Chapter 10

Capital Markets and the Pricing of Risk

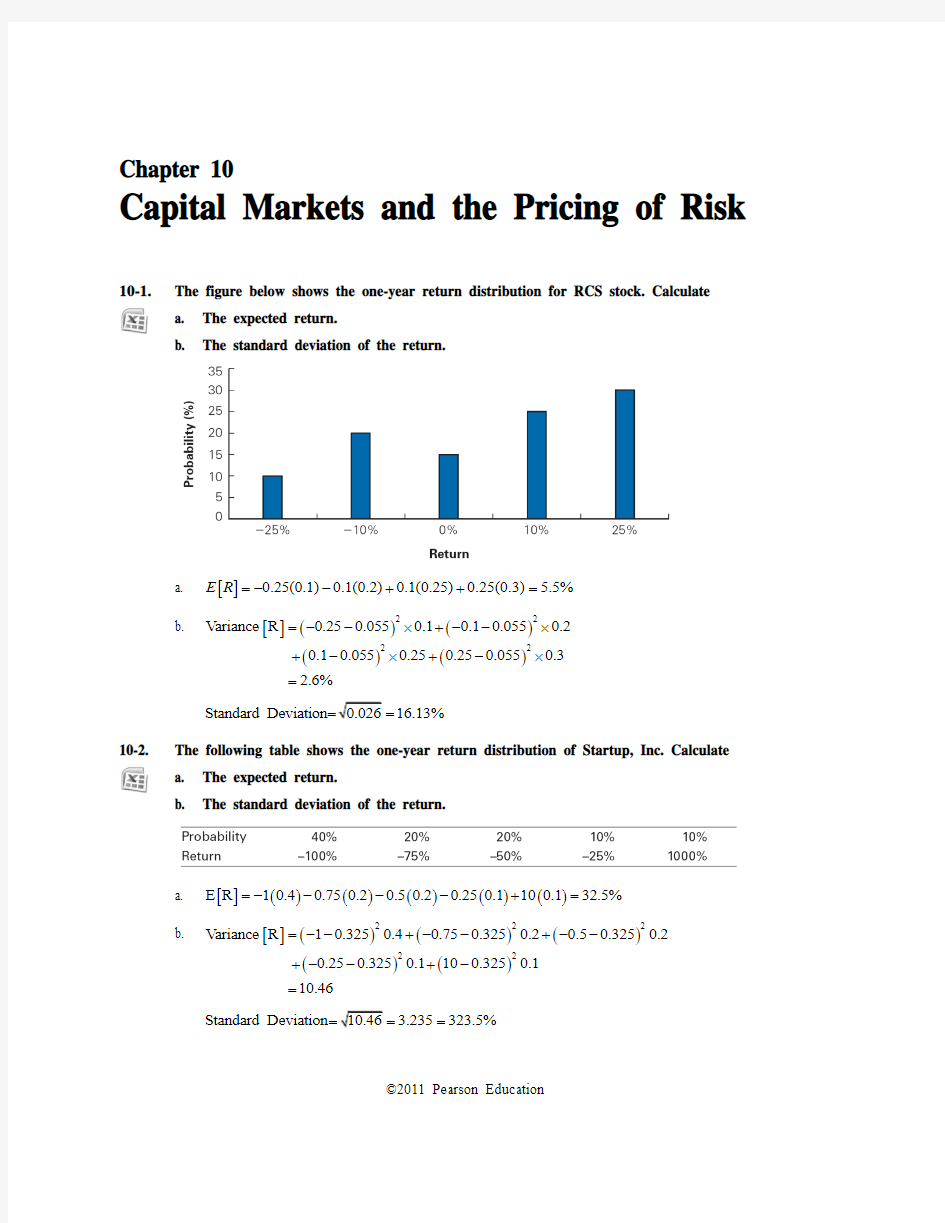

10-1.

The figure below shows the one-year return distribution for RCS stock. Calculate a. The expected return.

b.

The standard deviation of the return.

a.

[]0.25(0.1)0.1(0.2)0.1(0.25)0.25(0.3) 5.5%E R =--++=

b. []()()()()2

2

22

Variance R 0.250.0550.10.10.0550.20.10.0550.250.250.0550.32.6%

=--?+--?+-?+-?=

Standard Deviation 16.13%

10-2.

The following table shows the one-year return distribution of Startup, Inc. Calculate a. The expected return.

b.

The standard deviation of the return.

a.

[]()()()()()E R 10.40.750.20.50.20.250.1100.132.5%=----+=

b. []()()()()()2

2

2

22

Variance R 10.3250.40.750.3250.20.50.3250.20.250.3250.1100.3250.110.46

=--+--+--+--+-=

Standard Deviation 3.235323.5%==

Berk/DeMarzo?Corporate Finance, Second Edition135 10-3. Characterize the difference between the two stocks in Problems 1 and 2. What trade-offs would you face in choosing one to hold?

Startup has a higher expected return, but is riskier. It is impossible to say which stock I would prefer. It depends on risk performances and what other stocks I’m holding.

10-4. You bought a stock one year ago for $50 per share and sold it today for $55 per share. It paid a $1 per share dividend today.

a. What was your realized return?

b. How much of the return came from dividend yield and how much came from capital gain?

Compute the realized return and dividend yield on this equity investment.

a.

1(5550)

0.1212%

50

R

+-

===

b.

div 1

2% 50

R==

capital gain 5550

10% 50

R

-

==

The realized return on the equity investment is 12%. The dividend yield is 10%.

10-5. Repeat Problem 4 assuming that the stock fell $5 to $45 instead.

a. Is your capital gain different? Why or why not?

b. Is your dividend yield different? Why or why not?

Compute the capital gain and dividend yield under the assumption the stock price has fallen to $45.

a.

capital gain 4550/5010%.

R=-=-Yes, the capital gain is different, because the difference between

the current price and the purchase price is different than in Problem 1.

b. The dividend yield does not change, because the dividend is the same as in Problem 1.

The capital gain changes with the new lower price; the dividend yield does not change.

10-6. Using the data in the following table, calculate the return for investing in Boeing stock from January 2, 2003, to January 2, 2004, and also from January 2, 2008, to January 2, 2009, assuming all dividends are reinvested in the stock immediately.

136 Berk/DeMarzo ? Corporate Finance, Second Edition

10-7. The last four years of returns for a stock are as follows:

a. What is the average annual return?

b. What is the variance of the stock’s returns?

c. What is the standard deviation of the stock’s returns?

Given the data presented, make the calculations requested in the question. a.

4%28%12%4%

Average annual return 10%4

-+++==

b. 2222

(4%10%)(28%10%)(12%10%)(4%10%)Variance of returns 3

0.01867

--+-+-+-==

c. Standard deviation of returns 13.66%=

The average annual return is 10%. The variance of return is 0.01867. The standard deviation of returns

is 13.66%.

10-8.

Assume that historical returns and future returns are independently and identically distributed and drawn from the same distribution.

a. Calculate the 95% confidence intervals for the expected annual return of four different

investments included in Tables 10.3 and 10.4 (the dates are inclusive, so the time period spans 83 years). b. Assume that the values in Tables 10.3 and 10.4 are the true expected return and volatility

(i.e., estimated without error) and that these returns are normally distributed. For each

Berk/DeMarzo ? Corporate Finance, Second Edition 137

investment, calculate the probability that an investor will not lose more than 5% in the next year? (Hint : you can use the function normdist(x ,mean,volatility,1) in Excel to compute the probability that a normally distributed variable with a given mean and volatility will fall below x .)

c. Do all the probabilities you calculated in part (b) make sense? If so, explain. If not, can you

identify the reason?

