CHAPTER 14

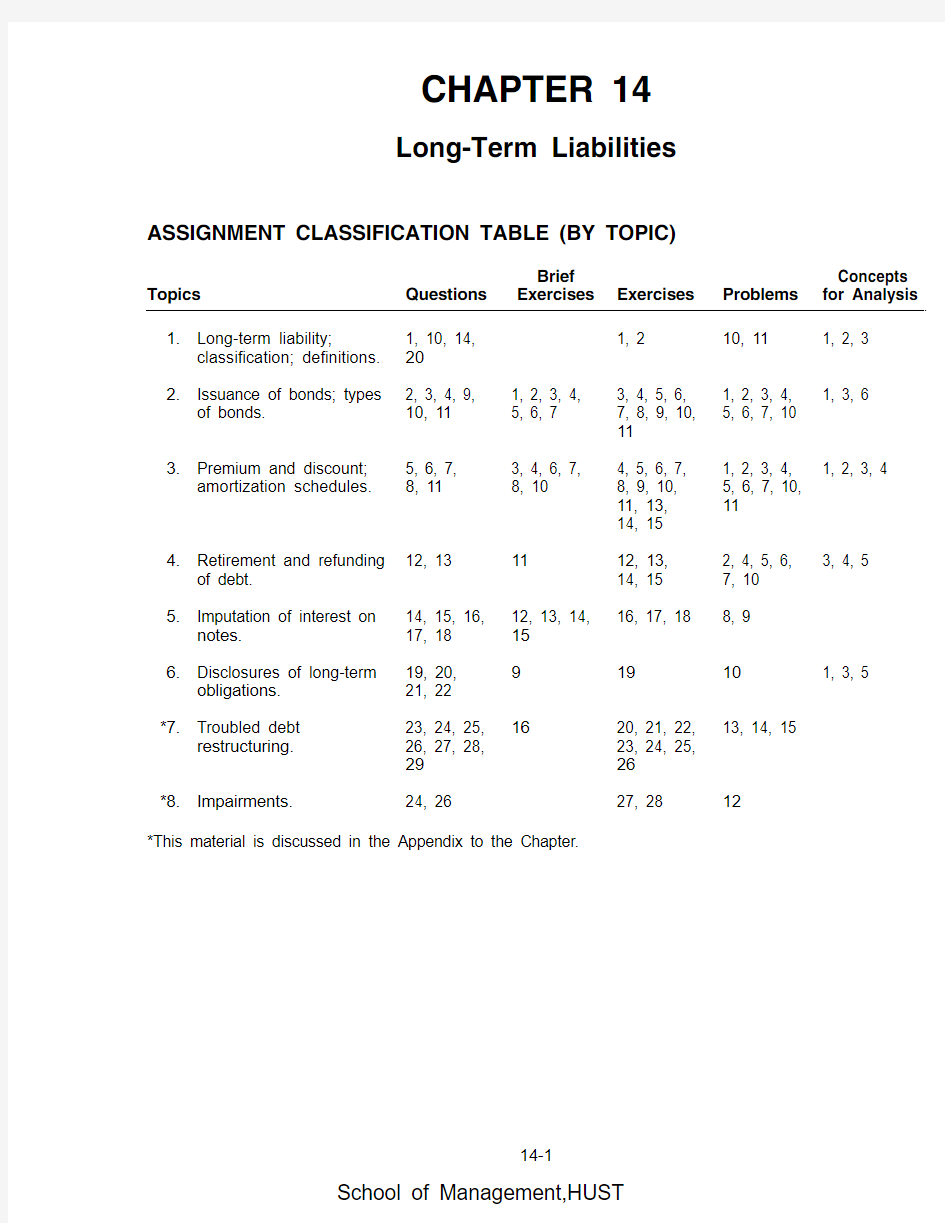

Long-Term Liabilities ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics Questions

Brief

Exercises Exercises Problems

Concepts

for Analysis

1.Long-term liability;

classification; definitions.1, 10, 14,

20

1, 210, 111, 2, 3

2.Issuance of bonds; types

of bonds.2, 3, 4, 9,

10, 11

1, 2, 3, 4,

5, 6, 7

3, 4, 5, 6,

7, 8, 9, 10,

11

1, 2, 3, 4,

5, 6, 7, 10

1, 3, 6

3.Premium and discount;

amortization schedules.5, 6, 7,

8, 11

3, 4, 6, 7,

8, 10

4, 5, 6, 7,

8, 9, 10,

11, 13,

14, 15

1, 2, 3, 4,

5, 6, 7, 10,

11

1, 2, 3, 4

4.Retirement and refunding

of debt.12, 131112, 13,

14, 15

2, 4, 5, 6,

7, 10

3, 4, 5

5.Imputation of interest on

notes.14, 15, 16,

17, 18

12, 13, 14,

15

16, 17, 188, 9

6.Disclosures of long-term

obligations.19, 20,

21, 22

919101, 3, 5

*7.Troubled debt

restructuring.23, 24, 25,

26, 27, 28,

29

1620, 21, 22,

23, 24, 25,

26

13, 14, 15

*8.Impairments.24, 2627, 2812 *This material is discussed in the Appendix to the Chapter.

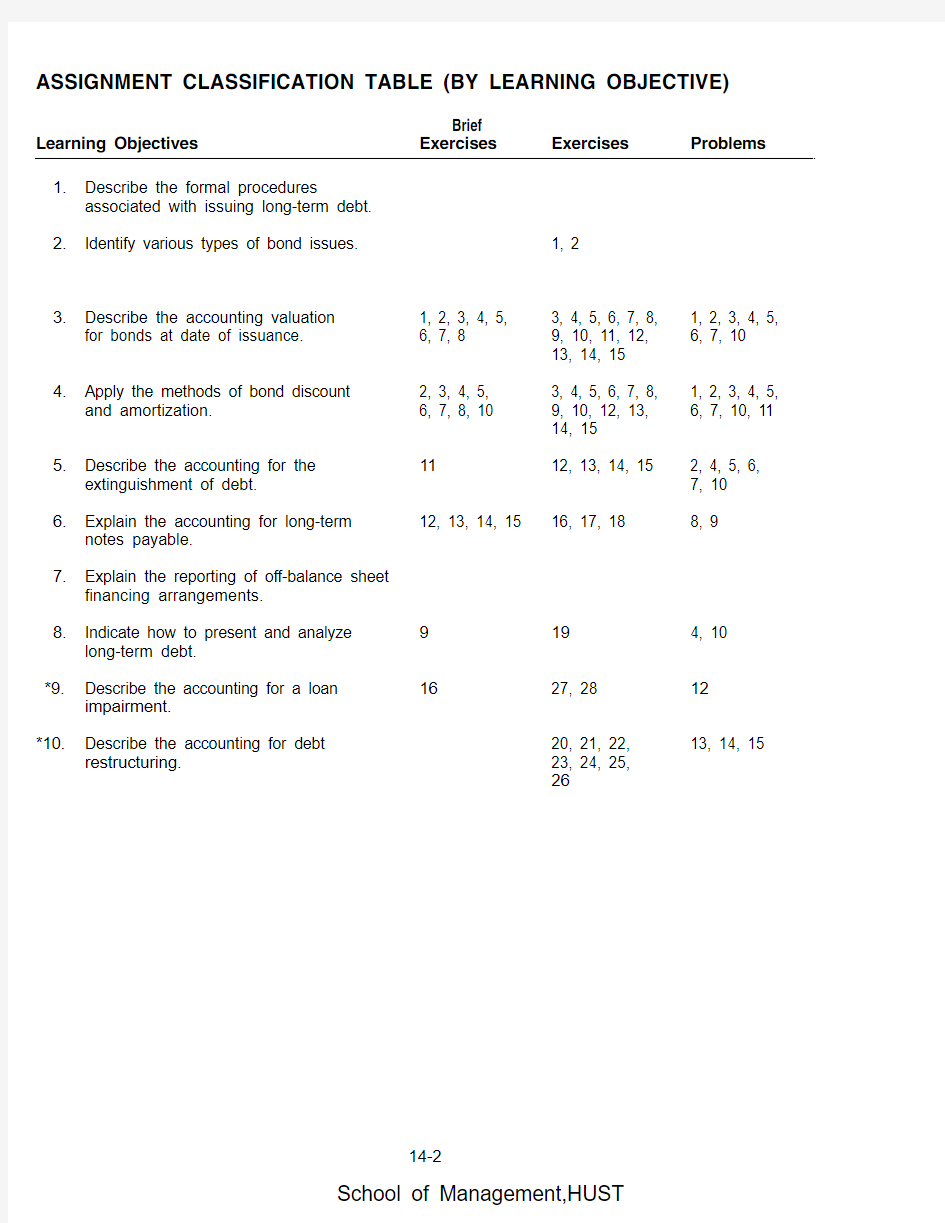

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives Brief

Exercises Exercises Problems

1.Describe the formal procedures

associated with issuing long-term debt.

2.Identify various types of bond issues.1, 2

3.Describe the accounting valuation

for bonds at date of issuance.1, 2, 3, 4, 5,

6, 7, 8

3, 4, 5, 6, 7, 8,

9, 10, 11, 12,

13, 14, 15

1, 2, 3, 4, 5,

6, 7, 10

4.Apply the methods of bond discount

and amortization.2, 3, 4, 5,

6, 7, 8, 10

3, 4, 5, 6, 7, 8,

9, 10, 12, 13,

14, 15

1, 2, 3, 4, 5,

6, 7, 10, 11

5.Describe the accounting for the

extinguishment of debt.1112, 13, 14, 152, 4, 5, 6,

7, 10

6.Explain the accounting for long-term

notes payable.

12, 13, 14, 1516, 17, 188, 9

7.Explain the reporting of off-balance sheet

financing arrangements.

8.Indicate how to present and analyze

long-term debt.

9194, 10

*9.Describe the accounting for a loan

impairment.

