, scarcity of trained employees, overbuilding in selected markets, and the inability to manage costs. Assisted living organizations and associations and the facilities' states are working to combat these problems by establishing new regulations and re- evaluating and creating new insurance and cost structures.

The assisted living industry, which is still a relatively new sector of elderly care, is anticipated to continue to grow as a viable alternative for long-term care. Factors that will aid in this upsurge include the continued number of people living to age 85 and over, elderly persons seeking appealing alte rnatives to inappropriate nursing home placement (e.g., being placed in a nursing home facility when they did not require that type of care), and government agencies recognizing these lifestyle trends and the possibility that they will introduce entitle ment programs to allow older people to choose a preferred assisted living setting. To provide future services to all elderly regardless of income, several states - including Connecticut, Illinois, Louisiana, and Rhode Island - are currently establishing pilot programs to address low-income residents' needs.

Several associations serve the industry. The organizations include the Assi sted Living Federation of America (ALFA, which may be reached at https://www.doczj.com/doc/ac11853147.html,), which is the largest trade association exclusively devoted to the assisted living industry and the population it serves. Other associations devoted to these facilities include the American Association of Homes and Services for the Aging (AAHSA, which may be reached at https://www.doczj.com/doc/ac11853147.html,) and the American Health Care Association (AHCA, which may be reached at https://www.doczj.com/doc/ac11853147.html,).

MATERIALS AND EQUIPMENT

Medical equipment and supplies, rehabilitative, and laboratory equipment; hospital beds; stretchers, wheelchairs and other walking aids; bathing equipment; first aid kits; wander-guard sensors (i.e., to keep dementia patients within the facility's premises).

Pharmaceuticals, including oral medications, subcutaneous injections (e.g., the vitamin B12, insulin),

eye/ear/nose drops, topical creams and ointments, suppositories/enemas, inhalers, etc.

Dietary and laundry equipment; housekeeping, cleaning, and maintenance equipment; recreational facilities and equipment; arts and crafts supplies.

Furnishings: tables, chairs, couches, televisions, VCRs.

Computer hardware and software; fax machines, copy machines.

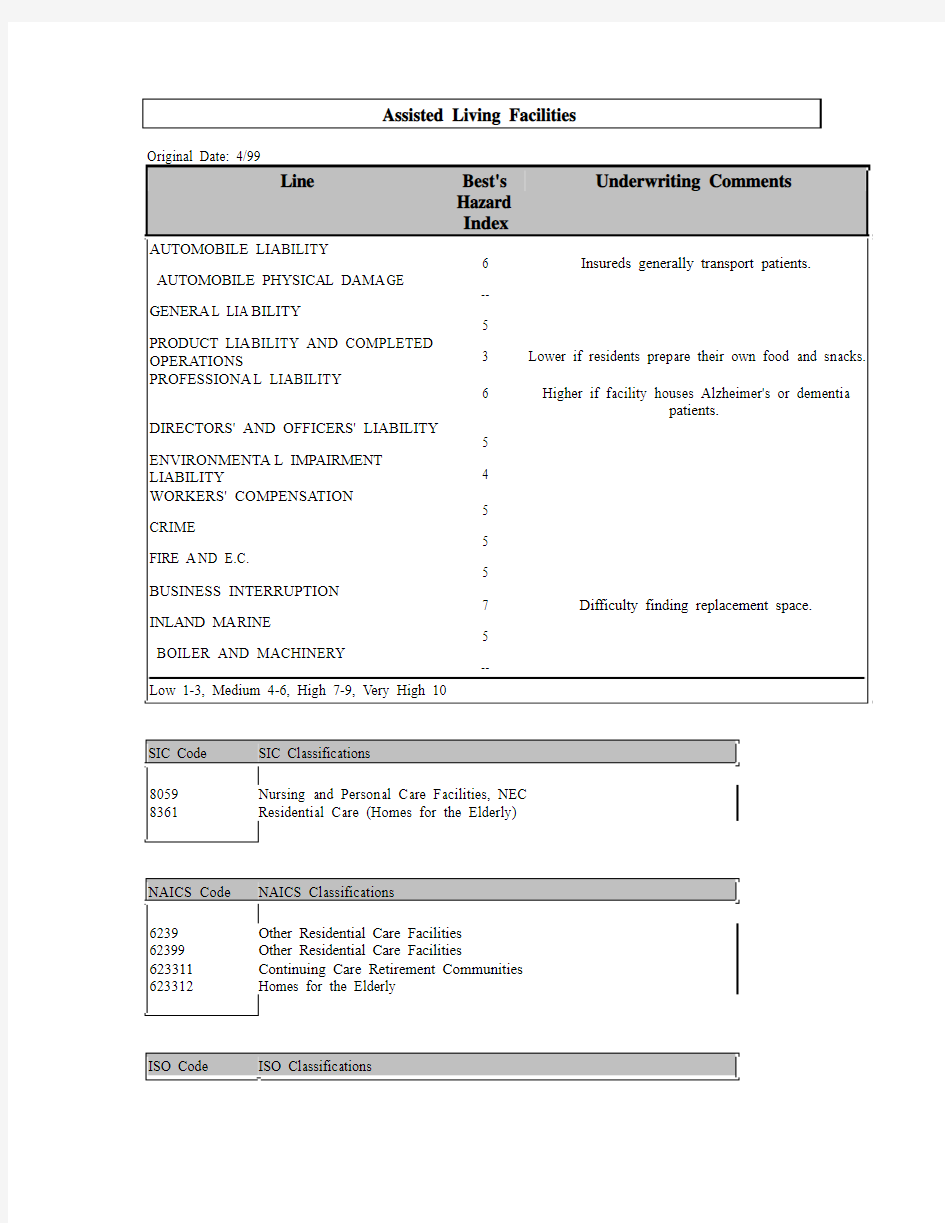

Automobile Liability

Because the majority of assisted living facilities will frequently transport residents to and from various locations, the Automobile Liability exposure will be significant. These facilities often transport residents to doctors' appointments, shopping malls, grocery stores, pharmacies, restaurants, theaters, libraries, and various other locations. Most facilities will have at least one vehicle to transport residents, although larger insureds may have a small fleet of vehicles. Assisted living facilities may also own cars, vans, or pickup trucks to run errands or get supplies. However, some facilities may require employees to use personal vehicles for business use, which would increase the exposure for this liability. Depending on the circumstances, travel may be done at night, when there is low visibility and drivers may be tired.