Investment

Return Volatility (Standard Deviation) Average Annual Return Standard Error Lower Bound Confidence Interval Upper Bound Confidence Interval Part b answer Small stocks 41.50% 20.90% 4.56% 11.79% 30.01% 26.63% 73.37% S&P 500 20.60% 11.60% 2.26% 7.08% 16.12% 21.02% 78.98% Corporate bonds 7.00% 6.60% 0.77% 5.06% 8.14% 4.87% 95.13% Treasury bills

3.10%

3.90%

0.34%

3.22%

4.58%

0.20%

99.80%

c. No. You cannot lose money on Treasury Bills. The problem is that the returns to Treasuries are

not normally distributed.

10-9.

Consider an investment with the following returns over four years:

a. What is the compound annual growth rate (CAGR) for this investment over the four years?

b. What is the average annual return of the investment over the four years?

c. Which is a better measure of the investment’s past performance?

d. If the investment’s returns are independent and identically distributed, which is a better

measure of the investment’s expected return next year? a.

b. see table above

c. CAGR

d. Arithmetic average

138Berk/DeMarzo?Corporate Finance, Second Edition

10-10. Download the spreadsheet from MyFinanceLab that contains historical monthly prices and dividends (paid at the end of the month) for Ford Motor Company stock (Ticker: F) from

August 1994 to August 1998. Calculate the realized return over this period, expressing your answer in percent per month.

Ford Motor Co (F)

Month Stock Price Div idend Return1+R

Aug-9743.0000.05199 1.05199

Jul-9740.8750.4200.08671 1.08671

Jun-9738.0000.01333 1.01333

May-9737.5000.07914 1.07914

Apr-9734.7500.4200.12096 1.12096

Mar-9731.375-0.045630.95437

Feb-9732.8750.02335 1.02335

Jan-9732.1250.3850.00806 1.00806

Dec-9632.250-0.015270.98473

Nov-9632.7500.04800 1.04800

Oct-9631.2500.3850.01232 1.01232

Sep-9631.250-0.067160.93284

Aug-9633.5000.03475 1.03475

Jul-9632.3750.3850.01189 1.01189

Jun-9632.375-0.113010.88699

May-9636.5000.01742 1.01742

Apr-9635.8750.3500.05382 1.05382

Mar-9634.3750.10000 1.10000

Feb-9631.2500.05932 1.05932

Jan-9629.5000.3500.03377 1.03377

Dec-9528.8750.02212 1.02212

Nov-9528.250-0.017390.98261

Oct-9528.7500.350-0.065060.93494

Sep-9531.1250.01220 1.01220

Aug-9530.7500.06034 1.06034

Jul-9529.0000.310-0.014790.98521

Jun-9529.7500.01709 1.01709

May-9529.2500.07834 1.07834

Apr-9527.1250.3100.02084 1.02084

Mar-9526.8750.02871 1.02871

Feb-9526.1250.03465 1.03465

Jan-9525.2500.260-0.084840.91516

Dec-9427.8750.02765 1.02765

Nov-9427.125-0.080510.91949

Oct-9429.5000.2600.07243 1.07243

Sep-9427.750-0.051280.94872

Aug-9429.250

Total Return (product of 1+R's) 1.67893

Equivalent Monthly return = (Total Return)^(1/36)-1 = 1.45%

Berk/DeMarzo?Corporate Finance, Second Edition139 10-11. Using the same data as in Problem 10, compute the

a. Average monthly return over this period.

b. Monthly volatility (or standard deviation) over this period.

Ford Motor Co (F)

Month Stock Price Dividend Return

Aug-9743.0000.05199

Jul-9740.8750.4200.08671

Jun-9738.0000.01333

May-9737.5000.07914

Apr-9734.7500.4200.12096

Mar-9731.375-0.04563

Feb-9732.8750.02335

Jan-9732.1250.3850.00806

Dec-9632.250-0.01527

Nov-9632.7500.04800

Oct-9631.2500.3850.01232

Sep-9631.250-0.06716

Aug-9633.5000.03475

Jul-9632.3750.3850.01189

Jun-9632.375-0.11301

May-9636.5000.01742

Apr-9635.8750.3500.05382

Mar-9634.3750.10000

Feb-9631.2500.05932

Jan-9629.5000.3500.03377

Dec-9528.8750.02212

Nov-9528.250-0.01739

Oct-9528.7500.350-0.06506

Sep-9531.1250.01220

Aug-9530.7500.06034

Jul-9529.0000.310-0.01479

Jun-9529.7500.01709

May-9529.2500.07834

Apr-9527.1250.3100.02084

Mar-9526.8750.02871

Feb-9526.1250.03465

Jan-9525.2500.260-0.08484

Dec-9427.8750.02765

Nov-9427.125-0.08051

Oct-9429.5000.2600.07243

Sep-9427.750-0.05128

Aug-9429.250

Average Monthly Return 1.60%

Std Dev of Monthly Return 5.46%

a. Average Return over this period: 1.60%

b. Standard Deviation over the Period: 5.46%

140Berk/DeMarzo?Corporate Finance, Second Edition

10-12. Explain the difference between the average return you calculated in Problem 11(a) and the realized return you calculated in Problem 10. Are both numbers useful? If so, explain why.

Both numbers are useful. The realized return (in problem 10.5) tells you what you actually made if you hold the stock over this period. The average return (problem 10.6) over the period can be used as an estimate of the monthly expected return. If you use this estimate, then this is what you expect to make on the stock in the next month.

10-13. Compute the 95% confidence interval of the estimate of the average monthly return you calculated in Problem 11(a).

Month Stock Price Dividend Return

Aug-98 44.625 -0.21711

Jul-98 57.000 0.420 -0.02678

Jun-98 59.000 0.13735

May-98 51.875 0.13233

Apr-98 45.813 23.680 0.07221

Mar-98 64.813 0.14586

Feb-98 56.563 0.10907

Jan-98 51.000 0.420 0.05884

Dec-97 48.563 0.12936

Nov-97 43.000 -0.01574

Oct-97 43.688 0.420 -0.02255

Sep-97 45.125 0.04942

Aug-97 43.000 0.05199

Jul-97 40.875 0.420 0.08671

Jun-97 38.000 0.01333

May-97 37.500 0.07914

Apr-97 34.750 0.420 0.12096

Mar-97 31.375 -0.04563

Feb-97 32.875 0.02335

Jan-97 32.125 0.385 0.00806

Dec-96 32.250 -0.01527

Nov-96 32.750 0.04800

Oct-96 31.250 0.385 0.01232

Sep-96 31.250 -0.06716

Aug-96 33.500 0.03475

Jul-96 32.375 0.385 0.01189

Jun-96 32.375 -0.11301

May-96 36.500 0.01742

Apr-96 35.875 0.350 0.05382

Mar-96 34.375 0.10000

Feb-96 31.250 0.05932

Jan-96 29.500 0.350 0.03377

Dec-95 28.875 0.02212

Nov-95 28.250 -0.01739

Oct-95 28.750 0.350 -0.06506

Sep-95 31.125 0.01220

Aug-95 30.750 0.06034

Jul-95 29.000 0.310 -0.01479

Jun-95 29.750 0.01709

May-95 29.250 0.07834

Berk/DeMarzo?Corporate Finance, Second Edition141 Month Stock Price Dividend Return

Apr-95 27.125 0.310 0.02084

Mar-95 26.875 0.02871

Feb-95 26.125 0.03465

Jan-95 25.250 0.260 -0.08484

Dec-94 27.875 0.02765

Nov-94 27.125 -0.08051

Oct-94 29.500 0.260 0.07243

Sep-94 27.750 -0.05128

Aug-94 29.250

Average Monthly Return 2.35%

Std Dev of Monthly Return 7.04%

Std Error of Estimate = (Std Dev)/sqrt(36) = 1.02%

95% Confidence Interval of average monthly return 0.31% 4.38%

10-14. How does the relationship between the average return and the historical volatility of individual stocks differ from the relationship between the average return and the historical volatility of large, well-diversified portfolios?

For large portfolios there is a relationship between returns and volatility—portfolios with higher returns have higher volatilities. For stocks, no clear relation exists.