1627, 2812

*10.Describe the accounting for debt restructuring.20, 21, 22,

23, 24, 25,

26

13, 14, 15

ASSIGNMENT CHARACTERISTICS TABLE

Item Description Level of

Difficulty

Time

(minutes)

E14-1Classification of liabilities.Simple15–20 E14-2Classification.Simple15–20 E14-3Entries for bond transactions.Simple15–20 E14-4Entries for bond transactions—straight-line.Simple15–20 E14-5Entries for bond transactions—effective-interest.Simple15–20 E14-6Amortization schedule—straight-line.Simple15–20 E14-7Amortization schedule—effective-interest.Simple15–20 E14-8Determine proper amounts in account balances.Moderate15–20 E14-9Entries and questions for bond transactions.Moderate20–30 E14-10Entries for bond transactions.Moderate15–20 E14-11Information related to various bond issues.Simple20–30 E14-12Entry for retirement of bond; bond issue costs.Simple15–20 E14-13Entries for retirement and issuance of bonds.Simple15–20 E14-14Entries for retirement and issuance of bonds.Simple12–16 E14-15Entries for retirement and issuance of bonds.Simple10–15 E14-16Entries for zero-interest-bearing debt.Simple15–20 E14-17Imputation of interest.Simple15–20 E14-18Imputation of interest with right.Moderate15–20 E14-19Long-term debt disclosure.Simple10–15 *E14-20Settlement of debt.Moderate15–20 *E14-21Term modification without gain—debtor’s entries.Moderate20–30 *E14-22Term modification without gain—creditor’s entries.Moderate25–30 *E14-23Term modification with gain—debtor’s entries.Moderate25–30 *E14-24Term modification with gain—creditor’s entries.Moderate20–30 *E14-25Debtor/creditor entries for settlement of troubled debt.Simple15–20 *E14-26Debtor/creditor entries for modification of troubled debt.Moderate20–25 *E14-27Impairments.Moderate15–25 *E14-28Impairments.Moderate15–25

P14-1Analysis of amortization schedule and interest entries.Simple15–20 P14-2Issuance and retirement of bonds.Moderate25–30 P14-3Negative amortization.Moderate20–30 P14-4Issuance and retirement of bonds; income statement

presentation.

Simple15–20 P14-5Comprehensive bond problem.Moderate50–65 P14-6Issuance of bonds between interest dates, straight-line,

retirement.

Moderate20–25

P14-7Entries for life cycle of bonds.Moderate20–25 P14-8Entries for zero-interest-bearing note.Simple15–25 P14-9Entries for zero-interest-bearing note; payable

in installments.

Moderate20–25

P14-10Comprehensive problem; issuance, classification,

reporting.

Moderate20–25

P14-11Effective-interest method.Moderate40–50 *P14-12Loan impairment entries.Moderate30–40

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

Item Description Level of

Difficulty

Time

(minutes)

*P14-13Debtor/creditor entries for continuation of troubled debt.Moderate15–25 *P14-14Restructure of note under different circumstances.Moderate30–45 *P14-15Debtor/creditor entries for continuation of troubled debt

with new effective-interest.

Complex40–50

CA14-1Bond theory: balance sheet presentations, interest rate,

premium.

Moderate25–30

CA14-2Various long-term liability conceptual issues.Moderate10–15 CA14-3Bond theory: price, presentation, and retirement.Moderate15–25 CA14-4Bond theory: amortization and gain or loss recognition.Simple20–25 CA14-5Off-balance-sheet financing.Moderate20–30 CA14-6Bond issue, ethics Moderate23–30

ANSWERS TO QUESTIONS

1.(a)Funds might be obtained through long-term debt from the issuance of bonds, and from the

signing of long-term notes and mortgages.

(b)A bond indenture is a contractual agreement (signed by the issuer of bonds) between the bond

issuer and the bondholders. The bond indenture contains covenants or restrictions for the protection of the bondholders.

(c)A mortgage is a document which describes the security for a loan, indicates the conditions

under which the mortgage becomes effective (that is, conditions of default), and describes the rights of the mortgagee under default relative to the security. The mortgage accompanies

a formal promissory note and becomes effective only upon default of the note.

2.If the entire bond matures on a single date, the bonds are referred to as term bonds. Mortgage

bonds are secured by real estate. Collateral trust bonds are secured by the securities of other corporations. Debenture bonds are unsecured. The interest payments for income bonds depend on the existence of operating income in the issuing company. Callable bonds may be called and retired by the issuer prior to maturity. Registered bonds are issued in the name of the owner and require surrender of the certificate and issuance of a new certificate to complete the sale. A bearer or coupon bond is not recorded in the name of the owner and may be transferred from one investor to another by mere delivery. Convertible bonds can be converted into other securities of the issuing corporation for a specified time after issuance. Commodity-backed bonds (also called asset-linked bonds) are redeemable in measures of a commodity. Deep-discount bonds (also called zero-interest bonds) are sold at a discount which provides the buyer’s total interest payoff at maturity.

3.(a)Yield rate—the rate of interest actually earned by the bondholders; it is synonymous with the

effective and market rates.

(b)Nominal rate—the rate set by the party issuing the bonds and expressed as a percentage of

the par value; it is synonymous with the stated rate.

(c)Stated rate—synonymous with nominal rate.

(d)Market rate—synonymous with yield rate and effective rate.

(e)Effective rate—synonymous with market rate and yield rate.

4.(a)Maturity value—the face value of the bonds; the amount which is payable upon maturity.

(b)Face value—synonymous with par value and maturity value.

(c)Market value—the amount realizable upon sale.

(d)Par value—synonymous with maturity and face value.

5. A discount on bonds payable results when investors demand a rate of interest higher than the rate

stated on the bonds. The investors are not satisfied with the nominal interest rate because they can earn a greater rate on alternative investments of equal risk. They refuse to pay par for the bonds and cannot change the nominal rate. However, by lowering the amount paid for the bonds, investors can alter the effective rate of interest.

A premium on bonds payable results from the opposite conditions. That is, when investors are

satisfied with a rate of interest lower than the rate stated on the bonds, they are willing to pay more than the face value of the bonds in order to acquire them, thus reducing their effective rate of interest below the stated rate.

6.Discount (premium) on bonds payable should be reported in the balance sheet as a direct

deduction from (addition to) the face amount of the bond. Both are liability valuation accounts.

Questions Chapter 14 (Continued)

7.Bond discount and bond premium may be amortized on a straight-line basis or on an effective-

interest basis. The profession recommends the effective-interest method but permits the straight-line method when the results obtained are not materially different from the effective-interest method. The straight-line method results in an even or average allocation of the total interest over the life of the notes or bonds. The effective-interest method results in an increasing or decreasing amount of interest each period. This is because interest is based on the carrying amount of the bond issuance at the beginning of each period. The straight-line method results in a constant dollar amount of interest and an increasing or decreasing rate of interest over the life of the bonds.

The effective-interest method results in an increasing or decreasing dollar amount of interest and

a constant rate of interest over the life of the bonds.

8.The annual interest expense will decrease each period throughout the life of the bonds. Under the

effective-interest method the interest expense each period is equal to the effective or yield interest rate times the book value of the bonds at the beginning of each interest period. When bonds are sold at a premium, their book value declines to face value over their life; therefore, the interest expense declines also.

9.Bond issuance costs according to APB Opinion No. 21 should be debited to a deferred charge

account for Unamortized Bond Issue Costs and amortized over the life of the issue, separately from but in a manner similar to that used for discount on bonds. The FASB in SFAC No. 3 takes the position that debt issue costs can be treated as either an expense of the period in which the bonds are issued or a reduction of the related debt liability.

10.Treasury bonds should be shown on the balance sheet as a deduction from the bonds payable.

11.The call feature of a bond issue grants the issuer the privilege of purchasing, after a certain date at

a stated price, outstanding bonds for the purpose of reducing indebtedness or taking advantage of

lower interest rates. The call feature does not affect the amortization of bond discount or premium;

because early redemption is not a certainty, life to maturity date should be used for amortization purposes.

12.It is sometimes desirable to reduce bond indebtedness in order to take advantage of lower pre-

vailing interest rates. Also the company may not want to make a very large cash outlay all at once when the bonds mature.

Bond indebtedness may be reduced by either issuing bonds callable after a certain date and then calling some or all of them, or by purchasing bonds on the open market and then retiring them.

When a portion of bonds outstanding is going to be retired, it is necessary for the accountant to make sure any corresponding discount or premium is properly amortized.

13.Gains or losses from extinguishment of debt should be aggregated and reported in income.

For extinguishment of debt transactions disclosure is required of the following items:

1. A description of the transactions, including the sources of any funds used to extinguish debt if

it is practicable to identify the sources.

2.The income tax effect in the period of extinguishment.

3.The per share amount of the aggregate gain or loss net of related tax effect.

14.The entire arrangement must be evaluated and an appropriate interest rate imputed. This is done

by (1) determining the fair value of the property, goods, or services exchanged or (2) determining the market value of the note, whichever is more clearly determinable.

Questions Chapter 14 (Continued)

15.If a note is issued for cash, the present value is assumed to be the cash proceeds. If a note is

issued for noncash consideration, the present value of the note should be measured by the fair value of the property, goods, or services or by an amount that reasonably approximates the market value of the note (whichever is more clearly determinable).

16.When a debt instrument is exchanged in a bargained transaction entered into at arm’s-length, the

stated interest rate is presumed to be fair unless: (1) no interest rate is stated, or (2) the stated interest rate is unreasonable, or (3) the stated face amount of the debt instrument is materially different from the current sales price for the same or similar items or from the current market value of the debt instrument.

17.Imputed interest is the interest factor (a rate or amount) assumed or assigned which is different

from the stated interest factor. It is necessary to impute an interest rate when the stated interest rate is presumed to be unfair. The imputed interest rate is used to establish the present value of the debt instrument by discounting, at that imputed rate, all future payments on the debt instrument. In imputing interest, the objective is to approximate the rate which would have resulted if an independent borrower and an independent lender had negotiated a similar transaction under comparable terms and conditions with the option to pay the cash price upon purchase or to give

a note for the amount of the purchase which bears the prevailing rate of interest to maturity. In order

to accomplish that objective, consideration must be given to (1) the credit standing of the issuer,

(2) restrictive covenants, (3) collateral, (4) payment and other items pertaining to the debt, (5) the

existing prime interest rate, and (6) the prevailing rates for similar instruments of issuers with similar credit ratings.

