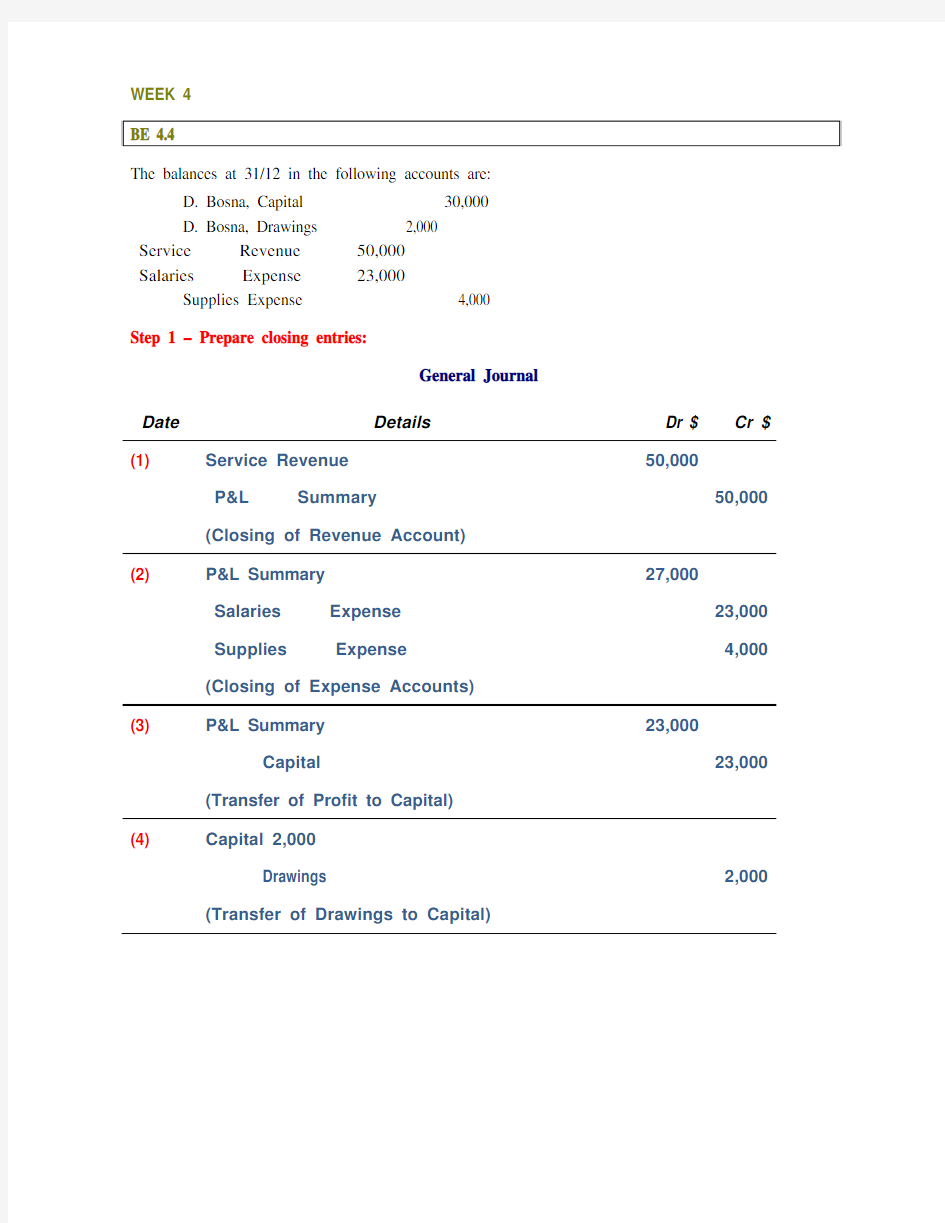

WEEK 4

BE 4.4

The balances at 31/12 in the following accounts are:

D. Bosna, Capital 30,000

D. Bosna, Drawings 2,000

Revenue 50,000

Service

Expense 23,000

Salaries

Supplies Expense 4,000

Step 1 – Prepare closing entries:

General Journal

Date Details Dr $ Cr $

(1) Service Revenue 50,000

Summary 50,000

P&L

(Closing of Revenue Account)

(2) P&L Summary 27,000

Expense 23,000

Salaries

Expense 4,000

Supplies

(Closing of Expense Accounts)

(3) P&L Summary 23,000

Capital 23,000

(Transfer of Profit to Capital)