10-15. Download the spreadsheet from MyFinanceLab containing the data for Figure 10.1.

a. Compute the average return for each of the assets from 1929 to 1940 (The Great Depression).

b. Compute the variance and standard deviation for each of the assets from 1929 to 1940.

c. Which asset was riskiest during the Great Depression? How does that fit with your intuition?

a/b.

S&P 500 Small Stocks Corp Bonds

World

Portfolio Treasury Bills CPI

Average 2.553% 16.550% 5.351% 2.940% 0.859%

Variance: 0.1018 0.6115 0.0013 0.0697 0.0002 0.0022

Standard

deviation: 31.904% 78.195% 3.589% 26.398% 1.310% 4.644%

Evaluate:

c. The riskiest assets were the small stocks. Intuition tells us that this asset class would be the riskiest. 10-16. Using the data from Problem 15, repeat your analysis over the 1990s.

a. Which asset was riskiest?

b. Compare the standard deviations of the assets in the 1990s to their standard deviations in

the Great Depression. Which had the greatest difference between the two periods?

c. If you only had information about the 1990s, what would you conclude about the relative

risk of investing in small stocks?

a. Using Excel:

S&P 500 Small Stocks Corp Bonds World Portfolio Treasury CPI

142Berk/DeMarzo?Corporate Finance, Second Edition

Bills Average 18.990% 14.482% 9.229% 12.819% 4.961% 2.935%

Variance: 0.0201 0.0460 0.0062 0.0194 0.0002 0.0002

Standard

deviation: 14.161% 21.451% 7.858% 13.938% 1.267% 1.239%

The riskiest asset class was small stocks.

b. The greatest absolute difference in standard deviation is in the small stocks asset class, which saw

standard deviation fall 56.7%. But in relative terms, the riskiness of corporate bonds rose 118%

(relative to 1940), while the riskiness of small stocks fell only 72.6% (relative to 1940 levels).

Inflation is now much less risky as well, falling in relative riskiness by 73.3%.

c. If you were only looking at the 1990s, you would conclude that small stocks are relatively less

risky than they actually are.

The results that one can derive from analyzing data from a particular time period can change depending on the time period analyzed. These differences can be large if the time periods being analyzed are short. 10-17. What if the last two decades had been “normal”? Download the spreadsheet from MyFinanceLab containing the data for Figure 10.1.

a. Calculate the arithmetic average return on the S&P 500 from 1926 to 1989.

b. Assuming that the S&P 500 had simply continued to earn the average return from (a),

calculate the amount that $100 invested at the end of 1925 would have grown to by the end

of 2008.

c. Do the same for small stocks.

a. The arithmetic average return of the S&P 500 from 1926–1989 is 12.257%.

b. Using 12.257% as the annual return during the period 1990-2008, $100 invested in the S&P 500 in

1926 would have grown to $442,618 by 2008.

c. The arithmetic average return for small stocks from 1926–1989 is 23.186%. Using 23.186% as the

annual return during the period 1990–2008, $100 invested in small stocks in 1926 would have

grown to $51,412,602 by 2008.

10-18. Consider two local banks. Bank A has 100 loans outstanding, each for $1 million, that it expects will be repaid today. Each loan has a 5% probability of default, in which case the bank is not repaid anything. The chance of default is independent across all the loans. Bank B has only one loan of $100 million outstanding, which it also expects will be repaid today. It also has a 5% probability of not being repaid. Explain the difference between the type of risk each bank faces.

Which bank faces less risk? Why?

The expected payoffs are the same, but bank A is less risky.

10-19. Using the data in Problem 18, calculate

a. The expected overall payoff of each bank.

b. The standard deviation of the overall payoff of each bank.

a. Expected payoff is the same for both banks

=?=

Bank B$100 million0.95$95 million

()

=??=

Bank A$1 million0.95100$95 million

b. Bank B

Berk/DeMarzo ? Corporate Finance, Second Edition 143

()()22

Variance 100950.950950.05475=-+-=

Standard Deviation 21.79

Bank A

()()2

2

Variance of each loan 10.950.9500.950.050.0475=--=

Standard Deviation of each loan 0.2179

Now the bank has 100 loans that are all independent of each other so the standard deviation of the average loan is

0.02179.

=

But the bank has 100 such loans so the standard deviation of the portfolio is

1000.02179 2.179,?= 2.1795

which is much lower than Bank B.

10-20. Consider the following two, completely separate, economies. The expected return and volatility

of all stocks in both economies is the same. In the first economy, all stocks move together —in good times all prices rise together and in bad times they all fall together. In the second economy, stock returns are independent —one stock increasing in price has no effect on the prices of other stocks. Assuming you are risk-averse and you could choose one of the two economies in which to invest, which one would you choose? Explain.

A risk-averse investor would choose the economy in which stock returns are independent because this risk can be diversified away in a large portfolio.

10-21. Consider an economy with two types of firms, S and I. S firms all move together. I firms move

independently. For both types of firms, there is a 60% probability that the firms will have a 15% return and a 40% probability that the firms will have a ?10% return. What is the volatility (standard deviation) of a portfolio that consists of an equal investment in 20 firms of (a) type S, and (b) type I?

a.

[]()()E R 0.150.60.10.40.05=-=

Standard Deviation 0.12247=

Because all S firms in the portfolio move together there is no diversification benefit. So the standard deviation of the portfolio is the same as the standard deviation of the stocks —12.25%. b. []()()E R 0.150.60.10.40.05=-=

Standard Deviation 0.12247=

Type I stocks move independently. Hence the standard deviation of the portfolio is ()SD Portfolio of 20 Type I stocks 2.74%.

=

=

144Berk/DeMarzo?Corporate Finance, Second Edition

10-22. Using the data in Problem 21, plot the volatility as a function of the number of firms in the two portfolios.

Berk/DeMarzo?Corporate Finance, Second Edition145

10-23. Explain why the risk premium of a stock does not depend on its diversifiable risk.

Investors can costlessly remove diversifiable risk from their portfolio by diversifying. They, therefore, do not demand a risk premium for it.

10-24. Identify each of the following risks as most likely to be systematic risk or diversifiable risk:

a. The risk that your main production plant is shut down due to a tornado.

b. The risk that the economy slows, decreasing demand for your firm’s products.

c. The risk that your best employees will be hired away.

d. The risk that the new product you expect your R&D division to produce will not materializ

e.

a. diversifiable risk

b. systematic risk

c. diversifiable risk

d. diversifiable risk

10-25. Suppose the risk-free interest rate is 5%, and the stock market will return either 40% or ?20% each year, with each outcome equally likely. Compare the following two investment strategies: (1)

invest for one year in the risk-free investment, and one year in the market, or (2) invest for both years in the market.

a. Which strategy has the highest expected final payoff?

b. Which strategy has the highest standard deviation for the final payoff?

c. Does holding stocks for a longer period decrease your risk?

R(i) : (1.05)(1.40)-1 = 47% or (1.05)(0.80) –1 = –16%

R(ii) : 1.42 -1 = 96%, 1.4 × 0.8 – 1 = 12%, 0.8 × 1.4 – 1=12%, .8 × .8 – 1 = –36%

a. ER(i) = (47% – 16%)/2 = 15.5%

ER(ii) = (96% + 12% + 12% – 36%)/4 = 21%

b. Vol(i) =sqrt(1/2 (47% – 15.5%)2 + 1/2(–16% – 15.5%)2) = 31.5%

Vol(ii)=sqrt(1/4 (96%-21%)2 + ?(12% – 21%)2 + 1/4(–36% – 21%)2) = 47.5%

c. No

10-26. Download the spreadsheet from MyFinanceLab containing the realized return of the S&P 500 from 1929–2008. Starting in 1929, divide the sample into four periods of 20 years each. For each

20-year period, calculate the final amount an investor would have earned given a $1000 initial investment. Also express your answer as an annualized return. If risk were eliminated by holding stocks for 20 years, what would you expect to find? What can you conclude about long-run diversification?