18. A fixed-rate mortgage is a note that requires payment of interest by the mortgagor at a rate that

does not change during the life of the note. A variable-rate mortgage is a note that features an interest rate that fluctuates with the market rate; the variable rate generally is adjusted periodically as specified in the terms of the note and is usually limited in the amount of each change in the rate up or down and in the total change that can be made in the rate.

19.FASB Statement No. 47 requires disclosure at the balance sheet date of future payments for

sinking fund requirements and the maturity amounts of long-term debt during each of the next five years.

20.Off-balance-sheet-financing is an attempt to borrow monies in such a way that the obligations are

not recorded. Reasons for off-balance sheet financing are:

1.Many believe removing debt enhances the quality of the balance sheet and permits credit to be

obtained more readily and at less cost.

2.Loan covenants are less likely to be violated.

3.The asset side of the balance sheet is understated because fair value is not used for many

assets. As a result, not reporting certain debt transactions offsets the nonrecognition of fair values on certain assets.

21.Forms of off-balance-sheet financing include (1) investments in non-consolidated subsidiaries for

which the parent is liable for the subsidiary debt; (2) use of special purpose entities (SPEs), which are used to borrow money for special projects (resulting in take-or-pay contracts; (3) operating leases, which when structured carefully give the company the benefits of ownership without reporting the liability for the lease payments.

22.In take-or-pay contracts, the outside party agrees to make specified minimum payments even if it

does not take possession of the contracted goods or services. In through-put contracts, the outside party agrees to pay specified amounts in return for processing or transportation services rendered by the debtor, which is usually the owner of a manufacturing or transportation facility.

Questions Chapter 14 (Continued)

*23.Two different types of situations result with troubled debt: (1) Impairments, and (2) Restructurings.

Restructurings can be further classified into:

a.Settlements.

b.Modification of terms.

When a debtor company runs into financial difficulty, creditors may recognize an impairment on

a loan extended to that company. Subsequently, the creditor may modify the terms of the loan, or

settles it on terms unfavorable to the creditor. In unusual cases, the creditor forces the debtor into bankruptcy in order to ensure the highest possible collection on the loan.

*24.A loan is considered impaired when it is probable that the creditor will be unable to collect all amounts due (both principal and interest) according to the contractual terms of the loan. If a loan is considered impaired, the loss due to impairment should be measured as the difference between the investment in the loan and the expected future cash flows discounted at the loan’s historical effective-interest rate. The loss is recorded on the books of the creditor. The debtor would not be aware of the entry made by the creditor and would not make an entry until settlement or if

a modification of items resulted.

*25.A transfer of noncash assets (real estate, receivables, or other assets) or the issuance of the debtor’s stock can be used to settle a debt obligation in a troubled debt restructuring. In these situations, the noncash assets or equity interest given should be accounted for at their fair market value. The debtor is required to determine the excess of the carrying amount of the payable over the fair value of the assets or equity transferred (gain). Likewise, the creditor is required to determine the excess of the receivable over the fair value of those same assets or equity interests transferred (loss). The debtor recognizes a gain equal to the amount of the excess and the creditor normally would charge the excess (loss) against Allowance for Doubtful Accounts. In addition, the debtor recognizes a gain or loss on disposition of assets to the extent that the fair value of those assets differs from their carrying amount (book value).

*26.(a)The creditor will grant concessions in a troubled debt situation because it appears to be the more likely way to maximize recovery of the investment.

(b)The creditor might grant any one or a combination of the following concessions:

1.Reduce the face amount of the debt.

2.Accept noncash assets or equity interests in lieu of cash in settlement.

3.Reduce the stated interest rate.

4.Extend the maturity date of the face amount of the debt.

5.Reduce or defer any accrued interest.

(c)A loan is impaired when there is a reduction in the likelihood of collecting the interest and

principal payments as originally scheduled. An impairment should be recorded by a creditor when it is “probable” that the payment will not be collected as scheduled. Debtors do not record impairments.

*27.When a loan is restructured, the creditor should calculate the loss due to restructuring by sub-tracting the present value of the restructured cash flows from the carrying value of the loan.

Interest revenue is calculated at the original effective rate applied towards the new carrying value.

The debtor will record a gain only if the undiscounted restructured cash flows are less than the carrying value of the loan. If a gain is recognized, subsequent payments will be all principal. There is no interest component. If the undiscounted cash flows exceed the carrying amount, no gain is recognized, and a new imputed interest rate must be calculated in order to recognize interest expense in subsequent periods.

Questions Chapter 14 (Continued)

*28.“Accounting symmetry” between the entries recorded by the debtor and the creditor in a troubled debt restructuring means that there is a correspondence or agreement between the entries recorded by each party. Impairments are nonsymmetrical because, while the creditor records

a loss, the debtor makes no entry at all. Troubled debt restructurings are nonsymmetrical because

creditors calculate their loss using the discounted present value of future cash flows, while debtors calculate their gain using the undiscounted cash flows. The FASB chose to accept this nonsymmetric treatment rather than address debtor accounting because it feared that expansion of the scope of FASB Statement No. 114 would further delay its issuance.

*29.A transaction would be recorded as a troubled debt restructuring by only the debtor if the amount for which the liability is settled is less than its carrying amount on the debtor’s books, but equal to or greater than the carrying amount on the creditor’s books. In addition to the situation created by the use of discounted versus undiscounted cash flows by creditors and debtors, this situation can occur when a debtor or creditor has been substituted for one of the parties to the original transaction.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 14-1

Present value of the principal

$300,000 X .37689$113,067

Present value of the interest payments

$13,500 X 12.46221 168,240 Issue price$281,307

BRIEF EXERCISE 14-2

(a)Cash...................................................................................200,000

Bonds Payable.....................................................200,000 (b)Interest Expense............................................................10,000

Cash ($200,000 X 10% X 6/12).........................10,000 (c)Interest Expense............................................................10,000

Interest Payable...................................................10,000 BRIEF EXERCISE 14-3

(a)Cash ($200,000 X 98%).................................................196,000

Discount on Bonds Payable......................................4,000

Bonds Payable.....................................................200,000 (b)Interest Expense............................................................10,000

Cash ($200,000 X 10% X 6/12).........................10,000 (c)Interest Expense............................................................10,000

Interest Payable...................................................10,000 Interest Expense (800)

Discount on Bonds Payable (800)

($4,000 X 1/5 = $800)

BRIEF EXERCISE 14-4

(a)Cash ($200,000 X 103%)...............................................206,000

Bonds Payable.....................................................200,000

Premium on Bonds Payable............................6,000 (b)Interest Expense.............................................................10,000

Cash ($200,000 X 10% X 6/12).........................10,000 (c)Interest Expense.............................................................10,000

Interest Payable...................................................10,000 Premium on Bonds Payable.......................................1,200

Interest Expense ($6,000 X 1/5 = $1,200).....1,200 BRIEF EXERCISE 14-5

(a)Cash....................................................................................510,000

Bonds Payable.....................................................500,000

Interest Expense..................................................10,000

($500,000 X 6% X 4/12 = $10,000)

(b)Interest Expense.............................................................15,000

Cash ($500,000 X 6% X 6/12 = $15,000)........15,000 (c)Interest Expense.............................................................15,000

Interest Payable...................................................15,000 BRIEF EXERCISE 14-6

(a)Cash....................................................................................372,816

Discount on Bonds Payable.......................................27,184

Bonds Payable.....................................................400,000 (b)Interest Expense.............................................................14,913

Cash.........................................................................14,000

Discount on Bonds Payable (913)

($372,816 X 8% X 6/12 = $14,913)

($400,000 X 7% X 6/12 = $14,000)

BRIEF EXERCISE 14-6 (Continued)

(c)Interest Expense............................................................14,949

Interest Payable...................................................14,000

Discount on Bonds Payable (949)

($373,729 X 8% X 6/12 = $14,949)

BRIEF EXERCISE 14-7

(a)Cash...................................................................................429,757

Bonds Payable.....................................................400,000

Premium on Bonds Payable............................29,757

(b)Interest Expense............................................................12,893

Premium on Bonds Payable......................................1,107

Cash........................................................................14,000

($429,757 X 6% X 6/12 = $12,893)

($400,000 X 7% X 6/12 = $14,000)

(c)Interest Expense............................................................12,860

Premium on Bonds Payable......................................1,140

Interest Payable...................................................14,000

($428,650 X 6% X 6/12 = $12,860)

BRIEF EXERCISE 14-8

Interest Expense........................................................................4,298

Premium on Bonds Payable (369)

Interest Payable...............................................................4,667 ($429,757 X 6% X 2/12 = $4,298)

($400,000 X 7% X 2/12 = $4,667)

BRIEF EXERCISE 14-9

Current liabilities$80,000 Bond Interest Payable

Long-term liabilities$2,000,000 Bonds Payable, due January 1, 2016 98,000 Less: Discount on Bonds Payable$1,902,000 BRIEF EXERCISE 14-10

Bond Issue Expense..................................................................18,000 Unamortized Bond Issue Costs..................................18,000 ($180,000 X 1/10)

BRIEF EXERCISE 14-11

Bonds Payable............................................................................600,000

Premium on Bonds Payable...................................................15,000 Unamortized Bond Issue Costs..................................5,250 Cash.....................................................................................594,000 Gain on Redemption of Bonds....................................15,750 BRIEF EXERCISE 14-12

(a)Cash....................................................................................100,000

Notes Payable.......................................................100,000 (b)Interest Expense.............................................................11,000

Cash ($100,000 X 11% = $11,000)...................11,000 BRIEF EXERCISE 14-13

(a)Cash....................................................................................31,776

Discount on Notes Payable........................................18,224

Notes Payable.......................................................50,000

BRIEF EXERCISE 14-13 (Continued)

(b)Interest Expense............................................................3,813

Discount on Notes Payable.............................3,813

($31,776 X 12%)

BRIEF EXERCISE 14-14

(a)Computer..........................................................................39,369

Discount on Notes Payable........................................10,631

Notes Payable......................................................50,000 (b)Interest Expense............................................................4,724

Cash........................................................................2,500

Discount on Notes Payable.............................2,224

($39,369 X 12% = $4,724)

($50,000 X 5% = $2,500)

BRIEF EXERCISE 14-15 Cash...............................................................................................50,000

Discount on Notes Payable....................................................18,224 Notes Payable...................................................................50,000 Unearned Revenue.........................................................18,224 [$50,000 – ($50,000 X .63552) = $18,224]

*BRIEF EXERCISE 14-16

Toni Braxton (Debtor): No Entry

National American Bank (Creditor):

Bad Debt Expense..........................................................225,000

Allowance for Doubtful Accounts....................225,000

SOLUTIONS TO EXERCISES

EXERCISE 14-1 (15–20 minutes)

(a)Valuation account relating to the long-term liability, bonds payable

(sometimes referred to as an adjunct account). The $3,000 would continue to be reported as long-term.