(4) Capital 2,000

Drawings 2,000

(Transfer of Drawings to Capital)

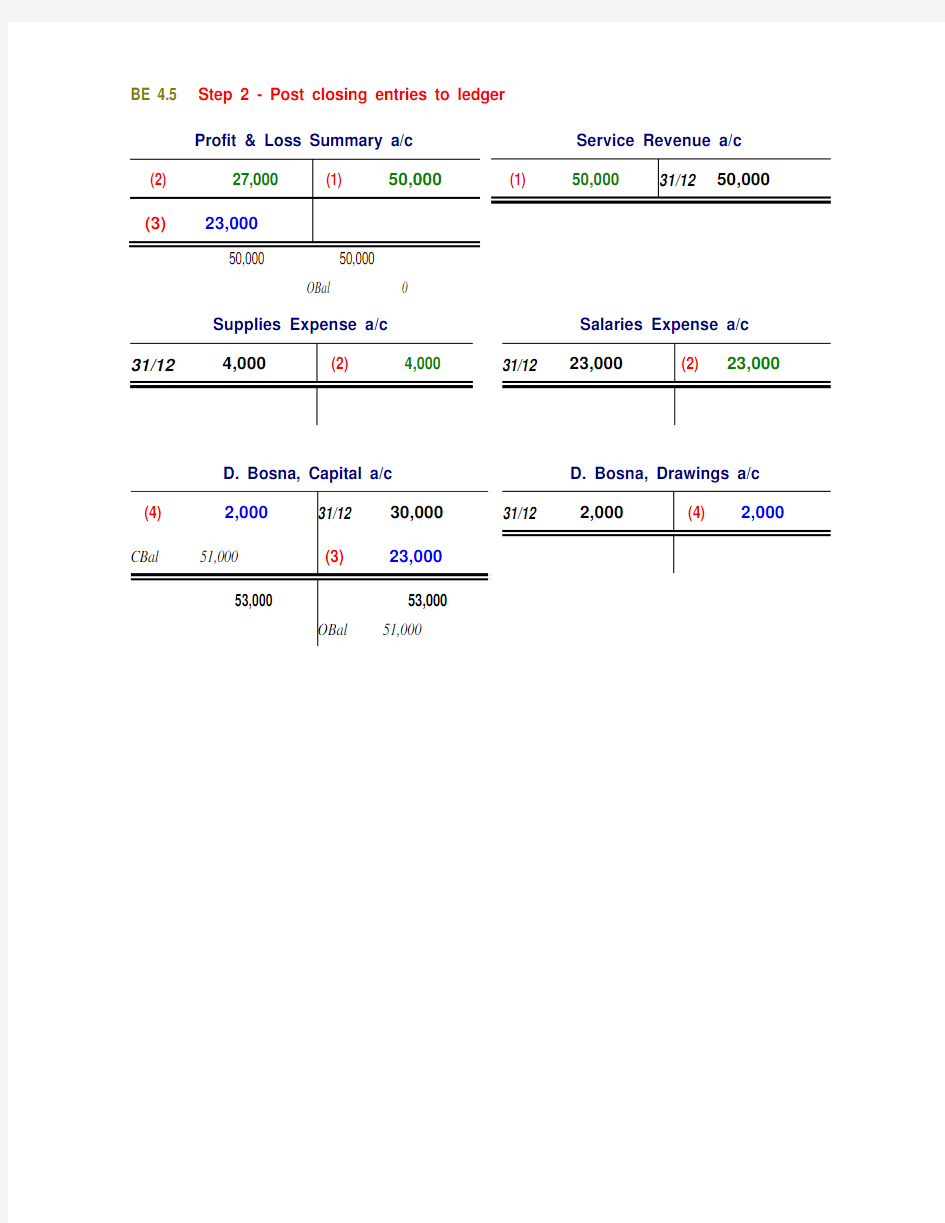

BE 4.5 Step 2 - Post closing entries to ledger

Profit & Loss Summary a/c Service Revenue a/c

(2) 27,000 (1) 50,000 (1) 50,00031/12 50,000

(3)23,000

50,000 50,000

OBal 0

Supplies Expense a/c Salaries Expense a/c

31/124,000 (2) 4,00031/12 23,000 (2) 23,000

D. Bosna, Capital a/c D. Bosna, Drawings a/c

(4)2,00031/12 30,00031/12 2,000 (4)2,000 CBal 51,000 (3)23,000

53,000 53,000

OBal 51,000

E4.12 (amended)