What are the frequency of travel, the radius of operations, and the hazards of typical routes? Most deliveries, pick-ups, and resident transports will be intermediate. Determine whether company-owned vehicles are used only to pick up supplies and run errands or are used to transport residents to and from facility-sponsored activities or off-premises locations (e.g., shopping malls, grocery stores, doctors' offices, and places of worship). According to the National Center for Assisted Living, the typical assisted living facility generates 1.73 trips per resident unit each day, as compared to 9.57 trips for the average single-family detached house and 6.59 trips for a low-rise apartment. What is the frequency of trips and destinations made by the insured and his or her employees? Routes to field trips may be unfamiliar t o the driver and may involve substandard or unpaved roads, or travel in high traffic, congested urban areas. Drivers may sometimes be required to operate vehicles before and after daylight, especially during the winter months. Darkness may result in decreased visibility, and at such times, drivers may be operating vehicles while they are fatigued. In addition, darkness may impede residents' visibility when boarding and

exiting vehicles. Are the insured's drivers required to operate vehicles while it is dark?

Does the insured operate a fleet of vehicles? Are the vehicles owned or leased? In some cases, insureds do not own buses but rather charter them for specific trips or tours. If so, determine the reputation of the bus company normally used by the insured.

Are safety restraints (e.g., seatbelts) used for all occupants? Are vehicles wheelchair-accessible? Due to various ailments and their frail nature, older people are more susceptible to injury in the event of an accident. Are residents assisted on and off the vehicle? Because accidents may occur during the loading or unloading of supplies or passengers, it is recommended that Automobile Liability and General Liability coverages be written by the same company for the same limits.

What are the number, age, type, and condition of the insured's vehicles? Owned or leased automobiles, vans, and buses may be used to run errands, to pick up supplies, and transport residents. Do employees ever take the insured's vehicles home at night or on the weekends? Occasionally, staff members may be called on to use their own vehicles. If employees use personal vehicles to run errands or transport residents, a nonowned vehicle exposure may exist.

What are the number, age, training, and experience of the insured's drivers? Does the facility transport clients, or do outside contractors provide transport services? Transporting elderly or disabled adults requires stable and experienced drivers. Does the insured have a safe-driver training program in place? An employee may be called upon to drive in an emergency; motor vehicle records should be obtained on all employees who are licensed drivers. Some facilities employ workers under the age of 25; a youthful operator exposure may exist. Request certificates of insurance from all drivers. Since the Fair Credit Reporting Act requires written permission from the driver to obtain MVRs, the insured should make obtaining this permission a part of the hiring process. Although infrequent, some facilities' drivers may operate oversized vehicles, such as buses or trucks. Operators of oversized autos will need the training necessary to drive these vehicles. A commercial driver's license (CDL) may be required to operate the oversized vehicles.

Does the insured have a vehicle maintenance program? The insured's vehicles should be kept in good condition, repaired promptly as needed, and inspected regularly. It is a positive underwriting sign if the insured contracts out vehicle maintenance to experienced mechanics. Employees should not be permitted to repair or assist in the repair of the insured's vehicles.

General Liability

Staff competence, the condition of the premises and equipment, and the physical layout of the building all affect the potential for injury. Many insureds will have a large number of visitors to their facilities daily. Primary premises exposures will be slips, trips, and falls. Additionally, some insureds may have volunteers working on site; this will increase the General Liability exposure. Because of the lack of uniform federal standards governing assisted living facilities, it is important for the underwriter to ascertain the standards (e.g., space and living quarter requirements) established by the state or county in which the facility is located and the degree to which these standards are adhered to by the insured's facility. Overall, assisted living facilities will have a moderate exposure in this line.

What is the layout of the insured's premises? The majority of fac ilities are freestanding; however, they may also be part of a continuing-care retirement community, seniors' apartment complex, or wing or floor of a nursing home. Assisted living facilities generally consist of a lobby, kitchen, administrative offices, a common dining hall, employee lounges, medical and treatment areas, restrooms, and a parking lot. Common areas may include sun porches, a veranda, a library, a billiards room, a television room, gardens, a beauty parlor/barber shop, and fitness rooms. Individual units or shared rooms may be clustered in groupings of six to eight, and they vary in size from one room to a full apartment. Full apartments generally contain a bedroom, bathrooms, closets, and kitchenette. These units often open in a suit e-like fashion into a common sitting area or s mall living room. Is the insured's facility owned or leased?

States have established requirements as to the space and type of living quarters for assisted living facilities. These resident unit requirements generally specify the minimum square footage, maximum number of individuals per unit, the areas or rooms to be included in each living quarter, and requirements for semi-private units. However, these requirements vary greatly from state to state. What are the insured's state requirements?

What are the insured's hours of operation? Assisted living facilities generally operate 24 hours a day, 7 days a week. However, administrative offices are typically open from 9 a.m. to 5 p.m., Monday through

Friday.

What are the average and maximum numbers of daily visitors to the insured's premises? Most facilities place no restrictions on visitors, who are generally allowed on the premises at any time. In addition, many insureds also allow residents to have overnight guests. What is the insured's visitation policy? Visitors to the site will usually include family members, clergy, delivery personnel, maintenance workers, inspectors (e.g., local building and health inspectors), guest speakers, and crafts/activities instructors. Does the insured offer tours (e.g., to potential clients, outside groups, or organizations) of the facility? An employee should accompany tour groups at all times. "Employees Only" signs should be posted in areas restricted to both visitors and residents. In some facilities, volunteers assist residents in writing letters, reading to them, or visiting them on a regular basis. Does the insured have volunteers who work in the facility and/or visit with residents? In some facilities, local clubs or social groups provide occasional entertainment or other services for the residents. Determine if such groups visit the insured's facility. Does an employee accompany the groups' members at all times while they are on the premises?

For visitors to the insured's premises, slips, trips, and falls will present the main General Liability exposure. What is the level of housekeeping on the insured's premises? The facility should be kept free of debris and clutter. Are residents allowed to empty their own trash into appropriately marked garbage containers located inside or outside the building? Trash and debris should be removed from the facility's premises on a daily basis. What is the condition of the insured's flooring? Floors should be swept and vacuumed on a daily basis. Worn, torn, or loose floor coverings should be repaired and replaced immediately. Spills should be cleaned up immediately, and "Caution - Wet Floors" signs di splayed. All electric wiring should be properly insulated and run inside the walls.