(b)Current liability if current assets are used to satisfy the debt.

(c)Current liability, $200,000; long-term liability, $800,000.

(d)Current liability.

(e)Probably noncurrent, although if operating cycle is greater than one

year and current assets are used, this item would be classified as current.

(f)Current liability.

(g)Current liability unless (a) a fund for liquidation has been accumu-

lated which is not classified as a current asset or (b) arrangements have been made for refinancing.

(h)Current liability.

(i)Current liability.

EXERCISE 14-2 (15–20 minutes)

(a)Discount on Bonds Payable—Contra account to bonds payable on

balance sheet.

(b)Interest expense (credit balance)—Reclassify to interest payable on

balance sheet.

(c)Unamortized Bond Issue Costs—Classified as “Other Assets” on

balance sheet.

(d)Gain on repurchase of debt—Classify as part of other gains and

losses on the income statement.

(e)Mortgage payable—Classify one-third as current liability and the

remainder as long-term liability on balance sheet.

EXERCISE 14-2 (Continued)

(f)Debenture bonds—Classify as long-term liability on balance sheet.

(g)Notes payable—Classify as long-term liability on balance sheet.

(h)Premium on bonds payable—Classify as adjunct account to Bonds

Payable on balance sheet.

(i)Treasury bonds—Classify as contra account to bonds payable on

balance sheet.

(j)Income bonds payable—Classify as long-term liability on balance sheet.

EXERCISE 14-3 (15–20 minutes)

1.Simon Company:

(a)1/1/07Cash.............................................................200,000

Bonds Payable...............................200,000

(b)7/1/07Bond Interest Expense...........................4,500

($200,000 X 9% X 3/12)

Cash...................................................4,500

(c)12/31/07Bond Interest Expense...........................4,500

Interest Payable.............................4,500

2.GarFunkle Company:

(a)6/1/07Cash.............................................................105,000

Bonds Payable...............................100,000

Bond Interest Expense................5,000

($100,000 X 12% X 5/12)

(b)7/1/07Bond Interest Expense...........................6,000

Cash...................................................6,000

($100,000 X 12% X 6/12)

EXERCISE 14-3 (Continued)

(c)12/31/07Bond Interest Expense...........................6,000

Interest Payable..............................6,000

Note to instructor: Some students may credit Interest Payable on 6/1/07. If they do so, the entry on 7/1/07 will have a debit to Interest Payable for $5,000 and a debit to Bond Interest Expense for $1,000.

EXERCISE 14-4 (15–20 minutes)

(a)1/1/08Cash ($600,000 X 102%).................................612,000

Bonds Payable........................................600,000

Premium on Bonds

Payable..................................................12,000 (b)7/1/08Bond Interest Expense...................................29,700

Premium on Bonds Payable (300)

($12,000 ÷ 40)

Cash...........................................................30,000

($600,000 X 10% X 6/12)

(c)12/31/08Bond Interest Expense...................................29,700

Premium on Bonds Payable (300)

Interest Payable......................................30,000

EXERCISE 14-5 (15–20 minutes)

(a)1/1/08Cash ($600,000 X 102%).................................612,000

Bonds Payable........................................600,000

Premium on Bonds Payable...............12,000 (b)7/1/08Bond Interest Expense....................................29,898

($612,000 X 9.7705% X 1/2)

Premium on Bonds Payable (102)

Cash............................................................30,000

($600,000 X 10% X 6/12)

EXERCISE 14-5 (Continued)

(c)12/31/08Bond Interest Expense.................................29,893

($611,898 X 9.7705% X 1/2)

Premium on Bonds Payable (107)

Interest Payable...................................30,000 Carrying amount of bonds at July 1, 2008:

Carrying amount of bonds at January 1, 2008$612,000

Amortization of bond premium

($300,000 – $29,898) (102)

Carrying amount of bonds at July 1, 2008$611,898 EXERCISE 14-6 (15–20 minutes)

Schedule of Discount Amortization

Straight-Line Method

Year Cash

Paid

Interest

Expense

Discount

Amortized

Carrying

Amount of

Bonds

Jan. 1, 2007$1,855,816.00 Dec. 31, 2007$200,000$228,836.80 $28,836.80* 1,884,652.80 Dec. 31, 2008200,000228,836.8028,836.80 1,913,489.60 Dec. 31, 2009200,000228,836.8028,836.80 1,942,326.40 Dec. 31, 2010200,000228,836.8028,836.80 1,971,163.20 Dec. 31, 2011200,000228,836.8028,836.80 2,000,000.00 *$28,836.80 = ($2,000,000 – $1,855,816) ÷ 5.

EXERCISE 14-7 (15–20 minutes)

The effective-interest or yield rate is 12%. It is determined through trial and error using Table 6-2 for the discounted value of the principal ($1,134,860) and Table 6-4 for the discounted value of the interest ($720,956); $1,134,860 plus $720,956 equals the proceeds of $1,855,816. (A financial calculator may be used to determine the rate of 12%.)

EXERCISE 14-7 (Continued)

Schedule of Discount Amortization

Effective-Interest Method (12%)

Year Cash

Paid

Interest

Expense

Discount

Amortized

Carrying

Amount of

Bonds

(1)(2)(3)(4)

Jan. 1, 2007$1,855,816.00 Dec. 31, 2007$200,000$222,697.92*$22,697.92 1,878,513.92 Dec. 31, 2008200,000225,421.6725,421.67 1,903,935.59 Dec. 31, 2009200,000228,472.2728,472.27 1,932,407.86 Dec. 31, 2010200,000231,888.9431,888.94 1,964,296.80 Dec. 31, 2011200,000235,703.20**35,703.20 2,000,000.00 *$222,697.92 = $1,855,816 X .12.

**Rounded.

EXERCISE 14-8 (15–20 minutes)

(a)Printing and engraving costs of bonds$12,000

Legal fees49,000 Commissions paid to underwriter 60,000 Amount to be reported as Unamortized Bond Issue

Costs$121,000 The Unamortized Bond Issue Costs, $121,000, should be reported as a deferred charge in the Other Assets section on the balance sheet. (b)Interest paid for the period from January 1

(July 1) to June 30 (December 31), 2007;

$2,000,000 X 10% X 6/12$100,000 Less: Premium amortization for the period from

January 1 (July 1) to June 30 (December 31), 2007

[($2,000,000 X 1.04) – $2,000,000] ÷ 10 X 6/12 4,000 Interest expense to be recorded on July 1

(December 31), 2007$ 96,000

EXERCISE 14-8 (Continued)

(c)Carrying amount of bonds on June 30, 2007$562,500

Effective-interest rate for the period from June 30

to October 31, 2007 (.10 X 4/12)X.033333 Interest expense to be recorded on October 31, 2007$ 18,750 EXERCISE 14-9 (20–30 minutes)

(a) 1.June 30, 2008

Cash............................................................4,300,920.00

Bonds Payable..............................4,000,000.00

Premium on Bonds Payable.....300,920.00

2.December 31, 2008

Bond Interest Expense..........................258,055.20

($4,300,920.00 X 12% X 6/12)

Premium on Bonds Payable................1,944.80

Cash..................................................260,000.00

($4,000,000 X 13% X 6/12)

3.June 30, 2009

Bond Interest Expense..........................257,938.51

[($4,300,920.00 – $1,944.80)

X 12% X 6/12]

Premium on Bonds Payable................2,061.49

Cash..................................................260,000.00

4.December 31, 2009

Bond Interest Expense..........................257,814.82

[($4,300,920.00 – $1,944.80 –

$2,061.49) X 12% X 6/12]

Premium on Bonds Payable................2,185.18

Cash..................................................260,000.00

此文档下载后即可编辑 (1)出售产品5件,价款600元,增值税102元,收到现金702元。借:库存现金702 贷:主营业务收入600 应交税费-----应交增值税(销项税额)102 (2)厂办主任王平因公外出,预借差旅费1500元,以现金支付。 借:其他应收款------备用金(王平)1500 贷:库存现金1500 (3)职工李红交回欠款500元。 借:库存现金500 贷:其他应收款-------其他应收暂付款(李红)500 4 大明公司现金清查,发现短缺360元,经查实,其中160元属于出纳员小王的责任,应由其赔偿,赔款尚未收到,另外200元无法查明原因,经批准作为管理费用处理。 借:待处理财产损溢-----待处理流动资产损溢360 贷:库存现金360 借:其他应收款------其他应收暂付款(小王)160 管理费用200 贷:待处理财产损溢-----待处理流动资产损溢360 5大明公司现金清查,发现库存现金溢余270元,经查实200元为多收A公司货款,其中70元无法查明原因,经批准作为营业外收入。 借:库存现金270

贷:待处理财产损溢-----待处理流动资产损溢270 借:待处理财产损溢-----待处理流动资产损溢270 贷:其他应付款-----其他应付暂收款(A公司) 200 营业外收入70 6大明公司收回A公司以转账支票偿还前欠货款1.8万元 借:银行存款18000 贷:应收账款-----A公司18000 7大明公司前欠天一公司货款15万元,现以信汇方式付款 借:应付账款-----天一公司150000 贷:银行存款150000 8甲企业为增值税一般纳税人,向银行申请办理银行汇票用以购买原材料,将款项250 000元交存银行转作银行汇票存款。根据银行盖章退回的申请书存根联: 借:其他货币资金——银行汇票存款250 000 贷:银行存款250 000 9甲企业购入原材料一批,取得的增值税专用发票上的原材料价款为200 000元,增值税税额为34 000元,已用银行汇票办理结算。 借:原材料200 000 应交税费——应交增值税(进项税额)34 000 贷:其他货币资金——银行汇票存款234 000 10甲企业于3月5日向银行申领信用卡,向银行交存50 000元。 借:其他货币资金——信用卡存款50 000