The balances in the following accounts are:

receivable 19,800

A/cs

87,800

rev

Commissions

Interest expense 6,300

Interest payable 0

(a) Prepare and post Adjusting Entries on 31/12:

Accrue $4,200 of commission earned but not received:

Dr Accounts Receivable 4,200

Cr Commission Revenue 4,200

Accrue $1,500 interest expense owing:

1,500

Expense

Interest

Dr

Cr Interest Payable 1,500

(b) Prepare and post Closing entries at 31st of December:

Close Revenue accounts:

Dr Commission Revenue 92,000

Cr P&L Summary 92,000

Close Expense accounts:

Dr P&L Summary 7,800

Cr Interest Expense 7,800

Transfer balance of P*L Summary to Capital

Dr P&L Summary 84,200

Cr Capital 84,200 (c) Prepare and post entries for January:

$4,200 Commission owed was received on Jan 10

10/1 Dr Cash 4,200

Cr Accounts Receivable 4,200

Paid $2,700 interest on Jan 15 ($1500 for last month)

15/1 Dr Interest payable 1,500

Dr Interest Expense 1,200

Cr Cash 2,700

Post entries at General Ledger for each of the following:

(1) Post adjusted entries at 31st Dec.

(2) Post closing entries at 31st Dec.

Balance the accounts on 31 Jan.

(3) Post entries for next month on Jan 10 and 15

Accounts Receivable Commission Revenue

31/12 19,800 (2) Clos. 92,000 31/12 87,800 (1) Adj. 4,200 (1) Adj. 4,200 Bal. 24,000(3) 10/1 4,200 Bal 0

Capital

CBal 84,200 (2)Clos 84,200

84,20084,200

OBal 84,200

Interest Payable Interest Expense

(1) Adj. 1,500 31/12 6,300 (2) Clos. 7,800

(1) Adj. 1,500

(3) 15/1 1,500

Bal 1,500Bal 0

(3) 15/1 1,200

Cash Profit and Loss Summary

(3) 10/ 1 4,200 (3) 15/1 2,700 (2) Exp 7,800 (2)Rev 92,000

(2) Capital 84,200

92,000 92000

O/Bal 0

Problem 4.5A

On 1 July 2007 Tsai Window Washing Pty Ltd opened for business. The company maintains the following Chart of Accounts:

A/c no. Account Name

101 Cash

112 Accounts

receivable.

supplies

128 Cleaning

insurance

130 Prepaid

157 Equipment

158 Accumulated depn – equipment

201 Accounts

payable

payable

212 Salaries

213 Tax

payable

capital

301 Share

earnings

302 Retained

306 Dividends

350 Profit and loss summary

revenue

400 Service

634 Cleaning supplies expense

expense

711 Depreciation

expense

722 Insurance

expense

726 Salaries

expense

727 Tax

(a)Journalise the following entries and

1/7Shareholders invested $12,000 into the business.

1/7Purchased used truck for $6,000. Paid $3,000 today with the balance on credit.

3/7Purchased $1,300 cleaning supplies on credit.

5/7Paid $1,200 for 1 year insurance policy.

12/7Invoiced customers $5,500 for cleaning services.

18/7Paid $1,000 on amount owing on truck and $800 on amount owing on supplies. 20/7Paid $1,400 for employee salaries.

21/7Collected $1,400 cash from customers invoiced on July 12.

31/7Paid $900 in dividends.

General Journal

Date Details Ref Dr $ Cr $

1/7 Cash 101 12,000

capital 301 12,000 Share

1/7 Equipment 157 6,000

Cash 101 3,000

Payable 201 3,000 Accounts

3/7 Cleaning

Supplies 128 1,300

Payable 201 1,300 Accounts

Insurance 130 1,200

5/7 Prepaid

Cash 101 1,200

Receivable 112 5,500

12/7 Accounts

Revenue 400 5,500 Service

Payable 201 1,800

18/7 Accounts

Cash 101 1,800

Expense 726 1 400

20/7 Salaries

Cash 101 1

400

21/7 Cash 101 1,400

Receivable 112 1,400 Accounts

31/7 Dividends 306 900

Cash 101 900

(b) Post these journal entries to the General ledger (done)

Please note: That an example of the cross referencing has been shown for the first two

journal entries on July 1st.