Does the insured comply with the provisions of the Americans with Disabilities Act (ADA) of 1992? This law requires that public buildings be wheelchair-accessible; restrooms and other areas of the facility must be readily accessible by wheelchair or other conveyances that assist di sabled or elderly residents. Since senior citizens and physically challenged residents may be hampered by the use of walkers, crutches, and wheelchairs, are emergency exit doors located throughout the premises? Are their locations indicated by signs clearly visible to residents and visitors? Stairs can be difficult for some elderly individuals to negotiate. Stairs should be in good condition, covered with a nonskid material, and equipped with sturdy handrails. Is the facility all on one level, or are there multiple levels? In most cases, a multi-level facility will require an elevator to assist seniors in moving from one level to the next. Who services the insured's elevators and how frequently? Generally, insureds will contract out elevator maintenance. Determine the reputation and loss history of the insured's elevator maintenance contractor.

Safety equipment should be installed or be available if needed in residents' bathrooms. This equipment may include grab bars, raised toilet seats, and seats in showers. Is safety equipment installed in the residents' bathrooms? Residents' living quarters should be equipped with emergency call systems linking the residents' units to nursing stations or other staff member locales. Is the insured's facility equipped with such systems?

The privacy of residents is a crucial element to these facilities. Privacy is primarily measured by the type

of unit, the ability of residents to lock their doors, and the staff's behavior. States that have based their policy on privacy have emphasized apartments with attached baths. When common or dormitory style bedrooms are provided, there should be a separation by partitions or screens to provide for privacy in ba th and toilet areas. As of 1998, 31 states had rules that allowed 2 people to share a unit or bedroom, and 11 of these states allowed sharing of units only by choice of the residents. What is the insured's state policy regarding privacy? Are two people allowed to share a unit or bedroom in the insured's state?

Most congregate assisted living facilities will have laundry facilities, unless commercial laundry services are used. Laundering facilities should be located in a specifically designated area. Insureds should prohibit visitors and residents from laundry areas because the chance of injury is increased as these individuals could be exposed to injuries from machinery and toxic cleaning solvents (e.g., detergents). Does the insured's facility have adequate room and space for sorting, processing, and storage of soiled materials? Provisions should be made for proper mechanical ventilation of the laundry, and adequate and effective lint traps should be provided for dryers.

Kitchens contain further potential for injury. The facility's kitchen should be separate from areas occupied by residents. Kitchen appliances may present a variety of hazards. For example, stoves may have open flames, while ovens may cause burns if residents reach over heated burners. The insured should restrict access to the kitchen to staff and kitchen employees only. Is the insured in compliance with local and state codes regulating kitchen and food preparation/serving areas? Many resident apartments/rooms contain a

kitchen or s mall "tea kitchen" (i.e., a kitchenette that contains a sink and refrigerator). Are residents' individual units equipped with kitchens? If so, the same hazards found in the facility's kitchen may also occur in residents' kitchens. Many resident kitchens have microwaves and/or hot plates. Do the insured's resident units have such appliances? If so, residents should be instructed how to properly operate these appliances. Injuries, such as strains, sprains, or falls, may result when residents reach for items in kitchen cabinets or shelves. If shelves are located too high off the ground, residents may climb onto chairs, potentially causing injury if chairs topple over or residents fall off them. Are cupboards and shelves in kitchen areas easily accessible so that residents do not have to climb or stretch to reach them?

Assisted living facilities often have microwave ovens on the premises in both the kitchen and residential units. Microwave rays present a danger to residents and workers with certain heart conditions who wear pacemakers. Does the insured post signs in kitchen areas that warn residents and employees that microwaves are being used?

Does the insured employ dietitians to assist residents who have special dietary needs (e.g., d iabetics)? Many assisted living facilities employ these individuals to prepare special dietary menus and requirements for patients who need specially prepared foods, such as no-salt diets and foods without sugar. Do dietitians instruct food preparation employees of any dietary needs? Are these specially prepared foods offered daily to residents with these requirements?

Does the insured have a pool on the premises? If the facility has a pool, particularly an in-ground pool or one that is a permanent structure and cannot be drained daily, the likelihood of a resident or visitor drowning will increase. A pool alarm should be used to alert staff if someone has fallen into the pool. What pool safety measures does the insured have in place? For example, an outdoor pool should be surrounded by a fence and have a locking gate installed on it to prevent access from outsiders. Does the insured employ a lifeguard? Staff should be trained in resuscitation techniques, and the insured should be in compliance with all state and local statutes regulating the operation of a public pool.

Medical research indicates that animals provide therapy to elderly and ailing persons. To meet these needs, along with providing companionship and enjoyment, some assisted living facilities allow residents to own pets (e.g., dogs, cats, or birds). According to the National Center for Assisted Living, nearly 50% of all facilities allow residents to keep small pets in their units or apartments. In addition, nearly 40% of all centers provide facility-owned pets for residents to enjoy. Does the insured's facility have its own pets? Are residents allowed to have pets in their living quarters or have pets brought to the facility by visitors? Some residents could develop an allergic reaction. Residents or visitors could be injured if not taught how to handle animals properly. Pets should be even-tempered and well-trained so they will not become agitated and bite, scratch, or claw residents or visitors. What is the level of supervision of these animals? All animals on the premises should be domesticated and non- aggressive, licensed and vaccinated, free from disease, effectively controlled, and prohibited from food preparation areas. What is the insured's practice?

Often, assisted living facilities will have artwork and decorative pieces (e.g., sculptures) displayed throughout the premises; some of the work hangs on walls and ceilings. This artwork could potentially fall and injure residents, visitors, or employees. How are decorative pieces secured to prevent them from falling?

Many facilities have large panes of glass both inside and outside (e.g., sliding glass doors, French windows). Glass should be properly etched or marked to prevent residents or visitors from walk ing into the clear glass.

What are the age, type, and condition of the insured's furnishings? Generally, residents bring their own furnishings for their living units. However, facilities will house a large number of furnishings, ranging from couches in lobbies and television rooms, to tables and chairs in recreation and dining areas. Furniture should be sturdy, free of splinters, and have no protruding nails or screws. Chairs, particularly those that swivel or rock, should be properly assembled and in good repair. What is the insured's practice of inspecting furnishings? The underwriter should evaluate the layout and condition of areas that contain seating furnishings (e.g., dining areas, recreation rooms). Is there adequate space between tables to allow residents to move comfortably and maneuver wheelchairs and walkers? In facilities where employees serve food to residents in dining rooms, there should be adequate space between tables to allow the servers to move freely. If tables are too crowded, the chance of a server dropping a hot plate on a resident may increase. Is there adequate space between tables in the insured's dining area?

In facilities that utilize servers in dining rooms, burns and cuts are potential hazards to residents. Thes e employees may spill hot dishes or beverages on residents or visitors, causing burns or damaging their

clothing. Are servers instructed how to properly carry trays and dishes? Do they warn diners that plates are hot? Cuts can be caused by broken glass or chipped dishware. Are glasses and dishes inspected before being used?