《新编财务会计》技能训练参考答案 项目一货币资金的核算 一、单选题 1.D 2. B 3. C 4 .B 5. B 6. A 7 .C 8. D 9. D 10.C 二、多选题 1、BCD 2、 ABCD 3 、ACD 4、 ABCD 三、业务处理题 1 借:其他应收款—王明 1000 贷:库存现金 1000 2 借:应收账款 23900 贷:主营业务收入20000 应交税费应交增值税(销项税额)3400 库存现金 500 3 借:管理费用 800 库存现金 200 贷:其他应收款—王明 1000 4 借:管理费用 600 贷:库存现金 600 5 借:管理费用1200 贷:其他货币资金1200 6 借:其他货币资金-存出投资款150000 贷:银行存款150000 7 借:其他货币资金10000 贷:银行存款 10000 8 借:应付账款 3500 贷:银行存款 3500 项目二存货的核算 一、单选题 1、 D 2、C 3、 C 4、D 5、A 6、C 7、A 8、C 9、D 10、C 11、C 12、B 13、D

二、多选题 1、AB 2、BC 3、A C 4、 B D 5、ABC 6、ABD 7、A CD 8、ACD 9、ACD 三、判断题 1、× 2、√ 3、× 4、× 5、× 6、× 7、× 8、× 9、√ 10、√ 四、计算分析题 1、 (1)编制与A材料初始计量有关的会计分录。 12月1日 借:原材料 82000 应交税费-应交增值税(进项税额)13600 贷:银行存款 95600 12月8日 借:原材料 32800 应交税费-应交增值阅(进项税额)5576 贷:应付账款 38376 12月15日 借:原材料 49200 贷:股本 40000 资本公积-股本溢价 9200 (2)编制发出A材料的会计分录。 借:生产成本 81600 管理费用 40800 贷:原材料 122400 (3)编制年末计提A材料跌价准备的会计分录。 借:资产减值损失 11600 贷:存货跌价准备 11600 2、 (1)A产品:有销售合同部分: A产品可变现净值﹦40×(11-0.5)﹦420 成本﹦40×10﹦400(万元) 这部分存货不需计提跌价准备 超过合同部分: A产品可变现净值﹦60×(10.2-0.5)﹦582(万元) 成本﹦60×10﹦600﹝万元﹞ 这部分存货需计提跌价准备18万元

试卷代号:2608期末考试中级财务会计二试题 一、单项选择题(从下列每小题的四个选项中,选择一个正确的,将其顺序号填在答题纸上-每小题2分,共20分) 1.对辞退福利的正确列支方法是( ) A.计人管理费用 B.计入营业外支出C.计入制造费用 D.计入销售费用 2.下列资产负债表项目中,可根据相应账户期末余额直接填列的是( ) A.应付债券 B.持有至到期投资C.应付账款 D.交易性金融资产 3.下列有关利润表的表述中,不正确的是( ) A.属于中报与年报B.属于动态报表C.反映经营成果D.采用“本期营业观”编制 4.Z公司涉及一桩诉讼,根据以往经验及公司所聘请律师本期的意见判断,公司在该桩诉讼中胜诉的可能性为30%,败诉的可能性有70%。如果败诉,公司将要支付40万元~60万元的赔偿款。据此,Z公司应在本期末资产负债表中确认预计负债金额( ) A.40万元 B.50万元C.60万元 D.100万元 5.因采购商品开具面值40万元,票面利率4%,期限3个月的商业汇票一张。该应付票据到期时,公司一共应偿付( ) A.440 000元 B.412 000元C.404 000元 D.400 000元 6. 12月31日“长期借款”账户余额600万元,其中明年4月末到期应偿还的金额为200 万元。则本年末资产负债表中“长期借款”项目填列的金额应为( ) A.200万元 B.400万元C.500万元 D.600万元 7.会计实务中,某项会计变化如果不易分清会计政策变更与会计估计变更时,正确的做法是( ) A.按会计估计变更处理 B.按会计政策变更处理 C.不作处理,待分清后再处理 D.在会计政策变更、会计估计变更的处理方法中任选一种 8.年末预提商品保修费15万元,但税法规定该项支出在实际发生时准予扣除。该项负债产生的暂时性差异类型为( ) A.O B.可抵扣暂时性差异15万元 C.不确定 D.应纳税暂时性差异15万元 9.企业现有注册资本2 000万元,法定盈余公积余额400万元。前年发生的亏损中尚有450万元未予弥补,据此,本年可用于弥补亏损的法定盈余公积数额为( ) A. 80万元 B.100万元 C.400万元 D.1 000万元 10.将面值1 000万元的股票按1 100万元的价格发行,支付发行费用35万元。该项股票发行,计人“资本公积一股本溢价”账户的金额应为( ) A.35万元 B.65万元 C.100万元 D.135万元 二、多项选择题(下列每小题的五个选项中有二至五个是正确的,请选出正确的,将其顺序号填在答题纸上,不选、多选或错选均不得分,少选可酌情给分。每小题3分,共15分)11.下列各项属于会计政策内容的有( ) A.坏账损失的核算方法 B.借款费用的核算方法C.所得税费用的核算 D.无形资产的使用寿命E.发出存货的计价方法 12.企业交纳的下列各项税金,应通过“营业税金及附加”账户核算的有( ) A.消费税 B.增值税 C.车船税 D.印花税E.营业税 13.下列各项中,应作为营业外支出核算的有( ) A.对外捐赠资产 B.存货非常损失 C.债务重组损失 D.税款滞纳金支出E.出售固定资产净损失

财务会计分录题及答案集团档案编码:[YTTR-YTPT28-YTNTL98-UYTYNN08]

(1)出售产品5件,价款600元,增值税102元,收到现金702元. 借:库存现金 702 贷:主营业务收入 600 应交税费-----应交增值税(销项税额)102 (2)厂办主任王平因公外出,预借差旅费1500元,以现金支付. 借:其它应收款------备用金(王平) 1500 贷:库存现金 1500 (3)职工李红交回欠款500元. 借:库存现金 500 贷:其它应收款-------其它应收暂付款(李红) 500 4 大明公司现金清查,发现短缺360元,经查实,其中160元属于出纳员小王责任,应由其赔偿,赔款尚未收到,另外200元无法查明原因,经批准作为管理费用处理. 借:待处理财产损溢-----待处理流动资产损溢 360 贷:库存现金 360 借:其它应收款------其它应收暂付款(小王) 160 管理费用 200 贷:待处理财产损溢-----待处理流动资产损溢 360 5大明公司现金清查,发现库存现金溢余270元,经查实200元为多收A公司货款,其中70元 无法查明原因,经批准作为营业外收入. 借:库存现金 270 贷:待处理财产损溢-----待处理流动资产损溢 270 借:待处理财产损溢-----待处理流动资产损溢 270 贷:其它应付款-----其它应付暂收款 (A公司) 200 营业外收入 70 6大明公司收回A公司以转账支票偿还前欠货款1.8万元 借:银行存款 18000 贷:应收账款 -----A公司 18000 7大明公司前欠天一公司货款15万元,现以信汇方式付款 借:应付账款-----天一公司 150000

第一章总论 【思考题】 1.说明财务会计与管理会计的区别与联系。 答:财务会计与管理会计的区别可概括为; (1)财务会计以计量和传送信息为主要目标 财务会计不同于管理会计的特点之一,是财务会计的目标主要是向企业的投资者、债权 人、政府部门,以及社会公众提供会计信息。从信息的性质看,主要是反映企业整体情况, 并着重历史信息。从信息的使用者看,主要是外部使用者,包括投资人、债权人、社会公众 和政府部门等。从信息的用途看,主要是利用信息了解企业的财务状况和经营成果。而管理 会计的目标则侧重于规划未来,对企业的重大经营活动进行预测和决策,以及加强事中控制。 (2)财务会计以会计报告为工作核心 财务会计作为一个会计信息系统,是以会计报表作为最终成果。会计信息最终是通过会 计报表反映出来。因此,财务报告是会计工作的核心。现代财务会计所编制的会计报表是以 公认会计原则为指导而编制的通用会计报表,并把会计报表的编制放在最突出的地位。而管 理会计并不把编制会计报表当做它的主要目标,只是为企业的经营决策提供有选择的或特定的管理信息,其业绩报告也不对外公开发表。 (3)财务会计仍然以传统会计模式作为数据处理和信息加工的基本方法 为了提供通用的会计报表,财务会计还要运用较为成熟的传统会计模式作为处理和加工信息的方法。传统会计模式也是历史成本模式,它依据复式簿记系统,以权责发生制为基础,采用历史成本原则。 (4)财务会计以公认会计原则和行业会计制度为指导 公认会计原则是指导财务会计工作的基本原理和准则,是组织会计活动、处理会计业务的规范。公认会计原则由基本会计准则和具体会计准则所组成。这都是我国财务会计必须遵循的规范。而管理会计则不必严格遵守公认的会计原则。 2.试举五个会计信息使用者,并说明他们怎样使用会计信息。 答: 股东。他们需要评价过去和预测未来。有关年度财务报告是满足这些需要的最重要的手段,季度财务报告、半年度报告也是管理部门向股东报告的重要形式。向股东提供这些报告是会计信息系统的传统职责,股东借助于财务报告反映的常规信息,获得有关股票交易和股利支付的情况,从而做出投资决策。 银行。他们对公司的信誉、偿债能力,以及企业的未来发展是非常关心的。公司的财务报告是这些信息的一个重要来源。银行人需要的有关借贷业务的常规信息,是通过与借款单位的会计信息交换得来的。 税务机关。他们需要有关公司利润和向国家交纳税额的信息;社会保障机关需要有关企业交纳各项社会保障基金的信息。 总经理。他要利用企业的会计信息对企业的生产经营进行管理。通过对企业财务状况、收入与成本费用的分析,可以发现企业在生产经营上存在的问题,以便采取措施,改进经营。 职工。作为一个利益集团,职工个人期望定期收到工资和薪金,并同时得到有关企业为个人提供社会保障的各类基金方面的信息和企业的某些综合性的信息,诸如工资平均水平、福利金和利润等,职工代表大会、工会也会代表职工要求得到这些信息,这些信息的大部分是由会计信息系统提供的。 3.何谓可靠性?可靠性是否意味着真实? 答:可靠性是指会计信息必须是客观的和可验证的。一项信息是否可靠取决于以下三个因素,即真实性、可核性和中立性。所谓真实性就是要如实表达,即会计核算应以实际发生的经济业务为依据,内容真实、数字准确、资料可靠,会计的记录和报告不加任何掩饰。 所谓可核性是指信息可经得住复核和验证,即由独立的专业和文化素养基本相同的人员,分别采用同一计量方法,对同一事项加以计量,能得出相同的结果。所谓中立性是指会计信息应不偏不依,不带主观成份。将真相如实地和盘托出,结论让用户自己去判断。会计人员不能为了某种特定利益者的意愿或偏好而对会计信