CASH No. 101

Debit Credit

Balance

Explanation Ref.

Date

Jul 1 Eg: Share Capital J1 12 00012 000

1 Eg: Equipment J1 3 000 9 000

5 J1 1 200 7 800

18 J1 1 800 6 000

20 J1 1 400 4 600

21 J1 1 400 6 000

31 J1 900 5 100

ACCOUNTS RECEIVABLE No. 112

Date

Balance

Explanation Ref.

Debit Credit

Jul 12 J1 5 500 5 500

21 J1 1 400 4 100

31 Adjusting J2

600

500 5

1

CLEANING SUPPLIES No. 128

Date

Debit Credit

Balance

Explanation Ref.

Jul 3 J1 1 300 1 300

600

31 Adjusting J2 700

PREPAID INSURANCE No. 130

Date

Balance

Debit Credit

Explanation Ref.

July 5 J1 1 200 1 200

100

31 Adjusting J2 100

1

157 EQUIPMENT No. Date

Balance

Debit Credit

Explanation Ref.

Jul 1 Eg: Cash/ A/c Payable J1 6 000 6 000

ACCUMULATED DEPRECIATION — EQUIPMENT No. 158

Date

Explanation Ref. Debit Credit Balance Jul 31 Adjusting J2 200 200

ACCOUNTS PAYABLE No. 201

Date

Explanation Ref. Debit Credit Balance Jul 1 Eg: Equipment J1 3 000 3 000 3 J1 1 300

4 300 18

J2

1 800

2 500

SALARIES PAYABLE No. 212

Date

Explanation Ref. Debit Credit Balance Jul 3 Adjusting J2 600 600

TAX PAYABLE

No. 213

Date

Explanation Ref. Debit Credit Balance Jul 31 Adjusting J2 1,200 1,200

SHARE CAPITAL No. 301 Date

Explanation Ref. Debit Credit Balance Jul 1

Eg: Cash

J1

12 000

12 000

RETAINED EARNINGS No. 302

Date

Explanation Ref. Debit Credit Balance Jul 31 Closing

J3

2,800

2,800

31

Closing J3 900

1,900

DIVIDENDS No. 306 Date Explanation Ref. Debit Credit Balance Jul 31

J1

900

900

31 Closing J3 900 0

PROFIT AND LOSS SUMMARY No. 350

Date Explanation Ref. Debit Credit Balance

Jul 31

Closing J3 7 000 7 000

4,2002,800 31 Closing J3

31 Closing J3

2,8000

SERVICE REVENUE No. 400

Balance

Debit Credit

Date

Explanation Ref.

Jul 12 J1 5 500 5 500

000

7

31 Adjusting J2 1

500

0000

7

31 Closing J3

CLEANING SUPPLIES EXPENSE No. 634

Date

Balance

Debit Credit

Explanation Ref.

700700

Jul 31 Adjusting J2

31 Closing J3 700 DEPRECIATION EXPENSE No. 711

Date

Balance

Explanation Ref.

Debit Credit

200 200

Jul 31 Adjusting J2

31 Closing J3 200 INSURANCE EXPENSE No. 722

Date

Balance

Debit Credit

Explanation Ref.

100100

Jul 31 Adjusting J2

31 Closing J3 100

TAX EXPENSE No. 724

Debit Credit

Balance

Explanation Ref.

Date

12001200

Jul 31 Adjusting J2

31 Closing J3 1200

SALARIES EXPENSE No. 726

Date

Balance

Explanation Ref.

Debit Credit

Jul 20 J1 1 400 1 400

000

600 2

31 Adjusting J2

31 Closing J3 2

000

(c) Prepare a Trial Balance as at 31 July on the worksheet

(d) Enter the following adjustments on the worksheet and complete the worksheet:

(1)$1,500 services provided but not invoiced or collected.

(2)Depreciation for the month on equipment is $200.

(3)One twelfth of the insurance has expired.

(4)$600 of cleaning supplies remain at the end of July.

(5)Unpaid employee salaries amount to $600.

(6)Tax at the rate of 30% is payable on profit (Hint: you will need to calculate profit for the

month).