146 Berk/DeMarzo ? Corporate Finance, Second Edition

If risk were eliminated by holding stocks for 20 years, you would expect to find similar returns for all four periods, which you do not.

10-27. What is an efficient portfolio?

An efficient portfolio is any portfolio that only contains systemic risk; it contains no diversifiable risk.

10-28. What does the beta of a stock measure?

Beta measures the amount of systemic risk in a stock

10-29. You turn on the news and find out the stock market has gone up 10%. Based on the data in

Table 10.6, by how much do you expect each of the following stocks to have gone up or down: (1) Starbucks, (2) Tiffany & Co., (3) Hershey, and (4) Exxon Mobil.

Beta*10% Starbucks 10.4% Tiffany & Co. 16.4% Hershey 1.9% Exxon Mobil 5.6%

10-30. Based on the data in Table 10.6, estimate which of the following investments do you expect to

lose the most in the event of a severe market down turn: (1) A $1000 investment in eBay, (2) a $5000 investment in Abbott Laboratories, or (3) a $2500 investment in Walt Disney.

For each 10% market decline, eBay down 10%*1.93 = 19.3%, 19.3% × 1000 = $193 loss; Abbott down 10%*.18 = 1.8%, 1.8% × 5000 = $90 loss; Disney down 10%*.96 = 9.6%, 9.6% × 2500 = $240 loss; Disney investment will lose most.

10-31. Suppose the market portfolio is equally likely to increase by 30% or decrease by 10%.

a. Calculate the beta of a firm that goes up on average by 43% when the market goes up and

goes down by 17% when the market goes down . b. Calculate the beta of a firm that goes up on average by 18% when the market goes down and

goes down by 22% when the market goes up . c. Calculate the beta of a firm that is expected to go up by 4% independently of the market. a.

()()4317 Stock 60Beta 1.5 Market 301040

--?=

===?--

b. () Stock 182240

Beta 1 Market 301040

?---=

===-?--

c. A firm that moves independently has no systemic risk so Beta = 0

Berk/DeMarzo ? Corporate Finance, Second Edition 147

10-32. Suppose the risk-free interest rate is 4%.

a. i. Use the beta you calculated for the stock in Problem 31(a) to estimate its expected return.

ii. How does this compare with the stock’s actual expected return?

b. i. Use the beta you calculated for the stock in Problem 31(b) to estimate its expected return.

ii. How does this compare with the stock’s actual expected return? a. E[R M ] = ? (30%) + ? (–10%) = 10% i.. E[R] = 4% + 1.5 (10% – 4%) = 13% ii. Actual Expected return = (43% – 17%) / 2 = 13% b. i. . E[R] = 4% – 1(10% – 4%) = -2%

ii. Actual l expected Return =

(–22% + 18%) / 2 = –2%

10-33. Suppose the market risk premium is 5% and the risk-free interest rate is 4%. Using the data in

Table 10.6, calculate the expected return of investing in

a. Starbucks’ stock.

b. Hershey’s stock.

c. Autodesk’s stock. a. 4%+1.04 × 5% = 9.2% b. 4% + 0.19 × 5% = 4.95% c. 4% + 2.31 × 5% = 15.55%

10-34. Given the results to Problem 33, why don’t all investors hold Autodesk’s stock rather than Hershey’s stock?

Hershey’s stock has less market risk, so investors don’t need as high an expected return to hold it. Hershey’s stock will perform much better in a market downturn.

10-35. Suppose the market risk premium is 6.5% and the risk-free interest rate is 5%. Calculate the

cost of capital of investing in a project with a beta of 1.2.

[]()()Cost of Capital E R 5 1.26.512.8%f m f r r β=+-=+=

10-36. State whether each of the following is inconsistent with an efficient capital market, the CAPM, or

both:

a. A security with only diversifiable risk has an expected return that exceeds the risk-free

interest rate. b. A security with a beta of 1 had a return last year of 15% when the market had a return of

9%. c. Small stocks with a beta of 1.5 tend to have higher returns on average than large stocks with

a beta of 1.5. a. This statement is inconsistent with both. b. This statement is consistent with both.

c. This statement is inconsistent with the CAPM but not necessarily with efficient capital markets.

Chapter 10 Return and Risk: The Capital-Assets-Pricing Model Multiple Choice Questions 1. When a security is added to a portfolio the appropriate return and risk contributions are A) the expected return of the asset and its standard deviation. B) the expected return and the variance. C) the expected return and the beta. D) the historical return and the beta. E) these both can not be measured. Answer: C Difficulty: Medium Page: 255 2. When stocks with the same expected return are combined into a portfolio A) the expected return of the portfolio is less than the weighted average expected return of the stocks. B) the expected return of the portfolio is greater than the weighted average expected return of the stocks. C) the expected return of the portfolio is equal to the weighted average expected return of the stocks. D) there is no relationship between the expected return of the portfolio and the expected return of the stocks. E) None of the above. Answer: C Difficulty: Easy Page: 261 3. Covariance measures the interrelationship between two securities in terms of A) both expected return and direction of return movement. B) both size and direction of return movement. C) the standard deviation of returns. D) both expected return and size of return movements. E) the correlations of returns. Answer: B Difficulty: Medium Page: 258-259 Use the following to answer questions 4-5: GenLabs has been a hot stock the last few years, but is risky. The expected returns for GenLabs are highly dependent on the state of the economy as follows: State of Economy Probability GenLabs Returns Depression .05 -50% Recession .10 -15 Mild Slowdown .20 5 Normal .30 15% Broad Expansion .20 25 Strong Expansion .15 40

综合接入中级级题库 一、是非题: 1.(√)PBX设备E1中继输出负载阻抗为75欧电阻(不平衡)或120欧(平衡)。 2.(×)PRI信令需要信令点编码。 3.(√)程控交换机是一个专用的计算机系统,由硬件和软件两部分所组成。 4.(√)E1接口共32时隙,每时隙速率为64Kbps, 64Kbpsх32=2,048,000bps,故E1口又 称为2M口。 5.(×)在 Windows 中,ping命令的-n 选项表示ping的网络号。 6.(√)空中接口Um进行数据包切割是由RLC层完成的。 7.(√)SDH具有路由自动选择功能,上下电路方便,维护、控制、管理功能强,标准统 一,便于传输更高速率的业务等优点。 8.(×)光纤收发器是媒体转换器,其主用功能是实现适合双绞线媒质(10BASE-TX、 100BASE-TX)传输的以太网信号和适合传输媒质(E1)传输的以太网信号之间的相互转换。 9.(√)虚拟网络是建立在局域网交换机或ATM交换机之上的,它以软件方式来实现逻辑 工作组的划分与管理,逻辑工作组的结点组成不受物理位置的限制。 10.(√)无线宽带接入系统由中心基站(HE)、远端站(CPE)和网络管理系统三部分组成。 11.光纤收发器纯粹是物理层的转换,用来把光纤信号转换成E1信号。 12.(√)协议转换器是把光端机的同步信号应用的某种协议转换为以太或者其他路由器或 者交换机可以接受的协议的一个设备。 13.(√)“光猫”是利用一对光纤进行单E1或单V.35或单10BaseT点到点式的光传输终 端设备。 14.(√)路由器是一种用于网络互连的计算机设备,但作为路由器,并不具备减少数据帧 的冲突和碰撞的作用。 15.(×)OSI参考模型描述的物理层,实现的主要功能在于提出了物理层比特流传输中的 差错控制方法。 16.(×)无盘工作站向服务器申请IP地址时,使用的是TCP协议。 17.(√)子网掩码产生在OSI参考模型的网络层。 18.(√)RFC文档是IETF 标准化组织的工作文件。 19.(√)从网络的层次结构考虑,一个IP地址必须指明两点:1、属于哪个网络 2、是 这个网络中的哪台主机。 20.(√)数据通信网是指为提供数据传输业务而建立和运营的网络,可分为公用数据网和 专用数据网。 21.(√)IP头中的生存期字段用于确定一个TCP/IP包未交付前可在网络上移动的时间。 22.(√)VLAN在现代组网技术中占有重要地位,同一个VLAN中的两台主机可以跨越多台 交换机。 23.(√)国内No.7信令网采用由HSTP、LSTP和SP组成的三级信令网。 24.(×)第3层交换机是靠mac地址来完成数据的转发。 25.(×)路由器是靠ip地址来完成数据的转发。 26.(×)两台主机在对ping过程中,主机ip地址可以不设在一个网段内,但必须设网关地 址。 27.(√)双绞线接法的标准有:EIA/TIA568B 标准和EIA/TIA568A标准。 28.(√)E1口共32个时隙。 29.(√)“位(bit)”是电子计算机中最小的数据单位,1个“字节(Byte)”= 8 个“位