A resident may choke on food while in the dining area. Are employees trained in the proper first aid methods? Designated employees should be trained in first aid and cardiopulmon ary resuscitation (CPR) techniques to provide medical assistance. Are first aid kits located throughout the facility? Is a first aid kit available in each medical room or treatment area?

Does the insured have an on-site physical therapy and/or exercise facility? These areas typically contain various fitness equipment, such as exercise bicycles, treadmills, whirlpools, and walking assistance apparatus (e.g., parallel bars). Is the insured's equipment in proper working order? Who is responsible for inspecting, maintaining, and repairing the equipment? An employee (e.g., physical therapist or therapy assistant) should be present at all times when residents are using physical therapy equipment, as they can fall or potentially suffer a heart attack from misuse or overuse of the equipment. Are employees present when residents use whirlpools? At what temperature are the insured's whirlpools set and maintained?

The insured may be liable for use of faulty medical equipment. Determine the reputation of th e insured's medical suppliers. Are new staff members trained in the proper use of equipment? Does the insured have an ongoing maintenance program, in accordance with the manufacturers' specifications?

Most states require persons to sign agreements or contracts prior to becoming residents of a facility. The scope of the agreement varies but usually includes provisions dealing with services, resident rights and responsibilities, occupancy, and discharge issues. Do the insured's contracts stipulate info rmation on resident charges and fees? Most agreements include a description of the fee or charges to be paid, the basi s of the fee or what is covered, who is responsible for payment, and the method and time of payment. Refund policy may also be covered by these agreements. Rules covering contracts specify the amount of advance notice tenants must be given when rates are changed. Does the insured's service provisions describe the services to be provided that are covered by the basic fee and any additio nal services that might be available? Some states also require that agreements contain resident rights and the provisions that allow staff to inspect living quarters, with the residents' permission. Terms of occupancy may also address provision of furnishings and the policy concerning pets. Do the insured's contracts cover such provisions? Determine what the insured's state regulations require for service and resident contracts.

Does the insured secure the facility with enclosed patios and/or courtyards? Security issues are of great concern for elderly persons, particularly those with Alzheimer's disease and dementia, as these individuals often lose their reasoning and judgment and are easily disoriented. For example, a common characteristic of Alzheimer's disease is a compelling need to roam or wander in a seemingly aimless manner. Does the insured have a wander-guard alarm so staff will be alerted when someone leaves the building?

What is the condition of the insured's sidewalks and parking lots? Sidewalks and parking lots should be free of cracks and potholes that could cause seniors, physically challenged residents, and other visitors to the premises to slip and fall. Are snow and ice removed promptly? Does the insured or his or her employees remove snow and ice or is this service contracted out? Sidewalks and parking lots should be well lit.

Product Liability and Completed Operations

The Product Liability exposure for assisted living facilities will be slight. Most facilities will prepare and serve lunch, snacks, and beverages. The most serious exposure will be the possibility of serving clients tainted or spoiled food. If residents prepare their own meals and snacks, the Product Liability exposure will decrease.

Does the facility serve and prepare snacks, meals, and beverages? Is the food prepared by an outside professional food staff, by the center's staff, or by volunteers? Kitchen facilities should be clean, and all foods should be checked thoroughly before being prepared and cleaned if necessary. Is food stored properly? Storage containers should be properly marked and covered. Food is subject to spoilage or deterioration due to age, contamination, improper storage, or incorrect temperature controls.

How long has the insured been in business? What is the insured's financial condition? Financial problems can result in lower food quality and reduced maintenance/housekeeping standards, which will increase the chance of claims. Check the insured's financial records.

Good housekeeping is essential to control pests. How often are the premises sprayed for pests? The underwriter should check contracts made with pest control services. Other good housekeeping procedures

should be maintained throughout the kitchen and food preparation and storage areas. Floors should be swept and mopped daily. Garbage should be emptied daily, and containers should be washed and sanitized at the end of each shift.

Employees working in the kitchen should be properly trained to operate kitchen appliances and equipment, as well as to prepare food items. Has the kitchen been inspected and found to be satisfactory by the local health inspector? Are food and beverages stored separately from the cleaning supplies? Determine the reputation of the manufacturers of these food items and appliances, and the loss histories of these suppliers. Who is responsible for repair of broken or damaged appliances?

Proper food controls are important to prevent foodborne illnesses such as escherichia coli (E.coli) and salmonella. These diseases are caused when bacteria that live in the intestinal tracts of animals pass into meat and poultry when the animal is slaughtered; both cause severe diarrhea, fever, and abdominal cramps. Does the insured's food service prepare foods such as beef, poultry, and shellfish? The Centers for Disease Control and Prevention (CDC) and the U.S. Food and Drug Administration (FDA) have published strict guidelines regarding the storage and handling of these food products. These guidelines include that raw shellfish should be tagged with an FDA National Shellfish Safety Program tag, that raw foods should be separated from other food items and stored on a clean shelf space in the refrigerator, and that food should be delivered and stored at 41° F or below. For more information, see the Product Liability and Completed Operations section of the Restaurants classification.

Leftover food may become tainted if improperly stored and ideally should be discarded daily. Is a dequate refrigeration available? Perishables should be promptly refrigerated after use. Who is responsible for maintenance of the refrigeration units?

Proper room temperatures should be maintained in all food preparation areas. The FDA requires that a ll vapors and fumes be vented outside. Proper ventilation must be provided in hot food preparation areas, utensil washing areas, garbage areas, and toilet areas. Is the insured in compliance with OSHA standard 1926.57, Ventilation? All kitchen hoods should be approved by the National Fire Protection Association (NFPA) and should provide the proper amount of exhaust recycling in cubic feet per minute (cfm).

Does the facility use disposable plates and utensils for food service, or does it use plates an d utensils that require washing? Are dishes and utensils washed by hand or in a dishwasher? After rinsing, dishes should be sanitized with a bleach solution (e.g., one tablespoon per gallon of hot water). For a detailed discussion on proper dishwashing and sanitizing techniques, see the Product Liability and Completed Operations section of the Restaurants classification.

Allergic reactions to foods can also lead to claims. Are facility employees informed of the ingredients in

all menu items? Insureds may keep a binder with written ingredients in the kitchen area that employees can reference. What is the insured's practice? Some patrons may be strict vegetarians due to health or religious reasons. Are vegetarian dishes offered to residents? Many elderly persons also have special dietary requirements (e.g., diabetics who can only have regulated amounts of sugar). Do dietitians consult with food preparation workers about residents' diet requirements?