(e)Prepare an income statement, a statement of changes in equity for the month ending

July 31, and a balance sheet as at July 31

(f)Journalise adjusting entries and post to the ledger (use J2 for the journal page)

(g)Journalise the closing entries, and post to the ledger

(use J3 for the journal page)

(h)Prepare a post-closing trial balance from the ledger a/c balances (and compare with your

worksheet)

Tsai Window Washing Pty Ltd

For the month of July, 2007

Trial Balance Adjustments Adjusted Trial Bal Income Statement B Account Name Dr Cr Dr Cr Dr Cr Dr Cr sh 5,100 5,100

counts Receivable 4,100 1,5005,600

eaning supplies 1,300 700600

epaid insurance 1,200 1001,100

uipment 6,000 6,000

c Dep – equip’t 200200

counts payable 2,500 2,500

laries payable 600600

x payable 1,2001,200

are capital 12,000 12,000

vidends 900 900

7,000

rvice revenue 5,500 1,500 7,000

eaning supplies exp 700700700

preciation expense 200200200

surance expense 100100100

laries expense 1,400 6002,0002,000

x expense 1,2001,2001,200

20,000 20,000 4,3004,30023,50023,500 4,2007,000

t Profit 2,800

tals 7,0007,000

Tsai Window Washing Pty Ltd

Income Statement

For the Month Ending 31 July 2007

$ $

Revenues

Service revenue 7,000

Expenses

Salaries expense 2,000 Depreciation expense 200 Insurance expense 100 Supplies expense 700

3,000Profit before tax 4,000Tax expense 1.200Net profit after tax

2,800

Tsai Window Washing Pty Ltd Statement of Changes in Equity For the Month Ending 31 July 2007

Retained Earnings $ Share

Capital $ Opening Bal., 1 July 0 0Plus : Share Issue 12,000

Net Profit for period

2,800 Less : Dividends 900 Ending bal, 31 July 1,900

12,000

Tsai Window Washing Pty Ltd

Balance Sheet

as at 31 July 2007

ASSETS

Current Assets

Cash 5,100

Receivable 5,600

Accounts

Cleaning

Supplies 600

Insurance 1,10012,400 Prepaid

Non-Current Assets

Equipment 6,000

Less: Accumul. Dep. – Equip. 2005,800 Total Assets 18,200 LIABILITIES AND SHAREHOLDERS EQUITY

Current Liabilities

Payable 2,500

Accounts

Tax

Payable 1,200

Payable 6004,300 Salaries

Shareholders Equity

Capital 12,000

Share

Earnings 1,90013,900 Retained

Total Liabilities and Sh. Equity 18,200

(f) General Journal (continued)

Date Details Ref Dr $ Cr $

(f) Adjusting Entries

31/7 Accounts

Receivable 112 1,500

Revenue 400 1,500 Service

31/7 Depr. Expense – Equip. 711 200

Accum. Dep. – Equip. 158 200 Expense 722 100

31/7 Insurance

Insurance 130 100 Prepaid

31/7 Cleaning Supplies Expense 634 700

Supplies 128 700 Cleaning

Expense 726 600

31/7 Salaries

Payable 212 600 Salaries

31/7 Tax

Expense 727 1,200

Payable 213 1,200 Tax

(g) General Journal (continued)

Date Details Ref Dr $ Cr $

(g) Closing Entries:

31/7 Service Revenue 400 7,000

P&L Summary 350 7,000 31/7 P&L Summary 350 4,200

Salaries

Expense

Depr. Exp – Equipment Insurance

Expense Cleaning Supplies Exp. Tax

expense 726

711

722

634

724

2,000

200

100

700

1200

31/7 P&L Summary 350 2,800

Retained Earnings 301 2,800

31/7 Retained Earnings 301 900

Dividends 306 900

(h) Post-closing trial balance

Account Name Dr $ Cr $

Cash 5,100 Accounts receivable 5,600

Cleaning supplies 600

Prepaid insurance 1,100

Equipment 6,000 Accumulated depreciation 200

Accounts payable 2,500

Tax payable 1,200

Salaries payable 600

Share capital 12,000

Retained earnings 1,900

18,400

18,400

Use of a Classified Balance Sheet:

Liquidity Analysis Working Capital

= Current Assets – Current Liabilities = 12,400 – 4,300

= $8,100

Current Ratio

= Current Assets / Current Liabilities = 12,400 / 4,300

= 2.88 times

Solvency Analysis

Debt to Equity Ratio

= Total Liabilities / Total Owners’ Equity = 4,300 / 13,900

= 0.3093 or 30.93%

Debt to Assets Ratio

= Total Liabilities / Total Assets

= 4,300 / 18,200

= 0.2362 or 23.62%