项目一财务管理总体认知 一、单项选择题 1.下列各项企业财务管理目标中,能够同时考虑资金的时间价值和投资风险因素的是( D )。 A.产值最大化 B.利润最大化 C.每股收益最大化 D.企业价值最大化 2.企业筹资活动的最终结果是( D )。 A.银行借款 B.发行债券 C.发行股票 D.资金流入 7.相对于每股收益最大化目标而言,企业价值最大化目标的不足之处是( D )。 A.没有考虑资金的时间价值 B.没有考虑投资的风险价值 C.不能反映企业潜在的获利能力 D.某些情况下确定比较困难 9.下列法律法规同时影响企业筹资、投资和收益分配的是( A )。 A.公司法 B.金融法 C.税法 D.企业财务通则 10.在市场经济条件下,财务管理的核心是( B )。 A.财务预测 B.财务决策 C.财务控制 D.财务分析 二、多项选择题 2.企业财务管理的基本内容包括( ACD )。 A. 筹资决策 B.技术决策 C.投资决策 D.盈利分配决策 3.财务管理的环境包括( ABCD )。 A.技术环境 B.经济环境 C.金融环境 D.法律环境 4.以下项目中属于“利润最大化”目标存在的问题有( ABCD )。 A.没有考虑利润实现时间和资金时间价值 B.没有考虑风险问题 C.没有反映创造的利润与投入的资本之间的关系 D.可能导致企业短期财务决策倾向,影响企业长远发展

5.以股东财富最大化作为财务管理目标存在的问题有( ABC )。 A.通常只适用于上市公司 B.股价不能完全准确反映企业财务管理状况 C.对其他相关者的利益重视不够 D.没有考虑风险因素 6.下列财务管理的目标当中,考虑了风险因素的有( BCD )。 A.利润最大化 B.股东财富最大化 C.企业价值最大化 D.相关者利益最大化 7.在分配活动中,企业财务管理的核心任务是( BC )。 A. 确定筹资结构 B. 确定分配规模 C.确定分配方式 D. 确定投资方向 8.利润最大化目标和每股利润最大化目标存在的共同缺陷有( ABD )。 A.没有考虑货币时间价值 B.没有考虑风险因素 C.没有考虑利润与资本的关系 D. 容易导致短期行为 11.下列属于货币市场工具的有( BD )。 A.股票 B.短期国库券 C.债券 D.回购协议 项目二财务管理价值观念培养 一、单项选择题 2.一定时期内每期期初等额收付的系列款项是( A )。 A.即付年金 B.永续年金 C.递延年金 D.普通年金 4.年内复利m次时,其名义利率r与实际利率i之间的关系是( A )。 A.i=(1+r/m)m-1 B. i=(1+r/m)-1 C.i=(1+r/m)-m -1 D. i=l-(1+r/m)-m 5.甲某拟存入一笔资金以备3年后使用。假定银行3年期存款年利率为5%,甲某3年后需用的资金总额为34 500元,则在单利计息情况下,目前需存入的资金为( A )元。 A.30 000 B.29 803.04 C.32 857.14 D.31 500 6.如果某人5年后想拥有50 000元,在年利率为5%、单利计息的情况下,他现在必

CHAPTER 2 Financial Statements & Cash Flow Multiple Choice Questions: I. DEFINITIONS BALANCE SHEET b 1. The financial statement showing a firm’s accounting value on a particular date is the: a. income statement. b. balance sheet. c. statement of cash flows. d. tax reconciliation statement. e. shareholders’ equity sheet. Difficulty level: Easy CURRENT ASSETS c 2. A current asset is: a. an item currently owned by the firm. b. an item that the firm expects to own within the next year. c. an item currently owned by the firm that will convert to cash within the next 12 months. d. the amount of cash on hand the firm currently shows on its balance sheet. e. the market value of all items currently owned by the firm. Difficulty level: Easy LONG-TERM DEBT b 3. The long-term debts of a firm are liabilities: a. that come due within the next 12 months. b. that do not come due for at least 12 months. c. owed to the firm’s suppliers. d. owed to the firm’s shareholders. e. the firm expects to incur within the next 12 months. Difficulty level: Easy NET WORKING CAPITAL e 4. Net working capital is defined as: a. total liabilities minus shareholders’ equity. b. current liabilities minus shareholders’ equity. c. fixed assets minus long-term liabilities. d. total assets minus total liabilities. e. current assets minus current liabilities. Difficulty level: Easy LIQUID ASSETS d 5. A(n) ____ asset is on e which can be quickly converted into cash without significant loss in value.

集团客户互联网专线解决方案 运营商全业务运营的竞争激烈程度可以用三个关键词来概括:“全方位”“全品牌”“全客户”。其中对集团客户的争夺就是各家运营商竞争的焦点。面对电信、联通的传统优势市场,中国移动必须采取精细化运营管理,在提高集团客户的粘度的同时,提高自身的竞争力。 中国移动集团客户业务发展目标 在集团客户互联网专线建设中,中国电信、中国联通凭借传统的固网资源优势,在用户数量上占据绝对优势,同时通过主动关怀计划、业务捆绑、下调资费等手段不断抢夺集团客户市场。因此,在集团宽带用户规模方面,中国移动还处于相对弱势的地位,这对于中国移动的集团客户宽带建设提出了挑战。 从中国移动对集团客户业务KPI考核的角度来分析,一方面要提高集团客户信息化收入,另一方面要提高集团客户目标市场的保有率,进一步分解为四个目标: ■服务目标:需要提高客户的满意度 ■客户目标:需要迅速提高专线的数量和覆盖率 ■收入目标:需要保证信息化收入及其增长率 ■产品目标:需要考虑重要行业的信息化应用及提供全业务服务。 中国移动集团客户互联网专线建设面临的挑战 目前,各省移动公司集团客户互联网专线的组网模式基本相同,基于提高市场竞争力的考虑,移动一般都为集团客户提供路由器和接入交换机,具体组网示意如下: 在集团客户互联网专线业务方面,各省移动公司的建设部门、运维部门及市场部门面临着一系列严峻的挑战。 ■横向竞争力弱:与中国电信和中国联通相比,中国移动在互联网内容资源、出口带宽资源、非对称网间结算及运营经验等方面均存在不足,而依靠单一的产品功能或者价格很难打动客户,导致中国移动的整体竞争力弱,影响互联网专线数量的迅速增长。

1)单选题,共20题,每题5.0分,共100.0分1 单选题 (5.0分) 资产未来创造的现金流入现值称为? A. 资产的价格 B. 资产的分配 C. 资产的价值 D. 资产的体量 2 单选题 (5.0分) 谁承担了公司运营的最后风险? A. 债权人 B. 股东 C. 管理层 D. 委托人 3 单选题 (5.0分) 金融市场有哪些类型? A. 货币市场 B. 资本市场 C. 期货市场 D. 以上都是 4 单选题 (5.0分) 以下哪项是债券价值评估方式? A. 现值估价模型 B. 到期收益率 C. 债券收益率 D. 以上都是 5 单选题 (5.0分) 融资直接与间接的划分方式取决于? A. 融资的受益方 B. 金融凭证的设计方 C. 融资来源 D. 融资规模