Are employees trained in proper hygiene methods? Does the insured post a policy regarding proper hygiene in the food area? Food prep workers should wear hairnets. In addition, food servers should wear their hair pulled back. Are employees instructed to wash their hands before handling food?

Is any merchandise or food sold in vending machines? If so, is a selection of food offered to accommodate patients with certain dietary restrictions (e.g., diabetics)? Ascertain the number and types of machines on the premises, the vendor's reputation, and whether any liability is assumed by the insured. For more information, refer to the Product Liability and Completed Operations section of the Vending and Amusement Machine Operators classification.

Professional Liability

The Professional Liability exposure assisted living facilities face will be significant. Exposures include insufficient licensing of personnel and the facility, negligent dispensing and administering of medications, and noncompliance with state specifications on the designated number of workers per residents. If the facility houses Alzheimer's or dementia patients, employees should be required to have additional training or the exposure for this liability will increase.

States license assisted living facilities. Since these facilities are generally less intensive than a skilled nursing home, assisted living facilities will typically have fewer licensing requirements; however, since they often provide more services than an independent living retirement community, they will require a

higher number of licenses than those residences. Is the insured's facility licensed by the state and in good standing? Is the facility Medicaid certified? There are several types of licenses that an assisted living facility might hold, including a standard license issued to provide basic support services; a limited nursing license that allows the facility to provide residents with more assistance and specified limited nursing services that may be defined by the Agency for Health Care Administration; a limited mental health license that provides for supervision and monitoring by specialized staff and individualized supportive services to meet the special needs of the resident; or an extended congregate care license that is designed to enable residents to "age in place" (otherwise, they might be disqualified from continued residency based on their level of care needs). "Aging in place" essentially is designed to protect patients from being removed from an assisted living facility as their need for additional services or medical treatment increases. What type of license does the insured's facility hold?

Does the facility have separate areas for caring for sick residents if they are unable to remain in their living quarters? Who administers medications and what are their experience, qualifications, and training? Claims commonly result from negligent dispensing and administration of drugs. Although some states require a licensed nurse to administer drugs and medications, many others require only that an employee receive some training in medication administration. All medications should be kept in a locked cabinet.

Does a physician prescribe all administered drugs, and are all prescriptions dispensed in accordance with written drug orders? Determine if the insured has a licensed pharmacy on the premises or an agreement with an outside licensed pharmacy or pharmacist consultant. Is the insured's pharmacist currently licensed by the state in which he or she practices? Determine the training, experience, and qualifications of the pharmacist or individuals who dispense and administer medications to residents.

Records of receipt and disposition of controlled drugs should be sufficiently detailed and accurate. What is the insured's system for recording drugs taken from the pharmacy or medication-dispensing area and administered to patients? The facility's medical personnel should be aware of any allergies residents might have. Are all adverse incidents regarding medications recorded and reported to a physician? The nursing staff should be periodically provided with refresher courses and new information on drug therapy.

Some medications and drugs must be stored in a specific temperature or in or out of the light (e.g., Diazepam, or valium, which is indicated to be stored between 15° and 30° C and kept in a tightly-closed, light-resistant container). Are all drugs stored under proper temperature, light, and security?

Is self-administration of medication allowed in the insured's facility? Most assisted living facilities allow residents to keep medications in their apartments or units. Are residents who self-medicate encouraged to have their medications reviewed by a health care professional at least annually or more often if necessary? Does the facility have policies and procedures that do not interfere with the rights of the resident, but protect the health and safety of other residents? For example, a resident may wander into the wrong room and take medicine that belongs to someone else.

Does the insured have any policies for prescription medications? Generally, prescription medications should have a pharmacy label that includes the resident's name, name of the medication, prescribed dosage, and directions for use. Medications should only be used for the resident identified on the pharmacy label. Does the insured keep stock of commonly used, over-the-counter medications? Does the insured dispose of medications after the death or eviction of a resident? It is a positive underwriting sign if insureds develop and follow a written policy for the disposition of unused, outdated, or recalled medications. Does the insured have such a policy in use?

A critical area of staffing for facilities is 24-hour awake staff to deal with residents suffering from dementia because many such persons are awake and active at night. Do facilities with these patients have staff available 24 hours a day? Staff members should be available not just for monitoring and supervision but also to provide individual attention and activities, even during the evening hours. Having staff to fill this need on a 24-hour basis both occupies the person with dementia and avoids disturbance of residents who are sleeping. What is the insured's practice for staff involved in the care of residents with dementia? What are the training, experience, and qualifications of professional services' employees? Most insureds and their employees have special training as a result of either state requirements or assis ted living residence policies. Some states require special staff certification and training. What is the experience of the insured's physicians, nurses, and other professionals on staff, and what are the privileging procedures for attending physicians? What are the insured's criteria for medical staff qualifications? Physicians must be properly licensed and certified. Nurses should have a bachelor's degree, associate degree, or certification from an accredited college, university, or nursing school. State requirements indicate the number of years of experience these individuals must have. Many insureds require that direct care staff be

certified nurses or home health aides. What is the insured's practice?

Most states require their facilities to have a certain number of staff members per residents. For example, in Georgia, an assisted living facility must have 1 staff person per 15 residents during working hours and 1 per 25 residents during nonworking hours. Determine the ratio of nurses to patients. Is the insured's number of staff sufficient to meet the needs of the residents?

State requirements vary as to the requirements of other staff members. Many states are adding requirements that staff in facilities serving Alzheimer's patients receive special training to respond to these patients' unique needs. For example, in Maine, all new employees in facilities with Alzheimer's/Dementia Care Units are required to receive a minimum of eight hours of classroom orientation and eight hours of clinical orientation. If the insured houses Alzheimer's patients, what are the employees' educational and training requirements?

Requirements for training new staff vary from state to state. The rights of residents is the most frequently cited area for required training. Most state regulations require an orientation for new staff and annual in-service training. What is the insured's practice for training new employees? Some states require direct care staff to successfully complete an approved course, while others specify the areas to be covered during training, the number of hours to be spent in training, and requirements for both topic areas and the number of hours. Training requirements may be grouped into five domains: direct care, health related, knowledge areas, safety and emergency issues, and process.

Have any of the insured's professional workers ever had complaints filed against them alleging professional misconduct? Elder abuse by caretakers at seniors' residence facilities have been reported in the media, and assisted living facilities must take every precaution to prevent claims of this type. Defending against these claims is expensive, even if the facility is later cleared of all charges. Charges of abuse can result from a staff membe r restraining or punishing an unruly resident. Does the facility forbid employees to engage in any type of corporal punishment? Are employees trained in the proper ways to restrain an unruly resident? The facility's discipline policy should be discussed with all caregivers and the residents themselves.