{财务管理财务会计}财务会计习题及答案

第二章货币资金和交易性金融资产 业务题: 1.甲企业系上市公司,按季对外提供中期财务报表,按季计提利息。2008年有关业务如下: (1)1月5日甲企业以赚取差价为目的从二级市场购入一批债券作为交易性金融资产,面值总额为2000万元,票面利率为6%,3年期,每半年付息一次,该债券发行日为2007年1月1日。取得时支付的价款为2060万元,含已到付息期但尚未领取的2007年下半年的利息60万元,另支付交易费用40万元,全部价款以银行存款支付。 (2)1月15日,收到2007年下半年的利息60万元。 (3)3月31日,该债券公允价值为2200万元。 (4)3月31日,按债券票面利率计算利息。 (5)6月30日,该债券公允价值为1960万元。 (6)6月30日,按债券票面利率计算利息。 (7)7月15日,收到2008年上半年的利息60万元。 (8)8月15日,将该债券全部处置,实际收到价款2400万元。 要求:根据以上业务编制有关交易性金融资产的会计分录。 2.宏达公司2008年4月5日购入M上市公司的股票200万股作为可供出售金融资产,每股20元(含已宣告但尚未发放的现金股利2元),另支付相关费用20万元。5月15日收到现金股利400万元。6月30日每股公允价值为18.4元,9月30日每股公允价值为18.8元,12月31日每股公允价值为18.6元。2009年1月5日,宏达公司将上述M上市公司的股票对外出售100万股,每股售价为18.8元。宏达公司对外提供季度财务报告。 要求:根据上述资料编制宏达公司有关会计分录。(金额单位:万元)

财务会计习题答案

财务会计练习题 一、货币资金核算: 1.新蒙公司在200x年第1季度发生下列业务: (1)1月1日核定销售部门备用金定额3000元,用现金支票支付。3月30日销售部门前来报销零星开支,共计2345元。 1月1日 借:备用金3000 贷:银行存款3000 3月30日 借:管理费用2345 贷:现金2345 (2)l月8日委托开户银行汇往广州工商银行20000元开立采购专户,2月6日采购员交来采购发票两张,价税合计为19305元。同时报销差旅费1150元,用现金支付。2月15日接到开户银行通知,剩余的外埠存款695元已转回开户银行。 1月8日 借:其他货币资金——外埠存款20000 贷:银行存款20000 2月6日 借:材料采购16500 应交税费——应交增值税2805 贷:其他货币资金——外埠存款19305 借:管理费用1150 贷:现金1150 2月15日 借:银行存款695 贷:其他货币资金——外埠存款695 (3)2月3日销售商品收到买方转账支票一张,价款金额24000元,增值税4080元。 借:银行存款28080 贷:应交税费——应交增值税4080 主营业务收入24000 (4)3月10日从银行提取现金30000元,备发工资。 借:现金30000 贷:银行存款30000 (5)3月31日清查时发现库存现金溢余240元,原因待查。 借:现金240 贷:待处理财产损益240 要求:为上述经济业务编制会计分录。 2.现行银行结算方式有哪些?各自特点和适用范围是什么?

结算工具:票据化的结算方式和银行转账结算 票据化的结算方式:支票、银行本票、银行汇票、商业汇票 银行转账结算:汇兑、委托收款、托收承付、信用卡 同域结算:支票、银行本票异地结算:汇票、托收承付通用结算:银行汇票、商业汇票、委托收款 银行汇票是汇款人将款项缴存当地银行,由银行签发给汇款人据以办理转账结算或支取现金的票据。 商业汇票(分商业承兑汇票,银行承兑汇票)是收款人或付款人(或承兑申请人)签发,由承兑人承兑,并于到期日向收款人或被背书人支付款项的一种结算方式。 银行本票是申请人将款项交存银行,由银行签发给其凭以办理转账结算或支取现金的票据。 支票(分现金支票,转账支票)是银行的存款人签发给收款人办理结算或委托开户银行将款项支付给收款人的票据。 汇兑(信汇,电汇)是指汇款单位委托银行将款项汇给外地收款人的结算方式。委托收款是指收款人向银行提供收款依据,委托银行向付款人收取款项的一种结算方式。 托收承付是指根据经济合同,由收款单位发货后委托银行向异地付款单位收取款项,付款单位向银行承认付款的结算方式。 信用卡是商业银行向个人和单位发行的,凭以向特约单位购物、消费和向银行存取现金,且具有消费信用的特制载体卡片。 3.桂新有限责任公司为一般纳税人(按17%交纳增值税)。20×7年9月发生下列经济业务: (1)从本市宏达工厂购进A材料10 000元,增值税1 700元,货款签发转账支票支付,材料验收入库。 借:原材料 10000 应交税费——应交增值税 1700 贷:银行存款 11700 (2)签发现金支票,从银行提取现金3 000元备用。 借:现金 3000 贷:银行存款 3000 (3)填制银行汇票委托书,委托银行开出金额为400 000元的银行汇票。银行收妥款项,开给银行汇票。 借:其他货币资金——银行汇票 400000 贷:银行存款 400000 (4)采购员持银行汇票到外地前进工厂采购B材料,收到有关发票账单,计列B材料300 000元,增值税51 000元。B材料尚未到达。 借:材料采购 300000 应交税费——应交增值税 51000

会计分录练习题及答案 一、东方公司为增值税一般纳税人工业企业,2001年月12月份发生下列业务: 1、开出现金支票从银行提取现金2000元备用; 借:库存现金 2000 贷:银行存款 2000 2、用现金支付生产车间办公用品费440元; 借:制造费用 440 贷:库存现金 440 3、收到盛达公司前欠货款80000元,存入银行; 借:银行存款 80000 贷:应收账款---盛达公司 80000 4、向前进工厂销售A产品一批,不含增值税的售价为100000元,增值税17000元,款项尚未收到; 借:应收账款---前进工厂 117000 贷:主营业务收入 100000 应交税费—应交增值税(销项税) 17000 5、接到开户银行的通知,收到光明公司前欠货款150000元; 借:银行存款 150000 贷:应收账款---光明工厂 150000 6、向大华公司销售B产品一批,不含增值税的售价为200000元,增值税为34000元,合计234000元, 当即收到大华公司签发并承兑的面值为234000元,期限为三个月的商业汇票一张; 借:应收票据--大华公司 234000 贷:主营业务收入 200000 应交税费—应交增值税(销项税额) 34000 7、接到开户银行的通知,胜利工厂签发并承兑的商业汇票已到期,收到胜利工厂支付的票据款120000元; 借:银行存款 120000 贷:应收票据--胜利工厂 120000 8、向宏达公司购买一批甲材料,按合同规定,东方公司用银行存款预付购货款50000元; 借:预付账款--宏达公司 50000 贷:银行存款 50000 9、接上题,收到宏达公司发来的甲材料一批,增值税专用发票上注明的买价为80000元,增值税为13600 元,合计93600元。扣除预付款50000元,余额43600元东方公司用银行存款支付,甲材料已验收入库; 借:原材料—甲材料 80000 应交税费—应交增值税(进项税额) 13600 贷:预付账款--宏达公司 93600 借:预付账款 43600 贷:银行存款 43600 10、厂部办公室张强因公出差,预借差旅费800元,付以现金; 借:其他应收款--张强 800 贷:库存现金 800 11、张强出差回来,向公司报销差旅费700元,余款交回现金; 借:管理费用 700 库存现金 100 贷:其他应收款--张强 800 12、向科达公司购进甲材料一批,增值税专用发票上注明的买价为500000元,增值税85000元,价税合计

财务会计习题及答案 单项选择题 1.同一会计主体在不同会计期间尽可能采用相同的会计处理方法和程序,这一原则在会计上称之为( )。 A.可比性原则 B.一贯性原则 C.相关性原则 D.配比性原则 2.下列各项支出中,属于企业收益性支出的是( )。 A.购入不需要安装设备支付的运杂费 B.购买土地使用权支付的耕地占用税 C.以购买债券形式进行长期投资时支付的经纪人佣金(金额较小) D.申请专利时支付的注册费 3.企业在现金清查中发现多余现金,在未经批准处理之前,应借记“现金”科目,贷记( )科目。 A. “营业外收入” B. “待处理财产损溢” C. “其他应付款” D. “其他业务收入” 4.经过“银行存款余额调节表”调整后的银行存款余额为( )。 A.企业账上的银行存款余额 B.银行账上的企业存款余额 C.企业可动用的银行存款数额 D.企业应当在会计报表中反映的银行存款余额 5.下列应收、暂付款项中,不通过“其他应收款”科目核算的是( )。 A.预付给企业内部各单位的备用金 B.应向运输部门索赔的村料短缺赔款 C.应向职工收取的各种垫付款项 D.应向购货方收取的代垫运杂费 6.按照企业会计制度规定,下列票据中应作为应收票据核算的是( )。 A.支票 B.银行本票