6 单选题 (5.0分) 以下哪种不是财务分析方法? A. 比较分析 B. 对比分析 C. 趋势百分比分析 D. 财务比例分析 7 单选题 (5.0分) 以下哪个不是价值的构成? A. 现金流量 B. 现值 C. 期限 D. 折现率 8 单选题 (5.0分) 比率分析的目的是为了? A. 了解项目之间的关系 B. 了解金融发展变化 C. 分析资金流动趋势 D. 分析金融风险 9 单选题 (5.0分) 影响公司价值的主要因素是? A. 市场 B. 政策 C. 信息 D. 时间 10 单选题 (5.0分) 以下哪种是内部融资方式? A. 留存收益 B. 股票 C. 债券 D. 借款 11 单选题 (5.0分)

什么是营运资本? A. 流动资产-流动负债 B. 流动资产+流动负债 C. 流动资产*流动负债 D. 流动资产/流动负债 12 单选题 (5.0分) PMT所代表的含义是? A. 现值 B. 终值 C. 年金 D. 利率 13 单选题 (5.0分) 金融市场的作用是什么? A. 资金的筹措与投放 B. 分散风险 C. 降低交易成本 D. 以上都是 14 单选题 (5.0分) 以下哪项不是财务管理的内容? A. 筹资 B. 融资 C. 信贷 D. 营运资本管理 15 单选题 (5.0分) 微观金融的研究对象是什么? A. 机构财政 B. 账目管理 C. 股市投资 D. 公司理财 16 单选题 (5.0分) 计划经济时代企业的资金来源是?

中南大学现代远程教育课程考试复习试题及参考答案 公司理财 、名词解释 1.财务分析 2.年金 3.风险报酬 4.机会成本 5.贝他系数 6.债券 7.时间价值 8.财务杠杆 9. 信用政策10.市场风险11.经济批量12.租赁 13. 经营杠杆14. 优先股15. 资金成本16. 最优资本结构 、判断正误 1.企业价值最大化强调的是企业预期的获利能力而非实际利润() 2.企业股东、经营者、在财务管理工作中的目标是一致的,所以他们之间没有任何利害冲突() 3.对于借款企业来讲,若预测市场利率上升,应与银行签订浮动利率合同;反之,则应签订固定利率合同() 4.在终值和计息期不变的情况下,贴现率越高,则现值越小() 5.递延年金终值受递延期的影响,递延期越长,递延年金的终值越大;递延期越短,递延年金的终值越小() 6.存本取息可视为永续年金的例子() 7.在一般情况下,报酬率相同时人们会选择风险大的项目;风险相同时,会选择报酬率高的项目() 8.在期望值不同的情况下,标准离差率越大,风险越大;反之标准离差率越小,风险越小 () 9.如果一个企业的盈利能力越高,则该企业的偿债能力也一定较好() 10.产权比率高,是高风险、高报酬的财务结构;产权比率低,是低风险、低报酬的财务结构() 11. 风险和损失属于同一概念() 12.资产负债率中的负债总额不仅应包括长期负债,还应包括短期负债() 13.筹资渠道解决的是资金来源问题,筹资方式则解决通过何种方式取得资金的问题,它们之间是一一对应关系数() 14.普通股股东具有查账权,因此每位股东都可以自由查阅公司的账目() 15.一般而言而,利息保障系数越大,表明企业可以还债的可能性也越大() 16.在杠杆租赁中,出租人也是借款人() 17.现金折扣政策“ 2/10 ”表示:若在2天内付款,可以享受10%的价格优惠() 18.发行普通股筹集的资本是公司最基本的资本来源,它反映了公司的实力,可作为其他方式筹资的基础,尤其可为股东提供保障,增强公司的举债能力() 19.订货成本与企业每次订货的数量无关() 20.已获利息倍数中的“利息费用”仅指财务费用中的利息费用,而不包括计入固定资产成本中的资本化利息() 21.一般认为,补偿性余额使得其名义借款高于实际可使用款项,从而名义借款利率大于实际借款利率() 22. 优先股股东没有表决权()

政企集团客户双跨专线国际专线试题库 产品1:双跨专线(含国际专线) 一.单选题(共20题) 1、PTN 的中文含义是()。 A. 准同步数字体系 B.同步数字体系 C.分组传送网 D.波分复用 答案:C 2、WDM/OTN 技术是以()为基础 A. 准同步数字体系 B.同步数字体系 C.分组传送网 D.波分复用 答案:D 3、当业务颗粒达到10G 以上时,一般采用来()承载。 A.SDH B.PTN C.WDM/OTN D.MSTP 答案:C 5、PTN 一种基于分组交换的.面向连接的多业务承载技术,能够在传 送层更加有效地传递分组业务,并提供电信级的OAM 和保护;从技术原理来看,在安全.保护.QOS 等方面和()类似;是中国移动主推的传输技术。 A.SDH/MSTP B.OTN C.WDM D.PDH 答案:A 6、非249 家战略客户中,数据专线.MPLS-VPN 专线和静态I P 路由接入方式的互联网专线能享受到的资费折扣最低为() A.1 折 B.2 折 C.3 折 D.4 折 答案:B 7、在A PN 专线.集团短彩信.语音专线.MPLS VPN 专线中,互联网专 线中,金牌级服务客户对应的业务保障等级是() A.AAA B.AA C.A D.普通 答案:A 9、图中场景主要适用于客户的哪些需求()

A. 跨资源池调度.容灾.备份.数据迁移等场景 B. 互联网接入,刚性带宽需求。 C. 企业混合云的部署 D. 专线的快速开通和自助服务 答案:A 10、中国移动跨省专线均采用()保护技术。 A.线性1+1 保护 B.线性1:1 保护 C.线性1:N 保护 D.线性N:N 保护 答案:A 11、资源厚覆盖的定义是()。 A.将光缆自分纤点延伸至集团客户楼宇的局前井或弱电井 B.将光 缆自分纤点延伸至集团客户楼宇500 米处 C.将光缆自分纤点延伸至集团客户楼宇800 米处 D.移动光缆有两条以上的路由到达集团客户楼宇 答案:A 12、4、客户采用G E 口开通600M PTN 专线,配置C IR=600M,PIR= 800M。那么,忙时,可保证()Mbps 速率;空闲时,速率可达()Mbps。 A.600,800 B.600,1400 C.800,1400 D.800,600 答案:A 13、网络人员在业务正式开通后,应同步回复业务开通单,并将集团专线业务

【思考与练习题】部分习题参考答案 第3章 6. 该公司资产负债表为 XX公司资产负债表XX年12月31日资产期末余额负债及所有者权益期末余额 流动资产流动负债 现金及其等400 应付账款600 价物800 应交税金200 应收账款1200 流动负债合计800 流动资产合计非流动负债 非流动资产3400 应付债券700 固定资产8200 非流动负债合计700 无形资产11600 所有者权益 非流动资产合计实收资本8800 股本溢价1900 留存收益600 所有者权益合计11300 资产总计12800 资产及所有者权益合计12800 7. 公司2007年的净现金流为-25万元。 8. 各比例如下: 4. (1)1628.89 元;(2)1967.15 元;(3)2653.30 元 5. 现在要投入金额为38.55万元。 6. 8年末银行存款总值为6794.89元(前4年可作为年金处理)。 7. (1)1259.71 元;(2)1265.32 元;(3)1270.24 元;(4)1271.25 元;(5)其他条件不变的情况下,同一利息期间计息频率越高,终值越大;至琏续计算利息时达到最大值。 8. (1)每年存入银行4347.26元;(2)本年存入17824.65元。 9. 基本原理是如果净现值大于零,则可以购买;如果小于零,则不应购买。 NPV=-8718.22,小于零,故不应该购买。 第5章 8. (1)该证券的期望收益率=0.15 X 8%+0.30X 7%+0.40X 10%+0.15X 15%=9.55%

---------------------------------------- 精品文档

Chapter 20 Issuing Securities to the Public Multiple Choice Questions 1. An equity issue sold directly to the public is called: A. a rights offer. B. a general cash offer. C. a restricted placement. D. a fully funded sales. E. a standard call issue. 2. An equity issue sold to the firm's existing stockholders is called: A. a rights offer. B. a general cash offer. C. a private placement. D. an underpriced issue. E. an investment banker's issue. 3. Management's first step in any issue of securities to the public is: A. to file a registration form with the SEC. B. to distribute copies of the preliminary prospectus. C. to distribute copies of the final prospectus. D. to obtain approval from the board of directors. E. to prepare the tombstone advertisement. 4. A rights offering is: A. the issuing of options on shares to the general public to acquire stock. B. the issuing of an option directly to the existing shareholders to acquire stock. C. the issuing of proxies which are used by shareholders to exercise their voting rights. D. strictly a public market claim on the company which can be traded on an exchange. E. the awarding of special perquisites to management.