Does the insured perform criminal background checks on potential applicants? Some facilities perform a criminal check and Adult Abuse Registry check on employment applicants. Some states' legislation indicates that facilities should not employ or retain a worker who has had a substantiated charge, in any state, of abuse, neglect, or exploitation, or who has been convicted of an offense for actions relating to bodily injury, theft or misuse of funds or property, or other crimes inimical to the public welfare. Does the insured's state indicate such provisions? Insureds should retain records of any criminal and Adult Abuse Registry checks. What requirements must the insured follow to make reports to his or her state's Adult Abuse Registry?

Directors' and Officers' Liability

Assisted living facilities will have a moderate Directors' and Officers' Liability exposure. Possible exposures for this liability include insufficient continuing education requirements and mishandling of funds.

Does the insured have one or more administrators who oversee the facility's operations? Assisted living facilities generally have at least one administrator who is responsible for the overall operation of th e facility. He or she ensures that all staff members are qualified to care for the residents and are competent in performing their duties consi stent with applicable state and federal regulations. It is the administrator's duty to assure that each resident receives all services indicated in the resident's service plan. Administrators should be state licensed. In some states, administrators are required to complete a state-approved certification program. These requirements vary greatly from state to state. What are the insured's state requirements on certification of administrators? Additionally, many administrators annually accumulate continuing education units (CEUs) appropriate to the scope of services provided. These CEUs may be approved by the state's board of nursing facility administrators, board of nursing, board of social work, or other appropriate state agency.

Obtain a full disclosure of ownership and an annual operating budget and financial statement on the insured's facility. State licensure and federal certification reports are public records and should also be obtained. Does the insured maintain incident and accident report files? Determine if these report files are submitted to the proper authority as required.

Review the admin istrative policies and procedures concerning admissions, transfers, discharges, charges,

payments, safekeeping of residents' valuables, and handling of residents' personal and financial affairs. Do the insured's policies and procedures protect against allegations of the mishandling of resident funds; billing for deceased or discharged residents; double-billing; improperly assigning the cost of the owners' or administrators' personal items; kickbacks; billing for services not utilized by the patient; and other financial irregularities?

Environmental Impairment Liability

Assisted living facilities will have a minor Environmental Impairment Liability. Claims may arise from improper waste disposal and water temperatures. State and local agencies have regulations for air, water, and ground pollution control. These regulations should be checked to see which ones impact upon the insured's operation of his or her facility. If the insured has a medical laboratory area on-site, the exposure for this liability will increase.

Although rare, an assisted living facility may have a laboratory on the premises. Does the insured have an on-site laboratory area? Medical laboratories handle many hazardous and toxic chemicals. Does the insured follow Environmental Protection Agency (EPA) guidelines regarding the collection and disposal of waste chemicals? What is the volume of hazardous substances in laboratory areas? In most facilities, the amount of toxic chemicals kept in the laboratories is s mall enough to make a claim unlikely.

An assisted living facility's water supply should be taken from a water system that is protected, operated, and maintained in conformance with state and local regulations. Do the insured's state and/or local regulations indicate the maximum temperature for residents' units; for example, in Vermont, hot water for use in residents' units may not exceed 110° F. In addition, water temperatures in the central kitchen and laundry areas used for sanitizing should meet local and state health department standards. What is the insured's practice? Water that is unsafe for drinking should be appropriately labeled and segregated. Some facilities discharge their wastewater into municipal sewage systems. Wastes are compatible with municipal treatment facilities for the most part. However, the insured should establish in-process controls - such as mercury, barium, and silver collection procedures - to prevent the discharge of toxic, radioactive, or highly corrosive wastes. Is the insured's business connected to municipal treatment facilities? Facilities that are not so connected should treat their wastewater.

Potentially infectious or pathological wastes should be kept separate from other trash by means of colored containers and colored trash bags coverage. Some employees, such as physicians, social workers, and dietitians, may be available on call.

Employees may suffer various types of injuries, such as slips, trips, and falls. What is the level of housekeeping? Areas should be kept free of debris and clutter. Trash and debris should be removed from the premises on a daily basis. What is the condition of the insured's flooring? Floors should be swept and vacuumed every day. Worn, torn, or loose floor coverings should be repaired and replaced immediately. Spills should be cleaned up immediately, and "Caution - Wet Floor" signs displayed. Is there adequate aisle space between desks in office areas? Wiring and telephone cords should not be stretched across aisles or walkways.

Employees are subject to repetitive motion injuries, such as carpal tunnel syndrome, as a result of their use of computers, typewriters, and calculators. In addition, direct care personnel may suffer back injuries, including sprains, strains, dislocations, and hernias, resulting from lifting residents who may have fallen

or need assistance with getting out of bed. In addition, back injuries may result from maneuvering patients in wheelchairs (e.g., placing strain on the employee's back or muscles, or incorrectly turning their bodies to push or pull the chair). Lifting heavy objects may also cause these injuries. Does the insured instruct all employees in proper lifting techniques? Employees should be encouraged to obtain help before moving o r lifting residents and heavy items.

Service personnel (e.g., laundry, food service, maintenance) may experience other types of injuries, including cuts, burns, and eye and skin irritations. For employees who work in the food service area, cuts from kitchen equipment may be common. What is the layout of the kitchen, including the arrangement of the equipment? How are knives and other sharp objects stored? Burns from kitchen stoves and grills may also occur. Are employees trained in the proper use and safety of kitchen equipment?

In facilities where employees serve food to residents in dining areas, are servers trained how to properly carry trays and hot dishes? To accommodate a large number of residents, employees may be hurried as they deliver food to the tables. Are employees instructed to warn other employees when they are nearby with hot dishes or heavy trays? Burns can be prevented if cooks use padded mittens to handle pots.

Does the insured have a laundry operation on the premises? Laundry personnel may be exposed to lifting injuries, steam and hot water burns, iron burns, and irritating detergents. Floors are often wet and slippery in these areas; falls may be common. Are "Caution - Wet Floor" signs posted in laundry areas? Are spills, such as water puddles caused by washers, mopped up immediately?

Maintenance workers may be injured while making indoor repairs and while cleaning the facility areas. Falls and tool-related injuries are major exposures for these workers. Do the insured's employees make repairs to outdoor pools or grounds? Are they trained on proper safety precautions in these areas (e.g., not using electrical appliances or tools near water)?