C.商业汇票 D.银行汇票 7.某工业企业2001年1月1日甲材料账面实际成本90000元,结存数量500吨;1月2日购进甲材料500吨,每吨实际单价200元;1月15日购进甲材料300吨,每吨实际单价180元;1月4日和20日各发出甲材料100吨。如该企业按移动平均法计算发出甲材料的实际成本,则2002年1月31日甲材料账面余额为()。 A.206452元 B.208000元 C.206000元 D.206250元 8.某工业企业为增值税一般纳税企业,材料按计划成本核算,甲材料计划单位成本为每千克35元。企业购入甲材料500千克,增值税专用发票上注明的材料价款为17600元,增值税额2992元。企业验收入库时实收490千克,短缺的10千克为运输途中定额损耗。该批入库材料的材料成本差异为()。 A.450元 B.100元 C.3442元 D.3092元 9.某企业1月1日以97000元的价格,购入甲公司当日发行的债券,债券面值为100000元,期限为3年,年利率为10%,债券溢价或折价采用直线法摊销。该企业本年年末确认的本年债券投资收益为 ()元。 A.10000 B.11000 C.9700 D.10700 10.采用权益法核算长期股权投资时,对于被投资企业因外币资本折算引起所有者权益的增加,投资企业应按所拥有的表决权资本的比例计算应享有的份额,将其计入()。 A.资本公积 B.投资收益 C.其他业务收入 D.营业外收入 11.某企业1月1日以97000元的价格,购入甲公司当日发行的债券,债券面值为100000元,期限为3年,年利率为10%,债券溢价或折价采用直线法摊销。该企业本年年末确认的本年债券投资收益为 ()元。 A.10000 B.11000 C.9700 D.10700

财务会计练习题答案 一、单选题 1、某固定资产使用年限为5年,在采用年数总和法计提折旧的情况下,第一年的年折旧率为( )。 A.20% B.33% C.40% D.50% [答案]B [解析]年折旧率=尚可使用年限/预计使用年限年数总和=5/【(1+2+3+4+5)】=33%。 2、某固定资产原值为250000元,预计净残值6000元,预计可以使用8年,按照双倍余额递减法计算,第二年应提取的折旧( )元 A 46875 B 45750 C 61000 D 30500 答案:A 解析:折旧率=2/8*100%=25% 第一年折旧额=250000*25%=62500 第二年折旧额=(250000-62500)*25%=46875 3、某项固定资产原值为40000元,预计净残值2000元,折旧年限为4年,采用年数总和法计提折旧,则第三年折旧额为( ) A7600元B 8000元C 3800元D 12000元 答案:A 解析:第三年折旧额为(40000-2000)* (2/10)=7600元 4、一台机器设备原值80000元,估计净残值8000元,预计可使用12年,按直线法计提折旧,则第二年应计提折旧为( )元。 A.6600 B.6000 C.7000 D.8000 [答案]B [解析]采用直线法计提折旧,年折旧额=(80000-8000)/12=6000元。 5、下列各因素中,计提固定资产折旧时通常不考虑的是( )。 A.固定资产原值 B.固定资产预计净残值 C.固定资产使用年限 D.固定资产实际净残值 [答案]D 解析:影响固定资产计提折旧的因素主要包括: (1)计提折旧基数,即固定资产的原始价值或固定资产的账面净值; (2)固定资产的折旧年限; (3)折旧方法; (4)固定资产净残值,此净残值是预计的,而不是实际的。 6.某企业2007年5月期初固定资产原值为100000元,5月增加了一项固定资产入账价值为500万元;同时5月份减少了固定资产原值600万元;则5月份该企业应提折旧的固定资产原值为( )万元 A 100000 B 100500 C 99900 D 99400 答案:A

中级财务会计习题与案例练习题答案

练习题参考答案 第一章总论 (一)单项选择题 1.C 2.B 3.A 4.A 5.D 6.C 7.B 8.C 9.D 10.D 11.C 12.B 13.A 14.B 15.B 16.D (二)多项选择题 1.AB 2.ABCDE 3.BCDE 4.ABDE 5.CDE 6.ABCDE 7.BDE 8.ACDE 9.ABCDE 10.ABDE 11.AB (三)判断题 1.× 2.√ 3.× 4.√ 5.× 6.× 7.× 8.√ 9.× 10.× 11.× 12.√ 13.√ 14.√ 15.× 16.× 17.√ 18.× 19.√20.× 第二章货币资金 (一)单项选择题 1.D 2.C 3.D 4.A 5.C 6.D 7.D 8.A 9.A 10.A 11.A 12.D【解析】存出投资款用于投资业务,其他各项一般用于采购和结算。(二)多项选择题 1.ABC 2.ABCD 3.ABC 4.ACE 5.BDE 6.ABCE 7.BCDE 8.CDE

9.BCDE【解析】银行汇票存款、银行本票存款、信用卡存款,以及外埠存款一般用于采购和结算业务,而存出投资款用于投资业务。 10.BCD (三)判断题 1.× 2.× 3.× 4.√ 5.√ 6.× 7.× 8.× 9.× 10.× 11.√ 12.× 13.× 14.× (四)计算及账务处理题 1.(1)借:库存现金 3 000 贷:银行存款 3 000 (2)借:管理费用 320 贷:库存现金 320 (3)借:其他应收款——李民 1 000 贷:库存现金 1 000 (4)借:库存现金 46 000 贷:银行存款 46 000 (5)借:应付福利费 600 贷:库存现金 600 (6)借:库存现金 585 贷:主营业务收入 500 应交税费——应交增值税(销项税额) 85 (7)借:应付工资 45 200

项目一 一、单项选择题 1.对期末存货采用成本与可变现净值孰低计价,其所体现的会计信息质量要求是 (C ) 。 A. 及时性 B. 历史成本 C. 谨慎性 D. 配比性 2. 下列各项中,不属于企业收入要素范畴的是(D)。 A.销售商品收入 B.提供劳务取得的收入 C.出租无形资产取得的收入 D.出售固定资产取得的收益 3. 由于(A),导致了各种应计、递延等调整事项。 A.权责发生制 B.收付实现制 C.配比 D.客观性 4. 强调不同企业会计信息横向可比的会计信息质量要求是(C )。 A.客观性 B.配比 C.可比性 D.一贯性 5. 企业将融资租入固定资产按自有固定资产的折旧方法计提折旧,遵循的会计信息质量要求是(D)原则。 A.可比性 B.重要性 C.相关性 D.实质重于形式 6. 下列各项中可以引起资产和所有者权益同时发生变化的是(B)。 A.用税前利润弥补亏损 B.投资者投入资本 C.资本公积转增资本 D.提取法定盈余公积 7. 下列各项中,符合资产会计要素定义的是(C)。 A.计划购买的原材料 B.待处理财产损溢 C.委托代销商品 D.预收款项 8. 下列计价方法中,不符合历史成本计量基础的是(B)。 A.发出存货计价所使用的个别计价法 B.交易性金融资产期末采用公允价值计价 C.发出存货计价所使用的先进先出法 D.发出存货计价所使用的移动平均法 9. 关于损失,下列说法中正确的是(B)。 A.损失是指由企业日常活动所发生的、会导致所有者权益减少的、与向所有者分配利润无关的经济利益的流出 B.损失是指由企业非日常活动所发生的、会导致所有者权益减少的、与向所有者分配利润无关的经济利益的流出 C.损失只能计入所有者权益项目,不能计入当期利润 D.损失只能计入当期利润,不能计入所有者权益项目 10. 关于收入,下列说法中错误的是(D)。 A.收入是指企业在日常活动中形成的、会导致所有者权益增加的、与所有者投入资本无关的经济利益的总流入 B.收入只有在经济利益很可能流入从而导致企业资产增加或者负债减少、且经济利益的流入额能够可靠计量时才能予以确认 C.符合收入定义和收入确认条件的项目,应当列入利润表 D.收入是指企业在日常活动中形成的、会导致所有者权益或负债增加的、与所有者投入资本无关的经济利益的总流入

会计分录练习题及参考答案 一、练习工业企业供应过程主要经济业务的核算 1 ) 1 日,购入甲材料一批,价款为 100000元,增值 税税率为17% ,税额为17000 元,全部款项已用银行存款支付,材料已验收入库。 借:原材料 --- 甲材料 1 00000 应交税金 --- 应交增值税(进项税额)17000 贷:银行存款117000 2 ) 5 日,购入乙材料一批,增值税专用发票注明的价款为 元,增值税额为34000 元,企业开出商业承 200000 兑汇票一张,票面金额为234000元,材料尚在运输 途中。 借:在途物资 --- 乙材料200000 应交税金 --- 应交增值税(进项税额)34000 贷:应付票据234000 93600 元,材料已验收入库,款项未付(假设不考虑增值税) 3 ) 8 日,购入丙材料一批,价款为合计为 借:原材料 --- 丙材料93 600 贷:应付账款93600 要求:对上述业务作账务处理 二、练习工业企业生产过程主要经济业务的核算 7年 10 月份发生以下有关经济业务 1 )本月仓库共发出甲材料44000 元,其中生产 A 产品领用 16000 元,生产 B 产品领用 11800 元,车间管理 部门耗用 1200 元,行政管理部门耗用 9000 元,对外发出委托加工物资 5000 元,销售部门领用 1000 元。 借:生产成本 --- A 产品16000 ---B 产品11800 制造费用1200 管理费用9000 委托加工物资5000 销售费用1000 贷:原材料 --- 甲材料44000 2 )计提本月职工工资 55000 元,其中 A 产品生产工人工资 23000 元, B 产品生产工人工资 15000 元,车 间管理人员工资2900 元,行政管理人员工资 4100 元,销售部门人员10000 元。 借:生产成本 --- A 产品23000 ---B 产品15000 制造费用2900 管理费用4100 销售费用10000 贷:应付职工薪酬 --- 工资55000 3 )按职工工资总额的 14% 计提职工福利费。(注:具体分配金额按照上题金额分配) 借:生产成本 --- A 产品3220 ---B 产品2100 第1 页共9 页