习题一 1.5.1单项选择题 1 .不能偿还到期债务是威胁企业生存的()。 A .外在原因 B .内在原因 C .直接原因 D .间接原因 2.下列属于有关竞争环境的原则的是()。 A .净增效益原则 B .比较优势原则 C .期权原则 D .自利行为原则3.属于信号传递原则进一步运用的原则是指() A .自利行为原则 B .比较优势原则 C . 引导原则 D .期权原则 4 .从公司当局可控因素来看,影响报酬率和风险的财务活动是()。 A .筹资活动 B .投资活动 C .营运活动 D .分配活动 5 .自利行为原则的依据是()。 A .理性的经济人假设 B .商业交易至少有两方、交易是“零和博弈”,以及各方都是自利的 C .分工理论 D .投资组合理论 6 .下列关于“有价值创意原则”的表述中,错误的是()。 A .任何一项创新的优势都是暂时的 B .新的创意可能会减少现有项目的价值或者使它变得毫无意义 C .金融资产投资活动是“有价值创意原则”的主要应用领域 D .成功的筹资很少能使企业取得非凡的获利能力 7 .通货膨胀时期,企业应优先考虑的资金来源是() A .长期负债 B .流动负债 C .发行新股 D .留存收益 8.股东和经营者发生冲突的根本原因在于()。 A .具体行为目标不一致 B .掌握的信息不一致 C .利益动机不同 D ,在企业中的地位不同 9 .双方交易原则没有提到的是()。 A .每一笔交易都至少存在两方,双方都会遵循自利行为原则 B .在财务决策时要正确预见对方的反映 C .在财务交易时要考虑税收的影响 D .在财务交易时要以“自我为中心” 10.企业价值最大化目标强调的是企业的()。 A .预计获利能力 B .现有生产能力 C .潜在销售能力 D .实际获利能力11.债权人为了防止其利益受伤害,通常采取的措施不包括()。 A .寻求立法保护 B .规定资金的用途 C .提前收回借款 D .不允许发行新股12.理性的投资者应以公司的行为作为判断未来收益状况的依据是基于()的要求。 A .资本市场有效原则 B .比较优势原则 C .信号传递原则 D .引导原则13.以每股收益最大化作为财务管理目标,存在的缺陷是()。 A .不能反映资本的获利水平 B .不能用于不同资本规模的企业间比较 C .不能用于同一企业的不同期间比较 D .没有考虑风险因素和时间价值 14 .以下不属于创造价值原则的是()。 A .净增效益原则 B .比较优势原则 C .期权原则 D .风险—报酬权衡原则 15. 利率=()+通货膨胀附加率+变现力附加率+违约风险附加率+到期风险附加率。 A .物价指数附加率 B .纯粹利率 C .风险附加率 D .政策变动风险 1.5.2多项选择题

CHAPTER 8 Making Capital Investment Decisions I. DEFINITIONS INCREMENTAL CASH FLOWS a 1. The changes in a firm's future cash flows that are a direct consequence of accepting a project are called _____ cash flows. a. incremental b. stand-alone c. after-tax d. net present value e. erosion Difficulty level: Easy EQUIVALENT ANNUAL COST e 2. The annual annuity stream o f payments with the same present value as a project's costs is called the project's _____ cost. a. incremental b. sunk c. opportunity d. erosion e. equivalent annual Difficulty level: Easy SUNK COSTS c 3. A cost that has already been paid, or the liability to pay has already been incurred, is a(n): a. salvage value expense. b. net working capital expense. c. sunk cost. d. opportunity cost. e. erosion cost. Difficulty level: Easy OPPORTUNITY COSTS d 4. Th e most valuable investment given up i f an alternative investment is chosen is a(n): a. salvage value expense. b. net working capital expense.

公司理财复习题 一、单选选择题 1、企业的管理目标的最优表达是(C ) A.利润最大化 B.每股利润最大化 C.企业价值最大化 D.资本利润率最大化 2、把若干财务比率用线性关系结合起来,以此评价企业信用水平的方法是(B ) A杜邦分析法B沃尔综合评分法C预警分析法D经营杠杆系数分析3、“5C”系统中的“信用品质”是指( D ) A.不利经济环境对客户偿付能力的影响 B.客户偿付能力的高低 C.客户的经济实力与财务状况 D.客户履约或赖账的可能性4、投资报酬分析最主要的分析主体是( B ) A上级主管部门B投资人C长期债人D短期债权人 5、普通年金终值系数的倒数称为( B ) A复利终值系数B偿债基金系数C普通年金现值系数D投资回收系数6、为了直接分析企业财务善和经营成果在同行中所处的地位,需要进行同业比较分析,其中行业标准产生的依据是( D ) A历史先进水平B历史平均水平C行业先进水平D行业平均水平 7、J公司2008年的主营业务收入为500 000万元,其年初资产总额为650 000万元,年末资产总额为600 000万元,则该公司的总资产周转率为( D) A。77 B。83 C。4 D。8 8、下列选项中,不属于资产负债表中长期资产的是( A ) A应付债券B固定资产C无形资产D长期投资 9、计算总资产收益率指标时,其分子是( B )。 A. 利润总额 B. 净利润 C. 息税前利润 D. 营业利润 10.在财务报表分析中,投资人是指(D)。 A 社会公众B金融机构 C 优先股东D普通股东 11.流动资产和流动负债的比值被称为(A )。 A流动比率B速动比率C营运比率D资产负债比率12.下列各项中,(D)不是影响固定资产净值升降的直接因素。 A固定资产净残值B固定资产折旧方法 C折旧年限的变动D固定资产减值准备的计提 13、债权人在进行企业财务分析时,最为关注的是(B)。 A.获利能力 B.偿债能力 C.发展能力 D.资产运营能力 14、能够直接取得所需的先进设备和技术,从而能尽快地形成企业的生产经营能力的筹资形式是( B ) A.股票筹资B.吸收直接投资C.债券筹资D.融资租赁 15、下列项目中,属于非交易动机的有( D ) A支付工资B购买原材料C偿付到期债务D伺机购买质高价廉的原材料16、下列项目中属于非速动资产的有( D ) A.应收账款净额B.其他应收款C.短期投资 D.存货 17、下列( C)不属于固定资产投资决策要素。 A.可用资本的成本和规模 B. 项目盈利性 C. 决策者的主观意愿和能力 D. 企业承担风险的意愿和能力 18、确定一个投资方案可行的必要条件是( B )。