Employees may be exposed to a variety of communicable diseases. Though less likely, employees may also be exposed to serious bloodborne pathogens, such as HIV and hepatitis B. Are employees advised to get a hepatitis B vaccination? Is the insured in compliance with OSHA standard 1910.1030, Bloodborne Pathogens? Handwashing is the most common preventive measure against the spread of communicable diseases. Are all employees required to wash their hands with soap and water before preparing and serving food, after using the restroom, after assisting a resident in the restroom, and after caring for a sick or injured person?

What kinds of personal protective equipment does the insured provide for employees for dealing with bloodborne pathogens and other infections? When there is occupational exposure, the insured should provide employees with appropriate personal protective equipment (e.g., gloves, gowns, laboratory coats, face shields or eye protection, mouthpieces, resuscitation bags or other ventilation devices). During normal use, this equipment should prevent blood or other potentially infectious fluids from reaching employees' work clothes, street clothes, undergarments, and skin, eyes, mouth, or mucous membranes. Is the insured in compliance with OSHA standards 1910.133, Eye and Face Protection, and 1910.134, Respiratory Protection?

Is the insured in compliance with OSHA standard 1910.138, Hand Protection? Gloves should be worn when it may be reasonably anticipated that an employee may have hand contact with blood or other potentially infectious fluid, or when handling or touching contaminated items or surfaces. Disposable, single-use gloves must be discarded as soon as their ability to act effectively has been compromised; disposable gloves must not be washed or otherwise reused. Hypoallergenic gloves, glove liners, powderless gloves, or other measures should be provided for employees who may be allergic to the gloves normally provided.

Although rare, an assisted living facility may house a medical laboratory area to process results or blood work on residents. Does the insured's facility have such an area? If so, employees working in a medical laboratory may be exposed to toxic, caustic, and acidic chemicals. What chemicals does the insured use and store? Containers of hazardous chemicals (e.g., acetone, benzene, ethyl alcohol) should be labeled clearly and contain appropriate warning statements. Are emergency overhead showers or hoses and eyewash fountains provided in case of an emergency? It is advisable that laboratory areas stock special spill kits, chemical antidotes, and first aid kits.

Are any pre-employment examinations done? Because some staff may be called upon to lift residents or heavy equipment, they will require physical strength and agility. A re the insured's physical exams designed to test individuals' strength and agility? Some facilities perform a his coverage typically includes clothing, personal effects (e.g., radios and televisions), and additional personal items. Money and securities are not covered.

Does the insured store prescription medications on the premises? All drugs and medications should be kept in a locked cabinet or closet with limited access to employees; daily inventories should be taken. Does the insured have a system for recording medication withdrawals? Determine the insured's security methods. Are personnel required to wear identification badges? If so, determine if these badges designate who has access to medications and drugs.

What type of security measures is taken by the insured to protect the premises? It is recommended that service areas (e.g., laundry, food service) be kept locked at all times. All exit doors should be equipped with double- cylinder, dead-bolt locks; windows should be equipped with tamperproof locks. Do residents have their own lockable doors in their units or apartments? Parking lots and sidewalks should be well lit. What type of alarm system does the insured have installed? Ideally, the insured's alarm system should be connected to a central-station alarm monitoring facility. What is the response time of the local police?

Fire and E.C.

There will be a moderate Fire and E.C. exposure for assisted living facilities. Primary ignition sources include inadequate wiring, s moking, kitchen and cooking equipment, laundry facilities, and malfunctioning electronic equipment. Reducing the ignition sources will minimize the potential for fires and explosions. The fire load for these facilities includes furnishings, cleaning materials, trash, and paper products.

What are the age, type, condition, construction, and layout of the insured's premises? The majority of facilities are freestanding; however, they may also be part of a continuing-care retirement community, seniors' apartment complex, or wing or floor of a nursing home. Facilities vary in terms of size. Typically, assisted living facilities range from 40 to 120 units. These businesses may be housed in converted buildings or in newly constructed facilities. The structure may be made of wood, brick, or masonry. Doe s the insured share a building with other facilities? Adjacent facilities should be separated by a firewall that extends to the ceiling. What are the hazards presented by nearby occupancies?

What is the layout of the premises? Assi sted living facilities generally consist of a lobby, kitchen, administrative offices, medical and treatment areas, a common dining hall, employee lounges, restrooms, and a parking lot. Common areas may include sun porches, a veranda, a library, a fully-equipped kitchen designed for food preparation or a warming kitchen where food can be kept at proper serving temperatures, administrative offices, a medical or first aid office, activity rooms, gardens, a library, TV rooms, a beauty parlor/barber shop, and fitness rooms. Individual units, apartments, or shared rooms may be clustered in groupings of six to eight, and they generally contain a bedroom, bath, closets, and kitchenette. They often open in a suite-like fashion into a common sitting area or s mall living room.

Ignition sources typically include electrical wiring, kitchen appliances, laundry equipment, electrical equipment, heating equipment, and chemicals (if a medical laboratory is present on the premises). In older buildings, heating equipment (e.g., gas or electric furnace) may be inadequate or in poor condition. Is the heating system regularly inspected and maintained by a qualified professional? A poorly maintained heating system could ignite nearby combustible materials and cause a fire to spread throu gh the whole building. Many resident apartments or units have individually controlled heating and air conditioning systems. What type of systems do the insured's resident units have in place? How often are these systems inspected and maintained?

What is the age, type, and condition of all electrical equipment used by the insured? Office areas may contain typewriters, computers, desk lights, and other equipment that may be electrically powered. Individual units and common areas may also contain electrical appliances (e.g., TVs, VCRs, stereos). In addition, some medical equipment (e.g., X-ray machines, treatment lamps) may be electrically powered. All electrical equipment should be in good repair, inspected regularly, and serviced by a licensed professional. What are the training, experience, and qualifications of persons who inspect and service the insured's electrical equipment?

Equipment requiring high voltage to operate is most susceptible to electrical loss and fire. If the insured operates out of a converted or renovated structure, check if any rewiring has been done and whether the new wiring is able to handle the insured's electrical needs. Wiring should be in compliance with NFPA 70, National Electrical Code. Is a planned program of scheduled inspection of all wiring and preventive maintenance by a qualified electrician conducted to reduce the possibilities of electrical accidents? Is a continuous power system or backup power source available?

Kitchen facilities will present additional ignition sources; for example, stoves, ovens, toasters, hot plates, and microwave ovens could overheat or ignite nearby combustibles, causing a fire. Does the insured have a kitchen or food warming area? W iring on all electrical appliances found in the kitchen should be inspected periodically for fraying and cracking. Are these appliances properly grounded and NRTL-listed? When in use, are kitchen appliances always supervised by an employee? The insured should designate an employee to make sure that all appliances have been turned off at the end of the day.