《财务会计》试题及答案 一、单选题(每题2分,共20分) 1、下列有关会计主体与法律主体之间关系的说法正确的是(A)P4 A.会计主体不一定是法律主体,而法律主体必然是会计主体 B.法律主体不一定是会计主体,而会计主体必然是法律主体 C.法律主体不一定是会计主体,会计主体也不一定是法律主体 D.会计主体一定是法律主体,法律主体也一定是会计主体 2、库存现金清查中发现现金短缺,属于无法查明的其他原因,根据管理权限,经批准 后处理,应编制的会计分录为(D)P11 A.借:其他应收款——应收现金短缺款 贷:待处理财产损溢——待处理流动资产损溢 B.借:待处理财产损溢——待处理流动资产损溢 贷:其他应收款——应收现金短缺款 C.借:库存现金 贷:待处理财产损溢——待处理流动资产损溢 D.借:管理费用——现金短缺 贷:待处理财产损溢——待处理流动资产损溢 3、对于银行已经入账而企业尚未入账的未达账项,企业应当(C)P11 A.根据“银行对账单”记录的金额入账 B.在编制“银行存款余额调节表”的同时入账 C.等有关单据到达时再进行账务处理 D.根据“银行对账单”和“银行存款余额调节表”自制原始凭证入账 4、某企业与4月10日销售商品收到带息票据一张,面值50000元,年利率8%,6个 月期,于6月10日贴现,贴现率为10%,该企业实际收到的贴现金额应为(A)元P11 A.50267 B.49763 C.52000 D.50000 5、在会计实务中,预付账款业务不多时,企业可以通过(C)科目来核算预付账款 业务。P12 A.应收账款 B.其他应收款 C.应付账款 D.预收账款 6、企业对某项存货是否加以确认,应以企业对该项存货是否(C)为依据。P25 A.实际收到 B.支付货款 C.具有法定所有权 D.支付订金或签订合同 7、企业购入存货时,在允许折扣的期限内取得的现金折扣应(D)P25 A.作为营业外收入 B.作为其他收入 C.冲减存货账面成本 D.冲减当期财务费用

会计分录90-题及答案

会计分录90-题及答案

会计分录(90题) 1.经批准,企业投资者张某撤资,用银行存款支 付其撤资款50000元。 2.应收账款3000元确认无法收回,经批准列作 管理费用。 3.收到原材料一批价值400000元,作为外单位 对本单位的投资。(不考虑税) 4.期末,结转主营业务税金及附加600元。 5.用银行存款支付电汇手续费230元。 6.从银行取得期限6个月的借款100000元,存 入银行。 7.开出转账支票4000元,支付销售部门办公费。 8.用银行存款25000元购入一台全新设备,直接 交付使用。(不考虑增值税) 9.销售A产品100件,单价5400元,增值税税 率17%,款项收存银行计631800元。 10.企业在财产清查中,发现全新账外机器一台, 重置价50000元,原因待查。 11.国家投入新机器一台,价值30000元。 12.购买材料42000元,(不考虑增值税)货款已 付,材料尚未入库。

13.生产产品领用材料320公斤,单价90元,其 中:A产品用160公斤,B产品用150公斤,生产车间一般耗用8公斤,企业管理部门用2公斤。 14.以银行存款3000元付电费,其中企业管理部 门用2000元,生产车间1000元。 15.经公司董事会批准将资本公积金转增资本 50000元。 16.从银行提取1000元备用金。 17.收回某单位前欠本企业的货款10000元存入 银行。 18.以银行存款3000元,支付本月财产保险费。 19.接受某单位投资300000元,存入银行。 20.购入原材料一批,价款22000元,(不考虑增 值税)其中20000元用转账支票支付,余款用库存现金支付。 21.用银行存款50000元偿还到期的银行临时借 款。 22.接受某投资人的投资600000元,其中一台全 新设备150000元投入使用(不考虑增值税)一项专利权作价200000元,剩余部分通过银行划转。

一、单项选择题 1.企业对于重要的前期差错,应采用追溯重述法更正,这体现的是()要求。 A.可比性 B.重要性 C.客观性 D.明晰性 2.下列说法中,能够保证同一企业会计信息前后各期可比的是()。 A.为了提高会计信息质量,要求企业所提供的会计信息能够在同一会计期间不同企业之间进行相互比较 B.存货的计价方法一经确定,不得随意改变,如需变更,应在财务报告中说明 C.对于已经发生的交易或事项,应当及时进行会计确认、计量和报告 D.对期末存货采用成本与可变现净值孰低法计价 3.下列对会计基本假设的表述中恰当的是()。 A.持续经营和会计分期确定了会计核算的空间范围 B.一个会计主体必然是一个法律主体 C.货币计量为确认、计量和报告提供了必要的手段 D.会计主体确立了会计核算的时间范围 4.当期与以前期间、以后期间的差别,权责发生制和收付实现制的区别的出现,都是基于()的基本假设。 A.会计主体 B.持续经营 C.会计分期 D.货币计量 5.企业将融资租入固定资产按自有固定资产的折旧方法计提折旧,遵循的是()要求。 A.谨慎性 B.实质重于形式 C.可比性

D.重要性 6.依据企业会计准则的规定,下列有关收入和利得的表述中,正确的是()。 A.收入源于日常活动,利得也可能源于日常活动 B.收入会影响利润,利得也一定会影响利润 C.收入源于日常活动,利得源于非日常活动 D.收入会导致所有者权益的增加,利得不一定会导致所有者权益的增加 7.下列计价方法中,不符合历史成本计量基础的是()。 A.发出存货计价所使用的先进先出法 B.可供出售金融资产期末采用公允价值计价 C.固定资产计提折旧 D.发出存货计价所使用的移动平均法 8.资产按照预计从其持续使用和最终处置中所产生的未来净现金流入量的折现金额计量,其会计计量属性是()。 A.历史成本 B.可变现净值 C.现值 D.公允价值 9.强调不同企业会计信息可比的会计信息质量要求是()。 A.可靠性 B.可理解性 C.可比性 D.及时性 10.下列各项会计处理中,符合会计信息质量特征中实质重于形式要求的是()。 A.对于变成亏损合同的待执行合同按照或有事项进行核算 B.将融资租入的固定资产比照自有资产进行核算 C.将预期不能为企业带来经济利益的无形资产按其账面价值转为营业外支出 D.附有退货条款但不能确定退货可能性的商品销售在退货期满时确认收入 11.下列有关会计主体的表述不正确的是()。

2018年10月高等教育自学考试中级财务会计试题 (课程代码00155) 一、单项选择题:本大题共16小题,每小题1分,共16分。在每小题列出的备选项中只有一项是符合题目要求的,请将其选出。 1.在阅读财务报告时,企业债权人不太关注的信息是 A.企业的福利待遇如何 B.企业的获利情况怎样 C.企业的财力是否充裕 D.是否应该贷给企业更多的资金 2.企业核算固定资产采用折旧的方法,把固定资产的历史成本分摊到各个会计期间的费用或者相关产品的成本中,这种方法运用的会计基础假设是 A.会计主体 B.会计基础 C.会计分期 D.货币计量 3.在下列各项中,不属于我国企业财务会计信息质量要求的是 A.可理解性 B.权责发生制 C.相关性 D.及时性 4.企业赊销一批商品,规定的付款条件为:1/10、N/30,如果客户在现金折扣期内付款, 那么该折扣记入 A.管理费用 B.财务费用 C.制造费用 D.制造成本 5.对于银行已经入账而企业尚未入账的未达账项,企业应当 A.根据银行对账单记录的金额入账 B.根据银行对账单编制自制凭证入账 C.待结算凭证到达后入账 D.在编制银行存款余额调节表的同时入账 6.企业采用支付手续费方式委托代销商品,委托方确认商品销售收入的时间是 A.签订代销协议时 B.发出商品时 C.收到代销清单时 D.收到代销款时 7.如果企业的包装物数量不多,可以将包装物并入下列哪个科目进行核算? A.周转材料 B.低值易耗品 C.材料釆购 D.原材料 8.在每次收货以后,立即根据库存存货的数量和总成本,计算出新的平均单位成本,这种存货成本的计价方法是 A.零售计价法 B.月末一次加权平均法 C.移动加权平均法 D.先进先出法 9.在备抵法下,已核销的应收账款坏账又收回时,贷记“坏账准备”科目,借记的科目应是 A.其他应收款 B.应收票据 C.资产减值损失 D.应收账款 10.下列属于生产经营用固定资产的是 A.职工宿舍用房 B.制造车间用房 C.工会俱乐部用房 D.托儿所用房 11.下列不属于投资性房地产的是 A.自用的土地使用权 B.已出租的土地使用权 C.已出租的建筑物 D.持有并准条增值后转让的土地使用权 12.下列关于无形资产的特征描述中,错误的是

(1)出售产品5件,价款600元,增值税102元,收到現金702元. 借:库存現金 702 贷:主营业务收入 600 应交税费-----应交增值税(销项税额)102 (2)厂办主任王平因公外出,预借差旅费1500元,以現金支付. 借:其它应收款------备用金(王平) 1500 贷:库存現金 1500 (3)职工李红交回欠款500元. 借:库存現金 500 贷:其它应收款-------其它应收暂付款(李红) 500 4 大明公司現金清查,发現短缺360元,经查实,其中160元属于出纳员小王责任,应由其赔偿,赔款尚未收到,另外200元无法查明原因,经批准作为管理费用处理. 借:待处理财产损溢-----待处理流动资产损溢 360 贷:库存現金 360 借:其它应收款------其它应收暂付款(小王) 160 管理费用 200 贷:待处理财产损溢-----待处理流动资产损溢 360 5大明公司現金清查,发現库存現金溢余270元,经查实200元为多收A公司货款,其中70元无法查明原因,经批准作为营业外收入. 借:库存現金 270 贷:待处理财产损溢-----待处理流动资产损溢 270 借:待处理财产损溢-----待处理流动资产损溢 270 贷:其它应付款-----其它应付暂收款 (A公司) 200 营业外收入 70 6大明公司收回A公司以转账支票偿还前欠货款1.8万元 借:银行存款 18000 贷:应收账款 -----A公司 18000 7大明公司前欠天一公司货款15万元,現以信汇方式付款 借:应付账款-----天一公司 150000 贷:银行存款 150000 8甲企业为增值税一般纳税人,向银行申请办理银行汇票用以购买原材料,将款项250 000元交存银行转作银