第二章财务报表分析 一、单选题 1.假定甲公司向乙公司赊销产品,并持有丙公司的债券和丁公司的股票,且向戊公司支付公司债利息。在不考虑其他条件的情况下,从甲公司的角度看,下列各项中属于本企业与债权人之间财务关系的是()。(南京大学2011金融硕士) A.甲公司与乙公司之间的关系 B.甲公司与丙公司之间的关系 C.甲公司与丁公两之间的关系 D.甲公司与戊公司之间的关系 【答案】D 【解析】甲公司与乙公司是商业信用关系;甲公司为丙公司的债权人;甲公司是丁公司的股东;戊公司是甲公司的债权人。 2.杜邦财务分析体系的核心指标是()。(浙江财经学院2011金融硕士) A.总资产报酬率 B.可持续增长率 C.ROE D.销售利润率 【答案】C 【解析】杜邦分析体系是对企业的综合经营理财及经济效益进行的系统分析评价,其恒

等式为:ROE=销售利润率×总资产周转率×权益乘数。可以看到净资产收益率(ROE)反映所有者投入资金的获利能力,反映企业筹资、投资、资产运营等活动的效率,是一个综合性最强的财务比率,所以净资产收益率是杜邦分析体系的核心指标。 3.影响企业短期偿债能力的最根本原因是()。(浙江财经学院2011金融硕士)A.企业的资产结构 B.企业的融资结构 C.企业的权益结构 D.企业的经营业绩 【答案】D 【解析】短期偿债能力比率是一组旨在提供企业流动性信息的财务比率,有时也被称为流动性指标。它们主要关心企业短期内在不引起不适当压力的情况下支付账单的能力,因此,这些指标关注企业的流动资产和流动负债,但短期偿债能力比率的大小会因行业类型而不同,影响企业短期偿债能力的最根本原因还是企业的经营业绩。 4.市盈率是投资者用来衡量上市公司盈利能力的重要指标,关于市盈率的说法不正确的是()。(浙江工商大学2011金融硕士) A.市盈率反映投资者对每股盈余所愿意支付的价格 B.市盈率越高表明人们对该股票的评价越高,所以进行股票投资时应该选择市盈率最高的股票 C.当每股盈余很小时,市盈率不说明任何问题 D.如果上市公司操纵利润,市盈率指标也就失去了意义

一、单项选择题(每小题2分) 1、下列哪个恒等式是不成立的? C A. 资产=负债+股东权益 B. 资产-负债=股东权益 C. 资产+负债=股东权益 D. 资产-股东权益=负债 2、从税收角度考虑,以下哪项是可抵扣所得税的费用? A A. 利息费用 B. 股利支付 C. A和B D. 以上都不对 3、现金流量表的信息来自于 C A. 损益表 B. 资产负债表 C. 资产负债表和损益表 D. 以上都不对 4、以下哪项会发生资本利得/损失,从而对公司纳税有影响? B A.买入资产 B.出售资产 C.资产的市场价值增加 D.资产的账面价值增加 5、沉没成本是增量成本。 B A. 正确 B. 不对 6、期限越短,债券的利率风险就越大。B A. 正确 B. 不对 7、零息债券按折价出售。 A A. 正确 B. 不对 8、股东的收益率是股利收益率和资本收益率的和。 A A. 正确 B. 不对 9、期望收益率是将来各种收益可能性的加权平均数,或叫期望值。 A A. 正确 B. 不对 10、收益率的方差是指最高可能收益率与最低可能收益率之差。 B A. 正确 B. 不对 11.财务经理的行为是围绕公司目标进行的,并且代表着股东的利益。因此,财务经理在投资、筹资及利润分配中应尽可能地围绕着以下目标进行。 C A.利润最大化B.效益最大化C.股票价格最大化D.以上都行 12.在企业经营中,道德问题是很重要的,这是因为不道德的行为会导致 D A.中断或结束未来的机会B.使公众失去信心 C.使企业利润下降D.以上全对 13.在净现金流量分析时,以下哪个因素不应该考虑 A A.沉没成本B.相关因素C.机会成本D.营运资本的回收 14. 每期末支付¥1,每期利率为r,其年金现值为:D A. B. C. D. 15. 据最新统计资料表明,我国居民手中的金融资产越来越多,这说明了居民手中持有的金融资产是 D A.现金B.股票C.债券D.以上都对 16.除了,以下各方法都考虑了货币的时间价值。C A. 净现值 B. 内含报酬率 C. 回收期 D. 现值指数 17. 企业A的平均收账期为28.41天,企业B的平均收账期为48.91天,则 C A.企业B是一家付款长的客户 B.应该将平均收账期同使用的信用条件中的信用天数相比较 C.很难判断 18.为了每年年底从银行提取¥1,000,一直持续下去,如果利率为10%,每年复利一次,那么,你现在应该存多少钱?A A.¥10,000 B. ¥8,243 C. ¥6,145 D. ¥11,000 19. 大多数投资者是:A A. 规避风险的 B.对风险持中性态度的 C. 敢于冒险的 D. 以上都不对 20. 财务拮据通常伴随着 D

关于集团客户专线故障的分析与处理 0 引言 网络是现代社会生产力的倍增器,是信息化社会中企业经营、管理、发展的支撑。为保障集团客户业务的安全运行及生产,对集团客户网络的维护必然要在可靠性、安全性、使用快捷等方面有很高的要求,公司对客户提供如:互联网、数字电路、DDN、ATM专线等多种通信服务,由于服务对象的重要性和特殊性,所以集团客户区别于一般客户的地方很多,客户在通信网络使用过程中,由于各种原因,会随时产生一些故障,集团客户业务要求时间,要求质量,而且跨地域,跨公司,难判断障碍点,在维护的过程中走了很多弯路。本文主要通过几个实际案例来分析如何解决一些细小问题的故障处理。 1 实例分析 1)实例:局域网内两个或两个以上相同网关路由器互相干扰,导致网络掉线的问题 舒兰市A单位申请光纤互联网,组网方式:光纤收发器-路由器-交换机-电脑,安装一周后,网络经常掉线,而且一部分电脑可以上网,一部分电脑上不了网,有的时候全部上不去网,经测试,查出A单位局域网内除了主路由器之外又有两个级联的路由器,发现这两个路由器的LAN地址与主路由器LAN 地址192.168.1.1相同,之后把其中一个路由器LAN地址改成了192.168.100.1,另一个LAN地址改成了192.168.200.1,并把这两个路由器DHCP功能关掉了,重新启动局域网内所有设备,网络恢复正常,观察两天之后,网络正常,故障恢复,从这个故障处理过程看,原因是客户用这两个路由器的LAN口当交换机功能用的,而且作为交换机 用的这两个路由器的LAN地址和主路由器LAN地址都是同一网段的IP:192.168.1.1,路由器本身有DHCP功能,这就造成了局域网内部分电脑开机上网自动选择的是通过主路由net转换上网,而部分电脑上网有的时候自动选择的是通过级联的路由器net转换上网,而级联的路由器wan口是没有配置的,没有激活的,这两个路由器有的时候并没有起到交换机的作用,而是起到了路由的作用,这就是造成网络掉线的罪魁祸首。 2)实例:局域网内同一vlan交换机,同一ip段利用不同两个运营商的上行接口办公造成的网络风暴 舒兰市B单位办公大楼采用光纤收发器上行连接上级单位办公网络。办公大楼外部几个营业网点采用的是ADSL链路VLAN网方式汇聚到B单位办公大楼方式。客户反映外部部分营业网点网速慢不能办公,首先发现ping外部网点网络延时1 000多ms,丢包率70%,经测试在局端关掉几个ADSL端口,发现延时30ms,恢复正常,之后到达关掉ADSL端口的网点,仍然可以办公,后发现该单位正连接着其他运营商的线路办公,打开ADSL端口后网络又出现延时增大丢包。把另一个运营商的线路拔掉之后,网络恢复正常,其他几个点同样是这个问题造成的。从故障处理结果看,这个是典型的同一ip段同一个vlan交换机接了两个上行链路造成的网络风暴。致使网络故障。 3)实例:局域网内同一vlan交换机,两个IP段共同利用同一交换机上行两个办公系统造成的网络风暴 舒兰市C单位办公网组网方式是用传输设备搭建的vlan网:客户主交换机-