Storage of dry foodstuffs (e.g., flour) concentrates a high fuel loading in a relatively s mall area. Such items should be stored in covered metal bins.

Are cooking ranges protected with automatic extinguishing systems that cover both the grease producing surfaces and the exhaust ducts? Frequent cleaning of areas where grease buildup occurs is essential. Stoves should be equipped with hood and duct fire suppression systems that are inspected and cleaned regularly by a qualified contractor. Is the insured in compliance with all state and local ordinances regulating the operation of a commercial kitchen/food preparation area?

Laundry facilities contain both ignition sources and concentrations of combustibles (e.g., dryers). Malfunction of laundry equipment can cause fires that feed and spread rapidly due to accumulations of

linens. Are washers and dryers periodically serviced? The machines should be kept free of dust. Dryer exhaust ducts should be vacuumed or blown out frequently to prevent lint buildup. Is an automatic sprinkler provided at both ends of laundry chutes, at the top and in the receiving room?

Control of the storage and handling of flammable and combustible chemicals, particularly solvents, is a consideration if an assisted living facility houses a medical laboratory area. Are such chemicals stored on the premises? Unprotected gallon-size glass bottles of flammable solvents (e.g., acetone, methanol, and ethyl alcohol) are potentially dangerous. What is the insured's practice for storing and handling flammable and combustible chemicals?

Determine if the insured allows smoking on the premises. If s moking is permitted, is it restricted to certain areas? Are residents allowed to s moke in their rooms/apartments? "No Smoking" signs should be posted in all areas where smoking is prohibited. If smoking is permitted, ashtrays should be emptied into self-closing, fire-resistant containers. Where do residents dispose of smoking materials and ashes?

What are the average and maximum values exposed to loss? A typical assisted living facility will generally have many items of high value exposed to loss, such as medical equipment, whirlpools, audio/visual equipment, etc. Valuable papers and records, such as resident contracts and medical records, will be covered under Inland Marine; refer to the Inland Marine section of this classification for more information. What type of fire detection and suppression systems does the insured have in place? It is a positive underwriting sign if automatic sprinkler systems are installed in the structure. Is the insured in compliance with all fire codes? There should be a sufficient number of annually tagged and inspected Class ABC fi re extinguishers located throughout the premises, especially in kitchens, laundry areas, and resident units. These extinguishers should be used, placed, and maintained in accordance with NFPA 10, Standard on Portable Fire Extinguishers. Are extinguishers routinely serviced, and are employees trained in their use? Most facilities will be required by state and local building codes to have automatic sprinkler systems installed within the buildings and in individual living quarters. Does the insured hav e a sprinkler system in place in each resident's quarters? Determine if the insured has a sufficient number of smoke detectors in the facility and in each resident unit.

Does the insured maintain a written fire control and evacuation plan? These plans should be appropriately posted in each facility in a conspicuous place and kept up-to-date. Check the insured's state requirements on the number of fire drills that should be performed each year. For example, in Alabama, fire drills are required to be conducted at least 12 times per year, 4 times a year on each 8-hour shift. The drills may be announced to residents and employees in advance, and the drills should involve the actual evacuation of all residents to an assembly point as specified in the emergency plan and should provide residents with experience in exiting through all exits required by the state's code. What is the insured's practice?

Is the insured's business connected to a central-station alarm monitoring system? Instructions for fire emergencies, including emergency contact telephone numbers, should be clearly posted throughout the premises. Has the insured taken part in any pre-fire planning service? Determine the response time of the local fire service.

It is possible that a moral hazard may exist. How long has the insured been in business? Determine the facility's financial situation. The underwriter should examine the insured's financial statements for the last three to five years. What is the level of competition in the area?

Business Interruption

The Business Interruption exposure for assi sted living facilities will be substantial. If the insured operates a larger facility where many individuals reside, there may be difficulty in finding replacement space. Additionally, most insureds will likely choose to remain in the area where the previous center was located. Consequently, many insureds may choose to rebuild rather than to relocate.

Determine the time needed to rebuild or relocate; compliance with state governmental building standards may increase the time needed to rebuild. Since some of the residents may have no other place to reside (e.g., due to having sold a home to move into the facility), it may be difficult for them to seek immediate residence at another location. However, if they do seek residence at another facility, it may be difficult to attract those clients back to the insured's business once the facility has been rebuilt. Does the insured have an emergency backup plan in case the facility becomes unusable? Does the insured own or lease the premises? Depending on the severity of the damage to the premises, the facility may be operational while repairs are being done.

Relocation of patients may be necessary due to fire or related perils. Does the insured own another facility?

How long would it take to find nearby replacement space if the insured is unable to rebuild? Extra Expense coverage may be needed to cover the cost of renting an alternative facility. Insureds who decide to relocate will probably prefer to find replacement space in the vicinity of the original center to prevent the loss of most of their residents. Some insureds will have contingency plans in place prior to loss to ensure no interruption. What is the insured's practice?

Does the insured depend more on location or on reputation? As the number of elderly citizens continues to increase, the demand for assisted living facilities rises. Facilities are generally not dependent on specific locations, as the need for these facilities is nationwide. However, insureds may prefer to operate a facility somewhere that is more heavily populated, such as an urban or suburban area. According to the Assisted Living Federation of A merica, the location of an assisted living residence may determine the problems and challenges that the provider may experience. Urban locations tend to require higher

development/construction and labor costs while potentially providing, in the "right" location, a significant pool of income- and age-qualified residents. Suburban locations tend to require a strong sponsor/resident relationship where typically a parent is being moved closer to an adult child's family. A rural locale often results in lower development/construction costs and sometimes has less competition, but may require an operator to broaden his or her marketing to a larger geographic area in order to draw enough residents. What is the length of time needed to replace equipment? Ascertain whether medical equipment and supplies are easily replaceable. In general, most equipment and supplies typical of a standard assisted living facility will be readily available from local suppliers, and therefore, are not difficult to replace. However, some equipment, such as medical equipment, whirlpools, and audiovisual equipment, may be expensive to replace; this may increase the exposure. Loss of patients' records could cause a substantial delay in reopening. Does the insured have a policy on periodic backup of records?

Coverage for a loss of electrical power may be needed. In the event of a substantial power loss that cannot be restored by a backup system, the insured may have to make arrangements for relocating patients to other facilities. What is the insured's practice?

Inland Marine

There will be a moderate Inland Marine exposure for assisted living facilities. Insureds will likely require coverage for Goods in Transit, Electronic Data Processing (EDP), Accounts Receivable, and Valuable Papers and Records.